United Kingdom Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

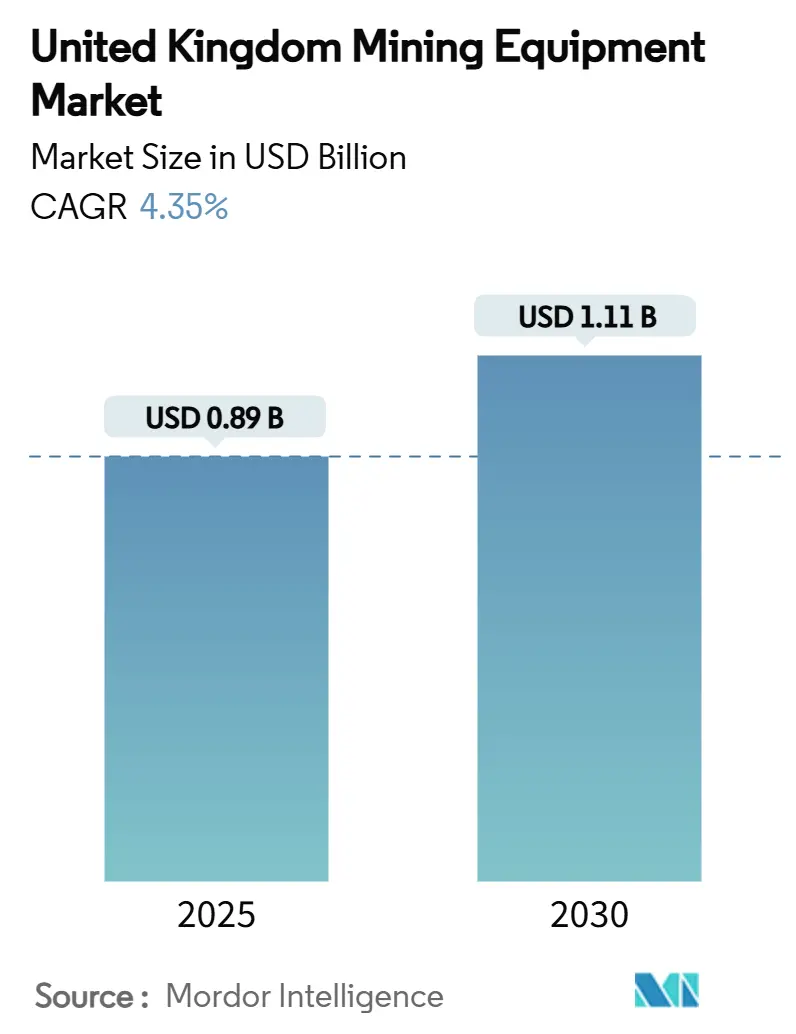

| Market Size (2025) | USD 0.89 Billion |

| Market Size (2030) | USD 1.11 Billion |

| Growth Rate (2025 - 2030) | 4.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mining Equipment Market Analysis by Mordor Intelligence

The United Kingdom mining equipment market size stands at USD 0.89 billion in 2025 and is forecast to reach USD 1.11 billion by 2030, registering a 4.35% CAGR during the forecast period. This growth trajectory reflects a pivot from coal toward critical-mineral extraction and infrastructure-driven aggregates, positioning the UK mining equipment market as a strategic tool for industrial decarbonization rather than a volume-led commodity play. Battery-critical metals, Stage V emission compliance, and autonomous haulage investments lift demand, while government incentives and electricity-cost relief strengthen capital-spending confidence. At the same time, stringent environmental permitting and commodity-price swings temper near-term equipment cycles. Competitive intensity remains moderate as global OEMs vie with local innovators whose zero-emission and digital offerings meet evolving safety and productivity benchmarks.

Key Report Takeaways

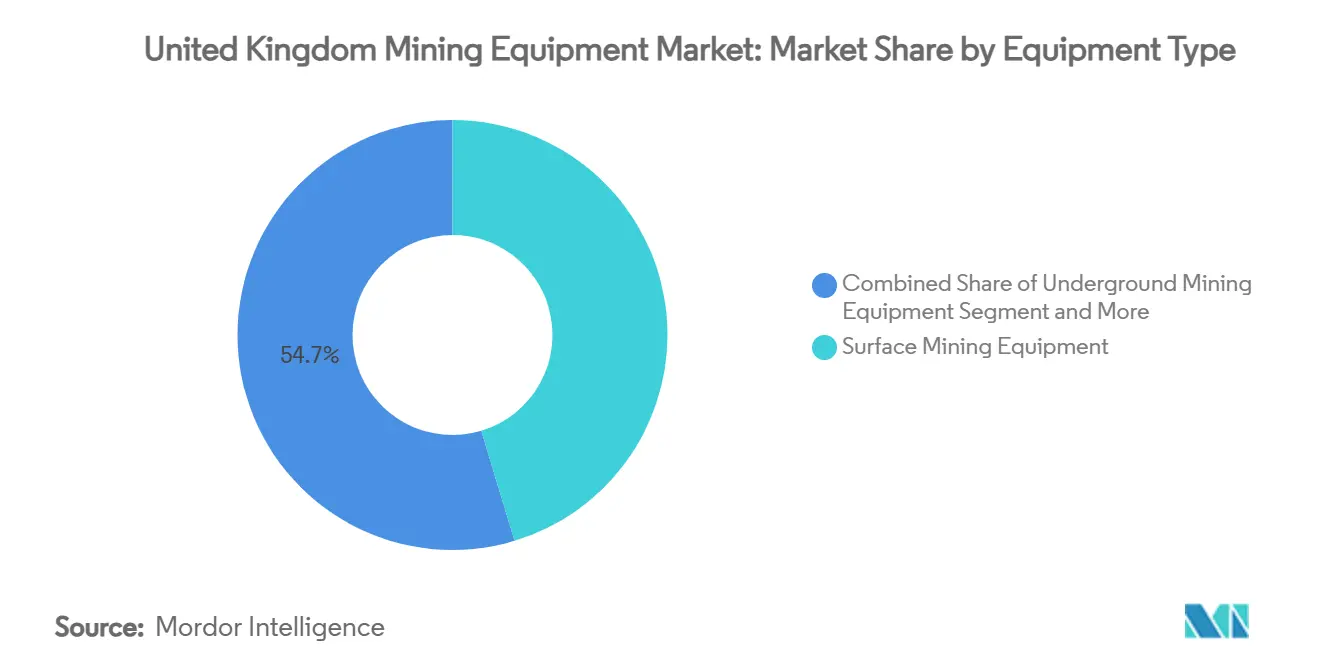

- By equipment type, surface mining captured 45.34% of the United Kingdom mining equipment market share in 2024, while loaders are projected to expand at a 7.46% CAGR through 2030.

- By automation level, manual equipment held a 53.72% share of the United Kingdom mining equipment market in 2024, whereas fully automated solutions recorded the fastest 9.23% CAGR to 2030.

- By powertrain type, ICE machines commanded 69.26% share of the United Kingdom mining equipment market size in 2024, with battery-electric variants advancing at a 9.28% CAGR through 2030.

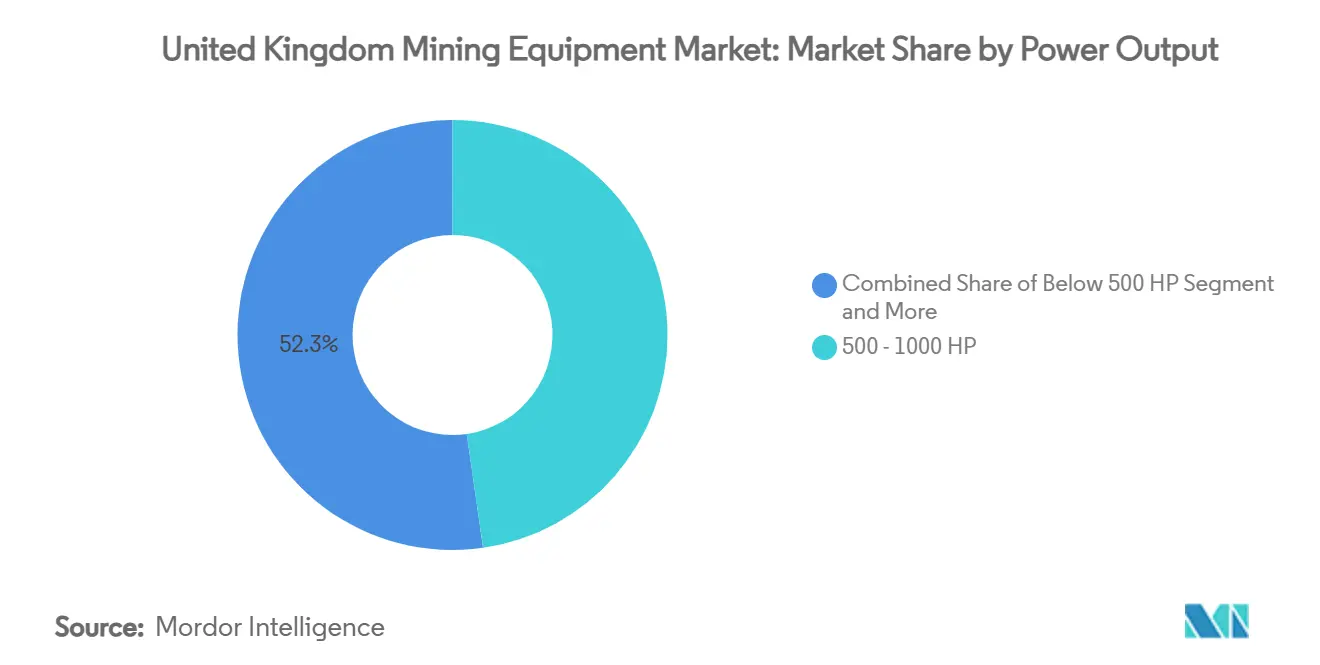

- By power output, the 500-1,000 HP bracket led the United Kingdom mining equipment market with 47.74% of the share in 2024; below-500 HP units are set to grow at an 8.37% CAGR through 2030.

- By application, metal mining accounted for a 42.19% share of the United Kingdom mining equipment market size in 2024, and mineral mining is progressing at a 7.43% CAGR to 2030.

- By geography, England dominated with a 68.74% share of the United Kingdom mining equipment market size in 2024, while Scotland posted the highest 8.54% CAGR to 2030.

United Kingdom Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery-critical metal demand | +1.2% | England, Scotland, Wales | Medium term (2-4 years) |

| UK Critical Minerals incentives | +0.8% | National, with early gains in Cornwall, Yorkshire | Long term (≥ 4 years) |

| Stage V fleet upgrades | +0.6% | National | Short term (≤ 2 years) |

| Autonomous haulage uptake | +0.5% | England, Scotland | Medium term (2-4 years) |

| Legacy-mine repurposing | +0.4% | Northern England, Wales, Scotland | Long term (≥ 4 years) |

| HS2/offshore-wind aggregates surge | +0.3% | England | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Growing Demand for Battery-Critical Metals

Lithium, cobalt, and rare-earth requirements for electric-vehicle batteries and renewable-energy hardware reshape equipment specifications toward precision extraction and contamination-controlled processing. Cornish Lithium’s underground brine trial—viewed as the first domestic source of battery-grade lithium—requires narrow-vein drills, high-recovery pumps, and modular processing lines capable of operating in complex geological formations. The British Geological Survey has mapped prospective critical-metal zones across Scotland, Wales, and Northern England, prompting demand for advanced core-drilling rigs and geophysical sensors[1]“Critical Raw Materials Prospective Areas,”, British Geological Survey, bgs.ac.uk. Repurposing disused coal workings for geothermal heat extraction further boosts orders for submersible pumps and remote-monitoring systems that can handle corrosive fluids. Operators consider equipment lifespan and recyclability because recovery rates directly influence national supply-security metrics under the Critical Minerals Strategy. As domestic output scales, the UK mining equipment market benefits from long-term procurement visibility and a pivot toward high-value, low-volume ore bodies.

Government Incentives under the UK Critical Minerals Strategy

The strategy allocates credit guarantees through UK Export Finance and streamlines planning to accelerate mine openings, creating direct demand pull for crushers, milling circuits, and heavy-haul fleets. Tax relief on energy-intensive industries from 2027 lowers operating expenditure, making electrically powered drills and loaders cost-competitive against diesel peers[2]“Critical Minerals Strategy,”, UK Government, gov.uk. Public-private ventures with Canada and other allies unlock co-funded pilot plants, spurring orders for materials-handling and beneficiation systems tailored to midstream refining. Policy coherence across business, energy, and treasury departments links grants to verifiable sustainability metrics, steering OEMs toward zero-tailpipe and low-noise platforms.

Fleet Replacement to Meet Stringent Stage V Emission Norms

Stage V rules covering engines up to and above 560 kW oblige operators to retire older fleets or retrofit diesel particulate filters and selective catalytic reduction kits[3]“Stage V Engines,”, Komatsu Ltd., komatsu.com. Compliance deadlines in 2026–2027 create a front-loaded replacement curve for trucks, face shovels, and generators. OEMs that embed after-treatment hardware without compromising torque retain procurement preference, raising the premium segment’s share of the UK mining equipment market. Anticipated tightening toward Stage VI and forthcoming non-road decarbonization guidelines encourage buyers to favor future-proofed electric or alternative-fuel platforms. Consequently, financing houses treat compliant assets as lower risk, improving lease availability and shortening payback periods despite up-front price premiums.

Rising Adoption of Autonomous Haulage Systems

Autonomous rigs cut labor exposure and improve payload consistency, aligning with the Health and Safety Executive’s targets on workplace injuries. Caterpillar’s million-meter milestone in autonomous drilling signals the maturity of machine-guidance algorithms, reducing blast variation and downstream processing costs. Integration of lidar, radar, and 5G connectivity enables real-time fleet optimization, a key advantage in weather-sensitive UK quarries where workable hours are narrow. Wider adoption is projected to raise equipment utilization rates by 15-20%, reinforcing a positive feedback loop for further automation investments within the United Kingdom mining equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Permitting & ESG scrutiny | -0.7% | National, particularly scenic areas in Cornwall, Lake District | Long term (≥ 4 years) |

| Commodity volatility | -0.5% | National | Short term (≤ 2 years) |

| Automation skill shortage | -0.4% | England, Scotland | Medium term (2-4 years) |

| Post-Brexit confidence gap | -0.3% | National, with higher impact in Northern England, Wales | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Environmental Permitting and ESG Scrutiny

Developers must navigate overlapping national, devolved, and local regulations that protect Areas of Outstanding Natural Beauty and require biodiversity net-gain commitments. Separate surface and subsurface mineral rights complicate land access, lengthening approval timelines and inflating legal expenditure[4]“Environmental Permitting Guidance,”, UK Government, gov.uk. ESG reporting has become mainstream, and large operators now benchmark Scope 1 and Scope 2 emissions, pushing equipment buyers to prioritize electric, hydrogen, or HVO-ready drivetrains. Community consultations often demand noise-suppression packages and real-time environmental monitoring, adding up to 10% to base equipment cost. These layers of oversight slow procurement and temper the overall CAGR of the United Kingdom mining equipment market.

Commodity-Price Volatility Curbing CAPEX Cycles

Fluctuating global prices for copper, lithium, and aggregates translate directly into project cash-flow uncertainty, prompting operators to postpone fleet expansion until payback visibility improves. Lenders hedge risk through higher interest spreads and tighter covenants, making advanced technology acquisitions harder to justify during downturns. Consequently, operators favor modular, lease-friendly assets that can be redeployed swiftly between pits, although such flexibility may compromise peak productivity. Procurement cycles, therefore, show a pronounced stop-start pattern, shaving 0.5% from the long-range growth trajectory of the UK mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Mining Dominates Infrastructure Demand

Surface extraction tools retained 45.34% of the United Kingdom mining equipment market share in 2024 on large aggregates contracts for HS2 and offshore wind-foundation quarries. Loaders spearhead growth at a 7.46% CAGR as autonomous guidance and Stage V engines lift productivity and cut fuel burn. Drills and breakers receive steady demand because critical-mineral exploration calls for high-precision core sampling to mitigate dilution. Crushing and screening lines scale with brown-field capacity additions around Midlands quarries, while compact jaw crushers gain traction on urban renewal sites. Haul-truck demand bifurcates: high-tonnage diesel units service open-pit limestone, whereas emerging battery-electric variants tackle underground mineral deposits where ventilation costs dominate. Overall, surface equipment remains the anchor of the UK mining equipment market, although technological shifts favor electrified and automated sub-segments.

A more minor yet strategically important share accrues to underground and mineral-processing machinery, reflecting the UK’s push to domesticate lithium and rare-earth value chains. As pilot plants transition to commercial throughput, dense-media separators, column flotation cells, and high-pressure grinding rolls appear on tender lists. The loaders sub-category benefits from battery swap systems that support 22-hour duty cycles, addressing ventilation bottlenecks. Together, these trends support the gradual broadening of the UK mining equipment market beyond conventional aggregates toward higher-margin critical-mineral flowsheets.

By Automation Level: Manual Operations Face Transformation Pressure

Manual machines still represent the majority 53.72% share of the United Kingdom mining equipment market size in 2024, reflecting entrenched operator habits and the versatility of human oversight on complex geological faces. Nevertheless, fully autonomous fleets are projected to clock a 9.23% CAGR through 2030, underpinned by falling sensor costs and improved network connectivity on remote sites. Semi-autonomous retrofit kits bridge the gap, enabling tele-operated dozers and drill rigs that let single operators manage multiple machines from centralized control rooms. Adoption accelerates where labor shortages coincide with strict safety targets, such as night shifts in deep quarries. Insurance premiums already recognize lower accident exposure on autonomous haulage, trimming the total cost of ownership and nudging late adopters along the curve.

Operators pursue a phased roadmap: loader bucket assist today, autonomous haulage next, then fully robotized drilling. Early installations show payload variance dropping below ±3%, translating to smoother mill feed and lower energy per ton milled. Though manual assets remain indispensable for irregular tasks such as maintenance or geotechnical inspections, their market share will steadily shrink as algorithms and edge computing extend to finer operational decisions.

By Powertrain Type: Electric Transition Accelerates Despite ICE Dominance

Internal combustion engines maintained a 69.26% share of the United Kingdom mining equipment market size in 2024, thanks to mature supply chains and refueling convenience. Stage V certification and HVO compatibility mitigate emissions while preserving uptime, ensuring diesel’s relevance on high-duty cycles. Yet battery-electric units are forecast to grow at a 9.28% CAGR, driven by ventilation-cost savings underground and electricity-price relief for energy-intensive users granted from 2027. JCB’s hydrogen-combustion demonstrations offer an alternative zero-carbon pathway for duties beyond the current battery range.

Hybrid drivetrains are a transitional step, pairing regenerative braking with downsized engines to achieve double-digit fuel savings on long-haul roads. Charging-infrastructure pilots co-located with wind farms showcase renewable-powered pits, reinforcing decarbonization narratives demanded by downstream customers. Consequently, the powertrain mix of the UK mining equipment market is expected to shift markedly by 2030, with electrified, hydrogen-ready, and hybrid platforms eating into diesel’s legacy leadership.

By Power Output: Compact Equipment Gains Urban Mining Traction

Units rated below 500 HP are poised for an 8.37% CAGR as the reuse of brownfield sites and urban tunneling programs call for maneuverable, low-noise assets. Battery-powered mini-excavators and wheeled loaders enable night-shift operation under stringent municipal ordinances, strengthening their economic case despite higher acquisition costs. Meanwhile, the 500-1,000 HP class retains 47.74% the United Kingdom mining equipment market share, ideally balancing payload, transport dimensions, and fuel efficiency for quarry benchmarks.

Above-1,000 HP bulldozers and haul trucks remain indispensable on high-throughput limestone and hard-rock operations but face site-access and emissions barriers in densely populated areas. OEM traction motors and inverter technology now trickle down to mid-power classes, blurring traditional segmentation lines. Over the forecast period, differential growth rates will gradually re-weight the UK mining equipment market toward compact but high-utilization assets, especially in regions pursuing low-carbon urban regeneration.

By Application: Critical Minerals Drive Metal-Mining Growth

Metal-mining applications held 42.19% of the United Kingdom mining equipment market share in 2024 as copper, tin, and tungsten pits in Cornwall and North Yorkshire expanded output in response to EU supply-chain directives. Mineral mining covering aggregates and industrial minerals will grow faster at a 7.43% CAGR, reflecting both lithium commercialization and sustained construction demand. Coal-mining equipment purchases have plateaued since thermal power retirement, transitioning to maintenance of legacy stock only.

Precision ore-sorting sensors and variable-frequency drives are critical when targeting high-grade yet geologically complex ore bodies required for clean-energy supply chains. Tailings-reprocessing plants further widen the equipment palette by introducing paste thickeners and filter presses designed to reclaim metals while reducing waste volumes. These technological inflections widen the value density per tonne mined, underpinning continued capital formation across greenfield and brownfield projects within the United Kingdom mining equipment market.

Geography Analysis

England continues to dominate the United Kingdom mining equipment market, with a 68.74% share in 2024. Large-scale infrastructure sustains high-volume surface-equipment demand, such as HS2’s 10 million-tonne aggregate program and offshore wind-foundation rollouts under the Clean Power 2030 plan. The Midlands, Yorkshire, and Cornwall form a triangle of activity where replacement cycles overlap with niche lithium exploration, generating parallel orders for heavy crushers and narrow-vein miners. The proximity of the supply chain to the Port of Felixstowe and other logistics hubs simplifies equipment import, refurbishment, and spare parts distribution, lowering downtime.

Scotland holds the fastest projected growth at an 8.54% CAGR as critical-mineral exploration and mine-water geothermal schemes move from pilot to commercial scale. The Coal Authority calculates that a single 6-MW mine-water heat system can offset CO₂, attracting municipal funding and equipment tenders for submersible pumps, heat exchangers, and monitoring instrumentation. Rugged terrain, harsher weather, and remote locations drive higher cold-start reliability and telematics specifications, favoring OEMs with proven Nordic or Canadian field experience.

Wales leverages its industrial mining heritage to repurpose shafts for rare-earth and geothermal projects. Planning authorities increasingly require zero-tailpipe equipment for underground use, propelling battery-loader demand. Northern Ireland’s quarry clusters supply domestic and Irish infrastructure, supporting a steady replacement rhythm for articulated dump trucks and mobile screens. Together, these trends illustrate the geographic heterogeneity underpinning future UK mining equipment market allocations.

Competitive Landscape

The competitive arena is moderately concentrated: five global OEMs command the lion’s share yet face niche rivalry from domestic and Asian challengers. Caterpillar, Komatsu, and Sandvik maintain broad portfolios, established dealerships, and financing arms, securing framework agreements with tier-one miners. Sandvik and Epiroc capitalize on battery-electric offerings for underground deployments, each announcing record multi-million-dollar orders through 2025 that illustrate accelerating fleet turnover toward electrification.

JCB amplifies local relevance through its hydrogen-engine prototype program, which aligns with government hydrogen-strategy grants and enhances political goodwill. The company’s robust rental and service network shortens lead times for mid-power equipment, blunting price competition from low-cost Asian entrants. SANY and XCMG, meanwhile, extend European footprints via joint ventures with global miners, leveraging attractive lease terms to penetrate price-sensitive fleets.

Sensor and software suppliers like Luminar and Ouster ride the automation wave, embedding lidar packages into OEM ecosystems and earning recurring revenue from analytics subscriptions. These partnerships underscore a shift from hardware-only offerings toward lifecycle service models that bundle autonomy, electrification, and predictive maintenance. Over the horizon, competitive advantage will hinge on demonstrable emission cuts, data-driven productivity gains, and the ability to customize for the diverse operating environments that typify the UK mining equipment market.

United Kingdom Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Sandvik AB

Epiroc AB

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CATL and BHP are set to delve into battery innovations tailored for mining equipment and locomotives. Their focus spans rapid charging infrastructures, energy storage systems, and battery recycling solutions tailored to BHP's mining endeavors.

- June 2025: BHP has inked a partnership with XCMG Mining Equipment, aiming to enhance fleet solutions across its worldwide operations. This collaboration, cemented through a comprehensive global agreement, emphasizes the strategic planning and deployment of mining equipment, aligning with BHP's stringent safety, technical, and sustainability

United Kingdom Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening Equipment |

| Loaders |

| Mining Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Below 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening Equipment | |

| Loaders | |

| Mining Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Below 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Geography | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

What is the forecast value of the UK mining equipment market by 2030?

USD 1.11 billion based on a projected 4.35% CAGR between 2025 and 2030.

Which equipment type currently leads sales in the United Kingdom?

Surface-mining machinery holds 45.34% of national demand.

How quickly are battery-electric machines expected to grow?

Battery-electric variants record a 9.28% CAGR, the fastest among powertrains.

Why are Stage V regulations significant for equipment buyers?

They mandate particulate- and NOx-reduction technology, triggering near-term fleet replacement and raising demand for compliant machines.

How are OEMs addressing zero-emission requirements for heavy-duty applications?

Approaches include battery-electric haulage, hydrogen-combustion engines, and HVO-compatible diesel platforms backed by government energy cost relief.

Page last updated on: