United States Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

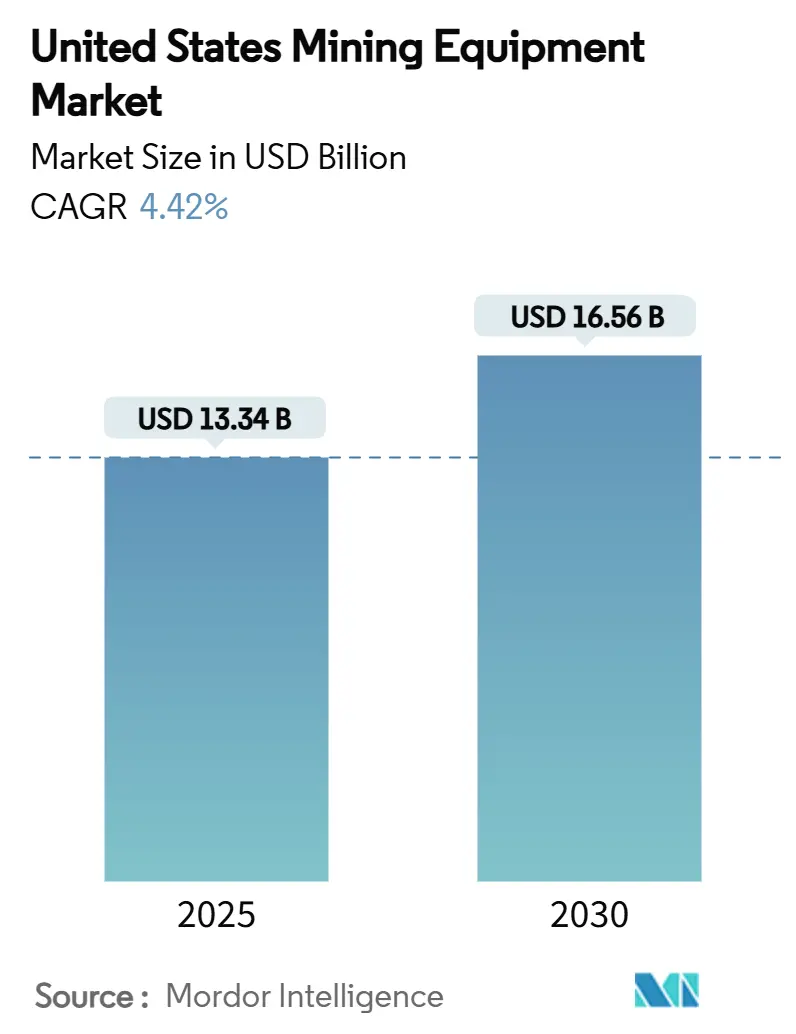

| Market Size (2025) | USD 13.34 Billion |

| Market Size (2030) | USD 16.56 Billion |

| Growth Rate (2025 - 2030) | 4.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Mining Equipment Market Analysis by Mordor Intelligence

The United States mining equipment market size stands at USD 13.34 billion in 2025 and is projected to reach USD 16.56 billion by 2030, advancing at a 4.42% CAGR. Together, federal infrastructure funding, fast-moving fleet-replacement cycles, and an accelerated pivot toward electrification and automation give the United States mining equipment market its forward momentum. Construction megaprojects seeded by the Infrastructure Investment and Jobs Act continue to draw vast quantities of aggregates and industrial minerals, prompting equipment orders that keep factory backlogs full. At the same time, operators confronting ventilation mandates in underground mines are embracing battery-electric vehicles that trim energy costs and curb emissions. Moderate but stable commodity prices encourage disciplined capital outlays, while talent shortages push mines to deploy autonomy and remote-operation platforms.

Key Report Takeaways

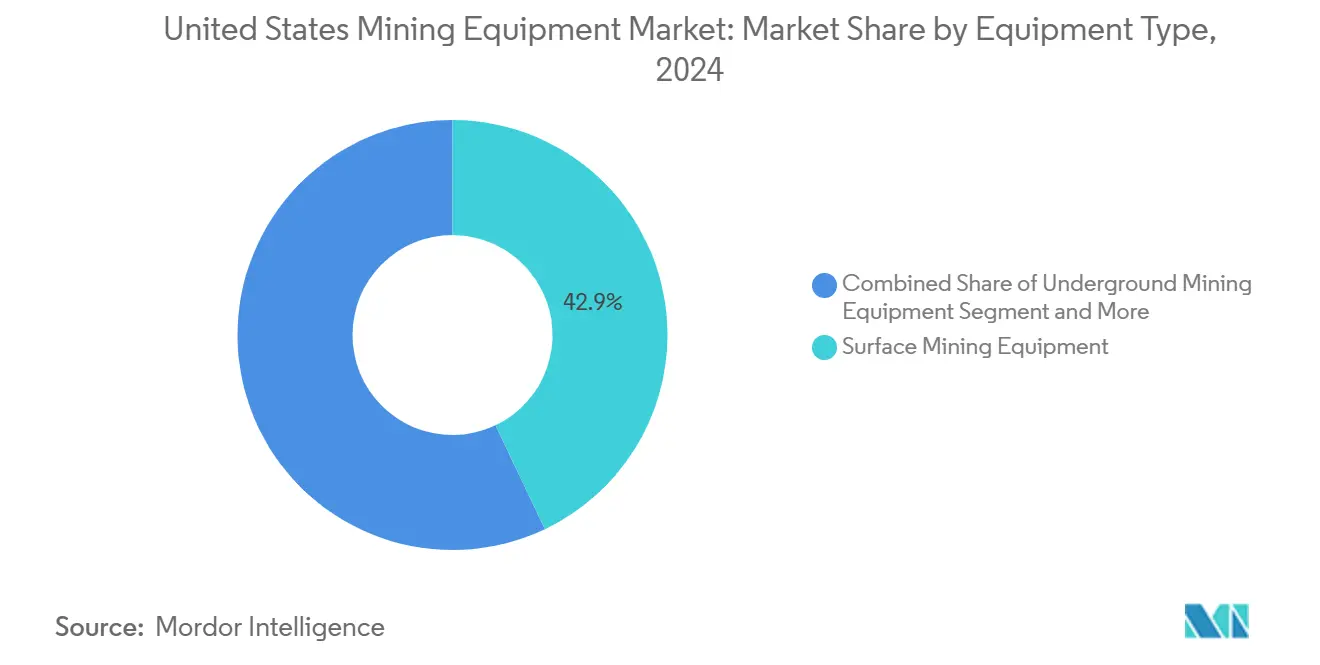

- By equipment type, surface mining equipment led with 42.93% revenue share of the United States mining equipment market in 2024; underground mining equipment is forecast to grow at a 10.11% CAGR through 2030.

- By power source, gasoline-powered machines accounted for a 65.97% revenue share of the United States mining equipment market in 2024, whereas electric equipment is set to accelerate at an 11.23% CAGR to 2030.

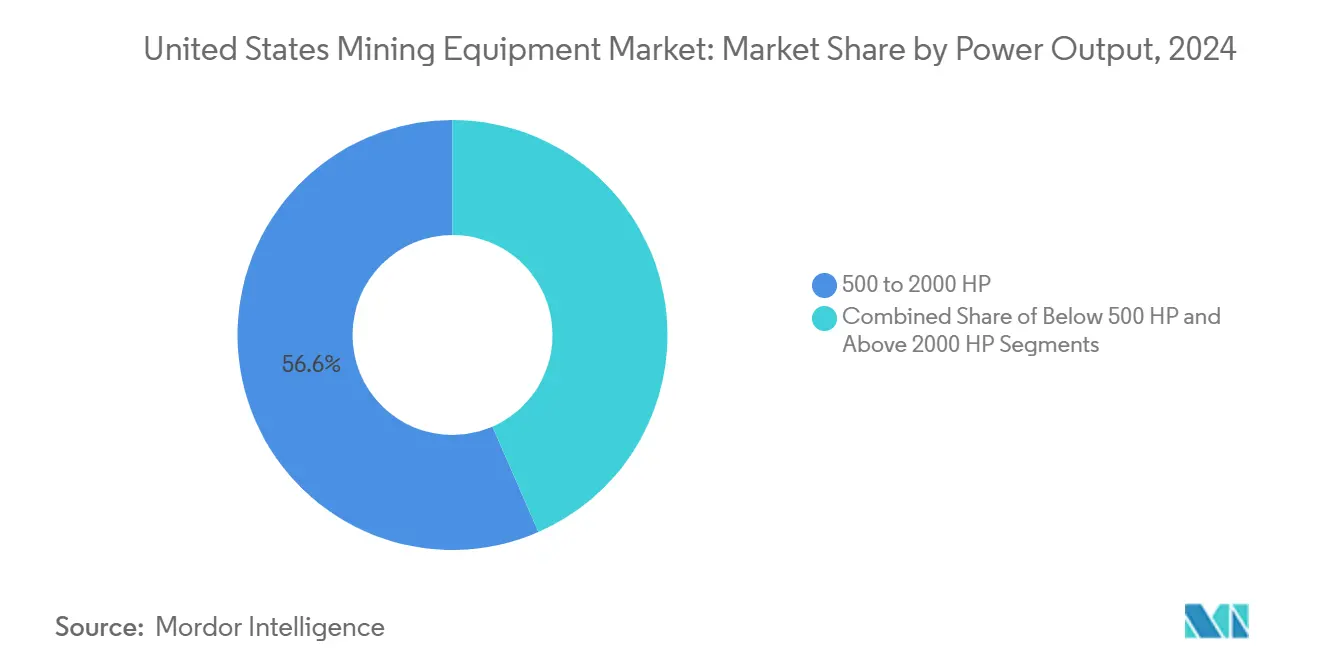

- By power output, the 500-2,000 HP band captured 56.55% revenue share of the United States mining equipment market in 2024, while below-500 HP machines are expected to expand at an 8.75% CAGR through 2030.

- By application, metal mining secured 47.12% revenue share of the United States mining equipment market in 2024 and is advancing at a 10.23% CAGR to 2030.

United States Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Infrastructure-Spending Boom | +1.2% | Western States, Appalachian Region, Texas | Medium term (2-4 years) |

| Ageing Fleet Replacement Cycle | +0.9% | Nevada, Arizona, Wyoming, Colorado | Long term (≥ 4 years) |

| Battery-Electric Equipment Shift | +0.8% | California, Nevada, Western Mining States | Medium term (2-4 years) |

| Critical-Minerals Projects Surge | +0.7% | Nevada, Wyoming, Texas, Rocky Mountain States | Long term (≥ 4 years) |

| Deep-Underground Mines Automation | +0.5% | Appalachian Region, Western Underground Operations | Medium term (2-4 years) |

| New Tax Incentives | +0.3% | National, Early Adoption In California, Nevada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure-Spending Boom

Congressional funding has released a wave of more than 60,000 transportation projects, pushing public-highway construction outlays significantly in 2024 and intensifying demand for aggregates, crushed stone, and industrial minerals. Mines located near road and rail corridors are scaling up fleet capacity to meet downstream material needs. Semiconductor fabrication plants and battery factories emerging under CHIPS and Inflation Reduction Act incentives require specialty quarried inputs, creating consistent pull-through for loaders, crushers, and screening systems. The multi-year pipeline gives manufacturers clear visibility that underpins investment in new assembly lines and digital platforms that enhance uptime.

Robust Replacement Cycle for Ageing Fleets

Deferred capital spending between 2015 and 2020 pushed the median economic life of haul trucks, drills, and excavators past optimal replacement thresholds, raising maintenance costs and compromising safety. With commodity prices now supportive and service-life economics deteriorating, fleet managers are retiring older assets and ordering next-generation units featuring fuel-optimization software and predictive-maintenance sensors. Haul-truck utilization exceeds 85%, yet unplanned downtime can consume 40–60% of ownership cost, making replacement the financially prudent option.

Shift To Battery-Electric Mobile Equipment

Battery-electric haul trucks deliver up to 65% lower operating costs per tonne than diesel peers, aided by regenerative braking and fewer moving parts. Underground mines champion the transition because eliminating diesel particulates slashes ventilation energy requirements by roughly 50% and improves worker safety. Charging-infrastructure outlays, once viewed as burdensome, are declining as high-capacity fast-charge and automated-swap systems mature. OEMs speed commercialization: Caterpillar’s automated energy-transfer platforms cut idle time and boost productivity.

Surge In Critical-Minerals Projects (Lithium, REE)

Large-scale lithium developments such as Thacker Pass (80,000 t lithium carbonate per year) and Rhyolite Ridge are driving demand for high-capacity loaders, dozers, and mobile crushers capable of handling abrasive clays. Rare-earth projects like Round Top in Texas require specialized materials-handling equipment that tolerates corrosive leach residues. OEMs respond with corrosion-resistant steel grades and sealed electrical harnesses tailored to harsh process environments. Regional clustering of these projects concentrates aftermarket services in Nevada, Wyoming, and Texas, prompting parts-distribution hubs and remote-diagnostics centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Metal-Price Cycles | -0.8% | National, Concentrated In Metal Mining States | Short term (≤ 2 years) |

| High CAPEX For Electric Equipment | -0.6% | Western States, Early Adoption Regions | Medium term (2-4 years) |

| Green-Field U.S. Mines Permit Delays | -0.4% | Western States, Federal Land Jurisdictions | Long term (≥ 4 years) |

| Skilled-Labor Shortages | -0.3% | National, Acute In Remote Mining Regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Metal-Price Cycles

Metal price volatility poses significant challenges to mining equipment investment decisions. Base metals have experienced dramatic price swings, largely influenced by macroeconomic factors such as U.S. Federal Reserve interest rate policies and fluctuations in the Chinese economy. These conditions directly affect the timing of equipment procurement, as mining companies often delay purchases and extend the service life of existing fleets to manage financial risk. This trend is reflected in the decline of the Producer Price Index for Total Mining Industries, which fell from 216.486 in April 2025 to 208.052 in May 2025, indicating broader commodity price pressures[1]"Producer Price Index by Industry: Total Mining Industries", FRED, fred.stlouisfed.org. Additionally, Chinese market manipulation and oversupply, particularly in nickel production through investments in Indonesia, have distorted prices, undermining investment confidence and leading to mine closures in higher-cost regions.

High Upfront CAPEX For Electrified Equipment

The transition to electrified mining equipment also faces significant barriers due to high upfront capital expenditures. Electrified equipment typically costs 15–25% more than diesel alternatives, despite offering lower operational costs and better performance in certain applications. For example, electric wheel loaders carry substantial price premiums and higher monthly ownership costs, which often offset fuel savings, creating financial hurdles for contractors and operators with limited capital budgets. Evaluating the total cost of ownership for electric equipment is complex, involving considerations such as charging infrastructure, battery replacement costs, and operational duty cycles, areas where many mining companies lack the necessary expertise. Battery technology, while improving, still accounts for 30–40% of the purchase price, and its replacement adds long-term financial commitments, creating acute challenges for smaller mining operations and contractors who lack the financial strength to absorb the higher initial costs, even when long-term operational savings justify the investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Underground Segment Gains Speed

The United States mining equipment market size for underground machinery is poised to outpace surface-equipment growth yet still trails the latter’s 42.93% revenue share. Surface fleets continue to dominate high-volume copper, gold, and coal pits, leveraging 400-short-ton haul trucks and electric-rope shovels capable of approximately 90% mechanical availability. Underground mining equipment captured 10.11% CAGR growth prospects through 2030, signaling the shift toward deeper deposits that require low-profile loaders, cable-bolt drills, and advanced ground-support systems.

Crushing, pulverizing, and screening systems thrive on both fronts. EPA dust-suppression standards accelerate the adoption of enclosed conveyors and wet-scrub systems that minimize particulate discharge. Drills and breakers innovate through automated collaring, reducing cycle time and improving fragmentation. Ancillary assets, conveyor trains, pumps, and ventilation fans, see digital retrofits that feed machine-health data into centralized mine-management dashboards.

By Power Source: Electric Momentum Accelerates

Gasoline models held 65.97% share of the United States mining equipment market in 2024, but Electric options logged an 11.23% CAGR, the fastest within power-source segmentation. Early movers validate performance: battery haul trucks meet 250-mile duty cycles on a single charge in select pits. The United States mining equipment market benefits from California’s off-road electrification grants that subsidize pilot deployments. Yet remote operations lacking grid capacity continue to rely on diesel or hybrid gensets.

Wider rollout hinges on scalable charging networks and dealer technicians skilled in high-voltage systems. Further, policy pressure adds urgency. Federal carbon-reduction targets and localized air-quality rules converge with investor mandates, prompting mines to include total emissions in project NPV models. Manufacturers bundle charging infrastructure with equipment sales, spreading capital burdens through service contracts that guarantee uptime.

By Power Output: Mid-Range Remains the Workhorse

In 2024, machines rated between 500 and 2,000 HP accounted for 56.55% of total revenues, showcasing a balance of capability and fuel efficiency in haulage, excavation, and processing. Meanwhile, the segment of machines rated below 500 HP is projected to grow at a CAGR of 8.75%, driven by the adoption of electrified narrow-vein loaders and compact articulated trucks, which are increasingly preferred in selective mining. On the other hand, machines exceeding 2,000 HP, such as draglines and ultra-class trucks, are being utilized in flat-lying coal and copper pits. These larger machines aim to reduce costs per tonne through economies of scale.

In the U.S. market, the ultra-power segment of mining equipment is witnessing growth, especially when pit-optimization studies advocate for higher bench heights and decreased traffic density. The OEMs are charting a course towards modular chassis designs. These designs are versatile, allowing for the integration of diesel, dual-fuel, or battery-electric drivelines. Such a strategy not only caters to evolving power technologies but also safeguards the residual value of the machines.

By Application: Metal Mining Commands Investment

In 2024, metal-ore extraction claimed a 47.12% market share and is projected to grow at a 10.23% CAGR. This growth is driven by domestic policies emphasizing strategic autonomy in the supply chains of copper, lithium, and rare-earth elements. As production decisions are made, the U.S. mining equipment market increasingly aligns with these projects. While non-metal mining, mainly aggregates, reaps benefits from infrastructure initiatives, its growth rates are tempering as quarry capacities approach their limits.

In export-driven basins, demand for coal equipment remains steady. This stability persists even as utilities adjust their fuel preferences, creating a lasting service market for draglines and highwall miners. Manufacturers are tailoring material-handling solutions: from high-abrasion liners designed for copper porphyries and acid-resistant pumps for lithium brines to rare-earth concentrators optimized for fine-particle recovery.

Geography Analysis

Western states dominate the United States mining equipment market, accounting for the bulk of surface copper and gold output as well as every large-scale lithium project currently in construction. Nevada ranks first in active fleet count, followed closely by Arizona and Wyoming. Regional service hubs in Elko, Reno, and Tucson stock critical components and dispatch field technicians by helicopter to remote sites when road access is limited during winter storms.

The Appalachian corridor centers on Pennsylvania, West Virginia, and Kentucky, where deep-coal operations rely on high-capacity continuous miners and longwall systems. As coal volumes plateau, these mines retrofit existing equipment with methane-capture systems and automation packages that compensate for scarce labor. Emerging critical-mineral pilot programs in the region explore rare-earth recovery from coal-ash reservoirs, creating new equipment niches for modular processing units.

Texas and the broader Rocky Mountain range represent a fast-rising cluster, anchored by the Round Top rare-earth project and a string of carbonate-hosted lithium prospects. State incentives speed permitting, while energy-sector infrastructure facilitates logistics for oversize equipment shipments. OEMs plan distribution centers in Amarillo and Cheyenne to shorten parts-delivery lead times. Alaska, with vast but undeveloped polymetallic deposits, sees early adoption of cold-weather autonomous haulage to mitigate workforce constraints and extreme-climate hazards.

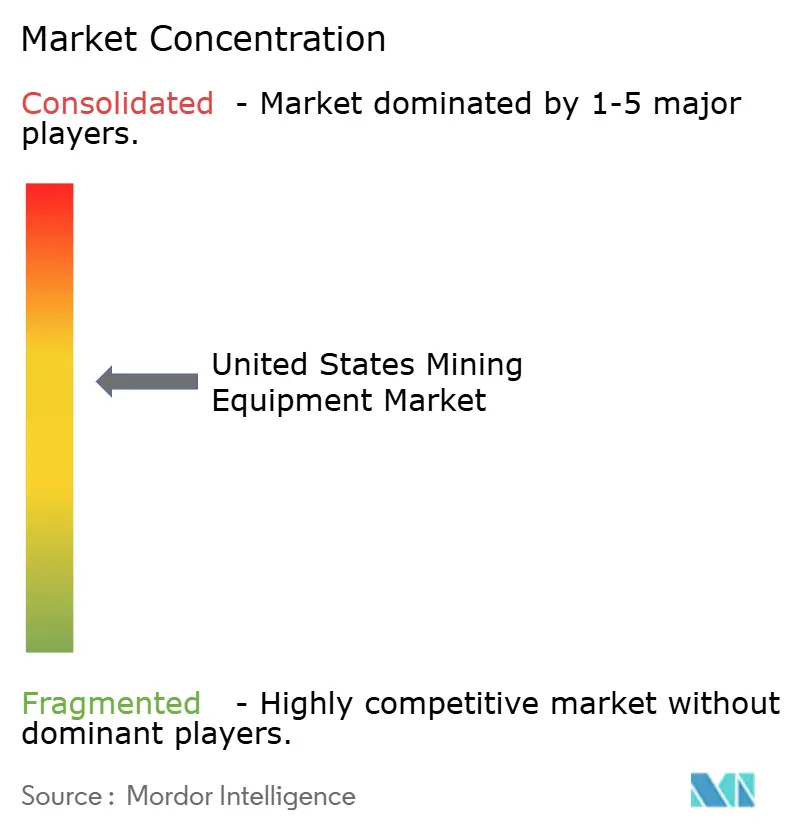

Competitive Landscape

In the U.S. mining equipment market, the top five players command a notable share, yet this concentration opens doors for specialized manufacturers and tech integrators to carve out their niches through innovation. Caterpillar Inc. stands at the forefront, capitalizing on its vast product range and robust service network. Meanwhile, Komatsu Ltd. zeroes in on cutting-edge automation and fuel-efficient technologies.

Technology is the theater of competition. Caterpillar’s MineStar Command platform has autonomously moved more than 8.6 billion metric tonnes without injury, giving customers hard evidence of productivity gains[2]“Cat MineStar Command for Hauling Manages the Autonomous Ecosystem to Increase Haulage Efficiency, Enhance Safety,” Caterpillar, cat.com. Epiroc fields a significant number of driverless drills and LHD units spanning mixed-brand fleets, capturing lucrative upgrade contracts. Sandvik pushes edge analytics solutions that predict component failure up to six weeks in advance, reducing downtime.

Niche challengers carve footholds by specializing in electric drive trains, fast-charge infrastructure, and harsh-environment materials. Modular Mining and Hexagon extend influence through fleet-optimization software that sits agnostic to hardware brand, diluting OEM lock-in. Dealer networks remain critical: mines often select equipment not just for performance but for the proximity and responsiveness of field-service teams.

United States Mining Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Hitachi Construction Machinery

-

Sandvik AB

-

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Caterpillar launched Cat Precision Mining at MINExpo, integrating ore-sensing technology with real-time material classification.

- September 2024: Komatsu unveiled its WX04B battery-electric LHD and HX45 haul truck, expanding its zero-emission underground line.

- September 2024: Epiroc showcased the SmartROC D65 battery-electric drill rig aimed at zero-emission surface operations.

- May 2024: Caterpillar announced a USD 90 million upgrade to Texas facilities to produce the new C13D industrial engine for heavy-duty off-highway equipment.

United States Mining Equipment Market Report Scope

| Underground Mining Equipment |

| Surface Mining Equipment |

| Crushing, Pulverizing and Screening Equipment |

| Drills and Breakers |

| Others |

| Gasoline |

| Electric |

| Below 500 HP |

| 500 to 2000 HP |

| Above 2000 HP |

| Metal Mining |

| Non-metal Mining |

| Coal Mining |

| Equipment Type | Underground Mining Equipment |

| Surface Mining Equipment | |

| Crushing, Pulverizing and Screening Equipment | |

| Drills and Breakers | |

| Others | |

| Power Source | Gasoline |

| Electric | |

| Power Output | Below 500 HP |

| 500 to 2000 HP | |

| Above 2000 HP | |

| Application | Metal Mining |

| Non-metal Mining | |

| Coal Mining |

Key Questions Answered in the Report

How large is the United States mining equipment market in 2025?

The market is valued at USD 13.34 billion in 2025.

What is the projected CAGR through 2030?

The United States mining equipment market is forecast to grow at a 4.42% CAGR to 2030.

Which equipment type is expanding fastest?

Underground mining equipment is projected to rise at a 10.11% CAGR through 2030.

Why are battery-electric machines gaining traction?

They cut operating costs by up to 65% per tonne and meet increasingly strict underground-ventilation and emissions rules.

Page last updated on: