DNA Forensics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

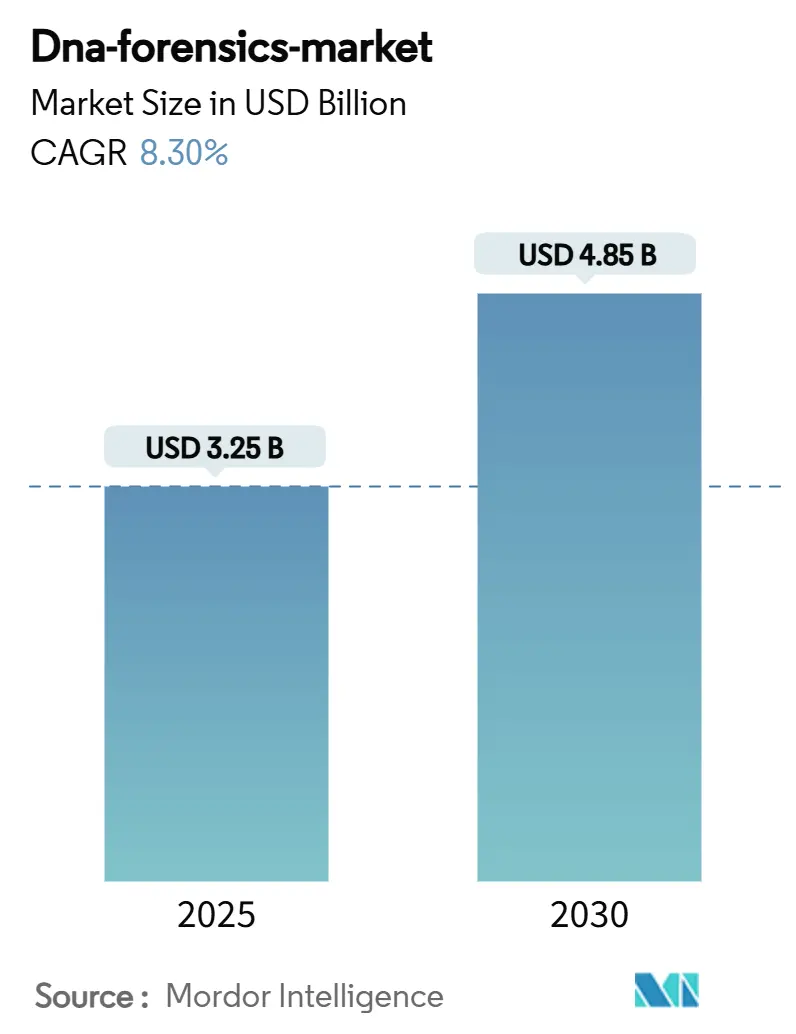

| Market Size (2025) | USD 3.25 Billion |

| Market Size (2030) | USD 4.85 Billion |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

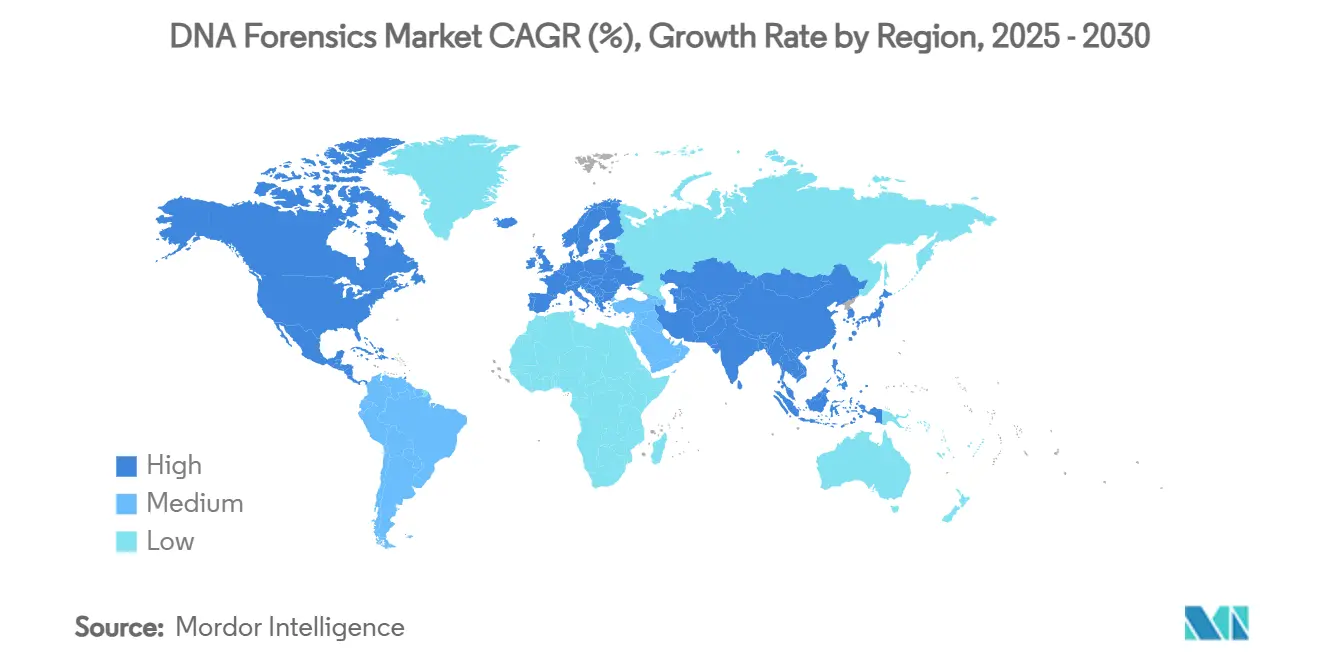

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA Forensics Market Analysis by Mordor Intelligence

The DNA forensics market size is valued at USD 3.25 billion in 2025 and is forecast to reach USD 4.85 billion by 2030, registering an 8.3% CAGR over 2025-2030. Rapid migration from capillary electrophoresis workflows toward next-generation sequencing (NGS) and rapid DNA platforms underpins this expansion. Government grant programs are accelerating laboratory modernization, while falling sequencing costs make high-throughput analysis viable for smaller facilities. Growing investigative use of forensic genetic genealogy, coupled with cross-border data-sharing initiatives, is widening the evidentiary value of DNA. Competitive intensity is rising as technology suppliers pursue vertical integration and AI-driven automation to overcome bio-informatics bottlenecks. Privacy legislation and accreditation timelines remain material headwinds, but have not derailed the overall growth trajectory of the DNA forensics market.

Key Report Takeaways

- By technology, PCR workflows retained 46.8% of the DNA forensics market share in 2024, whereas NGS recorded the fastest CAGR at 20.4% through 2030.

- By product type, rapid DNA analyzers delivered 18.7% CAGR and are reshaping field operations for law-enforcement agencies.

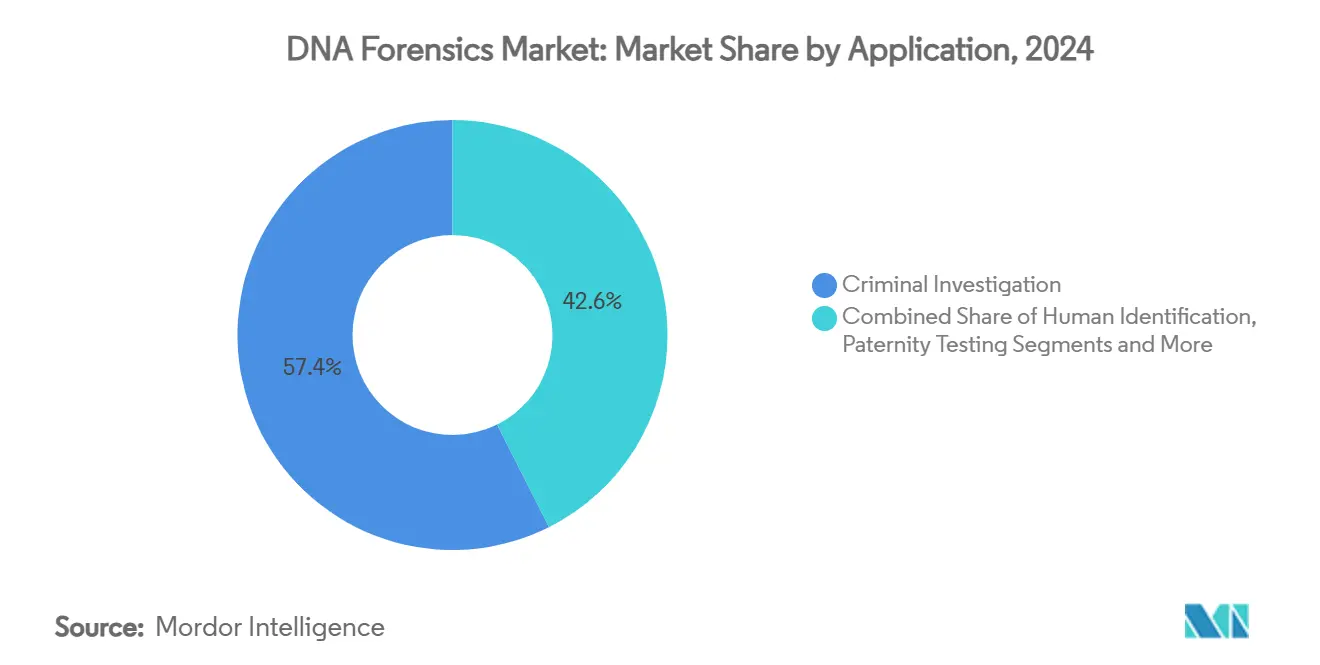

- By application, criminal investigation held 57.4% revenue share in 2024, while genetic genealogy is projected to expand at 23.9% CAGR over 2025-2030.

- By end user, government forensic laboratories commanded 48.1% of the DNA forensics market size in 2024; direct law-enforcement deployments are advancing at 18.1% CAGR.

- By geography, North America led with a 49.7% share in 2024, whereas Asia Pacific is forecast to record the highest regional CAGR at 17.4% through 2030.

Global DNA Forensics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Backlog Of Crime-Scene Samples & Cold Cases | +1.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Government Funding For Forensic-Lab Modernisation & Rapid-DNA Rollout | +2.10% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Falling Cost & TAT Of NGS-Enabled Forensic Workflows | +1.50% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Expansion Of National DNA Databases & Cross-Border Data-Sharing | +1.20% | Global, with regulatory variations by region | Medium term (2-4 years) |

| Investigative Genetic-Genealogy Integration With Law-Enforcement Platforms | +0.90% | North America & EU, limited APAC adoption | Medium term (2-4 years) |

| Portable Micro-Fluidic DNA Labs For On-Scene Disaster Response | +0.80% | Global, with emergency response focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Backlog of Crime-Scene Samples and Cold Cases

Laboratories recorded 194,067 DNA case entries in 2020, yet capacity constraints reduced annual submissions to 55,681 by 2023.[1]J.H. Smith and J.S. Horne, “Why Down-Managing Backlog Forensic DNA Case Entries Matters,” Journal of Forensic Sciences, forensicscijournal.com The gap between investigative demand and analytical throughput is steering procurement toward high-throughput NGS instruments, automated extraction robots, and sample-tracking LIMS. Untested sexual-assault kits remain a visible backlog; economic evaluations show USD 81 in societal savings for every USD 1 invested in kit testing. Legislated turnaround mandates in several US states create binding timelines that prioritize rapid DNA processing. Integrated forensic-intelligence dashboards now triage evidence based on investigative value, optimizing finite laboratory resources. Consequently, the DNA forensics market benefits from sustained capital expenditure as agencies race to clear legacy caseloads.

Government Funding for Forensic-Lab Modernization and Rapid-DNA Rollout

The National Institute of Justice awarded USD 13.6 million for 24 research projects in 2024, while the Debbie Smith DNA Backlog Grant authorizes USD 151 million annually through 2024.[2]National Institute of Justice, “NIJ Awards USD 14 Million to Support Forensic Science Research,” nij.ojp.gov Rapid DNA pilots demonstrate crime-rate reductions—Arizona reported a 42% drop in property offences after adopting portable analyzers. The Coverdell program has channeled USD 399 million into laboratory upgrades since its inception. European and Asia-Pacific governments are mirroring this approach, recognizing DNA infrastructure as critical public-safety capital. With grant cycles tied to measurable backlog reduction, recipient labs accelerate procurement of sequencers, robotics, and AI-powered interpretation tools, expanding the addressable DNA forensics market.

Falling Cost and Turnaround Time of NGS-Enabled Workflows

Whole-genome sequencing costs fell from USD 100 million in 2001 to roughly USD 500 in 2023. Forensic labs can now process degraded or mixed samples that previously yielded no interpretable STR profiles. Targeted DNA-RNA sequencing expands at 19.5% CAGR, with forensic genomics a prime use case. Massively parallel platforms such as AVITI™ achieve >90% Q30 scores, boosting evidentiary reliability. Rapid DNA instruments routinely deliver results within 90 minutes, compressing police investigative timelines. Cost deflation paired with speed turns NGS into a default tool for complex cases, further stimulating growth in the DNA forensics market.

Expansion of National DNA Databases and Cross-Border Data-Sharing

US policy now captures DNA from detained non-citizens, adding 1.5 million profiles since 2020 and elevating hit rates for violent crime investigations. Japan maintains 119,754 crime-scene profiles in its national index. Interpol and regional pacts enable cross-border comparison, which is vital for trafficking-related probes. India legislated the Bharatiya Sakshya Adhiniyam in 2023, which elevates scientific evidence in serious crimes and boosts demand for accredited labs. Larger databases exponentially increase match probability, propelling the adoption of familial searching and genetic genealogy. Database scale, therefore, magnifies the utility and investment case for the DNA forensics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Accreditation Timelines & Regulatory Complexity | -1.40% | Global, with varying standards by region | Medium term (2-4 years) |

| Privacy-Ethics Pushback Against DNA Database Growth | -0.90% | North America & EU primarily, emerging in APAC | Long term (≥ 4 years) |

| Bio-Informatics Talent Shortage In Smaller Regional Labs | -0.70% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Price Volatility From Proprietary Polymerase Supply Chains | -0.50% | Global, with higher impact on cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Accreditation Timelines and Regulatory Complexity

ISO/IEC 17025:2017 accreditation often requires extensive validation, as illustrated by Othram’s year-long process to certify massively parallel sequencing workflows. FBI Quality Assurance Standards demand multi-platform proficiency before CODIS contributions.[3]U.S. Congress, “34 USC DNA Identification,” uscode.house.gov Divergent European and North American standards complicate inter-laboratory data exchange. Emerging techniques such as DNA phenotyping and forensic genetic genealogy outpace existing guidelines, forcing labs to navigate uncertain regulatory terrain. The resulting time-to-market delays suppress near-term adoption and temper the growth rate of the DNA forensics market.

Privacy-Ethics Pushback Against DNA Database Growth

Maryland and Montana statutes now require judicial approval for genetic-genealogy searches. The 23andMe breach, which exposed 5.5 million profiles, intensified public scepticism and spurred class-action litigation. Social-media sentiment analysis finds balanced but fragile support for investigative genealogy. Ethical scrutiny of DNA collection from minority groups fuels global debate. Department of Justice interim guidelines aim to safeguard civil liberties, but patchy implementation adds compliance costs. These dynamics restrain unrestricted database expansion, moderating longer-term growth in the DNA forensics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rapid DNA Drives Innovation

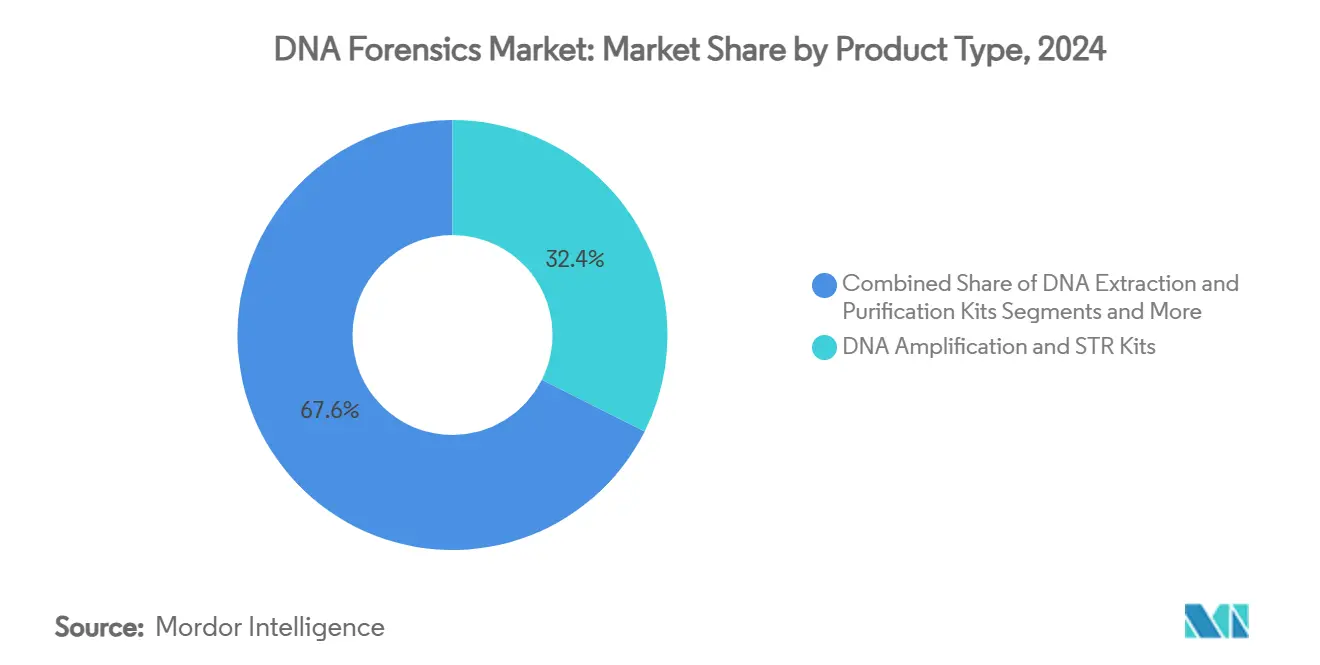

Rapid DNA analyzers captured 18.7% CAGR and redefine point-of-booking identification, whereas DNA amplification and STR kits maintained 32.4% market share in 2024. The DNA forensics market size for rapid systems is expected to widen as law-enforcement agencies internalize testing capacity. Consumables and reagents supply the largest recurring revenue pool, though proprietary polymerase sourcing exposes labs to price spikes. Promega’s enzyme innovation that cuts stutter noise strengthens legacy STR economics, ensuring the coexistence of rapid and traditional workflows.

Rapid platforms reduce booking-to-match cycles from days to under two hours, improving clearance rates and yielding tangible ROI for agencies. Portable units assist disaster-victim identification and refugee screening. DNA extraction kits remain indispensable, since high-quality inputs maximize downstream sequencing accuracy. AI-enabled interpretation modules embedded in new instruments decrease analyst workload, fostering broader adoption. Together, these factors cement rapid DNA as a strategic growth pillar within the DNA forensics market.

By Technology: NGS Disrupts PCR Dominance

PCR retained a 46.8% share in 2024, yet NGS technologies are scaling at a 20.4% CAGR. Hybrid laboratory models now combine quick STR screening with confirmatory NGS for degraded material. The DNA forensics market share for NGS workflows will climb as courts increasingly accept sequencing evidence.

AI-driven software discriminates true alleles from artefacts, minimizing human subjectivity. Mitochondrial DNA and Y-STR modules address niche maternal and paternal lineage questions. Cost per informative read continues to decline, bridging the affordability gap with PCR for routine cases. Rapid DNA remains irreplaceable for field deployment, but sequencing delivers decisive advantages for mixtures and minute, damaged fragments. Consequently, NGS is the disruptive force realigning the technology landscape of the DNA forensics market.

By Application: Genetic Genealogy Transforms Investigations

Criminal investigation maintained a 57.4% revenue share in 2024, grounded in stable violent-crime caseloads. Genetic genealogy, rising to 23.9% CAGR, is propelling cold-case resolutions and driving incremental spending. The DNA forensics market size for genealogy applications is forecast to cross USD 1 billion by 2030 as more jurisdictions permit familial searching.

High-profile successes such as the Golden State Killer case catalyzed adoption, with over 1,000 US cases solved through these methods. Genealogy now extends to missing persons and property crimes, albeit under stricter consent frameworks. Disaster-victim identification gains visibility after natural catastrophes, and defense departments deploy advanced genomics for battlefield remains. AI-enhanced pedigree reconstruction and facial phenotyping illustrate the depth of innovation reshaping the DNA forensics industry.

By End User: Law-Enforcement Agencies Expand Capabilities

Government forensic laboratories held 48.1% revenue share in 2024, reflecting entrenched accreditation status and CODIS privileges. Law-enforcement agencies exhibit 18.1% CAGR as they deploy in-house rapid DNA units at booking stations, eliminating courier delays. The DNA forensics market size attributed to police departments will accelerate as procurement frameworks mature.

Private labs specialize in genealogy and complex mixtures, carving a high-margin services niche. Academic-research centres push the technology frontier, often partnering with vendors for beta testing. Contract research organizations provide overflow capacity during surge periods. AI-enabled cloud platforms democratize data interpretation, allowing smaller agencies to leverage sophisticated analytics without on-premise bio-informatics talent. This diversification enlarges the addressable base of the DNA forensics market.

Geography Analysis

North America accounted for 49.7% of 2024 revenue due to CODIS's breadth and sustained federal grants. The United States hosts more than 550 accredited laboratories, and executive orders enforcing the DNA Fingerprint Act will intensify sample inflows. Canada and Mexico adopt interoperable protocols, supporting regional collaboration. The DNA forensics market size in North America benefits from widespread rapid DNA pilots and the early court acceptance of NGS evidence.

Europe presents a mature but innovation-friendly landscape, aided by the European Network of Forensic Science Institutes and regional harmonization efforts. Eurofins’ multi-country laboratory network accelerates cross-border casework, while Promega’s eight-colour PowerPlex 18E kit caters to regional allele frequency needs. Despite Brexit-related administrative reviews, data-sharing agreements remain functional. Privacy regulations such as GDPR shape informed-consent frameworks, yet steady capital investment persists.

Asia Pacific is the fastest-growing region at 17.4% CAGR. India operates over 50 forensic labs following legislative reforms favoring scientific evidence. Japan’s national database registers robust growth, and portable DNA units support earthquake-response missions. China’s expansion continues despite international scrutiny of minority-focused collection programs. Variable accreditation standards and talent shortages create entry barriers but also opportunities for technology providers. Overall, divergent regional dynamics collectively contribute to the sustained expansion of the DNA forensics market.

Competitive Landscape

The market remains moderately fragmented. Thermo Fisher Scientific plans USD 40-50 billion in acquisitions, signalling a sustained appetite for vertical integration. QIAGEN’s USD 150 million purchase of Verogen consolidated NGS assay design with sample-to-answer workflows. Othram, funded at USD 33.2 million, occupies a specialized niche in forensic genetic genealogy, ranking third among 285 active competitors.

Illumina continues to dominate sequencing hardware, yet regulatory issues surrounding its GRAIL deal open competitive windows for emerging platforms. Portable rapid DNA device makers vie for police budgets, while software startups deliver AI-assisted interpretation engines to relieve analyst bottlenecks. Promega’s enzyme breakthrough and Eurofins’ service-network expansion exemplify diverse strategies for differentiation.

White-space opportunities exist in reagent supply-chain localization, integrated genealogy analytics, and subscription-based bioinformatics services. Continuous innovation and targeted M&A will therefore shape the competitive trajectory of the DNA forensics market.

DNA Forensics Industry Leaders

Thermo Fisher Scientific

QIAGEN N.V.

Promega Corporation

Illumina (Verogen forensic unit)

LGC Forensics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Promega launched the PowerPlex 18E System, designed for European laboratories, adding eight-colour STR chemistry.

- August 2024: Othram introduced Multi-Dimensional Forensic Intelligence (MDFI), a new approach in forensic genetic genealogy that aims to enhance forensic DNA analysis capabilities through improved accuracy and efficiency of investigations.

- July 2024: QIAGEN partnered with Snow Molecular Anthropology Lab to support missing and murdered Indigenous people investigations.

- February 2024: Othram raised USD 6.56 million Series B funding to expand forensic genomic services.

Global DNA Forensics Market Report Scope

| DNA Amplification Kits |

| DNA Extraction & Purification Kits |

| DNA Quantification Instruments |

| Rapid-DNA Analyzers |

| Consumables & Reagents |

| PCR |

| STR Profiling |

| Next-Generation Sequencing (NGS) |

| Rapid DNA Technology |

| Mitochondrial DNA Analysis |

| Criminal Investigation |

| Human Identification & Paternity Testing |

| Disaster Victim Identification |

| Military & Defense Use-Cases |

| Genetic Genealogy & Ancestry Services |

| Government Forensic Laboratories |

| Independent / Private Forensic Labs |

| Law-Enforcement Agencies |

| Academic & Research Institutes |

| Contract Research Organisations (forensics) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | DNA Amplification Kits | |

| DNA Extraction & Purification Kits | ||

| DNA Quantification Instruments | ||

| Rapid-DNA Analyzers | ||

| Consumables & Reagents | ||

| By Technology | PCR | |

| STR Profiling | ||

| Next-Generation Sequencing (NGS) | ||

| Rapid DNA Technology | ||

| Mitochondrial DNA Analysis | ||

| By Application | Criminal Investigation | |

| Human Identification & Paternity Testing | ||

| Disaster Victim Identification | ||

| Military & Defense Use-Cases | ||

| Genetic Genealogy & Ancestry Services | ||

| By End-user | Government Forensic Laboratories | |

| Independent / Private Forensic Labs | ||

| Law-Enforcement Agencies | ||

| Academic & Research Institutes | ||

| Contract Research Organisations (forensics) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the DNA forensics market?

It is forecast to reach USD 579.45 million, reflecting an 8.9% CAGR from 2025.

Which region is growing fastest in the biological skin substitutes market?

Asia-Pacific leads with a projected 12.4% CAGR through 2030, driven by aging populations and improving healthcare infrastructure.

Which product category currently holds the largest biological skin substitutes market share?

Acellular matrices command 48.3% revenue share in 2024.

What factor is expected to have the greatest positive impact on future market growth?

Rising incidence of chronic wounds and burns contributes approximately +2.1 percentage points to forecast CAGR.

How are reimbursement changes influencing competitive dynamics?

Stricter coverage policies now favor products with published clinical-outcome data, prompting consolidation toward evidence-rich brands.

Why are military research programs significant for market innovation?

Defense-funded projects deliver shelf-stable, rapid-application grafts that migrate into civilian trauma care, expanding overall market demand.

Page last updated on: