Dog Dental Chews Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 0.78 Billion |

| Market Size (2030) | USD 1.14 Billion |

| Growth Rate (2025 - 2030) | 7.86% CAGR |

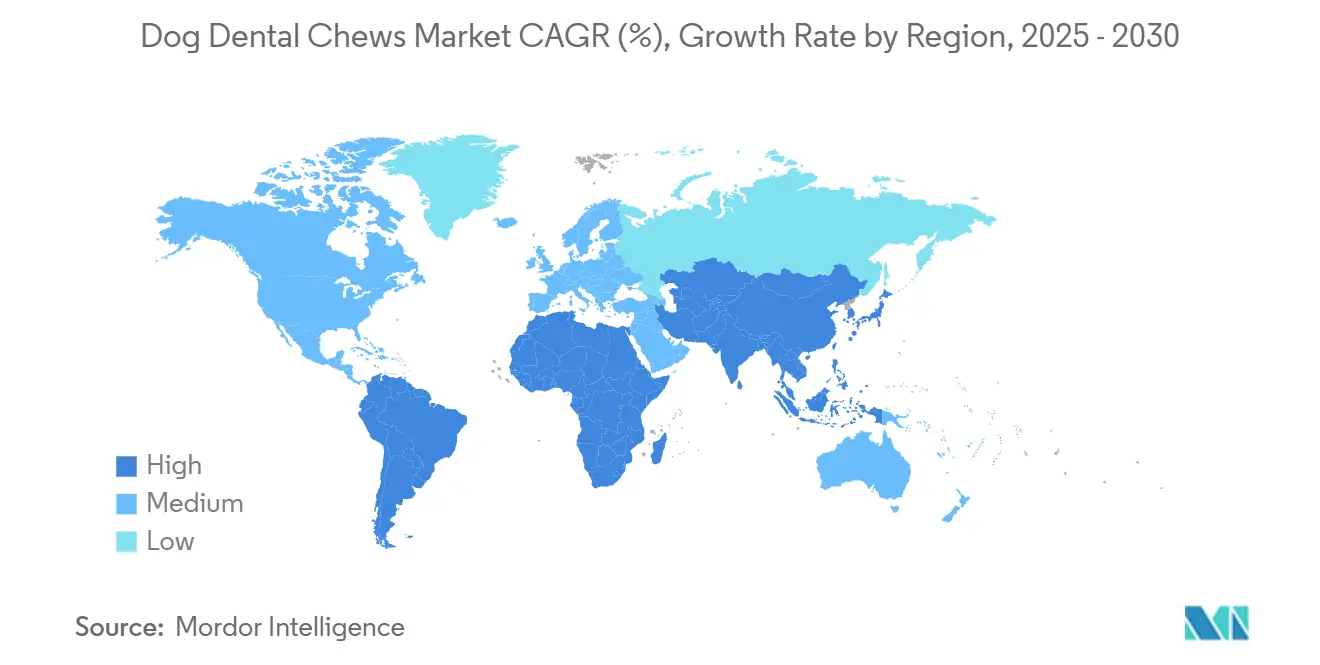

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

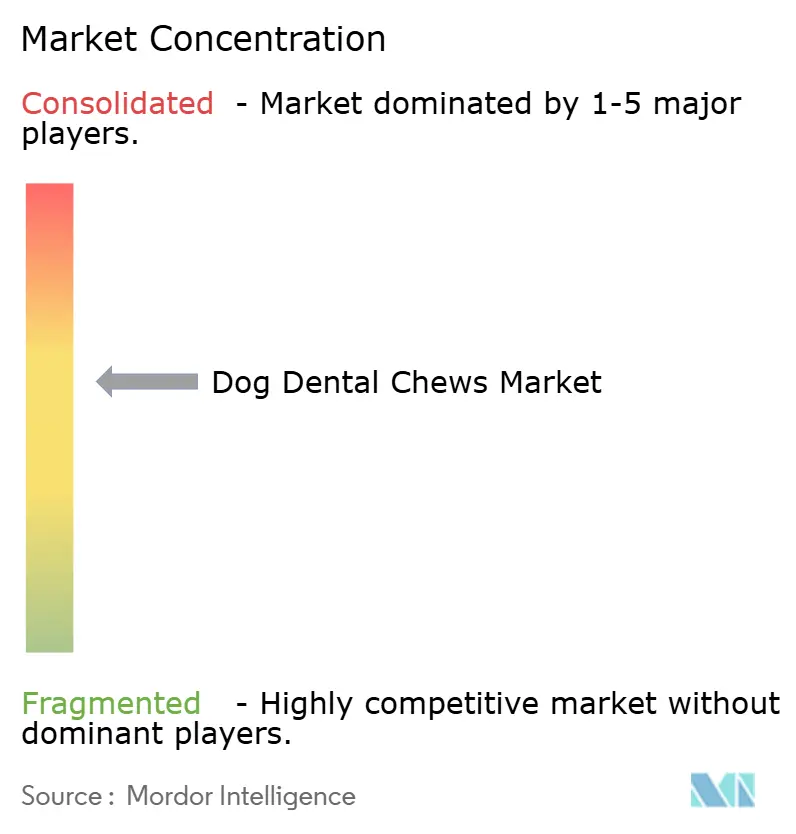

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dog Dental Chews Market Analysis by Mordor Intelligence

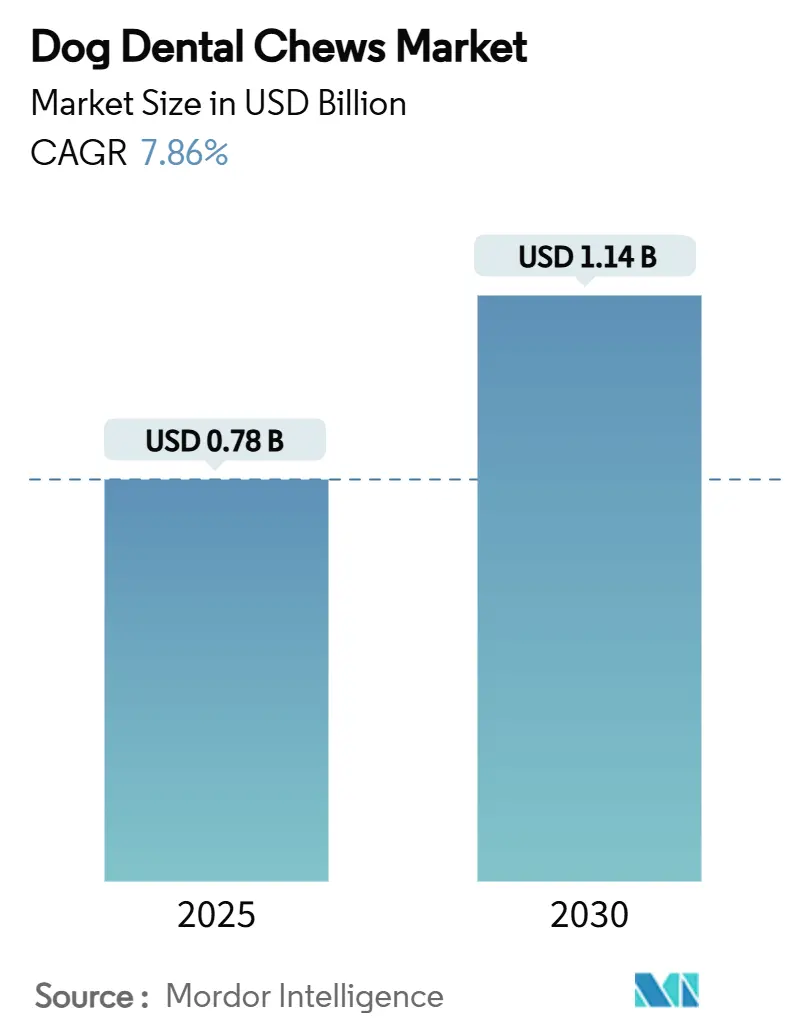

The dog dental chews market size stands at USD 0.78 billion in 2025 and is forecast to reach USD 1.14 billion by 2030, advancing at a 7.86% CAGR. Robust growth rests on rising veterinary awareness, accelerating pet humanization, and the fact that 80% of dogs over three years suffer from periodontal disease. North America commands today’s largest share, while Asia-Pacific is on track for the fastest-growing region through 2030 as Chinese and Indian pet owners steer spending toward functional oral-care treats. Stick-shaped chews dominate product form preferences, and probiotic variants post the fastest gains, and online subscription services reshape repeat-purchase behavior. Meanwhile, regulatory uncertainty around efficacy claims and safety concerns tied to rawhide continues to test product development agility.

Key Report Takeaways

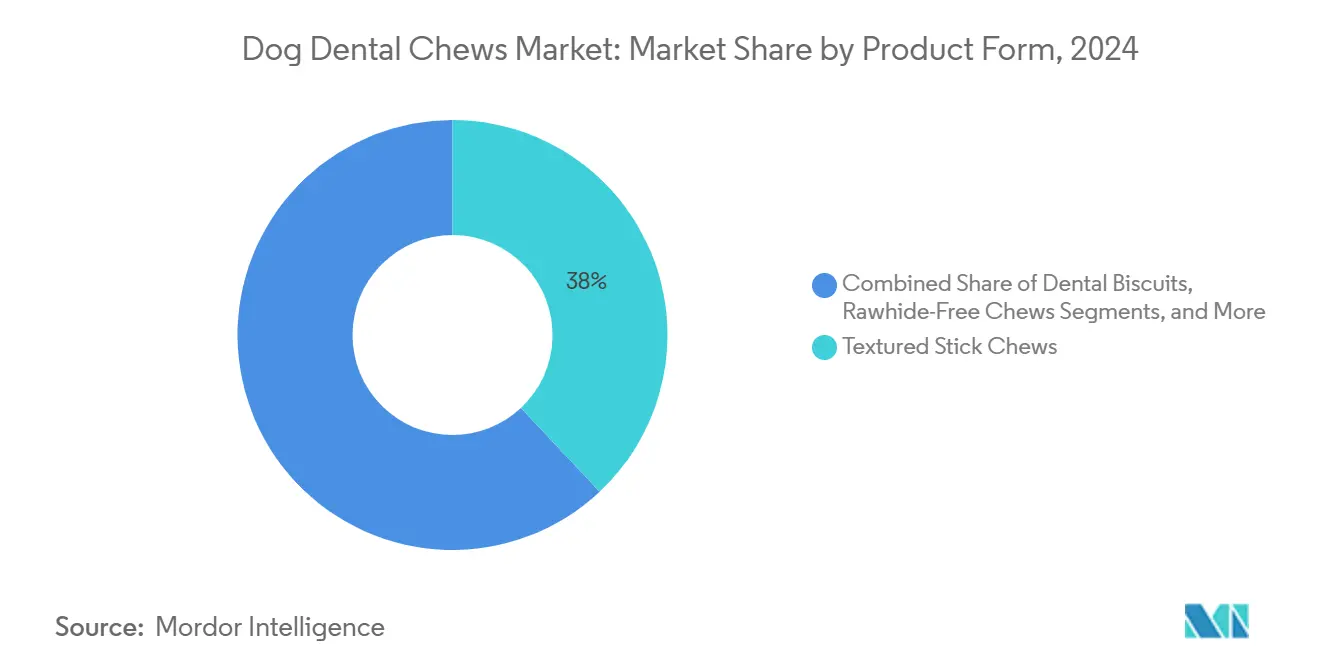

- By product form, the textured stick chews held 38.0% of the dog dental chews market share in 2024, and the functional and supplement chews are projected to rise at a 9.80% CAGR through 2030.

- By ingredient source, the animal-based commanded 52.0% of the dog dental chews market size in 2024, while plant-based is set to expand at a 10.90% CAGR to 2030.

- By dog size, the small dogs accounted for 44.0% of 2024 revenues, but products for large dogs are on course for a 8.50% CAGR between 2025 and 2030.

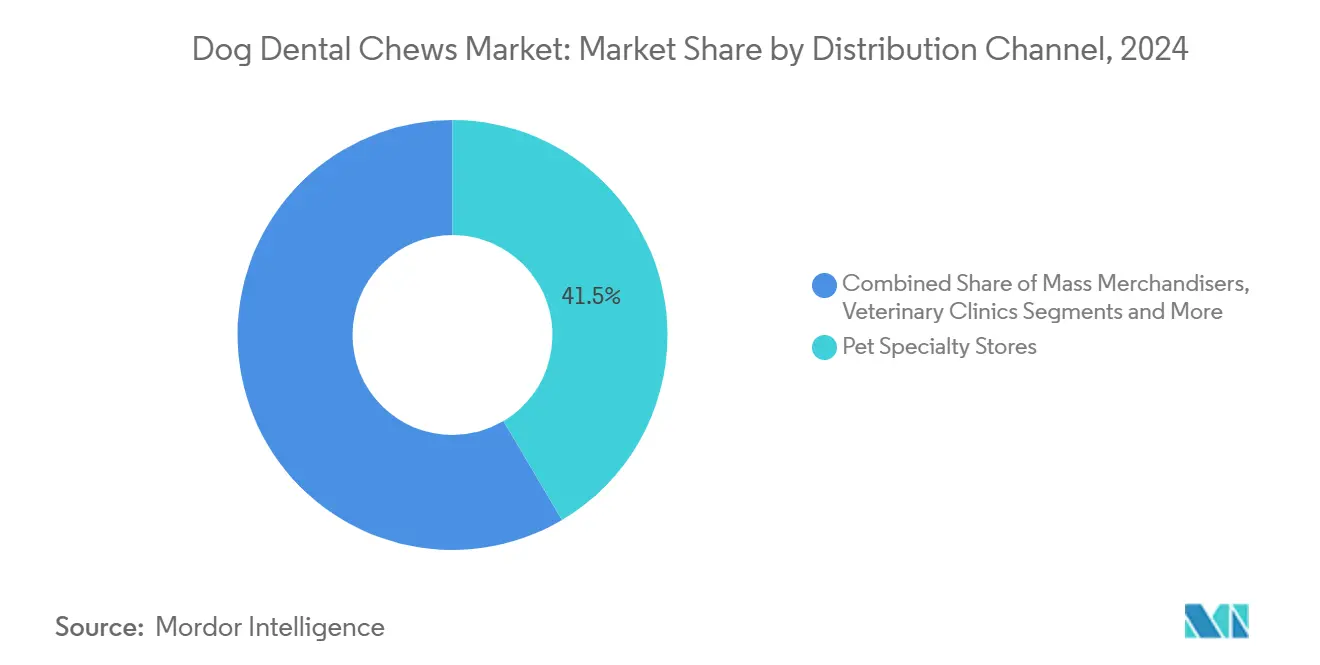

- By distribution channel, the pet specialty stores captured 41.5% of 2024 sales, and the online retail and subscription boxes are forecast to post an 11.20% CAGR through 2030.

- By geography, North America held a 42% market share in 2024, while the Asia-Pacific region is growing at a CAGR of 7.6% through 2030.

- The top five companies jointly held 62.8% of the total revenue shares in 2024.

Global Dog Dental Chews Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of periodontal disease in dogs | +2.1% | Global | Medium term (2-4 years) |

| Humanization and premiumization of dog treats | +1.8% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Veterinary endorsements and Veterinary Oral Health Council (VOHC) seal adoption | +1.4% | North America and Europe | Medium term (2-4 years) |

| E-commerce subscription model accelerates repeat purchases | +1.2% | Global, and strongest in North America | Short term (≤ 2 years) |

| Infusion of functional ingredients (probiotics, CBD) | +0.9% | North America and Europe | Medium term (2-4 years) |

| Sustainability push toward plant-based chew formats | +0.6% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Periodontal Disease in Dogs

More than 73% of dogs present dental problems during routine check-ups, prompting owners to view preventive chews as affordable substitutes for USD 170–350 professional cleanings. The Veterinary Oral Health Council (VOHC)-validated products that cut plaque by at least 20% strengthen the medical footing of daily chews, remove the “treat” stigma, and foster demand even when budgets tighten. The disease’s link to systemic heart, liver, and kidney complications further broadens the addressable audience beyond cosmetic care.

Humanization and Premiumization of Dog Treats

Pet owners increasingly embrace human-grade ingredients, organic seals, and elegant packaging that mirrors grocery-aisle cues. Premium lines embed narratives around ethical sourcing and sustainability, enabling brands to treat pricing as a health investment rather than a snack purchase. Multi-benefit chews combining oral care with digestive or anxiety relief widen Stock Keeping Unit (SKU) breadth and profit margins as millennials and Gen Z treat pets like family members.

Veterinary Endorsements and Veterinary Oral Health Council (VOHC) Seal Adoption

Third-party Veterinary Oral Health Council (VOHC) certification lifts consumer trust and provides veterinarians with clinically proven options to recommend during annual exams[1]Source: Veterinary Oral Health Council, “Accepted Products,” vohc.org. Clinic channels recorded a 12.8% CAGR to 2030 on the back of these endorsements, while approved products gained a defensible moat that discourages price erosion and rewards R&D investment. The endorsement ecosystem also facilitates market education initiatives that expand category awareness and usage frequency, particularly among first-time dental chew purchasers who rely on professional guidance for product selection.

E-Commerce Subscription Model Accelerates Repeat Purchases

Subscription delivery eliminates stock-out risk for daily chews, boosts compliance, and converts sporadic purchases into dependable cash flows. Direct-to-consumer pet specialist BARK generated 89% of its USD 490.2 million fiscal-2024 revenue online, underscoring the power of tailored refill calendars and data-driven upselling. Subscriptions also bypass retail mark-ups, improving margins and funding targeted marketing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity on dental efficacy claims | −1.3% | Global, and acute in North America and Europe | Medium term (2-4 years) |

| Safety concerns around rawhide and hard chews | −1.1% | Global | Short term (≤ 2 years) |

| Supply chain volatility for specialty natural inputs | −0.8% | Global, and acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Caloric scrutiny limiting treat usage among obese dogs | −0.7% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity on Dental Efficacy Claims

The Food and Drug Administration (FDA)'s October 2024 withdrawal from its Association of American Feed Control Officials (AAFCO) memorandum ends expedited ingredient reviews and forces brands into lengthier food-additive petitions, inflating time-to-market costs. Proposed Pet Nutrition Facts panels and labeling rules heighten compliance spend and favor incumbents with in-house regulatory talent[2]Source: Davis Wright Tremaine, “Understanding AAFCO's New Model Pet Food Regulations,” dwt.com. The regulatory ambiguity also constrains innovation in functional ingredients, where companies must balance product differentiation goals against compliance risks, potentially slowing the introduction of novel formulations that could drive category growth. The proposed PURR Act of 2024, which aims to centralize pet food regulation under FDA authority, adds another layer of uncertainty as industry stakeholders await implementation details that could reshape competitive dynamics.

Safety Concerns Around Rawhide and Hard Chews

Veterinary advisories about choking, blockages, and chemical residues prompt many owners to forgo chews altogether rather than evaluate safer substitutes. Recalls such as the 2024 Green Tripe metal contamination amplify reputational risks[3]Source: FDA, “TDBBS LLC Recalls Green Tripe Dog Treats Due to Potential Foreign Metal Object Contamination,” fda.gov. The safety concerns create competitive advantages for companies that invest in transparent sourcing, rigorous quality control, and clear safety communications, while potentially disadvantaging cost-focused manufacturers with less stringent quality standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Functional Innovation Drives Premium Growth

The textured stick chews generated 38.0% of 2024 revenue and remain the backbone of the dog dental chews market due to textured surfaces that extend chewing time and mechanically abrade plaque. Dental biscuits attract owners seeking convenient portion control that fits routine feeding. Rawhide-free chews gained popularity due to safety concerns, while the functional probiotic subcategory has started to influence consumer preferences. Functional and supplement chews post a 9.80% CAGR, using Lactobacillus or postbiotic complexes to pair digestive balance with tartar control.

Rapid functionalization underscores how wellness stacking unlocks premium shelf placement and repeat usage. Brands showcase clinical data alongside flavor innovation, and veterinarians increasingly prescribe daily probiotic chews when cleaning is scheduled far apart. As a result, the dog dental chews market size for functional formulations is projected to double by 2030, fostering R&D pipelines for enzyme blends and postbiotics that target sulfur-producing oral bacteria.

By Ingredient Source: Plant-Based Alternatives Gain Momentum

Animal-based ingredient source held a 52.0% share in 2024, leveraging innate palatability and carnivore positioning to drive velocity. Yet plant-based varieties are forecast to outpace the category at 10.90% CAGR. Kelp, chickpea, and sweet-potato matrices achieve mechanical abrasion while aligning with consumer sustainability goals. Hybrid recipes blend chicken or fish meals with upcycled vegetables to bridge taste and ethics.

The shift echoes broader human diet trends and is accelerated by steady improvements in texture and digestibility. European eco-labels and North American flexitarian pet owners spur supermarket shelf gains. This momentum positions plant formats as a pivotal driver of the dog dental chews market size in the coming years, particularly once life-cycle analyses quantify their reduced carbon footprint.

By Dog Size: Large Dog Segment Emerges as Growth Driver

Small dog breeds under 20 lb comprised 44.0% of 2024 spending because urban households dominate ownership patterns. Medium dogs benefit from standardized sizing across mass retailers. Large dog breeds command a 8.50% CAGR to 2030 as suburban migration and fenced backyards stimulate big-dog adoption.

Heavy-chewer strength requirements boost material costs, letting brands price large-breed chews at a premium that offsets volume dilution. Innovations such as PetIQ’s Minties large-dog rollout fill prior gaps and encourage retailers to dedicate shelf real estate to size-specific SKUs. Robust growth in this demographic significantly lifts the dog dental chews market, compensating for slower unit expansion in mature small-breed segments.

By Distribution Channel: Digital Transformation Accelerates

Pet specialty stores preserved 41.5% of 2024 market share due to knowledgeable staff capable of explaining VOHC endorsements and ingredient differences. Online platforms already capture a significant buoyed by auto-ship convenience and bundled subscription incentives that cut basket friction. Mass merchandisers account for serving price-sensitive customers seeking introductory oral-care products.

Online retail and subscription boxes enjoy a 11.20% CAGR, well above store growth, as refill cadence aligns with daily-chew consumption. Personalized landing pages, dental-health tracker apps, and loyalty points encourage customers to share pet data, fuelling agile R&D. Consequently, the dog dental chews market continues to lean digital, with brands investing in CRM and last-mile logistics to capture lifetime value.

Geography Analysis

North America remains the revenue leader, accounting for 42% in 2024, backed by high per-capita spending on veterinary services and preventive pet health products. VOHC seals, strong clinic networks, and mass-market education campaigns keep daily use habits entrenched. The United States is driving growth, with pet expenditures projected to reach nearly USD 200 billion by 2030, and dental chews capturing an increasing share of this spending.

Europe offers a mature but premium-oriented opportunity. The region’s EUR 29.1 billion (USD 31.7 billion) pet products market favors sustainable packaging and organic claims. Germany tallied pet product sales of EUR 6.81 billion (USD 7.4 billion) in 2024, forecast to climb toward EUR 8.4 billion (USD 9.2 billion) by 2029. Private-label penetration of 34% in the EUR 10.8 billion (USD 11.8 billion) regional pet-food subset casts a spotlight on value, yet rigorous European Union regulations around additives reward scientifically proven formulations.

Asia-Pacific exhibits the fastest trajectory, expanding at 7.6% CAGR through 2030. China’s USD 41.9 billion 2024 consumer pet market posts 7.5% annual growth, with pet food representing more than half of expenditure and United States suppliers maintaining 69% share on premium positioning. Local manufacturing hubs in provinces such as Shandong offer export scalability while domestic demand soars on urban middle-class adoption of oral-care routines. India, meanwhile, sees specialty retailers and e-commerce start-ups preparing for an influx of first-time dog owners keen on functional chews.

Competitive Landscape

The dog dental chews market shows moderate concentration in 2024. Mars, Incorporated holds a significant market share through its Greenies franchise, while Nestle (Purina) maintains a strong position with DentaLife. Virbac S.A., Blue Buffalo Pet Products, Inc. (a subsidiary of General Mills, Inc.), and PetSmart LLC complete the top five, collectively accounting for a major portion of the market. Strategic investments in AI diagnostics, such as Mars, Incorporated's USD 1 billion Greenies Canine Dental Check rollout, demonstrate how incumbents fuse hardware and data analytics to defend share.

Mid-tier challengers differentiate with functional ingredients and plant-forward recipes. Swedencare’s VOHC-approved PlaqueOff bites use organic kelp powder, while Other Half Pet’s postbiotic bacon chews broaden multi-benefit appeal. Digital natives rely on subscription economics to undercut retail margins and to harness customer data, allowing agile SKU innovation that responds to emerging flavor or health-need micro-segments.

Acquisition pipelines remain active. General Mills absorbed Whitebridge Pet Brands in late 2024 to augment its Blue Buffalo treat arm, and Mars expanded its continental diagnostics footprint via Cerba Vet. Equipment supplier JBT’s takeover of Marel strengthens manufacturing support infrastructure for co-packers serving both legacy and emerging chew brands.

Dog Dental Chews Industry Leaders

Mars, Incorporated

Blue Buffalo Pet Products, Inc. (General Mills, Inc.)

PetSmart LLC

Virbac S.A.

Nestlé (Purina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mars launched the GREENIES Canine Dental Check, an AI-powered tool trained on over 53,000 dog mouth images that enables pet parents to monitor dental health using smartphone photos. This USD 1 billion digital health investment represents a significant technology integration that could reshape how consumers approach preventive dental care and strengthen brand loyalty through value-added services.

- May 2025: Other Half Pet introduced Doggie Dental, featuring the Canine Oral Health Postbiotic (COHP) that demonstrated efficacy in reducing bad breath compounds and disrupting harmful oral biofilms in clinical trials. The bacon-flavored product targets daily use and includes human-grade ingredients like kelp and milk thistle, expanding the functional ingredient category.

- January 2025: JBT Corporation finalized its acquisition of Marel, a provider of equipment and services for pet food producers, strengthening the manufacturing infrastructure that supports dental chew production and processing capabilities.

- May 2024: Mars completed its acquisition of Cerba HealthCare Group's stake in French veterinary diagnostics businesses Cerba Vet and ANTAGENE, enhancing its veterinary diagnostics portfolio and expanding European market presence through integrated health solutions.

Global Dog Dental Chews Market Report Scope

| Textured Stick Chews |

| Dental Biscuits |

| Rawhide-Free Chews |

| Functional and Supplement Chews |

| Animal-based |

| Plant-based |

| Hybrid Ingredients |

| Small (Less than 20 lbs) |

| Medium (21-50 lbs) |

| Large (More than 50 lbs) |

| Pet Specialty Stores |

| Mass Merchandisers |

| Veterinary Clinics |

| Online Retail and Subscription Boxes |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Form | Textured Stick Chews | |

| Dental Biscuits | ||

| Rawhide-Free Chews | ||

| Functional and Supplement Chews | ||

| By Ingredient Source | Animal-based | |

| Plant-based | ||

| Hybrid Ingredients | ||

| By Dog Size | Small (Less than 20 lbs) | |

| Medium (21-50 lbs) | ||

| Large (More than 50 lbs) | ||

| By Distribution Channel | Pet Specialty Stores | |

| Mass Merchandisers | ||

| Veterinary Clinics | ||

| Online Retail and Subscription Boxes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the dog dental chews market projected to grow through 2030?

It is projected to advance at a 7.86% CAGR, lifting value from USD 0.78 billion in 2025 to USD 1.14 billion in 2030.

Which product form leads current sales?

Textured stick chews hold 38.0% of 2024 revenue owing to their effective plaque-scraping design.

Why are functional and supplement chews gaining popularity?

They combine oral care with digestive support, fueling a 9.80% CAGR that outpaces every other product form.

Which region shows the strongest growth momentum?

Asia-Pacific records a 7.6% CAGR as rising middle-class pet ownership reshapes spending in China and India.

How concentrated is the competitive landscape?

The top five manufacturers control 62.8% of revenue, positioning the category in a moderately consolidated range.

Page last updated on: