Vietnam Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

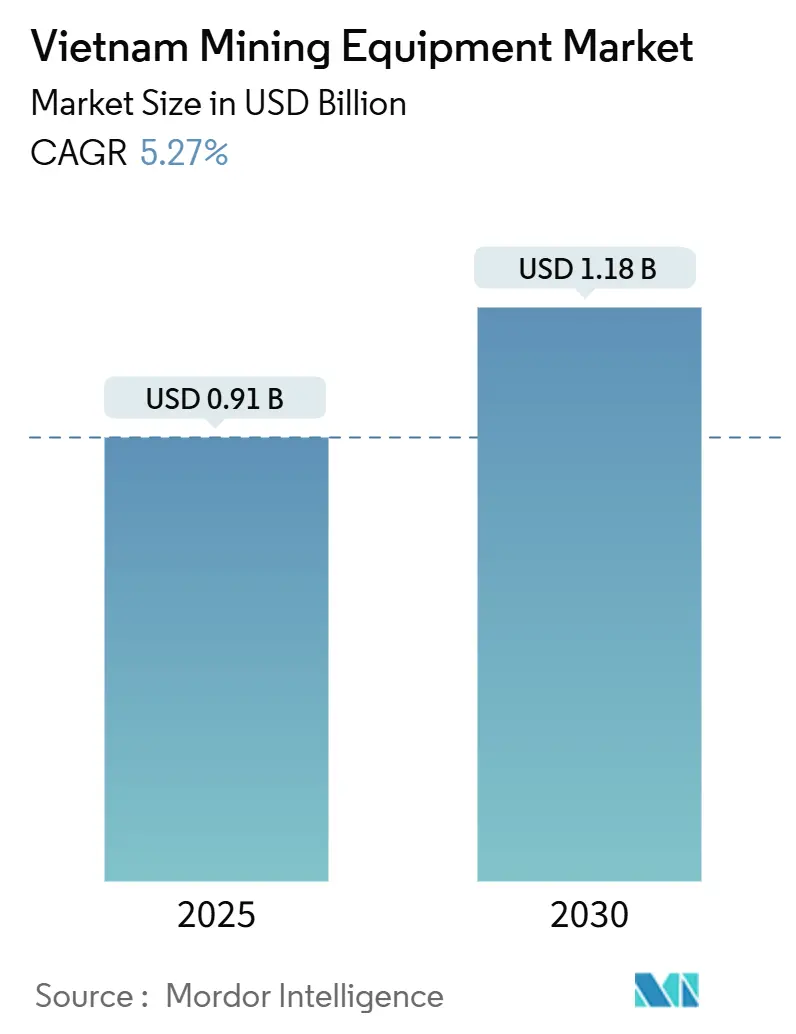

| Market Size (2025) | USD 0.91 Billion |

| Market Size (2030) | USD 1.18 Billion |

| Growth Rate (2025 - 2030) | 5.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Mining Equipment Market Analysis by Mordor Intelligence

The Vietnam mining equipment market size was USD 0.91 billion in 2025 and is projected to reach USD 1.18 billion by 2030, representing a 5.27% CAGR during the forecast period. Vietnam’s mining equipment market is gaining momentum, driven by robust infrastructure investment, extensive reserves of rare earths and bauxite, and increasing foreign direct investment. Electrification and automation are advancing due to environmental regulations and the expansion of service networks. However, growth is tempered by metal price volatility, grid limitations in remote areas, and a shortage of skilled automation talent. Technology providers offering integrated digital solutions, clean-power drivetrains, and comprehensive service packages are well-positioned to capitalize on emerging opportunities as the market transitions toward higher-value, lower-emission operations.

Key Report Takeaways

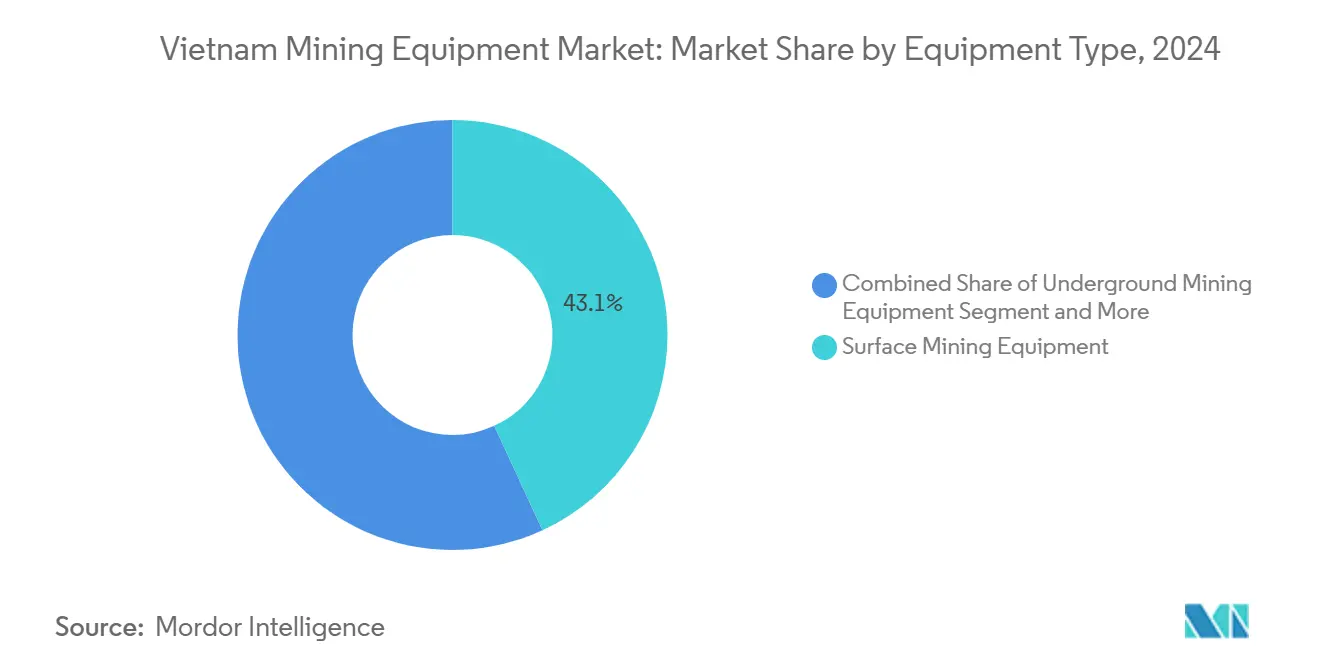

- By equipment type, Surface Mining Equipment led with 43.13% Vietnam mining equipment market share in 2024; Mineral Processing Equipment is forecast to expand at a 7.79% CAGR through 2030.

- By automation level, Manual Equipment accounted for 64.11% of the Vietnam mining equipment market size in 2024, while Fully Autonomous Equipment is projected to post an 8.14% CAGR to 2030.

- By powertrain, Internal Combustion Engine rigs retained 77.29% share of the Vietnam mining equipment market size in 2024; Battery-Electric Vehicles represent the fastest trajectory at a 9.21% CAGR to 2030.

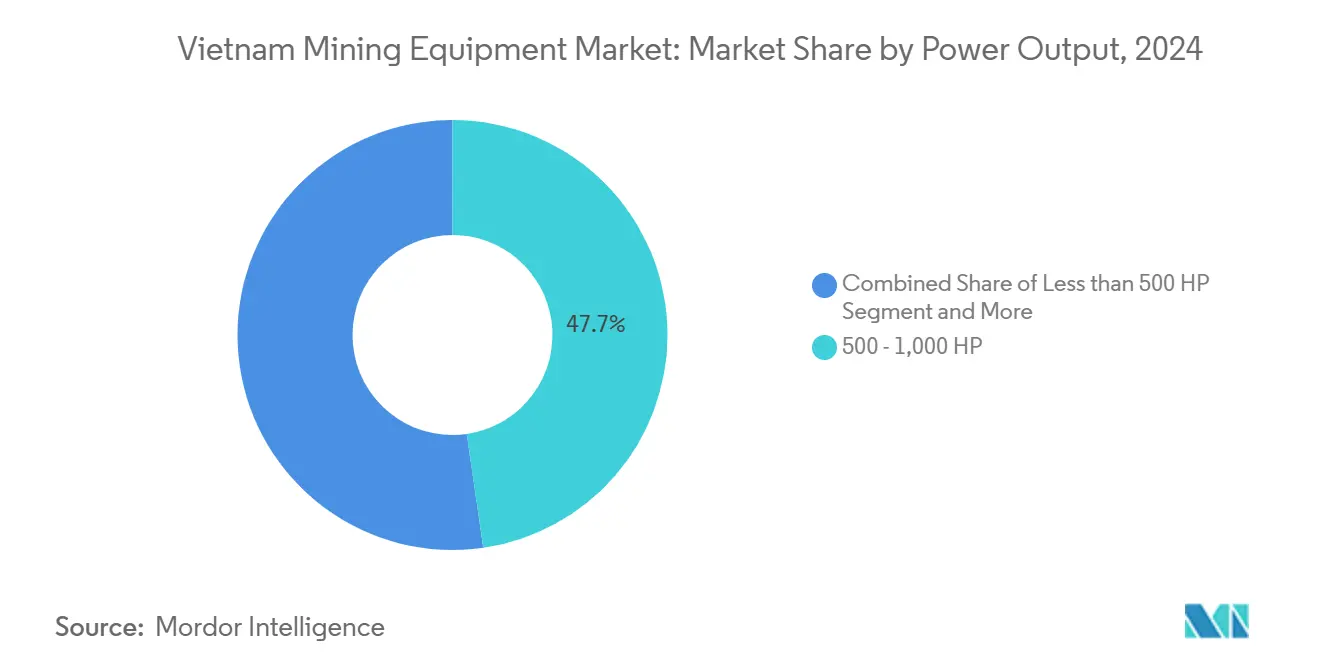

- By power output, the 500-1,000 HP class commanded 47.71% Vietnam mining equipment market share in 2024; equipment below 500 HP is on track to grow at a 7.61% CAGR over the outlook period.

- By application, Metal Mining captured 49.82% of the Vietnam mining equipment market size in 2024; Mineral Mining is set to rise at a 8.72% CAGR between 2025-2030.

Vietnam Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New Bauxite and Rare-Earth Projects | +1.2% | Dak Nong and Lam Dong provinces | Medium term (2-4 years) |

| Infrastructure Spending Surge | +0.9% | Nationwide, priority north & central | Short term (≤ 2 years) |

| Rising Foreign Investment | +0.8% | Mineral-rich provinces nationwide | Medium term (2-4 years) |

| OEM After-Sales Expansion | +0.6% | Urban and industrial zones | Short term (≤ 2 years) |

| Stricter Dust and Noise Norms | +0.5% | Nationwide | Medium term (2-4 years) |

| AI-Driven Fleet Optimization | +0.4% | Large-scale operations nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Pipeline of New Bauxite and Rare-Earth Projects

In Dak Nong and Lam Dong, a USD 8 billion investment in bauxite development has sped up the procurement of large excavators, 90-tonne haul trucks, and high-throughput crushers essential for open-pit operations[1]“Bauxite Development Master Plan 2025,” Vietnam Ministry of Natural Resources and Environment, monre.gov.vn. Flagship projects such as Tan Rai and Dong Pao demand integrated beneficiation plants, tilting the Vietnam mining equipment market toward sophisticated mineral processing systems. Clustered project geography enables equipment owners to pool maintenance resources, lowering the total cost of ownership and boosting supplier service density. The long reserve life of these deposits ensures recurring aftermarket parts revenue for OEMs throughout the asset cycle. Suppliers offering modular, easily relocatable processing lines gain a competitive edge as operators seek flexibility to match the evolving nature of ore bodies.

Growing Foreign Direct Investment Inflows into Mining

Revisions to Vietnam’s Investment Law shortened permit cycles and lifted foreign ownership caps, raising mining FDI to its highest level since 2024[2]“FDI Statistics 2024,” Vietnam Foreign Investment Agency, fia.gov.vn. Overseas operators bring stringent EHS standards that necessitate automated drilling rigs, digital fleet management systems, and dust suppression packages, thereby pivoting equipment orders toward premium specifications. Cross-border joint ventures accelerate technology transfer in autonomous haulage and machine-learning predictive maintenance platforms, moving the Vietnam mining equipment market toward Industry 4.0 maturity. International financing terms often bundle equipment lease-backs, lowering cap-ex hurdles for local partners while locking suppliers into long-haul parts contracts. Elevated import volumes of advanced rigs are spurring domestic component supply chains for hydraulic cylinders and battery packs, further embedding global OEMs in Vietnam’s industrial ecosystem.

Stricter Dust and Noise Norms Spurring Equipment Upgrades

The Law on Geology and Minerals effective July 2025 imposes lower particulate and decibel ceilings, compelling miners to retrofit enclosed-cab haul trucks and integrate fog-cannon dust suppression on crushers. Compliance windows coincide with planned mid-life overhauls for many fleets, prompting a wave of replacement purchases arching through 2026-2027. Suppliers with emission-certified engines and low-noise hydraulic systems capture premium pricing as operators race to meet audits. Environmental certification now acts as a pre-qualification gate in state mineral auctions, steering demand toward electric and hybrid drivetrains. Equipment that supports real-time emissions monitoring further differentiates bids, embedding telemetry modules across new deliveries. Aggregate impact is a structural upgrade cycle that raises the technology baseline of the Vietnam mining equipment market.

AI-Enabled Fleet Optimization Raises Productivity

Large-scale operations adopting AI algorithms report utilization upticks by optimizing dispatch, loading, and idle time metrics [3]“Digital Solutions Portfolio White Paper,” Epiroc, epiroc.com. Integration of 5G connectivity enables sub-second data links between loaders and trucks, supporting collision avoidance and real-time grade control. Pilot projects demonstrate positive ROI within 18 months, catalyzing board-level approval for phased automation rollouts among tier-one mines. Vendors supplying open-architecture platforms gain favor as operators seek to future-proof their systems against rapid advancements in sensor technology. Yet, limited technical talent constrains penetration to financially strong producers capable of funding training programs. Over the long term, AI functionality is expected to embed across mid-tier fleets, widening the addressable Vietnam mining equipment market for digital solutions

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coal and Metal Price Volatility | -0.8% | Nationwide | Short term (≤ 2 years) |

| Delays in Licensing and Land Access | -0.6% | Province-dependent | Medium term (2-4 years) |

| Weak Mine-Power Infrastructure | -0.5% | Northern & central highlands | Long term (≥ 4 years) |

| Talent Shortage in Autonomous Ops | -0.3% | High-tech mines nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Coal and Metal Commodity Prices

The World Bank expects metals to retreat 10% in 2025, squeezing cash flows and delaying cap-ex approvals for large crushers and autonomous haulers[4]“Commodity Markets Outlook 2025,” World Bank, worldbank.org. Price-sensitive Vietnamese operators are pivoting to life extension over replacement, elevating demand for rebuild kits but deferring new-build orders. Funding institutions tighten lending terms when prices soften, raising hurdle rates for marginal projects. Fluctuations particularly impact high-capital segments where payback stretches beyond typical commodity cycles. Suppliers mitigate the impact by expanding their rental fleets, offering customers flexibility until prices stabilize.

Underdeveloped Mine-Power Infrastructure in Remote Regions

Rolling blackouts expose the fragility of regional grids, forcing mines to lean on diesel gensets that raise operating costs and limit the adoption of battery-electric rigs. Weak transmission also restricts the deployment of real-time data platforms that require stable connectivity. Capital-intensive grid extensions often lag mining project timelines, compelling investors to self-fund micro-grids. Inadequate power curbs the economics of high-horsepower electric crushers and conveyors, slowing electrification in the Vietnamese mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Operations Drive Market Leadership

Surface Mining Equipment captured 43.13% of the Vietnam mining equipment market share in 2024 due to expansive open-pit bauxite plateaus and rare-earth orebodies. Large hydraulic excavators, 90-tonne rigid-frame trucks, and dozers dominate cap-ex budgets as miners target shallow ore seams that favor strip mining. Vendors report backlog strength for 350-tonne class excavators calibrated for Vietnam’s abrasive laterite soils. Meanwhile, Mineral Processing Equipment is advancing at a 7.79% CAGR through 2030, illustrating operator intent to move downstream into alumina refining and mixed rare-earth carbonate production. This switch increases the demand for modular crushing, screening, and flotation circuits that comply with tighter dust control regulations. Underground equipment maintains a foothold in northern coal seams but contributes modest volumes. Across categories, digital control retrofits are rising as fleets integrate data analytics for preventive maintenance.

Investment momentum in processing lines has repositioned suppliers of high-pressure grinding rolls and vertical mills as strategic partners in the Vietnam mining equipment market. Epiroc’s SmartROC D65 battery drill showcased at MINExpo 2024 signals a trend toward zero-emission surface rigs suited for Vietnamese environmental rules. Crushing-screening units also find application in the booming construction aggregates business, forging linkages between mining and infrastructure segments. Consequently, product-portfolio breadth has become a key tender criterion, favoring OEMs capable of supplying both primary extraction and downstream processing solutions.

By Automation Level: Manual Systems Persist Despite Autonomous Advances

Manual rigs constituted 64.11% of the Vietnam mining equipment market size in 2024, reflecting entrenched operator familiarity and lower upfront investment. Semi-autonomous technologies such as remote-controlled drilling robots provide incremental productivity without displacing cab operators, appealing to mines where skills upgrading is underway. Fully Autonomous units, though only a minority, are scaling at 8.14% CAGR as flagship bauxite projects pioneer 24/7 operations. Komatsu’s battery-electric WX04B LHD integrates advanced tele-operation, illustrating the convergence of automation and electrification. Adoption pacing hinges on connectivity infrastructure and cybersecurity readiness across remote sites.

In an effort to bridge the talent gap, OEMs have established simulator-based training centers in Hanoi and Ho Chi Minh City, accelerating the upskilling of autonomous dispatch supervisors. Mines are rolling out autonomy in remote zones, aiming to reduce risks associated with human-machine interactions. Thanks to government incentives from digital-transformation programs, pilot deployments receive partial subsidies, spurring further demand. Looking ahead, as the costs of LiDAR, radar, and onboard computing decrease, the forecasted deepening of automation penetration will broaden its applications from just haulage to include drilling and blasting.

By Powertrain Type: Electrification Accelerates Despite ICE Dominance

Despite commanding 77.29% share of the Vietnam mining equipment market in 2024, Internal Combustion Engine fleets face rising total cost of ownership as diesel prices trend upward and emission fees tighten. Battery-electric vehicles, which are growing at a 9.21% CAGR, reflect policy drivers and operational savings in underground mines, where ventilation costs decrease significantly when diesel fumes are eliminated. Hybrid drive-trains provide interim solutions for surface mines with irregular duty cycles, leveraging regenerative braking to shave fuel burn. Vale’s successful trials of 72-ton fully electric trucks offer proof points to Vietnamese miners evaluating high-payload electric vehicles.

Broad adoption, however, relies on the availability of charging infrastructure. Power-as-a-Service models are emerging, wherein utilities co-invest in fast-charging depots near pits, thereby de-risking capital expenditures for mine owners. Battery leasing schemes further lower barriers, bundling maintenance and end-of-life recycling. As gigafactories scale across Southeast Asia, localization of lithium-iron-phosphate packs is expected to compress unit costs, widening the TAM for electrified solutions within the Vietnam mining equipment market.

By Power Output: Mid-Range Equipment Dominates Operational Requirements

Units rated 500-1,000 HP delivered 47.71% of the Vietnam mining equipment market share in 2024, balancing productivity with maneuverability on bench widths typical of Vietnamese bauxite plateaus. OEM road-maps emphasize modular powertrains that allow the same chassis to host diesel, hybrid, or full-battery configurations within this horsepower band. Equipment below 500 HP is expected to grow at a 7.61% CAGR through 2030, driven by rising small-mine licenses and ancillary applications, such as pit maintenance and tailings re-handling. Above-1,000 HP machines remain confined to mega-quarries and face slow uptake given high capital thresholds and logistical challenges on narrower access roads.

Suppliers are integrating high-efficiency electric drivetrains even in sub-500 HP loaders, aligning with the regulatory push for emission reduction. Sensor suites standardizing in mid-range classes offer regression-based engine tuning to cut fuel consumption, demonstrating incremental gains short of complete electrification. Hence, power-output segmentation is increasingly a function of mine layout and haul-distance economics rather than purely ore hardness metrics.

By Application: Metal Mining Leads Diversified Demand Portfolio

Metal Mining accounted for 49.82% of the Vietnam mining equipment market share in 2024, reflecting robust investment in copper, gold, and, notably, rare-earth extraction, each of which requires precise, high-yield concentrator lines. Mineral Mining—covering bauxite, limestone, and industrial sands—is forecast at 8.72% CAGR through 2030, sustained by alumina demand and civil-works aggregates. Coal Mining, while historically dominant, is plateauing as Vietnam’s energy mix transitions toward renewables, although underground safety upgrades still drive niche orders for gas-monitoring and roof-bolting equipment.

The discovery of 40 new gold prospects, totaling 30 tonnes, sparks fresh demand for cyanide-free leaching technology and enclosed ball mills that mitigate dust exposure. Meanwhile, rare-earth processing plants require solvent-extraction mixers and high-gradient magnetic separators, creating a white space for specialized OEM entrants. The diversified application mix cushions the Vietnam mining equipment market against volatility in any single commodity, encouraging vendors to develop cross-commodity platforms that are adaptable via quick-change attachments and software presets.

Geography Analysis

Vietnam constitutes a single-country focus but exhibits pronounced regional disparities shaping procurement patterns. Northern border provinces leverage mature rail and road grids linking to Chinese supply chains, enabling rapid spares replenishment and facilitating cross-border equipment leasing. Central highlands, home to rich bauxite seams, confront steeper logistics costs given mountainous terrain and sparse power transmission; OEMs respond with mobile service caravans and genset-integrated charging pods, sustaining fleet reliability. Southern industrial corridors around Ho Chi Minh City benefit from deep-water ports that streamline imports of oversize haul trucks and crushers.

Nationally, implementation of the Law on Geology and Minerals since July 2025 harmonizes licensing yet allows provinces discretion over environmental audits, generating localized compliance niches. Provinces accelerating infrastructure buildouts attract higher concentrations of mobile crushers and screening units for aggregate production, swelling service footprints in those clusters. Conversely, remote rare-earth concessions often necessitate initial helicopter transport for surveying drills, later transitioning to all-terrain carriers once access roads mature.

Supply-chain resilience improved after the government fast-tracked customs digitalization, slashing clearance times and reducing demurrage charges on imported excavators. However, grid reliability remains uneven; frequent blackouts in Dak Nong led fleet managers to retain diesel redundancy even when piloting battery-electric haul trucks. This patchwork grid dynamic underscores why hybrid solutions maintain relevance despite policy preference for zero-emission rigs. Mastering provincial idiosyncrasies—from labor regulations to tax incentives—defines competitive success in the Vietnam mining equipment market.

Competitive Landscape

The Vietnam mining equipment market is moderately fragmented, yet high-technology subsegments display emerging consolidation. Global majors—Caterpillar, Komatsu, and Epiroc—leverage R&D heft and embedded telematics platforms to sustain pricing power. Their nationwide service hubs and financing arms foster stickiness among tier-one miners that prioritize reliability and lifecycle costing.

Domestic champion Deo Ca Group dominates tunneling equipment share and significant order book, benefiting from in-house manufacturing and deep relationships with local EPC contractors. Technology partnerships are proliferating; Builder X Robotics retrofits AI control kits onto legacy fleets, enabling cost-constrained miners to leapfrog into semi-autonomy without wholesale fleet replacement.

Aftermarket services form the new battleground as OEMs chase recurring revenue. Weichai Vietnam’s dense depot network reduces mean-time-to-repair, eroding gray-market parts sales and fortifying brand loyalty. Finance plus service bundles—combining lease, maintenance, and battery leasing—are gaining traction among mid-tier operators prioritizing cash-flow flexibility. Suppliers able to integrate equipment, software, and services into cohesive solutions are best placed to fortify market share as the Vietnam mining equipment market advances toward value-driven procurement models.

Vietnam Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Epiroc AB

Sandvik AB

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Epiroc has introduced its latest electric-driven drills: the Pit Viper 271 XC E, Pit Viper 275 XC E, and Pit Viper 291 E. These drills, part of Epiroc's Smart and Green Series, deliver the same innovative performance while ensuring zero exhaust emissions, no fuel consumption, and a reduced carbon footprint.

- August 2025: Vietnam and Australia have strengthened their cooperation in rare mineral management. The mission focused on three key objectives: enhancing the Vietnam-Australia partnership, improving the skills of Vietnamese officials in policy-making, planning, and mining operations, and sharing expertise in managing geological resources, particularly strategic minerals.

Vietnam Mining Equipment Market Report Scope

The Vietnam Mining Equipment Market Report is Segmented by Equipment Type (Surface Mining Equipment, Underground Mining Equipment, and More), Automation Level (Manual Equipment, and More), Powertrain Type (Internal Combustion Engine Vehicles, and More), Power Output (Less Than 500 HP, and More), and Application (Metal Mining, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders & Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

How large is the Vietnam mining equipment market in 2025?

The Vietnam mining equipment market size is USD 0.91 billion in 2025.

What is the expected growth rate for mining equipment demand in Vietnam?

Mining Equipment demand is projected to rise at a 5.27% CAGR through 2030.

Which equipment category leads spending within Vietnam?

Surface Mining Equipment leads, accounting for 43.13% market share in 2024.

Why is electrification gaining traction in Vietnamese mines?

Stricter environmental rules effective July 2025 and lower underground ventilation costs are accelerating battery-electric equipment uptake.

What limits faster adoption of fully autonomous mining fleets?

Limited technical workforce and inconsistent connectivity infrastructure constrain widespread deployment of fully autonomous equipment.

Page last updated on: