Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

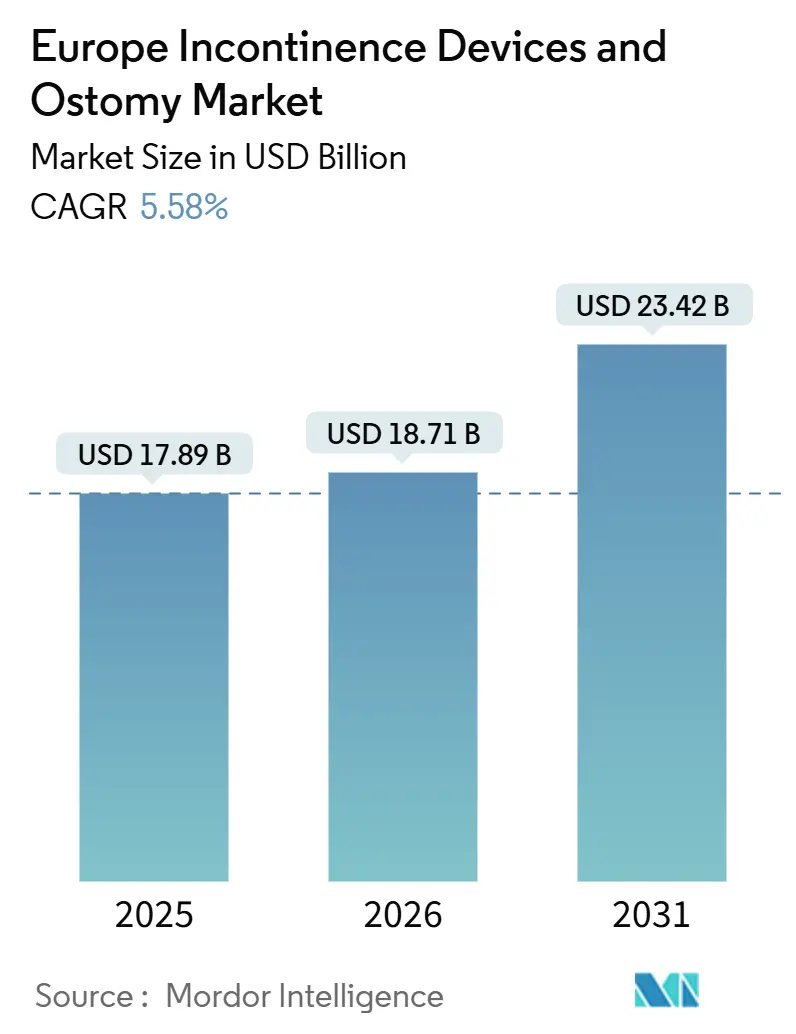

| Base Year Market Size (2025) | USD 17.89 Billion |

| Market Size (2026) | USD 18.71 Billion |

| Market Size (2031) | USD 23.42 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Incontinence Devices And Ostomy Market Analysis by Mordor Intelligence

The Europe Incontinence Devices And Ostomy Market size was valued at USD 17.89 billion in 2025 and is estimated to grow from USD 18.71 billion in 2026 to reach USD 23.42 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

Adoption accelerates as Western Europe’s public insurers reimburse most long-term continence supplies, prompting hospitals and home-care providers to standardize procurement through multi-year tenders. Vendors intensify focus on disposable pads, intermittent catheters, and ostomy bags that shorten inpatient stays and prevent pressure injuries, helping health systems curb nursing hours and readmissions. Meanwhile, digital pelvic-floor stimulators and connected ostomy pouches feed real-time data into tele-urology platforms, giving clinicians remote visibility of stoma output, leakage events, and catheter dwell times. Sustainability mandates under the EU circular-economy plan push manufacturers to integrate biodegradable non-wovens, mono-material film barriers, and post-consumer recycled plastics across their product lines.

Key Report Takeaways

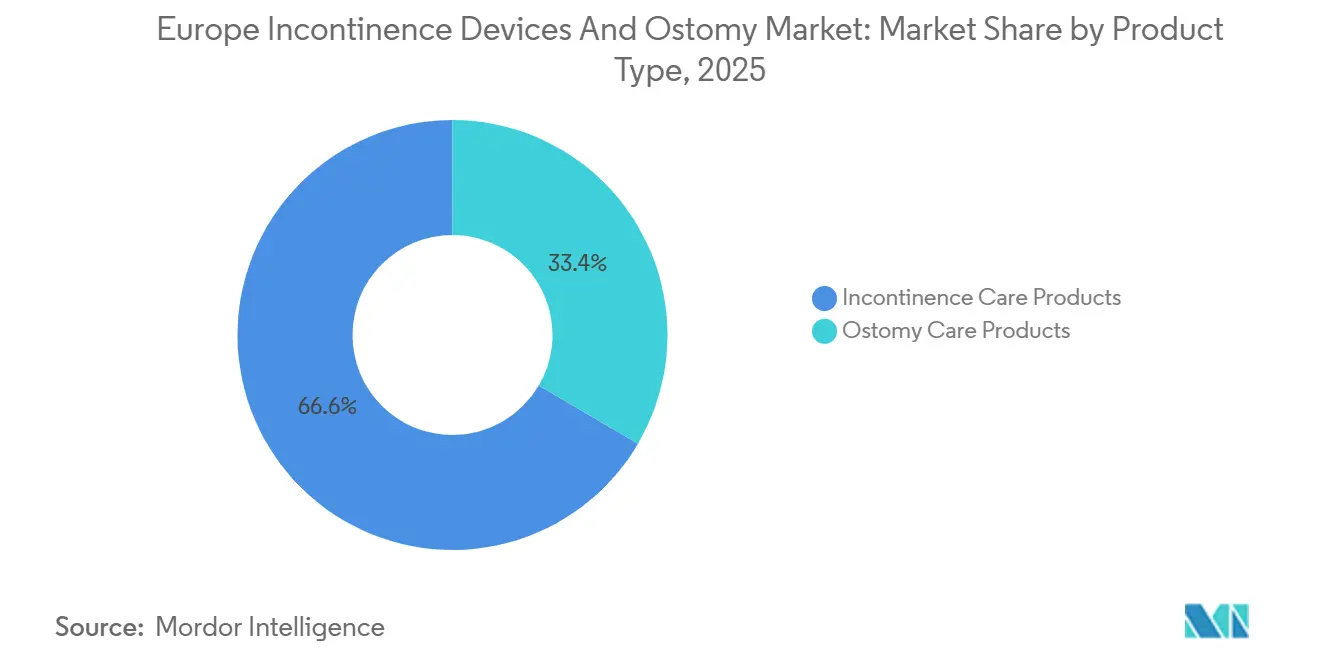

- By product type, incontinence care products led the Europe incontinence devices and ostomy market with 66.56% market share in 2025, while disposable pads and catheters are forecast to expand at an 8.80% CAGR through 2031.

- By application, colorectal cancer accounted for a 34.55% share of the Europe incontinence devices and ostomy market size in 2025 and is advancing at a 7.20% CAGR through 2031.

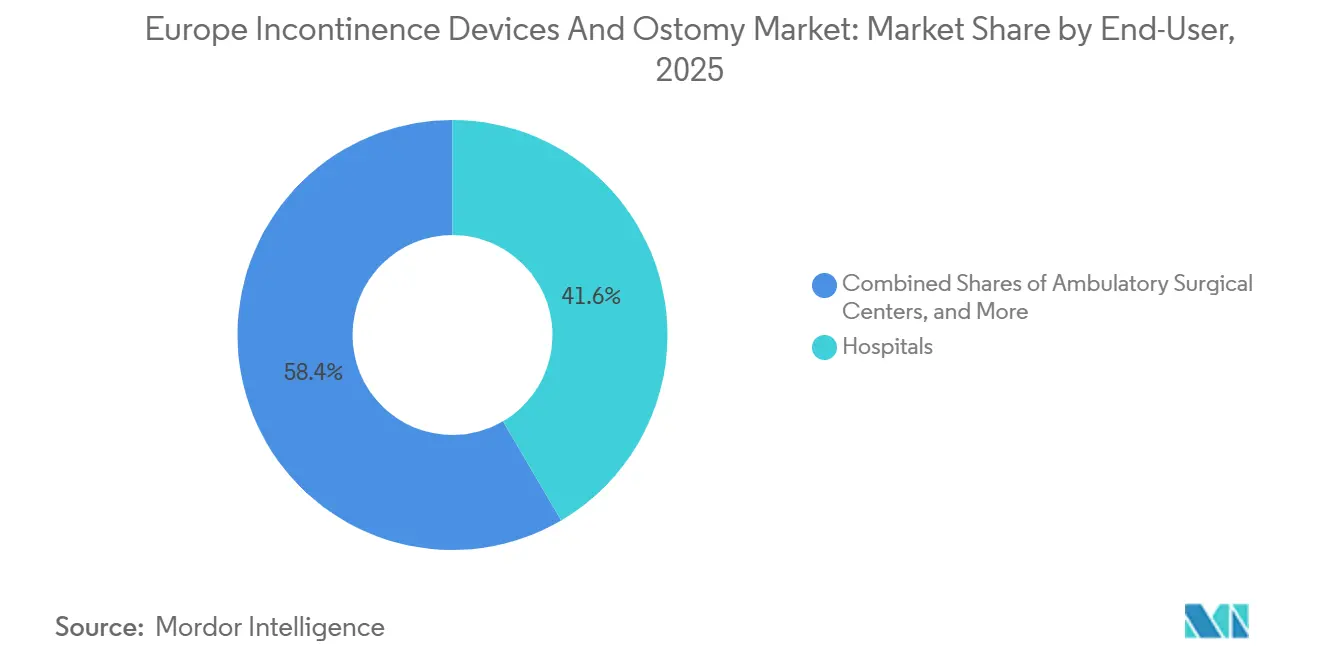

- By end-user, hospitals accounted for 41.56% in 2025; home care settings are poised for a 5.84% CAGR from 2026 to 2031.

- By distribution channel, institutional tender procurement dominated with 45.45% in 2025, while online pharmacies and subscription services are projected to grow at an 8.03% CAGR through 2031.

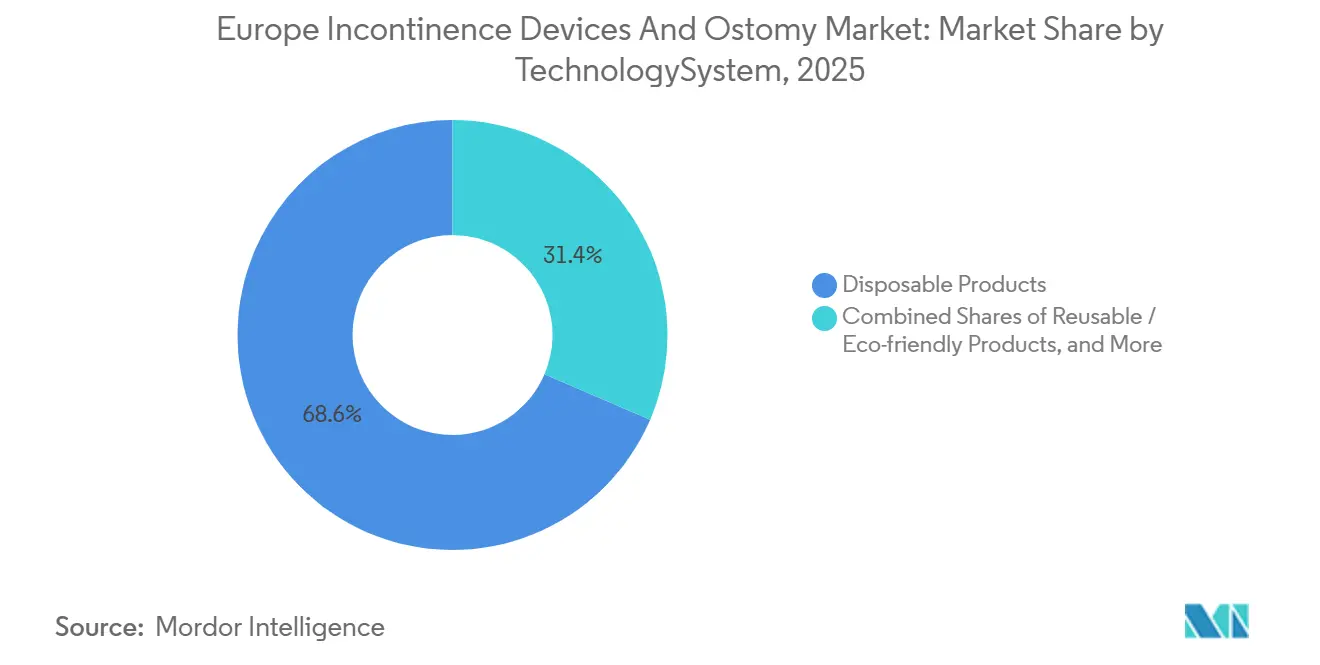

- By technology, disposable products commanded 68.56% in 2025; smart or connected continence and ostomy devices are set to post a 9.11% CAGR during 2026-2031.

- By region, Germany held 22.33% in 2025, whereas the United Kingdom is on track for the fastest 5.69% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Incontinence Devices And Ostomy Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging & obese demographic shift | +0.8% | Western & Northern Europe | Long term (≥ 4 years) |

| Rising renal and urological disorders | +0.6% | Germany, Benelux, Nordics | Medium term (2-4 years) |

| Growing colorectal & bladder cancer burden | +0.7% | United Kingdom, France, Italy | Long term (≥ 4 years) |

| Robust Western European reimbursement | +0.5% | Germany, France, Netherlands | Medium term (2-4 years) |

| Uptake of tele-urology & remote monitoring | +0.4% | United Kingdom, Scandinavia | Short term (≤ 2 years) |

| EU circular-economy pressure on disposables | +0.3% | EU-27 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric and Obese Population

Europe has the world’s oldest regional median age, and 34% of citizens aged 65+ report urge or stress incontinence episodes every week.[1]Eurostat, “Population Structure and Ageing,” ec.europa.eu Obesity prevalence passes 22% in Germany and the United Kingdom, and excess abdominal pressure accelerates pelvic-floor weakening that triggers leakage. Urologists prescribe single-use catheters and pads to prevent recurrent urinary tract infections, driving bulk demand in outpatient clinics. Parallel gerontology guidelines recommend early adoption of bowel management pouches for seniors recovering from colorectal surgery, as they can increase ostomy bag volume. As life expectancy stretches to 83 years in Spain, years lived with chronic conditions and disability continue to rise, strengthening the customer base for the European incontinence devices and ostomy market.

Increasing Prevalence of Renal & Urological Disorders

Type 2 diabetes and hypertension increase chronic kidney disease incidence, which now affects 10% of adults in northern Europe. Hemodialysis patients often require intermittent catheterization and high-output urostomy pouches to manage fluid balance between sessions. National health funds reimburse closed-end drainage bags that allow secure night-time urine collection, expanding recurring unit sales. Awareness programs by urological associations encourage primary-care physicians to screen for neurogenic bladder after stroke and channel referrals to specialized continence centers. Device makers partner with dialysis clinics to bundle ostomy accessories with weekly treatment packs, thereby increasing product penetration among end-stage renal disease patients.

Higher Incidence of Colorectal & Bladder Cancer

EUROCARE-6 data show colorectal cancer incidence reaching 67 per 100,000 in 2025, with over 45% of resections resulting in temporary or permanent stomas.[2]European Renal Association, “Chronic Kidney Disease in Europe,” era-edta.org Bladder cancer five-year prevalence exceeds 200,000 across Germany, France, and Italy. Surgical oncology units prioritize pouching systems with convex barriers and odor-neutralizing filters to reduce post-operative complications. Vendors increasingly supply pre-cut wafers and moldable seals to address irregular peristomal contours seen after radical cystectomy. Growth in minimally invasive colorectal procedures increases the use of one-piece drainable bags in enhanced recovery protocols aimed at 48-hour discharge benchmarks. These oncologic trends sustain volume growth for the European incontinence devices and ostomy market.

Strong Reimbursement for Chronic Care in Western Europe

Statutory health insurance in Germany and France fully covers up to 120 urine collection bags or 90 absorbent adult diapers per month, removing economic friction for patients. National procurement agencies award multi-year framework contracts that lock in volume commitments for preferred suppliers, stabilizing revenue visibility. Reimbursement parity for eco-friendly reusable diaper lines enables manufacturers to recoup R&D costs for compostable fibers. In parallel, the French Social Security finance law of 2026 extended coverage to sensor-based catheter alarms that alert caregivers to blockage risks, an early commercial win for connected continence devices.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Peristomal Skin Complications | -0.4% | Pan-Europe | Medium term (2-4 years) |

| Eastern & Southern Europe Reimbursement Gaps | -0.5% | Poland, Romania, Greece | Long term (≥ 4 years) |

| High Lifetime Cost Of Premium Supplies | -0.3% | Spain, Portugal | Short term (≤ 2 years) |

| MDR Post-Market Compliance Cost | -0.4% | EU-27 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complications & Peristomal Skin Issues with Long-Term Use

Nearly 35% of ostomates experience dermatitis or mucocutaneous separation in the first year post-surgery, raising readmission risk. Chronic leakage corrodes confidence in one-piece bags, fostering hesitation among new patients. Negative experiences circulate on patient forums, lengthening adoption curves in direct-to-consumer channels. Providers must invest in extra nursing hours and hydrocolloid dressing kits, inflating episode-of-care costs for insurers, such as quality-of-life concerns, tempering the rapid expansion of the European incontinence devices and ostomy market.

Reimbursement Gaps in Eastern & Southern Europe

Public coverage in Poland caps reimbursable adult diapers to 3 units per day, forcing families to pay out of pocket. Greek Social Insurance only refunds 75% of the ostomy wafer cost, weakening affordability. Lower household incomes lead to longer wait times and product rationing, thereby suppressing replacement frequency. Multinationals concentrate sales efforts in high-value Western economies, leaving peripheral markets underserved. Aggregate demand growth across Eastern and Southern Europe therefore trails the regional average, dampening total market acceleration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Incontinence Care Dominates Revenue Mix

In 2025, incontinence care products captured 66.56% of the Europe incontinence devices and ostomy market, supported by large-volume contracts for adult diapers, pads, and intermittent catheters in public hospitals. The prevalence of urge and overflow incontinence among seniors drives procurement toward absorbent underpads that meet EU tensile-strength and biodegradability criteria. Manufacturers leverage plant-based fluff pulp and SAP blends to meet eco-label thresholds without compromising absorbency. The Europe incontinence devices and ostomy market size for disposable pads is now forecast to grow at an 8.80% CAGR through 2031 as aging households and nursing homes prioritize leak-proof nightwear.

Ostomy care products, while smaller in share, exhibit premium ASPs thanks to convexity technology and charcoal-infused filters that curb odor. Two-piece drainable systems are gaining favor among high-output ileostomy patients because barrier rings can prolong wear time up to 7 days. Skin-friendly hydrocolloid wafers with ceramide additives reduce peristomal dermatitis incidence by 21%, boosting switching momentum away from legacy PVC pouches. Vendors invest in pediatric pouches with cartoon imagery, a fast-growing micro-segment as survivorship improves in childhood Hirschsprung disease.

By Application: Colorectal Cancer Drives Ostomy Demand

Colorectal cancer surgeries accounted for 34.55% of regional revenue in 2025, and the Europe incontinence devices and ostomy market size associated with these procedures is slated for a 7.20% CAGR during 2026-2031. Enhanced screening uptake via FIT tests boosts early detection, yet surgery rates remain high, sustaining stoma creation volumes. Fast-track recovery protocols mandate low-profile silicone baseplates, accelerating pull-through of one-piece bags.

Spinal cord injury and neurogenic bladder segments record steady growth as urban mobility accidents persist. Urostomy pouches with anti-reflux valves prevent ascending infections in paraplegic patients. Benign prostatic hyperplasia cases treated via trans-urethral resection continue to prescribe indwelling Foley catheters post-operatively, although intermittent self-catheterization programs lower infection risk and cut inpatient stay lengths.

By End-User: Hospitals Anchor Procurement but Home-Care Rises

Hospitals accounted for 41.56% of sales in 2025, as they remain the primary dispensing point for post-surgical stoma kits and high-value neuromodulation implants. Centralized purchasing grants them volume rebates of up to 18%. However, the home-care setting is forecast to grow at a 5.84% CAGR as community nurses train ostomates in self-care protocols and families subscribe to doorstep delivery plans to avoid pharmacy queues.

Long-term care and nursing homes are shifting toward high-capacity overnight diapers to reduce linen changes and staff workload. To improve dignity, facilities adopt odor-control polymers and breathable back-sheets that reduce pressure injuries. Smart sensor clips that notify caregivers via Wi-Fi when saturation exceeds 80% been successfully piloted in Dutch eldercare chains, signaling future up-scaling.

By Distribution Channel: Institutional Tenders Dominate, E-Commerce Surges

Institutional tender procurement represented 45.45% of sales in 2025, reflecting Europe’s publicly funded health systems. National tenders typically bundle pads, catheters, and auxiliary cleaning wipes under a three-year framework, locking in price ceilings. Local distributors team with global OEMs to satisfy language-specific labeling and overnight delivery terms.

Online pharmacies and subscription services are set to grow at an 8.03% CAGR through 2031. Chronic users value discrete monthly shipments and app-based reorder reminders. Vendors partner with payment platforms to offer pay-as-you-go plans, widening access for cash-strapped households. E-commerce also boosts the availability of stoma-friendly clothing and neoprene swim covers, cross-selling adjacent accessories that enrich basket size within the European incontinence devices and ostomy market.

By Technology/System: Disposable Lines Prevail, Smart Devices Accelerate

Disposable offerings accounted for 68.56% in 2025, driven by infection-control policies and caregiver convenience. Manufacturers redesign diaper cores to use 30% recycled fluff without compromising tensile strength, aligning with the EU plastic tax. However, smart and connected continence and ostomy devices are expected to post a 9.11% CAGR. Embedded pH sensors detect alkaline shifts that precede urinary tract infections, alerting users before symptom onset. Data-driven insights lower emergency visits, building a cost-saving case for payers to sponsor device upgrades.

Reusable garment shells with removable absorbent liners gain traction among eco-conscious millennials managing post-partum incontinence. RFID-tagged catheter packaging aids hospital stock tracking, minimizing expired inventory and easing EU MDR traceability requirements.

Geography Analysis

Germany, holding 22.33% of regional value in 2025, benefits from compulsory insurance that reimburses high-elasticity catheter sets and hydrocolloid wafers. Domestic players such as B. Braun leverage local manufacturing to avoid import duties, while university hospitals in Berlin trial next-generation sacral neuromodulation devices that deliver closed-loop nerve stimulation. Government funding for digital health apps allows prescription of continence management software, nurturing integrated care pathways.

The United Kingdom is poised for the fastest 5.69% CAGR, as NHS supply chain frameworks endorse eco-certified diapers with at least 50% renewable content. Post—Brexit regulatory alignment through the UKCA mark streamlines market entry for U.S. catheter brands, intensifying competition. Community pharmacies expand stoma care advisory desks, and Clinical Commissioning Groups reimburse tele-urology consultations, amplifying adoption of connected pouches.

Southern Europe lags the regional average because Spain and Italy face fragmented reimbursement systems. Nonetheless, an aging population and rising obesity are driving volume growth, especially in Catalonia’s public eldercare network. National Recovery and Resilience Plans unlock EU funds for nursing home modernization, including sensor-equipped pads that can integrate with central monitoring dashboards. The Rest of Europe bloc, covering Central and Eastern nations, is witnessing a gradual transition from gauze and cotton cloth to modern disposable briefs, with NGOs donating starter kits to improve dignity for low-income ostomates.

Competitive Landscape

Multinationals such as Coloplast, ConvaTec, and Hollister dominate ostomy bags and skin barriers, together controlling close to half of the segment revenue. Coloplast’s SenSura Mio portfolio integrates elastic adhesive technology that conforms to hernia bulges, tightening user loyalty. ConvaTec invests in moldable seals that can be reshaped multiple times without losing tack, enhancing first-time fit for irregular body profiles.

In incontinence care, Essity’s TENA and Kimberly-Clark’s Depend lines enjoy strong brand recognition and direct-to-consumer marketing budgets that outpace those of regional peers. Essity pilots carbon-negative diaper cores made with forest-residue-based SAP at its Swedish R&D hub, pledging a 2030 net-zero footprint that aligns with hospital sustainability targets. Axonics and Medtronic compete in sacral neuromodulation, with Axonics’ rechargeable stimulator promising 15-year battery life that lessens explant surgeries.

Local specialists such as Paul Hartmann and Salts Healthcare supply hospital-grade dressings, leveraging established procurement relationships to cross-sell ostomy accessories. Start-ups like Atlantic Therapeutics introduce wearable pelvic-floor stimulators that pair with smartphone coaching apps, broadening non-surgical management options. Supply-chain consolidation emerges as distributors Ontex and Abena form purchasing alliances to pool raw-material contracts and stabilize pricing amid volatility in fluff pulp prices.

Europe Incontinence Devices And Ostomy Industry Leaders

Kimberly-Clark Corporation

Unicharm Corporation

Hollister Inc.

Coloplast A/S

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Coloplast launched the digital Ostomy Follow-up Platform across Germany, enabling stoma nurses to schedule virtual skin checks and automatically reorder supplies.

- November 2025: Amara Therapeutics introduced Dry Days Health, an innovative virtual clinic designed to address the needs of women managing urinary incontinence. Despite its high prevalence globally, this condition remains significantly undertreated.

- June 2025: Medtronic received the CE mark under the EU MDR for the InterStim X rechargeable sacral neuromodulation system, which extends battery life to 15 years.

Europe Incontinence Devices And Ostomy Market Report Scope

As per the scope of the report, ostomy surgery is a procedure that allows bodily waste to pass through a surgically created stoma on the abdomen. Ostomy care products, such as skin barriers and ostomy bags, provide a means to collect waste from a surgically diverted biological system. In incontinence, there is a lack of voluntary release of urine from the urinary bladder, for which several disposable incontinence products (DIPs) are manufactured by leading medical device companies.

The Europe incontinence devices and ostomy market is segmented by product type, application, end-user, distribution channel, technology/system, and region. By product, the market is segmented into incontinence care products and ostomy care products. Incontinence care products are further segmented into absorbents, incontinence bags, and pelvic-floor stimulation & neuromodulation devices. By ostomy care products, the market is further segmented into ostomy bags, skin barriers, irrigation products, and other ostomy products. By application, the market is segmented into bladder cancer, colorectal cancer, Crohn's disease, kidney stone, chronic kidney failure, and other applications. By end user, the market is segmented into hospitals, ambulatory surgical centers, home care settings, long-term care & nursing homes, and others. By distribution channel, the market is segmented into institutional tender procurement, retail pharmacies, and online pharmacies & subscription services. By technology/system, the market is segmented into disposable products, reusable/eco-friendly products, and smart/connected continence & ostomy devices. By region, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. The report offers the value (in USD) for the above segments.

By Product Type

| Incontinence Care Products | Absorbent Pads & Underpads | |

| Intermittent Catheters | ||

| Incontince Bags | ||

| Pelvic-Floor Stimulation & Neuromodulation Devices | ||

| Ostomy Care Products | Ostomy Bags | One-piece Systems |

| Two-piece Systems | ||

| Drainable vs Closed-end | ||

| High-output & Pediatric Pouches | ||

| Skin Barriers & Seals | ||

| Irrigation & Accessories | ||

| Others | ||

By Application

| Bladder Cancer |

| Colorectal Cancer |

| Crohns & Ulcerative Colitis |

| Benign Prostatic Hyperplasia / Post-Prostatectomy |

| Spinal Cord Injury & Neurogenic Bladder |

| Kidney Stone & Chronic Kidney Failure |

| Others |

By End-User

| Hospitals |

| Ambulatory Surgical Centers |

| Home-Care Settings |

| Long-term Care & Nursing Homes |

| Others |

By Distribution Channel

| Institutional Tender Procurement |

| Retail Pharmacies |

| Online Pharmacies & Subscription Services |

By Technology / System

| Disposable Products |

| Reusable / Eco-friendly Products |

| Smart / Connected Continence & Ostomy Devices |

By Region

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product Type | Incontinence Care Products | Absorbent Pads & Underpads | |

| Intermittent Catheters | |||

| Incontince Bags | |||

| Pelvic-Floor Stimulation & Neuromodulation Devices | |||

| Ostomy Care Products | Ostomy Bags | One-piece Systems | |

| Two-piece Systems | |||

| Drainable vs Closed-end | |||

| High-output & Pediatric Pouches | |||

| Skin Barriers & Seals | |||

| Irrigation & Accessories | |||

| Others | |||

| By Application | Bladder Cancer | ||

| Colorectal Cancer | |||

| Crohns & Ulcerative Colitis | |||

| Benign Prostatic Hyperplasia / Post-Prostatectomy | |||

| Spinal Cord Injury & Neurogenic Bladder | |||

| Kidney Stone & Chronic Kidney Failure | |||

| Others | |||

| By End-User | Hospitals | ||

| Ambulatory Surgical Centers | |||

| Home-Care Settings | |||

| Long-term Care & Nursing Homes | |||

| Others | |||

| By Distribution Channel | Institutional Tender Procurement | ||

| Retail Pharmacies | |||

| Online Pharmacies & Subscription Services | |||

| By Technology / System | Disposable Products | ||

| Reusable / Eco-friendly Products | |||

| Smart / Connected Continence & Ostomy Devices | |||

| By Region | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How large will the Europe incontinence devices and ostomy market be by 2031?

It is projected to reach USD 23.42 billion by 2031, advancing at a 5.58% CAGR from 2026.

Which product category currently leads sales?

In 2025, incontinence care products, mainly pads and catheters, accounted for 66.56% of regional revenue.

What is the fastest-growing technology segment?

Smart or connected continence and ostomy devices are forecast to grow at a 9.11% CAGR between 2026 and 2031.

Why is the United Kingdom the fastest-expanding market?

NHS adoption of eco-certified disposables and tele-urology platforms lifts demand, delivering a projected 5.69% CAGR.

How do EU sustainability rules affect suppliers?

Circular-economy directives push manufacturers toward biodegradable materials and recycling programs, shaping product redesigns and procurement criteria.

Which companies dominate the competitive landscape?

Kimberly-Clark Corporation, Unicharm Corporation, Hollister Inc., Coloplast A/S, and B. Braun SE collectively control a little over 60% of regional sales.

Page last updated on: