North America Construction Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

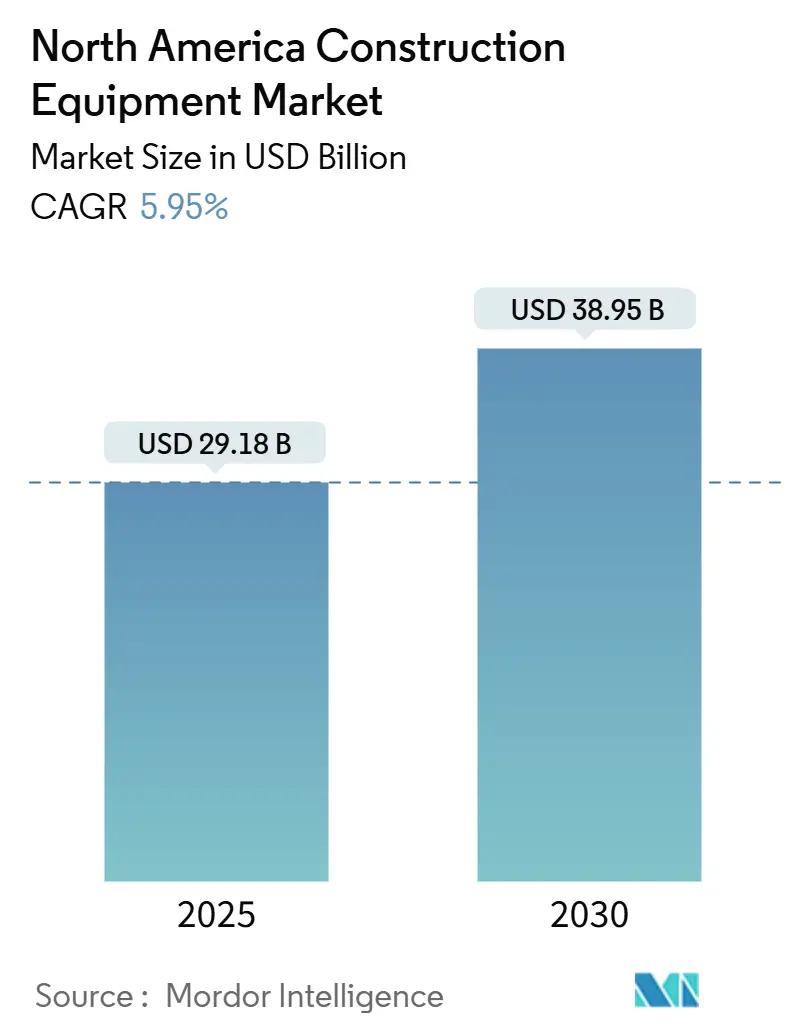

| Market Size (2025) | USD 29.18 Billion |

| Market Size (2030) | USD 38.95 Billion |

| Growth Rate (2025 - 2030) | 5.95% CAGR |

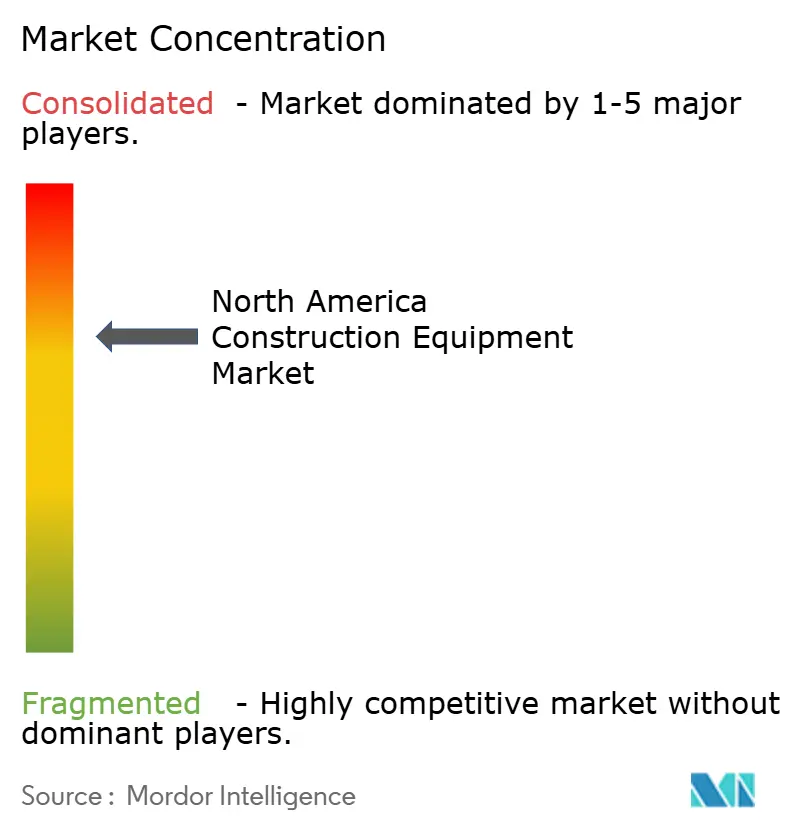

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Construction Equipment Market Analysis by Mordor Intelligence

The North American Construction Equipment market size stands at USD 29.18 billion in 2025 and is projected to reach USD 38.95 billion by 2030, reflecting a 5.95% CAGR over the forecast period. Robust federal appropriations fuel significant upgrades to roads, bridges, and broadband networks, leading to a sustained demand for earthmoving and concrete machinery. This long-term investment cycle is bolstering growth across various equipment categories. Rental operators are reaping the benefits and enjoying heightened utilisation rates as contractors lean towards short-term rentals over capital purchases, a shift driven mainly by rising loan costs. The stricter enforcement of Tier 4 Final and Stage V emissions standards hastened fleet replacements, amplifying the demand for newer, compliant machinery. Concurrently, data-centre construction projects, particularly in the U.S., need specialised equipment, further broadening the market's demand landscape. Although recent steel tariffs have pressured component costs, the overall price escalation has been modest. Average equipment prices have slightly increased, ensuring affordability and bolstering ongoing procurement activities.

Key Report Takeaways

- By equipment type, earthmoving captured 49.52% of the North American construction equipment market share in 2024, and light and Compact Tools are expanding at a 6.21% CAGR to 2030.

- By propulsion type, internal combustion powertrains accounted for 81.21% of the North American construction equipment market size in 2024, while Battery Electric recorded the highest projected CAGR at 8.23% through 2030.

- By capacity, heavy machines above 11 tons held a 45.29% share of the North American construction equipment market in 2024; compact units under 6 tons advanced at a 7.18% CAGR to 2030.

- By power output, equipment rated 250–500 HP led the North American construction equipment market, with a 38.31% share in 2024; engines up to 250 HP are forecast to grow at a 7.27% CAGR through 2030.

- By application, infrastructure applications captured 43.21% of the North American construction equipment market share in 2024; residential and Commercial construction is set to grow fastest, with a 7.35% CAGR to 2030.

- By sales channel, rental channels commanded a 54.28% share of the North American construction equipment market size in 2024 and are progressing at a 6.37% CAGR from 2025 to 2030.

- By country, the United States controlled 78.63% of the North American construction equipment market share in 2024; Canada is poised for the quickest expansion at a 6.24% CAGR through 2030.

North America Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Infra Funding Fuels Equipment Demand | +1.1% | United States, spillover to Canada | Medium term (2-4 years) |

| Rental Model Gains Over Ownership | +0.8% | North America | Long term (≥ 4 years) |

| Stricter Emission Norms Drive Fleet Replacement | +0.7% | United States, Canada | Medium term (2-4 years) |

| Data Center Boom Lifts Specialized Machinery Needs | +0.6% | United States, select Canadian markets | Short term (≤ 2 years) |

| Canadian Critical-Minerals Projects Boost Off-Road Demand | +0.5% | Canada, northern US regions | Long term (≥ 4 years) |

| OEM Telematics Contracts Accelerate New Sales | +0.4% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Federal-Level Infrastructure Funding Pipeline

Multi-year Infrastructure Investment and Jobs Act disbursements give contractors predictable workloads, prompting early fleet procurement and replacement decisions. Road and bridge work remains the heaviest consumer of 250–500 HP bulldozers and excavators, and Buy-American clauses push buyers toward locally manufactured units. With state agencies releasing bundled tenders, OEM order books stay healthy, cushioning market volatility. The predictable flow of projects also lets rental fleets pre-position high-horsepower assets near priority corridors to maximise utilisation. Overall, the funding pipeline lifts baseline demand even during periods of tighter credit availability.

Stricter Tier 4/Stage V Emission Norms Triggering Fleet Replacement

Urban job-site restrictions banning older diesel engines compel contractors to phase out non-compliant fleets. OEMs bundle diesel particulate filters and selective catalytic reduction systems as standard, limiting aftermarket retrofits’ attractiveness[1]“Tier 4/Stage V Compliance Drives Fleet Turnover,”, CONEXPO-CON/AGG, conexpoconagg.com. Compliance timelines accelerate orders for new diesel and emerging electric units, raising OEM margins through technology-rich variants. Because public projects often stipulate emission thresholds, adherence becomes a prerequisite for bidding, directly linking regulation to sales growth. As fleets modernise, telematics integration deepens, producing recurring service revenue for OEMs.

Canadian Critical-Minerals Projects Scaling Up Off-Road Equipment Demand

Federal incentives for lithium, nickel, and rare-earth extraction drive procurement of 500-HP plus haul trucks, graders, and loaders capable of handling arctic terrain. The CAD 42.5 million (USD 31.2 million) infrastructure allocation for northern mine access roads alone lifts the requirement for heavy dozers and articulated dump trucks[2]“Canada’s Critical Minerals Corridor Investment,”, Mining & Energy, miningandenergy.ca. OEMs with winterisation packages and heated cabs enjoy a competitive edge. Long project lifecycles mean units stay active for over eight years, translating into strong aftermarket parts demand and field service contracts.

OEM Telematics-Driven Productivity Contracts Accelerating New Sales

Manufacturers now sell subscription-based uptime guarantees bundled with factory telematics, enabling data-driven preventive maintenance. Contractors appreciate reduced unplanned downtime, and OEMs lock in multiyear service revenue that smooths cyclical swings. Telematic insights feed into residual-value optimisation, assuring lease companies of stronger resale prices. As proof points multiply, more fleet owners trade older iron for sensor-equipped replacements, nudging volume and service margins higher.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest Rates Curb Capex | -0.9% | North America | Short term (≤ 2 years) |

| Operator Skill Shortages Persist | -0.6% | United States, Canada | Long term (≥ 4 years) |

| United States Steel Tariffs Inflate Component Costs | -0.5% | United States, spillover to Canada | Short term (≤ 2 years) |

| Grid & Fast-Charging Gaps Delay E-Equipment Uptake | -0.4% | North America, urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Environment Curbing Capex

High interest rates on loans for construction equipment are making new units less affordable, resulting in a significant drop in equipment-finance volumes from the previous year. In response, smaller contractors are delaying fleet renewals, extending the lifecycles of their assets, and increasingly turning to the used equipment market. Although OEM captive-finance arms are rolling out promotional rates to boost demand, a broader tightening of credit is still holding back short-term sales. Yet, with the Federal Reserve expected to ease by 2026, there's a brighter medium-term outlook. Meanwhile, resellers are pivoting, focusing on flexible lease-to-own structures to keep showroom traffic steady and engage buyers.

Acute Operator-Skill Shortages

Canada’s construction industry faces a talent mismatch rather than a labour surplus, with unemployment coexisting alongside persistent project backlogs. Skilled roles—exceptionally seasoned excavator operators—are in short supply, commanding wage premiums and inflating labour budgets. The shortage is exacerbated by retiring baby boomers and underdeveloped training pipelines, leading to idle machinery even among well-funded contractors. While OEMs are accelerating the rollout of semi-autonomous features to mitigate labour gaps, complex tasks like finish grading still require human expertise. These conditions will sustain operator shortages well into the next decade, reinforcing the urgency for workforce development and automation innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Earthmoving Holds the Lead While Compacts Surge

Earthmoving equipment controlled 49.52% of the North American Construction Equipment market size in 2024. The dominance stems from large-scale roadway excavation and grading needs that rely on high-horsepower dozers and excavators. Continuous allocations from the Infrastructure Investment and Jobs Act ensure multi-year pipelines for heavy earthmoving fleets, while resale values stay resilient due to global demand for second-life exports. Competitive rental yards stock surplus crawler excavators to meet periodic spikes in bid-let activity, smoothing fleet utilisation.

Light and Compact Tools represent the most dynamic category, registering a 6.21% CAGR through 2030. Urban infill projects with restricted access embrace mini-excavators, skid steers, and compact wheel loaders that manoeuvre easily in tight spaces. These machines typically fall below 6 tons, dovetailing with rental house inventory strategies aimed at high-turnover assets. Their lower fuel consumption aligns with contractor sustainability targets, and battery-powered variants offer low-noise operation suitable for residential work.

By Propulsion Type: Diesel Dominant but Electrics Accelerate

Internal combustion engines retained 81.21% of the North American construction equipment market size in 2024, thanks to widespread fueling infrastructure and proven torque delivery in heavy-duty applications. OEM roadmaps show continued diesel optimisation via advanced aftertreatment and low-idle control. Fleet owners value the familiarity and field service know-how attached to diesel, reinforcing replacement decisions within the same powertrain.

Battery Electric units grow at an unmatched 8.23% CAGR, supported by municipal emission mandates and indoor job-site regulations that limit diesel exhaust. Early adopters include utility contractors and warehouse developers needing zero-tailpipe emission equipment. High upfront cost and charging logistics still constrain broader uptake, yet technological advances point to longer duty cycles and faster DC charging, which will gradually erode diesel’s dominance beyond 2030.

By Capacity: Heavy Machines Drive Funding Projects While Compacts Flourish

Heavy units over 11 tons accounted for 45.29% of the North American Construction Equipment market size in 2024. Mega-projects such as interstate upgrades and port expansions necessitate high-capacity machines capable of moving bulk material quickly. Rental fleets maintain deep inventories of 30-ton excavators and 12-ton loaders, given their essential role in contract milestone adherence.

Compact machinery under 6 tons is forecast to grow at a 7.18% CAGR, reflecting strong housing starts and small-lot commercial redevelopment. Their lighter footprints reduce site remediation costs, while transportability on light-duty trailers cuts logistic expenses for contractors covering dispersed job sites. OEMs now bundle quick-attach couplers, making compacts even more versatile across trenching, lifting, and landscaping tasks.

By Power Output: Mid-Range Horsepower Dominates, Lower Output Gains Pace

Machines rated 250–500 HP captured 38.31% share of the North American Construction Equipment market size in 2024, offering an ideal compromise between bucket capacity and fuel burn for mainstream earthworks. Contractors appreciate the benefits of standardisation, streamlining parts inventories, and operator training across fleets.

Up to 250 HP is advancing at a 7.27% CAGR, buoyed by the growth of compact and medium excavators used in urban and utility trenching. Electrification suits this power band, with battery capacities now sufficient for full-shift performance on many metropolitan job sites. OEM demonstration projects show total cost-of-ownership parity within five years when factoring in fuel savings and reduced maintenance.

By Application: Infrastructure Remains Core, Housing Rebounds

Infrastructure work held 43.21% of 2024 demand, led by roadway resurfacing and bridge rehabilitation programs that require sustained equipment deployment. Public-private partnerships accelerate airport and port expansions, lifting material-handling cranes and concrete pavers. Mining and quarry projects maintain baseline demand for large, rigid haulers, especially in the western United States.

Residential and Commercial building activities clock a 7.35% CAGR, reflecting a rebound in single-family housing starts and the need for mixed-use developments near urban cores. Compact earthmovers and telehandlers thrive in these settings, as developers face tighter site footprints and community noise ordinances.

By Sales Channel: Rental Commands and Expands

Rental businesses amassed 54.28% of the North American Construction Equipment market size in 2024. Consolidation among leading lessors improves geographic coverage, reducing downtime for cross-border contractors. Digital rental platforms now integrate telematics feeds, allowing on-the-fly utilization optimization and automated off-hire scheduling.

Rental is also the fastest-growing channel at 6.37% CAGR, powered by elevated interest rates and stringent balance-sheet management practices. Contractors appreciate off-balance-sheet treatment and built-in maintenance clauses. Used-equipment sales complement rental offerings, providing exit channels for fleets older than five years without clogging inventories.

Geography Analysis

The United States accounted for 78.63% of the 2024 demand, propelled by the Infrastructure Investment and Jobs Act and a surge in hyperscale data-centre projects. Specialised foundation equipment, such as low-vibration pile drivers, remains in short supply, supporting premium rental rates. Steel tariffs effective 2025 raise component costs, yet OEM pricing discipline has limited year-over-year equipment inflation to 2.1% through October 2024, preserving purchasing intent. Tight credit continues to nudge buyers toward lease structures until expected rate cuts materialise after 2026.

Canada is projected to grow at a 6.24% CAGR, underpinned by critical minerals mining initiatives and federal support totalling CAD 42.5 million for access roads and processing infrastructure. Harsh-climate equipment retrofits—heated fuel lines, insulated cabs, and low-temp hydraulics—become differentiators for OEMs seeking share. Skill shortages keep utilisation just below optimal, encouraging adoption of semi-autonomous haulage solutions to offset operator gaps.

The Rest of North America, including Mexico, captures incremental opportunities as near-shoring of manufacturing triggers greenfield industrial parks requiring earthworks, drainage, and utility installation. Local dealer acquisitions by United States rental majors improve parts availability and service coverage, lowering downtime for cross-border contractors. However, potential tariff escalations on Canadian steel would raise input costs for Mexican assemblers, potentially altering supply-chain sourcing strategies.

Competitive Landscape

Global OEMs contend with a large population of regional manufacturers and rental consolidators, producing a fragmented competitive mix. United Rentals’ acquisition of H&E exemplifies how scale in fleet size and geographic reach confers pricing power and enhanced service breadth[3]“United Rentals Completes H&E Deal,”, Equipment World, equipmentworld.com. Telematics platforms from Caterpillar and Komatsu now offer uptime-linked pricing, shifting focus from unit sales toward lifecycle customer value.

White-space exists in fast-charging infrastructure for electric excavators and loaders. Start-ups are partnering with utilities to deploy mobile battery containers, while established OEMs co-develop charging standards to future-proof next-generation fleets. JLG’s acquisition of AUSA signals a bid to broaden niche product portfolios and penetrate compact all-terrain segments that are attractive to landscaping and agriculture customers.

Price stabilisation after 2024 inflation spikes gives financially healthy manufacturers room to invest in autonomous functionality and alternative fuels, including hydrogen fuel-cell prototypes for remote mining. Rental Equipment Register notes rising experimentation with equipment-as-a-service contracts, where contractors pay only for productive hours, further blurring the line between ownership and rental.

North America Construction Equipment Industry Leaders

Caterpillar Inc.

Deere & Company

Komatsu Ltd.

Volvo CE

CNH Industrial

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: United Rentals has acquired H&E Rentals for USD 4.8 billion, including USD 1.4 billion in net debt. This strategic move bolsters United Rentals with an additional fleet of 64,000 units spread across 160 locations.

- December 2024: Bee Equipment Sales has been acquired by SMT’s ROMCO division, broadening its reach to 16 locations across Texas and New Mexico.

North America Construction Equipment Market Report Scope

| Earthmoving |

| Material Handling |

| Concrete and Road Machinery |

| Light / Compact Tools |

| Internal Combustion |

| Hybrid Hydraulic |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| Heavy ( Above 11 t ) |

| Medium (6 - 11 t) |

| Compact / Mini ( Below 6 t ) |

| Up to 250 HP |

| 250 - 500 HP |

| Above 500 HP |

| Infrastructure |

| Residential and Commercial Construction |

| Mining and Quarrying |

| Oil & Gas / Pipelines |

| Industrial & Manufacturing |

| New Equipment |

| Rental |

| Used / Refurbished |

| United States |

| Canada |

| Rest of North America |

| By Equipment Type | Earthmoving |

| Material Handling | |

| Concrete and Road Machinery | |

| Light / Compact Tools | |

| By Propulsion Type | Internal Combustion |

| Hybrid Hydraulic | |

| Battery-Electric | |

| Hydrogen Fuel-Cell | |

| By Capacity | Heavy ( Above 11 t ) |

| Medium (6 - 11 t) | |

| Compact / Mini ( Below 6 t ) | |

| By Power Output | Up to 250 HP |

| 250 - 500 HP | |

| Above 500 HP | |

| By Application | Infrastructure |

| Residential and Commercial Construction | |

| Mining and Quarrying | |

| Oil & Gas / Pipelines | |

| Industrial & Manufacturing | |

| By Sales Channel | New Equipment |

| Rental | |

| Used / Refurbished | |

| By Country | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North American Construction Equipment market in 2025?

It is valued at USD 29.18 billion in 2025 and is projected to grow at a 5.95% CAGR through 2030.

Which equipment category holds the largest share?

Earthmoving equipment leads with 49.52% share in 2024, driven by road and bridge projects.

What is driving the shift toward equipment rental?

High loan rates and the need for flexible, emission-compliant fleets push contractors to rental models commanding 54.28% share in 2024.

How fast is Battery Electric equipment adoption growing?

Battery Electric propulsion is registering a 8.23% CAGR due to emission regulations and urban-site restrictions.

Which country is expanding most quickly within North America?

Canada shows the fastest growth, forecast at a 6.24% CAGR through 2030 on the back of critical-minerals and oil-sands projects.

Page last updated on: