Digital Door Lock Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

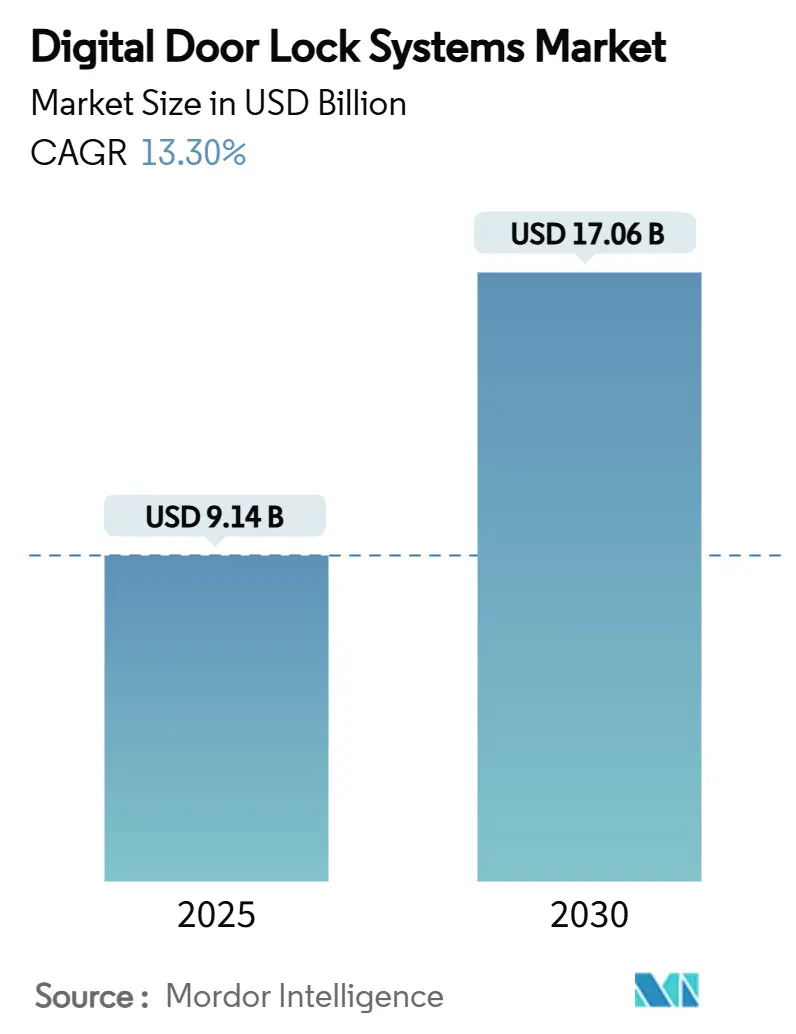

| Market Size (2025) | USD 9.14 Billion |

| Market Size (2030) | USD 17.06 Billion |

| Growth Rate (2025 - 2030) | 13.30% CAGR |

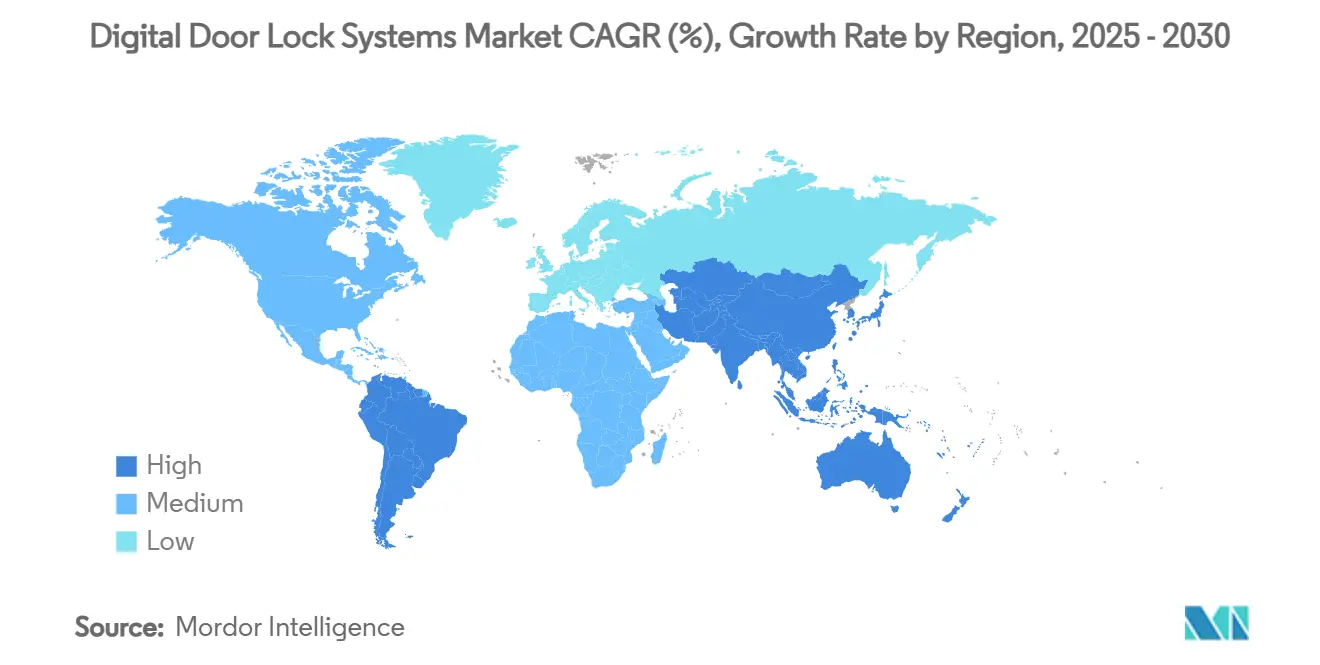

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

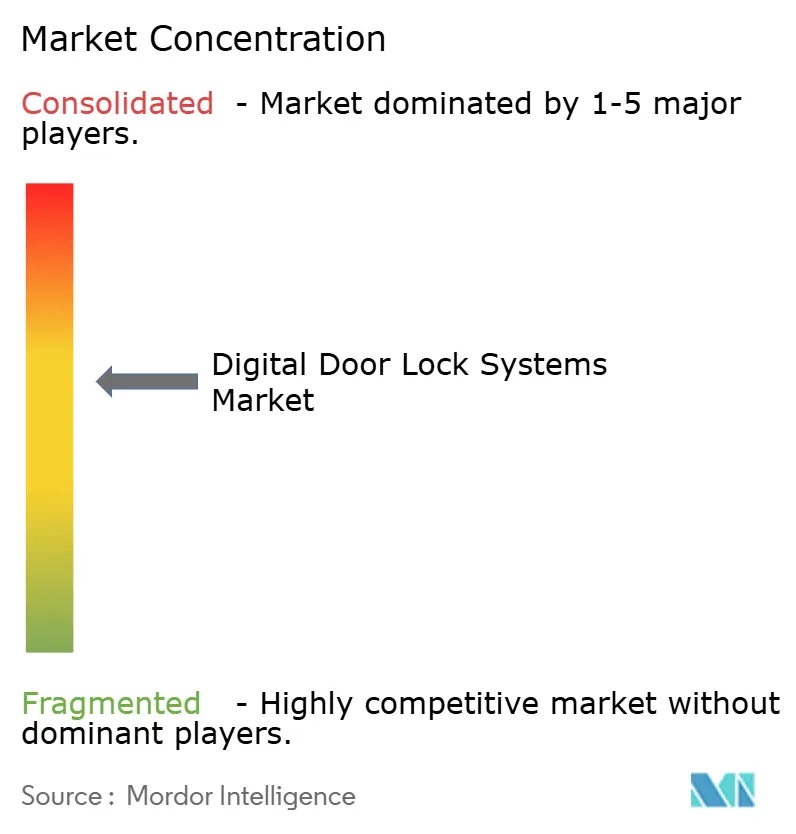

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Door Lock Systems Market Analysis by Mordor Intelligence

The digital door lock systems market size stands at USD 9.14 billion in 2025 and is expected to reach USD 17.06 billion by 2030, reflecting a 13.30% CAGR. This growth momentum comes from the convergence of smart-home adoption, falling component prices, and post-pandemic demand for touch-free security. Standardization efforts such as Matter and Aliro remove interoperability barriers and raise buyer confidence. Biometric accuracy now meets enterprise security thresholds and encourages wider consumer uptake. Manufacturers also benefit from insurance incentives that reward connected security installations, while urban micro-apartment projects accelerate bulk deployments.

Key Report Takeaways

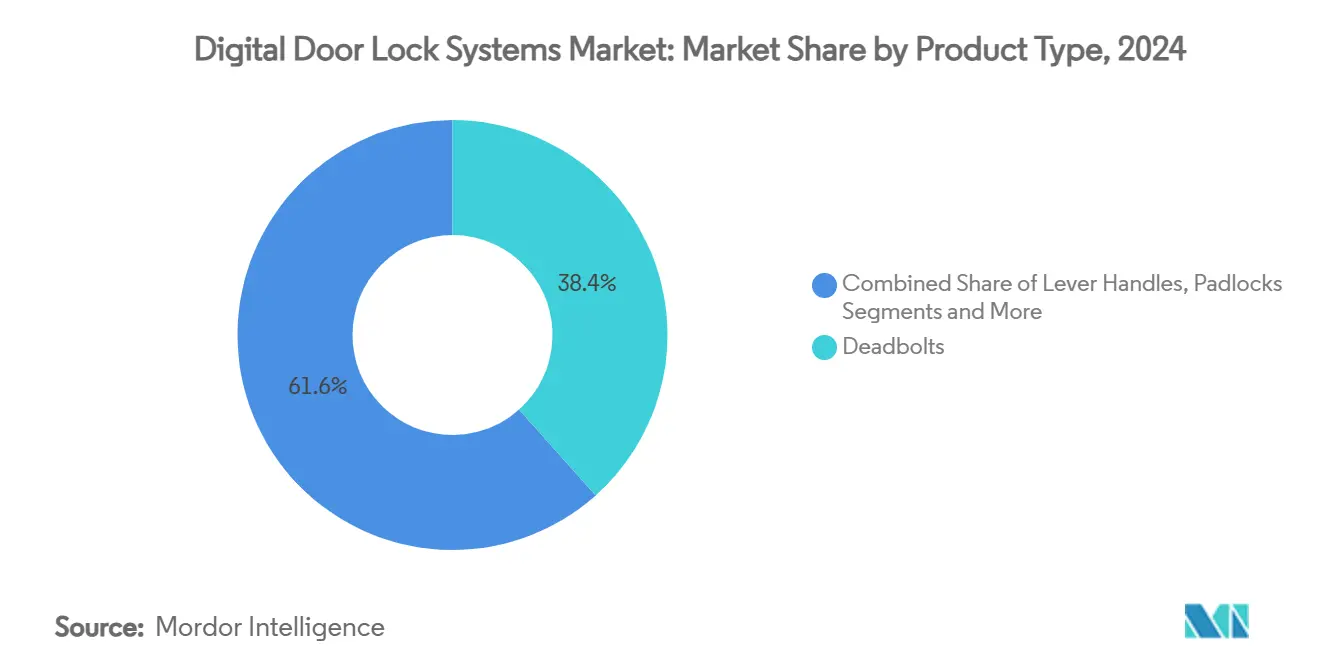

- By product type, deadbolts led with 38.4% of digital door lock systems market share in 2024; Padlocks are projected to expand at a 13.4% CAGR through 2030.

- By technology, keypad / PIN solutions accounted for 41.2% of digital door lock systems market size in 2024; Connectivity-based locks are set to grow at a 13.9% CAGR through 2030.

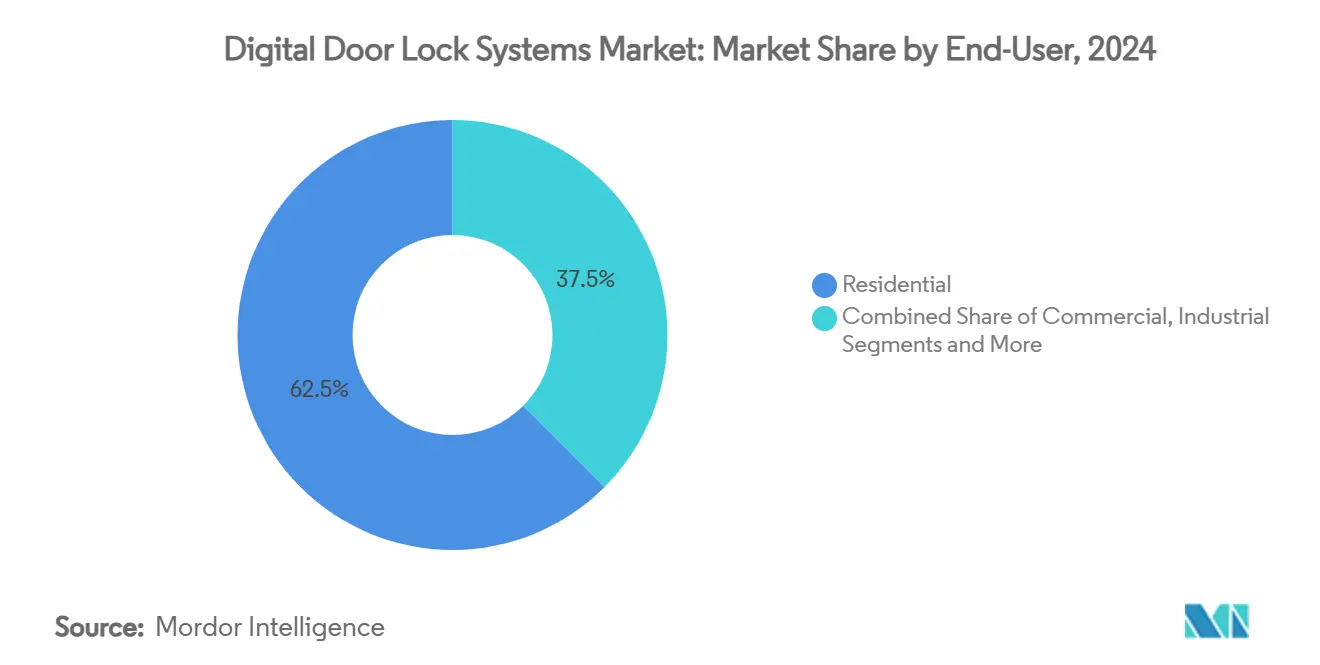

- By end-user, residential applications commanded 62.5% share of the digital door lock systems market size in 2024; Industrial and critical infrastructure demand is rising at a 14.1% CAGR through 2030.

- By sales channel, offline distribution retained 71.3% revenue share in 2024; Online sales will advance at a 14.2% CAGR through 2030.

- By geography, North America held 34.8% share of the digital door lock systems market size in 2024; Asia Pacific is forecast to post a 13.5% CAGR through 2030.

Global Digital Door Lock Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing smart-home adoption | +3.3% | Global, with North America & EU leading | Medium term (2-4 years) |

| Declining sensor and module costs | +2.4% | APAC core, spill-over to global markets | Short term (≤ 2 years) |

| Biometric accuracy improvements | +2.0% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Post-COVID touch-free access mandates | +1.6% | Global, strongest in commercial sectors | Short term (≤ 2 years) |

| Insurance-premium incentives | +1.1% | North America & EU primarily | Long term (≥ 4 years) |

| Urban micro-apartments and co-living boom | +1.3% | APAC urban centers, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Smart-Home Adoption

Smart-home ecosystems position digital locks as core infrastructure rather than luxury add-ons. Matter and Aliro protocols let smartphones and voice assistants manage locks seamlessly, removing the need for proprietary hubs. Kwikset’s ultra-low-power Wi-Fi modules simplify installation while extending battery life.[1]Silicon Labs, “Kwikset Chooses Ultra-Low-Power WiFi SoC,” SILABS.COM Consumer studies show more than half of device owners now rate interoperability as a top purchase factor, which reinforces demand for standards-compliant locks. Insurance providers in North America and Europe discount premiums for connected doors, adding a financial motive for adoption. Together these factors keep the digital door lock systems market on a steep growth path.

Declining Sensor and Module Costs

Fingerprint readers and connectivity chipsets drop in price each year as semiconductor scale grows. Silicon Labs’ single-chip Wi-Fi platforms cut bill-of-materials counts and improve energy efficiency. The Z-Wave Alliance has certified more than 4,300 interoperable products, which drives volume and further lowers costs. [2]Z-Wave Alliance, “Product Catalog,” Z-WAVEALLIANCE.ORGAsia Pacific manufacturers leverage vertical supply chains to offer competitively priced smart locks, expanding the addressable customer base. Battery-free NFC harvesting prototypes promise additional lifetime cost cuts once reliability improves.

Biometric Accuracy Improvements

Advanced algorithms now recognize faces in poor lighting and can adjust for aging or accessories. ZKTeco and Zwipe showed biometric smart cards that pair with locks for multi-factor authentication.[3]ZKTeco, “Collaboration with Zwipe,” ZKTECO.EUPhilips Home Access demonstrated palm-vein recognition with extremely low false acceptance rates. AI-based learning further reduces false rejections over time, boosting user satisfaction in residential and commercial sites. High-security sectors adopt these features quickly, and mainstream consumers follow as prices fall.

Post-Pandemic Touch-Free Mandates

Commercial property managers embed contactless entry in long-term capital budgets. Ultra-wideband chips enable hands-free unlocking when an authorized phone approaches, as seen in ASSA ABLOY’s robotics collaboration. Hotels deploy mobile keys through dormakaba platforms to cut queue times and sanitation labor. The shift also creates recurring software subscriptions for credential management, giving vendors predictable revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and privacy concerns | -2.0% | Global, strongest in EU and regulated sectors | Short term (≤ 2 years) |

| Interoperability standards fragmentation | -1.6% | Global, particularly affecting premium segments | Medium term (2-4 years) |

| Recycling and e-waste compliance costs | -1.1% | EU and developed markets with strict regulations | Long term (≥ 4 years) |

| Energy-harvesting reliability limits | -0.8% | Global, concentrated in battery-free applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Privacy Concerns

The EU Cyber Resilience Act mandates secure development, SBOM maintenance, and vulnerability management with fines up to EUR 15 million for non-compliance. Smaller firms face higher per-unit compliance costs, lengthening time-to-market. Consumers also worry about cloud storage of biometric data, especially in regions with strict privacy laws. These factors slow purchase decisions and raise development budgets.

Interoperability Standards Fragmentation

Despite Matter’s progress, many installed systems still rely on proprietary or legacy protocols. Installers must master multiple standards, raising service costs and inventories. Consumers hesitate when compatibility is unclear, which tempers high-end growth until ecosystems converge. Associations such as the Connectivity Standards Alliance continue to promote harmonization, but fragmentation remains a near-term headwind. [4]Connectivity Standards Alliance, “Matter State of the Art,” CSASTANDARDS.ORG

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deadbolts Remain the Anchor of Residential Security

Deadbolts represented 38.4% of digital door lock systems market share in 2024 thanks to retrofit ease and robust build quality. They integrate aesthetic finishes with standard door preps, limiting labor time. Lever handles dominate commercial settings where accessibility codes favor push-down operation, yet their overall share trails deadbolts. Padlocks post a 13.4% CAGR through 2030 as factories and logistics operators demand portable, app-controlled security. ASSA ABLOY’s Centrios padlock line manages up to 200 users per device, illustrating how industrial buyers support premium pricing.

Rim and mortise lock bodies satisfy niche architectural needs where vintage doors or regional standards rule out tubular options. Growth for these categories lags the broader market yet remains steady in renovation segments. Together, product diversification ensures suppliers capture multiple use cases while deadbolts stay the revenue cornerstone of the digital door lock systems market.

By Technology: Connectivity Drives the Next Adoption Wave

Keypad / PIN locks held 41.2% of digital door lock systems market size in 2024 because they deliver reliable access without smartphones. Adoption spans all income levels and climate zones, keeping this technology relevant. Biometric models serve premium buyers seeking convenience and higher security, while RFID smart-card variants fit offices that need centralized credential audits.

Wi-Fi, Bluetooth, Z-Wave, and Thread connectivity options grow at 13.9% CAGR. Matter certification allows a single app to enroll devices from multiple brands, which accelerates do-it-yourself installations. Ultra-wideband advances promise true hands-free entry by measuring distance with centimeter precision. Connectivity now differentiates products more than mechanical strength, signaling maturity of the digital door lock systems market.

By End-User: Industrial Demand Surges

Residential buyers accounted for 62.5% of digital door lock systems market share in 2024 as smart-home bundles made connected locks mainstream. User priorities center on curb appeal, mobile notifications, and easy retrofits. Commercial offices and hotels require audit trails and multi-door scheduling, supporting SaaS upsell potential.

Industrial and critical infrastructure sites climb at a 14.1% CAGR through 2030. Mandates for documented access and remote credential revocation drive conversions from mechanical keys to connected locks. Government facilities look for FIPS and other certifications, narrowing the field to established brands. Cross-segment technology transfer, such as AI-based authentication, further expands the industrial addressable market.

By Sales Channel: E-Commerce Gains Ground

Offline retail and integrator channels kept 71.3% of revenue in 2024. Storefronts let buyers assess build quality and obtain same-day installation, which remains important for time-sensitive projects. Professional installers add value by linking locks with alarms and cameras.

Online platforms nonetheless rise at 14.2% CAGR through 2030. Brands sell direct to end users and include video tutorials that cut support calls. Subscription management portals bundle software with hardware, creating long-tail revenue. Data analytics from direct channels inform feature roadmaps faster than traditional distribution feedback loops, giving digital natives a strategic edge in the digital door lock systems market.

Geography Analysis

North America commanded 34.8% of digital door lock systems market size in 2024, supported by high disposable incomes and widespread smart-home ecosystems. United States builders frequently specify connected locks in new single-family and multifamily projects, and insurance discounts further incentivize upgrades. Canada and Mexico follow similar patterns though with smaller absolute volumes.

Asia Pacific is on track for a 13.5% CAGR through 2030. China leverages domestic mass production to drive cost-effective adoption, while rising middle-class households in India integrate smart locks into fast-growing urban housing. Japan and South Korea favor premium biometric features, which pushes technology leaders to launch advanced models early in these markets.

Europe maintains steady demand underpinned by strong building codes and data privacy regulation. The EU Cyber Resilience Act raises the security baseline, benefitting compliant suppliers. Southern Europe prioritizes affordability and basic connectivity, whereas Germany and the Nordic countries select high-spec models with sustainability credentials.

Competitive Landscape

The market is moderately consolidated. ASSA ABLOY leads with successive acquisitions including Level Lock for USD 16 million and InVue for USD 165 million in 2024 that broaden its technology stack and retail presence. Allegion cooperates with the Connectivity Standards Alliance to advance the Aliro protocol, reinforcing its ecosystem role. Dormakaba strengthens service capabilities through targeted purchases such as Montagebedrijf van den Berg in early 2025.

Innovators target specific pain points rather than compete head-on with incumbents. Lockly combines 2K video with facial recognition for premium residential buyers, and ZKTeco pairs biometric readers with smart cards for high-security European installations. Semiconductor firms such as Silicon Labs secure design wins by offering ultra-low-power Wi-Fi SoCs tailor-made for smart locks. The interplay of hardware, software, and services shapes competition as vendors shift toward recurring revenue models within the digital door lock systems market.

Digital Door Lock Systems Industry Leaders

ASSA ABLOY

Allegion (Schlage)

Dormakaba Group

Samsung SDS

Honeywell International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ASSA ABLOY acquired InVue for USD 165 million, expanding asset protection and software revenue streams.

- January 2025: Lockly announced Vision Prestige video smart lock with facial recognition and UWB hands-free entry for launch in Q4 2025.

- January 2025: Allegion debuted Schlage Sense Pro and Arrive Smart WiFi deadbolts with Matter-over-Thread compatibility.

- January 2025: Philips Home Access introduced a Matter-ready deadbolt featuring palm-vein biometrics and HD video.

Global Digital Door Lock Systems Market Report Scope

| Deadbolts |

| Lever Handles |

| Padlocks |

| Others (Rim, Mortise, etc.) |

| Biometric (Fingerprint, Face) |

| Keypad / PIN |

| RFID / Smart Card |

| Connectivity (Wi-Fi, Bluetooth, Z-Wave) |

| Residential |

| Commercial (Offices, Retail, Hospitality) |

| Industrial and Critical Infrastructure |

| Government and Public Buildings |

| Offline (DIY, Pro-install, Distributors) |

| Online (e-commerce, D2C) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Deadbolts | ||

| Lever Handles | |||

| Padlocks | |||

| Others (Rim, Mortise, etc.) | |||

| By Technology | Biometric (Fingerprint, Face) | ||

| Keypad / PIN | |||

| RFID / Smart Card | |||

| Connectivity (Wi-Fi, Bluetooth, Z-Wave) | |||

| By End-user | Residential | ||

| Commercial (Offices, Retail, Hospitality) | |||

| Industrial and Critical Infrastructure | |||

| Government and Public Buildings | |||

| By Sales Channel | Offline (DIY, Pro-install, Distributors) | ||

| Online (e-commerce, D2C) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the global digital door lock systems market?

The digital door lock systems market size is USD 9.14 billion in 2025.

What CAGR is projected for digital door lock systems between 2025 and 2030?

The market is forecast to grow at a 13.3% CAGR through 2030.

Which product type leads the digital door lock systems market?

Deadbolts hold the lead with 38.4% revenue share in 2024.

Which region is the fastest growing in digital door locks?

Asia Pacific is expected to record a 13.5% CAGR up to 2030.

What is the key driver behind market growth?

Rising smart-home adoption and interoperability standards are major growth catalysts.

Which sales channel is expanding most rapidly?

Online direct-to-consumer sales are advancing at a 14.2% CAGR.

Page last updated on: