DNA Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 15.62 Billion |

| Market Size (2030) | USD 23.39 Billion |

| Growth Rate (2025 - 2030) | 9.87% CAGR |

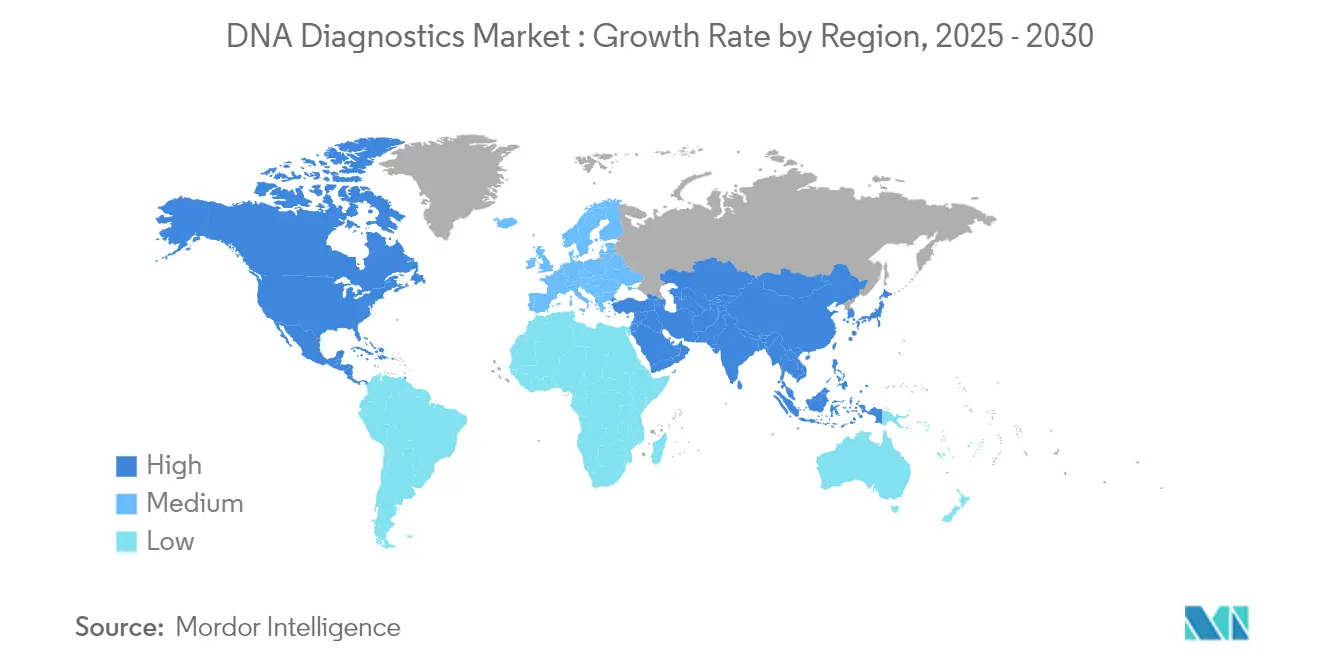

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA Diagnostics Market Analysis by Mordor Intelligence

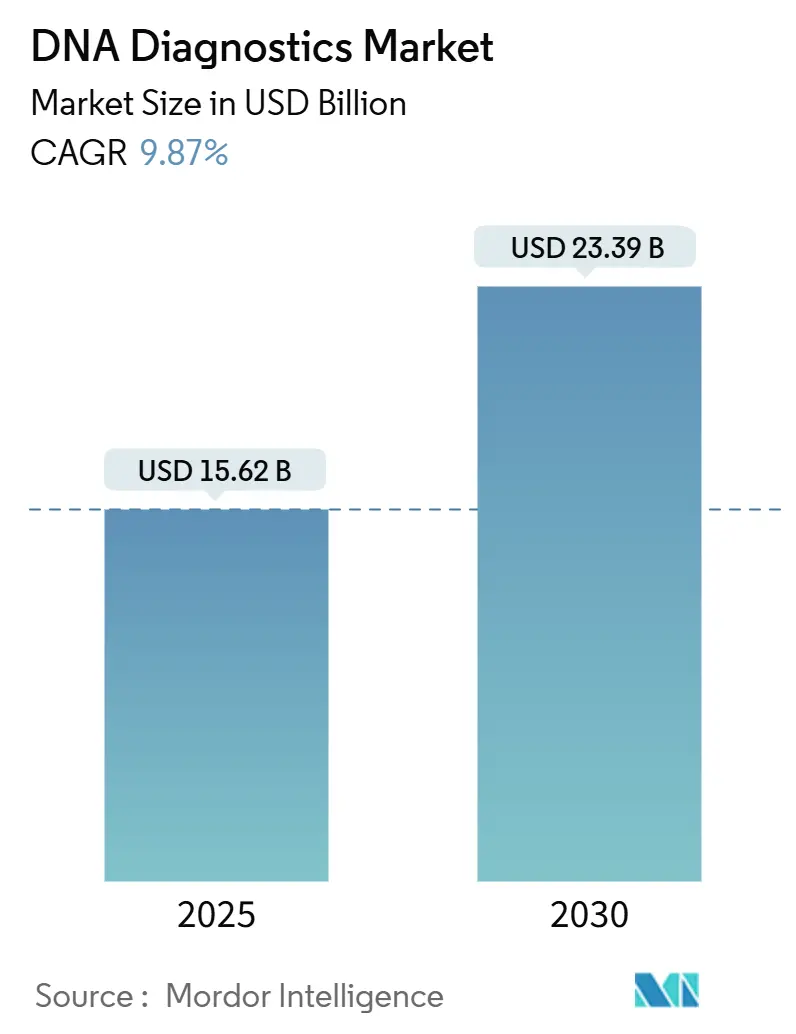

The DNA Diagnostics Market size is estimated at USD 15.62 billion in 2025, and is expected to reach USD 23.39 billion by 2030, at a CAGR of 9.87% during the forecast period (2025-2030).

DNA Diagnostics Market Overview

The DNA diagnostics industry is undergoing significant transformation, driven by advancements in technology and evolving healthcare paradigms. Leading healthcare organizations are reinforcing their commitment to innovation by making substantial investments in research and development (R&D). For example, in January 2025, the Global Health Innovative Technology (GHIT) Fund announced an investment of approximately JPY 2 billion (USD 12.7 million) across eight initiatives aimed at improving diagnostics and treatments for neglected tropical diseases (NTDs) and malaria. The integration of next-generation sequencing (NGS) and automation has revolutionized laboratory operations, enabling higher sample throughput with enhanced accuracy.

The industry is also experiencing a pronounced shift toward preventive healthcare and personalized medicine. Public health initiatives that prioritize early detection are gaining traction. For instance, the Centers for Disease Control and Prevention (CDC) reported in November 2024 that the United States' newborn screening program helps approximately 15,000 infants annually by identifying and treating serious, treatable conditions through genetic testing. Similarly, India's Department of Biotechnology-Unlocking Mother and Child Health through Innovative Diagnostics (DBT-UMMID) initiative has successfully screened over 33,000 newborns for genetic disorders as of July 2024. These programs highlight the growing incorporation of DNA diagnostics into routine healthcare protocols worldwide.

Strategic collaborations and technological partnerships are playing a pivotal role in reshaping the DNA diagnostics market. A notable example is the collaboration between Oxford Nanopore Technologies and SeqOne, an artificial intelligence (AI) developer, in March 2024. This partnership aims to enhance clinical diagnostic testing capabilities through next-generation sequencing approaches. Such alliances are becoming increasingly prevalent as companies combine expertise in genomics, AI, and data analytics to develop advanced diagnostic solutions. Additionally, the market is witnessing a surge in direct-to-consumer genetic testing services. For instance, in May 2024, iMeUsWe launched comprehensive DNA testing services through partnerships with established players like MapMyGenome.

The commercialization landscape of DNA diagnostics is undergoing a significant shift, driven by innovative business models and service delivery methods. A prime example is BillionToOne, which successfully raised USD 130 billion in venture capital funding in June 2024, achieving a billion-dollar valuation. This milestone reflects strong investor confidence in DNA diagnostic technologies. Companies are increasingly focusing on creating comprehensive testing solutions that integrate traditional diagnostic methods with advanced bioinformatics and artificial intelligence. This trend is particularly evident in the oncology segment, where firms are developing multi-modal testing approaches that combine various diagnostic technologies to enhance accuracy and clinical utility.

Global DNA Diagnostics Market Trends and Insights

Rising Prevalence of Genetic Disorders and Increased Need for Early Disease Detection

The global rise in genetic disorders is significantly driving the growth of the DNA diagnostics market. In February 2024, the Government of the United Kingdom reported that approximately 6,000 children are born each year in the United Kingdom with a genetic condition. By 2024, over 7,000 distinct genetic disorders had been identified, with advancements in genetic research continually uncovering new conditions. This growing complexity has compelled healthcare systems worldwide to enhance their genetic testing capabilities. Research indicates that early genetic diagnosis can reduce treatment costs by up to 70% through preventive interventions and targeted therapies.

The hereditary nature of genetic disorders has had a profound impact on healthcare screening protocols, resulting in a growing number of individuals seeking genetic testing for both personal health management and family planning purposes. This trend is particularly evident in the increasing demand for carrier screening, which helps identify potential genetic risks in prospective parents. Additionally, the rising awareness of genetic predispositions to various diseases has encouraged individuals to adopt a proactive approach to genetic testing. This shift is further supported by advancements in genetic testing technologies, which have made these tests more accessible and reliable, thereby fostering greater adoption across diverse demographics.

Early disease detection has emerged as a critical growth driver in the DNA diagnostics market, as evidenced by the success of newborn screening programs. For instance, in April 2024, Parent Project Muscular Dystrophy (PPMD) announced a significant milestone in Duchenne muscular dystrophy newborn screening: Ohio will become the first state to implement comprehensive screening for all newborns. Each year, more than 129,000 babies are born in Ohio, and the state anticipates identifying approximately 35 cases of Duchenne muscular dystrophy annually. This initiative was pioneered when Ohio Governor Mike DeWine signed House Bill 33 (HB 33) into law in July 2023, setting a benchmark that was subsequently adopted by New York and Minnesota. The ability of DNA diagnostics to detect disease risks and genetic predispositions before symptoms appear has transformed preventive healthcare strategies.

The expansion of early detection capabilities has had a particularly significant impact on oncology, where genetic testing now enables the identification of cancer risks years before traditional diagnostic methods. Recent advancements in DNA diagnostics have facilitated the detection of over 50 types of hereditary cancers, with high accuracy rates for specific cancer-related genetic mutations. The preventive value of early genetic testing is further highlighted by studies showing that individuals identified with genetic predispositions to diseases can lower their risk through preventive measures and lifestyle changes when detected early.

Advancements in Diagnostic Techniques and AI Integration

Artificial intelligence and advanced diagnostic techniques have revolutionized DNA diagnostics. Machine learning algorithms now boast accuracy rates of up to 95% in interpreting genetic variants. Thanks to these technological strides, the time for genetic analysis has been slashed. Next-generation sequencing platforms can now process multiple samples simultaneously, condensing testing durations from weeks to mere days. Moreover, AI-driven analyses have markedly enhanced the precision of genetic variant classifications. Recent studies highlight a 40% drop in variants of uncertain significance (VUS) when juxtaposed with traditional methods.

The fusion of bioinformatics and AI has paved the way for deeper insights into genetic data, unveiling new patterns in diseases and their genetic links. Today's DNA diagnostic platforms can concurrently analyze millions of genetic variants. AI systems excel at pinpointing intricate patterns and relationships, a feat beyond the reach of traditional methods. Furthermore, machine learning's integration has democratized genetic testing. Automated systems have cut analysis costs by up to 60%, all while upholding high accuracy. This affordability surge empowers a broader range of healthcare providers to deliver in-depth genetic testing services.

Growing R&D Investments and Supportive Government Funding for Genomic Research

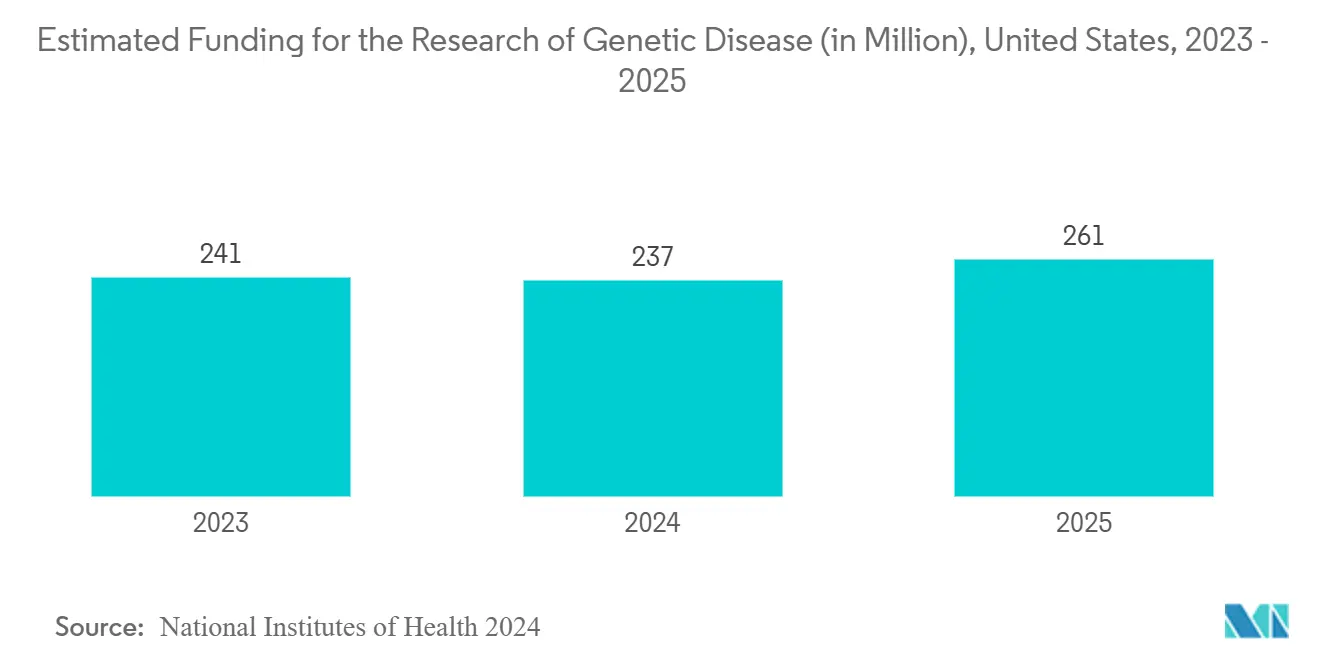

In March 2023, the Government of Canada announced a significant investment of USD 400 million over six years (2021-2027) to support genomics research, reflecting its strategic focus on advancing DNA diagnostics. This initiative aligns with increasing private-sector investments in genetic research. Additionally, in September 2023, the National Institutes of Health (NIH) introduced the Multi-Omics for Health and Disease Consortium, allocating an initial funding of approximately USD 11 million in its first year. The consortium aims to accelerate progress in generating and analyzing "multi-omic" data, thereby driving innovation in human health research. These investments have catalyzed significant advancements in diagnostic technologies, with research institutions reporting a rise in patent applications for novel DNA diagnostic methods over the past two years.

Globally, government-led initiatives have created a conducive environment for the growth of DNA diagnostics, with several countries implementing comprehensive genetic testing programs. For example, in August 2023, Japan enacted the "Genome Medicine Promotion Act," underscoring the increasing governmental emphasis on advancing genetic medicine. These funding efforts have not only expedited technological progress but also enhanced the accessibility of genetic testing. Public health programs have recorded a notable increase in the number of individuals receiving genetic counseling and testing services.

DNA Diagnostics Market Product and Service Segment Analysis

Reagents and Kits Segment in DNA Diagnostics Market

In 2024, the reagents and kits segment is projected to maintain its dominant position in the DNA diagnostics market, capturing an estimated 45% market share. This segment's leadership is attributed to the sustained demand for diagnostic testing supplies, which are critical for applications such as infectious disease diagnostics and oncology testing. The increasing prevalence of genetic disorders, coupled with the growing focus on early disease detection, has driven the need for consistent replenishment of these diagnostic supplies. Additionally, stringent quality control requirements and standardization protocols in diagnostic laboratories have further fueled the demand for certified reagents and kits. The segment's strong performance is also supported by advancements in technology, which have enabled more accurate and efficient diagnostic procedures. Furthermore, the expansion of testing capabilities in hospitals and diagnostic laboratories has ensured a steady demand for these essential consumables. The segment's market position is further bolstered by the rising adoption of molecular diagnostic techniques across both developed and emerging markets.

Services and Software Segment in DNA Diagnostics Market

The services and software segment emerges as the fastest-growing category in the DNA diagnostics market, projected to achieve a remarkable CAGR of 10.5% from 2025 to 2030. This surge is largely driven by the rising adoption of artificial intelligence and machine learning in diagnostics. Demand for cloud-based diagnostic solutions and data management platforms further propels this segment's growth. Healthcare facilities are now opting for all-encompassing diagnostic service packages, which encompass data analysis, interpretation, and storage. As genetic testing becomes more intricate, there's a burgeoning market for specialized diagnostic services and advanced analytical software. Moreover, the push towards laboratory automation and digital pathology has heightened the appetite for advanced software solutions. The segment's expansion is also bolstered by a growing reliance on bioinformatics tools for extensive genetic data analysis and interpretation.

DNA Diagnostics Market Technology Segment Analysis

PCR Segment in DNA Diagnostics Market

Polymerase Chain Reaction (PCR) technology maintains its dominant position in the DNA diagnostics market, commanding approximately 35% of the market share in 2024. This leadership position is primarily attributed to PCR's widespread adoption in clinical diagnostics, research laboratories, and hospitals due to its reliability and versatility. The segment's strength is further reinforced by the continuous introduction of automated PCR systems and real-time PCR platforms, which have significantly improved testing efficiency and accuracy. The development of multiplex PCR assays has expanded the technology's application scope, particularly in infectious disease diagnostics and genetic testing. Recent advancements in digital PCR technology have enhanced the segment's capability for absolute quantification and rare mutation detection. The integration of artificial intelligence and machine learning algorithms with PCR systems has also contributed to improved result interpretation and reduced processing times. Additionally, the COVID-19 pandemic has substantially increased the installed base of PCR instruments, creating a lasting impact on the segment's market position.

Sequencing Segment in DNA Diagnostics Market

The sequencing segment is emerging as the fastest-growing technology in the DNA diagnostics market, projected to achieve a remarkable CAGR of 10.09% from 2025 to 2030. This robust growth is primarily driven by significant advancements in next-generation sequencing (NGS) technologies and their expanding role in precision medicine and personalized healthcare. The increasing utilization of whole-genome sequencing and targeted sequencing methods in oncology and rare disease diagnostics is a key factor propelling this segment's expansion. Furthermore, advancements in long-read sequencing technologies are unlocking new opportunities for complex genetic analyses and the detection of structural variants. The introduction of portable sequencing devices has further democratized access to sequencing technology, particularly in point-of-care settings. Declining costs of sequencing, combined with faster turnaround times, have enhanced the technology's accessibility for clinical laboratories and research institutions. Additionally, the segment's growth is being driven by the rising demand for non-invasive prenatal testing and liquid biopsy applications. The adoption of cloud-based sequencing data analysis platforms has also significantly improved the technology's utility in clinical environments.

DNA Diagnostics Market Application Segment Analysis

Oncology Testing Segment in DNA Diagnostics Market

The oncology testing segment has emerged as the dominant force in the DNA diagnostics market, commanding approximately 35% of the market share in 2024. This substantial market position is primarily driven by the increasing global cancer burden and the growing adoption of precision medicine approaches in cancer treatment. The segment's leadership is further strengthened by continuous technological advancements in genetic testing methodologies, particularly in liquid biopsy and circulating tumor DNA analysis. Healthcare providers' increasing reliance on molecular diagnostics for cancer screening, diagnosis, and monitoring has significantly contributed to this segment's dominance. The integration of artificial intelligence and machine learning in cancer diagnostics has enhanced the accuracy and efficiency of oncology testing, further solidifying its market position. Additionally, the growing emphasis on personalized cancer treatment protocols and the rising demand for companion diagnostics have been crucial factors in maintaining this segment's market leadership.

Infectious Disease Diagnostics Segment in DNA Diagnostics Market

The infectious disease diagnostics segment is projected to exhibit the highest growth rate in the DNA diagnostics market, with an estimated CAGR of 11.89% from 2025 to 2030. This remarkable growth trajectory is primarily attributed to the increased focus on pandemic preparedness and the rising demand for rapid, accurate diagnostic solutions for infectious diseases. The segment's expansion is further accelerated by the development of advanced molecular diagnostic techniques that enable faster and more precise pathogen detection. The integration of next-generation sequencing technologies in infectious disease testing has opened new opportunities for comprehensive pathogen profiling. Growing investments in research and development of point-of-care molecular diagnostic solutions have significantly contributed to this segment's rapid growth. The increasing adoption of automated testing platforms and the rising demand for multiplex testing capabilities have also been crucial drivers of this segment's exceptional growth rate.

DNA Diagnostics Market End-User Segment Analysis

Diagnostic Laboratories Segment in DNA Diagnostics Market

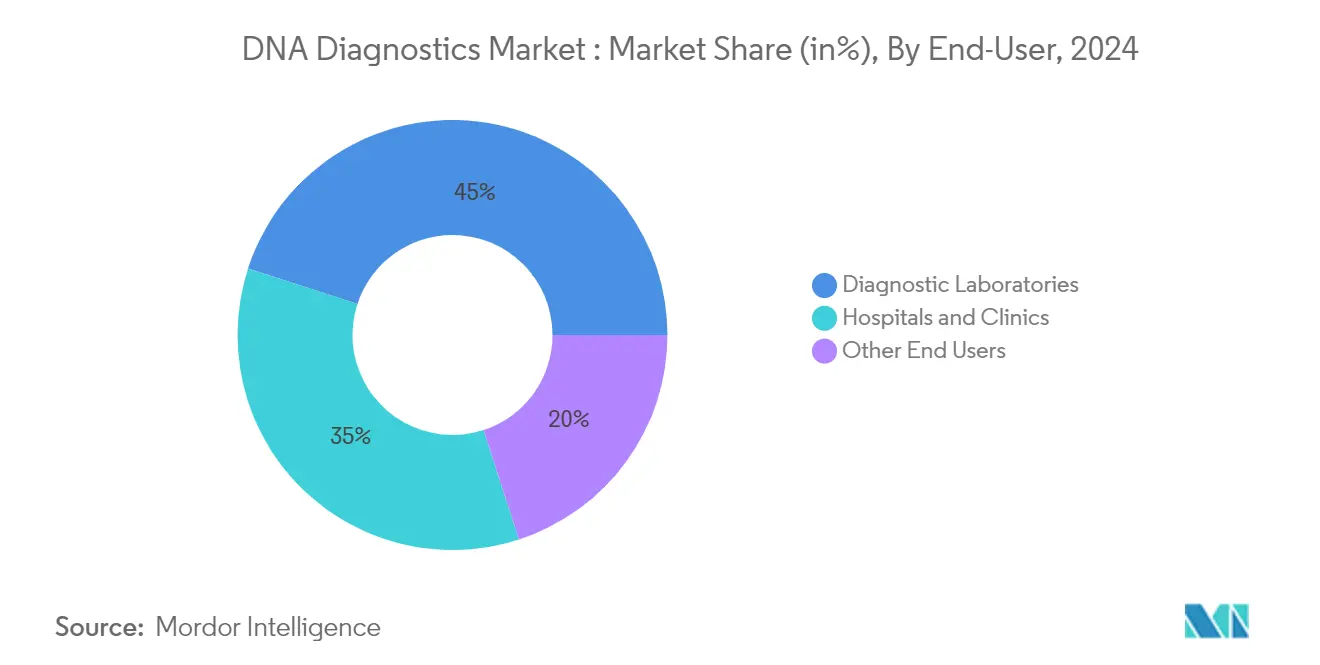

Diagnostic laboratories have emerged as the dominant segment in the DNA diagnostics market, commanding approximately 45% of the market share in 2024. This leadership position is attributed to their specialized focus on genetic testing services and superior technical capabilities. Diagnostic laboratories benefit from high-throughput testing capabilities, enabling them to process large volumes of samples efficiently. These facilities typically maintain state-of-the-art equipment and employ specialized personnel trained in genetic testing procedures. The segment's prominence is further strengthened by its ability to serve multiple healthcare facilities simultaneously, creating economies of scale. Additionally, diagnostic laboratories often participate in research collaborations and clinical trials, enhancing their market position. Their ability to invest in advanced technologies and maintain quality control standards has made them the preferred choice for complex genetic testing procedures.

Hospitals and Clinics Segment in DNA Diagnostics Market

The hospitals and clinics segment is experiencing the fastest growth in the DNA diagnostics market, with a projected CAGR of 12% from 2025 to 2030. This rapid expansion is driven by the increasing integration of genetic testing into routine clinical care and the growing demand for personalized medicine. Hospitals and clinics are actively investing in in-house genetic testing capabilities to reduce turnaround times and improve patient care coordination. The segment's growth is further accelerated by the rising adoption of point-of-care genetic testing solutions and increasing insurance coverage for genetic tests. Enhanced focus on preventive healthcare and early disease detection has led to greater incorporation of genetic testing in hospital protocols. Additionally, the growing trend of hospital-laboratory partnerships and the expansion of specialty genetic clinics within hospital systems are contributing to this segment's rapid growth.

DNA Diagnostics Market Geography Segment Analysis

DNA Diagnostics Market in North America

North America holds a leading position in the global DNA diagnostics market, accounting for approximately 43% of the total market share in 2024. This leadership is driven by the region's advanced healthcare infrastructure and robust government initiatives that actively support genetic research and testing. The presence of prominent market players and research institutions has been instrumental in driving continuous advancements in DNA diagnostic technologies. Favorable reimbursement policies and significant healthcare expenditure in the region have enabled the widespread adoption of advanced diagnostic solutions. Additionally, the growing awareness of personalized medicine and preventive healthcare among the population has significantly increased the demand for genetic testing services. The region's well-established regulatory framework provides comprehensive guidelines for diagnostic testing, fostering trust among healthcare providers and patients. Furthermore, North America's strategic focus on early disease detection and prevention has cultivated a strong market for various DNA diagnostic applications, including oncology testing and prenatal screening.

DNA Diagnostics Market in Europe

Europe is poised to see steady growth in its DNA diagnostics market from 2025 to 2030. This growth is bolstered by robust research and development in genetic testing technologies, coupled with Europe's well-structured healthcare system. Notably, European nations excel in rolling out nationwide genetic screening programs, with a focus on prenatal and newborn testing. Established biotechnology firms and research institutions in the region have been pivotal in driving innovation in diagnostic technologies. Furthermore, the EU's In Vitro Diagnostic Regulation (IVDR) has been instrumental in standardizing testing procedures and upholding quality control. As investments in healthcare infrastructure rise and awareness of genetic disorders grows, the market continues to expand. Additionally, strong partnerships between academic institutions and industry players in Europe have catalyzed ongoing technological advancements in DNA diagnostic solutions.

DNA Diagnostics Market in Asia-Pacific

The Asia-Pacific region is anticipated to emerge as the fastest-growing market in the DNA diagnostics sector, with a projected CAGR of approximately 11% during the forecast period from 2025 to 2030. This growth is primarily attributed to key drivers such as the rapid development of healthcare infrastructure and increasing healthcare expenditure in emerging economies. The region is undergoing a notable transformation in its healthcare ecosystem, with countries like China and India making significant investments in genetic research and diagnostic facilities. The rising awareness of genetic testing and its applications in preventive healthcare has substantially boosted the demand for DNA diagnostic services. Additionally, the expanding middle-class population, coupled with higher disposable incomes, has enhanced access to advanced diagnostic solutions. Government initiatives aimed at healthcare modernization and the integration of advanced diagnostic technologies have further created a conducive market environment. Moreover, the region benefits from the growth of medical tourism and the establishment of state-of-the-art diagnostic centers.

DNA Diagnostics Market in Middle East and Africa

The DNA diagnostics market in the Middle East and Africa region offers distinct opportunities, driven by increasing healthcare investments and efforts to modernize medical infrastructure. The region, particularly the Gulf Cooperation Council (GCC) countries, is experiencing notable advancements in genetic testing capabilities. Growing awareness regarding genetic disorders and their prevention has significantly boosted the adoption of DNA diagnostic services. The high prevalence of genetic disorders, often attributed to consanguineous marriages, has created a substantial demand for genetic testing services. Government-led initiatives aimed at enhancing healthcare services and improving access to advanced diagnostic technologies have further propelled market growth. The establishment of new diagnostic centers, along with strategic partnerships with international healthcare providers, has expanded the availability of genetic testing services. Furthermore, the rise in healthcare tourism across the Middle East has played a pivotal role in driving the demand for advanced diagnostic services in the region.

DNA Diagnostics Market in South America

South America is positioning itself as a high-potential market for DNA diagnostics, driven by advancements in healthcare infrastructure and a growing understanding of the benefits of genetic testing. The adoption of advanced diagnostic technologies is increasing across the region, with Brazil leading as a key contributor. Healthcare modernization initiatives, coupled with rising private sector investments, are significantly driving market growth. Efforts to improve healthcare accessibility have resulted in the establishment of numerous diagnostic centers and laboratories. Furthermore, the rising awareness of personalized medicine and genetic disorders is unlocking new growth opportunities in the market. Strategic partnerships between local healthcare providers and international diagnostic companies are enabling technology transfer and fostering market development. Additionally, the region's diverse genetic pool is generating interest in population-specific genetic studies and diagnostics, presenting unique and untapped market opportunities.

Competitive Landscape

Top Companies in DNA Diagnostics Market

The DNA diagnostics market is led by prominent players including Agilent Technologies, Inc., Beckman Coulter, Inc., Bio-Rad Laboratories, F. Hoffmann-La-Roche AG, GE Healthcare, Illumina, Inc., Myriad Genetics, Oxford Nanopore Technologies plc. , Qiagen N.V, Siemens Healthineers AG, and Thermo Fisher Scientific Inc. These industry leaders have demonstrated consistent focus on product innovation, particularly in developing advanced sequencing technologies and automated diagnostic platforms. Companies are increasingly investing in artificial intelligence and machine learning capabilities to enhance their diagnostic accuracy and throughput. Strategic collaborations with healthcare providers and research institutions have become a key trend, enabling companies to expand their market presence and technological capabilities. Geographic expansion, particularly in emerging markets, has been prioritized through both direct presence and distribution partnerships. The industry has also witnessed a strong emphasis on developing integrated diagnostic solutions that combine hardware, software, and services to provide comprehensive testing solutions.

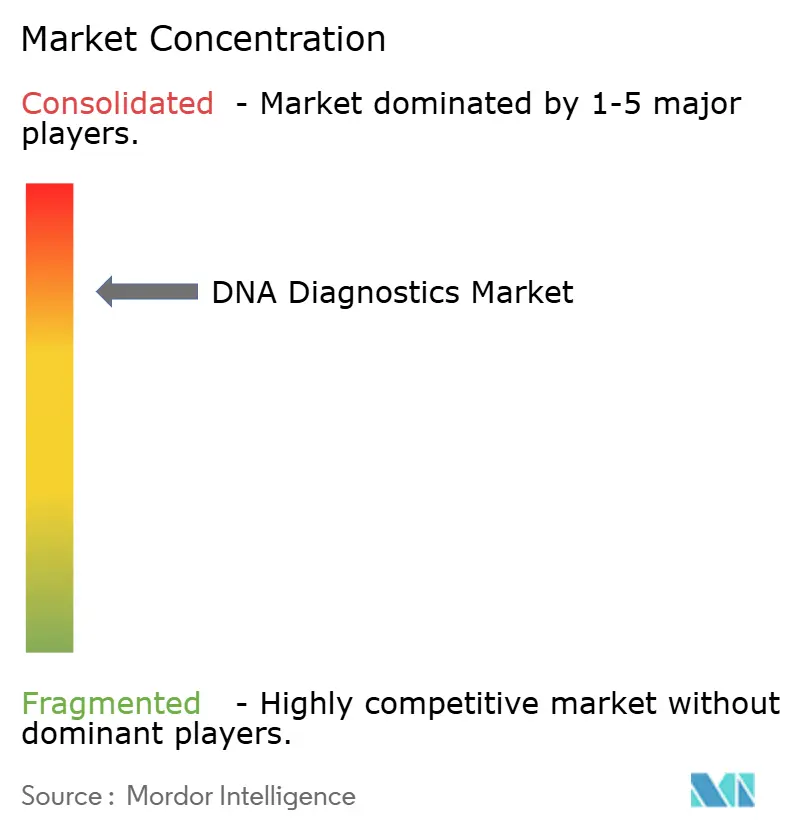

Market Structure Shows Strategic Consolidation Patterns

The DNA diagnostics market exhibits a relatively consolidated structure dominated by global conglomerates with diverse healthcare portfolios, alongside specialized diagnostic companies focusing on specific testing segments. These major players have established strong market positions through extensive R&D capabilities, broad product portfolios, and global distribution networks. The market has witnessed strategic consolidation through mergers and acquisitions, particularly targeting companies with complementary technologies or regional market access. Large companies have been actively acquiring innovative startups and smaller firms to enhance their technological capabilities, especially in areas like next-generation sequencing and point-of-care diagnostics.

The competitive dynamics are characterized by a mix of global players and regional specialists, with the latter holding significant market share in specific geographic regions or specialized testing segments. Market consolidation has been driven by the need to achieve economies of scale, expand technological capabilities, and strengthen market presence in key regions. Companies have been increasingly focusing on vertical integration strategies, controlling various aspects of the value chain from research and development to commercialization. The industry has also seen the emergence of strategic partnerships between diagnostic companies and healthcare providers, aimed at developing integrated diagnostic solutions and improving market access.

Innovation and Integration Drive Future Success

Success in the DNA diagnostics market increasingly depends on companies' ability to innovate while maintaining cost-effectiveness and operational efficiency. Incumbent players must focus on continuous technological advancement, particularly in areas like automation, artificial intelligence integration, and point-of-care testing capabilities. Building comprehensive diagnostic platforms that offer integrated solutions for multiple testing needs has become crucial for maintaining market leadership. Companies need to strengthen their direct presence in emerging markets while developing products tailored to local healthcare needs and regulatory requirements. Establishing strong relationships with healthcare providers, research institutions, and regulatory bodies has become essential for long-term success.

For contenders looking to gain market share, focusing on specialized market segments or specific geographic regions offers a viable entry strategy. Success factors include developing innovative technologies that address unmet diagnostic needs, building efficient distribution networks, and establishing strong intellectual property portfolios.

DNA Diagnostics Industry Leaders

Agilent Technologies, Inc.

Bio-Rad Laboratories

F. Hoffmann-La-Roche AG

Myriad Genetics

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Myriad Genetics, Inc. announced that it presented innovative research at the annual Society for Maternal-Fetal Medicine (SMFM) Conference. The company’s study, titled “Fetal fraction amplification enables accurate prenatal cell-free DNA (cfDNA) screening at eight weeks gestation,” received the prestigious “Dru Carlson Memorial Award for Best Research in Ultrasound and Genetics” from SMFM.

- November 2024: ProPhase Labs, Inc. has unveiled DNA Complete, Inc., its wholly owned subsidiary. DNA Complete introduces a pioneering direct-to-consumer DNA test, capable of sequencing nearly the entirety of a customer's genome. With this innovative service, customers gain comprehensive insights into their health, wellness, and ancestral lineage.

- May 2024: iMeUsWe announced collaboration with MapMyGenome to provide comprehensive DNA testing services including genetic health insights, wellness assessments, ancestry information, and expert genetic counseling.

- March 2024: Nucleus Genomics introduced its full DNA analysis product to make the benefits of personalized medicine accessible to a broader audience. The Nucleus platform enables users to obtain comprehensive insights into their genetic risks for various diseases, including type 2 diabetes, breast cancer, and several others.

Global DNA Diagnostics Market Report Scope

As per the scope of the report, DNA diagnostics refers to the use of DNA-based tests and techniques to identify genetic disorders, infectious diseases, and other medical conditions. It involves analyzing an individual's genetic material to detect mutations, variations, or pathogens that may cause diseases. DNA diagnostics are widely used in personalized medicine, oncology, infectious disease detection, prenatal screening, forensic analysis, and hereditary disease risk assessment.

The DNA diagnostics market is segmented as product and service, technology, application, end-user, and geography. By product and service, the market is segmented as reagents and kits, instruments, services, and software. By technology, the market is segmented as polymerase chain reaction, microarray, in situ hybridization, sequencing, mass spectroscopy, and other technologies. By application, the market is segmented as infectious disease diagnostics, oncology testing, myogenic disorders, prenatal testing, preimplantation testing, and other applications. By end-user, the market is segmented as diagnostic laboratories, hospitals and clinics, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions, globally. The report offers the value (in USD) for the above-mentioned segments.

| Reagents and Kits |

| Instruments |

| Services and Software |

| Polymerase Chain Reaction |

| Microarray |

| In Situ Hybridization |

| Sequencing |

| Mass Spectroscopy |

| Other Technologies |

| Infectious Disease Diagnostics |

| Oncology Testing |

| Myogenic Disorders |

| Prenatal Testing |

| Preimplantation Testing |

| Other Applications |

| Diagnostic Laboratories |

| Hospitals and Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product and Service | Reagents and Kits | |

| Instruments | ||

| Services and Software | ||

| By Technology | Polymerase Chain Reaction | |

| Microarray | ||

| In Situ Hybridization | ||

| Sequencing | ||

| Mass Spectroscopy | ||

| Other Technologies | ||

| By Applications | Infectious Disease Diagnostics | |

| Oncology Testing | ||

| Myogenic Disorders | ||

| Prenatal Testing | ||

| Preimplantation Testing | ||

| Other Applications | ||

| By End-User | Diagnostic Laboratories | |

| Hospitals and Clinics | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the DNA Diagnostics Market?

The DNA Diagnostics Market size is expected to reach USD 15.62 billion in 2025 and grow at a CAGR of 9.87% to reach USD 23.39 billion by 2030.

What is the current DNA Diagnostics Market size?

In 2025, the DNA Diagnostics Market size is expected to reach USD 15.62 billion.

Which is the fastest growing region in DNA Diagnostics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in DNA Diagnostics Market?

In 2025, the North America accounts for the largest market share in DNA Diagnostics Market.

What years does this DNA Diagnostics Market cover, and what was the market size in 2024?

In 2024, the DNA Diagnostics Market size was estimated at USD 14.08 billion. The report covers the DNA Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the DNA Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: