Forensic Imaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

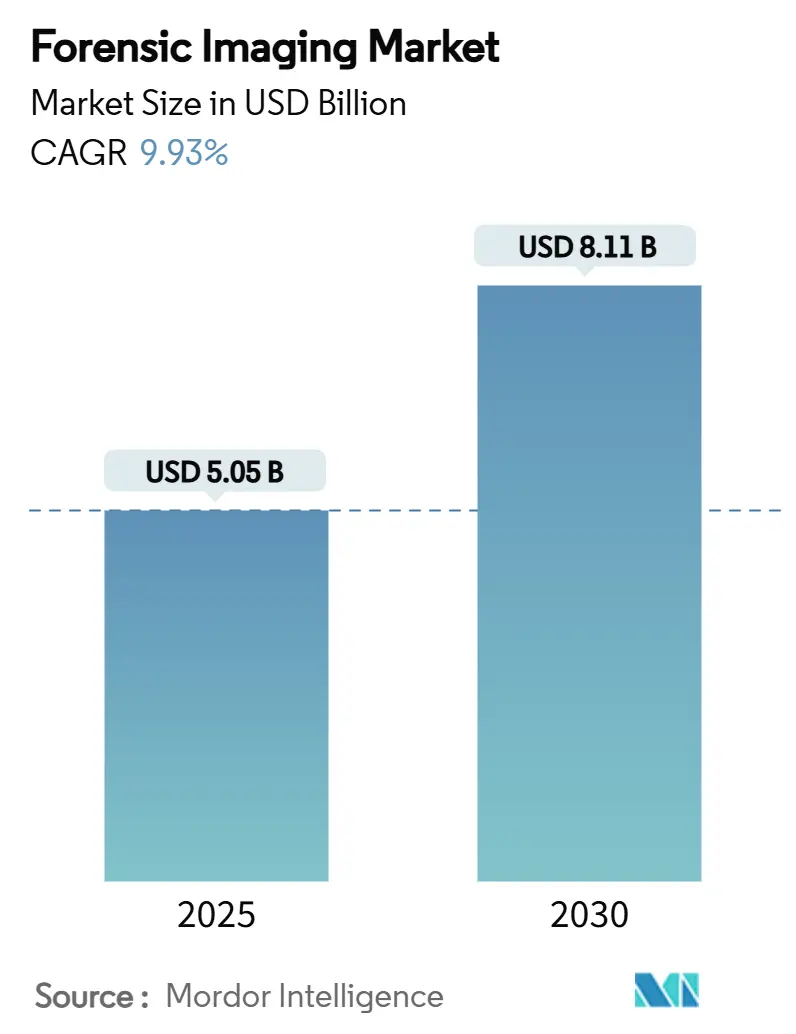

| Market Size (2025) | USD 5.05 Billion |

| Market Size (2030) | USD 8.11 Billion |

| Growth Rate (2025 - 2030) | 9.93% CAGR |

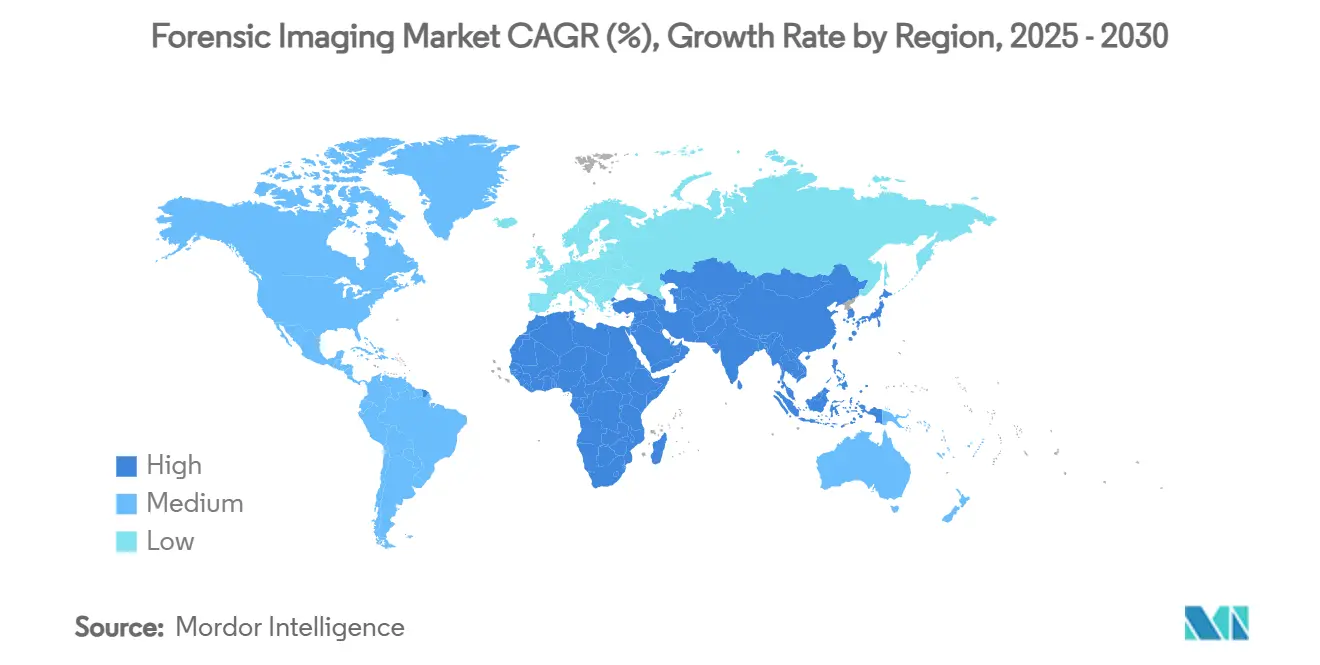

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

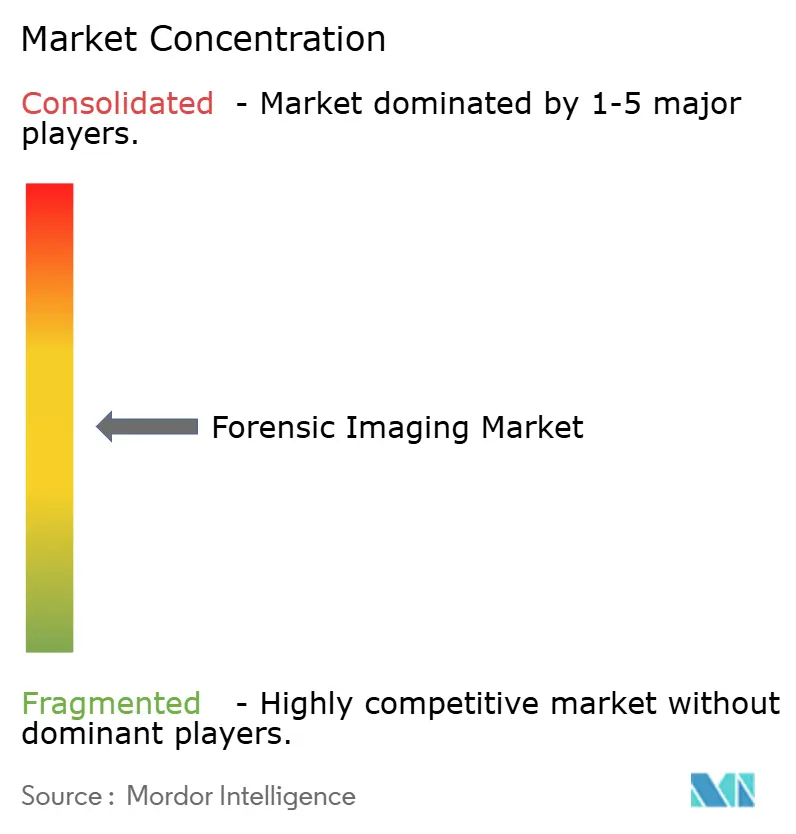

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forensic Imaging Market Analysis by Mordor Intelligence

The forensic imaging market size stands at USD 5.05 billion in 2025 and is projected to reach USD 8.11 billion by 2030, reflecting a 9.93% CAGR. This sustained expansion signals how rapidly courts, investigators, and medical examiners are embracing advanced visual-evidence tools. Momentum comes from rising acceptance of digital exhibits in court, faster turnaround expectations in criminal investigations, and the growing need to handle sensitive post-mortem cases with minimal invasiveness. Vendors that pair high-resolution scanners with artificial-intelligence-driven analytics are enjoying faster order cycles, while cloud-enabled archives are starting to unlock cross-border collaboration despite lingering privacy concerns. Capital-budget pressure, however, still limits adoption in smaller laboratories; many either lease equipment or rely on regional centers of excellence for complex scans.

Key Report Takeaways

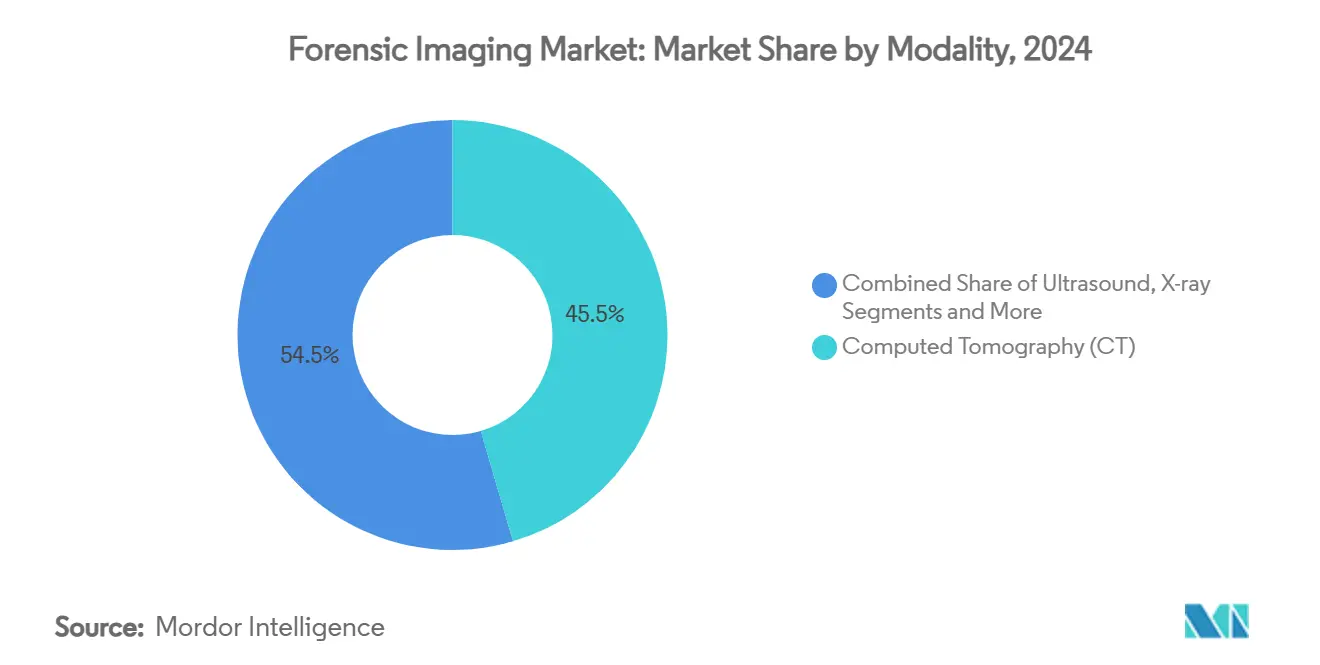

- By modality, computed tomography captured 45.46% of forensic imaging market share in 2024. Micro-CT and nano-CT are advancing at a 13.57% CAGR through 2030, the fastest pace among modalities.

- By component, hardware accounted for 56.24% of the forensic imaging market size in 2024. Software is projected to expand at a 12.32% CAGR between 2025-2030.

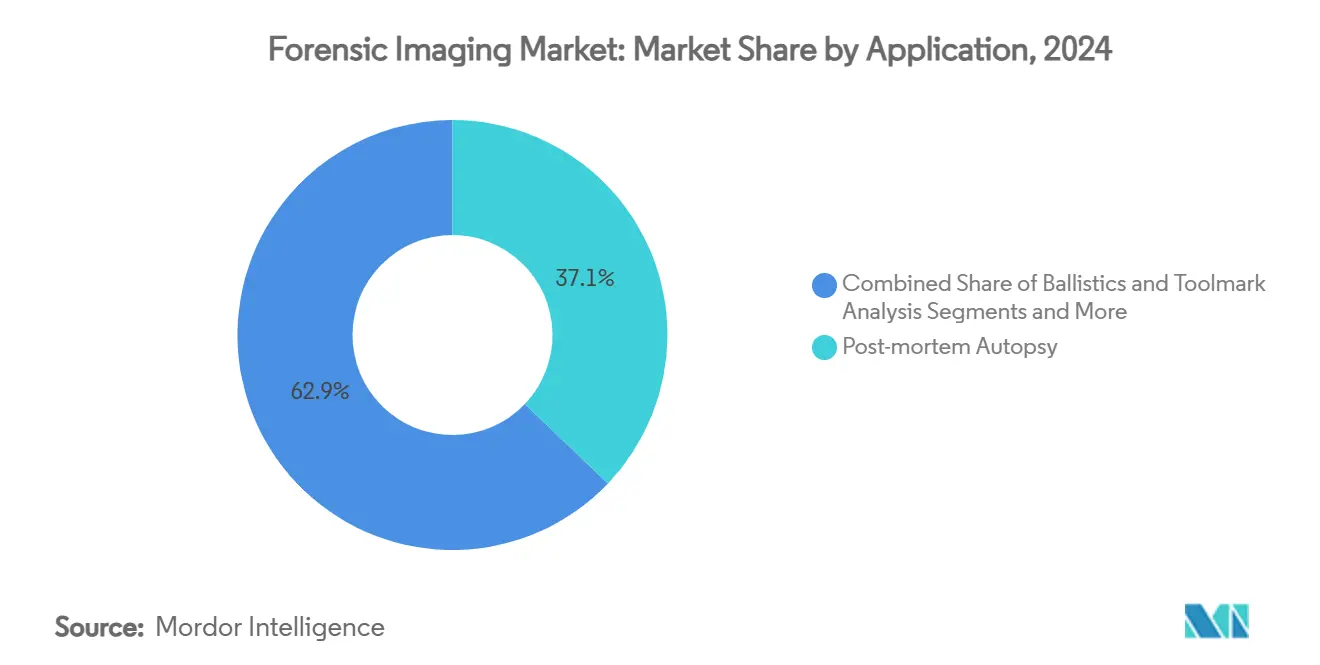

- By application, post-mortem autopsy held 37.13% revenue in 2024, while crime-scene reconstruction is forecast to climb 13.57% annually to 2030.

- By end user, Forensic laboratories represented 39.43% of end-user spending in 2024; independent practitioners show the highest growth outlook at 12.67% CAGR.

- By geography, North America led with 37.65% share in 2024; Asia-Pacific is expected to grow 11.14% annually to 2030.

Global Forensic Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virtopsy adoption for minimally invasive autopsy | +2.1% | Europe, North America, global roll-out | Medium term (2-4 years) |

| Judicial acceptance of digital evidence | +1.8% | North America, EU, APAC spill-over | Long term (≥ 4 years) |

| 3D imaging plus AI for crime-scene reconstruction | +2.3% | Developed markets worldwide | Short term (≤ 2 years) |

| Government funding for lab modernization | +1.7% | Asia-Pacific core, MEA spill-over | Medium term (2-4 years) |

| Portable systems for wildlife forensics | +0.9% | Conservation hotspots worldwide | Long term (≥ 4 years) |

| Low-dose micro-CT for historical-remains work | +0.8% | Europe, North America, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Virtopsy for Minimally Invasive Autopsy

Digital autopsy procedures let pathologists inspect internal injuries without cutting tissue, an advantage in regions where cultural or religious norms discourage conventional autopsies. High-resolution CT and MRI scans paired with automated segmentation can reveal trauma patterns, foreign objects, or disease markers in a format easily shared with investigating officers. Researchers recently demonstrated fully segmented mummy scans that preserved ancient specimens intact.[1]Ahmed Hassan, “Automated Segmentation of Microtomography Imaging of Egyptian Mummies,” NCBI, ncbi.nlm.nih.gov Following the 2024 launch of the Philippine National Forensics Institute, several Southeast-Asian states budgeted for virtopsy suites, expanding the forensic imaging market in lower-income economies. When trauma is complex—multiple gunshot wounds, blast injuries, or decomposed remains—the technique also safeguards evidence integrity, reducing chain-of-custody disputes in court.

Increasing Judicial Acceptance of Digital Evidence

Courts today routinely weigh 3D crime-scene reconstructions, CT slice stacks, and AI-enhanced video during deliberations. ISO/IEC 27042 guidelines require continuity, validity, and reproducibility, forcing vendors to embed audit trails and immutability checks into imaging platforms.[2]ISO/IEC 27042 Working Group, “Digital Evidence Examination,” iso27001security.com While the 2024 Washington v. Puloka ruling excluded an AI-filtered video due to protocol gaps, the decision also clarified the validation data judges expect—a roadmap for vendors and practitioners to align workflows. When 3D models improve juror comprehension of ballistic trajectories, admissibility tends to follow, but inconsistency among jurisdictions still fragments global uptake.

Integration of 3D Imaging with AI for Crime-Scene Reconstruction

Deep-learning pipelines can now label hard-to-spot toolmarks, estimate victim age from skull images with high accuracy, and auto-register disparate photo sets into millimeter-precise 3D meshes.[3]Bum-Joo Cho, “Estimating Infant Age from Skull X-ray Images Using Deep Learning,” Nature Scientific Reports, nature.com Early adopters report faster case closure and reduced technician-hours, a compelling savings metric for budget committees. Neural networks that process thermal and hyperspectral frames add layers of evidence otherwise invisible to the human eye. Barriers remain—high-performance compute clusters and specialist training—but subscription-based cloud services are lowering entry costs for midsized labs.

Government Funding for Forensic-Lab Modernization

National grant programs have pivoted toward digital-evidence infrastructure. The U.S. National Institute of Justice earmarked funds in 2025 for high-throughput CT scanners as part of its broader backlog-reduction initiative. India and the Philippines now bundle imaging hardware, data-management platforms, and multi-year training into single tenders, putting holistic solutions ahead of piecemeal purchases. Vendors able to certify interoperability with ISO and SWGDE protocols win more bids, shaping product-road-map priorities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced imaging systems | -1.9% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shortage of trained forensic-imaging specialists | -1.4% | Worldwide, especially APAC & MEA | Medium term (2-4 years) |

| Inconsistent admissibility standards for 3D imaging | -1.1% | North America, EU focus | Long term (≥ 4 years) |

| Data-privacy worries around cloud archives | -0.8% | EU, North America, rising globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Imaging Systems

A multi-slice CT rig suitable for virtopsy can exceed USD 3 million, an outlay that also demands shielded rooms and heavy-duty power feeds. Smaller county labs often postpone upgrades or rely on regional hubs, dampening total equipment orders. Leasing helps, yet contract clauses sometimes restrict mid-cycle software refreshes, locking buyers into five-year technology without AI extensions.

Shortage of Trained Forensic-Imaging Specialists

Modern systems call for cross-disciplinary talent—radiology, coding, forensic methodology. Global supply of such professionals lags demand, and salaries have climbed accordingly. Several governments now subsidize certificate programs, but many graduates prefer clinical radiology roles with higher pay, prolonging the skills gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: CT anchors adoption while micro-CT races ahead

Computed tomography commanded 45.46% of the forensic imaging market share in 2024, underscoring its role as the default scan for virtual autopsy and internal-injury mapping. Micro-CT and nano-CT together are projected to expand at a 13.46% CAGR to 2030, driven by laboratories that need sub–100 µm resolution for trace evidence and heritage-remains work. X-ray digital radiography remains relevant because it is portable and budget-friendly, enabling rural facilities to participate in the forensic imaging market without major infrastructure changes. Magnetic-resonance imaging is gaining traction for soft-tissue pathology and post-mortem clot detection, supported by new low-field systems that reduce installation costs. Surface-scanning and photogrammetry units are recording brisk orders as agencies shift from paper sketches to millimeter-precise 3D models for scene documentation.

CT's dominance rests on its ability to deliver stackable slice data that integrates smoothly with AI segmentation pipelines, shortening examination time. The modality's share is also protected by hospital co-usage, which pushes annual scanner utilization above 80% in high-population regions. Micro-CT's upside hinges on heritage institutions that now budget for dual-use scanners able to handle both archaeological and criminal-case specimens. Thermal imaging and hyperspectral cameras remain niche but are posting double-digit growth in wildlife-crime units, where hidden wounds or contraband markings require non-visible-spectrum capture. Continuous software upgrades allow older X-ray suites to add AI capabilities, extending hardware life cycles and tempering capital-spending spikes.

By Component: Hardware dominates but software sets the pace

Hardware held 56.24% of forensic imaging market revenue in 2024 because every lab must first invest in scanners, detectors, and shielding before running analyses. The software segment is projected to grow 12.32% annually through 2030 as AI automates segmentation, age estimation, and toolmark comparison, shifting revenue toward subscriptions. Vendors now bundle chain-of-custody encryption into viewing platforms to align with ISO/IEC 27042 evidence-integrity rules. Cloud-enabled analysis is catching on in regions with clear data-sovereignty guidance, although many EU labs still keep primary archives on-premise to satisfy GDPR obligations. Services—covering calibration, training, and remote reads—add resilience for laboratories that lack in-house expertise.

Growth on the hardware side continues as emerging economies build greenfield forensic campuses and replace analog X-ray rooms with 64-slice CT systems. Yet margins are shifting toward feature-rich software modules that slot into existing scanners, letting agencies defer costly replacements. Deep-learning packages now estimate adolescent clavicle age within two years of ground truth, a capability that improved courtroom confidence in 2025 trials. Vendors that combine hardware sales with multi-year service agreements win tenders because they solve staffing gaps as well as technology needs. Such wrap-around contracts boost recurring revenue and deepen customer lock-in, subtly raising the long-term forensic imaging market share of full-line suppliers.

By Application: Reconstruction surges while autopsy stays core

Post-mortem autopsy accounted for 37.13% of 2024 revenue and remains the backbone of the forensic imaging market; many jurisdictions now mandate a CT scan for every suspicious death. Crime-scene reconstruction is projected to rise 13.57% annually to 2030, fueled by investigators who need navigable 3D environments that clarify bullet trajectories and blood-spatter angles for juries. Ballistics and toolmark units rely on micro-CT to study rifling grooves without touching the projectile, preserving pristine evidence for later confirmation. Wildlife-forensics imaging is no longer fringe, as customs officers deploy portable CT to verify ivory seizures within hours. Pattern-and-trace documentation also benefits from photogrammetry that captures shoe impressions in under a minute at sub-millimeter fidelity.

The appeal of reconstruction tools lies in their courtroom impact; immersive fly-throughs reduce juror confusion and cut expert-witness time, making prosecutors willing to fund upgrades. Autopsy imaging continues to expand through virtopsy programs that respect cultural or religious limits on invasive procedures while improving diagnostic accuracy. Age-estimation protocols using skull-based AI shorten unidentified-victim workflows and lessen morgue storage backlogs. Wildlife applications attract NGO grants, diversifying revenue and cushioning public-budget swings. Expanding use cases are making imaging essential rather than a specialist add-on, driving growth in the forensic imaging market.

By End User: Labs lead but independents accelerate

Forensic laboratories generated 39.43% of 2024 demand because they process bulk caseloads and hold accreditation for evidence submission. Independent practitioners, though smaller in absolute dollars, are slated for 12.67% CAGR as courts increasingly seek outside experts to avoid perceived bias. Hospitals and academic medical centers leverage existing scanners to perform virtopsy work after clinical hours, boosting scanner utilization and lowering per-case cost. Law-enforcement agencies now purchase portable X-ray or CT vans for bomb-scene sweeps and clandestine-grave searches, spreading imaging closer to the point of investigation. Research institutes secure grants to refine protocols that later migrate into frontline practice, seeding future equipment refresh cycles.

Private experts often rent scanner time or partner with hospitals, lifting market penetration without large capital outlays. Their rise also spurs demand for user-friendly software that can run on standard workstations instead of dedicated clusters. Public labs respond by expanding service menus—such as rapid 48-hour CT reads—to retain clients and protect their forensic imaging market share. University programs train the next cohort of imaging technologists, addressing the skills shortage that otherwise constrains growth. Collaboration among all user groups accelerates protocol standardization, reinforcing admissibility and amplifying the forensic imaging market size outlook.

Geography Analysis

North America generated 37.65% of 2024 revenue, buoyed by long-standing grant programs and comprehensive accreditation frameworks. Federal funds helped smaller counties access high-slice CT systems, while national working groups published imaging protocols that courts readily cite. Deep-learning clavicle-age models refined in U.S. centers demonstrate how academic-forensic collaboration accelerates innovation. Nonetheless, data-privacy debates regarding cloud backups continue, prompting some states to mandate in-country storage.

Asia-Pacific is the fastest-growing region, tracking 11.14% CAGR through 2030. India, the Philippines, and Indonesia each broke ground on modern forensic campuses in 2024-2025, allotting funds not just for scanners but also fiber networks and AI workstations. Training remains a pressing need; many governments finance overseas fellowships or invite vendor-led boot camps. Currency fluctuations occasionally delay tenders, yet population size, urbanization, and judicial backlogs make APAC the long-term growth engine for the forensic imaging market.

Europe ranks third by value but first in cross-border standardization. GDPR compliance influences hardware encryption modules and pushes vendors toward zero-knowledge cloud architectures. Research grants in Germany, France, and the Nordics sponsor cultural-heritage scans—mummies, medieval remains, historic timber—blurring boundaries between archaeology and criminology. These dual-use projects sustain demand even when police budgets tighten

Competitive Landscape

Market fragmentation defines the current phase: no vendor tops a 10% global revenue share across all modalities. Large medical-imaging firms leverage existing MRI and CT lines but face competition from specialists in micro-CT, photogrammetry, and crime-scene lidar. Software pure-plays gain traction by licensing AI modules agnostic of scanner brand, attracting labs looking to stretch hardware lifespans. Strategic alliances—hardware maker plus AI startup plus cloud-storage vendor—now appear in most bid documents as buyers favor turnkey solutions.

Training services are increasingly bundled with equipment, a response to the skills shortage. Firms operating mobile training academies win goodwill and often secure follow-on maintenance contracts. Patent activity concentrates on automated segmentation and digital-evidence chain-of-custody logging. Portable systems form a white-space arena: ruggedized CT backpacks, drone-mounted thermal cameras, and handheld X-ray tablets are still rare but drawing venture funding

Forensic Imaging Industry Leaders

Canon Medical Systems

GE HealthCare

FARO Technologies

Leica Microsystems

Carl Zeiss AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bayer launched Centafore™, an Imaging Core Lab unit offering contract services that span clinical-trial support and SaMD validation.

- February 2025: Canon Healthcare USA bought a Cleveland facility to serve as headquarters and imaging-innovation hub in partnership with Cleveland Clinic

- April 2024: The U.S. National Institute of Justice released dental-radiograph-based age-estimation guidelines accepted under Daubert standards

Global Forensic Imaging Market Report Scope

| X-ray (Digital Radiography) |

| Computed Tomography (CT) |

| Magnetic Resonance Imaging (MRI) |

| Micro-CT & Nano-CT |

| Ultrasound |

| 3D Surface & Photogrammetry |

| Thermal Imaging |

| Other Emerging Modalities |

| Hardware |

| Software |

| Services |

| Post-mortem Autopsy (Virtopsy) |

| Crime-Scene Reconstruction |

| Ballistics & Toolmark Analysis |

| Age Estimation & Identification |

| Pattern & Trace Evidence Documentation |

| Wildlife Forensics |

| Other Applications |

| Forensic Laboratories |

| Hospital & Academic Medical Centers |

| Law-Enforcement Agencies |

| Research Institutes & Universities |

| Independent Forensic Practitioners |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | X-ray (Digital Radiography) | |

| Computed Tomography (CT) | ||

| Magnetic Resonance Imaging (MRI) | ||

| Micro-CT & Nano-CT | ||

| Ultrasound | ||

| 3D Surface & Photogrammetry | ||

| Thermal Imaging | ||

| Other Emerging Modalities | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | Post-mortem Autopsy (Virtopsy) | |

| Crime-Scene Reconstruction | ||

| Ballistics & Toolmark Analysis | ||

| Age Estimation & Identification | ||

| Pattern & Trace Evidence Documentation | ||

| Wildlife Forensics | ||

| Other Applications | ||

| By End User | Forensic Laboratories | |

| Hospital & Academic Medical Centers | ||

| Law-Enforcement Agencies | ||

| Research Institutes & Universities | ||

| Independent Forensic Practitioners | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the global value of the forensic imaging market in 2025?

The market is valued at USD 5.05 billion in 2025.

How fast is the forensic imaging market expected to grow?

It is forecast to record a 9.93% CAGR and reach USD 8.11 billion by 2030.

Which modality leads current spending?

Computed tomography accounts for 45.46% of 2024 revenue.

Which region shows the strongest growth outlook?

Asia-Pacific is projected to expand 11.14% per year to 2030.

What is the main barrier to adoption in emerging markets?

High capital costs and a shortage of trained imaging specialists hinder uptake.

Why are independent forensic practitioners gaining share?

Courts demand specialized, impartial testimony, and privatized services meet that need while public labs face backlogs.

Page last updated on: