Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 123.04 Billion |

| Market Size (2031) | USD 160.32 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

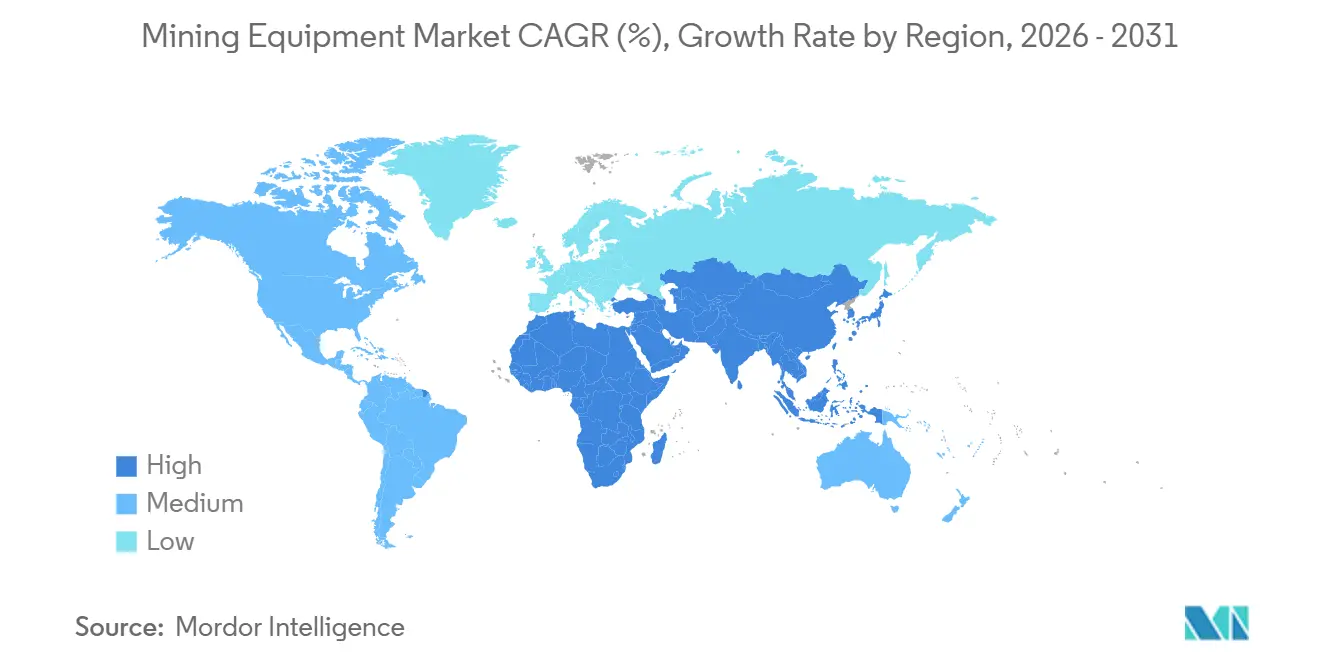

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining Equipment Market Analysis by Mordor Intelligence

The mining equipment market size is projected to be USD 117.60 billion in 2025, USD 123.04 billion in 2026, and reach USD 160.32 billion by 2031, growing at a CAGR of 5.44% from 2026 to 2031. Growth is driven by brisk capital spending on battery-mineral projects, the accelerated replacement of diesel fleets in Canada, Chile, and Australia, and renewed iron-ore developments in Western Australia and Brazil. Surface fleets continue to dominate procurement budgets, yet underground loaders and drill rigs are scaling rapidly as lithium and copper ore bodies move deeper and narrower. Financing linked to verified emission reductions is saving 150–200 basis points from lease rates on zero-emission trucks, further tilting demand toward battery-electric models. Competitive pressure is intensifying as XCMG and SANY underprice Western OEMs, while Caterpillar and Komatsu defend share through proprietary digital platforms that lock customers into bundled service contracts.

Key Report Takeaways

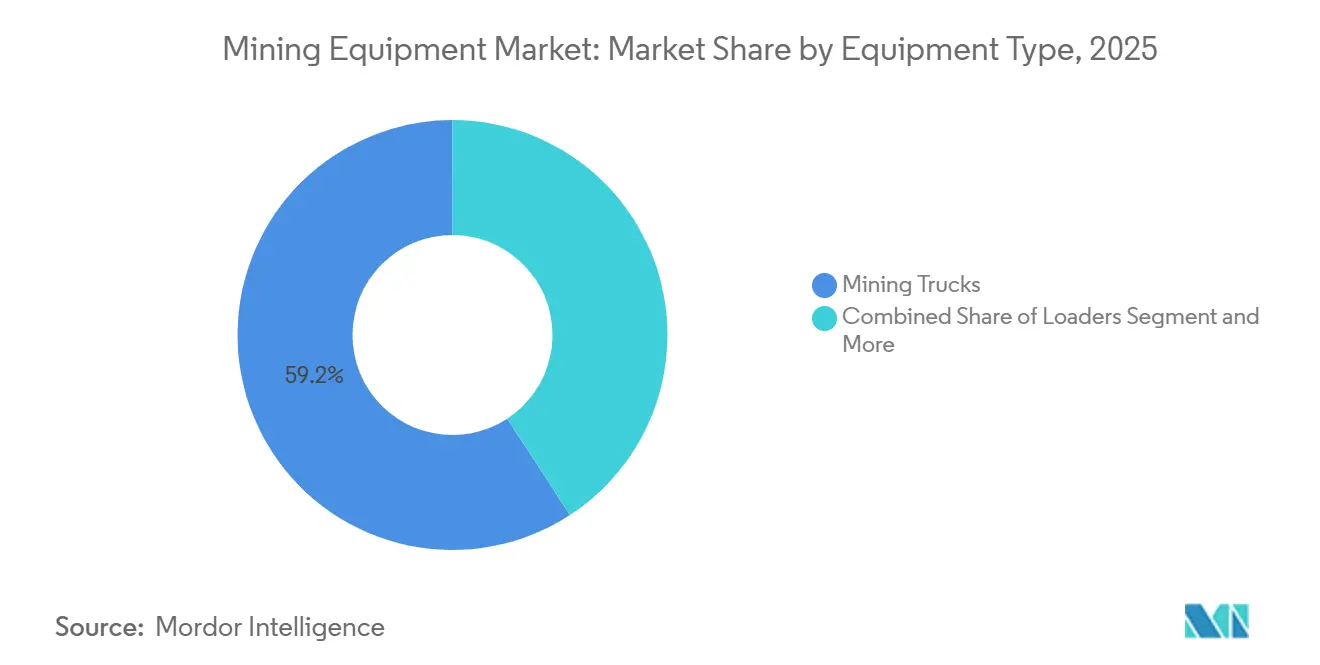

- By equipment type, mining trucks accounted for 59.22% of the mining equipment market share in 2025; drills and breakers are forecast to expand at a 6.91% CAGR through 2031.

- By automation level, manual fleets held 81.65% of the installed base in 2025, while fully autonomous equipment is expected to advance at a 15.01% CAGR to 2031.

- By powertrain type, internal-combustion vehicles captured 86.24% of 2025 revenue, and battery-electric units are growing at a 12.86% CAGR.

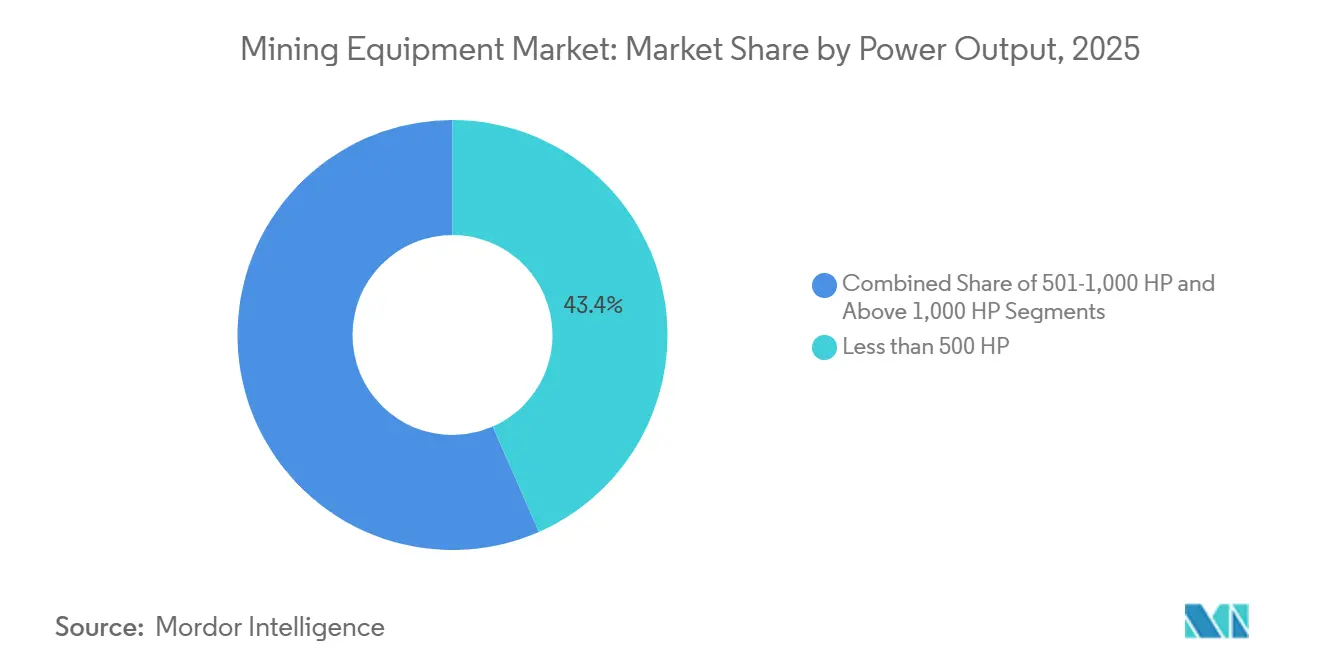

- By power output, units under 500 HP captured 43.42% of 2025 revenue; equipment above 1,000 HP is forecast to rise at a 6.29% CAGR between 2026 and 2031.

- By application, metal mining contributed 48.15% of the mining equipment market size in 2025, whereas mineral mining is projected to register a 9.03% CAGR through 2031.

- By mining type, surface mining accounted for 69.04% of the market share in 2025, while underground mining will expand at an 8.45% CAGR through 2031.

- By geography, Asia-Pacific accounted for 59.35% of the global mining equipment market size in 2025, and the Middle East and Africa region is poised for an 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Battery Minerals | +1.2% | Asia-Pacific, North America, South America | Medium term (2-4 years) |

| Mine Electrification Mandates | +0.9% | Canada, Chile, Australia, European Union | Short term (≤ 2 years) |

| Sustained Capex in African Mining | +0.8% | Middle East and Africa | Medium term (2-4 years) |

| Recovery of Greenfield Iron-Ore | +0.7% | Western Australia, Brazil | Long term (≥ 4 years) |

| Emissions-Linked Financing | +0.6% | Global | Short term (≤ 2 years) |

| Shift to Predictive Maintenance | +0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Critical Minerals for Battery Supply Chains (Asia and United States)

Lithium, cobalt, and nickel expansions are reshaping procurement, as battery-metal mines require high-throughput crushers and flotation cells distinct from base-metal circuits. Chilean brine projects now deploy solar-powered pumps that cut diesel use significantly, whereas Western Australia’s hard-rock lithium sites specify above 1,000-horsepower haul trucks to manage spodumene densities higher than iron ore. In the United States, the Inflation Reduction Act sourcing rules steer buyers toward Caterpillar and Komatsu to capture domestic-content tax credits. Congolese cobalt projects are upgrading from manual excavators to semi-autonomous loaders to meet traceability rules, and Indonesian nickel laterite operators are installing rotary kilns and electric arc furnaces that create an addressable market for mineral-processing equipment. These factors push the mining equipment market toward specialized, higher-margin systems that command pricing power despite broader cost pressure.

Accelerated Mine Electrification Mandates in Canada, Chile and Australia

Canada requires underground mines to field zero-emission units for at least 50% of mobile fleets, rising to 75% by 2030 [1]“Government of Canada Regulations for Zero-Emission Mining,” Natural Resources Canada, nrcan.gc.ca. New South Wales rolled out a ventilation-cost levy, leveling the playing field for battery-electric loaders at significant depths. As a result of these policies, operators are now retiring diesel assets much earlier than anticipated, leading to a surge in demand for Epiroc’s ST18 Battery and Sandvik’s LH518B. Additionally, lenders are now mandating ISO 14001-compliant transition plans as a prerequisite for disbursement of funds, underscoring the growing nexus between decarbonization efforts and capital accessibility.

Sustained Capex Up-Cycle in African Copper, Cobalt and Lithium Projects

Between 2024 and 2027, several projects across Africa, collectively valued at a significant amount, are making headway. In Zambia, operations are delving deeper, now surpassing considerable depths with the aid of new Sandvik drills. Meanwhile, South African platinum mines are transitioning from diesel scoops to battery-electric units, a move aimed at adhering to stringent particulate limits. In a bid to counter tenure risks, lithium ventures in both Zimbabwe and Namibia are opting for modular Metso crushing plants. Additionally, Chinese OEMs are carving out a significant presence in the region, clinching tenders by providing deferred payment options and forging local assembly partnerships. Collectively, these strategic maneuvers signal robust growth prospects for the mining equipment market in the Middle East and Africa.

Recovery of Greenfield Iron-Ore Projects in Western Australia and Brazil

In 2024-2025, several iron-ore projects in the Pilbara achieved Final Investment Decisions (FIDs), significantly increasing capacity and requiring a substantial number of ultra-class trucks. Fortescue's Iron Bridge magnetite mine harnessed the power of autonomous Komatsu 980E-4 trucks, operating around the clock and achieving notable cost savings for every tonne transported[2]“Iron Bridge Project Update,” Fortescue Metals Group, fmgl.com.au. Vale made a comeback with Brazil's Capanema and Vargem Grande projects, placing orders for advanced mining equipment, and both regions are adopting trolley-assist systems that significantly reduce diesel consumption. Higher iron-ore pellet premiums have revived magnetite ventures and validated investments in advanced crushing and beneficiation plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ore-Grade Deterioration Inflates Ownership Cost | −0.7% | South America, Africa | Long term (≥ 4 years) |

| Grid Constraints Delay BEV Deployment | −0.5% | Australia, Chile, Africa | Medium term (2-4 years) |

| Talent Shortage for Autonomous Mining | −0.4% | Global | Medium term (2-4 years) |

| Uneven Permitting Timelines for Mines | −0.3% | European Union, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ore-Grade Deterioration Inflating Total Cost-Of-Ownership

In 2024, copper grades at Escondida have declined, prompting BHP to move significantly more waste material and substantially increase tire usage. Similarly, gold grades in West Africa have also dropped, leading to a notable rise in ore processing through crushers. Lower grades amplify the costs of downtime; for example, a haul-truck malfunction at a low-grade copper pit now results in significant losses. In response, operators are opting for larger-payload trucks to extend component lifespan. However, this approach significantly raises initial capital investment and reduces returns. While in-pit crushing and conveying provides a potential solution, it depends on long-term reserve certainty, which many deposits currently lack.

Grid Constraints at Remote Mines Delaying BEV Deployment

Pilbara's iron-ore mines, located far from high-voltage lines, struggle as existing microgrids fall short, unable to deliver the significant power required to recharge multiple haul trucks during shift changes. In the Atacama Desert, brine projects grapple with hefty connection fees, accounting for a substantial portion of the capital expenditure for typical brine developments. South African platinum mines face daily load-shedding challenges, and the necessary battery storage installations would significantly increase costs per site. While hydrogen trucks sidestep grid dependence, they require expensive refueling stations, and the price of green hydrogen is considerably higher than that of diesel. Trolley-assist hybrids, however, are constrained to stable ramp profiles, limiting their broader applicability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Trucks Lead, Drills Accelerate

Mining trucks captured 59.22% of the mining equipment market share in 2025, cementing their status as the single-largest revenue contributor to the overall mining equipment market. Ultra-class haulage remains indispensable at large copper and iron-ore pits where payloads exceed 360 tonnes and haul distances stretch beyond 5 kilometers. Despite this dominance, procurement managers are trimming absolute truck counts by 15–20% in autonomous fleets, reallocating capital toward high-precision peripheral gear that maximizes cycle efficiency.

Drills and breakers are projected to post a 6.91% CAGR from 2026 to 2031, the fastest rate among equipment types, as deeper, harder orebodies boost demand for high-power rotary rigs, long-hole drills, and rock-breakers that can operate reliably in 200 megapascal ground. Autonomous drilling systems add a further productivity kicker by delivering tighter blast fragmentation, reducing downstream energy needs in crushing circuits. This shift reshapes procurement strategies: operators are bundling truck orders with drill-automation packages to secure integrated dispatch and data analytics support. This pattern strengthens OEM cross-selling leverage within the mining equipment market.

By Automation Level: Manual Fleets Face Accelerated Obsolescence

Manual fleets held 81.65% of the mining equipment market share in 2025, yet fully autonomous units had notably higher availability compared to their manned counterparts, resulting in considerably more annual running hours per unit. Fully autonomous equipment is set to grow at a 15.01% CAGR by 2031. The mining equipment market is witnessing a rapid expansion in autonomous systems, driven by insurers offering substantial premium reductions for accident-free records. The industry is shifting away from semi-autonomous solutions toward fully driverless systems, driven by superior data clarity and reduced training requirements.

Manual gear persists in artisanal and union-sensitive jurisdictions, and underground latency issues limit manual oversight in narrow areas. Regulatory inertia outside Australia, Canada, and Chile slows approvals, but once frameworks are codified, suppressed demand could trigger a step-change. Battery-electric drive trains align naturally with autonomy because instant torque and fewer mechanical parts simplify control logic, strengthening the virtuous cycle between electrification and automation.

By Powertrain Type: Electrification Accelerates Despite Infrastructure Gaps

Internal-combustion equipment accounted for 86.24% of 2025 revenue, while battery-electric vehicles are projected to grow at a 12.86% CAGR by 2031, driven by annual ventilation savings in deep nickel mines. Hybrids bridge the gap in regions lacking robust grids; Caterpillar’s 794 AC electric drive truck achieves notable fuel savings on Chilean grades. Hydrogen fuel-cell prototypes remain costly, but pilot programs continue in areas where grid links are not feasible.

Tier 4 Final engines narrowed the upfront premium versus battery units by adding expensive after-treatment, and trolley-assist systems slash diesel burn on ramp haulage. Surface coal sites still favor diesel due to commodity economics, whereas underground base-metal mines transition fastest because of ventilation regulations. As charging infrastructure matures, battery-electric vehicle penetration is expected to outstrip that of hybrids within the decade, reshaping the powertrain economics of the mining equipment industry.

By Power Output: Ultra-Class Equipment Gains Traction

Equipment rated below 500 HP retained the largest 2025 share, accounting for 43.42% of the mining equipment market, due to its versatility in underground headings and mid-scale pits, where maneuverability and low ventilation loads are decisive. In contrast, ultra-class machinery above 1,000 HP is projected to deliver the fastest growth, expanding at a 6.29% CAGR from 2026 to 2031 as miners consolidate material-handling tasks into fewer, higher-capacity units that lower cost-per-ton metrics in large open pits. This dynamic positions the high-horsepower tier as a pivotal value-creation pocket within the overall mining equipment market size during the forecast window.

The momentum behind ultra-class trucks and excavators is reinforced by technology advances that boost power density and fuel efficiency. Weichai Power’s second-generation mining engines, unveiled in May 2025 with ratings up to 2,800 kW (about 3,754 HP), illustrate the industry’s commitment to marrying raw output with improved specific fuel consumption. Mid-range (500-1,000 HP) machines continue to bridge operational flexibility and haulage capacity, while sub-500 HP units gain productivity from electrification packages that eliminate diesel emissions in confined headings, trimming ventilation cost. Across all brackets, OEMs are prioritizing engine improvements, intelligent power-management software and emissions-compliant designs, shifting competitive emphasis from sheer horsepower to lifecycle efficiency and total cost of ownership.

By Application: Mineral Mining Gains on Battery-Material Demand

Metal mining accounted for 48.15% of 2025 revenue, driven by copper, iron ore, and gold. However, mineral mining is expected to grow at a 9.03% CAGR by 2031, as projects for lithium hydroxide, high-purity quartz, and rare earths proliferate. Coal demand softens in OECD nations but remains strong in the Asia-Pacific; Coal India ordered several mining trucks in late 2024. Autonomy and electrification adoption rates diverge by commodity: metal mines account for a notable share of BEV and autonomous-truck deployments, whereas coal remains overwhelmingly manual.

Mineral mining fragments into niche equipment: brine pumps for salars, dense-media separation for hard-rock lithium, and solvent extraction for rare earths. Metal miners focus on trolley assists, drilling accuracy, and grade-control systems. Regional correlations persist—Asia-Pacific’s mineral expansion centers on aggregates, while Africa flags copper and cobalt for battery chains. This differentiation keeps the mining equipment market heterogeneous and ripe for specialized OEM plays.

By Mining Type: Surface Dominates While Underground Gains Momentum

Surface mining accounted for 69.04% of the mining equipment market share in 2025, reflecting the prevalence of open-pit copper, iron-ore, coal, and bauxite operations that depend on large fleets of trucks, shovels, and draglines. The scale of these operations—often exceeding 200 million tons per annum—keeps surface fleets indispensable for bulk commodities even as autonomy and trolley-assist electrification curb unit fuel burn. Capital budgets in Western Australia’s Pilbara and Brazil’s Carajás continue to gravitate toward ultra-class surface gear, reinforcing the segment’s spending heft.

Underground mining is forecast to expand at an 8.45% CAGR between 2026 and 2031, handily outpacing surface growth as high-grade zones migrate deeper and narrow-vein battery-mineral deposits proliferate. Battery-electric loaders and articulated trucks are gaining traction in Canada, Finland, and South Africa, where ventilation regulations are pushing operators to replace diesel units 5 to 7 years early, a dynamic that is multiplying the underground slice of the mining equipment market. Autonomy also penetrates underground faster than on surface ramps because confined headings create controlled navigation environments, enabling OEMs to bundle drive-by-wire kits with battery packs and digital twins. The convergence of electrification and automation, therefore, positions underground projects as pivotal demand nodes despite their smaller tonnage footprint in the global mining equipment market.

Geography Analysis

The Asia-Pacific region maintained a 59.35% mining equipment market share in 2025, buoyed by Chinese coal mechanization, Indonesian nickel growth, and Indian iron-ore upgrades. Chinese fleet renewals plateau as coal volumes stabilize and emission rules tighten, but Indonesia ordered several haul trucks to feed stainless-steel capacity. Australia transitions from expansion to replacement demand, swapping diesel for autonomous BEVs to meet 2030 targets. Japan and South Korea import most of their equipment, yet their domestic firms—Komatsu, Hitachi, and Hyundai—export a notable share of their output.

The Middle East and Africa region is poised for an 8.04% CAGR through 2031, driven by Saudi phosphate, South African platinum modernization, and Congolese copper. Recently, Ma’aden placed the region’s most significant single order, securing a substantial number of Caterpillar 795F AC trucks for Wa’ad Al Shamal. Responding to South Africa's upcoming diesel particulate limits, Impala Platinum made a strategic move by ordering a significant number of Sandvik BEV loaders. Meanwhile, DRC’s Kamoa-Kakula is pioneering energy innovation in frontier markets, operating autonomous trucks powered by a solar-plus-battery microgrid.

North America trends toward replacement spending and autonomy retrofits. In Canada, Newmont’s Borden was positioned as an all-electric underground gold mine, highlighting the direction of fleet electrification.[3]“Coleman Mine BEV Case Study,” Vale S.A., vale.com

Whereas in South America, Chile, copper pits are adopting trolley assists, achieving a considerable reduction in diesel consumption per ton hauled. Brazil is bolstering its iron-ore capacity, with additional Liebherr T 284s set to arrive over the next few years. However, Europe is facing challenges: recently, no greenfield hard-rock mine secured financial closure due to regulatory uncertainties, stalling capital influx. These regional disparities highlight the significant impact of policy and commodity dynamics on the mining equipment market.

Competitive Landscape

In 2025, Caterpillar, Komatsu, and Sandvik collectively maintained a significant share of the market revenue, but their dominance is gradually declining. Chinese competitors, offering lower prices and local assembly, are increasingly capturing market share. Meanwhile, Western giants like Caterpillar and Komatsu are securing customer loyalty through bundled hardware-software contracts—such as Cat's MineStar and Komatsu's KOMTRAX. These contracts, which integrate predictive maintenance and operator training, significantly increase customers' switching costs. Sandvik and Epiroc have established a strong presence in battery-electric underground markets, where operational savings from reduced ventilation costs justify higher capital investments. XCMG and SANY are gaining traction in the global haul-truck market by leveraging financing deals with flexible payment options and local content.

Autonomous technology has become a critical area of competition. Komatsu's FrontRunner operates across multiple continents, while Caterpillar's Command manages a substantial fleet, creating a duopoly that poses challenges for other OEMs. The development of autonomous systems has seen significant advancements, with a growing number of patent filings reflecting the industry's focus on innovation. Komatsu, Caterpillar, and Hitachi have emerged as leaders in this space, securing a considerable share of these patents. This technological race is reshaping the competitive landscape, as companies strive to enhance operational efficiency and safety through automation. The adoption of autonomous solutions is also driving changes in workforce dynamics, requiring new skill sets and training programs to manage and operate these advanced systems.

Compliance with ISO 17757 safety standards now requires an extended validation period, raising barriers for new entrants. This regulatory requirement has added complexity to the development and deployment of autonomous and safety-critical systems, making it more challenging for smaller players to compete. The trend of consolidation continues, with established players strengthening their positions through strategic acquisitions and investments. For instance, Epiroc acquired a battery-drive specialist to expand its capabilities in sustainable mining solutions. At the same time, Komatsu has invested in lithium-ion cell production to secure a reliable supply chain for its electric equipment. Meanwhile, start-ups are actively exploring emerging technologies such as hydrogen fuel-cell trucks and AI-driven diagnostics. These innovations aim to address market gaps that incumbents have yet to fully exploit, creating opportunities for disruption and industry growth.

Mining Equipment Industry Leaders

Caterpillar Inc.

Liebherr-International AG

Epiroc AB

Komatsu Ltd.

Sandvik AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Vale and Caterpillar agreed to expand the Pará Northern System autonomous-truck fleet from 14 to almost 90 units by 2028.

- October 2025: India’s BEML partnered with Italy’s Tesmec to introduce surface miners capable of cutting and crushing without blasting.

- September 2025: Weir unveiled redesigned ENDURON jaw and cone crushers with hydraulic power units enabling push-button CSS adjustments.

- April 2025: Epiroc won an underground-equipment order and full-service contract from Hindustan Zinc covering six to eight years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global mining equipment market as the value of new, factory-built machinery and vehicles, including excavators, haul trucks, loaders, drills, crushers, and mineral-processing systems, that are purchased for surface or underground extraction and material handling across metal, mineral, and coal operations.

Scope exclusion: Refurbished machines, equipment leased or rented, consumable wear parts, and standalone software licenses are not counted.

Segmentation Overview

- By Equipment Type

- Surface Mining Equipment

- Underground Mining Equipment

- Mineral Processing Equipment

- Drills and Breakers

- Crushing, Pulverizing and Screening

- Loaders and Haul Trucks

- By Automation Level

- Manual Equipment

- Semi-Autonomous Equipment

- Fully Autonomous Equipment

- By Powertrain Type

- Internal-Combustion Engine Vehicles

- Battery-Electric Vehicles

- Hybrid Vehicles

- By Power Output

- Less than 500 HP

- 500 - 1,000 HP

- Above 1,000 HP

- By Application

- Metal Mining

- Mineral Mining

- Coal Mining

- By Mining Type

- Surface Mining

- Underground Mining

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Sweden

- Rest of Europe

- Asia

- China

- India

- Japan

- South Korea

- Indonesia

- Rest of Asia

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Democratic Republic of Congo

- Zambia

- Rest of Africa

- Oceania

- Australia

- New Zealand

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured discussions with procurement heads at iron-ore, copper, and coal producers in Asia-Pacific, the Americas, and Africa, together with senior product managers at dealer networks, validated utilization cycles, average selling prices, and emerging demand for sub-500 HP battery-electric loaders.

Follow-up surveys of equipment-finance specialists refined replacement-rate assumptions.

Desk Research

Analysts compiled baseline data from open sources such as UN Comtrade shipment codes for HS-84 mining machinery, the International Council on Mining and Metals production tables, USGS mineral statistics, and national safety-agency equipment registries.

Additional context came from World Bank commodity price series, OECD gross fixed capital formation, and OEM investor filings.

Subscription resources, notably D&B Hoovers for company financials and Dow Jones Factiva for news on capacity additions, supplemented the public record.

The sources cited here illustrate the range; many others informed data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down production and trade rebuild established 2025 demand volumes; then selective bottom-up roll-ups of sampled OEM unit shipments multiplied by verified ASPs cross-checked totals.

Key inputs include the top-40 miners' capital expenditure outlook, average copper and thermal coal prices, drilled meterage split between surface and underground sites, horsepower mix, and battery-electric penetration.

Forecasts to 2030 are generated through multivariate regression combined with scenario analysis so price elasticity and commodity cycle swings adjust growth paths.

Where bottom-up gaps appeared, regional import data and capacity utilization curves bridged differences before final reconciliation.

Data Validation & Update Cycle

Each draft model runs through anomaly screens that compare outputs with historical replacement curves and ICMM safety inspection counts.

Variances greater than five percent trigger re-verification with sources or fresh calls to respondents.

Reports refresh annually, with interim updates when events such as major mine closures, regulatory shifts, or large fleet electrification orders materially change demand.

Why Mordor's Mining Equipment Baseline Commands Reliability

Published estimates often differ because firms adopt varying scopes, price bases, and refresh timings, and because some fold in rental or service revenue while others do not.

Key gap drivers include differing inclusion of used equipment sales, treatment of maintenance contracts as equipment revenue, currency conversion practices, and the commodity basket chosen to project future investment.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 123.04 B (2025) | Mordor Intelligence | |

| USD 148.74 B (2024) | Global Consultancy A | Counts rental and aftermarket services, relies mainly on vendor revenue disclosures |

| USD 141.31 B (2023) | Trade Journal B | Combines used equipment sales and applies uniform ASP uplift without geography weighting |

The comparison shows that Mordor's disciplined scope selection, variable-level validation, and yearly refresh cycle deliver a balanced and transparent baseline that decision-makers can trace to clear inputs and repeatable steps.

Key Questions Answered in the Report

How large is the global mining equipment sector today and what value is expected by 2031?

It generated USD 123.04 billion in 2026 and is forecast to reach USD 160.32 billion by 2031 at a 5.44% CAGR.

Which region currently drives the highest equipment demand?

Asia-Pacific leads with 59.35% of 2025 revenue, propelled by coal mechanization, nickel expansions, and large iron-ore fleets.

What growth rate is projected for underground mining equipment?

The underground mining segment is set to grow at an 8.45% CAGR through 2031 as ore bodies move deeper and narrower.

Why is the Middle East & Africa outlook so strong?

New copper, cobalt, lithium, and phosphate projects are fueling an 8.04% regional CAGR through 2031.

Page last updated on: