Market Overview

| Study Period | 2019 - 2030 |

|---|---|

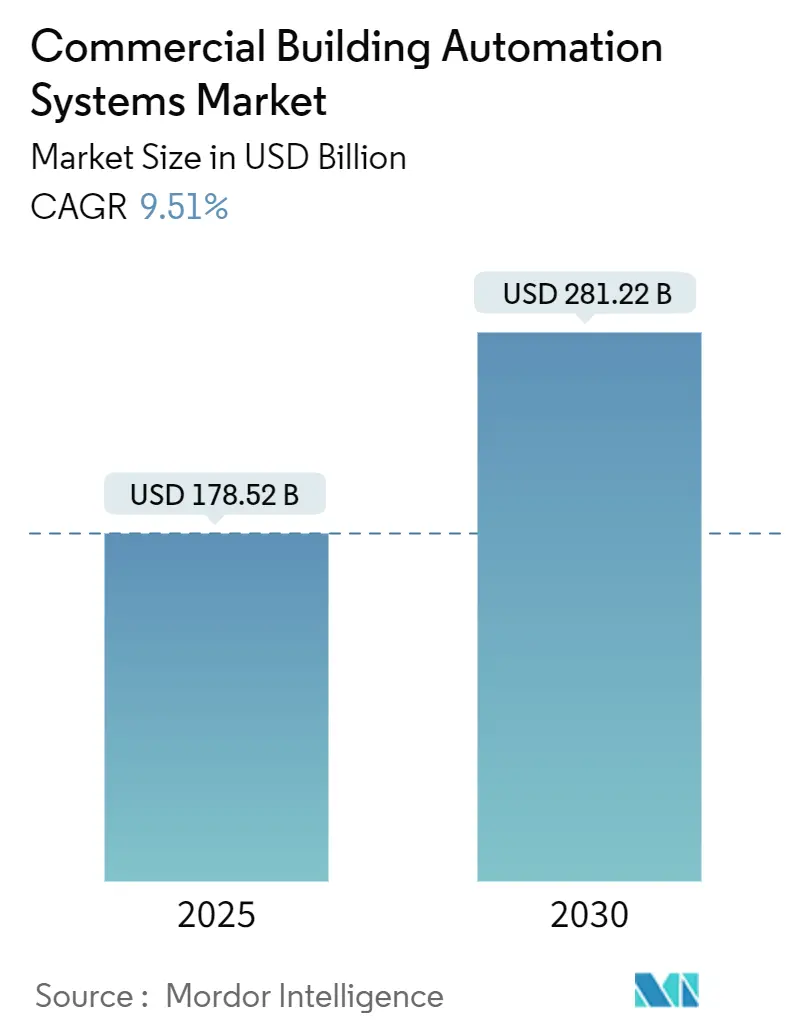

| Market Size (2025) | USD 178.52 Billion |

| Market Size (2030) | USD 281.22 Billion |

| Growth Rate (2025 - 2030) | 9.51% CAGR |

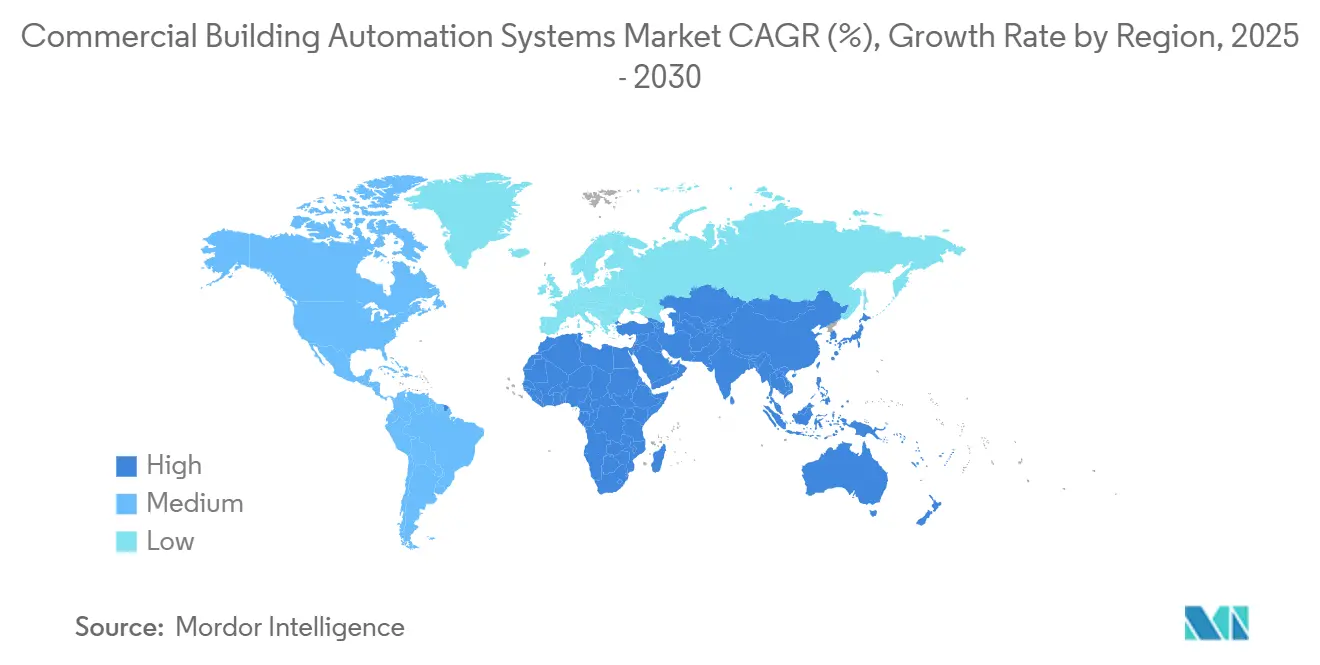

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Building Automation Systems Market Analysis by Mordor Intelligence

The commercial building automation systems market is valued at USD 178.52 billion in 2025 and is forecast to reach USD 281.22 billion by 2030, expanding at a 9.51% CAGR. Demand accelerates as artificial intelligence now augments building controls, regulators tighten energy-efficiency mandates, and real estate owners seek quantifiable ESG outcomes. Owners retrofit legacy stock to cut utility bills and to satisfy the European Union’s zero-emission building targets, while North American tax incentives offset upfront costs. Rapid cloud adoption enables remote monitoring services, and green bond issuances channel new capital into smart building upgrades. Competitive intensity rises as traditional conglomerates integrate AI modules and start-ups pitch autonomous optimisation tools that promise double-digit energy savings.[1]U.S. Securities and Exchange Commission, “Proposed Climate-Related Disclosures,” sec.gov

Key Report Takeaways

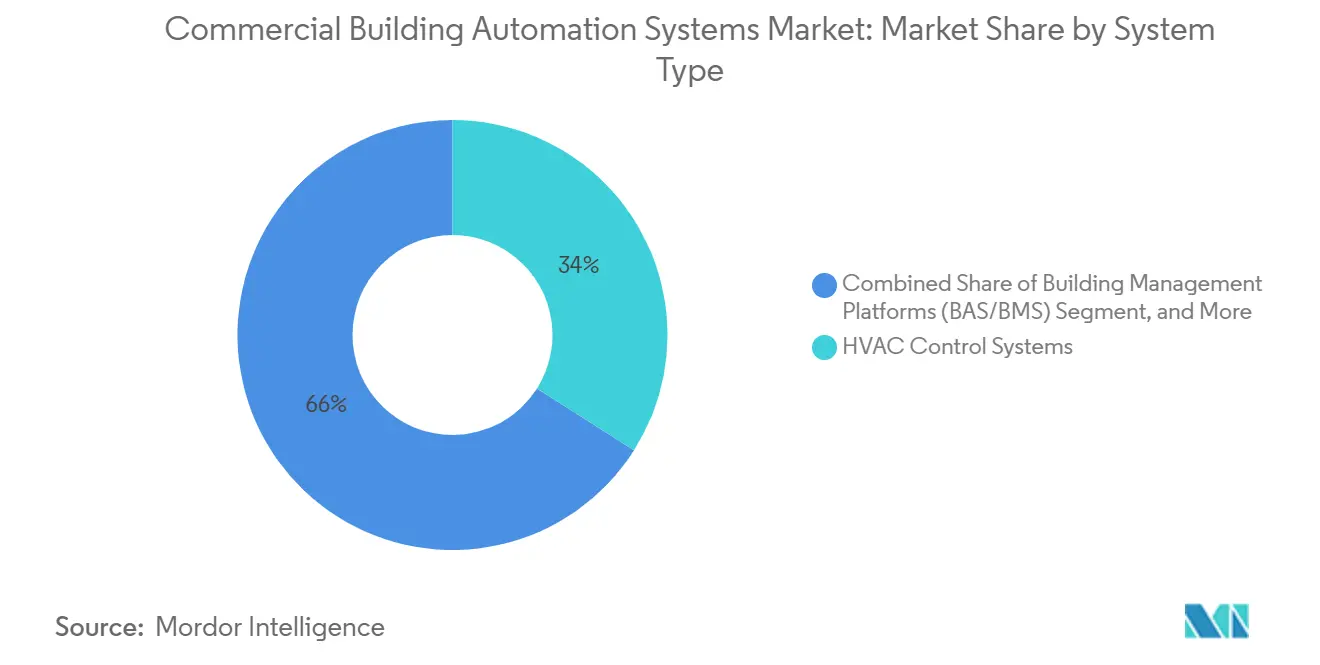

- By system type, HVAC control systems led with 34.0% of the commercial building automation systems market share in 2024, while AI-enabled fault detection and diagnostics is projected to advance at an 10.67% CAGR through 2030.

- By building type, office buildings held 28.1% of the commercial building automation systems market share in 2024, whereas healthcare facilities are projected to show the fastest growth, with a 10.61% CAGR to 2030.

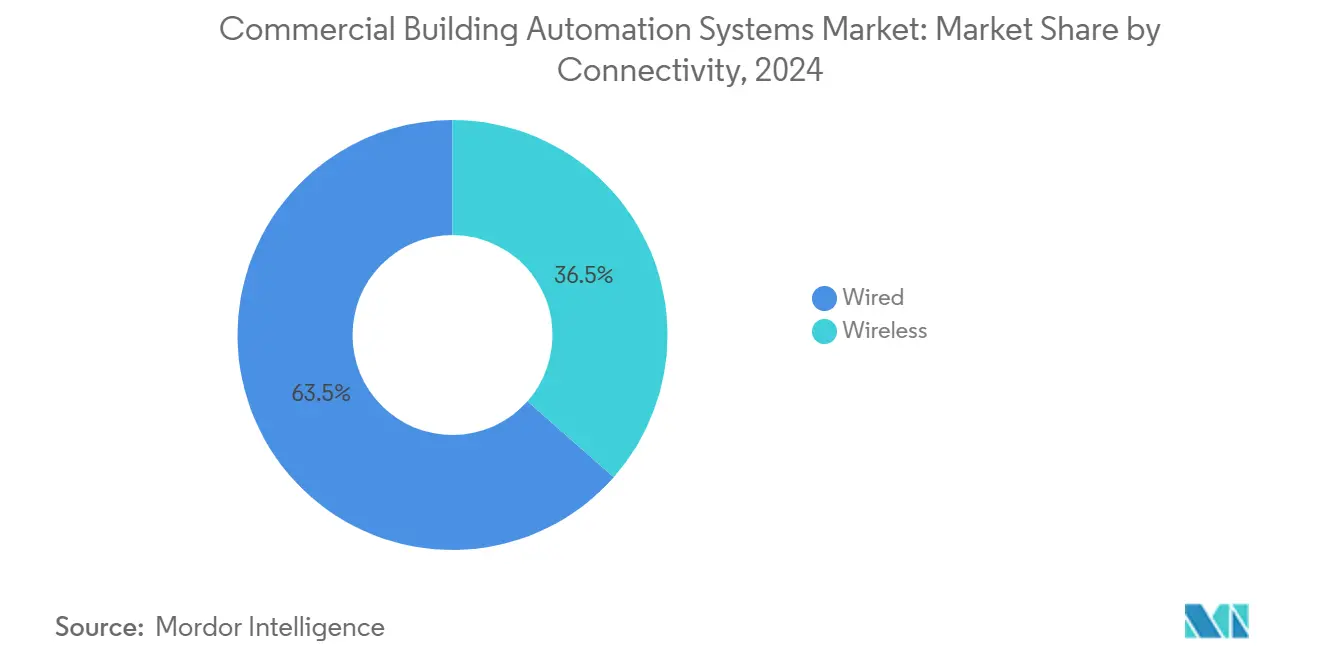

- By connectivity, wired BACnet commanded a 63.5% market share of the commercial building automation systems market in 2024; however, wireless LoRa is projected to grow at a 9.79% CAGR.

- By service type, installation and integration accounted for 46.2% of the commercial building automation systems market share in 2024, and managed and cloud services are forecast to rise at a 9.89% CAGR.

- By geography, North America captured 37.8% of the commercial building automation systems market share in 2024, while Asia-Pacific is poised for the highest 10.77% CAGR through 2030.

Global Commercial Building Automation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising energy-efficiency regulations | +2.10% | Global, with EU leading implementation | Medium term (2-4 years) |

| Mandatory ESG reporting for listed real-estate trusts (REITs) | +1.80% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Accelerated retro-commissioning of aging HVAC stock | +1.50% | North America core, spill-over to EU | Long term (≥ 4 years) |

| Convergence of OT and IT via BACnet/IPv6 | +1.30% | Global, with advanced markets first | Medium term (2-4 years) |

| AI-enabled fault detection and diagnostics (FDD) | +1.90% | Global, concentrated in smart cities | Short term (≤ 2 years) |

| Growing green-bond financing for smart buildings | +0.90% | Global, with Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy-Efficiency Regulations

The revised Energy Performance of Buildings Directive obliges all new European buildings to meet zero on-site fossil-fuel emissions by 2030 and makes automation mandatory for non-residential systems above 70 kW. This single policy expands the commercial building automation systems market because owners must install smart controls to demonstrate compliance with the directive’s Smart Readiness Indicator. Similar rules in California and Singapore mirror the European model, signalling global convergence toward compulsory automation. Investors interpret these mandates as de-risking signals, so capital flows shift toward projects that already embed advanced control platforms. Vendors now bundle compliance reporting dashboards with every new controller, reducing customer friction and accelerating upgrade cycles.

Mandatory ESG Reporting for Listed Real-Estate Trusts

REITs must disclose granular energy data under the EU Corporate Sustainability Reporting Directive and soon under proposed US SEC climate rules. Green bonds totalling USD 12 billion issued by REITs in 2024 require ongoing performance verification that legacy meters cannot deliver. As a result, the commercial building automation systems market becomes a compliance-driven procurement priority, transforming smart controls from optional efficiency upgrades into core fiduciary infrastructure. Cloud dashboards now provide automated audit trails that streamline annual sustainability reports and lower the cost of capital for owners with transparent energy metrics.

Convergence of OT and IT via BACnet / IPv6

BACnet Secure Connect encrypts traffic with Transport Layer Security and supports IPv6 addressing, allowing building devices to sit securely on corporate IT networks. Direct internet connectivity permits large-scale sensor deployments without complex proprietary gateways and slashes commissioning labour. Operators gain real-time visibility across multi-site portfolios, which boosts demand for analytics subscriptions. These developments lift the commercial building automation systems market by overcoming past cyber-security objections in healthcare and critical infrastructure.[2]Automated Logic, “BACnet Secure Connect Technical Brief,” automatedlogic.com

AI-Enabled Fault Detection and Diagnostics (FDD)

Artificial-intelligence modules embedded in modern controllers analyse sensor streams and predict anomalies before they escalate into costly failures. Case studies show energy savings of 25% and greenhouse-gas reductions of 40%, figures that quickly justify retrofit budgets. Johnson Controls’ OpenBlue platform now uses generative AI to recommend 130 categories of optimisation actions that can trim utility bills by 30% and cut maintenance costs 20%. Vendors bundle FDD with cloud dashboards, allowing regional facilities managers to supervise multi-site portfolios from a single screen. Insurance providers have begun offering premium discounts when autonomous diagnostics are in place, further accelerating uptake. As smart-city programs scale, municipal building codes increasingly reference predictive maintenance standards, embedding FDD into procurement specifications and lifting near-term demand across all major regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security certification gaps for legacy BMS | -1.40% | Global, acute in critical infrastructure | Short term (≤ 2 years) |

| Split-incentive dilemma in leased commercial space | -1.10% | Global, pronounced in mature markets | Medium term (2-4 years) |

| Shortage of trained system integrators | -1.70% | Global, severe in North America | Long term (≥ 4 years) |

| Volatile semiconductor supply for controller boards | -1.20% | Global, concentrated in Asia supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Certification Gaps for Legacy BMS

Older building management systems seldom meet current cyber-security benchmarks. Owners must either fund expensive custom protections or accept elevated risk, delaying upgrade decisions. Healthcare operators face the sharpest dilemma because patient-critical systems cannot tolerate breaches yet must still hit energy targets. Standardisation efforts such as BACnet Secure Connect are helpful, but widespread retrofits demand capital and skilled integrators, both in short supply.

Shortage of Trained System Integrators

he HVAC trade needs 500,000 extra workers each year, while the pool of certified technicians has halved over the past decade. Project timelines slip when qualified labour is unavailable, limiting the commercial building automation systems market. Manufacturers now run academy programs and develop low-code configuration tools to reduce labour intensity, yet the demographic gap between retiring experts and incoming graduates remains wide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: AI Integration Extends HVAC Leadership

HVAC controls held 34.0% of 2024 revenue, the largest slice of the commercial building automation systems market. Energy-saving mandates and ageing chillers trigger retrofit waves. AI-enabled fault detection and diagnostics grows at 10.67% CAGR because predictive insights cut maintenance bills by up to 20%. Building management platforms gain traction as cloud migration centralises dashboards for ESG auditing. Security, lighting, and energy-metering systems integrate through common APIs, creating cross-selling openings.

The commercial building automation systems market size for AI-enabled modules is on course to almost triple by 2030 as algorithms become standard features on new controllers. Vendors embed self-learning models that recalibrate setpoints daily, delivering quick payback periods that appeal to cash-constrained owners. As interoperability improves, buyers increasingly favour holistic platforms able to orchestrate HVAC, lighting, blinds, and access across a single user interface.[3]Johnson Controls, “OpenBlue Platform Delivers Predictive Savings,” johnsoncontrols.com

By Building Type: Healthcare Growth Surpasses Office Base

Office buildings contributed 28.1% of revenue in 2024, reflecting an extensive installed base that now upgrades systems to meet hybrid-work comfort expectations. Healthcare’s 10.61% CAGR is the fastest because infection-control guidelines demand precise air-exchange rates and humidity controls. A single US children’s hospital saved USD 681,000 annually after automating its utility plant. Retail and hospitality chains adopt AI optimisation to match energy use with fluctuating occupancy, while universities invest in campus-wide upgrades tied to decarbonisation pledges.

The commercial building automation systems market size for healthcare facilities widens as funding programs offset capital costs for critical-care upgrades. Owners value real-time indoor-air-quality dashboards that help earn well-building accreditations and reduce liability. As these requirements tighten, vendors position integrated suites that bundle HVAC, lighting, and security into outcome-based service contracts.[4]LoRa Alliance, “Building Automation Case Studies,” lora-alliance.org

By Connectivity: Wireless Protocols Complement Wired Backbone

Wired BACnet retained 63.5% share in 2024 because mission-critical sites still prioritise deterministic performance. Wireless LoRa, however, expands at 9.79% CAGR, offering kilometre-scale range and decade-long battery life that simplify retrofits. Wi-Fi and Zigbee support bandwidth-heavy cameras and dense lighting meshes respectively. Thread gains traction in new construction for its IPv6 native stack and strong security.

Hybrid deployments dominate the commercial building automation systems market. Gateways translate between wired and wireless segments so owners can add sensors without replacing existing trunks. One mixed-protocol deployment saved USD 45,000 a year and trimmed energy consumption 45% in its first twelve months.

By Service Type: Cloud Platforms Shift Budgets from CapEx to OpEx

Installation and integration accounted for 46.2% of 2024 revenue, yet managed services expand at 9.89% CAGR as owners prefer pay-as-you-save contracts. A cloud-hosted platform recently delivered 7.3% savings during initial commissioning and up to 25% during full remote control for a Californian client. Performance-based agreements guarantee outcomes, so vendors assume optimisation responsibility and finance upgrades through shared-savings models.

Subscription growth lifts recurring revenue and raises switching costs, reinforcing vendor lock-in. The commercial building automation systems market size for managed services benefits from plummeting sensor prices and secure remote access that reduce on-site visit requirements. Providers bundle analytics, compliance reporting, and cyber-security updates in one monthly fee, simplifying procurement for asset managers.

Geography Analysis

North America led with 37.8% revenue share in 2024. Federal tax credits offset retrofit costs and mature distributor networks shorten delivery times. Ageing commercial stock and rising utility rates sustain upgrade demand.

The commercial building automation systems market in Asia-Pacific grows fastest at 10.77% CAGR. Rapid urbanisation in China and India drives new builds that specify smart controls from the blueprint stage. China’s smart-building standard GB/T 39190-2020 sets IoT requirements that increase baseline specifications for controls.

Europe remains a solid growth region as revised energy directives compel zero-emission targets and system integrations. Government retrofit funds subsidise sensors and analytics layers. South America and the Middle East and Africa show emerging potential tied to commercial construction booms and rising awareness of green-building certifications. Multinationals acquire regional distributors to secure early mover advantage, as evidenced by ABB’s USD 150 million wiring-accessory buy in China.

Competitive Landscape

The commercial building automation systems market features moderate fragmentation. Siemens, Schneider Electric, and Johnson Controls anchor global footprints with end-to-end portfolios, yet nimble AI specialists disrupt pricing and feature expectations. Bosch’s USD 8 billion purchase of Johnson Controls’ HVAC division shows incumbents doubling down on integrated solutions. Trane Technologies secured BrainBox AI to fold generative optimisation into its chiller range.

Traditional players market reliability, global service teams, and life cycle guarantees. New entrants emphasise cloud-native stacks that update weekly and provide API access for third-party apps. Patent filings rise for autonomous optimisation and encrypted transport protocols, signalling a race to lock in software differentiation.

Strategic alliances accelerate product rollouts. Honeywell bundles cybersecurity services with each access-control sale and trains reseller channels on threat-monitoring add-ons. Schneider Electric funds partner programs that certify local integrators on its edge-AI controllers, addressing labour shortages. Vendors target underserved small-to-medium buildings with wireless retrofit kits that install in days and pay back inside three years, widening addressable demand.

Commercial Building Automation Systems Industry Leaders

Siemens AG

Schneider Electric SE

Johnson Controls International plc

Honeywell International Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ABB closed the acquisition of Siemens’ Wiring Accessories business in China, adding USD 150 million revenue.

- April 2025: Johnson Controls reported a 155% three-year ROI for its OpenBlue platform in a Forrester study.

- March 2025: BrainBox AI launched ARIA, a generative AI assistant that cuts HVAC energy up to 25%.

- February 2025: Schneider Electric unveiled SpaceLogic Touchscreen Room Controller with 35% energy-saving potential.

Global Commercial Building Automation Systems Market Report Scope

The Commercial Building Automation Systems Market is Segmented by System Type (HVAC Control Systems, Building Management Platforms (BAS/BMS), Security and Access Control, Energy Management and Metering, Lighting Control), Building Type (Offices, Retail and Mixed-Use, Hospitality, Healthcare Facilities, Educational Campuses), Connectivity (Wired, and Wireless), Service Type (Consulting and Audit, Installation and Integration, Managed and Cloud Services) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By System Type

| HVAC Control Systems |

| Building Management Platforms (BAS/BMS) |

| Security and Access Control |

| Energy Management and Metering |

| Lighting Control |

By Building Type

| Offices |

| Retail and Mixed-Use |

| Hospitality |

| Healthcare Facilities |

| Educational Campuses |

By Connectivity

| Wired (BACnet MS/TP, KNX, Modbus) |

| Wireless (Wi-Fi, Zigbee, Thread, LoRa) |

By Service Type

| Consulting and Audit |

| Installation and Integration |

| Managed and Cloud Services |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By System Type | HVAC Control Systems | ||

| Building Management Platforms (BAS/BMS) | |||

| Security and Access Control | |||

| Energy Management and Metering | |||

| Lighting Control | |||

| By Building Type | Offices | ||

| Retail and Mixed-Use | |||

| Hospitality | |||

| Healthcare Facilities | |||

| Educational Campuses | |||

| By Connectivity | Wired (BACnet MS/TP, KNX, Modbus) | ||

| Wireless (Wi-Fi, Zigbee, Thread, LoRa) | |||

| By Service Type | Consulting and Audit | ||

| Installation and Integration | |||

| Managed and Cloud Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the commercial building automation systems market?

The commercial building automation systems market size stands at USD 178.52 billion in 2025.

How fast will the commercial building automation systems market grow through 2030?

The market is forecast to expand at a 9.51% CAGR, reaching USD 281.22 billion by 2030.

Which system type leads market revenue today?

HVAC control systems lead with a 34.0% share, reflecting mandatory efficiency upgrades.

Why is Asia-Pacific the fastest-growing region?

Rapid urbanisation in China and India and supportive smart-building standards propel an 10.77% CAGR in Asia-Pacific.

What role does artificial intelligence play in building automation?

AI-enabled fault detection and diagnostics can cut energy use by up to 25% and is the fastest-growing segment at 10.67% CAGR.

Which connectivity technology is growing fastest for retrofits?

Wireless LoRa shows a 9.79% CAGR because it covers long distances, uses little power, and minimizes disruption during installation.

Page last updated on: