Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 120.65 Billion |

| Market Size (2031) | USD 154.92 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

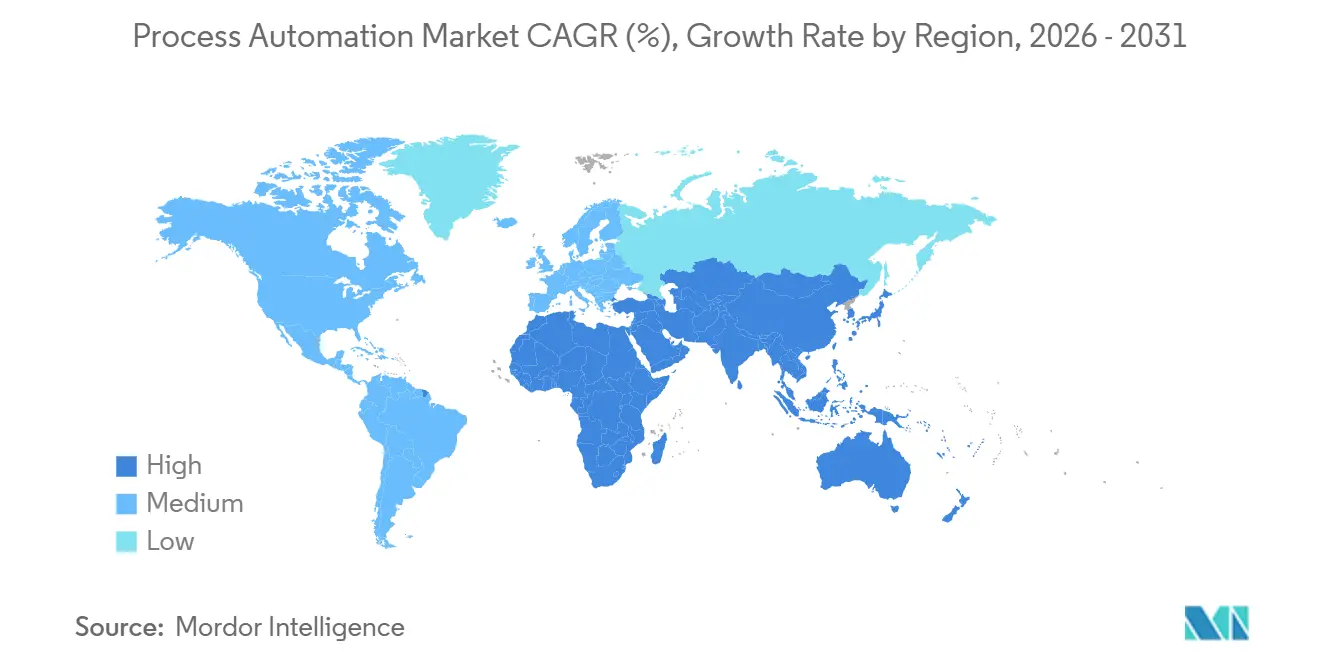

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Process Automation Market Analysis by Mordor Intelligence

The process automation market size is projected to expand from USD 114.84 billion in 2025 and USD 120.65 billion in 2026 to USD 154.92 billion by 2031, registering a 5.13% CAGR between 2026 to 2031. The growth curve reflects a broad pivot from reactive maintenance toward predictive, software-defined control architectures that embed artificial intelligence at the edge. Capital budgets are shifting away from cyclic hardware replacements and toward subscription-based manufacturing execution platforms that shorten time-to-insight. Compliance mandates such as pharmaceutical serialization and refinery flare-gas recovery continue to accelerate digital-twin adoption, while petrochemical operators retrofit distributed control systems to optimize volatile feedstock yields. Convergence of operational technology with cloud-native analytics is also expanding the addressable base for edge gateways and secure connectivity layers.

Key Report Takeaways

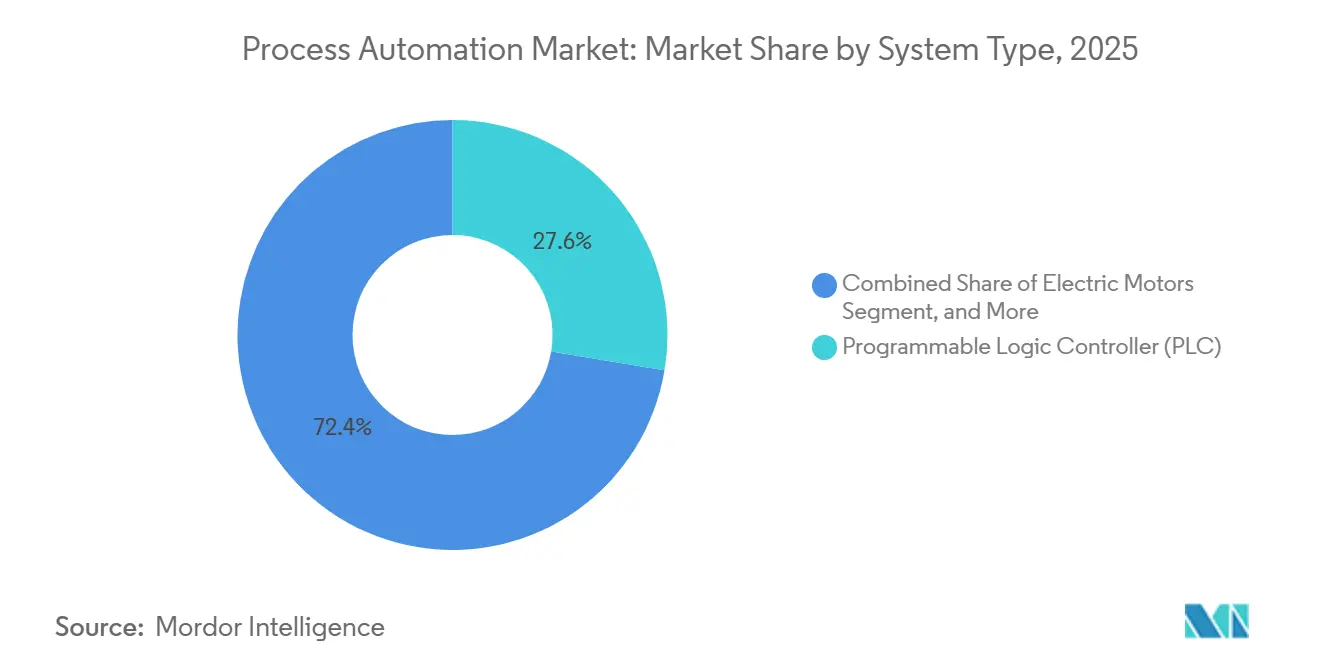

- By system type, programmable logic controllers led with 27.63% of the process automation market share in 2025, while manufacturing execution systems are forecast to expand at a 5.29% CAGR through 2031.

- By communication protocol, wired links commanded 63.72% of the process automation market in 2025, whereas wireless deployments are projected to grow at a 5.18% CAGR through 2031.

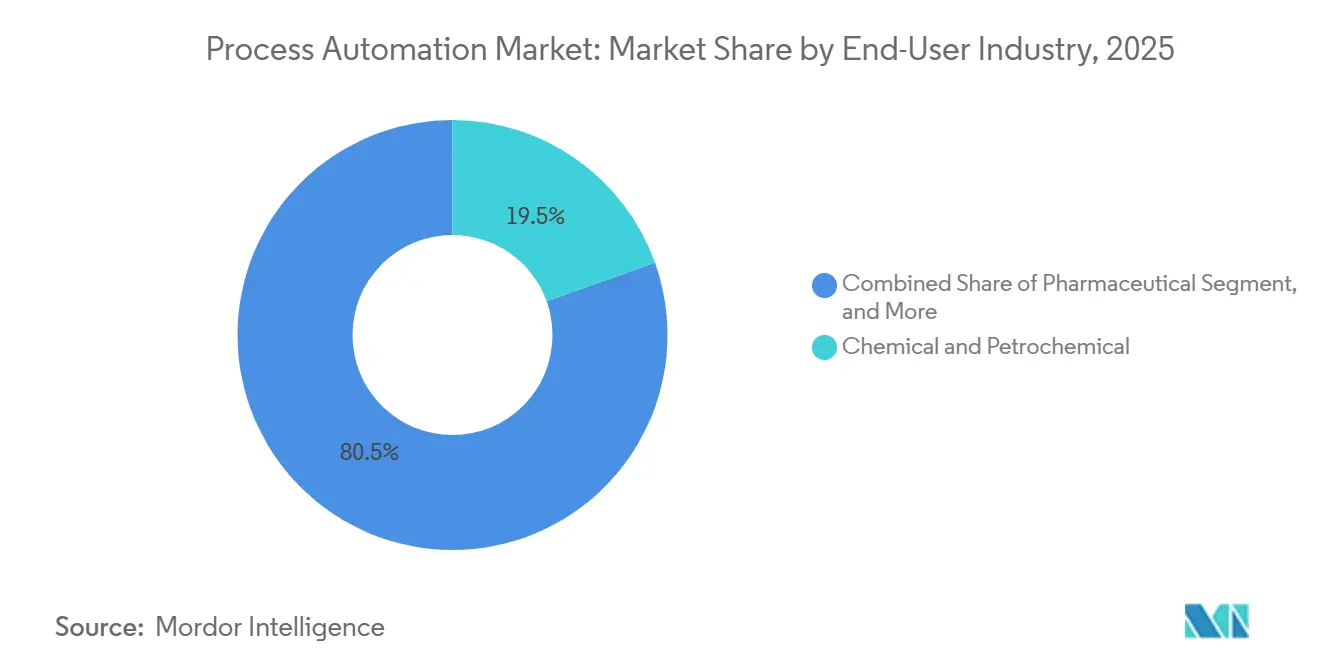

- By end-user industry, chemical and petrochemical plants held 19.53% of the process automation market share in 2025, and the pharmaceutical segment is advancing at a 5.32% CAGR over the same horizon.

- By deployment mode, on-premises installations accounted for 70.81% of the process automation market in 2025, while cloud architectures are set to grow at a 5.22% CAGR through 2031.

- By geography, North America captured 33.28% of revenue in 2025, and the Asia Pacific is poised to record a 5.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Process Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Robotics | +0.7% | Global, Asia-Pacific leading | Medium term (2-4 years) |

| Growing Emphasis on Energy Efficiency and Cost Reduction | +0.8% | Europe and North America, spillover to Middle East | Short term (≤ 2 years) |

| Emergence of Industrial Internet of Things (IIoT) | +0.9% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Demand for Safety Automation Systems | +0.6% | Global, stringent in Europe and North America | Long term (≥ 4 years) |

| Rise of AI-Driven Predictive Maintenance Platforms | +0.8% | North America and Europe early adopters, Asia-Pacific scaling | Medium term (2-4 years) |

| Regulatory Push Toward Carbon-Neutral Manufacturing | +0.7% | Europe leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Robotics

Industrial robot installations hit 553,052 units in 2024, with Asia Pacific accounting for 73% of deployments.[1]International Federation of Robotics, “World Robotics 2025 – Industrial Robots,” IFR.org Collaborative robots now handle hazardous materials and aseptic fills, reducing ergonomic injuries while maintaining compliance with stringent exposure limits. Talent shortages in remote petrochemical hubs are prompting operators to assign machine-vision-equipped robots to flange inspection and valve actuation. A joint study found that pairing robotics with digital-twin simulations accelerates new-product ramp-up by 22%. Early pilots of humanoid robots in pharmaceutical cleanrooms are underway, with the robots moving items between isolators without breaching Grade A conditions.

Growing Emphasis on Energy Efficiency and Cost Reduction

The European Union earmarked EUR 150 billion (USD 169.5 billion) to decarbonize heavy industry by 2040, explicitly funding upgrades such as variable-frequency drives.[2]European Union, “Clean Industrial Deal,” Europa.eu The United States Department of Energy identified process heating as 68% of manufacturing energy use and recommended model-predictive control for furnaces. Deployments of AI-driven thermal-management software have cut natural-gas consumption by 14% and delivered payback in less than 18 months, according to vendor filings. Integrated energy-management systems tied directly to distributed control networks have achieved 19% utility savings compared with standalone platforms.

Emergence of Industrial Internet of Things (IIoT)

IIoT architectures are evolving from star topologies to edge-fog hierarchies that preprocess sensor data locally, slashing cloud egress charges and enabling sub-50-millisecond control loops.[3]Institute of Electrical and Electronics Engineers, “Edge Computing for Industrial IoT: A Review,” Ieee.org Private 5G now underpins autonomous guided vehicles in smart factories, with a flagship installation unveiled in March 2025. Time-sensitive networking standards enable deterministic Ethernet across both safety and analytics traffic, validated by multi-vendor testbeds. Hybrid wired-wireless frameworks are thus increasingly feasible for the process automation market, allowing mobile sensors to coexist with legacy fieldbus assets.

Demand for Safety Automation Systems

Regulatory scrutiny is intensifying after incident investigations linked 23% of major chemical releases to inadequate safety-layer independence. Updated ISA-84 guidance stresses proof-test intervals aligned with probabilistic risk assessments, which is boosting demand for smart positioners and partial-stroke testing valves. Turnkey safety PLC platforms that integrate seamlessly with distributed control systems continue to win high-hazard projects; one vendor captured contracts at 12 LNG terminals in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital and Integration Complexity | −0.5% | Global, acute in brownfield sites | Short term (≤ 2 years) |

| Cybersecurity Vulnerabilities in OT Networks | −0.4% | Global, heightened in critical infrastructure | Medium term (2-4 years) |

| Shortage of Domain-Specific Automation Talent | −0.3% | North America and Europe most affected | Long term (≥ 4 years) |

| Legacy Brownfield Interoperability Pitfalls | −0.3% | Global, concentrated in mature industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital and Integration Complexity

Brownfield automation projects routinely exceed budgets by 30-40% due to unforeseen protocol mismatches, prompting 62% of North American plants to cite capital constraints as a barrier, despite attractive paybacks. Multi-vendor environments magnify complexity, and hourly rates for system integrators have climbed 18% since 2024. Operators are weighing cloud subscriptions that convert CapEx to OpEx, yet skepticism persists in jurisdictions with strict data-sovereignty rules.

Cybersecurity Vulnerabilities in OT Networks

In 2025, federal authorities issued 47 advisories addressing vulnerabilities in industrial control systems. Fourteen distinct threat groups are actively targeting operational technology, posing significant risks to critical infrastructure. Notably, only 34% of sites have implemented robust IT-OT segmentation, leaving the majority exposed to potential cyber threats. Furthermore, many facilities, already constrained by budgetary pressures, face a challenging financial and operational predicament. Frequent hardware replacements are often required because legacy PLCs lack the capability to support modern encryption standards, further straining resources and operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: MES Gains as Real-Time Traceability Becomes Non-Negotiable

Manufacturing execution systems experienced the fastest growth trajectory in the process automation market, expanding at a 5.29% CAGR as serial-number traceability and lot genealogy move from optional to mandatory in pharmaceuticals and food production. Programmable logic controllers safeguard their 27.63% market share in core motor and valve loops, yet face commoditization pressure as software-defined control gains mindshare.

Distributed control systems remain indispensable in continuous operations such as refining, where hundreds of loops demand unified historian access and alarm rationalization. Supervisory control and data acquisition platforms cover geographically dispersed pipelines and water utilities, while edge-native human-machine interfaces on tablets and AR headsets trim operator workload. Siemens’ unified PCS neo release exemplifies the push to consolidate control and safety functions on a virtualized backbone, thereby shrinking cabinet footprints and simplifying spares management.

By Communication Protocol: Wireless Ascends as Private 5G Matures

Wired Ethernet, fieldbus, and fiber links maintained a dominant 63.72% share of the process automation market in 2025, thanks to deterministic latency and electromagnetic immunity. Wireless connections are projected to grow at a compound annual growth rate (CAGR) of 5.18%, driven by the adoption of private 5G slices. These slices provide guaranteed sub-10-millisecond service levels, which are critical for enabling advanced applications such as mobile robotics and augmented reality (AR) maintenance.

WirelessHART and ISA100.11a support brownfield retrofits without recabling, offering migration paths that appeal to cash-constrained operators. Time-sensitive networking bridges wired and wireless domains by synchronizing endpoints within microseconds, validated in a cross-vendor testbed that delivered servo-class performance. Heightened cybersecurity scrutiny means wireless nodes now ship with WPA3 encryption and certificate management baked in, mitigating the perception gap between copper and air.

By End-User Industry: Pharmaceutical Segment Accelerates on Continuous Manufacturing

Chemical and petrochemical plants held 19.53% of the process automation market share in 2025, anchored by large installed bases of reactors, crackers, and distillation trains. Digital-twin overlays are now designed to model feedstock volatility effectively, facilitating real-time, minute-by-minute set-point adjustments. These adjustments enhance operational efficiency by optimizing yields and achieving measurable reductions in carbon emissions.

The pharmaceutical segment is forecast to record a 5.32% CAGR through 2031, driven by U.S. FDA guidance endorsing continuous manufacturing. Continuous lines integrate process analytical technology and real-time release testing, necessitating high-speed data historians and secure cloud replication. Water utilities, pulp mills, and food processors follow suit, albeit with distinct compliance clocks that modulate investment pacing.

By Deployment Mode: Cloud Gains Ground as Hybrid Architectures Prove Viable

In 2025, on-premises configurations represented a significant 70.81% share of the process automation market, primarily driven by persistent concerns regarding latency and data custody. At the same time, hybrid topologies are experiencing rapid adoption, contributing to a projected 5.22% compound annual growth rate (CAGR) for cloud deployments. This growth is supported by the implementation of edge gateways, which efficiently process large volumes of sensor data and transmit only the most relevant insights for further analysis.

Global cloud hyperscalers have introduced comprehensive bundled reference architectures designed to encrypt data both during transit and while at rest. These solutions help streamline audit compliance for facilities operating under IEC 62443 standards. Although European data-sovereignty regulations necessitate the use of regional nodes, the deployment of distributed edge clusters effectively addresses most latency-sensitive operational requirements. Simultaneously, these clusters enable the seamless integration of scalable and advanced analytics capabilities in the background.

Geography Analysis

North America contributed 33.28% of 2025 revenue, anchored by petrochemical retrofits along the Gulf Coast and water-utility SCADA upgrades funded by the Infrastructure Investment and Jobs Act. A maturing installed base of 1990-era control systems is approaching end-of-support, driving replacements that incorporate encrypted protocols and zero-trust segmentation. Canada’s oil-sands operators apply edge analytics to steam-assisted gravity drainage, trimming natural-gas demand when Henry Hub prices spike above USD 3 per MMBtu. Mexico’s aerospace and automotive clusters deploy manufacturing execution systems for rules-of-origin traceability under the USMCA framework.

Asia Pacific will expand at a 5.44% CAGR through 2031, propelled by China’s 14th Five-Year Plan, which has already certified more than 2,100 lighthouse factories. India’s production-linked incentives subsidize automation in pharmaceuticals and food, speeding adoption among small and medium-sized firms. Japan’s Society 5.0 vision taps collaborative robots and AR headsets to mitigate labor shortages amid a population that is 29% over 65 years old. South Korea’s semiconductor fabs implement advanced process control at 3-nanometer nodes, demonstrating that deterministic loop closure is achievable on converged Ethernet backbones.

Europe enforces energy-monitoring and cybersecurity-by-design mandates via the Clean Industrial Deal and the draft Cyber Resilience Act. Germany’s 2025 budget channels EUR 10 billion (USD 11.3 billion) into variable-frequency drives and heat-recovery schemes. The United Kingdom’s Advanced Manufacturing Plan offers innovation loans for digital twins, aiming to achieve net-zero manufacturing outcomes by 2040. South America, the Middle East, and Africa trail in installed base yet host megaprojects such as Saudi Arabia’s NEOM and Brazil’s deepwater presalt fields, which specify IEC 62443 compliance from day one.

Competitive Landscape

The process automation market is moderately concentrated: the top five suppliers, ABB, Siemens, Schneider Electric, Emerson Electric, and Rockwell Automation, collectively hold about 40% of global revenue. Each incumbent is pivoting toward software-as-a-service pricing, bundling analytics, remote support, and cybersecurity patching into multiyear subscriptions that deepen lock-in. Rockwell’s FactoryTalk hub and Siemens’ Industrial Operations X are flagships of this transition, offering low-code workflow designers and Git-native version control.

Mid-tier challengers such as Beckhoff Automation and WAGO accelerate adoption among cost-sensitive SMEs with PC-based controllers that leverage commercial off-the-shelf silicon. Patent activity in 2024-2025 shows a surge in edge-AI inference chips hardened for −40 °C to +85 °C operation, opening new possibilities for on-sensor analytics without backhaul latency. Vendors that bundle commissioning, operator training, and managed cybersecurity services consistently outcompete hardware-only bids because plant managers increasingly evaluate the lifetime cost of ownership rather than sticker price.

Interoperability is the primary white space: protocol gateways that bridge PROFIBUS, Modbus, and EtherNet/IP without introducing single points of failure or command premium pricing. IEC 62443 zone-and-conduit segmentation is now a mandatory checkbox in bid specifications, with vendors racing to certify products across multiple profiles. Start-ups advocating software-defined control promise portable logic across vendor ecosystems, appealing to operators weary of proprietary lock-in, yet proof points in Safety Integrity Level 3 environments remain scarce.

Process Automation Industry Leaders

ABB Ltd.

Dassault Systemes SE

Eaton Corporation plc

Emerson Electric Co.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Siemens committed EUR 2 billion (USD 2.26 billion) to expand its Amberg Electronics Plant, integrating generative-AI inspection and autonomous material handling.

- November 2025: Schneider Electric completed its EUR 1.8 billion (USD 2.03 billion) acquisition of Planon Group, extending EcoStruxure into facility management.

- October 2025: ABB partnered with Covariant to embed foundation AI models in industrial robots for adaptive pharmaceutical packaging.

- September 2025: Rockwell Automation launched FactoryTalk Design Studio 2.0, a cloud-native collaborative engineering suite.

Global Process Automation Market Report Scope

The Process Automation Market Report is Segmented by System Type (Supervisory Control and Data Acquisition (SCADA), Programmable Logic Controller (PLC), Distributed Control System (DCS), Manufacturing Execution System (MES), Valves and Actuators, Electric Motors, Human Machine Interface (HMI), Process Safety Systems, Sensors and Transmitters, Other System Types), Communication Protocol (Wired Protocol, and Wireless Protocol), End-User Industry (Chemical and Petrochemical, Paper and Pulp, Water and Wastewater Treatment, Energy and Utilities, Oil and Gas, Pharmaceutical, Food and Beverages, Other End-User Industries), Deployment Mode (On-premise, and Cloud-based), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By System Type

| Supervisory Control and Data Acquisition (SCADA) |

| Programmable Logic Controller (PLC) |

| Distributed Control System (DCS) |

| Manufacturing Execution System (MES) |

| Valves and Actuators |

| Electric Motors |

| Human Machine Interface (HMI) |

| Process Safety Systems |

| Sensors and Transmitters |

| Other System Types |

By Communication Protocol

| Wired Protocol |

| Wireless Protocol |

By End-User Industry

| Chemical and Petrochemical |

| Paper and Pulp |

| Water and Wastewater Treatment |

| Energy and Utilities |

| Oil and Gas |

| Pharmaceutical |

| Food and Beverages |

| Other End-User Industries |

By Deployment Mode

| On-premise |

| Cloud-based |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| Italy | |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By System Type | Supervisory Control and Data Acquisition (SCADA) | |

| Programmable Logic Controller (PLC) | ||

| Distributed Control System (DCS) | ||

| Manufacturing Execution System (MES) | ||

| Valves and Actuators | ||

| Electric Motors | ||

| Human Machine Interface (HMI) | ||

| Process Safety Systems | ||

| Sensors and Transmitters | ||

| Other System Types | ||

| By Communication Protocol | Wired Protocol | |

| Wireless Protocol | ||

| By End-User Industry | Chemical and Petrochemical | |

| Paper and Pulp | ||

| Water and Wastewater Treatment | ||

| Energy and Utilities | ||

| Oil and Gas | ||

| Pharmaceutical | ||

| Food and Beverages | ||

| Other End-User Industries | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| Italy | ||

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the process automation market by 2031?

The process automation market is projected to reach USD 154.92 billion by 2031.

Which region will record the fastest growth through 2031?

Asia Pacific is expected to grow at a 5.44% CAGR, the quickest among all regions.

Which system type is expanding most rapidly?

Manufacturing execution systems are forecast to post a 5.29% CAGR as real-time traceability becomes mandatory.

How large is the wired segment within current architectures?

Wired protocols held 63.72% of 2025 revenue, reflecting the preference for deterministic latency.

Why is cloud adoption accelerating in industrial plants?

Hybrid edge-cloud models cut upfront capital, enable scalable analytics, and still meet latency targets, pushing cloud deployments toward a 5.22% CAGR.

What is the biggest challenge to wider automation rollout?

High initial capital outlays and integration complexity, particularly in brownfield sites, remain the primary barriers despite attractive paybacks.

Page last updated on: