Compact Construction Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

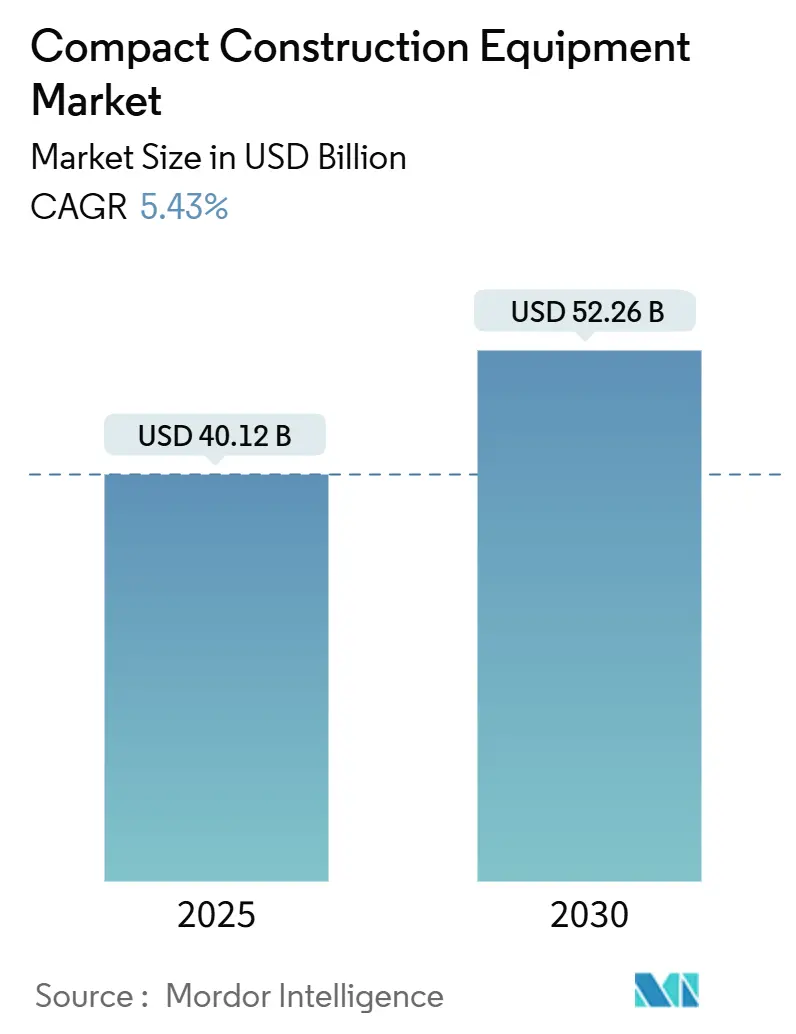

| Market Size (2025) | USD 40.12 Billion |

| Market Size (2030) | USD 52.26 Billion |

| Growth Rate (2025 - 2030) | 5.43% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

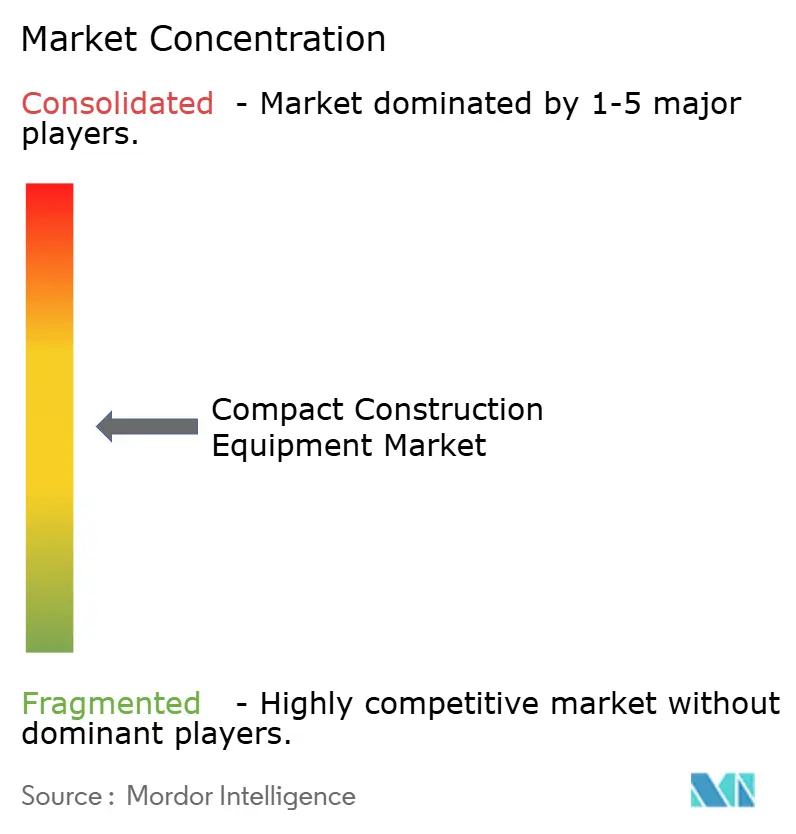

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compact Construction Equipment Market Analysis by Mordor Intelligence

The compact construction equipment market size reached USD 40.12 billion in 2025 and is forecast to attain USD 52.26 billion by 2030, expanding at a 5.43% CAGR over the period. Rising urban‐infill projects favor machines under 13 tons, while emission rules accelerate battery-electric adoption. Strong rental penetration, especially among sub-10-ton fleets, keeps utilization high and shortens refresh cycles. Rapid telematics deployment increases uptime and addresses operator shortages by enabling predictive maintenance. Combined, these forces create steady demand even as traditional heavy-equipment categories mature.

Key Report Takeaways

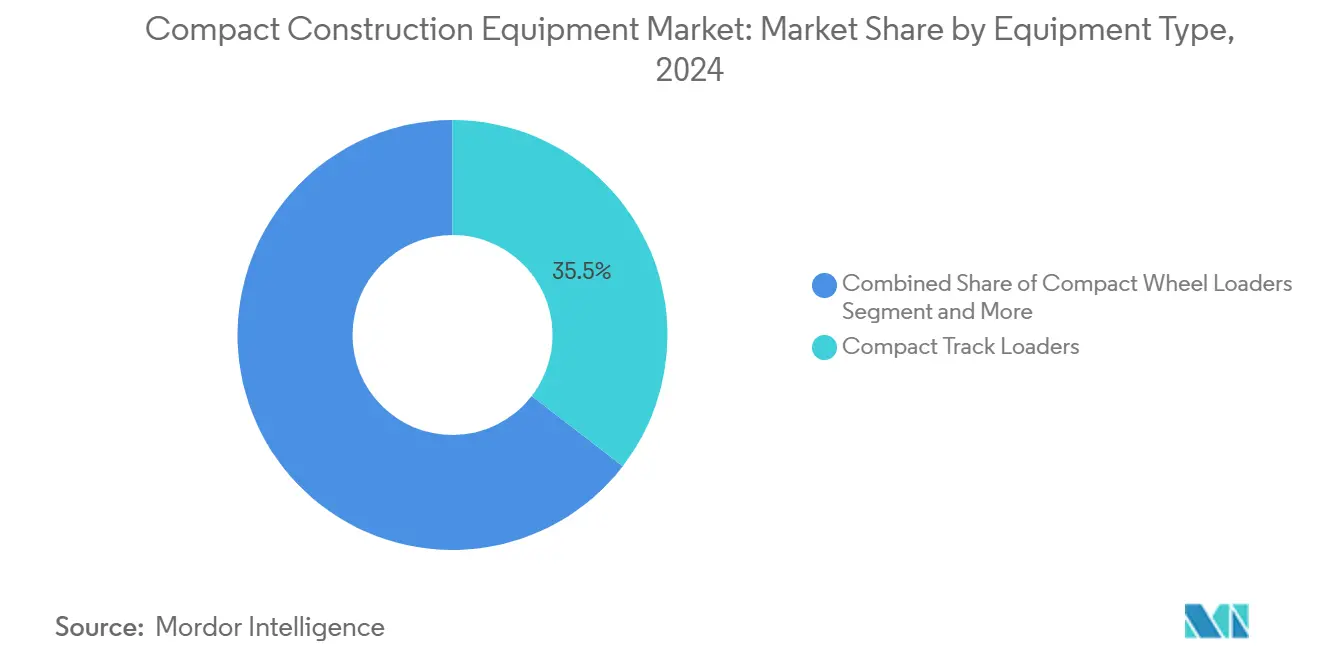

- By equipment type, compact track loaders led with 35.45% of compact construction equipment market share in 2024; compact excavators are projected to grow at a 10.48% CAGR through 2030.

- By operating weight, the 2 to 5 ton class accounted for 47.96% of the compact construction equipment market size in 2024, while the sub-2-ton category is set to advance at a 7.59% CAGR to 2030.

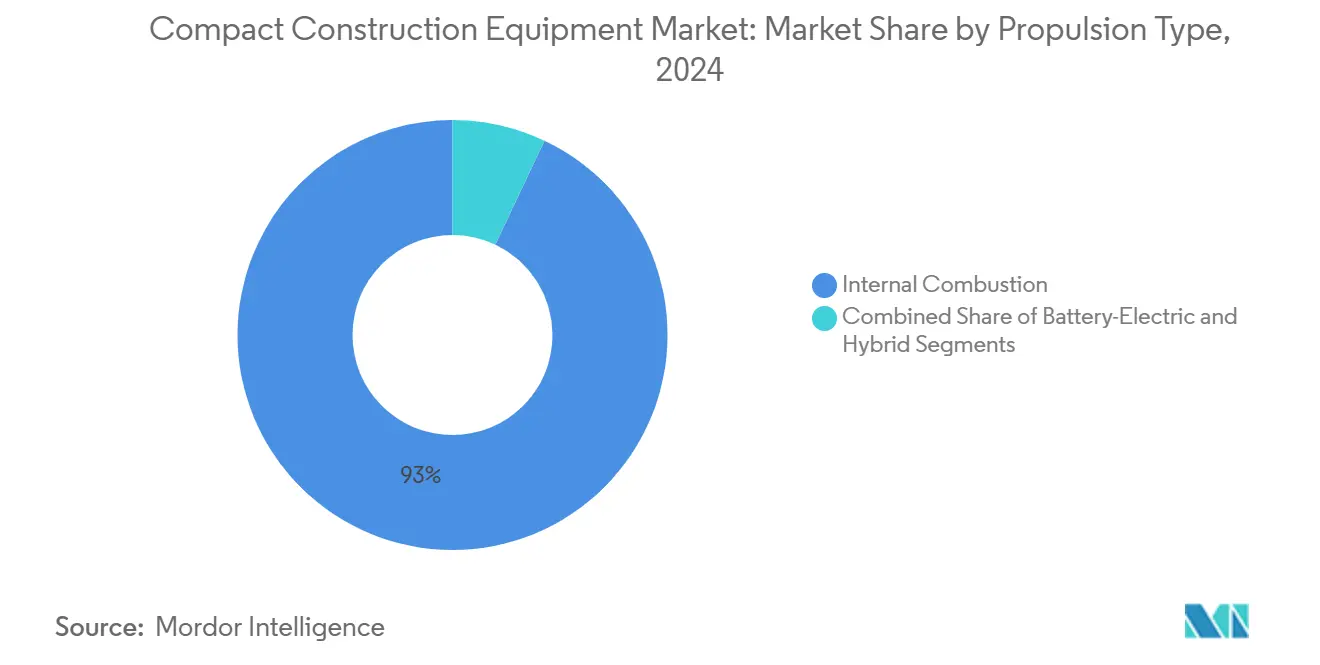

- By propulsion type, internal combustion engines retained 92.96% of the compact construction equipment market size in 2024, but battery-electric units are forecast to surge at a 14.97% CAGR.

- By end-user vertical, residential construction held a 29.19% share of the compact construction equipment market size in 2024; utilities and energy show the fastest growth at a 6.68% CAGR.

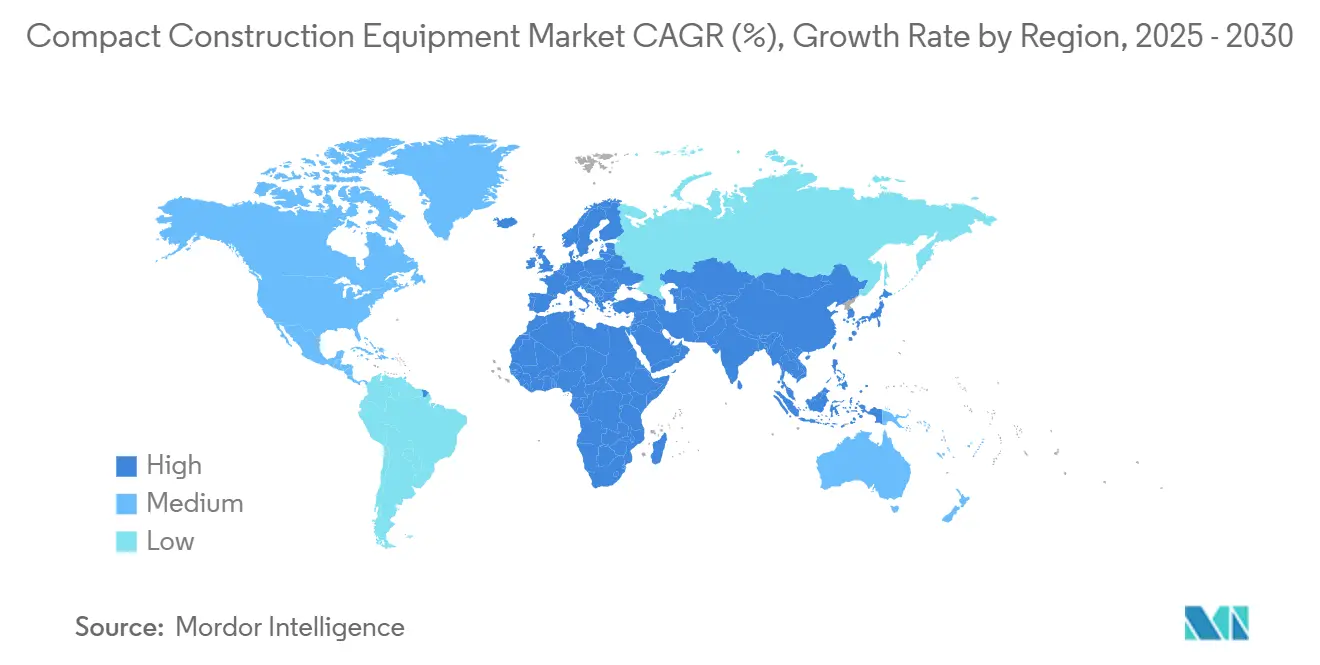

- By geography, North America captured 46.92% market share in 2024, while Europe is projected to be the fastest growing at 6.95% CAGR through 2030.

Global Compact Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urban-Infill Projects | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Adoption of Battery-Electric Machines | +1.1% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Shift to Compact Track Loaders | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Rental Channel Expansion | +0.7% | Global, led by North America | Medium term (2-4 years) |

| AI-Enabled Telematics | +0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Small Renewable-Energy Projects | +0.4% | Global, concentrated in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban-Infill Projects Spurring Compact Equipment Demand

City redevelopment squeezes site footprints, making maneuverability critical. Sub-5-ton excavators and compact track loaders deliver needed precision without exceeding noise limits. Contractors report less downtime because smaller machines navigate tight alleys that restrict larger equipment. Labor shortages heighten the value of multipurpose compact units, allowing a single operator to complete diverse tasks. U.S. builders requires 439,000 additional workers in 2025, reinforcing the move toward productive, smaller machines[1]“ABC projects 439,000 net new construction workers needed in 2025,” Equipment World staff, equipmentworld.com.

Emission-Driven Adoption of Battery-Electric Compact Machines

Stage V rules in Europe and California’s Clean Construction policies impose strict tailpipe limits. Battery-electric excavators now achieve 6-8-hour duty cycles and can fast-charge in under two hours, enabling full-shift operation in urban cores. Singapore funds a major portion of purchase costs for approved electric models, narrowing the price gap[2]“Electric Excavator Subsidy Program,” Singapore Government, gobusiness.gov.sg. Contractors gain nighttime working allowances because electric units cut noise to 70 dB or below.

Contractor Shift to Compact Track Loaders from Skid Steers

Contractors are increasingly choosing compact track loaders over skid steers because of their better stability and reduced ground impact, especially on soft or uneven terrain. This makes them ideal for jobs like landscaping and utility work, where minimizing surface damage is important. Track loaders also handle heavier attachments more effectively, adding to their versatility on site. Quick-change systems make it easier for operators to switch between tasks without delays, improving overall efficiency. The shift reflects a broader trend toward equipment that offers both performance and adaptability in varied conditions.

Expansion of Rental Channels Focused on Sub-10-Ton Machinery

The rental market is increasingly focused on compact equipment, especially sub-10-ton machinery, as contractors look for flexible solutions that match shorter project timelines and specialized tasks. Renting allows access to the latest technology without the financial burden of ownership, making it a practical choice for many firms. Major rental companies are expanding their fleets and geographic reach to meet rising demand, consolidating assets for better efficiency. This shift reflects broader changes in construction economics, where agility and cost control are key. Despite competitive pressure, rental growth remains strong, signaling continued interest in compact equipment solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BEV Cost | -0.9% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Skilled Operator Shortage | -0.5% | Global, acute in North America & Europe | Medium term (2-4 years) |

| LFP Battery Cell Supply Tightness | -0.3% | Global, supply chain concentrated in Asia | Short term (≤ 2 years) |

| Grid-Power Constraints | -0.2% | Global, particularly remote/rural projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Battery-Electric Variants

Battery-electric compact equipment still faces a major adoption hurdle due to its high upfront cost—typically 40–60% more than diesel alternatives. This premium is largely driven by expensive lithium-ion batteries, specialized electronics, and limited production scale. While electric models offer lower operating costs over time, their economic viability depends heavily on usage patterns—urban, high-utilization settings tend to justify the investment faster than rural, low-use scenarios. Case Construction’s 580 EV backhoe loader showcases the potential, but buyers must carefully assess total cost of ownership. Government incentives and financing programs, like Singapore’s 70% subsidy for electric excavators, are key to closing the affordability gap and accelerating adoption.

Shortage of Skilled Compact-Equipment Operators

The construction industry is facing a serious shortage of skilled equipment operators, which is slowing down project timelines and limiting the use of compact machinery. This issue is especially challenging in compact equipment categories, where operators need to be versatile across different machines and attachments, making training more complex. With many experienced operators nearing retirement and few new entrants joining the field, the talent pipeline is shrinking. Rising wages reflect the imbalance between supply and demand, pushing companies to explore automation and remote operation technologies. While solutions like simulation-based training are emerging, adoption is still limited due to cost and user acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Versatility Drives Excavator Upswing

Compact track loaders, retain 35.45% of compact construction equipment market share in 2024 owing to multipurpose attachments and low ground pressure. Compact excavators capture the fastest 10.48% CAGR, fueled by utility trenching and foundation works in dense urban cores. Their tail-swing radius under 5 feet enables street repairs without lane closures. Rental depots prioritize these two categories, accounting for over half of annual compact construction equipment market size turnover. Demand for compact wheel loaders remains steady in aggregate yards and recycling centers, where bucket capacity outweighs digging precision.

Forklifts address vertical material placement on mixed-use developments, a niche yet essential task. Scissor lifts answer height-access needs in building maintenance and fit-outs. Electric variants gain traction first in excavators where duty cycles align with current battery technology. Compact track loaders’ sealed undercarriage design lowers maintenance frequency, a key rental advantage. High-flow hydraulic options support snow-removal blowers and cold-planer attachments, broadening seasonal use.

By Operating Weight: Sub-2-Ton Machines Find City Niches

The 2 to 5 ton band contributes 47.96% to 2024 revenue, reflecting its balance of lift capacity and trailer portability. Contractors move these units between sites with standard pickup trucks, reducing transport fees. Below-2-ton models post a 7.59% CAGR, serving backyard pool digs and basement excavations unreachable by larger gear. Their small footprint meets European road regulations that cap axle loads in historic districts.

Machines weighing 5 to 8 tons tackle deeper utility trenches and small bridge repairs where power margins matter. The 8 to 13 ton class borders mid-size territory but remains inside the compact definition under certain regulatory schemes. Fuel burn rises sharply past 8 tons, prompting interest in hybrid systems that recapture swing energy. Sub-2-ton units often integrate retractable undercarriages to fit through 30-inch doorways, enabling interior demolition tasks.

By Propulsion Type: Electric Momentum Builds

Internal combustion engines generated 92.96% of 2024 value, yet battery-electric units are scaling rapidly at a 14.97% CAGR. Battery-electric propulsion systems are gaining momentum in the construction equipment market, though traditional internal combustion engines still dominate. The growth in electric options is fueled by stricter emissions regulations, falling battery costs, and improvements in energy storage that make electric machines more viable for full-day use. Lithium iron phosphate batteries are becoming the preferred choice due to their safety and durability, although supply chain challenges are causing delays.

Internal combustion engines continue to be favored for demanding applications and remote job sites where charging options are limited. Hybrid systems offer a middle ground, reducing emissions and fuel use without relying entirely on batteries. Charging infrastructure is lagging behind equipment availability, but mobile battery systems are emerging as creative solutions for off-grid locations. Government incentives are helping speed up the transition by making electric equipment more financially accessible.

By End-User Vertical: Residential Construction Drives Demand

Residential construction held a 29.19% market share in 2024, driven by infill and remodeling projects where sub-5-ton excavators and compact track loaders can work within tight setbacks and noise limits. Builders favor quick-attach hydraulics and multi-purpose attachments (augers, trenchers, breakers) to compress task sequences and reduce subcontractor dependencies. Battery-electric minis are gaining share in urban neighborhoods thanks to low emissions and evening/overnight work allowances, while telematics helps small contractors track utilization and preventive maintenance. Rental fleets remain the primary access route for homeowners and small builders, keeping refresh cycles short and ensuring availability across peak seasons.

The utilities and energy sectors, growing at a 6.68% CAGR are quickly becoming key drivers of compact equipment demand, especially for renewable energy projects like solar and wind installations. These jobs often require machines that can operate on sensitive terrain with minimal disruption, making compact, low-impact equipment a preferred choice. Residential construction also continues to be a major market, with compact machines well-suited for tight spaces and smaller-scale projects like accessory dwelling units. The growing emphasis on sustainability and efficient site management is pushing contractors to adopt versatile equipment that meets both environmental and operational needs.

Geography Analysis

North America generated 46.92% of 2024 revenue, supported by residential starts and infrastructure renewal targeting water, power, and broadband networks. Federal funding bolsters demand for sub-5-ton excavators that minimize street disruption. The United States accounts for three-quarters of regional sales, while Canada benefits from resource projects using compact track loaders on soft ground. Mexico’s factory expansions drive forklift and scissor lift adoption, although overall growth lags.

Europe records the fastest 6.95% CAGR to 2030, rebounding from a 2024 dip when mini-excavator sales fell significantly. Emission mandates tighten fleet renewal cycles, boosting electric penetration by 2027. Germany invests in renewable-energy grids, requiring trenching equipment with narrow footprints. The United Kingdom’s urban regeneration schemes specify compact machines to protect heritage buildings. Scandinavia pilots autonomous compact loaders for snow clearance, reflecting labor shortages.

Asia-Pacific shows mixed dynamics. China leads global electric equipment deliveries. Domestic growth steadies but export orders rise as Chinese OEMs target emerging markets with cost-competitive electric minis. India sustains double-digit expansion on metro and highway builds. Japan upgrades aging utilities with low-noise electric excavators suitable for dense neighborhoods. Southeast Asian nations trial battery-swap stations at urban job sites, preparing for wider rollouts.

Competitive Landscape

The compact construction equipment market exhibits moderate fragmentation, indicating substantial white-space opportunities for both market expansion and competitive repositioning. This fragmentation reflects the diverse application requirements across compact equipment categories, where specialized capabilities and regional preferences prevent dominant market consolidation typical in heavy construction equipment segments. Caterpillar leverages parts logistics and dealer coverage to defend share, while Kubota scales European mini-excavator capacity. Chinese entrants such as XCMG expand abroad, offering electric minis at comparatively lower list prices.

Technology alliances shape strategy. HD Hyundai collaborates with robotics firms to field autonomous dig cycles, cutting per-meter excavation costs. Manufacturers are forging partnerships to speed up development timelines and distribute R&D costs across various product platforms, focusing on technology differentiation through electrification, telematics integration, and autonomous capabilities. Rental giants influence specifications, favoring machines with standardized quick couplers to maximize fleet flexibility.

Battery partnerships secure cell supply, a critical advantage during 2025 shortages. White-space opportunities cluster in sub-2-ton electrics, teleoperated skid steers, and AI maintenance dashboards. Start-ups focusing on battery-swap ecosystems attract venture funding, targeting downtime reduction. Established brands counter with integrated chargers and predictive analytics. The race to embed autonomous capabilities in compact machines accelerates as labor scarcity persists.

Compact Construction Equipment Industry Leaders

Caterpillar Inc.

Yanmar Compact Equipment

Doosan Bobcat

CNH Industrial

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Yanmar Compact Equipment released four new construction-grade models with 360° visibility and auto two-speed.

- April 2025: CASE Construction Equipment introduced an electric compact wheel loader alongside upgrades to track loaders and skid steers.

- April 2025: Hyundai Construction Equipment Europe unveiled its first electric mini excavator plus new skid steer and tracked loader models.

- December 2024: Kubota announced a 40% expansion of European mini-excavator capacity by 2028.

Global Compact Construction Equipment Market Report Scope

| Compact Excavators |

| Compact Wheel Loaders |

| Compact Track Loaders |

| Forklifts |

| Aerial Work Platforms – Scissor Lifts |

| Other Equipment Types |

| Below 2 Ton |

| 2 to 5 Ton |

| 5 to 8 Ton |

| 8 to 13 Ton |

| Internal Combustion Engine |

| Battery-Electric (Li-ion) |

| Hybrid Electric |

| Residential Construction |

| Commercial Construction |

| Industrial Facilities and Plants |

| Infrastructure Development |

| Utilities and Energy |

| Landscaping and Agriculture |

| Other End-User Verticals |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Compact Excavators | |

| Compact Wheel Loaders | ||

| Compact Track Loaders | ||

| Forklifts | ||

| Aerial Work Platforms – Scissor Lifts | ||

| Other Equipment Types | ||

| By Operating Weight | Below 2 Ton | |

| 2 to 5 Ton | ||

| 5 to 8 Ton | ||

| 8 to 13 Ton | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery-Electric (Li-ion) | ||

| Hybrid Electric | ||

| By End-User Vertical | Residential Construction | |

| Commercial Construction | ||

| Industrial Facilities and Plants | ||

| Infrastructure Development | ||

| Utilities and Energy | ||

| Landscaping and Agriculture | ||

| Other End-User Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the compact construction equipment market in 2025?

The compact construction equipment market size reached USD 40.12 billion in 2025.

What CAGR is forecast for compact equipment through 2030?

The market is projected to expand at a 5.43% CAGR between 2025 and 2030.

Which equipment type is growing fastest?

Compact excavators are set to grow at a 10.48% CAGR as urban utility work rises.

Which propulsion technology shows the highest growth?

Battery-electric models lead with a 14.97% CAGR, driven by emission regulations.

Which region is expanding most rapidly?

Europe posts the fastest 6.95% CAGR owing to strict emission rules and urban densification.

Page last updated on: