Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

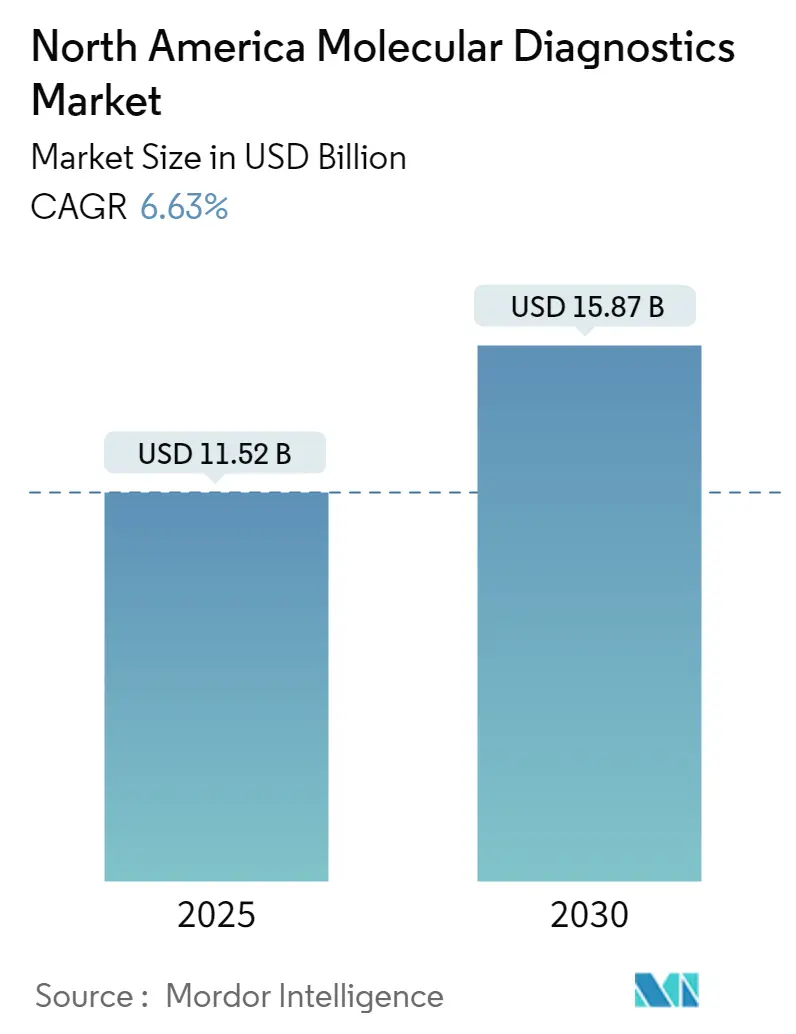

| Market Size (2025) | USD 11.52 Billion |

| Market Size (2030) | USD 15.87 Billion |

| Growth Rate (2025 - 2030) | 6.63% CAGR |

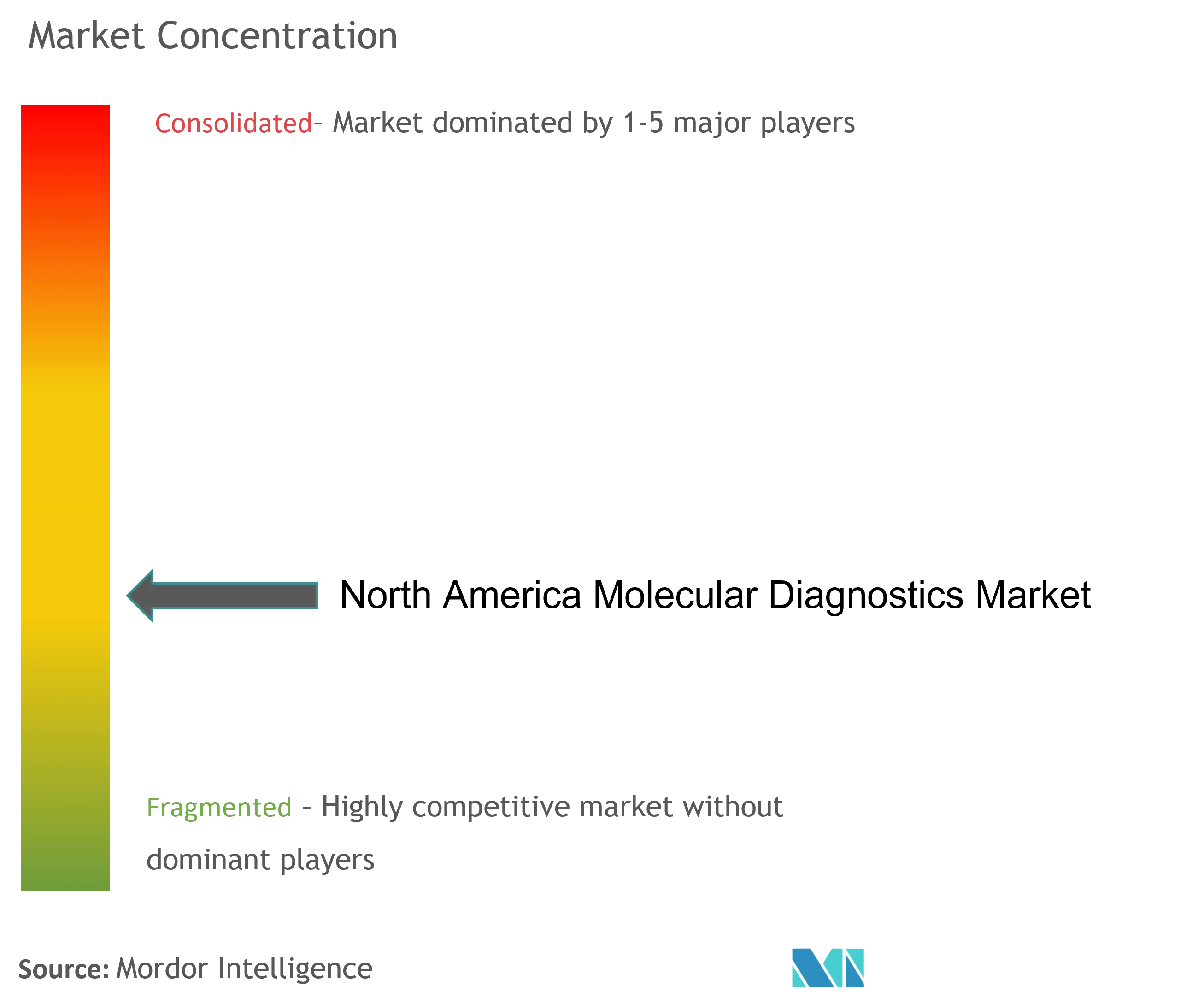

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Molecular Diagnostics Market Analysis by Mordor Intelligence

The North America Molecular Diagnostics Market size is estimated at USD 11.52 billion in 2025, and is expected to reach USD 15.87 billion by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

The molecular diagnostics landscape in North America is experiencing significant transformation driven by technological advancements in diagnostic methodologies and automation. Advanced molecular diagnostic testing platforms are increasingly incorporating artificial intelligence and machine learning capabilities to enhance accuracy and reduce turnaround times. These innovations are particularly evident in the development of next-generation sequencing technologies and automated sample preparation systems, which are revolutionizing traditional diagnostic approaches. The integration of robotics and sophisticated software algorithms in diagnostic systems is setting new standards in laboratory automation, as demonstrated by recent developments in high-throughput diagnostic platforms.

The industry is witnessing a notable shift toward personalized medicine and precision diagnostics, with a growing emphasis on early disease detection and targeted therapeutic approaches. This evolution is particularly evident in the field of oncology and genetic testing, where molecular diagnostics play a crucial role in identifying specific genetic markers and mutations. According to the American Academy of Pediatrics data from March 2022, more than one million people in the United States have long-term hepatitis B infections, with early detection through molecular screening being crucial for effective management and treatment outcomes. This statistic underscores the critical role of molecular diagnostics in managing chronic conditions and preventing their progression.

The market is experiencing rapid advancement in in-situ hybridization technologies, enabling more precise visualization of genetic material at the cellular level. These developments are particularly significant in research applications and clinical diagnostics, allowing for more accurate detection of genetic abnormalities and disease markers. The introduction of novel assays and platforms is enhancing the capability to detect DNA copy numbers and structural variations, leading to more precise diagnostic outcomes. This technological evolution is particularly evident in the emergence of advanced platforms that enable single-molecule gene expression visualization with single-cell resolution.

Strategic collaborations and partnerships between diagnostic companies and healthcare providers are reshaping the competitive landscape. Companies are focusing on developing integrated diagnostic solutions that combine multiple testing capabilities on single platforms. For instance, in July 2022, BioGX introduced a point-of-care CE-marked, three-gene multiplex test on its pixl platform, exemplifying the industry's move toward more sophisticated and comprehensive diagnostic solutions. This trend toward consolidated testing platforms is improving laboratory efficiency and reducing operational costs while maintaining high diagnostic accuracy and reliability. The focus on molecular biomarker discovery and molecular analysis is further enhancing the precision of clinical molecular diagnostics.

North America Molecular Diagnostics Market Trends and Insights

Rising Prevalence of Chronic and Infectious Diseases

The increasing burden of chronic diseases, particularly cancer, continues to drive the demand for molecular diagnostics solutions across North America. According to the American Cancer Society's 2022 statistics, approximately 1,918,030 new cancer cases were predicted to occur in the United States, with breast cancer accounting for 290,560 new cases, leukemia with 60,650 new cases, and lymphoma with 89,010 new cases. The severity of the situation is further highlighted by the Canadian Cancer Statistics report, which revealed that an estimated 2 in 5 Canadians are likely to be diagnosed with cancer in their lifetime, emphasizing the critical need for advanced diagnostic solutions.

The growing prevalence of various types of cancer has prompted healthcare providers to focus on early detection and precise diagnosis, driving the adoption of molecular testing technologies. This trend is supported by continuous technological advancements in diagnostic solutions, such as the development of sophisticated testing platforms and companion diagnostics. For instance, in November 2022, Roche received FDA approval for VENTANA FOLR1 (FOLR1-2.1) RxDx assay, the first IHC-based companion diagnostic to identify ovarian cancer patients eligible for ELAHERE, demonstrating the industry's response to the increasing demand for precise diagnostic solutions for chronic diseases.

Understand The Key Trends Shaping This Market

Download PDF

Increasing R&D Funding and Demand for Point-of-Care Diagnostics

The substantial increase in research and development funding has become a crucial driver for the molecular diagnostics market in North America. According to the National Institutes of Health (NIH) 2022 update, significant investments have been made in research activities, with USD 212 million allocated for genetic testing and USD 4,666 million for emerging infectious diseases research in 2021. These investments have facilitated the development of innovative diagnostic solutions and enhanced testing capabilities, particularly in point-of-care settings where rapid and accurate results are essential for effective patient care.

The growing emphasis on point-of-care diagnostics has attracted significant private investment and sparked innovation in the field. This trend is exemplified by Visby Medical's successful funding round of USD 135 million in June 2022, aimed at scaling production capacity and expanding their product portfolio to bring PCR diagnostics directly to consumers' homes. Furthermore, the industry's commitment to innovation is demonstrated by developments such as Alercell's launch of LENA Q51(R) in January 2023, a sophisticated leukemia diagnostic test capable of detecting up to 51 gene mutations in leukemia patients. These advancements in rapid molecular diagnostics are revolutionizing the way healthcare providers approach disease diagnosis and treatment, making testing more accessible and efficient for patients across various healthcare settings.

Segment Analysis

PCR Segment in North America Molecular Diagnostics Market

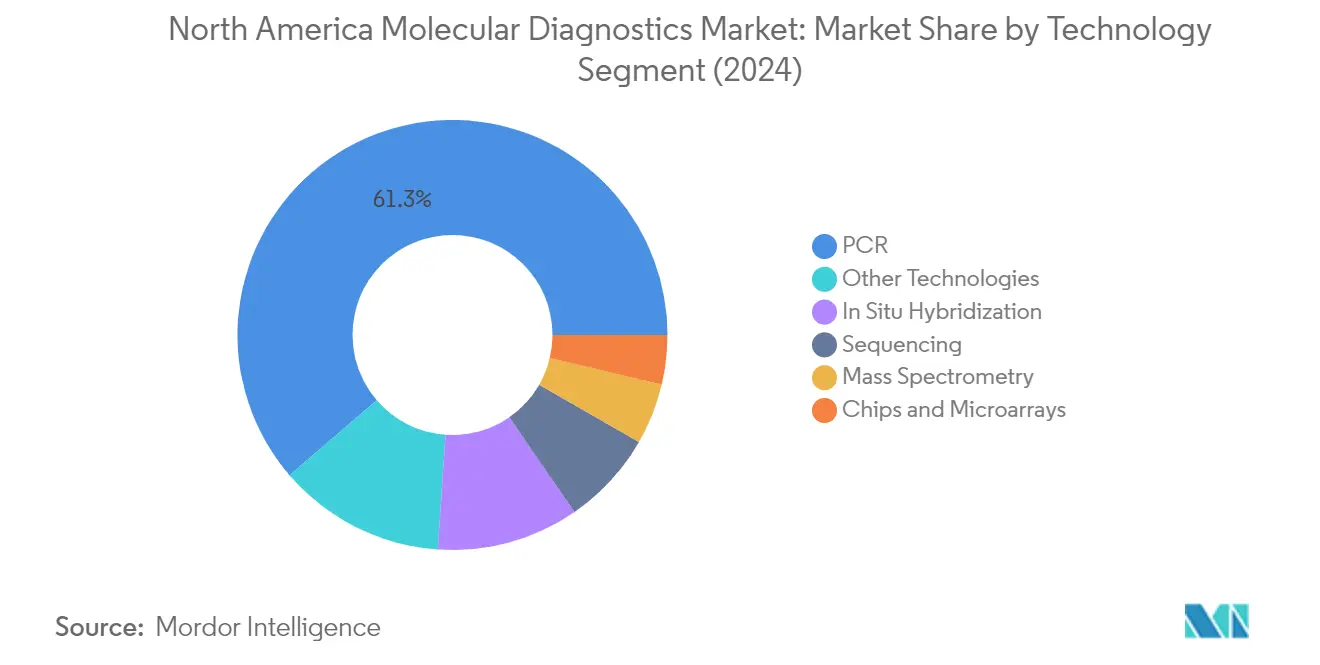

The Polymerase Chain Reaction (PCR) segment dominates the North America molecular diagnostics market, holding approximately 61% of the market share in 2024. This significant market position is attributed to PCR's widespread adoption in diagnostic laboratories and healthcare facilities across the region. The technology's versatility in detecting various genetic materials, coupled with its high accuracy and reliability, has made it the preferred choice for molecular testing. The segment's dominance is further strengthened by continuous technological advancements in PCR platforms, including the development of automated systems and real-time PCR capabilities that enhance testing efficiency and throughput. Additionally, the extensive application of PCR in infectious disease testing, genetic disorder screening, and oncology diagnostics has solidified its position as the cornerstone of molecular diagnostic testing in North America.

In Situ Hybridization Segment in North America Molecular Diagnostics Market

The In Situ Hybridization (ISH) segment is projected to exhibit the highest growth rate of approximately 7% during the forecast period 2024-2029. This robust growth is driven by the increasing adoption of ISH techniques in cancer diagnostics and research applications. The technology's ability to provide precise visualization and quantification of gene expression at the cellular level has made it invaluable in both clinical and research settings. The advancement of fluorescence in situ hybridization (FISH) and chromogenic in situ hybridization (CISH) techniques has expanded the application scope of ISH in detecting chromosomal abnormalities and gene amplifications. The segment's growth is further supported by ongoing technological innovations in probe design and detection methods, making ISH more sensitive and specific for various molecular pathology applications.

Remaining Segments in North America Molecular Diagnostics Market Technology Segmentation

The other significant segments in the North America molecular diagnostics market include Chips and Microarrays, Mass Spectrometry, Sequencing, and Other Technologies. Chips and Microarrays technology continues to play a crucial role in high-throughput genetic analysis and disease diagnosis. Mass Spectrometry has established itself as a powerful tool for protein analysis and biomarker detection. The Sequencing segment has gained prominence with the increasing adoption of next-generation sequencing technologies in clinical diagnostics. Other Technologies, including isothermal nucleic acid amplification and flow cytometry, contribute to the market's diversity by offering specialized solutions for specific diagnostic needs. Each of these segments brings unique capabilities to the molecular diagnostics landscape, addressing different aspects of disease diagnosis and monitoring.

Segment Analysis: By Application

Infectious Disease Segment in North America Molecular Diagnostics Market

The infectious disease segment continues to dominate the North America molecular diagnostics market, holding approximately 71% of the market share in 2024. This substantial market position is primarily driven by the increasing burden of infectious diseases across the region and the growing demand for rapid and accurate diagnostic solutions. The segment's prominence is further strengthened by the extensive application of molecular diagnostic techniques in detecting various pathogens, including respiratory infections, sexually transmitted diseases, and hospital-acquired infections. The continuous development of innovative molecular diagnostic solutions, particularly in areas of automated testing platforms and point-of-care diagnostics, has significantly enhanced the segment's market presence. Additionally, the segment's growth is supported by favorable reimbursement policies and increasing adoption of molecular testing in clinical laboratories across North America.

Oncology Segment in North America Molecular Diagnostics Market

The oncology segment is emerging as the fastest-growing segment in the North America molecular diagnostics market, with a projected growth rate of approximately 7% during the period 2024-2029. This remarkable growth is attributed to the increasing adoption of personalized medicine approaches in cancer treatment and the rising demand for early cancer detection methods. The segment is witnessing significant technological advancements in areas such as next-generation sequencing and digital PCR, enabling more precise and comprehensive cancer diagnostics. The expansion of molecular diagnostic applications in areas such as tumor profiling, treatment monitoring, and minimal residual disease detection is driving innovation in this segment. Furthermore, the growing focus on developing companion diagnostics for targeted cancer therapies and the increasing integration of molecular testing in routine cancer care protocols are contributing to the segment's rapid growth trajectory.

Remaining Segments in North America Molecular Diagnostics Market

The other segments in the North America molecular diagnostics market, including pharmacogenomics, genetic disease screening, human leukocyte antigen typing, and other applications, play crucial roles in different aspects of clinical diagnostics. The pharmacogenomics segment is gaining importance in personalized medicine applications, helping healthcare providers optimize drug therapies based on individual genetic profiles. Genetic disease screening continues to expand its applications in prenatal and newborn screening programs, while human leukocyte antigen typing remains essential in transplantation medicine. These segments are benefiting from ongoing technological advancements, increasing awareness about genetic testing, and growing adoption of precision medicine approaches in healthcare delivery.

Segment Analysis: By Product

Reagents Segment in North America Molecular Diagnostics Market

The reagents segment continues to dominate the North America molecular diagnostics market, accounting for approximately 84% of the total market revenue in 2024. This segment encompasses a comprehensive range of products including assay reagents, sample preparation reagents, control solutions, and test kits utilized in molecular diagnostic tests. The segment's prominence is driven by the increasing complexity of diseases and growing demand for early diagnosis, which necessitates the use of sophisticated reagent combinations in laboratories. The segment has maintained its leadership position due to the continuous need for reagents in various molecular diagnostic procedures, from routine testing to specialized diagnostic applications. Additionally, laboratories face increasing pressure to improve quality and provide rapid results, which drives the demand for reagents that can perform multiple functions efficiently. The segment's growth is further supported by technological advancements in reagent development and the increasing automation of molecular diagnostic procedures.

Remaining Segments in North America Molecular Diagnostics Market

The instruments and other products segments play vital complementary roles in the molecular diagnostics market. The instruments segment includes sophisticated equipment such as high-performance liquid chromatography (HPLC) systems, molecular diagnostic analyzers, mass spectrometry (MS) systems, nuclear magnetic resonance (NMR) devices, real-time PCR machines, and point-of-care testing devices. These instruments form the backbone of molecular diagnostic testing infrastructure in laboratories and healthcare facilities. The other products segment encompasses molecular panels, software solutions, and various supporting products that enhance the efficiency and accuracy of molecular diagnostic procedures. This segment is particularly important in providing data management solutions and workflow optimization tools that are essential for modern diagnostic laboratories. Both segments contribute to the overall ecosystem of molecular diagnostics by enabling accurate testing, efficient workflow management, and improved patient care delivery.

Segment Analysis: By End User

Laboratories Segment in North America Molecular Diagnostics Market

The laboratories segment continues to dominate the North America molecular diagnostics market, accounting for approximately 51% of the total market share in 2024. This significant market position is attributed to the presence of numerous accredited laboratories offering various diagnostic services including in-vitro diagnostics, companion diagnostics, and clinical diagnostics across the region. The segment's strength is further reinforced by the increasing adoption of automation in diagnostic laboratories, which has substantially enhanced testing efficiency and accuracy. Modern laboratories are equipped with high-quality equipment and advanced molecular diagnostic platforms that enable precise results and comprehensive testing capabilities. The segment's growth is also supported by strategic partnerships between market players and diagnostic labs, leading to continuous technological advancements and expanded service offerings. Additionally, these facilities maintain high standards through CLIA certification and CAP accreditation, ensuring reliable and standardized testing procedures across the network of diagnostic centers.

Hospitals Segment in North America Molecular Diagnostics Market

The hospitals segment is projected to exhibit the highest growth rate in the North America molecular diagnostics market during the forecast period 2024-2029, with an expected growth rate of approximately 5%. This accelerated growth is primarily driven by the increasing integration of molecular diagnostic facilities within hospital centers, enabling immediate access to testing services and faster turnaround times for results. Hospitals are increasingly establishing dedicated molecular diagnostic departments equipped with state-of-the-art testing platforms and automated systems. The segment's growth is further supported by the advantages of bulk purchasing power for reagents and kits, allowing hospitals to achieve significant cost efficiencies through economies of scale. Moreover, hospitals are actively forming strategic partnerships with diagnostic companies to enhance their testing capabilities and expand their service offerings. The trend toward establishing in-house molecular diagnostic facilities in hospitals is also being driven by the growing demand for rapid and accurate diagnostic results for improved patient care outcomes.

Remaining Segments in North America Molecular Diagnostics Market End User Segmentation

The other end users segment encompasses molecular diagnostic testing conducted in academic research laboratories, home care settings, and ambulatory surgical centers. These settings play a crucial role in advancing diagnostic capabilities through research and development activities, particularly in developing novel diagnostic tests for early disease detection. Academic research laboratories contribute significantly to the validation and development of new molecular diagnostic techniques, while home care settings are gaining prominence due to the increasing demand for point-of-care testing solutions. The segment is witnessing growing importance with the rise of personalized medicine and the increasing need for accessible diagnostic solutions outside traditional healthcare settings. Additionally, ambulatory surgical centers are expanding their diagnostic capabilities to provide comprehensive care services, contributing to the overall market growth.

Geography Analysis

North America Molecular Diagnostics Market in the United States

The United States dominates the North America molecular diagnostics market, holding approximately 87% of the total market share. The market's robust growth is driven by the high adoption of technologically advanced products, continuous product launches and innovations, and the presence of key market players. The country's well-established healthcare infrastructure and favorable reimbursement policies have significantly contributed to market expansion. Additionally, the increasing prevalence of chronic diseases, particularly cancer and cardiovascular conditions, has generated substantial demand for molecular diagnostic testing solutions. The presence of sophisticated research facilities and clinical laboratories has enabled the rapid implementation of new diagnostic technologies. Furthermore, the strong focus on preventive healthcare and early disease detection has created a conducive environment for market growth. The country's regulatory framework, while stringent, has been instrumental in maintaining high-quality standards and fostering innovation in molecular diagnostic technologies.

North America Molecular Diagnostics Market in Canada

Canada represents a dynamic market in the molecular diagnostics sector, projected to grow at approximately 5% CAGR from 2024 to 2029. The country's healthcare system's increasing focus on preventive care and early disease detection has been a significant growth driver. The rising proportion of the aging population, coupled with the growing burden of chronic diseases such as hypertension and cancer, has intensified the demand for advanced molecular diagnostic solutions. Canadian healthcare facilities have been actively adopting innovative diagnostic technologies to improve patient care outcomes. The country's robust research and development infrastructure has facilitated the development and validation of new molecular diagnostic tests. Moreover, the collaboration between academic institutions and diagnostic companies has accelerated technological advancements in the field. The government's supportive policies and investments in healthcare infrastructure have further strengthened the market's growth trajectory. Additionally, the increasing awareness among healthcare providers and patients about the benefits of molecular diagnostics has contributed to market expansion.

North America Molecular Diagnostics Market in Mexico

Mexico has emerged as a significant market for molecular diagnostics, driven by increasing healthcare expenditure and growing awareness about advanced diagnostic technologies. The country's healthcare system has been undergoing significant modernization, with a growing emphasis on incorporating advanced diagnostic solutions. The rising prevalence of infectious diseases and genetic disorders has created a substantial demand for molecular diagnostic tests. Mexico's expanding healthcare infrastructure and increasing access to advanced medical technologies have supported market growth. The country has also witnessed growing investments in research and development activities related to molecular diagnostics. Furthermore, the presence of both public and private healthcare facilities adopting molecular diagnostic technologies has contributed to market expansion. The increasing focus on personalized medicine and precision diagnostics has also driven the adoption of molecular diagnostic solutions. Additionally, collaborations between international diagnostic companies and local healthcare providers have enhanced the availability and accessibility of advanced diagnostic services.

North America Molecular Diagnostics Market in Other Countries

The molecular diagnostics market in other North American regions demonstrates varying levels of development and adoption. These regions have shown increasing interest in implementing advanced diagnostic technologies to improve healthcare delivery. The market dynamics in these areas are influenced by factors such as healthcare infrastructure development, government initiatives, and increasing awareness about molecular diagnostic technologies. Local healthcare providers are increasingly recognizing the importance of molecular diagnostics in improving patient care outcomes. The growing focus on preventive healthcare and early disease detection has created opportunities for market expansion. Additionally, partnerships between international diagnostic companies and local healthcare facilities have helped in technology transfer and market development. These regions are also witnessing gradual improvements in healthcare infrastructure and increasing investments in diagnostic capabilities. The trend towards personalized medicine and precision diagnostics has further stimulated interest in molecular diagnostic technologies.

Competitive Landscape

Top Companies in North America Molecular Diagnostics Market

The North America molecular diagnostics market features prominent players like F. Hoffmann-La Roche, Abbott Laboratories, Illumina, Hologic, Qiagen, and Danaher Corporation, who have established strong market positions through continuous innovation and strategic expansion. These companies have demonstrated remarkable operational agility, particularly evident in their rapid response to developing diagnostic solutions during the COVID-19 pandemic. Product innovation remains a key focus area, with companies investing substantially in research and development to introduce advanced molecular diagnostic testing platforms, automated systems, and expanded test menus. Strategic moves, including partnerships with healthcare providers, research institutions, and technology companies, have strengthened market presence, while geographical expansion efforts have focused on penetrating emerging markets and establishing regional manufacturing facilities. The industry has witnessed significant advancements in areas such as next-generation sequencing, PCR-based diagnostics, and point-of-care testing solutions, reflecting the companies' commitment to technological leadership.

Consolidated Market with Strong Growth Potential

The molecular diagnostics market in North America exhibits a relatively consolidated structure, dominated by large multinational conglomerates with diverse healthcare portfolios alongside specialized molecular diagnostics firms. These established players possess significant advantages in terms of research capabilities, manufacturing infrastructure, and distribution networks, creating substantial entry barriers for new entrants. The market has witnessed active merger and acquisition activity, with larger companies acquiring innovative startups and smaller firms to expand their technological capabilities and product portfolios. Companies like Danaher Corporation and Thermo Fisher Scientific have particularly pursued aggressive acquisition strategies to strengthen their market positions and acquire cutting-edge technologies.

The competitive dynamics are characterized by intense rivalry among established players, who compete primarily through product differentiation, technological innovation, and service quality. Market leaders have maintained their positions through substantial investments in research and development, strong intellectual property portfolios, and extensive distribution networks. The industry has seen increasing collaboration between diagnostic companies and pharmaceutical firms, particularly in developing companion diagnostics, while also witnessing the emergence of specialized players focusing on specific disease areas or technological platforms.

Innovation and Adaptability Drive Market Success

For incumbent companies to maintain and expand their market share, focusing on technological innovation and operational efficiency has become crucial. Success factors include developing integrated diagnostic platforms, expanding test menus, and improving automation capabilities to meet the growing demand for high-throughput testing. Companies must also strengthen their digital capabilities, including data analytics and artificial intelligence integration, while maintaining strong relationships with healthcare providers and regulatory bodies. The ability to adapt to changing healthcare needs, such as the recent pandemic response, while maintaining cost-effectiveness and quality standards, remains critical for market leadership.

New entrants and smaller players can gain ground by focusing on niche markets, developing specialized diagnostic solutions, and leveraging technological innovations to address unmet medical needs. The industry's regulatory environment continues to evolve, particularly regarding test validation and approval processes, making regulatory compliance expertise essential for success. While the risk of substitution from alternative diagnostic methods remains relatively low, companies must continue to demonstrate the clinical utility and cost-effectiveness of their molecular diagnostic solutions. Building strong relationships with laboratory chains, hospitals, and healthcare networks is crucial, as these end-users significantly influence market adoption and success.

North America Molecular Diagnostics Industry Leaders

Abbott Laboratories

Agilent Technologies

Danaher Corporation (Cepheid Inc)

F. Hoffmann-la Roche Ltd

Hologic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2022: Roche received the U.S. FDA premarket approval for the Cobas HIV-1 assay to be used with the Cobas 5800 System, a Class 2 exempt medical device in the United States. The assay offers a PCR testing solution that aids clinicians in diagnosing infectious diseases.

- June 2022: Bruker Corporation launched DART-EVOQ triple quadrupole mass spectrometer for high-throughput quantitative analyses to expand its mass spectrometry inside and outside the laboratory to Point-of-Need (PoN) offerings.

North America Molecular Diagnostics Market Report Scope

As per the scope of the report, molecular diagnostic tests detect specific sequences in DNA or RNA (including single nucleotide polymorphisms (SNP), deletions, rearrangements, insertions, and others), which may or may not be associated with diseases. The North America Molecular Diagnostics Market is Segmented by Technology (In-situ Hybridization, Chips and Microarrays, Mass Spectrometry, Sequencing, PCR, and Other Technologies), Application (Infectious Disease, Oncology, Pharmacogenomics, Microbiology, Genetic Disease Screening, Human Leukocyte Antigen Typing, and Blood Screening), Product (Instrument, Reagent, and Other Products), End User (Hospitals, Laboratories, and Other End Users), and Geography (United States, Canada, and Mexico). The report offers the value (in USD million) for the above segments.

By Technology

| In-situ Hybridization |

| Chips and Microarrays |

| Mass Spectrometry (MS) |

| Sequencing |

| PCR |

| Other Technologies |

By Application

| Infectious Disease |

| Oncology |

| Pharmacogenomics |

| Microbiology |

| Genetic Disease Screening |

| Human Leukocyte Antigen Typing |

| Blood Screening |

By Product

| Instrument |

| Reagent |

| Other Products |

By End User

| Hospitals |

| Laboratories |

| Other End Users |

Geography

| United States |

| Canada |

| Mexico |

| By Technology | In-situ Hybridization |

| Chips and Microarrays | |

| Mass Spectrometry (MS) | |

| Sequencing | |

| PCR | |

| Other Technologies | |

| By Application | Infectious Disease |

| Oncology | |

| Pharmacogenomics | |

| Microbiology | |

| Genetic Disease Screening | |

| Human Leukocyte Antigen Typing | |

| Blood Screening | |

| By Product | Instrument |

| Reagent | |

| Other Products | |

| By End User | Hospitals |

| Laboratories | |

| Other End Users | |

| Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How big is the North America Molecular Diagnostics Market?

The North America Molecular Diagnostics Market size is expected to reach USD 11.52 billion in 2025 and grow at a CAGR of 6.63% to reach USD 15.87 billion by 2030.

What is the current North America Molecular Diagnostics Market size?

In 2025, the North America Molecular Diagnostics Market size is expected to reach USD 11.52 billion.

Who are the key players in North America Molecular Diagnostics Market?

Abbott Laboratories, Agilent Technologies, Danaher Corporation (Cepheid Inc), F. Hoffmann-la Roche Ltd and Hologic Corporation are the major companies operating in the North America Molecular Diagnostics Market.

What years does this North America Molecular Diagnostics Market cover, and what was the market size in 2024?

In 2024, the North America Molecular Diagnostics Market size was estimated at USD 10.76 billion. The report covers the North America Molecular Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Molecular Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: