Market Overview

| Study Period | 2019 - 2031 |

|---|---|

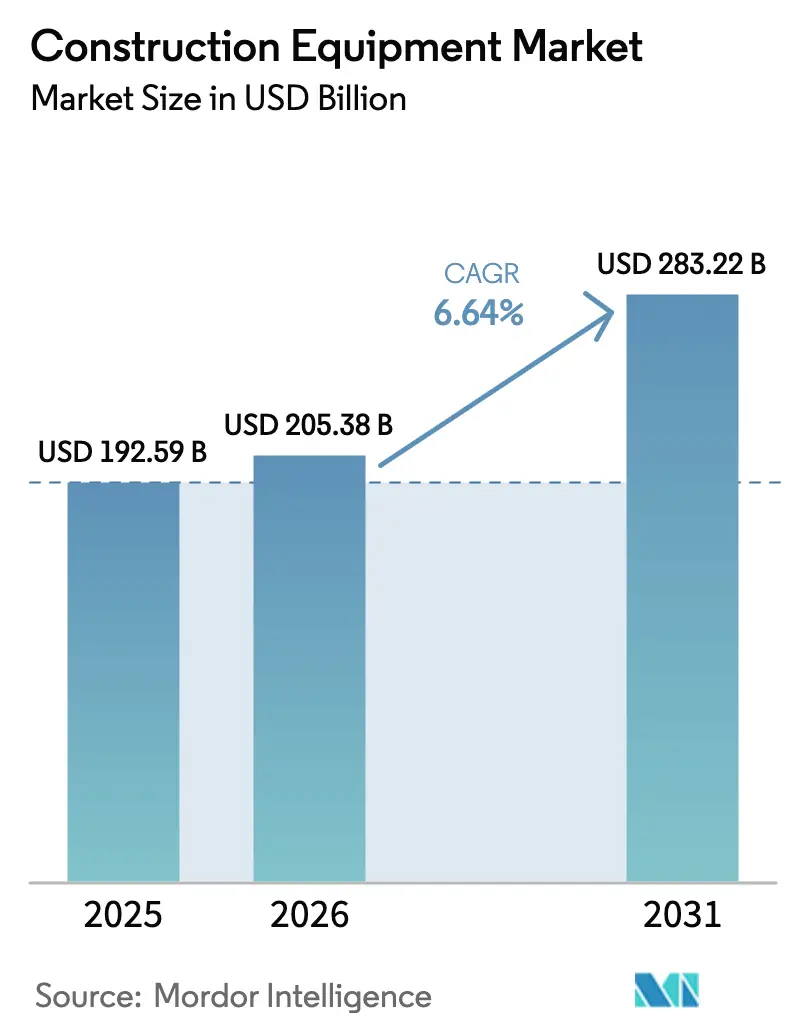

| Market Size (2026) | USD 205.38 Billion |

| Market Size (2031) | USD 283.22 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

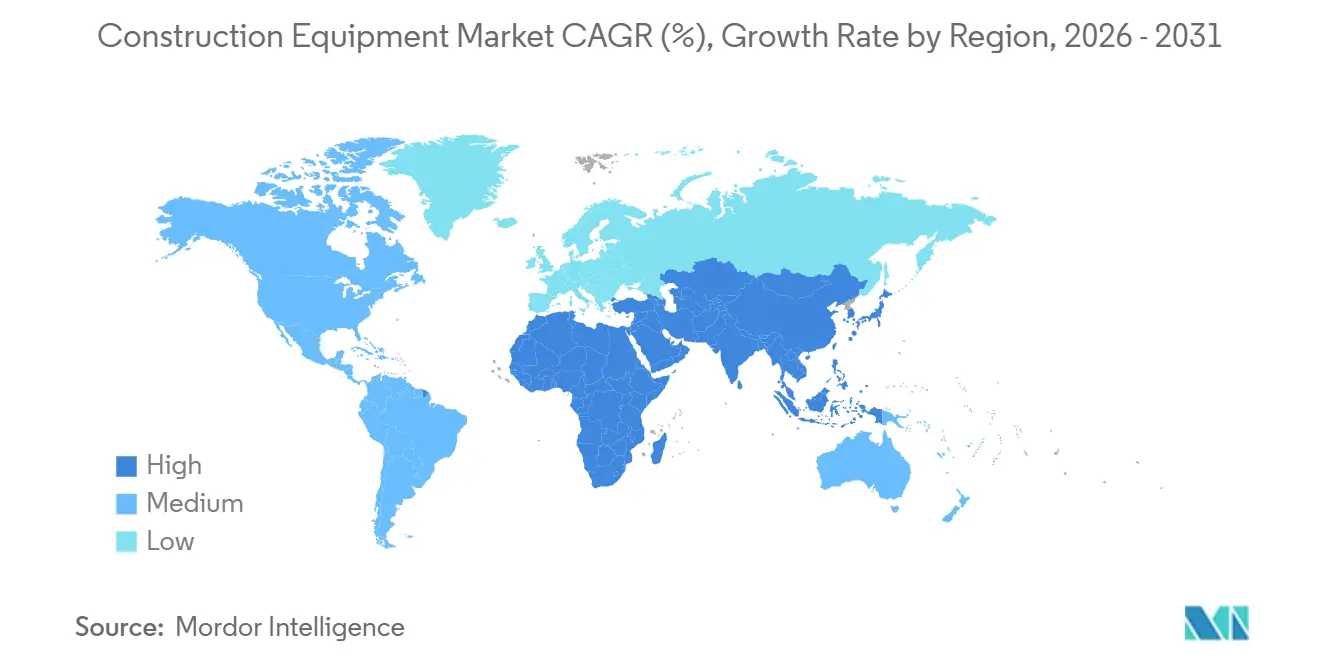

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Equipment Market Analysis by Mordor Intelligence

The construction equipment market stands at USD 205.38 billion in 2026 and is forecast to climb to USD 283.22 billion by 2031, registering a 6.64% CAGR during the period, underscoring steady gains in market size and profit pools. Robust government spending on roads, rail, power transmission, and semiconductor fabs underpins demand across earthmoving, material-handling, and concrete machinery. Asia’s mega-project pipeline, the electrification push in Europe and North America, and the industry-wide tilt toward rental fleets jointly reinforce a resilient growth outlook. Competitive intensity is sharpening as Chinese OEMs capture share abroad while Western leaders pivot to service-centric offerings and autonomous technologies. The construction equipment market is also shaped by quicker fleet renewal cycles driven by Stage V and EPA Phase 3 regulations, tightening the gap between product and digital service launches.

Key Report Takeaways

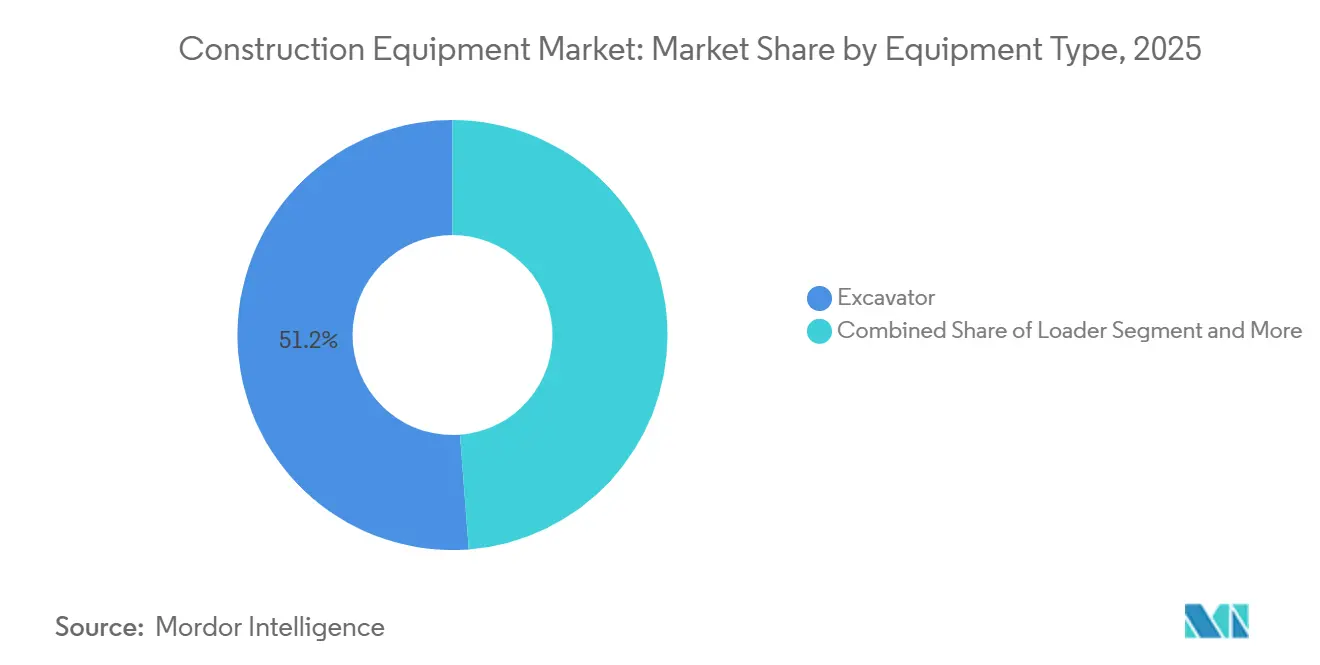

- By equipment type, excavators captured 51.24% of the construction equipment market share in 2025, and is expected to grow at a 7.15% CAGR through 2031.

- By propulsion type, internal-combustion engines retained a 90.12% share, while hybrid battery-electric units are set to expand at a 22.16% CAGR, the quickest pace across the construction equipment market.

- By equipment size, heavy machines above 11 tons held around 71.10% of the construction equipment market size in 2025, while compact/mini (less than 6 tons) equipment category is set to register a 14.55% CAGR.

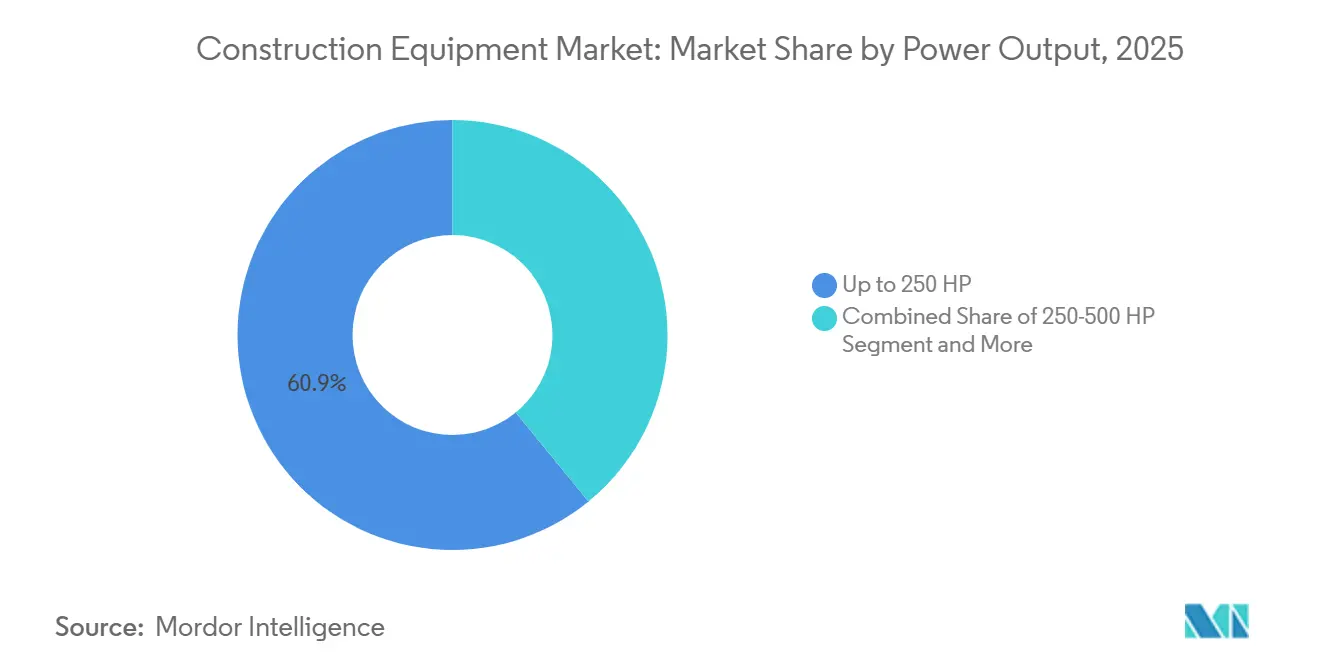

- By power output, sub-250 HP models commanded a 60.85% share, whereas the 250–500 HP band records the highest projected CAGR of 9.62% through 2031.

- By application, infrastructure projects accounted for 73.15% of the construction equipment market share in 2025, whereas mining and quarrying are projected to post a 9.05% CAGR.

- By geography, Asia Pacific led with 45.80% of the construction equipment revenue share in 2025, whereas the Middle East and Africa region is set to register fastest CAGR of 9.12%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Construction Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-Infrastructure Pipelines in Asia | +1.8% | Asia Pacific, Middle East | Medium term (2-4 years) |

| U.S. IRA and CHIPS Acts | +1.2% | North America | Medium term (2-4 years) |

| Rental-First Procurement | +1.1% | Global | Medium term (2-4 years) |

| EU Stage V Caps | +0.9% | Europe | Short term (≤ 2 years) |

| Critical Raw-Material Extraction Surge | +0.7% | Africa | Long term (≥ 4 years) |

| Job-Site Automation | +0.6% | North America, Europe, and advanced Asian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mega-infrastructure Pipelines Across Asia driving Over USD 2 tn Annual Equipment Demand

A committed project pipeline exceeding USD 3.7 trillion is transforming allocation priorities, pulling large dozers, 45-ton excavators, and high-capacity concrete pumps into Asian depots ahead of other regions. Saudi Arabia alone awarded USD 55 billion in projects in 2024, a 57% jump year-on-year, while the UAE lifted awards by 200% to USD 34 billion. OEMs are tailoring sales mixes toward higher horsepower and longer-reach booms, anchoring revenue in the construction equipment market through larger ticket sizes and aftermarket contracts.

U.S. IRA and CHIPS Acts Accelerating Earth-Moving Purchases for On-shoring Projects

Federal incentives for semiconductor fabs, EV plants, and grid upgrades have created a structural pull for 250-500 HP dozers and excavators across the Sun Belt. The American Society of Civil Engineers identifies a USD 3.7 trillion infrastructure gap by 2035, ensuring sustained visibility for OEM order books[1]“A Comprehensive Assessment of America’s Infrastructure 2025,” American Society of Civil Engineers, infrastructurereportcard.org. Contractors, faced with labor constraints, are leaning toward larger units that compress project schedules and ease per-hour operating budgets.

Rental-first Procurement Shift Among Tier-2 Contractors Expanding Utilization Rates

Rental revenues are set to touch USD 82.6 billion in 2025, reflecting a broad contractor preference for off-balance-sheet equipment access. Utilization rates on connected rental fleets often exceed 85%, roughly 30% higher than owned machines, reinforcing a virtuous loop of asset sweating, predictive maintenance, and residual value optimization. OEMs are realigning channel strategies, embedding telematics that feed real-time data to rental partners and promote service contracts.

EU Stage V Emission Caps forcing Rapid Fleet Renewal Toward Hybrid/E-equipment

Stage V rules now encompass engines below 19 kW and mandate finer particulate thresholds. Atlas Copco notes that compact equipment compliance necessitates diesel particulate filters, while Perkins reports 28% higher power density in new Stage V engines. This regulatory pulse accelerates the construction equipment market shift toward battery-electric compact loaders and hybrid drive lines in mid-range excavators.

Restraints Impact Analysis of Construction Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hydraulic Component Shortages | -1.1% | Global | Short term (≤ 2 years) |

| Lithium-Ion Cell Scarcity | -0.8% | Global | Short term (≤ 2 years) |

| Persistent Skills Gap | -0.6% | South America, with spillover to Africa | Long term (≥ 4 years) |

| Municipal Noise-Abatement Bylaws | -0.5% | Urban centers in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Lead-time Spikes (Beyond 42 Weeks) Due to Hydraulic Component Shortages

Delivery windows stretch beyond 42 weeks for critical hydraulic valves and pumps, forcing contractors to adjust project phasing. Market leaders increasingly vertically integrate to secure supply, echoing Caterpillar’s expanded in-house component machining. Persistent bottlenecks threaten to defer replacement cycles and dampen near-term construction equipment market momentum until inventories normalize.

Lithium-ion Cell Scarcity Inflating TCO of Electric Heavy Machinery

Heavy-duty battery packs compete with automotive demand, inflating upfront prices on 20-ton electric excavators by 30% versus diesel peers. This gap compresses buyer ROI windows even though life-cycle costs remain favorable. OEMs with captive battery supply or strategic joint ventures capture early share in the electric slice of the construction equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Construction Equipment Market Segment Analysis

By Equipment Type:

Excavators Anchor Versatility Across ApplicationsExcavators commanded 51.24% construction equipment market share in 2025 and are projected to register a 7.15% CAGR to 2031. Hydraulic efficiency, quick-attach tooling, and telematics integration sustain demand across road-building, utilities, and demolition. Loaders remain second in volume, with wheel loaders favored for paved operations and track loaders for soft terrain. Crane demand follows high-rise and bridge timelines, while graders and rollers maintain road surfaces to millimeter tolerances.

Bulldozers thrive in mining benches where slope stability requires significant drawbar pull, and dump trucks handle hauls beyond 500 meters. Specialty machines, including concrete pumps and trenchers, together hold a significant share of construction equipment market size. Komatsu’s hydrogen-powered prototype signals future fuel diversification, though widespread adoption awaits refueling infrastructure expansion [2]“Hydrogen Excavator Prototype Press Release,” Komatsu, komatsu.com.

By Propulsion Type:

Electrification Gains Amid Diesel DominanceInternal combustion units accounted for 90.12% of 2025 shipments, yet hybrids battery electric models will rise at 22.16% CAGR as regulations tighten. Hybrid systems pair smaller diesel engines with batteries, cutting fuel by 25–35% and enabling quiet, zero-tailpipe operation for idling and indoor work. Caterpillar’s 323 electric excavator delivered lower operating costs on grid-connected redevelopment jobs and logged significant orders by end-2025 [3]“323 Electric Excavator Fact Sheet,” Caterpillar, caterpillar.com.

Globally, hydrogen fuel-cell rigs are operational in limited numbers, primarily in pilot programs across Japan, Germany, and South Korea. JCB is sidestepping the costs associated with fuel cells, aiming to commercialize its hydrogen combustion engine by 2027. The market for zero-emission construction equipment is closely tied to grid capacity and charging infrastructure. As a result, some buyers are leaning towards hybrids, which offer a diesel fallback until a reliable power source is widely available.

By Equipment Size:

Heavy Gear Dominates While Compact OutpacesHeavy equipment larger than 11 tons captured 71.10% of the construction equipment market share in 2025, fueled by freeway, port, and dam projects that demand 45-ton excavators and 60-ton ADTs. Procurement agencies favor large units to accelerate earthworks and lower per-cubic-meter movement costs.

Compact machines below 6 tons are rising faster, expected to register a 14.55% CAGR as dense cities favor agile skid steers, mini loaders, and zero-tail-swing excavators. Quick-attach couplers and a broadening attachment catalog now allow a single compact base unit to replace multiple dedicated tools, improving job-site economics for small contractors and rental fleets alike.

By Power Output:

Mid-Range Engines Strike Optimal BalanceMachines up to 250 HP held 60.85% of the construction equipment market size in 2025, balancing fuel economy with sufficient breakout force for mixed-use projects. OEM product roadmaps emphasize modular engine families that scale from 140 HP to 250 HP using common blocks and electronic controls, reducing parts inventory.

The 250-500 HP cohort is forecasted to expand at 9.62% CAGR to 2031, propelled by high-throughput export terminals and mining overburden removal. Advances in aftertreatment design, including compact SCR modules, now enable Tier 4/Stage V compliance without enlarging engine bays, preserving machine geometry. Units above 500 HP occupy a niche yet indispensable role in ultra-large earthworks and open-pit mining, where cycle time gains translate into outsized production benefits.

By Application:

Infrastructure Leads, Mining Emerges FastestInfrastructure projects represented 73.15% of the construction equipment market in 2025 as governments financed bridge refurbishments, rail extensions, and renewable-energy corridors. U.S. federal outlays via the Infrastructure Investment and Jobs Act are funneled toward highways, while Asia focuses on megacity metro lines. Neighboring segments, such as residential and commercial buildings, maintain stable volumes but face cyclical moderation tied to interest-rate regimes.

Mining and quarrying is the fastest-growing application at a 9.05% CAGR to 2031. Demand for copper, lithium, and rare earths vital to energy transition technologies drives multi-billion-dollar pit expansions across Africa and South America. Autonomous haulage and teleremote drilling, once confined to iron-ore majors, are cascading into mid-tier miners, expanding the technology adoption curve in the construction equipment market.

Geography Analysis

APAC Construction Equipment Market

Asia Pacific led with 45.80% of the construction equipment market in 2025, underpinned by China’s Belt and Road Initiative and India’s National Infrastructure Pipeline. Chinese crawler excavator volumes are set to exceed 150,000 units by 2027, more than doubling 2023 output and reinforcing supplier economies of scale. Manufacturers route high-power diesel inventory to Southeast Asia and GCC job sites while shipping compact electric loaders to Japanese and Korean cities.

MEA Construction Equipment Market

The Middle East and Africa posts the fastest trajectory at 9.12% CAGR through 2031 as Saudi Arabia’s Vision 2030 and the UAE’s Dubai Urban Master Plan funnel billions into housing, tourism, and logistics. Project awards jumped significantly in 2024, tightening regional equipment supply and prompting OEMs to stage temporary import yards at Jebel Ali Port. Heat-tolerant battery chemistries and sealed cabin filtration systems are differentiators in the Gulf slice of the construction equipment market.

North America Construction Equipment Market

North America maintains a solid outlook propelled by industrial reshoring and infrastructure revamps backed by the IRA and CHIPS legislation. EPA Phase 3 standards, effective model year 2027, are nudging fleets toward hybrid and electric compact equipment for urban utility work. Rental giants consolidate to secure scale, evidenced by multi-billion-dollar acquisitions that compress dealer networks and elevate access fees.

Regulatory Landscape

The construction equipment market is being shaped by tightening non-road emissions regimes and expanding safety and product-compliance rules that increasingly cover connected and software-enabled machines. In Europe, EU Stage V requirements continue to drive aftertreatment adoption and faster fleet refresh cycles, while Regulation (EU) 2025/14 (effective 28 January 2025) establishes a harmonized EU type-approval and individual approval system for the road safety of non-road mobile machinery that circulates on public roads. This affects equipment configurations used for roadworks and municipal applications.

In North America, US EPA Tier 4 standards for non-road diesel engines under 40 CFR Part 1039 remain the baseline compliance framework as of 2026. Regulatory momentum is also visible in California, where CARB restarted Tier 5 engine emissions rulemaking work in February 2026 after about a year of inactivity, supporting OEM and fleet planning around next-step emission pathways. Separately, the EU Machinery Regulation (EU) 2023/1230 becomes fully applicable from 20 January 2027, adding requirements that bring AI, connected systems, and cybersecurity considerations into machinery compliance programs.

Value Chain Analysis

The value chain runs from upstream inputs (steel, castings, electronics, engines, hydraulics, undercarriage and tracks) to midstream manufacturing and integration by global OEMs, including Caterpillar, Komatsu, Volvo CE, Deere, Hitachi Construction Machinery, XCMG, SANY, Liebherr, Kubota, and Manitou. On the downstream side, demand is met through dealers, rental fleets, contractors, and a growing set of aftermarket and digital service providers. Component availability continues to influence delivery performance, with hydraulics (valves, pumps) and electronic control modules often among the most schedule-sensitive subsystems for earthmoving and material-handling equipment.

The chain is also being reshaped by localization and platform sharing to manage cost and compliance complexity. In Europe, Kubota and Liebherr announced an OEM supply partnership in April 2025 covering 9-ton and 11-ton wheeled excavators, with production starting in 2026, and Kubota also agreed in April 2025 to procure 14-ton hydraulic excavators from Sumitomo Construction Machinery for the European market. Electrification inputs are increasingly strategic: Manitou Group and Hangcha Group signed an agreement in July 2025 to create a joint venture in Le Mans, France, focused on manufacturing and distributing lithium-ion batteries, and Cummins and Komatsu signed an MOU in September 2025 to collaborate on hybrid powertrain development for surface haulage mining equipment.

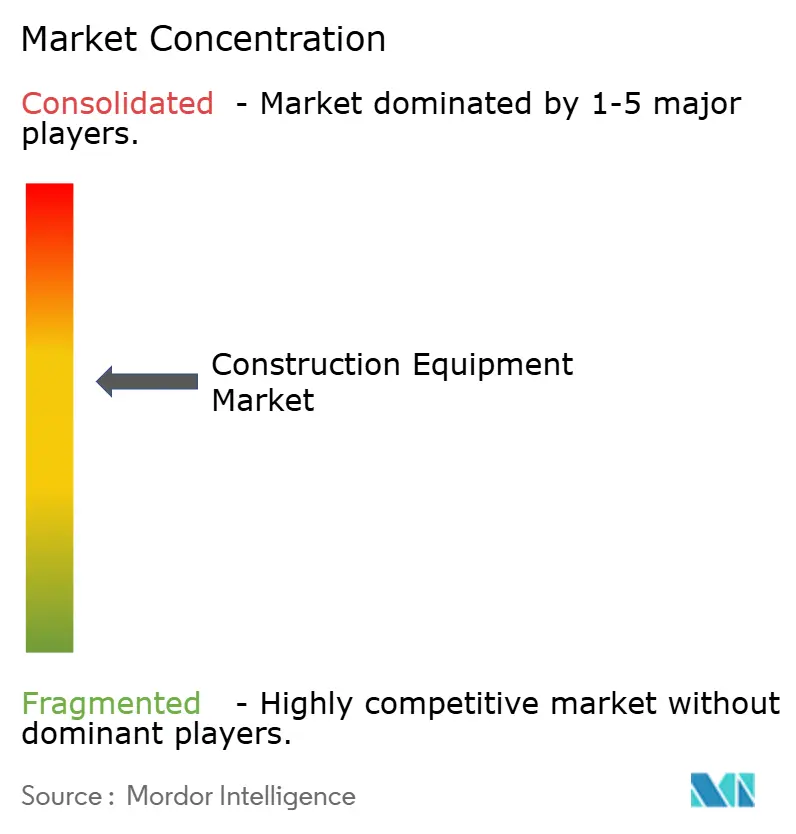

Competitive Landscape

The construction equipment market displays moderate concentration; the top five OEMs, including Caterpillar and Hitachi Construction Machinery, controlled a significant share of global shipments in 2025. Competition intensifies around digital services, autonomous operation, and fuel-agnostic powertrains rather than pure horsepower races. Caterpillar’s shift toward an integrated value chain covering design, logistics, and remanufacturing exemplifies the pivot from iron sales to lifetime service revenue.

Merger and acquisition activity underscores portfolio realignment; Komatsu’s purchase of GHH boosted its underground footprint, while FAYAT’s acquisition of Mecalac broadened its compact offering. Chinese challengers like SANY and XCMG continue double-digit export growth, aided by competitive pricing and accelerated electric rollouts. Rental market consolidation, highlighted by Herc Holdings’ and United Rentals’ consecutive purchases of H&E Equipment Services, reduces bargaining fragmentation and places further pressure on OEM discounting.

Product launches mirror the electrification and automation themes. Komatsu’s Smart Construction 3D guidance enables full 360-degree bucket rotation, creating digital twins that feed progress analytics. Caterpillar’s Stage V telehandlers integrate factory telematics for predictive maintenance, while JCB’s Texas plant expansion signals confidence in sustained U.S. demand. These moves redefine competitive levers beyond unit sales toward data, uptime guarantees, and circular economy programs.

Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Volvo Construction Equipment

Deere & Company

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Construction Equipment Market Companies Covered in this Report

- Caterpillar Inc.

- Komatsu Ltd.

- Deere & Company

- Hitachi Construction Machinery Co., Ltd.

- Volvo Construction Equipment

- CNH Industrial (CASE, New Holland)

- Liebherr-International AG

- Bobcat Company

- Kobelco Construction Machinery Co., Ltd.

- SANY Group

- Xuzhou Construction Machinery Group Co., Ltd.

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- JCB Limited

- HD Hyundai Infracore Co., Ltd.

- Terex Corporation

- Astec Industries, Inc.

- Kubota Corporation

- Sumitomo (HSC Cranes)

Market Opportunities and Future Outlook

Electrification, hybridization, and digital job-site workflows are expanding the addressable value pool beyond iron sales into batteries, software, services, and productivity tooling. OEM actions point to where demand is being cultivated: at CONEXPO-CON/AGG 2026, multiple manufacturers showcased electric, hybrid, and hydrogen-powered equipment across core categories. This indicates that alternative propulsion has moved into mainstream product planning rather than remaining confined to isolated pilots. In May 2026, Liebherr outlined a technology-neutral decarbonization approach, pairing electrification for smaller units with 700-bar gaseous hydrogen storage concepts for larger machines, and highlighting whitespace for suppliers that can package machines, energy storage, and on-site refueling or charging solutions into implementable offerings.

Large project categories and funding mechanisms also create near-term opportunity pockets for earthmoving and compact fleets. In the United States, industry sources have cited rising data center build activity as a demand driver for excavators, loaders, and compact equipment, reinforcing pull from industrial and site-prep work alongside traditional transport infrastructure. At the same time, the September 30, 2026 deadline in the US Congress tied to renewal timing for the Infrastructure Investment and Jobs Act (IIJA) serves as a planning anchor for infrastructure-heavy fleets, increasing the importance of flexible channels such as rental and used equipment as contractors manage timing and procurement risk. Stabilizing key supply bottlenecks (hydraulics, electronics, battery packs) and expanding service coverage in high-growth regions (Asia Pacific and the Middle East and Africa) remain key to capturing project-driven demand.

Recent Industry Developments in Construction Equipment Market

- July 2026: Caterpillar completed the acquisition of Skycatch, a provider of spatial data capture and AI-powered geospatial analysis used in mining and large earthmoving operations. The deal strengthens Caterpillar's technology stack for site digitization and productivity workflows, extending differentiation beyond machine hardware into data-driven services and automation enablers.

- June 2026: Volvo Construction Equipment delivered the first serial-produced A30 Electric articulated haulers to LNS for deployment on the Hafslund hydropower project in Norway. The handover moves battery-electric hauling from prototype activity into early commercial fleet use, giving contractors and OEMs operating references for zero-emission material movement on major infrastructure sites.

- June 2025: Herc Holdings acquired H&E Equipment Services for USD 5.3 billion, accelerating consolidation in the equipment rental channel. A larger combined fleet and footprint increases purchasing leverage and standardizes telematics and service practices, influencing OEM pricing dynamics and aftermarket attach rates.

Construction Equipment Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the construction equipment market is defined as the demand and supply of machines used to execute construction, earthmoving, lifting, hauling, compaction, and related jobsite activities, measured as manufacturer level equipment value in USD across major regions.

Scope exclusions: We exclude standalone jobsite consumables and purely hand-operated tools that are not categorized as construction equipment machines.

Segments Covered in This Report

- By Equipment Type

- Excavator

- Loader

- Mobile Cranes

- Motor Graders

- Bulldozers

- Road Rollers

- Dump Trucks

- Others

- By Propulsion Type

- Internal Combustion

- Hybrid Battery Electric

- Hydrogen Fuel-Cell

- By Equipment Size

- Heavy ( Above 11 tons)

- Medium (6-11 tons)

- Compact/Mini (less than 6 tons)

- By Power Output

- Up to 250 HP

- 250 - 500 HP

- Above 500 HP

- By Application

- Infrastructure

- Residential and Commercial Construction

- Mining and Quarrying

- Oil and Gas/Pipelines

- Industrial and Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean picture of demand signals and supply capacity by geography, then mapping those signals to equipment categories used in construction and adjacent work. We relied on public and official datasets such as national statistics releases on construction output and housing starts, customs trade statistics for machinery categories, and regulators publishing emissions rules that shape replacement cycles, for example EU Stage V and US EPA off-road standards. We also used technical and adoption context from sources such as peer-reviewed journals and patent databases to confirm where electrified or alternative powertrains are becoming practical.

To translate these signals into a usable model, we pulled supporting information from company filings and investor presentations, association and authority websites, and credible press coverage of project pipelines and machine launches. Where needed, paid subscriptions were used only for structured company financials and for shipment and import-export intelligence, mainly to cross-check volumes and pricing bands that were directionally consistent. The desk sources listed here are illustrative and not exhaustive, and additional public references were reviewed to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test assumptions that are hard to read from public data, such as typical utilization patterns, buying versus rental mix, and price movements by machine class. We spoke with a spread of stakeholders across the value chain, including OEM-facing channel participants, fleet owners and rental firms, contractors, and service providers. We then checked that the themes were consistent across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 44% |

| Mid tier: 60% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 14% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where construction activity, infrastructure spend signals, and equipment intensity are used to reconstruct the demand pool by region, and then allocated across major equipment classes. The model is anchored on practical inputs, including construction output and project starts, mining and quarrying activity where relevant, equipment replacement cycles influenced by emissions compliance, and the share of rental fleets in total equipment usage. For value sizing, we track average selling price direction by machine size bands and power output ranges, then reconcile it with interview feedback on recent discounting and financing conditions.

After the first pass, results are corroborated with selective bottom-up approximations, including sampled unit volumes multiplied by indicative ASP ranges, and channel checks on shipment trends for high-volume categories, for example excavators, loaders, cranes, graders, rollers, and dump trucks. When gaps appear in country data, we fill them using proxy indicators such as construction output, import dependence, and fleet age patterns, then recheck assumptions with primary inputs. For forecasting, scenario analysis is applied around the most sensitive drivers, mainly construction spending momentum, interest-rate sensitivity of private projects, and the pace of adoption of new propulsion types. The final path is selected based on the consensus direction heard from practitioners.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and the first checks focus on whether implied unit demand and ASP movement look realistic for each region. Variance checks are then done across adjacent indicators, such as construction activity versus equipment imports, and anomalies are reviewed by another analyst before sign-off. If a number moves outside expected bands, we reopen the underlying assumptions and, when needed, re-contact respondents to confirm what changed in the market.

The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts on emissions, sharp swings in raw material costs that affect pricing, or visible changes in construction pipelines. Before delivery, a final pass is completed so clients receive the latest view that is consistent across the narrative, exhibits, and the market model.

Mordor Intelligence's Construction Equipment Market Estimate Compared With Other Published Estimates

Published market numbers for construction equipment often do not match because each publisher draws the market boundary differently, and then uses different year cutoffs and pricing assumptions to convert units into USD value. The spread can also widen when the forecast path reflects an aggressive or conservative view of construction spending and replacement demand.

Equipment scope and value accounting are usually the biggest gap drivers. Some estimates blend in a broader set of off-highway machines or include services and solutions revenue, which can lift the total even if unit demand is similar. Differences also come from how ASP progression is handled across heavy, medium, and compact equipment, plus whether currency conversion uses an annual average or a point-in-time rate, and how recently the inputs were refreshed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 205.38 B (2026) | |

| Global Consultancy A | USD 242.17 B (2025) | Uses a different base year and, based on the scope notes, may apply a broader global revenue framing without the same equipment boundary and category-level unit and pricing cross-checks, which can shift totals upward. |

| Industry Publisher B | USD 258.54 B (2025) | Includes both heavy and compact equipment and also mentions products plus services/solutions, which expands what is counted beyond equipment-only value and can inflate the headline figure versus an equipment sales-only view. |

Construction output signals, import and shipment direction, and category-level unit checks are the evidence used to keep the 2026 value tied to the equipment demand pool in Mordor Intelligence's estimate. When you line up the year, keep equipment-only boundaries consistent, and apply repeatable ASP logic by size and power bands, the range across publishers becomes explainable and easier to use for planning.

Key Questions Answered in the Report

What is the current size of the construction equipment market?

The market is valued at USD 205.38 billion in 2026 and is projected to reach USD 283.22 billion by 2031.

Which region dominates construction equipment demand today?

Asia Pacific leads with 45.80% revenue share, fueled by large-scale infrastructure pipelines in China, India, and GCC countries.

How fast is battery-electric construction equipment growing?

Battery-electric models are expanding at a 24.3% CAGR, the fastest of all propulsion types, propelled by stricter emission zones and noise ordinances.

Why are rental channels gaining ground in equipment acquisition?

Rental fleets offer contractors capital flexibility, access to the latest technology, and utilization rates that exceed owned equipment.

Which equipment category holds the largest market share?

Earthmoving machinery, including excavators, loaders, and dozers, held 59.10% of the construction equipment market share in 2025.

Page last updated on: