Container Handling Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

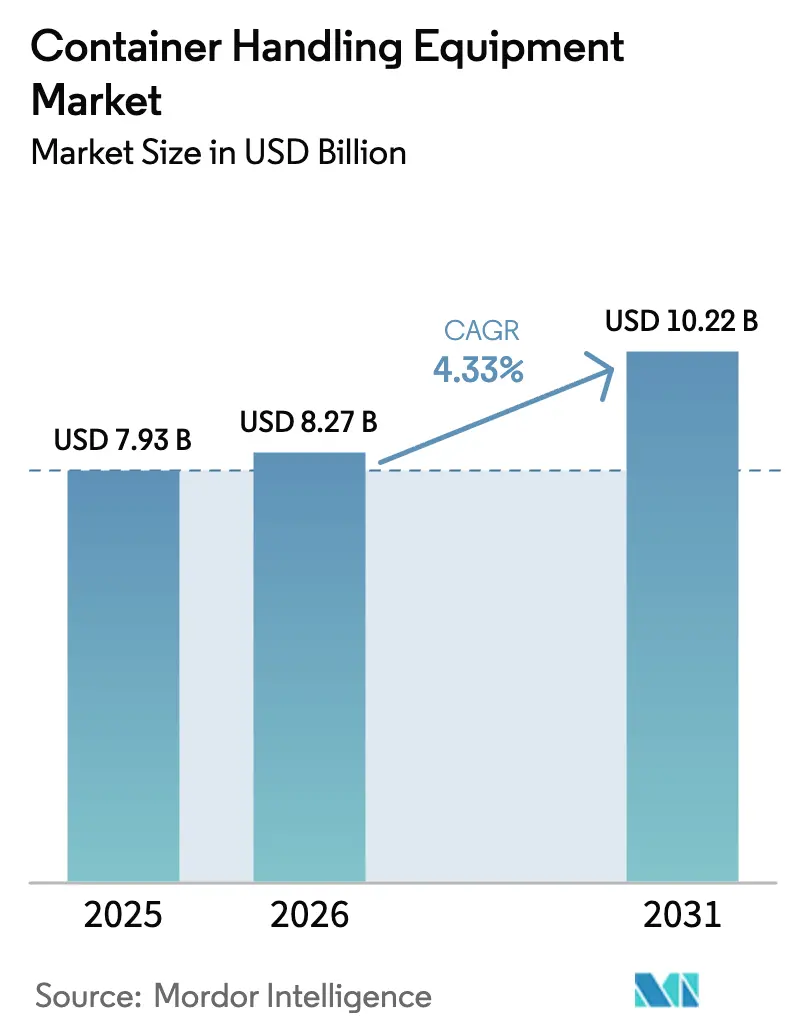

| Market Size (2026) | USD 8.27 Billion |

| Market Size (2031) | USD 10.22 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Container Handling Equipment Market Analysis by Mordor Intelligence

The container handling equipment market size is expected to grow from USD 7.93 billion in 2025 to USD 8.27 billion in 2026 and is forecast to reach USD 10.22 billion by 2031 at a 4.33% CAGR over 2026–2031. This measured growth reflects operators balancing aggressive decarbonization mandates with the capital intensity of fleet electrification. Terminal owners are delaying blanket replacements until charging infrastructure and grid upgrades materialize, while technology suppliers focus on modular retrofits that minimize downtime. The Asia-Pacific emerged as a significant revenue contributor, while the battery-electric propulsion segment is witnessing substantial growth. This trend highlights that advancements in propulsion technology are expected to play a more significant role in shaping the next investment cycle, surpassing throughput volume.

Competitive pressures are escalating, with Chinese manufacturers offering considerably lower prices than their European counterparts for similar specifications. In response, established brands are prioritizing lifecycle-service contracts that encompass predictive maintenance, energy-management software, and uptime assurances. Furthermore, inland depots and rail yards, which seaports have traditionally overshadowed, are now experiencing steady expansion. This development is driven by shippers shifting transloading activities inland to mitigate congestion at marine gateways.

Key Report Takeaways

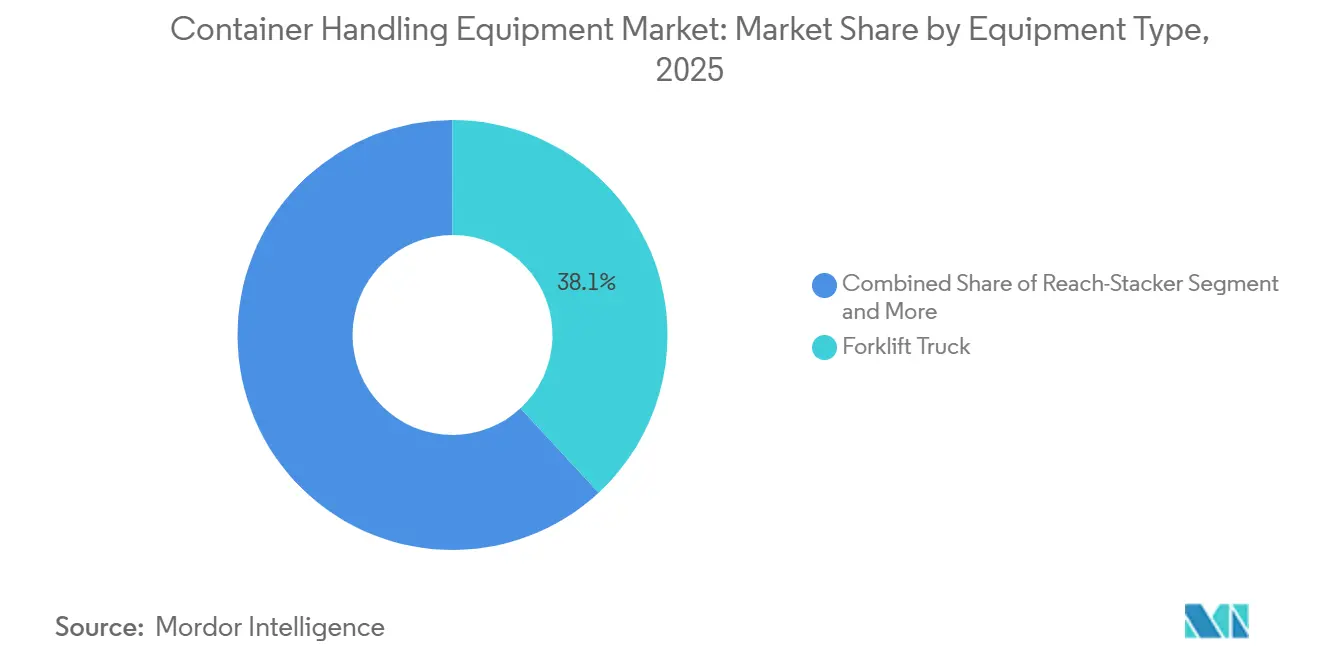

- By equipment type, forklift trucks captured 38.12% of the container handling equipment market share in 2025, while automated guided vehicles are projected to grow at a 10.85% CAGR through 2031.

- By propulsion type, diesel-powered units maintained 58.04% of the container handling equipment market size in 2025; battery-electric units are advancing at a 17.31% CAGR through 2031.

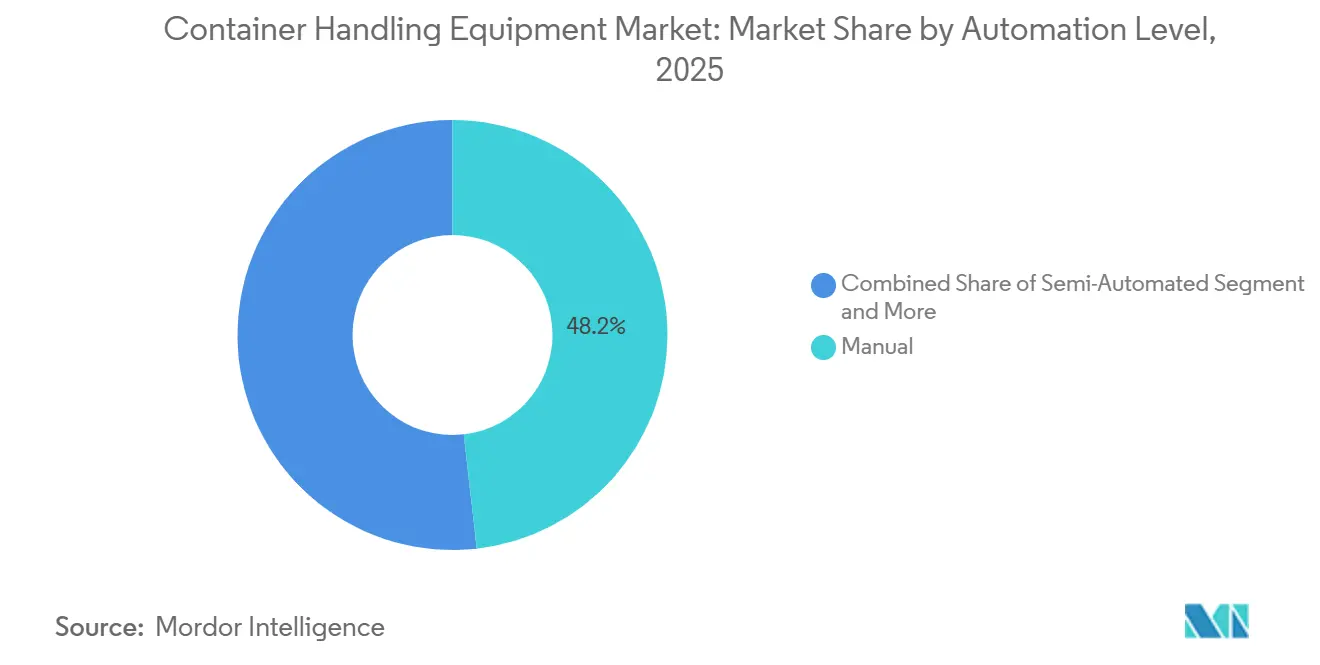

- By automation level, manual systems held 48.15% of the container handling equipment market share in 2025; fully automated configurations are expected to expand at a 20.14% CAGR through 2031.

- By end-user, seaports and river terminals contributed 73.25% of the container handling equipment market size in 2025, whereas inland depots and rail yards are projected to rise at an 8.96% CAGR through 2031.

- By geography, the Asia-Pacific region controlled 44.22% of the container handling equipment market size in 2025, and is projected to advance at a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Container Handling Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automating Terminal Operations | +1.5% | Asia-Pacific core, expanding to the Middle East and South America | Long term (≥4 years) |

| Electrifying Container Handling Fleets | +1.2% | Global, with North America and the EU leading | Medium term (2-4 years) |

| Global Port Capacity Expansion | +0.9% | Global, concentrated in Asia-Pacific and the Middle East | Short term (≤2 years) |

| Modular High-Capacity Charging | +0.6% | North America, EU, select Asia-Pacific hubs | Medium term (2-4 years) |

| Secondary Market for Reach Stacker | +0.4% | Global, emerging in North America and the EU | Medium term (2-4 years) |

| Hydrogen Port Handlers | +0.3% | EU hubs and select Middle East terminals | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Automation and Digitalization of Terminal Operations

PSA's Tuas facility in Singapore has implemented advanced automation technologies, which have significantly improved operational efficiency and reduced workforce requirements. Konecranes' remote operating stations in Hamburg enable a single operator to manage multiple ship-to-shore cranes simultaneously, enhancing crane utilization during off-peak shifts. At Tianjin Port, the integration of 5G connectivity ensures precise coordination of autonomous transporters, facilitating safe and efficient mixed-traffic operations. Middleware overlays from Navis and Kalmar are being utilized to upgrade legacy terminal operating systems; however, the implementation process requires a considerable amount of time. In the future, standardized data exchange can reduce integration friction; for container-equipment condition/event messaging, ISO 9897 (CEDEX) defines general communication codes.

Growing Emphasis on Electrification of Container-Handling Fleets

Regulators are tightening emissions standards, prompting operators to adopt battery-electric fleets where utilization is high enough to ensure payback within one business cycle. DP World has deployed all-electric internal transfer vehicles at Laem Chabang as part of its terminal decarbonization roadmap; broader terminal-equipment electrification is being phased rather than completed as a full-fleet conversion. The United States Environmental Protection Agency disbursed USD 411 million in 2024 under the Clean Ports Program to replace several diesel units by 2027 [1]“Clean Ports Program Funding,” U.S. Environmental Protection Agency, epa.gov. High-utilization terminals in California and New Jersey are leading the transition to electric equipment. At the same time, smaller facilities delay investments due to the significantly higher costs of electric units compared to diesel. APM Terminals Barcelona has significantly reduced on-site nitrogen oxides emissions after deploying battery-electric straddle carriers, although the installation required a substantial grid upgrade, co-funded by the port authority. Several ports across North America and Europe have formed the Zero Emission Port Equipment Alliance to standardize charging protocols and leverage bulk battery procurement to achieve cost efficiencies.

Port Capacity Expansion and Rising Global TEU Throughput

Global container throughput experienced significant growth, with capacity expansions primarily focused in the Middle East and Southeast Asia. DP World expanded its Jebel Ali Terminal 4, enhancing capacity and incorporating advanced automation technologies. King Abdullah Port in Saudi Arabia also increased its capacity, adding state-of-the-art equipment to improve operational efficiency. In Singapore, the focus remains on leveraging automation to maximize productivity due to limited land availability. Conversely, terminals in the United States continue to lag in automation adoption, significantly trailing behind global leaders like China, as noted by the Government Accountability Office.

Modular High-Capacity Charging Infrastructure Speeds Electric Roll-Outs

Charging continues to be a significant challenge for the container handling equipment market. At the Port of Los Angeles, ABB's modular system combines fast chargers with a battery storage unit, enabling efficient charging during shift changes without incurring additional demand penalties. Kalmar's FastCharge technology allows rapid charging and is now utilized at multiple terminals worldwide. Siemens' mobile chargers provide adaptability, as they can be relocated across terminal zones to accommodate changing yard layouts. However, despite these technological advancements, high-capacity charging increases overall project costs, and utility demand charges significantly impact operating savings. In Rotterdam, a pilot microgrid that integrates wind power with vehicle-to-grid technology demonstrates the potential to reduce electricity costs effectively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Costs, Slow Returns | -1.1% | Global, acute in emerging markets | Short term (≤2 years) |

| Volatile Component Lead Times | -0.8% | Global, concentrated in North America and the EU | Short term (≤2 years) |

| Legacy Port Grid Bottlenecks | -0.6% | North America, EU, select Asia-Pacific ports | Medium term (2-4 years) |

| Complex Brownfield System Integration | -0.5% | Global, severe at terminals with legacy TOS | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Long Pay-Back Periods

Battery-electric units are significantly more expensive than their diesel counterparts, with charging infrastructure further increasing project budgets. For example, battery-electric reach-stackers are priced considerably higher than diesel models, and fast chargers also add substantial costs. Operators in emerging markets encounter difficulties in obtaining financing, as local banks remain cautious about residual values. This caution leads to higher lease rates compared to diesel. Although the United States Inflation Reduction Act provides investment tax credits, the associated tax-equity structures tend to prolong project timelines [2]“Inflation Reduction Act Guidance,” U.S. Department of the Treasury, treasury.gov. Battery replacements, required after several years of use, often represent a high cost that is frequently excluded from initial budgets. This omission can substantially reduce anticipated savings. Smaller terminals, handling lower volumes of cargo, struggle to distribute fixed infrastructure costs effectively. Consequently, diesel continues to be the more cost-effective option unless regulations enforce a transition.

Supply-Chain Lead-Time Volatility for Critical Components

Lead times for lithium-ion battery packs and industrial semiconductors have significantly increased, creating challenges in meeting equipment deployment timelines before grant deadlines. Battery manufacturers are focusing on automotive clients, resulting in limited availability for industrial sectors. Foundries are reallocating capacity away from legacy semiconductor nodes used in motor controllers due to lower profitability. Tariff uncertainties related to Chinese steel are driving a shift toward local fabrication, but the establishment of new facilities involves extended ramp-up periods. Reliance on single sources for traction motors and inverters has caused delays in fulfilling several major orders. To address these challenges, operators are placing equipment orders much earlier, a strategy that secures supply but restricts financial flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Forklift Dominance Meets AGV Disruption

Forklift trucks accounted for 38.12% of the container handling equipment market share in 2025, a testament to their versatility across seaports, inland depots, and warehouses. Automated guided vehicles, although starting from a smaller base, are growing at a 10.85% CAGR, propelled by rising labor costs and a push for continuous operations. By the mid-2020s, terminal tractors are expected to lead the shift toward electrification, with battery-electric models gaining significant traction. In contrast, reach-stackers are slower to adopt electrification due to the higher energy demands of their telescopic-boom work cycles compared to fixed-mast forklifts. Straddle carriers are increasingly utilizing hybrid diesel-electric drivetrains, which efficiently capture braking energy and provide notable fuel savings without requiring charging infrastructure.

The deployment of automated guided vehicles (AGVs) is expected to expand globally, with notable adoption in key regions. Although AGVs involve higher initial costs, they deliver operational efficiencies by optimizing container-yard density and reducing truck waiting times. Additionally, rubber-tired gantry and ship-to-shore cranes are being equipped with remote-operation capabilities, enhancing their utilization during non-peak hours. Fully autonomous rail-mounted gantry cranes have demonstrated significant safety improvements and operational efficiency gains. However, AGV projects continue to face challenges related to infrastructure costs for guidance systems, necessitating careful evaluation of long-term costs before implementation.

By Propulsion Type: Diesel Incumbency Faces Electric Acceleration

Diesel propulsion retained 58.04% of the container handling equipment market share in 2025, reflecting the entrenched installed base and ubiquitous refueling infrastructure. Battery-electric equipment is projected to expand at a 17.31% CAGR through 2031, driven by declining battery prices. Hybrid units captured a nominal share of new sales, offering emissions gains without a full charging infrastructure. Hydrogen has remained niche but is poised to grow as green hydrogen production scales up at major hub ports.

In the near future, the United States EPA plans to replace a significant number of diesel units, focusing on key states such as California, New Jersey, and Washington. Meanwhile, European ports will soon face penalties for non-compliant diesel units, driving a shift towards electrification. Although diesel continues to dominate high-utilization assets—those operating extensively throughout the year—due to the advantage of continuous refueling over charging downtimes, the total cost of ownership is transforming. In many regions, electricity costs are increasing compared to diesel prices.

By Automation Level: Manual Operations Persist Amid Autonomous Gains

Manual systems held 48.15% of the container handling equipment market share in 2025, mainly because labor-intensive emerging markets have wage levels below the breakeven point of automation. Semi-automated solutions captured a significant share by adding collision avoidance and smart positioning without eliminating drivers. Fully automated configurations are projected to grow at a 20.14% CAGR through 2031, particularly in China and the Middle East, where greenfield projects are increasingly adopting lights-out operations. Yangshan Phase IV operates entirely without manual intervention, achieving high handling accuracy and lower operating costs.

Brownfield retrofits are generally slower and more expensive to implement. In Hamburg, remote-operated cranes significantly improved utilization but required extensive customization of the TOS over a prolonged period. In the United States and certain European regions, labor agreements restrict the extent of automation, necessitating the use of hybrid fleets and limiting the immediate adoption of automation. Meeting ISO 3691-4 safety standards adds considerable costs due to the need for redundant sensors. However, automated yards demonstrate clear advantages by delivering higher throughput per acre, which becomes increasingly critical as land availability near urban gateways diminishes.

By End-User: Seaports Lead, Inland Depots Accelerate

Seaport and river terminals represented 73.25% of the container handling equipment market size in 2025, driven by the concentration of international trade at marine gateways. Inland depots and rail yards, however, are projected to grow at an 8.96% CAGR through 2031, as beneficial cargo owners pursue near-dock transloading and enhance supply chain resilience. Container freight stations serving e-commerce captured a significant share of demand, leveraging high-density storage systems.

Rail-linked inland depots use electric reach-stackers and rubber-tired gantry cranes to offload double-stack trains, cutting marine terminal dwell times by 20-30%. BNSF Railway’s procurement of electric gantry cranes for Southern California intermodal sites demonstrates rail’s rising role. Warehouse operators favor lithium-ion forklifts that allow opportunity charging, avoiding floor-space-intensive battery swaps. The shift inland is expected to grow as seaport land values and urban restrictions limit on-dock expansion.

Geography Analysis

The Asia-Pacific region accounted for 44.22% of the container handling equipment market share in 2025 and is projected to grow at a 6.88% CAGR through 2031. China alone processed more than 220 million TEUs from January to August 2024 and is replicating the Yangshan Phase IV automation model at Qingdao and Tianjin. India’s Jawaharlal Nehru Port Authority (JNPA) has stated its container handling capacity is expected to increase to about 10.4 million TEUs by 2027 as projects come online. Southeast Asian hubs, such as Singapore and Port Klang, utilize automation to offset tightening labor markets. At the same time, Japan and South Korea are prioritizing the electrification of existing fleets to meet their carbon-neutral pledges.

Europe held a notable share of 2025 revenue, constrained by mature throughput and labor protections, yet propelled by zero-emission deadlines. Rotterdam handled 13.8 million TEU in 2024 and continues to electrify and pilot alternative fuels alongside shore power initiatives to reduce maritime-related CO2 emissions by 2030. Hamburg’s remote crane program has improved utilization, and Antwerp-Bruges is investing in electric tractors and automated rail-mounted gantries. Southern European ports, such as Valencia and Piraeus, are expanding their capacity to capture near-shored manufacturing flows into the Mediterranean. North America captured a significant share of the container handling equipment market size in 2025. The Port of Los Angeles received a USD 411.7 million Clean Ports Program grant, supporting replacement of nearly 425 pieces of cargo-handling equipment and installation of ~300 charging ports (plus other supporting infrastructure) over the implementation window[3]. Canada’s Vancouver and Montreal focus on automated gantry cranes to integrate with cross-country rail corridors, while Mexican ports benefit from nearshoring trends in the United States.

The Middle East and Africa held a notable position in the market. DP World’s Jebel Ali Terminal 4 significantly increased its capacity and introduced advanced automated equipment in 2025. Saudi Arabia’s King Abdullah Port expanded its operations, while Egypt’s Suez Canal Container Terminal implemented new electric gantry cranes. South Africa, despite operational challenges, has committed substantial investments toward port modernization. Turkey’s Ambarlı Port is upgrading its infrastructure with autonomous guided vehicles to enhance connectivity along the Europe-Central Asia corridors. South America also held a modest share of the market. Brazil’s key ports underwent modernization as part of privatization efforts. Peru’s Callao port enhanced its infrastructure with advanced cranes and gantry systems in 2025. Argentina and Chile are adopting automation technologies to address labor-related challenges. Furthermore, restrictions on transit through the Panama Canal, caused by drought conditions, have shifted demand to Pacific Coast terminals, driving increased equipment procurement.

Competitive Landscape

The container handling equipment market is moderately concentrated, with Kalmar, Konecranes, ZPMC, Liebherr, and SANY together supplying a notable share of global shipments in 2025. Chinese makers use vertically integrated supply chains to underprice European rivals by up to 30%, forcing incumbents to compete on lifecycle services.

Retrofit electrification is an emerging area of opportunity. Taylor Machine Works offers a kit to convert diesel reach-stackers, targeting North American and European units. GAUSSIN fields autonomous electric tractors with five-minute battery swaps and has pilots in Dubai and Singapore. Software platforms are becoming central; Kalmar TLS and Navis N4 vie to become the operating system for automated terminals, echoing platform plays in adjacent industries. Patent activity in collision avoidance and energy optimization rose, led by Konecranes, ABB, and Siemens.

Lifecycle revenue now outweighs hardware margins. Operators demand performance guarantees tied to uptime and kilowatt-hours consumed. Chinese brands respond with on-site parts depots, while European firms bundle remote diagnostics and predictive analytics. Regional assemblers retain footholds where local-content rules apply, sustaining fragmentation below the top tier.

Container Handling Equipment Industry Leaders

SANY Group

Liebherr Group

Konecranes Oyj

Kalmar Corporation (Cargotec)

Shanghai Zhenhua Heavy Industries Co., Ltd. (ZPMC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Luka Koper ordered four Konecranes electric rubber-tired gantry cranes for delivery in 2026 to extend its 2024 electrification program.

- October 2025: APM Terminals Lázaro Cárdenas received a fully electric Super-Post-Panamax ship-to-shore crane to support a capacity lift to 2.2 million TEU by 2026.

- October 2025: Konecranes debuted the Noell hydrogen fuel-cell straddle carrier at TOC Americas after trials at HHLA’s test field in Hamburg.

- March 2025: EUROGATE Hamburg placed an order for 15 hybrid Noell straddle carriers with modular drive trains enabling future battery or hydrogen retrofits.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the container handling equipment market as the global sales value of purpose-built machines, such as reach stackers, straddle carriers, rubber-tired gantry cranes, ship-to-shore cranes, terminal tractors, automated guided vehicles, and heavy forklifts, that move ISO freight containers within seaports, river terminals, rail yards, inland depots, and large warehouses. These units are counted the year they are factory-built and first delivered into service, regardless of leasing model or geographic destination.

Scope exclusion: software and standalone automation systems that do not ship with physical lifting hardware are outside the market.

Segmentation Overview

- By Equipment Type

- Forklift Truck

- Reach Stacker

- Straddle Carrier

- Rubber Tired Gantry Crane

- Ship-to-Shore Crane

- Automated Guided Vehicle (AGV)

- Terminal Tractor/Yard Truck

- By Propulsion Type

- Diesel

- Hybrid

- Battery Electric

- Hydrogen Fuel Cell

- Others (Gasoline, LPG, etc.)

- By Automation Level

- Manual

- Semi-Automated

- Fully Automated

- By End-User

- Seaport and River Terminals

- Inland Container Depots/Rail Yards

- Container Freight Stations and Warehouses

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Turkey

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed port engineering heads, equipment procurement managers, finance controllers at leading OEMs, and yard automation specialists across Asia-Pacific, Europe, North America, and the Gulf. These dialogues clarified renewal triggers, emerging hydrogen trials, and realistic automation pay-back periods, which we then used to tighten model assumptions and stress-test early desk findings.

Desk Research

We began by mapping the installed base, replacement cycles, and new-build deliveries using open datasets from bodies such as UNCTAD, the International Association of Ports and Harbors, and the World Bank's maritime trade indicators. National customs logs, port authority throughput dashboards, and equipment certification lists added fine-grained shipment clues, while energy transition road maps from the International Energy Agency informed propulsion splits. Company 10-Ks, investor decks, and equipment testing certificates were mined through Dow Jones Factiva and D&B Hoovers to anchor average selling prices and OEM revenue mix. The United States EPA, the European Environment Agency, and China's MIIT offered regulatory timelines that guided our drivetrain forecast. The sources cited above are illustrative; many additional public and paid references fed the desk study matrix.

Market-Sizing & Forecasting

A top-down demand pool was first built by correlating global loaded-container throughput, average container moves per new machine, and fleet renewal ratios. Results were checked with selective bottom-up roll-ups of sampled OEM shipments multiplied by region-specific ASPs to tune currency effects and niche equipment premiums. Key variables include global TEU growth, port capex intensity, average power train cost deltas, terminal automation penetration, diesel-to-electric price spreads, and fleet age distribution. Forecasts use a multivariate regression that links equipment demand to TEU volume, port capex indices, and an electrification index, after which three scenario layers adjust for trade elasticity shocks. Data gaps in sampled ASPs are bridged through weighted regional proxies validated during primary calls.

Data Validation & Update Cycle

Before sign-off, model outputs undergo variance checks against historical sales curves, import-export anomalies, and capital equipment price indices. Senior analysts review the workbook and trigger re-contacts when deviations breach preset bands. We refresh every twelve months and issue interim patches if sizable regulatory or trade events occur.

Why Mordor's Container Handling Equipment Baseline Commands Reliability

Published numbers often diverge because firms select different equipment sets, apply varied ASP progression rules, or freeze exchange rates at dissimilar points. We disclose each filter and update cadence, allowing buyers to trace every step.

Key gap drivers arise when others omit inland depots, mix broader material handling categories, apply single global prices, or project aggressive automation uptake without validating capital budgets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.27 B (2025) | Mordor Intelligence | - |

| USD 8.03 B (2024) | Global Consultancy A | Excludes yard tractors and hydrogen units, relies on TEU proxy with minimal ASP nuance |

| USD 7.99 B (2024) | Trade Journal B | Counts only seaport terminals, omits inland depots and rail yards |

| USD 8.75 B (2025) | Industry Association C | Blends cranes with generic material handling gear and applies a flat global ASP |

The comparison shows that once scope, equipment mix, and pricing logic are aligned, our figure sits mid-range and therefore offers a balanced anchor. Clients can depend on Mordor's disciplined source mix, transparent filters, and annual refresh cycle for decisions that withstand board-level scrutiny.

Key Questions Answered in the Report

What is the projected global value of container handling equipment by 2031?

The sector is forecast to reach USD 10.22 billion by 2031, up from USD 8.27 billion in 2026.

Which propulsion technology is growing fastest in container terminals?

Battery-electric equipment is expanding at a 17.31% CAGR through 2031 as falling battery prices and emissions mandates align.

Why are inland container depots gaining equipment demand?

Near-dock transloading strategies shift boxes away from congested seaports, pushing inland depot and rail-yard equipment demand at an 8.96% CAGR through 2031.

How are ports overcoming grid-capacity constraints for electrification?

Terminals pair fast chargers with on-site battery storage or microgrids, shaving peak demand charges and avoiding multi-year utility upgrades.

Page last updated on: