Pet DNA Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

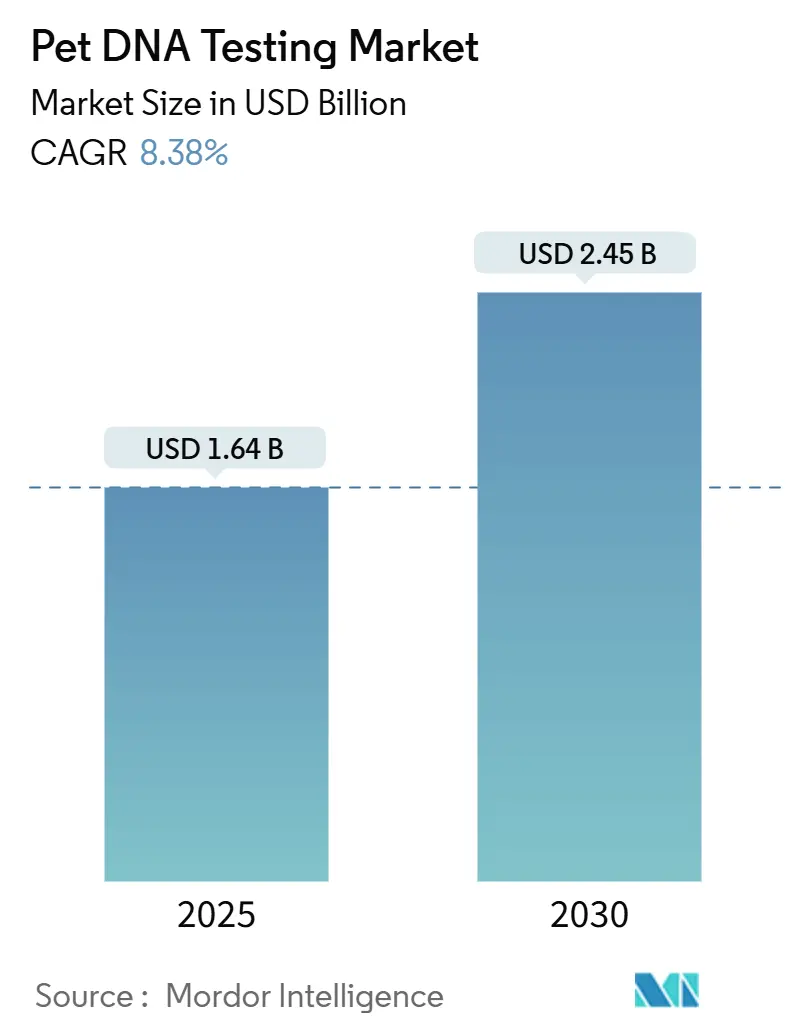

| Market Size (2025) | USD 1.64 Billion |

| Market Size (2030) | USD 2.45 Billion |

| Growth Rate (2025 - 2030) | 8.38% CAGR |

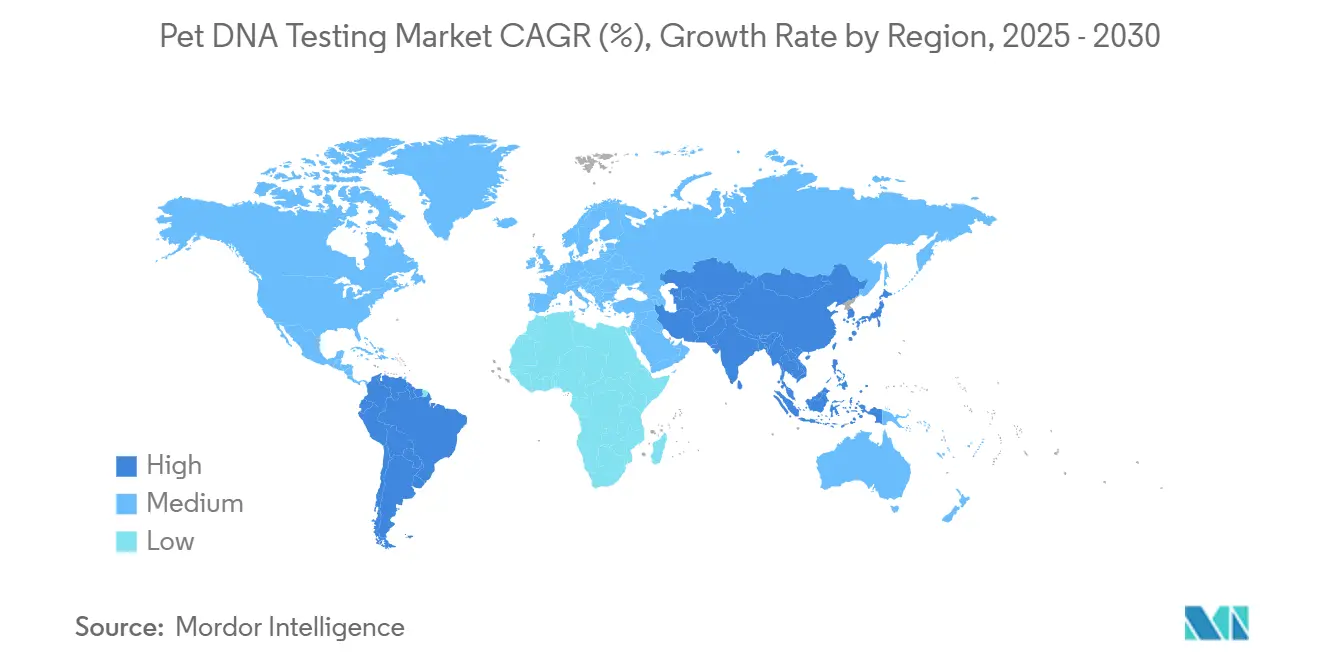

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet DNA Testing Market Analysis by Mordor Intelligence

The Pet DNA Testing Market size is estimated at USD 1.64 billion in 2025, and is expected to reach USD 2.45 billion by 2030, at a CAGR of 8.38% during the forecast period (2025-2030).

Demand climbs as next-generation sequencing (NGS) prices keep falling, direct-to-consumer (DTC) e-commerce simplifies access, and owners seek preventive insights that rival human genomics. The pet DNA testing market is also benefiting from steady upgrades in laboratory automation, deeper veterinary integration, and an expanding body of peer-reviewed evidence that validates clinical applications. Strategic consolidation—led by Mars Petcare, Zoetis, and a handful of niche innovators—continues to enlarge bio-repositories, sharpen test accuracy, and unlock cross-selling opportunities that extend from breed identification to oncology screening. Asia-Pacific is set to outpace every other region, translating growing pet-humanization and shrinking household sizes into double-digit test adoption. Meanwhile, the United States maintains a robust early-mover advantage as the Food and Drug Administration (FDA) elevates laboratory-developed tests (LDTs) to full medical-device status, a step that will force laggards to upgrade quality systems or exit the market.

Key Report Takeaways

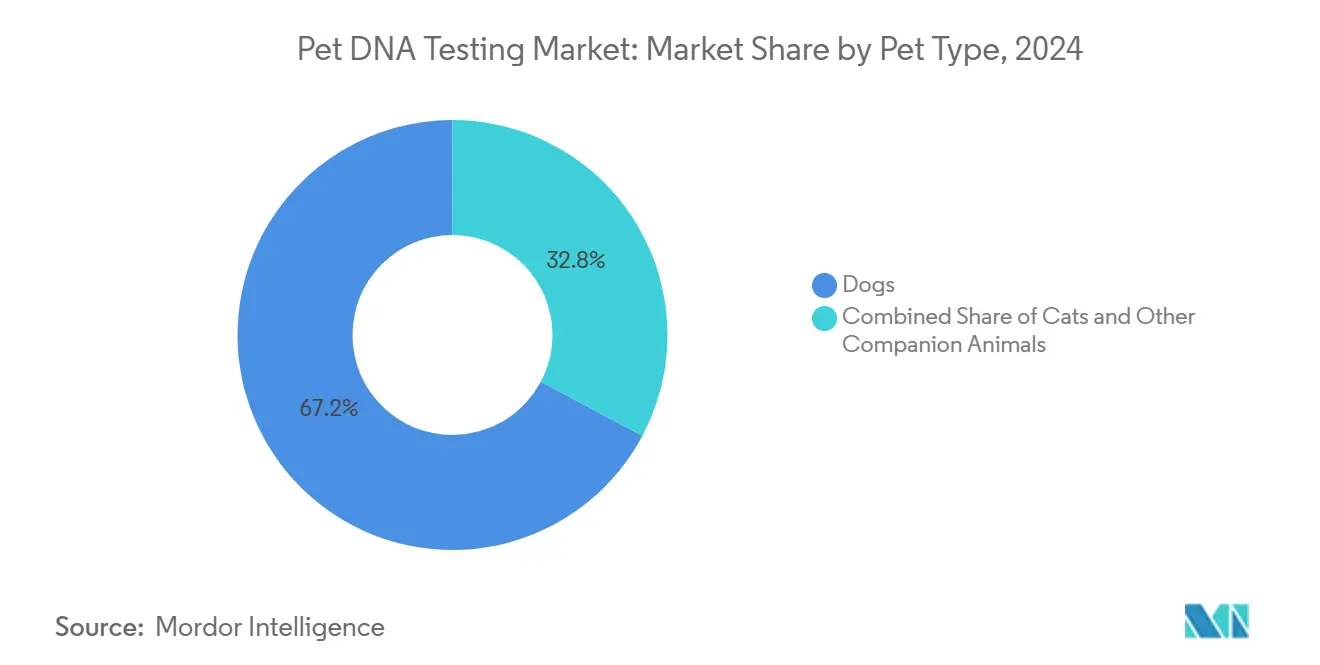

- By pet type, dogs secured 67.24% of the pet DNA testing market share in 2024, while cats are forecast to expand at a 12.39% CAGR through 2030.

- By test type, breed identification captured 51.88% of the pet DNA testing market size in 2024, whereas disease-specific testing is projected to grow at 11.44% CAGR to 2030.

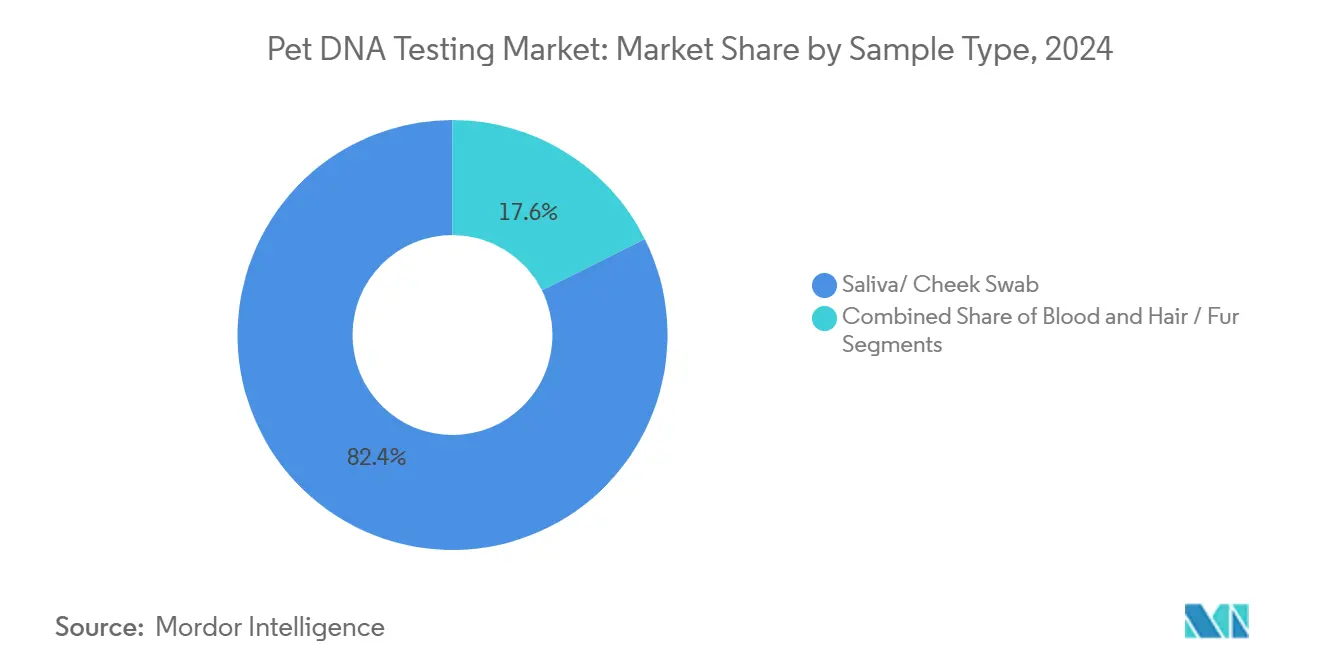

- By sample type, saliva/cheek swab commanded 82.37% share of the pet DNA testing market size in 2024, and blood collection shows the fastest 10.53% CAGR through 2030.

- By end user, individual pet owners accounted for 73.28% share of the pet DNA testing market size in 2024; veterinarians post the highest 12.03% CAGR through 2030.

- By geography, North America led with 44.33% revenue share in 2024, while Asia-Pacific is advancing at an 11.56% CAGR to 2030.

Global Pet DNA Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet-humanization | +2.1% | Global, strongest in APAC & North America | Medium term (2-4 years) |

| Technological advances in NGS & microarray | +1.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Proliferation of DTC e-commerce platforms | +1.4% | Global, accelerated in APAC | Short term (≤ 2 years) |

| Veterinary adoption of liquid-biopsy genomics | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Insurers introducing breed-specific premiums | +0.9% | North America & Europe | Long term (≥ 4 years) |

| Integration with smart-collar health IoT | +0.7% | North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet-Humanization Driving Demand for Advanced Wellness Insights

Urban consumers increasingly see pets as family members, and more than half of Chinese owners describe their animals as “children,” increasing willingness to purchase premium healthcare services such as genomics. Millennials and Gen Z households in Asia-Pacific are pushing premium pet-service spending up by 10% annually, reinforcing repeat purchases of DNA kits and ancillaries. Mars Petcare’s plan to enroll 20,000 animals in its Biobank exemplifies how large players convert emotional attachment into longitudinal genomic datasets. The combination of rising disposable income, smaller household sizes, and heightened preventive-care awareness underpins sustained growth for the pet DNA testing market. Veterinary clinics report more frequent wellness queries tied to breed-specific risks, further validating market momentum.

Technological Advances in NGS & Microarray Cut Test Costs

Illumina-based workflows let firms such as Basepaws interrogate more than 280 genetic markers at retail prices below USD 200, a steep drop compared with costs seen two years ago.[1]Basepaws Editorial Team, “Basepaws Launches the Most Extensive DNA Test for Dogs, Focused on Health and Early Detection of Disease Risk,” Basepaws, basepaws.comLow-pass whole-genome sequencing at 3.6× coverage delivers high single-nucleotide polymorphism concordance, trimming reagent budgets and turnaround times.[2]Dylan N. Clements, “A Cautionary Tale of Low-Pass Sequencing and Imputation with Respect to Haplotype Accuracy,” Genetics Selection Evolution, gsejournal.biomedcentral.com The FDA’s bioinformatics webinar on NGS data submissions signals regulatory comfort with modern pipelines, which reduces compliance uncertainty. Together these advances set a new baseline for comprehensive screening, making multi-panel tests the default offering in the pet DNA testing market.

Proliferation of DTC E-Commerce Platforms for Pet Care

Digital storefronts remove veterinary gatekeeping and enable straight-through fulfillment, accelerating the pet DNA testing market by broadening reach and reducing acquisition costs. Mars Petcare and other investors have poured capital into pet-tech start-u ps that blend genetic reports with subscription nutrition or insurance. Embark’s relative-finder tool adds social-network appeal and encourages re-testing as new relatives appear. Royal Canin counters with a clinic-only genetics service, evidencing channel tension as brands juggle professional endorsement with consumer convenience. Platform plurality ultimately grows market depth, giving consumers multiple on-ramps to genomic insights.

Veterinary Adoption of Liquid-Biopsy Genomics for Oncology Screening

Antech’s Nu.Q Canine Cancer Test detects roughly 75% of common malignancies from a simple blood draw, illustrating how liquid biopsy augments routine checkups. Peer-reviewed studies show cfDNA-based assays deliver 0.93 AUC in hemangiosarcoma detection, marking clinical viability.[3]Soohyun Ko et al., “Early Detection of Canine Hemangiosarcoma via cfDNA Fragmentation and Copy Number Alterations in Liquid Biopsies Using Machine Learning,” Frontiers in Veterinary Science, frontiersin.org Early screening aligns with veterinarians’ preventive ethos and opens recurring revenue from serial monitoring. As more clinics integrate these tests into standard protocols, the pet DNA testing market gains a durable veterinary revenue stream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of test-accuracy standards & regulatory oversight | -1.6% | Global, most acute in developing markets | Short term (≤ 2 years) |

| High price sensitivity in emerging markets | -1.3% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Owner data-privacy concerns over genomic sharing | -0.9% | Europe (GDPR), North America | Long term (≥ 4 years) |

| Veterinarian skepticism due to weak phenotype correlation | -0.7% | Global, particularly developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Test-Accuracy Standards & Regulatory Oversight

A University of Colorado study found significant inter-company variance in breed calls, and some vendors appear to over-weight customer photos when generating reports. FDA plans to phase out enforcement discretion on LDTs by 2028, mandating full device-level validation that could lift compliance costs and spark consolidation. Inconsistent reference databases and voluntary labeling let firms market “high accuracy” without peer verification, fueling consumer mistrust. Short-term uncertainty may slow discretionary purchases in the pet DNA testing market until standards converge.

High Price Sensitivity in Emerging Markets

Although pet ownership is soaring in India and Vietnam, household income levels constrain spending on premium diagnostics. Tiered pricing—for example, USD 198 for basic parentage versus USD 398 for comprehensive feline panels—shows vendors experimenting with cost-down strategies. Currency fluctuations and import duties further widen the affordability gap, limiting penetration outside Tier-1 cities. Firms will need to localize product-market fit, bundle services, or adopt subscription models to capture these price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Retain Scale While Cats Accelerate

Dogs contributed the highest absolute revenue in 2024, anchored by 67.24% pet DNA testing market share and a deep reservoir of validated breed markers. Vendors exploit canines’ long pedigree history to cross-sell health and ancestry panels that command premium pricing. Cats, while starting from a smaller base, show a 12.39% CAGR that outpaces every other companion group as new feline-specific markers and oncology assays reach market. The pet DNA testing market size linked to feline services is expected to climb sharply through research collaborations such as Darwin’s Ark and Hill’s Pet Nutrition.

Growth drivers for canines now hinge on advanced offerings—including liquid biopsy and pharmacogenomics—because basic breed tests approach saturation. In contrast, cats benefit from a discovery phase where each incremental marker vastly improves diagnostic value. Strategic product roadmaps therefore allocate R&D toward feline panels and mixed-species innovations, aiming to diversify revenue as the dog segment matures.

By Test Type: Disease-Specific Panels Gain Traction

Breed identification still held 51.88% of revenue in 2024, reflecting consumer fascination with lineage. Yet disease-specific kits are forecast to deliver the fastest 11.44% CAGR, underlining a pivot toward clinical utility. The pet DNA testing market size attributable to oncology and cardiomyopathy screening rises with every new mutation validated in peer-reviewed literature.

While health-predisposition packages offer middle-ground value, vendors increasingly bundle them with disease panels to enhance stickiness. Machine-learning algorithms now mine sequence data to flag multi-gene risk profiles, bolstering veterinarian confidence. As insurers start linking premiums to genomic risk, demand for these high-specificity panels should intensify, further redefining revenue mix.

By Sample Type: Non-Invasive Dominance Meets Clinical Precision

Saliva or cheek swab provided 82.37% of 2024 revenue because consumers prize painless self-collection and mail-in simplicity. This share makes saliva the linchpin of the direct-to-consumer branch of the pet DNA testing market. Blood-based assays, growing at 10.53% CAGR, supply higher DNA concentration vital for copy-number and cfDNA analyses used in cancer detection.

Retail brands often upsell clinic-collected blood tests as add-ons when owners seek advanced insights, thereby unlocking hybrid revenue between online and brick-and-mortar channels. Hair and fur remain niche due to degradation concerns, yet ongoing improvements in extraction chemistry could make them viable for specific trait screens.

By End User: Veterinarians Rise as Clinical Gatekeepers

Individual pet owners still dominate sales with 73.28% revenue share in 2024 because DTC kits offer instant gratification and gifting appeal. Marketing campaigns around holidays keep this channel vibrant. Yet veterinarian purchases are growing 12.03% CAGR as practices embed genomic insights into annual wellness exams, therapeutics decisions, and breed-specific counseling.

The pet DNA testing market is gradually rebalancing toward a dual-channel model wherein clinics validate or augment DTC findings, boosting credibility. Breeders and shelters rely on panel screens to manage hereditary diseases, reinforcing responsible breeding standards, while research institutes push discovery pipelines that ultimately feed commercial panels.

Geography Analysis

North America continues to anchor 44.33% of global revenue, reflecting mature pet care culture, high disposable income, and early adoption of genetic wellness products. Regulatory transparency from the FDA and a dense network of accredited labs accelerate product rollouts, while mega-players like Zoetis expand reference labs to increase turnaround speed . Vendor focus now pivots to deeper clinical integration, anticipating the LDT sunset rule that will reward early compliance.

Asia-Pacific, projected to post an 11.56% CAGR, is the fastest-growing theater, driven by shrinking birth rates and rising pet substitution. Goldman Sachs expects China’s urban pet population to top 70 million by 2030, nearly doubling the count of children under four. Rapid e-commerce adoption lowers barriers, but price sensitivity forces localized SKUs and tiered services. Countries such as South Korea and Japan show strong uptake of premium companion diagnostics, while India demonstrates volume potential once costs align with local purchasing power.

Latin America, the Middle East, and Africa collectively remain under 10% of global sales today. Limited veterinary infrastructure and import tariff regimes constrain penetration. Nonetheless, growing middle-class households in Brazil, Saudi Arabia, and South Africa present future upside, especially if vendors collaborate with regional distributors to mitigate logistics costs. Localization of reference genomic databases will also be crucial to improve test relevance for non-Western breeds.

Competitive Landscape

The pet DNA testing market sits in a moderately consolidated phase. Mars Petcare’s recent acquisitions of Heska and Cerba Vet/ANTAGENE amplify its data footprint and broaden cross-linkages between consumer and veterinary diagnostics. Zoetis counters via Basepaws and a growing network of state-of-the-art labs, leveraging its entrenched veterinary relationships to scale rapidly. Embark positions itself as the academic partner of choice, co-developing panels with Cornell University, while Royal Canin plays to veterinarian exclusivity, guarding premium brand equity.

Technology differentiation hinges on database depth, NGS throughput, and AI analytics that convert raw sequence into actionable wellness insights. Vendors also vie for smart-device partnerships that fuse genomic and biometric data, forming holistic health ecosystems. The FDA’s tighter oversight will likely squeeze smaller entrants that lack capital for validation studies, pushing the market toward an oligopoly of well-funded players.

White-space growth opportunities lie in emerging-market localization, companion species beyond dogs and cats, and subscription models that pair periodic sequencing with nutrition, insurance, or tele-vet access. Competitive intensity therefore remains high as companies race to lock in pet lifetime value across multiple service verticals.

Pet DNA Testing Industry Leaders

Mars Petcare

Embark Veterinary

Zoetis

DNA My Dog

Orivet Genetics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wisdom Panel scientists uncover an SLAMF1 variant linked to canine atopic dermatitis, enabling targeted breeding programs.

- May 2025: PooPrints partners with Ancestry to bundle breed and health insights into its DNA-based waste-management registry.

- April 2025: Mars Petcare finalizes the Cerba Vet and ANTAGENE acquisition, enhancing European diagnostics reach.

- March 2025: Wisdom Panel surpasses 5 million pets tested, marking a two-decade milestone in consumer genomics.

Global Pet DNA Testing Market Report Scope

| Dogs |

| Cats |

| Other Companion Animals |

| Breed Identification |

| Health Predisposition / Carrier Status |

| Trait & Physical Characteristics |

| Disease-Specific (e.g., Cancer Liquid Biopsy) |

| Saliva / Cheek Swab |

| Blood |

| Hair / Fur |

| Individual Pet Owners (DTC) |

| Veterinarians |

| Breeders & Shelters |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pet Type | Dogs | |

| Cats | ||

| Other Companion Animals | ||

| By Test Type | Breed Identification | |

| Health Predisposition / Carrier Status | ||

| Trait & Physical Characteristics | ||

| Disease-Specific (e.g., Cancer Liquid Biopsy) | ||

| By Sample Type | Saliva / Cheek Swab | |

| Blood | ||

| Hair / Fur | ||

| By End User | Individual Pet Owners (DTC) | |

| Veterinarians | ||

| Breeders & Shelters | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will the pet DNA testing market grow through 2030?

It is forecast to rise from USD 431.23 million in 2025 to USD 687.27 million by 2030, reflecting a 9.77% CAGR.

Which species contribute most to revenue today?

Dogs account for 67.24% of 2024 revenue thanks to extensive breed databases and high consumer awareness.

Why is Asia-Pacific considered the fastest-growing region?

Urban pet-humanization and shrinking family sizes push an 11.56% CAGR, aided by rapid e-commerce adoption.

What segment shows the quickest uptake among test types?

Disease-specific panels, especially those targeting cancer, are expanding at 11.44% CAGR through 2030.

How will FDA regulation affect suppliers?

LDTs will be treated as medical devices by 2028, so companies must validate accuracy and upgrade quality systems or risk market exit.

Are blood samples replacing saliva kits?

Saliva remains dominant for DTC kits, but blood collection is growing faster because it supports high-precision liquid biopsies used in clinics.

Page last updated on: