Door And Window Automation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

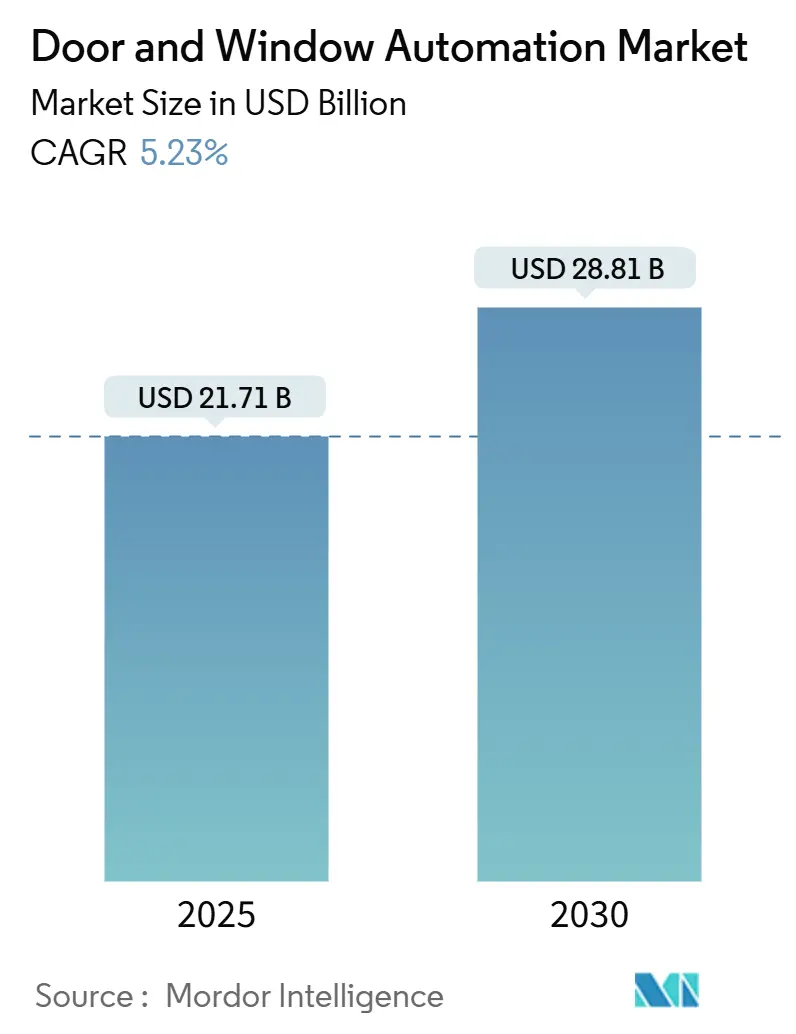

| Market Size (2025) | USD 21.71 Billion |

| Market Size (2030) | USD 28.81 Billion |

| Growth Rate (2025 - 2030) | 5.23% CAGR |

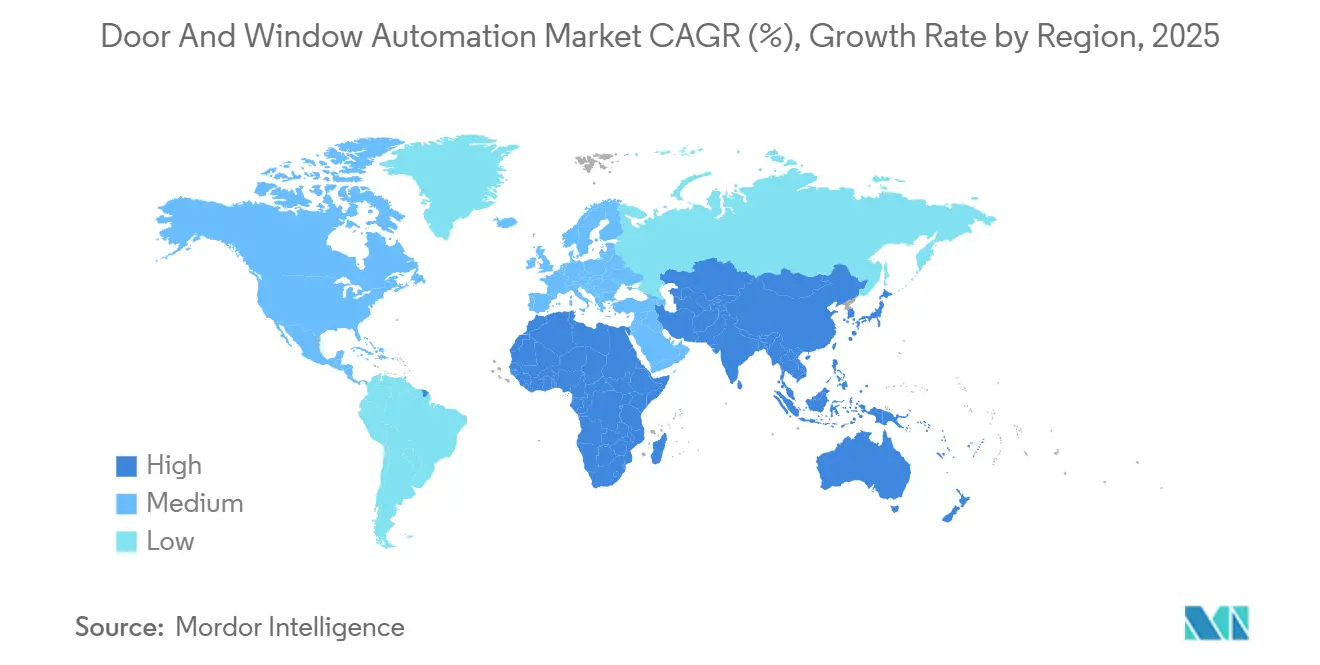

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Door And Window Automation Market Analysis by Mordor Intelligence

The door window automation market size stood at USD 21.71 billion in 2025 and is projected to reach USD 28.81 billion by 2030, reflecting a 5.23% CAGR over the forecast period. Rising demand for touch-free entrances in commercial real-estate, universal-design compliance for aging populations, and energy-efficiency mandates underpin the uptrend. Vendors are shifting toward smart, cloud-enabled solutions that integrate with building-management systems and deliver data-driven service models, while also countering supply-chain volatility for linear actuators with multi-sourcing and in-house motor design. Asia-Pacific retains scale advantage through strong construction pipelines in China, India, and Southeast Asia, whereas Middle East and Africa is evolving into the fastest growth pocket as luxury mixed-use projects and transport-hub expansions embrace automation. Competitive dynamics intensify as incumbents embed AI analytics and IoT connectivity into hardware to capture higher-margin service revenues and prolong asset life cycles.

Key Report Takeaways

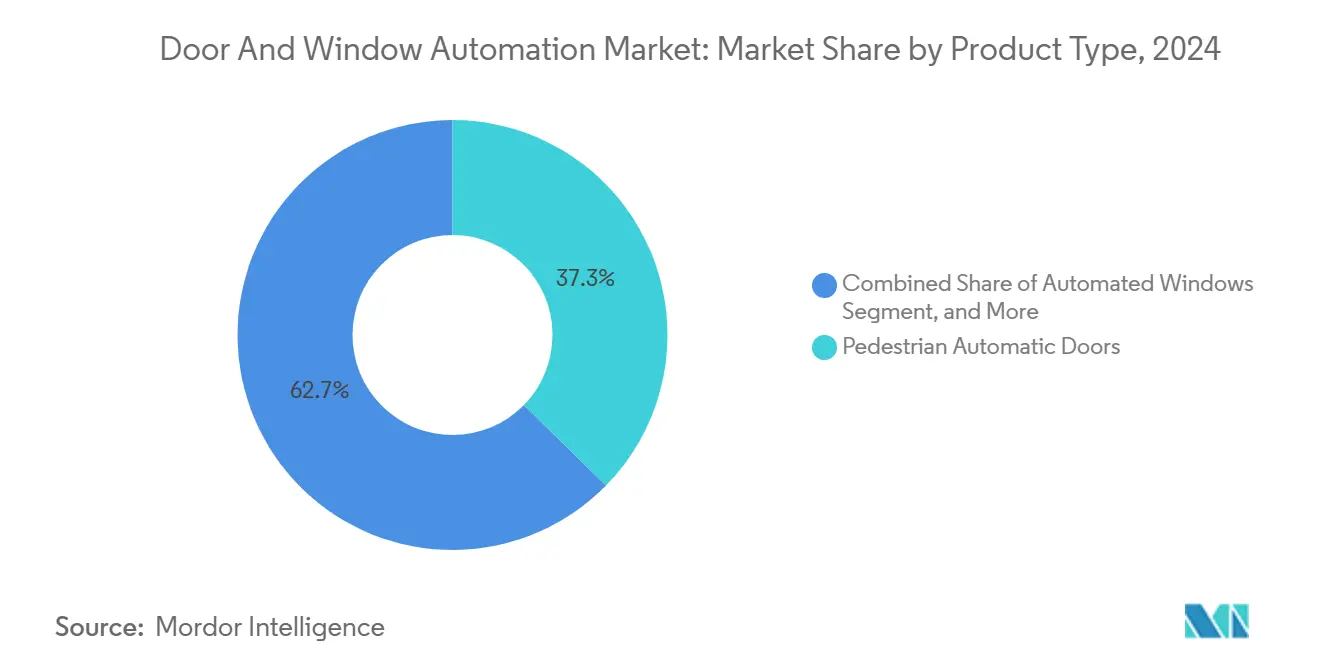

- By product type, pedestrian automatic doors held 37.34% of the door window automation market share in 2024, while automated windows are forecast to expand at a 5.89% CAGR to 2030.

- By component, operators and actuators commanded 41.78% of the door window automation market size in 2024, whereas access-control systems are advancing at a 5.54% CAGR through 2030.

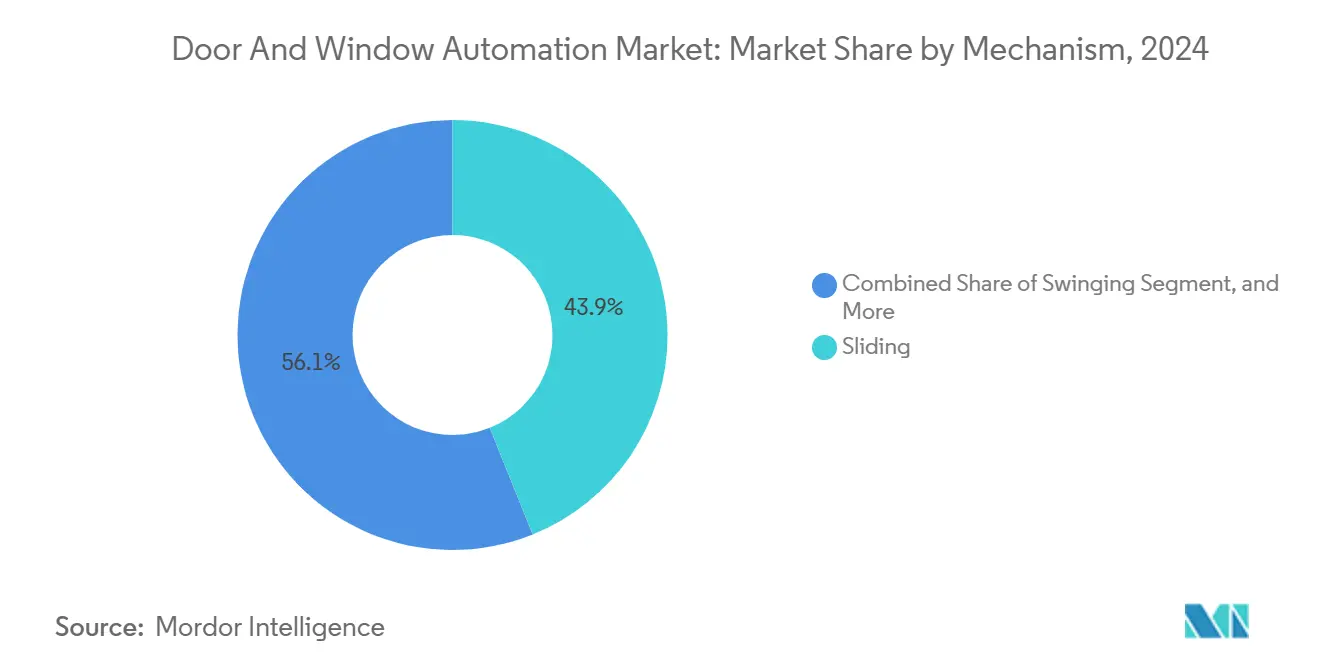

- By mechanism, sliding systems accounted for 43.92% of the door window automation market size in 2024 and revolving mechanisms record the highest forecast CAGR of 5.29% to 2030.

- By end-user, commercial buildings led with 47.63% revenue share in 2024; healthcare facilities are projected to surge at a 5.61% CAGR over the same horizon.

- By geography, Asia-Pacific captured 37.32% of 2024 revenue and Middle East and Africa is poised for a 6.11% CAGR through 2030.

Global Door And Window Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of smart-building energy-efficiency retrofits | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Heightened security regulations integrating automated access | +0.9% | Global, with emphasis on Asia-Pacific and MEA | Short term (≤ 2 years) |

| Population ageing and universal-design mandates | +0.8% | North America and EU primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Post-pandemic touch-free upgrades in transport hubs | +0.7% | Global, with priority in major transportation corridors | Short term (≤ 2 years) |

| Adaptive façade demand for natural-ventilation windows | +0.6% | EU and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Automated drone-dock doors in e-commerce fulfilment | +0.4% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Smart-Building Energy-Efficiency Retrofits

Global energy codes increasingly require high-performance fenestration, making automated windows and doors a direct path to compliance. California’s Title 24 sets strict U-factor thresholds, prompting facility owners to automate openings to reduce HVAC load. Research at KAIST showed responsive electrochromic modules trimming indoor temperature by 27.2 °C, underlining tangible savings for retrofit investors.[1]Hong Chul Moon, “Glare-Free, Energy-Efficient Smart Windows,” News at KAIST, news.kaist.ac.kr Toolsets such as dormakaba’s Door Efficiency Calculator translate those savings into payback periods for clients. Falling material costs for electrode-free electrochromic glass toward USD 80 per m² broaden the addressable market. Together, regulation, measurable ROI, and maturing technology place energy retrofits among the most powerful catalysts for the door window automation market.

Heightened Security Regulations Integrating Automated Access

Physical-security frameworks now stipulate unified door automation and credential management, especially in airports, hospitals, and government estates. Forty percent of enterprises reported live biometric deployments for physical access in 2024.[2]Jadhav Abhishek, “2 in 5 Businesses Now Use Biometrics,” biometricupdate.com Portland International Airport earmarked USD 600,000 for automated breach-control lanes to preserve traveler throughput without relaxing security. Healthcare operators equally converge on touch-free platforms like dormakaba TouchGo to balance HIPAA compliance with staff mobility. Industry standards are adding cybersecurity layers for encrypted door controllers, turning secure-by-design architecture into a procurement prerequisite.

Population Ageing and Universal-Design Mandates

Demographic aging in OECD economies intensifies enforcement of automatic-door provisions in codes such as the Americans with Disabilities Act and the 2022 California Building Code. The International Code Council updated accessibility benchmarks for power-operated doors, ensuring predictable opening forces and fail-safe closing cycles.[3]Kimberly Paarlberg, “New Automatic Door Requirements for Accessibility,” iccsafe.org Hospitals retrofit breakaway doors that double as emergency egress and infection-control barriers. Beyond mobility, universal design now incorporates cognitive aids such as illuminated push plates and audible status cues, expanding the functional brief for automation vendors.

Post-Pandemic Touch-Free Upgrades in Transport Hubs

Airports, metros, and intercity rail stations accelerate rollouts of touchless doors and self-boarding gates to rebuild passenger confidence. Automated exit-lane systems complemented by video analytics uphold separation accuracy while trimming manual staffing. Robotic assistants such as Munich Airport’s evoBOT integrate with automated doors for end-to-end baggage handling. IoT sensors feeding machine-learning engines enable dynamic door-cycle adjustments that smooth peak-hour congestion without sacrificing security. The proven uplift in dwell-time revenue and customer-satisfaction scores cements post-pandemic automation as a permanent operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and maintenance cost structure | -1.1% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Cyber-security and data-privacy vulnerabilities | -0.8% | Global, with emphasis on regulated industries | Medium term (2-4 years) |

| Linear-actuator component supply pinch | -0.6% | Global, with concentration in manufacturing hubs | Short term (≤ 2 years) |

| Fragmented certification standards in emerging markets | -0.4% | Primarily emerging markets in Asia-Pacific, MEA, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Installation and Maintenance Cost Structure

Turn-key industrial door automation can exceed USD 10,000 once specialized commissioning and safety edges are included, deterring uptake in cost-sensitive segments. Healthcare doors with impact-resistant edges and fail-secure mechanisms command further premiums. Volatile aluminum pricing, projected at USD 2,763 per ton in 2025, adds margin pressure. Extended total cost of ownership also factors in software subscriptions and cybersecurity patches, stretching budgets for small facilities.

Cyber-Security and Data-Privacy Vulnerabilities

Connected doors enlarge attack surfaces for hackers seeking lateral movement into building-management networks. Incidents drive end-users to demand end-to-end encryption, secure boot modules, and regular firmware audits, all of which raise acquisition and lifecycle costs. Mobile-credential ecosystems process sensitive PII, binding vendors to GDPR and state-level privacy compliance. Semiconductor shortages have pushed some OEMs toward lower-grade microcontrollers that may lack robust hardware roots-of-trust, creating latent vulnerability until supply normalizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pedestrian Doors Drive Volume, Windows Accelerate Innovation

Pedestrian automatic doors generated 37.34% of 2024 revenue within the door window automation market, reflecting their entrenched role in retail, office, and healthcare settings where constant footfall justifies automation. Volume scale has lowered installed-cost baselines, allowing suppliers to cross-sell IoT sensors and predictive service packages. Continued urban retail expansion and safety regulations are expected to maintain the segment’s leadership through 2030. In contrast, automated windows deliver the highest 5.89% CAGR, propelled by smart-facade projects that couple indoor-air-quality goals with renewable-energy modules such as transparent organic PV panes.

A proliferation of industrial drones in e-commerce logistics drives demand for rugged automatic doors on drone docks that secure goods while enabling unmanned flight operations. Premium curtain-wall systems featuring dynamic shading and electrochromic glass are gaining specification in high-rise offices seeking net-zero targets, further widening adoption of integrated window actuators. Overall, the product mix shift toward energy-harvesting and AI-controlled envelopes positions windows as the innovation frontier of the door window automation market.

By Component: Operators Lead Market, Access Control Systems Drive Innovation

Operators and actuators captured 41.78% of 2024 door window automation market size, cementing their status as the mechanical backbone across all product categories. Electric linear actuators alone accounted for a USD 20.5 billion sub-market in 2022 and are forecast at USD 34.3 billion by 2032. Manufacturers now embed brushless motors and regenerative braking features to improve energy profiles and extend maintenance intervals, bolstering value propositions for retrofit buyers.

Access-control systems log the fastest 5.54% CAGR as biometric, cloud, and mobile-credential technologies converge into unified identity platforms. AI-enabled edge controllers deliver real-time anomaly detection while reducing false alarms to single-digit percentages, supporting enterprise adoption in regulated sectors. Software-defined panels permit over-the-air feature upgrades, converting one-time hardware sales into recurring revenues. Sensors, control panels, and power-supply sub-assemblies likewise shift toward modular plug-and-play designs, shortening installation timelines and minimizing field calibration.

By Mechanism: Sliding Dominates, Revolving Gains Architectural Preference

Sliding systems retained 43.92% share of the door window automation market in 2024 thanks to space-saving tracks that accommodate wheelchair turning radii and merchandise displays. Vendors now offer low-profile headers and pocket designs that blend with frameless glass aesthetics, meeting contemporary architectural standards while sustaining throughput. Enhanced roller materials and self-cleaning tracks are extending duty cycles beyond 1 million openings, curbing service downtime.

Revolving doors, though holding a smaller installed base, post a 5.29% CAGR as architects pursue vestibule solutions that curb air infiltration and lower HVAC loads in premium office towers. Newly developed torque-sensing safety edges and integrated air curtains bolster energy-performance credentials, aligning with LEED and BREEAM scoring. Folding, tilt-and-turn, swinging, and pivoting mechanisms fill niche demands ranging from constrained corridors to panoramic retail frontages, but their adoption trajectory remains tied to specialized design briefs rather than volume roll-outs.

By End-User Industry: Commercial Buildings Lead, Healthcare Accelerates Adoption

Commercial real estate contributed 47.63% to 2024 revenue, illustrating how office campuses, malls, and mixed-use complexes form the demand locus for pedestrian door systems, façade venting, and integrated security portals. Asset managers leverage automation to elevate tenant experiences and to comply with accessibility codes. Meanwhile, healthcare facilities deliver a 5.61% CAGR, spurred by post-pandemic infection-control protocols and universal-design stipulations. Case in point: Northwell Health’s deployment of Acrovyn Doors blends antimicrobial surfaces with automated hinges, reinforcing clinical hygiene norms.

Industrial and logistics buildings accelerate adoption of high-speed fabric doors and dock levellers synchronized with autonomous guided vehicles, enhancing worker safety and throughput. Residential uptake concentrates in luxury apartments and assisted-living projects where touch-free entry systems improve convenience and safety for seniors. Airports, stadiums, and theme parks drive hospitality and leisure demand, while education and government campuses adopt automation selectively under budgetary constraints but must still meet Americans with Disabilities Act compliance.

Geography Analysis

Asia-Pacific’s 37.32% revenue share in 2024 underscores its dual role as manufacturing powerhouse and end-market. Chinese tier-one cities mandate smart building features, increasing attach rates for sensor-rich door operator packages, while India’s Smart Cities Mission finances integrated security and access systems in urban cores. Service-led revenue at KONE rose sharply in Asia-Pacific, evidencing a shift from new-unit sales toward modernization and lifecycle contracts.

Middle East and Africa, though smaller, advances at 6.11% CAGR as Doha, Riyadh, and Dubai commission mixed-use districts that prioritize seamless, climate-controlled access. Automated revolving doors with integrated air curtains mitigate dust and heat, supporting occupant comfort and energy‐management targets. Local distributors increasingly stock European and U.S. brands, shortening lead times and boosting after-sales coverage.

North America and Europe, characterized by stringent ADA and EN 16005 standards, concentrate investment in upgrading legacy hydraulic closers to motorized units with embedded diagnostics. California’s 2025 energy code revisions and the European Green Deal stimulate demand for window-actuation kits that integrate into BMS dashboards, while large public-sector retrofit budgets in schools and courthouses secure a steady flow of projects. These mature regions also pioneer cloud analytics that transform installed doors into data nodes for predictive maintenance, setting benchmarks that other geographies emulate.

Competitive Landscape

The door window automation industry remains moderately fragmented, yet consolidation momentum is unmistakable. ASSA ABLOY’s USD 350 million acquisition spree including SKIDATA, 3millID, and Third Millennium adds cloud parking and secure credential technologies that dovetail with its operator portfolio. dormakaba strengthened its Dutch airport vertical with Montagebedrijf van den Berg, enhancing direct project execution capability. Fortune Brands Innovations moved deeper into connected residential locks by purchasing Emtek, Schaub, Yale, and August lines from ASSA ABLOY, opening cross-selling avenues in the smart-home channel.

Beyond scale economics, competitive advantage pivots on digital ecosystems. Market leaders embed AI into controllers for self-diagnosis, while SaaS licensing yields recurring revenue ratios exceeding 35% for top players. Start-ups like NEXT Energy Technologies exploit patentable photovoltaic glass to disrupt incumbent façade solutions, attracting VC funding and early-adopter architects. Patent filings related to proximity-based object tracking for doors rose 18% YoY, highlighting R&D intensity. Collectively, these moves tighten margin pressure on mid-tier regional manufacturers that lack the capital to pivot from hardware to platform economics.

As decision makers seek end-to-end warranties and single-dashboard management, integrators capable of bundling operators, credentials, analytics, and field services are winning multi-site frameworks. This convergence positions diversified conglomerates to widen market share, while niche players focus on specialized segments such as sterile-room doors or drone-dock hatches to maintain relevance.

Door And Window Automation Industry Leaders

ASSA ABLOY AB

Allegion plc

Nabtesco Corporation

Stanley Access Technologies LLC

dormakaba International Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Fortune Brands Innovations finalized the acquisition of Emtek, Schaub, Yale, and August brands for projected USD 500–550 million revenue, targeting EPS accretion of USD 0.45-0.55 in year 3.

- February 2025: dormakaba bought Montagebedrijf van den Berg B.V. to fortify its Netherlands airport project pipeline, with immediate EPS accretion.

- January 2025: CAME Group reported EUR 335 million turnover for 2024, up 8.4%, and announced portfolio expansion for 2025.

- January 2025: ASSA ABLOY completed the acquisition of 3millID and Third Millennium Systems, adding USD 21 million in combined 2023 sales.

Global Door And Window Automation Market Report Scope

| Pedestrian Automatic Doors |

| Industrial Automatic Doors |

| Automated Windows |

| Automated Curtain Walls / Facades |

| Door and Window Operators / Actuators |

| Sensors and Detectors |

| Access Control Systems |

| Control Panels and Software |

| Power Supply and Motors |

| Sliding |

| Swinging |

| Folding |

| Revolving |

| Tilt and Turn (Windows) |

| Pivoting |

| Commercial Buildings |

| Residential Buildings |

| Industrial and Logistics Facilities |

| Healthcare Facilities |

| Transportation Hubs |

| Hospitality and Leisure |

| Education and Government |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Pedestrian Automatic Doors | ||

| Industrial Automatic Doors | |||

| Automated Windows | |||

| Automated Curtain Walls / Facades | |||

| By Component | Door and Window Operators / Actuators | ||

| Sensors and Detectors | |||

| Access Control Systems | |||

| Control Panels and Software | |||

| Power Supply and Motors | |||

| By Mechanism | Sliding | ||

| Swinging | |||

| Folding | |||

| Revolving | |||

| Tilt and Turn (Windows) | |||

| Pivoting | |||

| By End-user Industry | Commercial Buildings | ||

| Residential Buildings | |||

| Industrial and Logistics Facilities | |||

| Healthcare Facilities | |||

| Transportation Hubs | |||

| Hospitality and Leisure | |||

| Education and Government | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the door window automation market in 2025?

The door window automation market size reached USD 21.71 billion in 2025 and is projected to climb to USD 28.81 billion by 2030.

Which product category is growing the fastest?

Automated windows exhibit the strongest momentum with a 5.89% CAGR through 2030, spurred by smart-facade and energy-efficiency projects.

Which region is expected to grow most rapidly?

Middle East & Africa leads growth with a 6.11% CAGR, fueled by smart-city developments and luxury mixed-use construction.

What is driving adoption in healthcare facilities?

Infection-control protocols and universal-design mandates propel a 5.61% CAGR for healthcare installations of automated doors and windows.

How are vendors differentiating their offerings?

Leading firms embed IoT sensors, cloud analytics, and AI-based predictive maintenance to convert hardware sales into recurring service revenue streams.

What are the main barriers to wider adoption?

High upfront installation costs and cybersecurity concerns are the primary restraints, each trimming the forecast CAGR by roughly 1 percentage point.

Page last updated on: