Precision Genomic Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

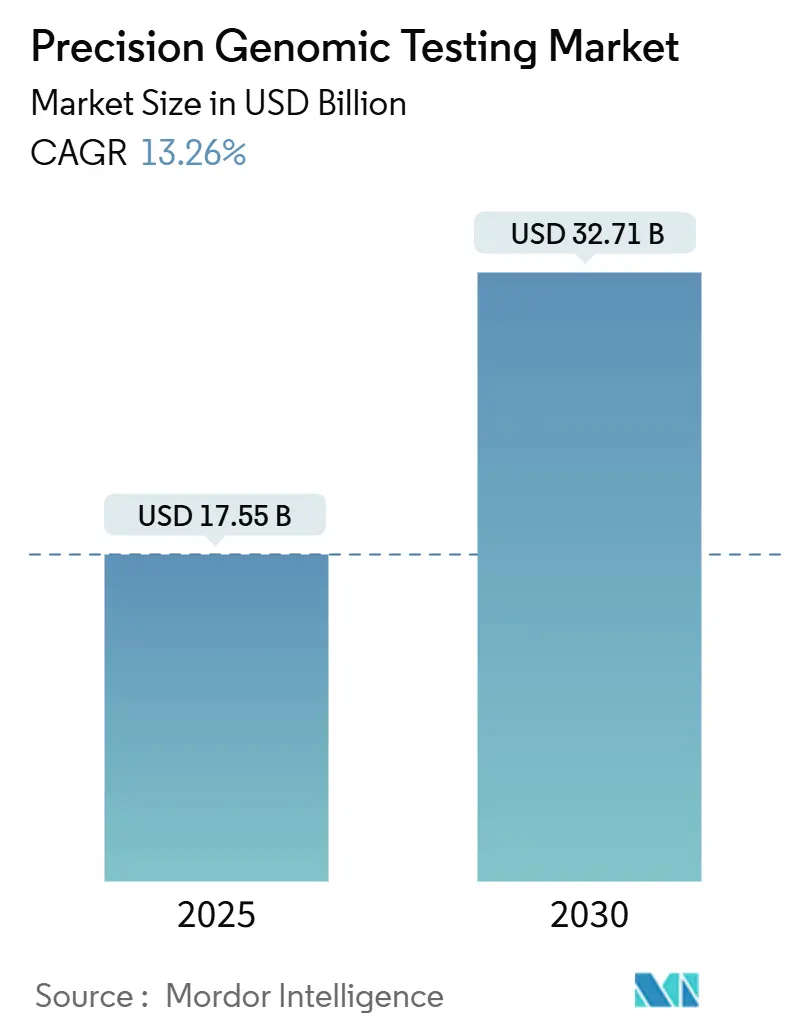

| Market Size (2025) | USD 17.55 Billion |

| Market Size (2030) | USD 32.71 Billion |

| Growth Rate (2025 - 2030) | 13.26% CAGR |

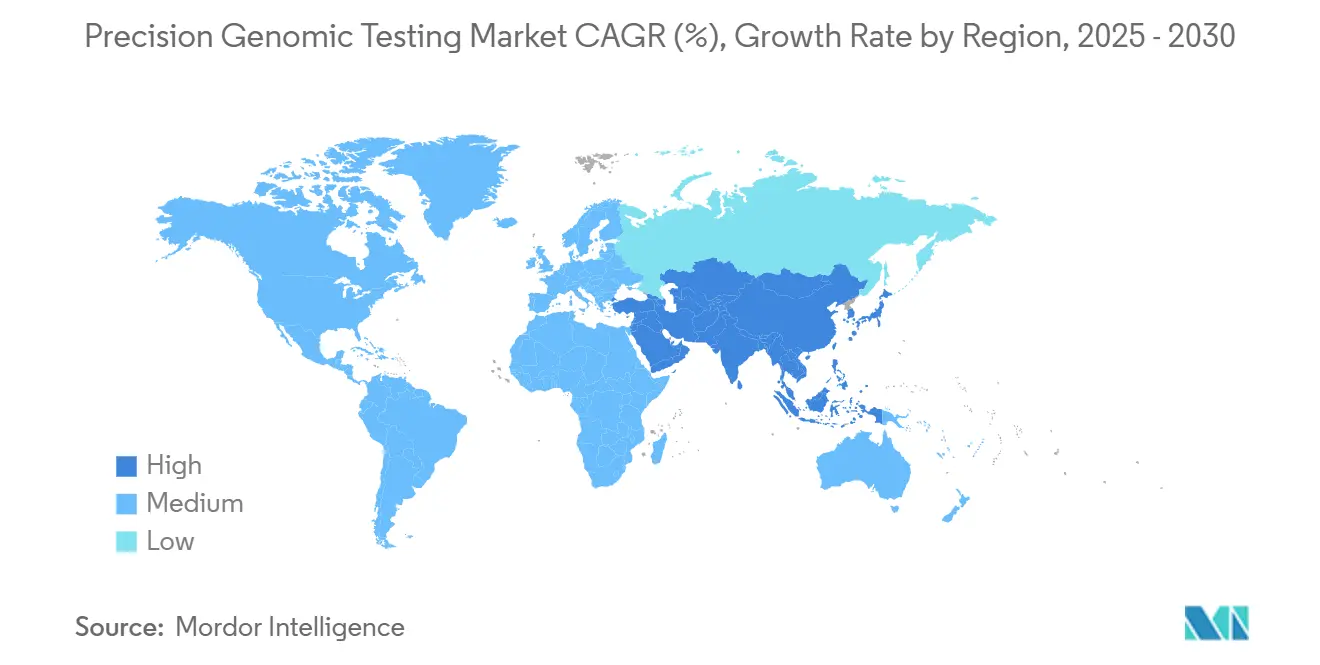

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Genomic Testing Market Analysis by Mordor Intelligence

The precision genomic testing market size stands at USD 17.55 billion in 2025 and is projected to reach USD 32.71 billion by 2030 at a 13.26% CAGR, underscoring how falling sequencing costs and pro-innovation regulation are reshaping clinical genomics.[1]World Intellectual Property Organization, “Measuring Genome Sequencing Costs and Its Health Impact,” WIPO.INT Technology advances, from roll-to-roll fluidics to ultra-long reads, are broadening test menus and lowering entry barriers, while companion-diagnostic approvals are aligning payers, regulators, and drug makers around disciplined evidence standards.[2]U.S. Food and Drug Administration, “FDA Takes Action Aimed at Helping to Ensure the Safety and Effectiveness of Laboratory Developed Tests,” FDA.GOV National population-genomics programs are fueling demand for large-scale sequencing, and AI-driven interpretation tools are shrinking result-delivery times for over-burdened clinical labs. Liquid biopsy adoption further accelerates volumes as blood-based assays gain parity with tissue testing for minimal residual disease monitoring and multi-cancer screening. Despite the optimistic outlook, reimbursement uncertainty, data-governance complexity, and workforce shortages temper near-term growth.

Key Report Takeaways

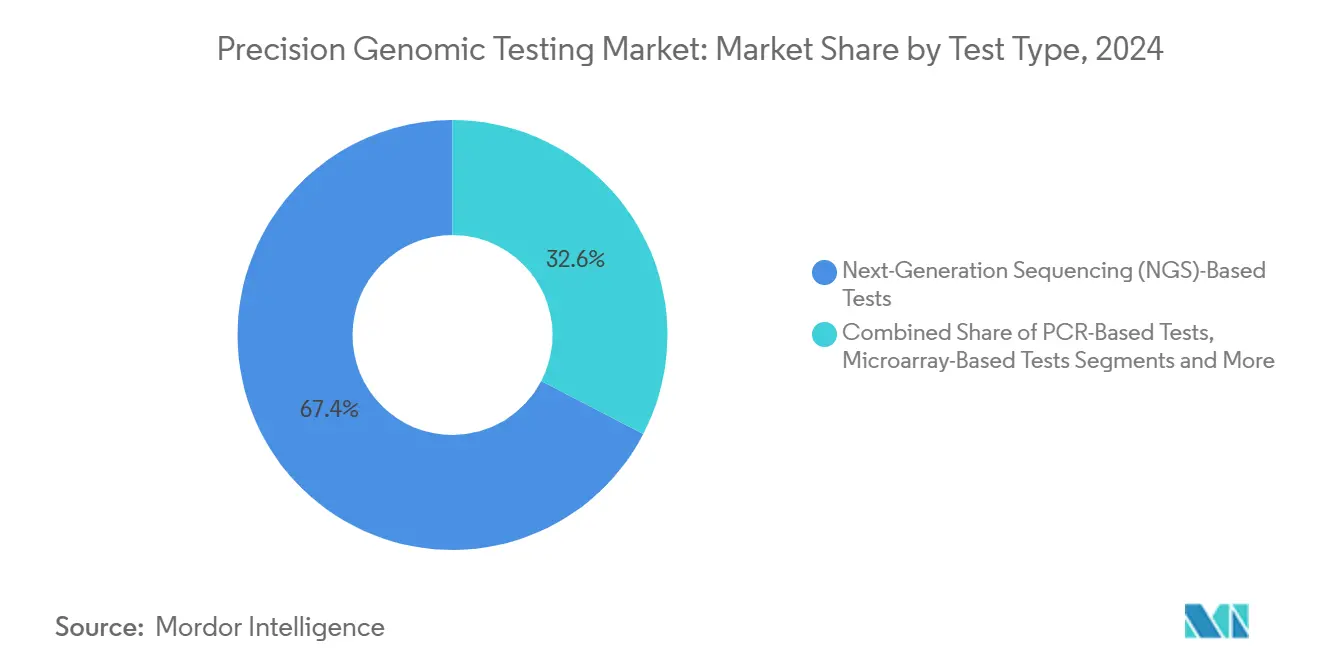

- By test type, next-generation sequencing captured 67.38% of precision genomic testing market share in 2024.

- By sample type, blood and plasma accounted for 57.58% share of the precision genomic testing market size in 2024 and are advancing at a 16.36% CAGR through 2030.

- By application, oncology led with 43.26% revenue share in 2024; rare and undiagnosed diseases are forecast to expand at a 16.48% CAGR to 2030.

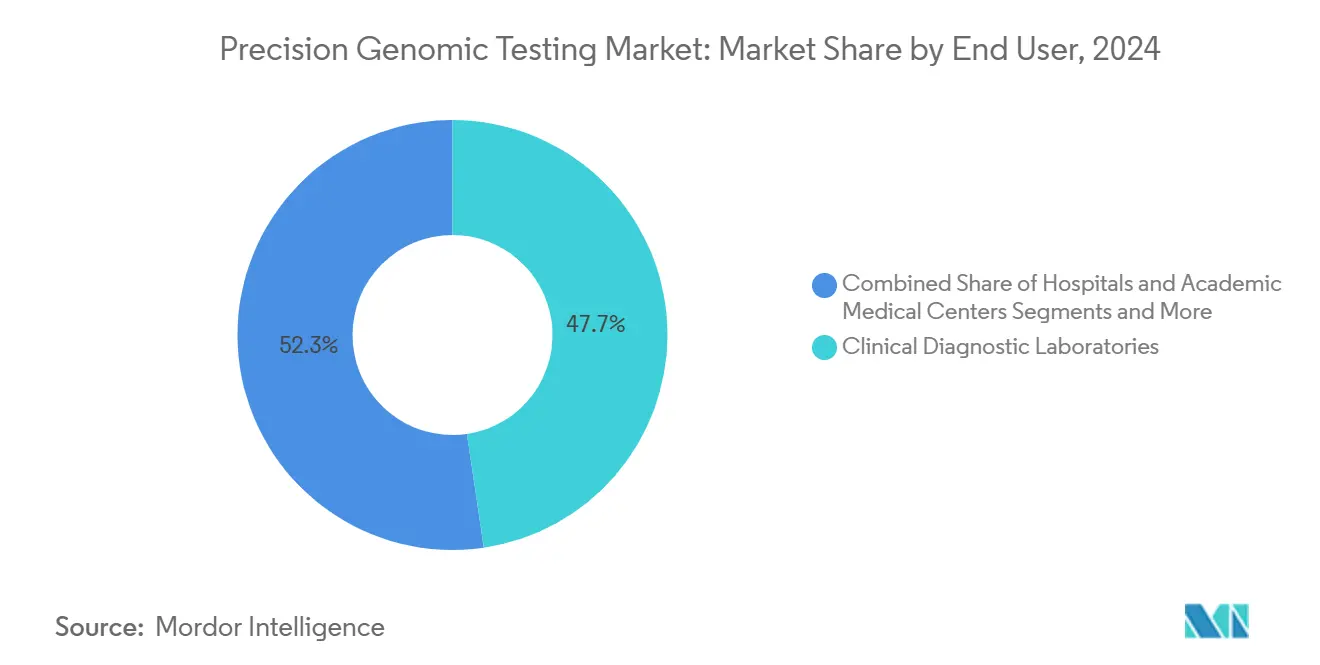

- By end-user, clinical diagnostic laboratories held 47.68% of the precision genomic testing market share in 2024, while biotechnology and pharmaceutical companies record the highest projected CAGR at 17.76% through 2030.

- North America commanded 36.88% of 2024 revenue, yet Asia-Pacific is projected to grow the fastest at 15.24% CAGR through 2030.

Global Precision Genomic Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in NGS costs | +2.8% | Global | Short term (≤ 2 years) |

| Regulatory backing for companion diagnostics | +2.1% | North America & EU | Medium term (2-4 years) |

| Expansion of national population-genomics initiatives | +1.9% | Global (early gains EU, APAC) | Long term (≥ 4 years) |

| Adoption of AI-driven variant interpretation | +1.7% | North America, EU, APAC | Medium term (2-4 years) |

| Emergence of liquid biopsy for early cancer detection | +2.3% | Global | Short term (≤ 2 years) |

| Precision-oncology clinical-trial enrollment growth | +1.4% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in NGS Costs

Sequencing costs plunged from USD 100 million in 2001 to little more than USD 500 per genome in 2023, paving the way for routine whole-genome sequencing in clinical settings. Innovations such as Oxford Nanopore’s ultra-long reads and roll-to-roll fluidics are pushing costs toward USD 10 per genome, accelerating market penetration in resource-constrained regions. Lower prices elevate test volumes in clinical labs and make genomic profiling a default component of drug-development pipelines. Emerging economies that once paid USD 4,500 per genome now treat population screening as financially viable. Strategic deals like Illumina-Tempus show how cheaper data generation married to analytics expands the precision genomic testing market.

Regulatory Backing for Companion Diagnostics

The FDA cleared multiple FoundationOne CDx liquid-biopsy extensions in 2024 and approved Guardant360 CDx for breast-cancer profiling, shifting liquid biopsy from experimental tool to care standard. Medicare’s transitional coverage pathway and the phased oversight of laboratory-developed tests give developers clearer commercialization roadmaps, while European IVDR alignment streamlines submissions for multinational launches. FDA guidance on AI-enabled devices allows continuous algorithm updates without resubmission, encouraging rapid product cycles. Together, these measures reduce compliance risk and build clinician confidence, expanding the precision genomic testing market.

Expansion of National Population-Genomics Initiatives

The Genome of Europe program allocated EUR 45 million to sequence 100,000 genomes across 27 nations by 2028. Australia’s Genomics Health Futures Mission invests USD 500.1 million over a decade to weave genomics into routine care for 200,000 citizens. Such efforts create reference datasets that improve diagnostic sensitivity for under-represented ethnicities and spur private-sector investment through predictable demand and harmonized data standards. NIH’s PRIMED consortium links 120 datasets from 45 countries, tackling polygenic-risk bias and accelerating algorithm-validation cycles.

Adoption of AI-Driven Variant Interpretation

GPT-4-style models now achieve 83% sensitivity in curating functional genetic evidence, reducing manual review backlogs.[3]Samuel J. Aronson, “GPT-4 Performance, Nondeterminism, and Drift in Genetic Literature Review,” NEJM.ORG AI enables non-geneticist clinicians to navigate complex reports, partially offsetting counselor shortages. Platforms overlaying pharmacogenomic guidance help optimize drug selection, while machine-learning pipelines refine CRISPR off-target predictions. The FDA’s predetermined change-control guidance assures vendors they can deploy continuous-learning models without serial filings, encouraging AI-centric product design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy & ethical concerns | -1.8% | EU (GDPR), Global | Medium term (2-4 years) |

| Reimbursement uncertainties | -2.1% | North America, EU | Short term (≤ 2 years) |

| Shortage of certified genomic counselors | -1.2% | Global (acute North America) | Long term (≥ 4 years) |

| Sample-quality variability in multi-omics testing | -1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy & Ethical Concerns

GDPR imposes strict consent and data-minimization rules, and upcoming European Health Data Space proposals may alter established safeguards, forcing labs to revamp governance frameworks. The United States lacks a unified genomic-privacy statute, creating patchwork obligations for commercial test providers. Cloud-based storage raises cross-border transfer issues, pushing adoption of federated-analysis models promoted by the Global Alliance for Genomics and Health. Compliance costs and legal uncertainty can delay launches, slowing the precision genomic testing market.

Reimbursement Uncertainties

Medicare’s local coverage determinations demand clear evidence of clinical utility, and pharmacogenomic panels still face narrow coverage windows. Private insurers layer prior-authorization requirements, burdening providers with complex paperwork and potentially deterring test ordering. Overseas, many health systems have not integrated precision tests into national benefit schemes, complicating multinational rollouts. While the FDA’s breakthrough-device pathway offers temporary relief, its sunset provisions re-introduce uncertainty, moderating precision genomic testing market uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: NGS Platforms Drive Market Evolution

NGS assays accounted for 67.38% of 2024 revenue, illustrating their role as the backbone of the precision genomic testing market. Liquid-biopsy NGS panels grow at 17.35% CAGR through 2030, helped by expanding multi-cancer screening indications and minimal residual disease surveillance. PCR retains value for rapid, targeted assays, while microarrays decline under the weight of broader NGS capabilities. Third-generation technologies from Pacific Biosciences and Oxford Nanopore add long-read accuracy, revealing complex structural variants missed by short-read systems. In niche areas like single-gene disorders, Sanger sequencing still validates critical variants when absolute accuracy trumps breadth. The precision genomic testing market size benefits as AI-powered callers such as DeepVariant raise diagnostic yield with fewer confirmatory tests.

The competitive field is also widening as startups offer benchtop sequencers with lower capital costs, democratizing access for regional hospitals. Cloud-native pipelines reduce on-premises IT burdens, and open-architecture systems enable plug-and-play reagent sourcing. Together, these evolutions ensure that sequencing remains the dominant engine in the precision genomic testing market.

By Application: Oncology Leadership Faces Rare-Disease Acceleration

Oncology held 43.26% of 2024 revenue, reflecting entrenched payer support for tumor sequencing and the steady supply of companion-diagnostic approvals. Yet rare-disease testing grows faster at 16.48% CAGR, spurred by the economic toll of diagnostic odysseys and emerging ultrarare gene-therapy trials. Pharmacogenomics is gaining momentum as AI stratification cuts adverse-drug events and streamlines formulary decisions, although reimbursement lags wider adoption. Reproductive applications continue to expand through preconception carrier screening and non-invasive prenatal testing, while neurological and cardiovascular genetics remain under-penetrated due to uncertain payer coverage. The precision genomic testing market size is expected to swell as pipelines broaden beyond oncology into multisystem disease management.

Clinical-workflow integration is key: automated decision-support dashboards are embedding genomic findings into electronic health records, enabling front-line physicians to act on complex variant data. Real-world evidence from large registries is building the case for broader payer approval, ensuring sustained precision genomic testing market expansion across indications.

By End-User: Clinical Labs Lead While Biotech Accelerates

Clinical diagnostic laboratories generated 47.68% of 2024 sales as hospitals outsourced high-complexity sequencing to accredited reference centers. Consolidation continues, with Labcorp acquiring select Invitae assets to deepen oncology and rare-disease portfolios. Biotech and pharma companies post a 17.76% CAGR by embedding population-scale datasets into discovery pipelines, exemplified by Regeneron’s USD 256 million purchase of 23andMe assets housing 15 million genomes. Academic medical centers serve as translational hubs, while research institutes advance multi-omics methodology despite episodic funding. Partnerships between diagnostics and pharma companies, such as Illumina-Tempus, align assay deployment with drug-trial needs, reinforcing the precision genomic testing market.

A shortage of in-house bioinformaticians pushes smaller labs toward managed-service models, while cloud-based LIMS platforms enable remote analysis. As payers link reimbursement to demonstrated clinical utility, labs with integrated interpretation services gain competitive edge, sustaining leadership in the precision genomic testing market.

By Sample Type: Blood Dominance Reflects Liquid-Biopsy Revolution

Blood and plasma represented 57.58% of 2024 revenue and grow fastest at 16.36% CAGR, signifying liquid biopsy’s shift from concept to widespread clinical tool. Sensitivity gains in cell-free DNA testing allow earlier cancer detection and longitudinal monitoring without invasive tissue collection. Saliva remains popular for direct-to-consumer germline tests and mass-screening drives; buccal swabs offer easy logistics for carrier screening and newborn programs. While tissue samples still underpin comprehensive somatic profiling, their growth stabilizes as blood-based assays close the performance gap. Cerebrospinal and urine testing unlock new neurologic and urologic applications, diversifying sample portfolios in the precision genomic testing market.

Efforts to standardize pre-analytic handling—temperature control, anticoagulant choice, shipping time—are critical to maintain consistency. AI models trained on high-quality blood-derived datasets further reinforce the centrality of liquid biopsy to the precision genomic testing market.

Geography Analysis

North America generated 36.88% of 2024 revenue, leveraging robust payer networks and FDA clarity. Market-access speed benefits from Medicare pathways, yet the region grapples with data-privacy debates and counselor shortages. U.S. labs are early adopters of AI assistants for result interpretation, and venture-backed startups fuel competitive churn. Canada’s national pharmacogenomic strategy supports reimbursed drug-gene testing, boosting regional volumes in the precision genomic testing market.

Europe trails slightly in revenue but commands strong policy momentum. The EUR 45 million Genome of Europe project and IVDR enforcement standardize workflows, improving cross-border data comparability. GDPR compliance, though stringent, builds public trust. Germany’s GenomDE program and the U.K.’s 100,000 Genomes Project set precedents for integrating sequencing into routine care, reinforcing regional growth.

Asia-Pacific records the fastest growth at 15.24% CAGR. China’s tiered hospital system embeds whole-genome sequencing in oncology pathways, and Japan subsidizes pharmacogenomic testing for select drugs. Australia’s national mission funds clinical pilots, while Singapore’s precision-medicine initiative uses AI models for disease-risk stratification. Infrastructure investment, supportive governments, and large gene pools position APAC as a future revenue leader in the precision genomic testing market.

Middle East and Africa and South America remain nascent but exhibit upticks in national-genome projects and private-lab construction. Saudi Arabia’s national biobank and Brazil’s SUS digital-health plan lay groundwork, though reimbursement gaps and IT shortages temper near-term scale. Over the forecast horizon, rising chronic-disease burden and lowered sequencing costs will unlock incremental demand for precision genomic testing market players.

Competitive Landscape

The precision genomic testing market shows moderate consolidation: top sequencing vendors, clinical-service labs, and AI-analytics platforms collectively command an estimated good revenue share. Illumina, Thermo Fisher, Guardant Health, and Foundation Medicine lead device and assay segments. Laboratory majors like Labcorp and Quest expand test menus via acquisitions, while tech-biotech hybrids (Tempus, Deep Genomics) introduce AI-first offerings.

Strategic moves intensify. Illumina added single-cell tech via Fluent Biosciences, strengthening multi-omics depth. Hitachi High-Tech bought Nabsys to secure electronic genome-mapping capability. Labcorp expanded its whole-genome partnership with Ultima Genomics, signaling a race for low-cost, high-throughput pipelines. Pharma-diagnostic collaborations co-develop assays bundled with targeted drugs, defending market share against commoditization.

Disruptors leverage cloud-native pipelines, federated-analysis models, and direct-to-consumer channels. AI-enabled variant calling and report automation compress turnaround time and reduce labor costs, challenging traditional lab advantage. Vendors providing end-to-end solutions—from sample logistics through clinical decision support—are best positioned as healthcare systems favor streamlined contracting. Cybersecurity credentials and compliance automation increasingly influence tender awards, shaping competitive dynamics in the precision genomic testing market.

Precision Genomic Testing Industry Leaders

Illumina Inc.

Thermo Fisher Scientific Inc

F. Hoffmann-La Roche Ltd

BGI Genomics

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Guardant Health introduced a hereditary-cancer blood test covering 82 genes, delivering results in 2-3 weeks and broadening its liquid-biopsy franchise.

- April 2025: Illumina and Tempus announced a partnership to speed AI-enabled evidence generation for NGS tests beyond oncology.

- January 2025: MaxCyte acquired SeQure Dx to integrate on-target/off-target editing assessments, enhancing cell-therapy regulatory packages.

Global Precision Genomic Testing Market Report Scope

| Next-Generation Sequencing (NGS)-Based Tests |

| PCR-Based Tests |

| Microarray-Based Tests |

| Sanger Sequencing Tests |

| Other Technologies |

| Oncology |

| Reproductive Health & Carrier Screening |

| Rare & Undiagnosed Diseases |

| Pharmacogenomics |

| Other Applications |

| Hospitals & Academic Medical Centers |

| Clinical Diagnostic Laboratories |

| Biotechnology & Pharmaceutical Companies |

| Research Institutes |

| Blood & Plasma |

| Saliva & Buccal Swab |

| Tumor Tissue |

| Other Sample Types |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Next-Generation Sequencing (NGS)-Based Tests | |

| PCR-Based Tests | ||

| Microarray-Based Tests | ||

| Sanger Sequencing Tests | ||

| Other Technologies | ||

| By Application | Oncology | |

| Reproductive Health & Carrier Screening | ||

| Rare & Undiagnosed Diseases | ||

| Pharmacogenomics | ||

| Other Applications | ||

| By End-User | Hospitals & Academic Medical Centers | |

| Clinical Diagnostic Laboratories | ||

| Biotechnology & Pharmaceutical Companies | ||

| Research Institutes | ||

| By Sample Type | Blood & Plasma | |

| Saliva & Buccal Swab | ||

| Tumor Tissue | ||

| Other Sample Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the precision genomic testing market expected to grow through 2030?

The precision genomic testing market is forecast to expand at a 13.26% CAGR from USD 17.55 billion in 2025 to USD 32.71 billion by 2030.

Why are liquid-biopsy NGS panels gaining traction?

Liquid biopsies combine non-invasive sampling with high sensitivity, leading blood and plasma to post a 16.36% CAGR and capture 57.58% of 2024 revenue.

What region is projected to record the highest growth?

Asia-Pacific is set to grow fastest at a 15.24% CAGR, supported by government-funded precision-health programs and AI-enabled diagnostic models.

Which end-user group is expanding most rapidly?

Biotechnology and pharmaceutical companies are growing at 17.76% CAGR as they integrate large genomic datasets into drug-development pipelines.

What remains the biggest obstacle to wider adoption?

Fragmented reimbursement policies create financial uncertainty, subtracting an estimated 2.1 percentage points from forecast CAGR.

How do AI tools influence variant interpretation?

AI models like GPT-4 boost literature-review sensitivity to 83%, cutting manual curation time and mitigating counselor shortages.

Page last updated on: