Tunnel Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

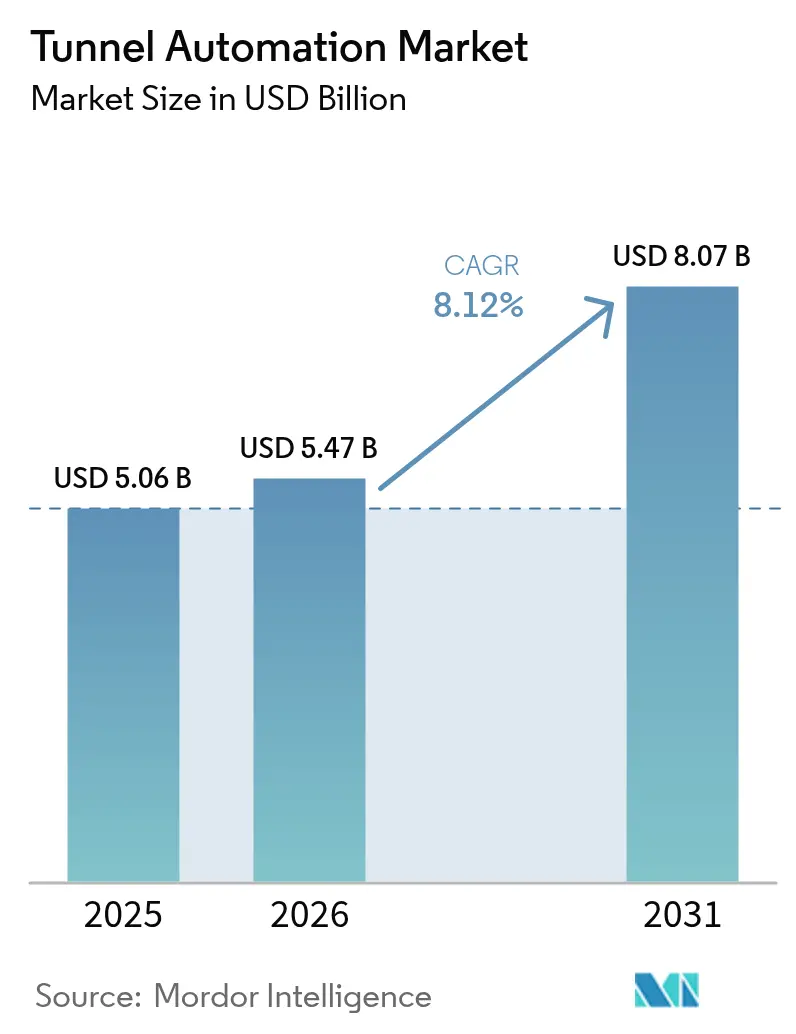

| Market Size (2026) | USD 5.47 Billion |

| Market Size (2031) | USD 8.07 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

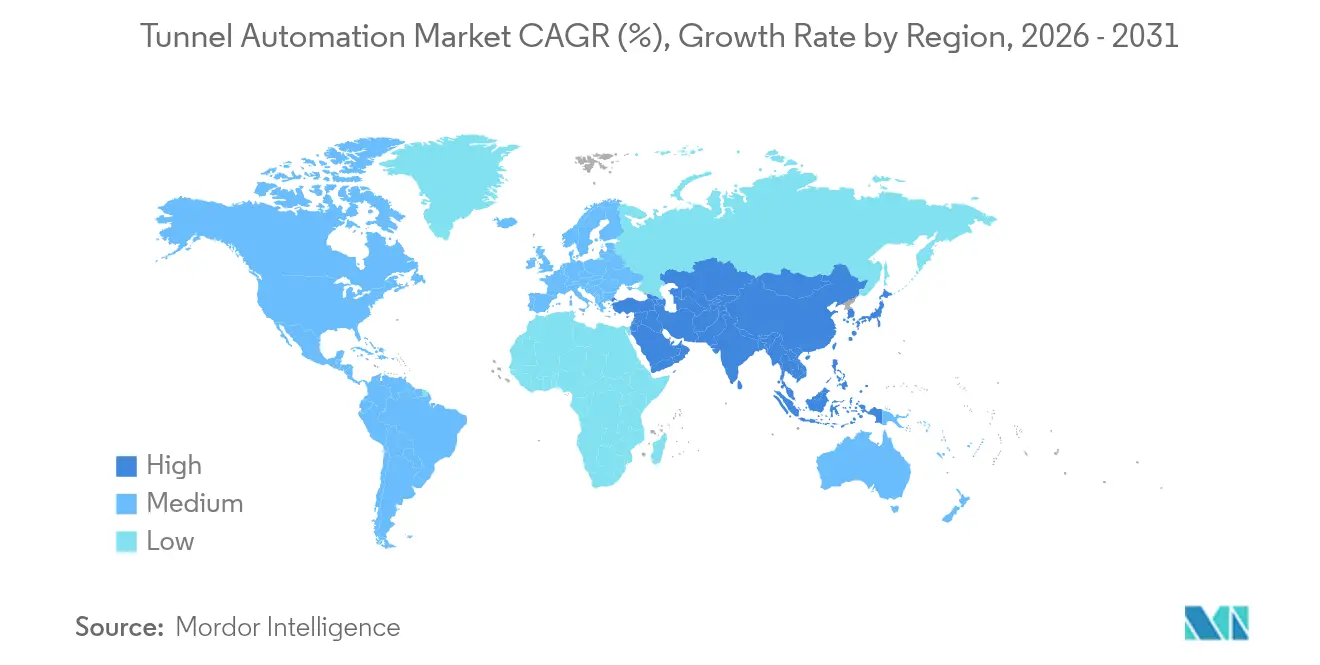

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tunnel Automation Market Analysis by Mordor Intelligence

The tunnel automation market size was valued at USD 5.06 billion in 2025 and estimated to grow from USD 5.47 billion in 2026 to reach USD 8.07 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031).[1]Federal Highway Administration, "National Tunnel Inspection Standards," ecfr.gov Intensifying regulatory mandates, widespread adoption of IoT-enabled supervisory control and data acquisition (SCADA) platforms, and sustained public-sector funding for transportation corridors are reinforcing the growth trajectory of the tunnel automation market. Hardware components remain indispensable, yet the market is rapidly pivoting toward software-rich, data-driven solutions that streamline maintenance, ensure real-time decision-making, and offset skilled labor shortages. Flexible financing models—especially energy-performance contracting—are also expanding adoption by converting capital expenditure into guaranteed operational savings. At the same time, heightened cyber-security and data-privacy standards are prompting operators to embed secure-by-design architectures across connected assets.

Key Report Takeaways

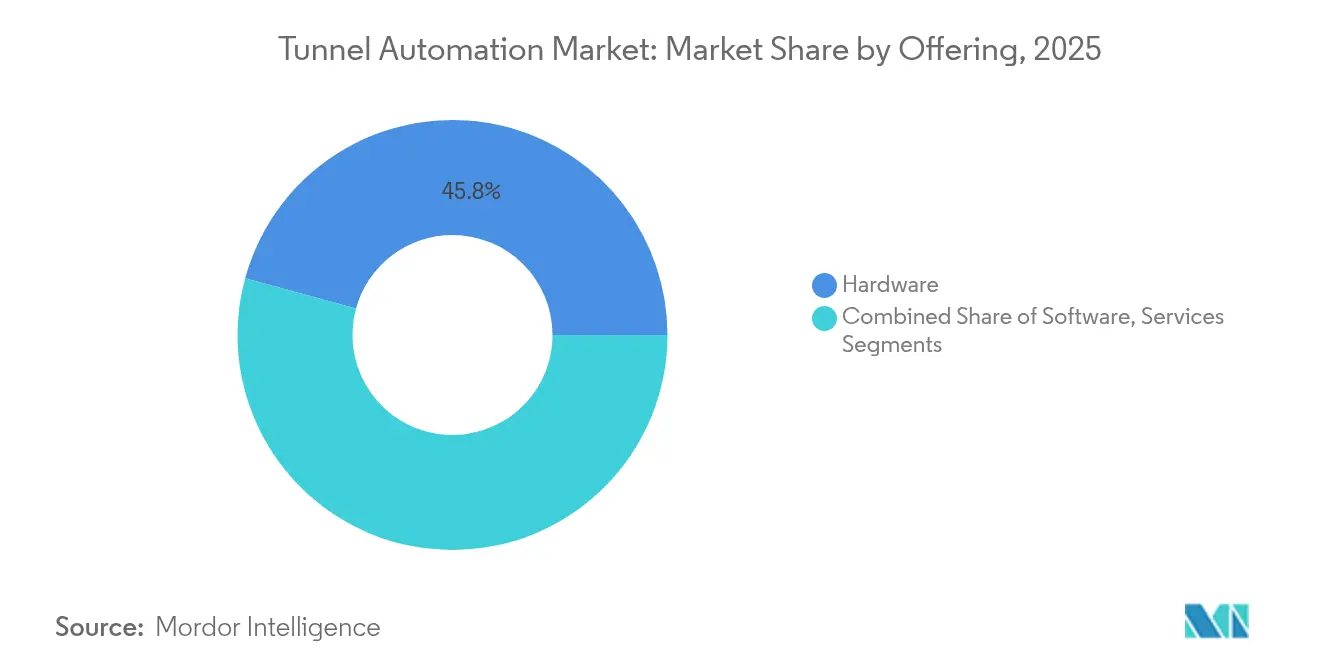

- By offering, hardware led with 45.75% revenue share in 2025, whereas software is forecast to grow at 9.62% CAGR through 2031, underscoring a decisive shift toward AI-driven capabilities.

- By component category, lighting and power supply systems captured 38.10% of the tunnel automation market share in 2025, while safety and fire-detection sensors are expected to expand at a 9.28% CAGR to 2031.

- By automation level, semi-automated installations accounted for 61.55% of the tunnel automation market in 2025, yet fully-automated systems are on track for the fastest 10.05% CAGR through 2031.

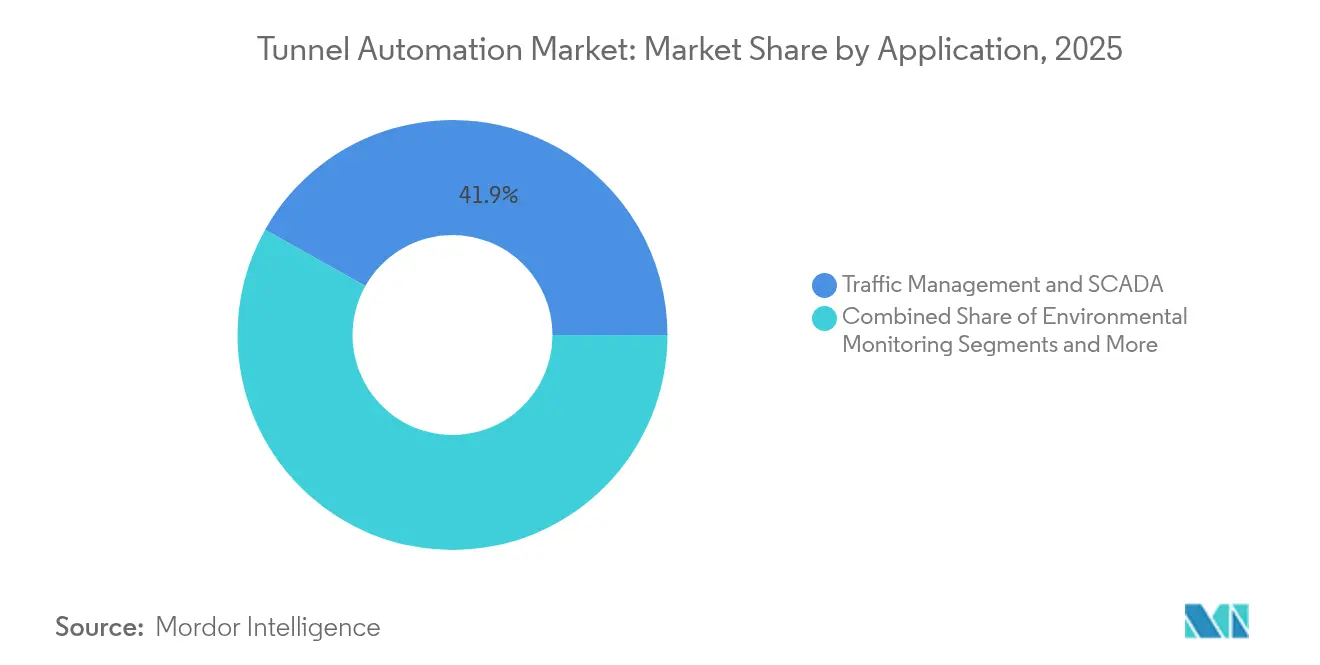

- By application, traffic management and SCADA solutions commanded 41.85% of revenue in 2025; environmental monitoring and ventilation platforms are projected to advance at a 9.33% CAGR between 2026 and 2031.

- By tunnel type, roadways and highways contributed 56.60% of 2025 volume, while railway and metro projects are forecast to enjoy the strongest 9.44% CAGR through 2031.

- By geography, Asia-Pacific held 42.10% of 2025 revenue; the Middle East is anticipated to achieve a 10.72% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Tunnel Automation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government regulations mandating tunnel safety and sustainability upgrades | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising integration of IoT-enabled SCADA and cloud analytics | +1.5% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Global surge in transportation infrastructure investments | +2.1% | APAC, Middle East, with selective EU projects | Long term (≥ 4 years) |

| AI-driven predictive lighting and ventilation optimisation | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Autonomous TBMs accelerating project timelines | +0.9% | APAC, selective North America projects | Long term (≥ 4 years) |

| Energy-performance-contracting models for legacy retrofit | +0.8% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Regulations Mandating Tunnel Safety and Sustainability Upgrades

Worldwide policy frameworks are accelerating the adoption curve of tunnel automation market deployments. The US National Tunnel Inspection Standards require biennial reviews and force operators to introduce automated safety systems, effectively creating a mandatory replacement cycle. Comparable directives within the Trans-European Transport Network compel projects like the Brenner Base Tunnel to employ advanced monitoring that can shift 50 million tonnes of freight from road to rail.[2]European Climate, Infrastructure and Environment Executive Agency, "Brenner Base Tunnel: shifting Alpine traffic from road to rail," cinea.ec.europa.euLegislated targets for energy savings add an environmental dimension by encouraging LED lighting retrofits and high-efficiency ventilation. China’s oversight bodies now require intelligent management across new expressways, as demonstrated by the Tianshan Shengli Tunnel’s in-house automation technology. The cumulative effect of these mandates is a sizeable, compliance-driven spending pool that shields capital budgets from typical deferment cycles.

Rising Integration of IoT-enabled SCADA and Cloud Analytics

Real-time analytics allow operators to reduce tunnel downtime by up to 40%, extending equipment life and aligning operations with predictive maintenance strategies. Siemens’ upgrades at Spain’s Somport Tunnel merged SIMATIC WinCC OA with redundant S7-1500H PLCs, delivering unified emergency and asset management. Advanced cloud platforms apply machine-learning algorithms to patterns in air-quality and equipment data, yet also widen the attack surface for malicious actors. Bridging this knowledge gap requires reskilling maintenance crews and formalizing cyber-security governance models that align operational technology (OT) with IT best practices.

Global Surge in Transportation Infrastructure Investments

Historic public-sector spending—exemplified by the Belt and Road Initiative, EUR 2.3 billion (USD 2.5 billion) contribution to the Brenner Base Tunnel, and Saudi Arabia’s NEOM smart-city megaproject—fuels demand for end-to-end automated solutions.[3]NEOM, "NEOM and Samsung C&T JV Announcement," neom.comAutonomous tunnel boring machines (TBMs), deployed for Sydney Metro West, underline how capital outlays are catalyzing product innovation and compressing construction timelines. Contracts based on performance metrics rather than equipment delivery are becoming the norm, transferring lifecycle risk to solution providers.

AI-driven Predictive Lighting and Ventilation Optimisation

Artificial intelligence now enables dynamic luminance tuning and smart ventilation, slashing energy consumption by up to 60% and cutting maintenance callouts. Signify’s LED rollout for Dublin Port Tunnel validates these gains with a demonstrable 60% electricity reduction. Integrating AI with building-information models improves failure prediction but necessitates robust sensor networks that can survive harsh, moisture-laden tunnel environments.

Restraints Impact Analysis of Tunnel Automation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and integration complexity | -1.4% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Cyber-security and data-privacy risks in connected assets | -0.8% | North America & EU regulatory focus, expanding globally | Medium term (2-4 years) |

| Fragmented procurement standards across transport agencies | -0.6% | Global, with regional variations in standards | Medium term (2-4 years) |

| Shortage of tunnel-automation talent in remote regions | -0.4% | Emerging markets, remote project locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Integration Complexity

Comprehensive automation requires significant capital, especially where legacy tunnels demand bespoke retrofit designs and phased rollouts that can stretch timelines by up to two years. US federal P100 standards for net-zero-ready facilities increase baseline specifications and thus initial budgets. [4]U.S. General Services Administration, "P100 Facilities Standards 2024," gsa.gov Energy-performance contracts partly offset these costs; Johnson Controls’ USD 5.8 million Cobb County program generated USD 2.06 million in utility savings, proving that guaranteed performance can unlock new funding channels. Persistent shortages of specialist technicians further complicate integration workstreams.

Cyber-security and Data-privacy Risks in Connected Assets

Connected SCADA architectures expose vital transport corridors to spoofing and denial-of-service attacks that jeopardize life-safety systems. Compliance with GDPR and emerging US state-level privacy acts raises additional burdens for operators collecting real-time environmental and traffic data. Lessons from autonomous haulage in mining reveal that OT environments need bespoke security protocols beyond conventional IT frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tunnel Automation Market Segment Analysis

By Offering:

Software Drives Next-Generation CapabilitiesHardware accounted for 45.75% of the tunnel automation market in 2025, reflecting the foundational need for sensors, controllers, and power infrastructure. Software, however, is set to outpace all other offerings with a 9.62% CAGR, propelled by AI-enabled analytics that facilitate predictive maintenance and autonomous decision-making.

Herrenknecht’s Connected platform illustrates the transition by tracking TBM performance globally and providing real-time insights that cut downtime. Services—installation, calibration, and lifecycle management—round out the portfolio and embody a rising share of recurring revenue as operators outsource expertise.

By Component:

Safety Systems Emerge as Growth LeadersLighting and power supply systems dominated with 38.10% share, emphasizing the importance of energy-efficient LEDs and smart power controls. Safety and fire-detection sensors are forecast to lead growth at 9.28% CAGR, aligned with stricter incident-prevention regulations.

ABB’s variable-speed ventilation drives inside Asia’s longest road tunnel exemplify component integration that enhances air-quality management while cutting energy costs ABB. The rising proliferation of multi-parameter sensors enables real-time structural health monitoring that was previously unattainable.

By Automation Level:

Fully-Automated Systems Gain MomentumSemi-automated solutions retained 61.55% share in 2025, mirroring operator preference for human oversight. Yet fully-automated platforms will record the fastest 10.05% CAGR as AI and machine-learning algorithms secure regulatory certification. The transition toward full automation is exemplified by Australia's deployment of autonomous tunnel boring machines for the Sydney Metro West project, representing the country's first fully autonomous TBM operation.

The automation level progression reflects technological maturity and regulatory acceptance of autonomous systems in critical infrastructure applications. Siemens Mobility's implementation of Communications-Based Train Control systems in Berlin's metro network demonstrates the pathway toward fully automated operations, with semi-automated systems serving as stepping stones to complete automation.

By Application:

Environmental Monitoring AcceleratesTraffic management and SCADA held 41.85% revenue in 2025, reflecting the need for centralized coordination across lighting, ventilation, and emergency systems. Environmental monitoring and ventilation platforms represent the fastest-growing segment at 9.33% CAGR, driven by stricter carbon-emission limits and the demand for healthier air quality inside urban tunnels.

AI-enabled ventilation algorithms have demonstrated up to 43.2% annual energy saving, helping operators contain rising electricity costs. Emergency and safety systems are experiencing steady growth driven by regulatory mandates and the need for comprehensive incident response capabilities that can coordinate with traffic management and environmental control systems.

By Tunnel Type:

Railways Drive Automation InnovationRoadways and highways contributed 56.60% of 2025 installations. Railway and metro tunnels, however, are projected to expand at a 9.44% CAGR as high-speed rail corridors and urban transit systems multiply.Water and utility conveyance tunnels, along with mining and energy applications, complete the tunnel type segmentation, each requiring specialized automation solutions.

Also, the 64-kilometer Brenner Base Tunnel will become the world’s longest underground railway and will rely on extensive automation to manage mixed passenger and freight traffic. Mining and energy tunnels are experiencing increased automation adoption driven by safety requirements and the need for remote monitoring capabilities in hazardous environments, with companies like Vale implementing IoT solutions to improve worker safety and operational efficiency

Geography Analysis

APAC Tunnel Automation Market

Asia-Pacific’s 42.10% hold on the tunnel automation market stems from relentless capital investment, state-backed industrial policies, and the widespread embrace of Industry 4.0 norms. China’s scale advantage enables shorter construction cycles, cutting project lead-times nearly in half through extensive automation, as demonstrated in Xinjiang’s Tianshan Shengli tunnel. Singapore’s Changi project underscores regional proficiency in integrating aviation infrastructure with state-of-the-art tunnel systems, while Australia’s autonomous TBMs confirm technical maturity. Public-private partnerships are standard, aligning operator incentives with long-run energy and safety objectives.

GCC Tunnel Automation Market

The Middle East is on a rapid ascent with a 10.72% CAGR outlook. Saudi Arabia’s Vision 2030 subsidizes large-scale, smart-city corridors where robotic fabrication, AI-assisted monitoring, and carbon-neutral targets converge. Qatar’s rail build-out and the UAE’s metro networks deploy modular tunnel packages that are pre-fitted with IoT sensors, reducing on-site configuration. Competitive procurement frameworks prioritize vendors that can deliver turnkey, fully integrated ecosystems.

Europe Tunnel Automation Market

Europe sustains measured growth supported by strict compliance regimes and cross-border megaprojects. The Brenner Base Tunnel attracts EU co-funding for modal-shift objectives, while Germany’s SüdLink electricity link uses Herrenknecht TBMs to lay power conduits that decarbonize the grid. Brownfield retrofits dominate, particularly LED replacements that achieve documented 60% energy savings.

Competitive Landscape

The tunnel automation market features moderate fragmentation, with industrial automation conglomerates and niche specialists vying for strategic primacy. Siemens AG, ABB Ltd, and Johnson Controls command extensive portfolios that combine hardware, software, and maintenance, positioning them to bid on turnkey contracts.

Meanwhile, Herrenknecht AG and SICK AG excel in high-value niches such as TBMs and environmental sensors, often partnering with larger players to expand global reach. Partnership activity is intensifying; SICK’s alliance with Endress+Hauser widens service coverage across process analyzers. Business models increasingly revolve around lifecycle service agreements and data-analytics subscriptions, securing annuity revenues while locking-in clients.

Investment in AI, cyber-secure architectures, and cloud connectivity remains the primary differentiation axis. Siemens AG committed roughly 8% of its FY 2024 revenue to R&D, reflecting its prioritization of predictive analytic platforms and digital twins Siemens AG. White-space opportunities persist in emerging regions where local players lack the depth to compete on integrated solutions. Regulatory credentials have also become a decisive tender prerequisite, favoring incumbents with proven safety certifications and cyber-resilience capabilities.

Tunnel Automation Industry Leaders

-

Siemens AG

-

Johnson Controls Inc.

-

ABB Limited

-

SICK AG

-

Signify Holding BV

- *Disclaimer: Major Players sorted in no particular order

Tunnel Automation Market Companies Covered in this Report

- Siemens AG

- ABB Ltd

- Johnson Controls International plc

- Signify Holding B.V.

- SICK AG

- SICE Tecnologíay Sistemas

- Agidens NV

- Indra Sistemas S.A.

- Advantech Co., Ltd.

- CODEL International Ltd

- Herrenknecht AG

- Schréder Group

- Nyx Hemera Technologies

- Tunnelsoft GmbH

- Epiroc AB

- Sandvik AB

- CRCHI (China Railway Construction Heavy Industry)

- CREC (Holding)

- LNSS China

- Phoenix Contact GmbH

- SITECO GmbH

Recent Industry Developments in Tunnel Automation Market

- February 2025: Siemens Mobility, in consortium with Leonhard Weiss, secured a €2.8 billion (USD 3.0 billion) contract with Deutsche Bahn to deliver modern control and safety technology across Germany’s network, reinforcing Siemens’ shift toward long-duration volume agreements.

- January 2025: Siemens Mobility won four HS2 contracts totaling €670 million (USD 708 million) that include Automatic Train Operations and Engineering Management Systems, extending its UK footprint and strengthening the company’s systems-integration credentials.

- January 2025: Epiroc and ABB executed an MoU to co-develop underground trolley systems for mining, aiming to co-deliver electrification and decarbonization at scale.

- December 2024: NEOM and Samsung C&T invested SAR 1.3 billion (USD 347 million) to deploy robotics that automate rebar-cage production, signaling the region’s readiness to scale construction automation.

Global Tunnel Automation Market Report Scope

Tunnels are underground passages used for transportation of freights, passengers, water, sewage, etc. Tunnel automation provides optimal solutions for heating, ventilation, and air conditioning, as well as signaling, lighting, emergency response, and surveillance. The use of tunnel automation can help reduce human error and improve economic profitability while providing a safe working environment. The scope of the study is limited to the types of tunnels such as railways and highways, and roadways. The market study doesn't offer a drill down breakup of the regional shares for the countries.

Segmentation Overview

| Hardware |

| Software |

| Services |

| Lighting and Power Supply |

| Signalisation and Control |

| HVAC and Ventilation |

| Safety / Fire-Detection Sensors |

| Other Components |

| Semi-Automated |

| Fully-Automated |

| Traffic Management and SCADA |

| Environmental Monitoring and Ventilation |

| Lighting Control |

| Emergency and Safety Systems |

| Roadways and Highways |

| Railways and Metros |

| Water and Utility Conveyance |

| Mining and Energy |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| ASEAN-5 | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Hardware | ||

| Software | |||

| Services | |||

| By Component | Lighting and Power Supply | ||

| Signalisation and Control | |||

| HVAC and Ventilation | |||

| Safety / Fire-Detection Sensors | |||

| Other Components | |||

| By Automation Level | Semi-Automated | ||

| Fully-Automated | |||

| By Application | Traffic Management and SCADA | ||

| Environmental Monitoring and Ventilation | |||

| Lighting Control | |||

| Emergency and Safety Systems | |||

| By Tunnel Type | Roadways and Highways | ||

| Railways and Metros | |||

| Water and Utility Conveyance | |||

| Mining and Energy | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| ASEAN-5 | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current tunnel automation market size and growth outlook?

The tunnel automation market size stood at USD 5.47 billion in 2026 and is expected to reach USD 8.07 billion by 2031, reflecting an 8.12% CAGR.

Which region leads the tunnel automation market today?

Asia-Pacific leads with 42.10% of global revenue in 2025 due to sustained infrastructure investment in China, Singapore, and Australia.

What segment is growing fastest within tunnel automation?

Software solutions are expanding at a 9.62% CAGR as operators transition toward AI-driven, predictive platforms.

Why are safety sensors a focal component for investment?

Heightened regulatory scrutiny has made real-time detection of fire, smoke, and structural anomalies essential, propelling safety sensors to a 9.28% CAGR trajectory.

Heightened regulatory scrutiny has made real-time detection of fire, smoke, and structural anomalies essential, propelling safety sensors to a 9.28% CAGR trajectory.

Energy-performance contracts convert capital outlays into guaranteed operating savings, as demonstrated by Johnson Controls’ USD 5.8 million Cobb County initiative.

What is the principal risk factor hampering tunnel automation deployments?

Cyber-security vulnerabilities in connected SCADA networks pose significant operational and compliance challenges, especially in regions with strict data privacy laws.

Page last updated on: