Disposable Medical Devices Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.03 Billion |

| Market Size (2031) | USD 18.74 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

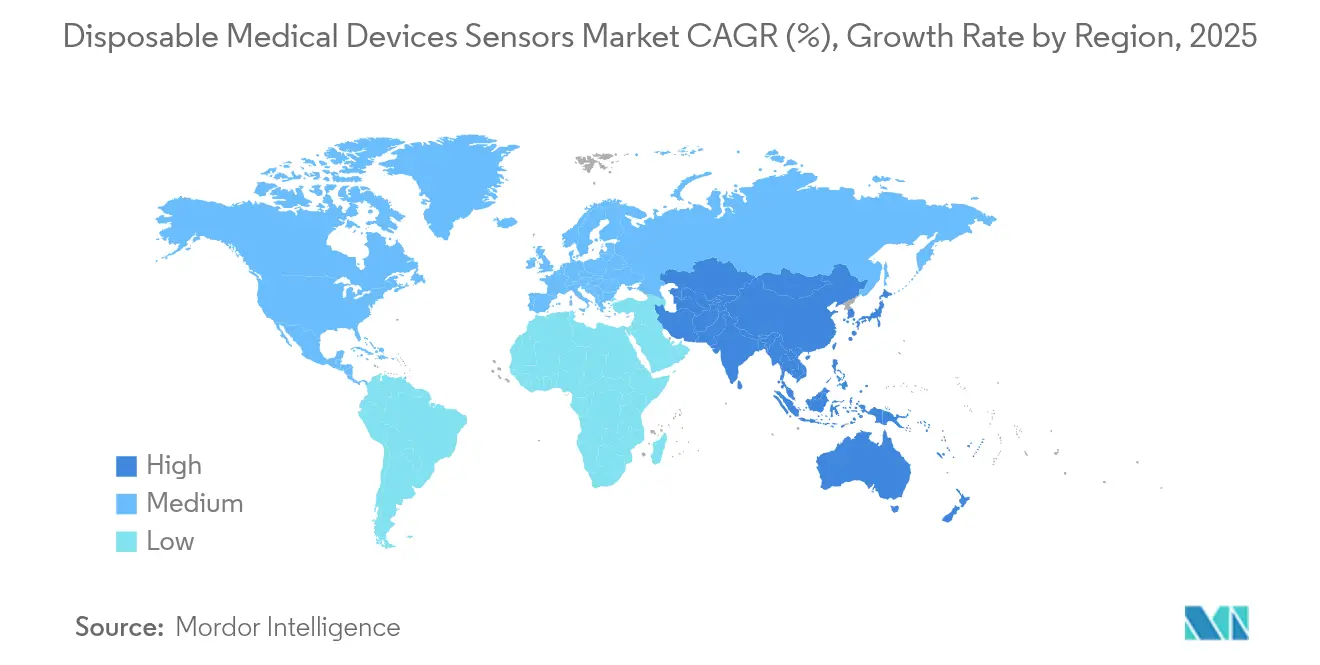

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

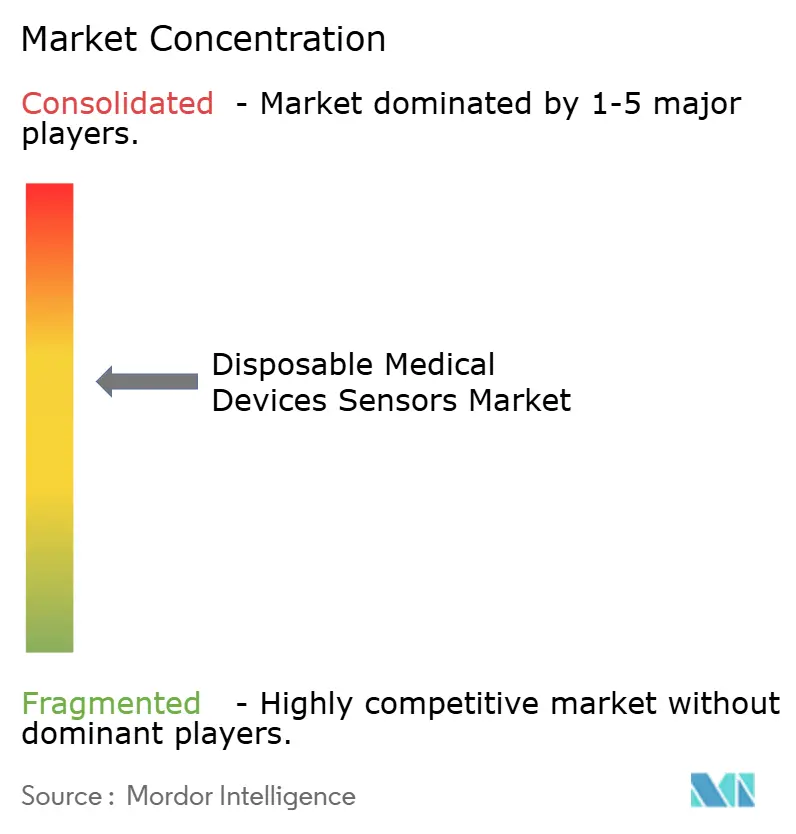

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Medical Devices Sensors Market Analysis by Mordor Intelligence

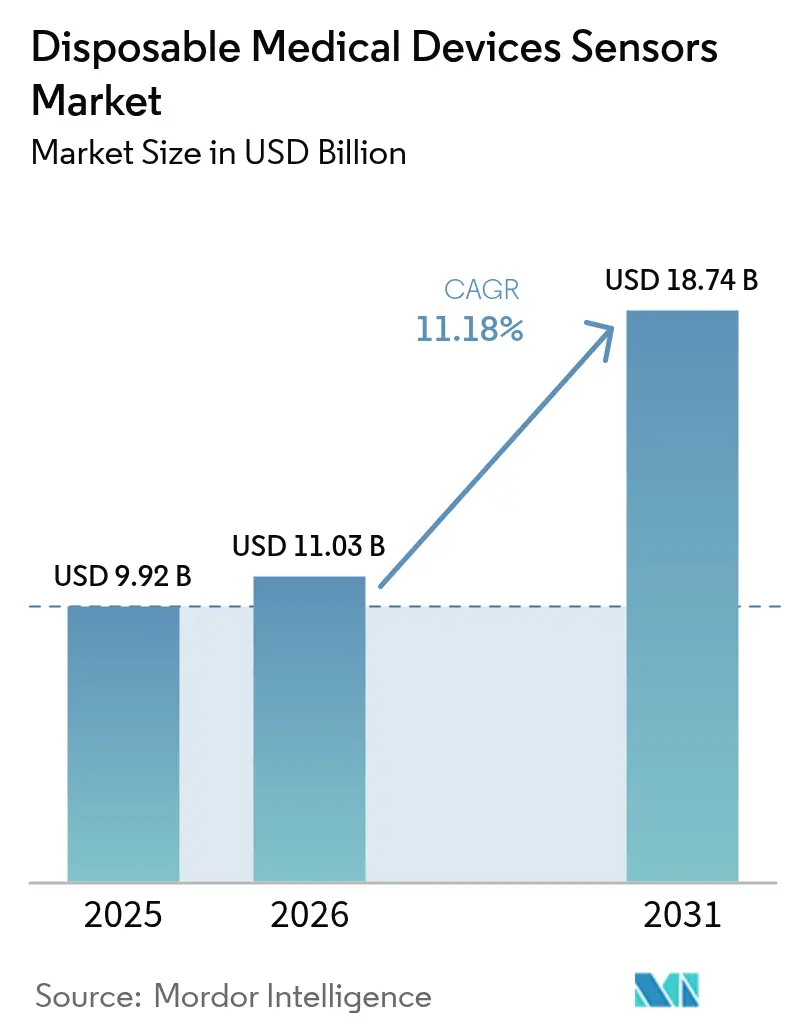

The disposable medical device sensors market size was valued at USD 9.92 billion in 2025 and estimated to grow from USD 11.03 billion in 2026 to reach USD 18.74 billion by 2031, at a CAGR of 11.18% during the forecast period (2026-2031). Continual emphasis on infection prevention, wider use of single-use devices during the COVID-19 pandemic, and accelerating demand for remote patient monitoring underpin this expansion[1]U.S. Food and Drug Administration, “Quality System Regulation Amendments,” fda.gov. Cost advantages over reusable devices, the shift toward home-based care, and rapid technology advances in miniaturization, connectivity, and biodegradability further stimulate growth. Competitive strategies center on partnerships that combine sensing hardware with data analytics, while providers amplify purchases to lower the risk of cross-contamination and avoid sterilization expenses. Finally, sustainability pressures are steering leading firms to explore eco-friendly materials and closed-loop recycling models, creating new innovation lanes for the disposable medical device sensors market.

Key Report Takeaways

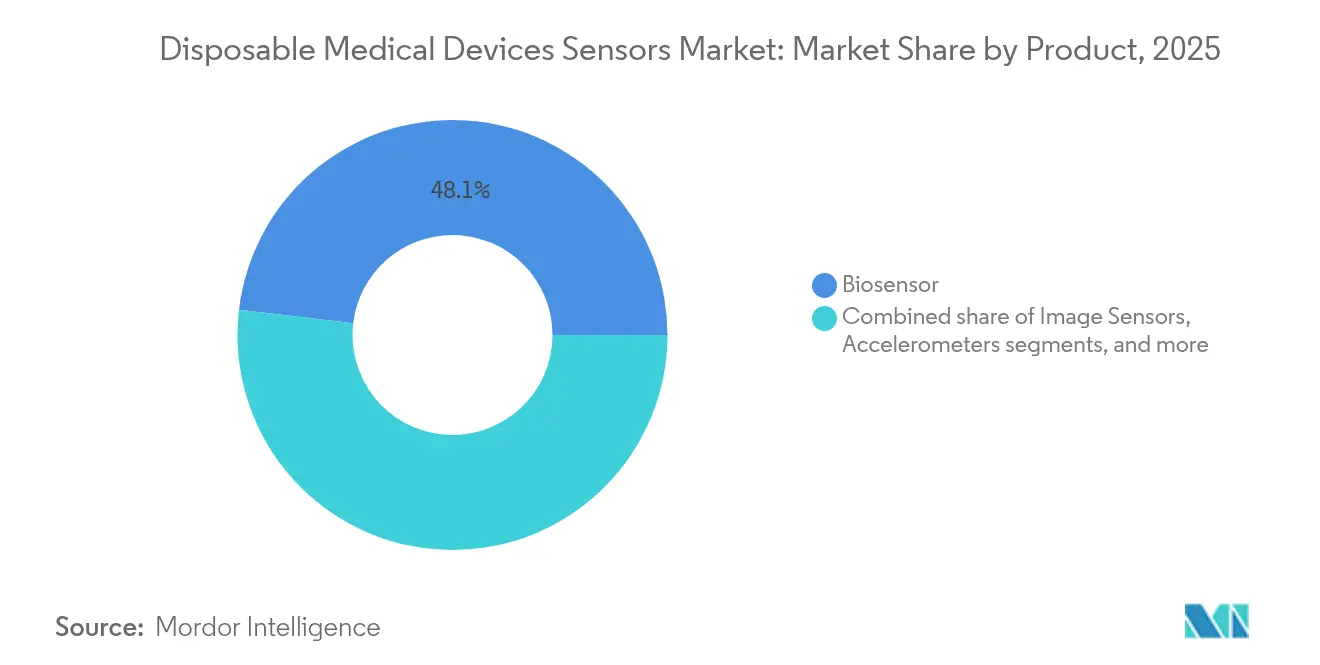

- By product category, biosensors led with 48.12% revenue share in 2025; image sensors are projected to expand at a 13.38% CAGR to 2031.

- By application, patient monitoring held 46.05% of the disposable medical device sensors market share in 2025, while diagnostics is expected to grow at 14.11% through 2031.

- By technology, MEMS accounted for a 42.25% share of the disposable medical device sensors marke size in 2025 and nanotechnology-enabled sensors are advancing at a 13.71% CAGR to 2031.

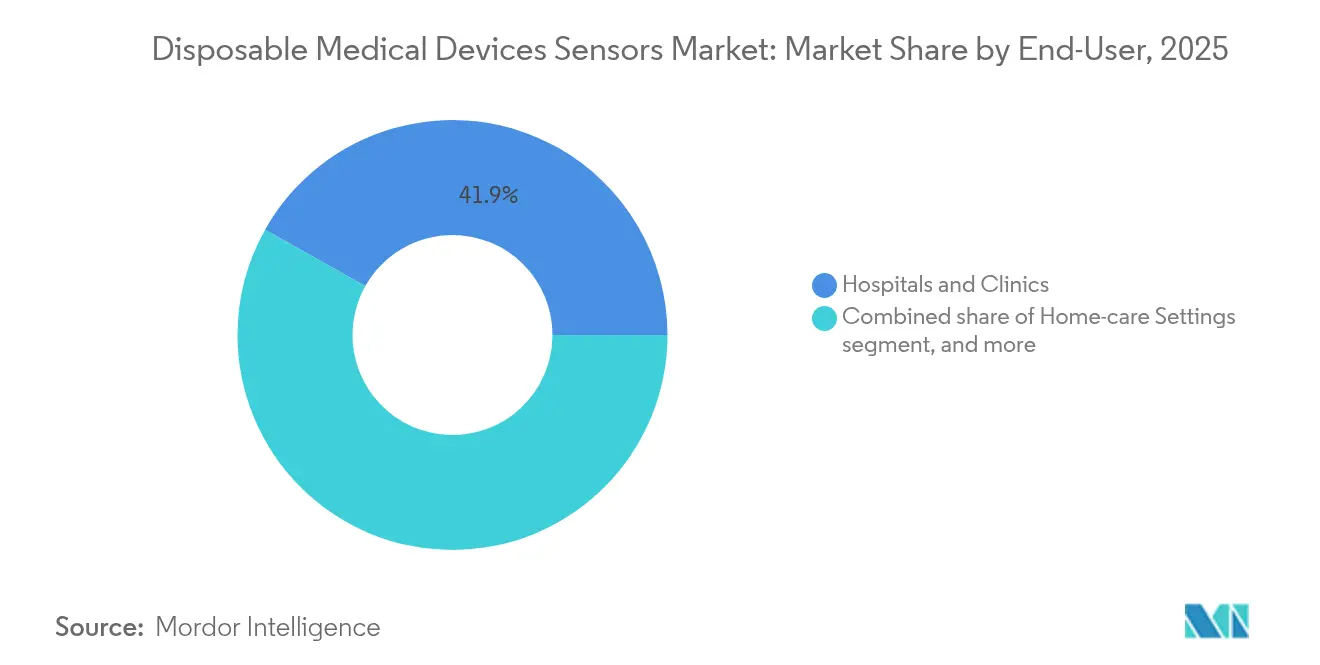

- By end-user, hospitals and clinics captured 41.85% of revenue in 2025; home-care settings are forecast to climb at a 14.33% CAGR to 2031.

- By geography, North America dominated with 38.21% share in 2025, whereas Asia-Pacific is anticipated to witness the fastest 12.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Medical Devices Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Chronic Diseases | +2.8% | Global, highest in North America & Asia-Pacific | Long term (≥ 4 years) |

| Rising Demand For Point-Of-Care Diagnostics | +2.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Expansion Of Wearable Health Monitoring Devices | +1.9% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Technological Advancements In Biosensor Miniaturization | +1.6% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing Adoption In Emerging Markets | +1.4% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Supportive Government And Reimbursement Policies | +1.2% | North America & European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Diseases

The number of adults living with diabetes exceeded 537 million in 2024, spurring unprecedented demand for disposable glucose-monitoring sensors such as Abbott’s FreeStyle Libre, which supports more than 6 million users across 60 countries. Providers increasingly favor single-use cardiac sensors for long-term rhythm assessment as cardiovascular disease remains the top global mortality cause. Continuous, disposable solutions remove sterilization tasks and maintain accuracy over extended use, supporting chronic-care protocols for aging populations. As health systems pivot from episodic to continuous care, the disposable medical device sensors market gains an enduring revenue stream from refill demand.

Rising Demand for Point-of-Care Diagnostics

The pandemic reinforced the clinical value of near-patient testing, and disposable biosensors proved essential for rapid antigen detection in emergency departments and rural clinics. U.S. regulators continue to ease market entry by granting expedited pathways for qualified point-of-care devices, enhancing speed to market. Smartphone-connected sensor sticks permit immediate readouts and cloud upload, reshaping diagnostic data flows. Faster diagnosis trims patient wait times, cuts downstream costs, and elevates clinical outcome expectations, ensuring a sustained lift for the disposable medical device sensors market.

Expansion of Wearable Health Monitoring Devices

Global shipments of consumer and medical wearables are on track to touch 2 billion units, with MEMS accelerometers and biosensors embedded for vitals tracking. Adhesive single-use patches improve skin comfort and reduce hygiene risks for multi-day wear. Advances from STMicroelectronics allow non-invasive, continuous cardiac and blood-pressure sensing in miniaturized form factors. Predictive analytics integrated into these wearables supports early intervention and chronic-disease adherence programs, further deepening disposable sensor penetration.

Technological Advancements in Biosensor Miniaturization

MEMS pressure sensors can now be manufactured for roughly USD 10 per unit while retaining clinical-grade accuracy, enabling cost-effective disposability[2]MEMS Exchange, “Cost Trends in Disposable Pressure Sensors,” mems-exchange.org. Nanostructured electrodes push detection limits to molecular levels, allowing earlier disease identification. Three-dimensional printing reduces development cycles, and biopolymers introduce compostable substrates that address disposal concerns. Coupled with low-power wireless chips, ultra-small sensors send data seamlessly to electronic health record systems, enhancing the appeal of the disposable medical device sensors market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Approval Process | −1.8% | Global, most pronounced in North America & Europe | Short term (≤ 2 years) |

| Concerns Over Data Privacy And Security | −1.2% | Global, highest in developed markets | Medium term (2-4 years) |

| Price Sensitivity In Cost-Constrained Settings | −0.9% | Emerging markets, rural healthcare facilities | Long term (≥ 4 years) |

| Limited Standardization And Interoperability | −0.7% | Global, affecting connected-device ecosystems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Process

New U.S. Quality System Regulation rules, effective February 2026, add clinical and documentation burdens that may lengthen time-to-market for smaller innovators. Interoperability guidelines now require compliance evidence during premarket submissions, driving extra verification costs[3]Regulatory Affairs Professionals Society, “FDA Interoperability Guidance for Devices,” raps.org. As harmonization across regions remains limited, firms must navigate multiple approval tracks, which can delay global releases and temporarily moderate growth for the disposable medical device sensors market.

Concerns Over Data Privacy and Security

Connected sensors enlarge attack surfaces for cyber threats, prompting hospitals to mandate rigorous encryption audits before purchase. HIPAA and GDPR frameworks require granular consent and robust data handling, complicating device design and adding cost. Lack of a unified cybersecurity benchmark leads manufacturers to adopt conservative architectures that may curtail feature sets and slow adoption, particularly in sensitive clinical workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Biosensors Lead Innovation Wave

Biosensors captured 48.12% of revenue in 2025, reinforcing their role as the principal growth engine of the disposable medical device sensors market. Electrochemical formats dominate glucose and cardiac-marker monitoring, while optical biosensors accelerate infectious-disease screening where rapid turnaround is critical. Image sensors hold the fastest 13.38% CAGR because advances in compact CMOS chips elevate capsule endoscopy and single-use scopes, broadening clinical reach. Pressure sensors remain staples in intensive-care units, replacing reusable transducers that require calibration. Accelerometers, temperature probes and hybrid devices complete an expanding toolkit for multi-parameter monitoring in hospital and home settings.

By Application: Diagnostics Drives Market Evolution

Patient monitoring held 46.05% of 2025 revenue as hospitals and payers endorsed continuous surveillance for chronic ailments and post-procedure recovery. Remote monitoring codes in the United States underpin large-scale rollouts, pushing disposable medical device sensors market share steadily higher in this category. Diagnostics, however, shows the sharpest 14.11% CAGR as point-of-care platforms shift testing from centralized labs to bedsides, retail clinics and even homes. Rapid antigen assays and lab-on-a-chip cartridges reduce diagnosis time from hours to minutes, improving triage and containment efforts.

By End-User: Home-Care Settings Transform Healthcare Delivery

Hospitals and clinics accounted for 41.85% of sales in 2025, driven by strict sterilization policies that favor single-use devices over reusable counterparts. Diagnostic labs depend on disposables to eliminate cross-sample contamination, preserving result integrity. Ambulatory surgical centers likewise deploy single-use sensors as outpatient procedures grow in complexity and monitoring requirements. These institutional customers anchor baseline demand, ensuring volume stability for producers.

By Technology: MEMS Dominance Faces Nanotechnology Challenge

MEMS platforms delivered 42.25% of 2025 revenue thanks to mature fabs that supply low-cost pressure, motion and flow sensors. CMOS imaging chips complement MEMS by powering high-resolution disposable scopes and retinal cameras. RFID and NFC tags provide instant connectivity, letting clinicians upload readings directly to electronic health records. Together, these technologies form the backbone of today’s disposable sensor ecosystem.

Geography Analysis

North America accounted for 38.21% of global revenue in 2025, sustained by sophisticated payer systems and rapid RPM reimbursement expansion. FDA exemptions for specific device classes shorten approval cycles and invite continued innovation. Leading providers integrate sensor data with electronic health records, demanding standardized communication protocols and boosting uptake across hospital networks.

Asia-Pacific is projected to register a 12.29% CAGR through 2031, the fastest worldwide. Government investment in public health infrastructure, a soaring chronic-disease burden, and rising consumer purchasing power fuel demand. China’s updated reimbursement policies and India’s cost-driven innovation culture provide fertile ground for local producers, challenging incumbent multinationals. Although venture financing cooled from prior peaks, strategic investors still back firms with differentiated, affordable solutions, enlarging total addressable volume for the disposable medical device sensors market.

Europe shows consistent growth supported by the EU Medical Device Regulation, which embeds environmental requirements that accelerate biodegradable sensor adoption. Sustainability mandates cause firms to redesign products and supply chains, spawning collaboration between materials scientists and device makers. The Middle East, Africa, and South America collectively offer untapped opportunities as hospital construction and universal health-coverage initiatives gather pace. Suppliers that tailor rugged, low-cost disposables to local conditions stand to capture early mover advantages and strengthen global diversity in the disposable medical device sensors market.

Competitive Landscape

Market structure remains moderately fragmented, though consolidation is anticipated as data analytics becomes integral to device value. Abbott and Medtronic forged an alliance to connect FreeStyle Libre sensors with automated insulin pumps, signaling a preference for cooperative ecosystems over isolated platforms. GE Healthcare’s AI Innovation Lab invests in deep-learning algorithms that complement its hardware footprint, reinforcing end-to-end solutions rather than stand-alone sensors.

Product differentiation increasingly rests on miniaturization and software sophistication. New entrants exploit 3-D printing and nanomaterials to leapfrog legacy designs at a fraction of historical development cost. Meanwhile, incumbents explore circular-economy models that convert used sensors into feedstock, aligning with hospital sustainability targets and warding off regulatory risk. Successful firms combine transparent data-security frameworks with scalable manufacturing to secure multi-year supply contracts and defend share in the disposable medical device sensors market.

Disposable Medical Devices Sensors Industry Leaders

Medtronic plc

GE Healthcare

Koninklijke Philips N.V.

Abbott Laboratories

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tandem Diabetes Care agreed with Abbott to link automated insulin delivery systems to forthcoming glucose-ketone sensors for proactive ketoacidosis prevention.

- April 2025: Biolinq raised USD 100 million Series C funding to commercialize color-changing multi-analyte wearable patches after completing pivotal U.S. trials.

- February 2025: TDK introduced Nivio xMR magnetic sensor that measures biomagnetic fields without shielded rooms, promising lower-cost imaging.

- August 2024: Medtronic secured FDA clearance for Simplera disposable CGM and formalized its global collaboration with Abbott for joint CGM development.

- August 2024: Abbott partnered with Medtronic to embed FreeStyle Libre technology in Medtronic insulin systems, targeting 11 million insulin-therapy users.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the disposable medical device sensors market as every single-use biosensor, image sensor, accelerometer, pressure sensor, or temperature sensor that converts physiological or biochemical signals into electrical outputs for human diagnostic, monitoring, or therapeutic use across hospital, ambulatory, and home-care settings.

Scope Exclusion: Reusable probes, multi-patient cables, and smart consumables such as infusion sets are excluded.

Segmentation Overview

- By Product

- Biosensors

- Electrochemical Biosensors

- Optical Biosensors

- Image Sensors

- Accelerometers

- Pressure Sensors

- Temperature Sensors

- Other Products

- Biosensors

- By Application

- Patient Monitoring

- Diagnostics

- Therapeutics

- By End-User

- Hospitals & Clinics

- Home-care Settings

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Research & Academic Institutes

- By Technology

- MEMS

- CMOS

- 3-D Printed Polymeric Sensors

- Nanotechnology-enabled Sensors

- RFID / NFC Tags

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- GCC

- Rest of South America

- Rest of Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Direct interviews with sensor OEM engineers, contract manufacturers, hospital procurement heads, and regulators across North America, Europe, and Asia helped us validate shipment volumes and average selling prices, while short surveys with endocrinologists clarified patient compliance and likely replacement frequency.

Desk Research

We drew on tier-one public sources such as WHO Global Health Observatory, OECD Health Statistics, FDA 510(k) clearances, UN Comtrade codes 9027 and 9026, and PubMed articles detailing sensor replacement cycles. Company filings, patent trends accessed through Questel, and news libraries on Dow Jones Factiva enriched pricing and competitive insight.

We also referenced paid data from D&B Hoovers and guidance from bodies like the Association for the Advancement of Medical Instrumentation and the Diabetes Technology Society to benchmark adoption. Many additional secondary references informed the analysis; the sources named above are illustrative, not exhaustive.

Market-Sizing & Forecasting

Sizing begins with a top-down rebuild of demand using global production and trade values, which we then test through selective bottom-up supplier revenue roll-ups and channel checks. Inputs include annual unit shipments, ASP spreads between MEMS and CMOS designs, prevalence of diabetes and chronic kidney disease, hospital infection penalty spending, and home-care kit penetration. A multivariate regression blended with ARIMA projects these drivers to 2030, and gaps in bottom-up samples are bridged by weighted regional proxies agreed with interviewees.

Data Validation & Update Cycle

At this stage, we run variance checks against historical series, resolve anomalies in peer reviews, and refresh the model annually, with interim edits for material regulatory or supply events before a final sweep prior to client delivery.

Why Our Disposable Medical Devices Sensors Baseline Commands Reliability

Published estimates often diverge because providers pick different sensor mixes, price assumptions, and refresh cadences. Our disciplined scope and annually updated variables give decision-makers a dependable yardstick.

Key gap drivers include inclusion of implantable probes by some publishers, constant 2021 prices, narrower geography, and straight-line CAGRs that ignore reimbursement reforms captured in Mordor's base case.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.92 B (2025) | Mordor Intelligence | |

| USD 9.52 B (2022) | Global Consultancy A | Older base year and flat ASP assumption |

| USD 8.63 B (2024) | Research Firm B | Excludes image sensors and home-care kits |

| USD 6.50 B (2021) | Industry Analytics C | Limited geography and constant FX |

Together, these contrasts show how Mordor's transparent variables and repeatable steps deliver a balanced, trusted baseline for the market.

Key Questions Answered in the Report

What is the current market size of disposable medical device sensors market?

The disposable medical device sensors market is valued at USD 11.03 billion in 2026 and is projected to hit USD 18.74 billion by 2031.

Which product segment holds the largest share?

Biosensors account for 48.12% of 2025 revenue, making them the leading product category.

Which application area is growing the fastest?

Diagnostics leads growth with a 14.11% CAGR to 2031 as point-of-care testing gains broad acceptance.

Why are home-care settings important for future demand?

Home-care applications post a 14.33% CAGR because payers and providers favor remote monitoring to cut hospitalization costs and improve patient comfort.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to grow at 12.29% CAGR through 2031, benefiting from expanding healthcare infrastructure and rising chronic-disease prevalence.

How are regulations affecting new sensor launches?

Tighter quality-system and interoperability rules extend development timelines and raise compliance costs, especially for small innovators, tempering short-term market growth.

Page last updated on: