Disposable Medical Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.55 Billion |

| Market Size (2031) | USD 18.81 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Disposable Medical Gloves Market Analysis by Mordor Intelligence

The Disposable Medical Gloves Market size was valued at USD 10.48 billion in 2025 and estimated to grow from USD 11.55 billion in 2026 to reach USD 18.81 billion by 2031, at a CAGR of 10.23% during the forecast period (2026-2031). This growth is benefits from structurally high glove-per-capita usage in healthcare, and the market now settles into a post-pandemic baseline that is still materially above 2019 levels. North America holds the largest Disposable Medical Gloves market share at 34% in 2024, and its continued preference for domestically manufactured PPE encourages local capacity additions. A notable observation is that purchasing managers are placing longer-tenor orders than during the crisis years, signaling confidence in price stability and supply security. At the same time, major distributors report that stockpiles built during the pandemic are steadily depleting, ensuring that replenishment demand underpins near-term volumes. Rising awareness of contact-based infection risks in non-hospital settings such as dental clinics and home care further widens the demand base. It subtly shifts the channel mix toward smaller order sizes.

Key Report Takeaways

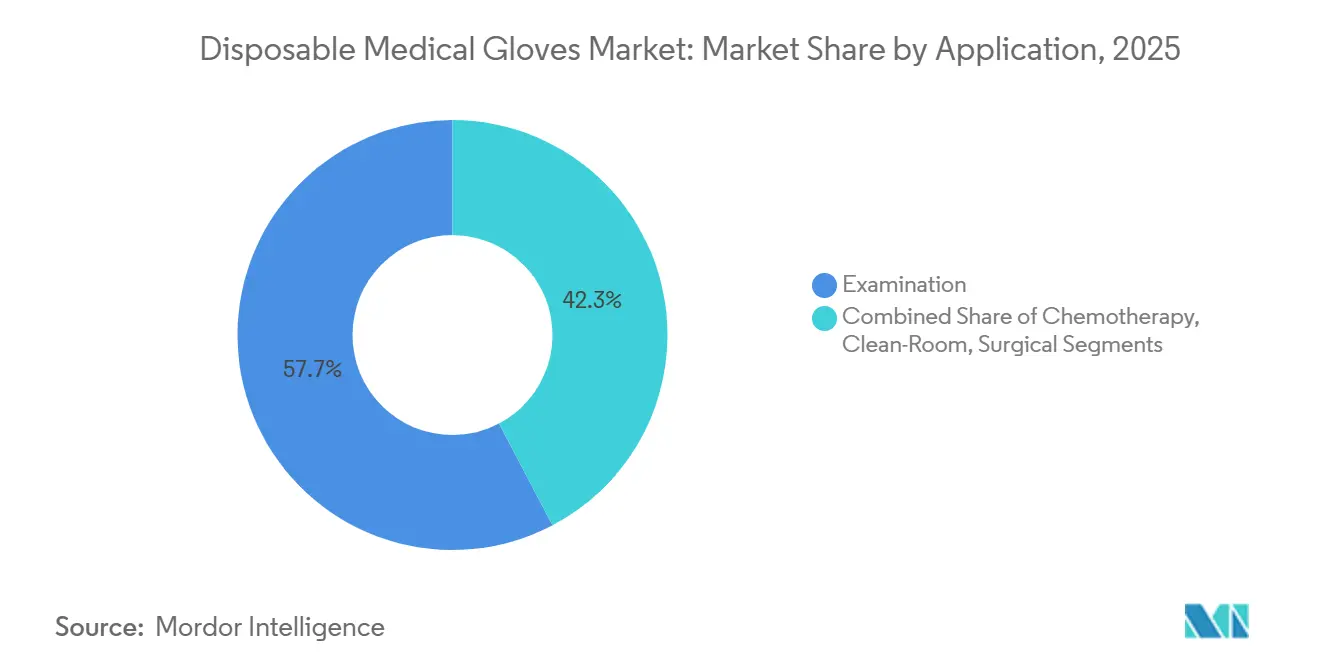

- By application, Examination gloves dominated with a 57.70% revenue share in 2025, while Chemotherapy gloves are projected to grow the quickest at a 11.15% CAGR through 2031.

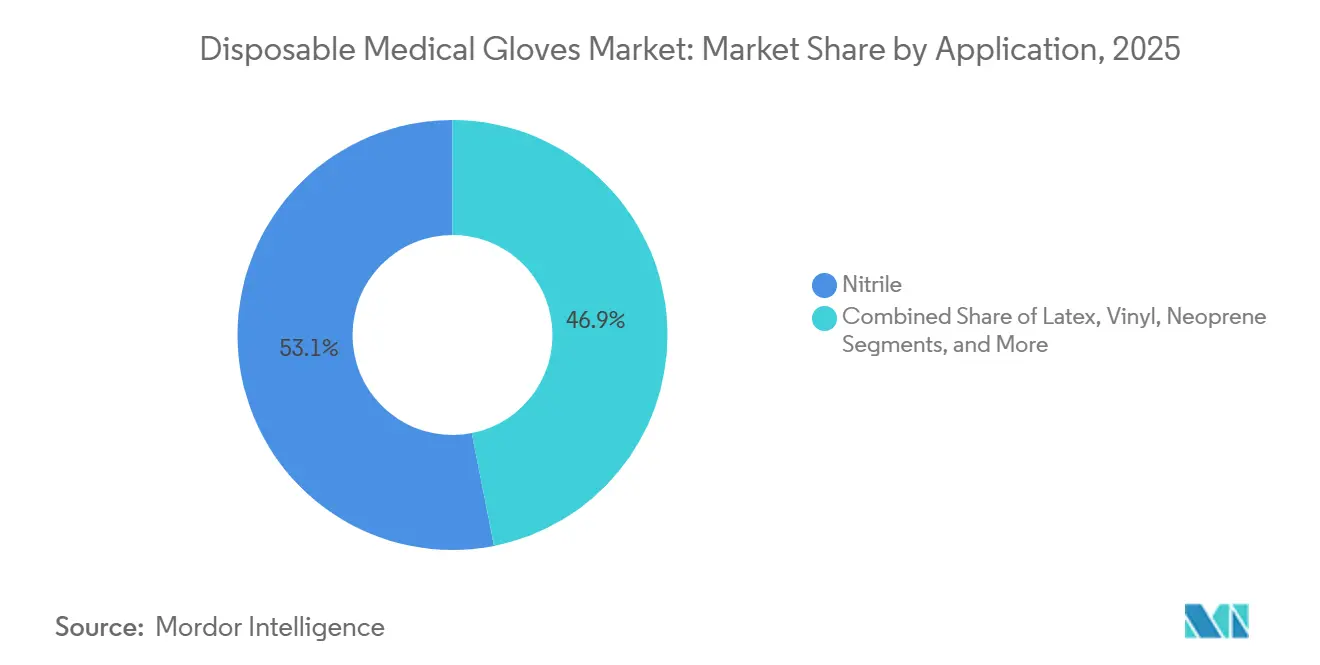

- By material, Nitrile accounted for the most significant 53.10% share of 2025 revenues; Neoprene is forecast to post the fastest CAGR at 11.98% during 2026-2031.

- By form, the Powder-free segment led with a 74.05% market share in 2025 and is also slated to remain the fastest-expanding category, advancing at a 10.55% CAGR to 2031.

- By sterility, Non-sterile gloves captured an 82.55% share in 2025, whereas Sterile gloves are expected to grow at the highest 11.35% CAGR over the forecast period.

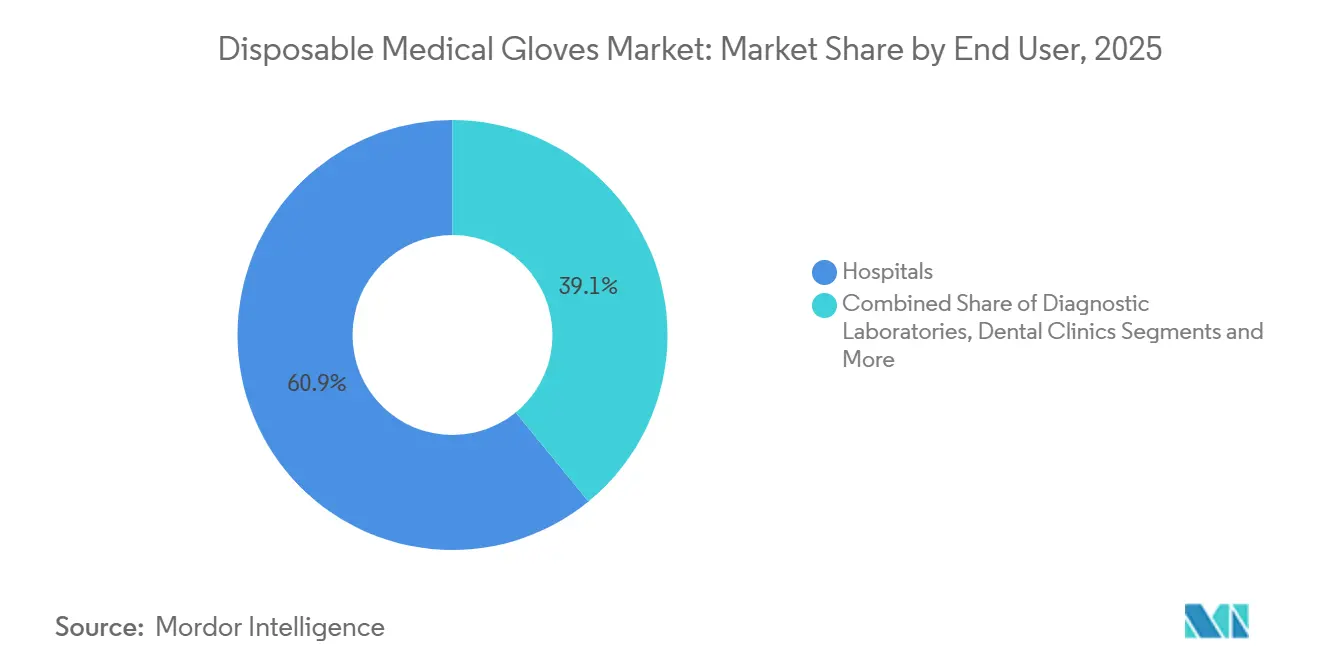

- By end user, Hospitals represented 60.90% of 2025 revenues; Ambulatory Surgical Centers are set to register the strongest growth, with an 10.65% CAGR through 2031.

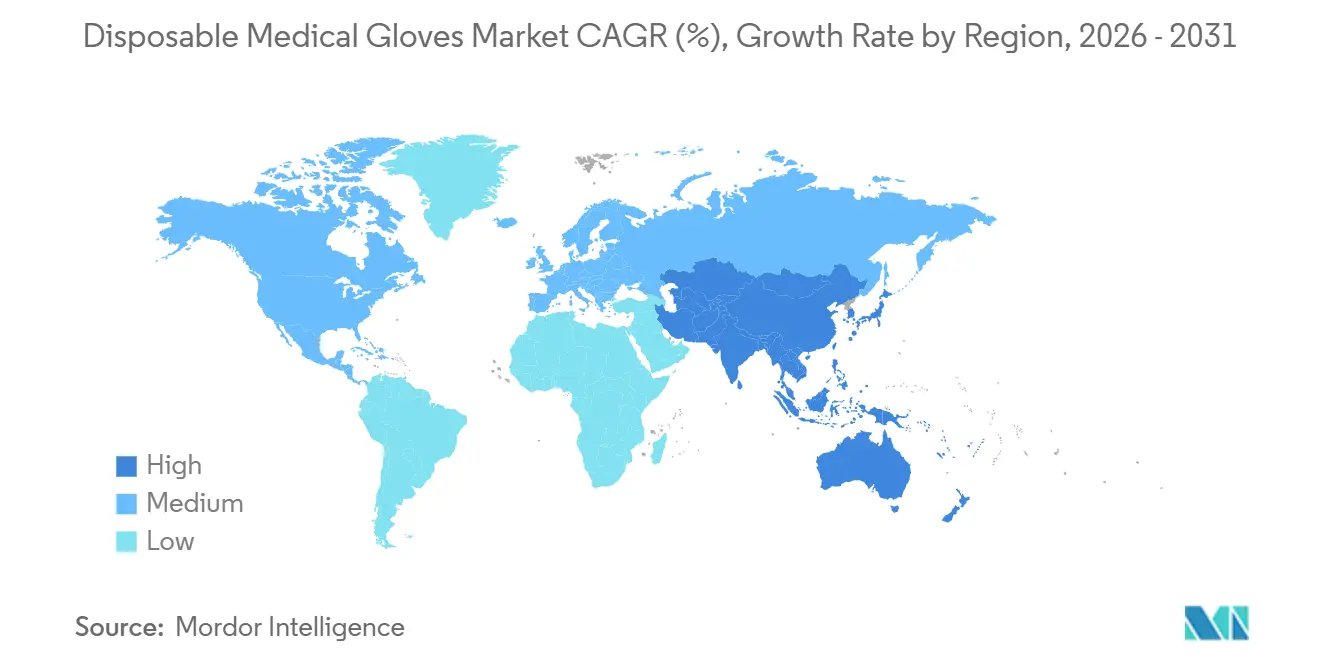

- By geography, North America was the largest region, holding 33.85% of 2025 revenues, while Asia-Pacific is projected to be the fastest-growing region at a 11.05% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Medical Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global infection-control standards | +2.8% | Global, especially North America & EU | Short term (≤2 yrs) |

| Rising surgical & diagnostic procedure volumes | +2.5% | Global, higher in aging regions | Long term (≥5 yrs) |

| Shift to synthetic (nitrile/neoprene) gloves for allergy compliance | +1.9% | Global, faster in developed markets | Medium term (~3-4 yrs) |

| Expansion of healthcare infrastructure & insurance in emerging economies | +1.7% | APAC core, spill-over to MEA | Long term (≥5 yrs) |

| Process & automation advances delivering high-volume, low-cost production | +1.4% | Global manufacturing hubs, led by Malaysia and U.S. on-shoring | Medium term (~3-4 yrs) |

| E-procurement platforms enabling bulk ordering by small clinics in emerging markets | +0.8% | Emerging markets, Latin America & Southeast Asia | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Stricter Global Infection-Control Standards Across Healthcare Facilities

Healthcare systems are tightening glove usage protocols, moving from generic examination gloves to highly task-specific variants. According to updated American Red Cross[1]American Heart Association and American Red Cross, “2024 Guidelines for First Aid,” December 10, 2024, www.ahajournals.orgguidelines released in November 2024, first-aid responders must don medical examination gloves for every patient interaction, a recommendation now echoed in many national protocols. Intensive-care audits under Australia’s 2024 safety framework[2]Australian Commission on Safety and Quality in Health Care. "Sustainable Glove Use for Healthcare Workers Fact Sheet." 2024, www.safetyandquality.gov.aushow average consumption of 30 pairs per patient per 12-hour shift, underscoring how protocols translate into volume. The shift obliges procurement teams to diversify SKUs, and that complexity spurs hospitals to adopt inventory-management software that flags impending stock-outs in real time.

Rising Surgical & Diagnostic Procedure Volumes Driven by Aging & Chronic-Disease Burden

Procedure growth remains a pillar of the Disposable Medical Gloves market expansion. Medicare data indicate 56 new ambulatory surgical centers certified in one recent quarter, illustrating how outpatient capacity absorbs rising surgical demand from the 65+ age cohort. Journal of Medicine, Surgery, and Public Health projections show patients over 65 could account for 39% of all U.S. surgeries by 2034, translating directly into higher sterile-glove pull-through. A similar demographic trend in Europe, where the senior population could approach 30% by mid-century, suggests that procedure-linked glove volumes will stay elevated even if per-procedure glove counts stabilize.

Industry-Wide Shift to Synthetic (Nitrile/Neoprene) Gloves for Allergy Compliance

Latex allergies in 1-6% of healthcare workers continue to catalyze migration toward synthetic materials. Nitrile already commands 53% disposable medical gloves market share, and neoprene, expanding at 11.2% CAGR, is steadily gaining acceptance because its elasticity closely mimics latex. Hospital purchasing data from large integrated delivery networks show a measurable drop in latex SKUs year-on-year, driven equally by staff preference surveys and insurer guidelines that discourage allergen exposure. An emerging nuance is that synthetic-glove makers now market softer film formulations that enhance tactile sensitivity, lowering the residual switching cost for long-time latex users.

Expansion of Healthcare Infrastructure & Insurance Coverage in Emerging Economies

Asia Pacific posts the fastest regional growth at 9.3% CAGR, backed by new hospital construction, public-insurance rollouts, and vibrant medical-tourism flows. Malaysian Investment Development Authority[3] Malaysian Investment Development Authority, “Malaysia’s Medical Devices Industry: Immense Growth Potential,” March 15, 2023, www.mida.gov.mybriefings confirm that domestic producers still supply roughly 60% of the world’s medical gloves, and their move into accelerator-free products bolsters export competitiveness under tightening Western regulations. Trade diversion effects from higher U.S. tariffs on Chinese gloves further improve Southeast Asian producers’ order books, while Indian consumables distributors report that expanding health-insurance schemes support a broader product mix beyond basic examination gloves. These dynamics collectively channel investment into local warehousing and just-in-time delivery models within fast-growing urban hospital clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in natural rubber & nitrile-butadiene feed-stock prices | −1.8% | Global, sharper in Asia | Short term (≤ 2 yrs) |

| Intensifying environmental & sustainability regulations on single-use plastics | −1.2% | North America & EU, gradual global spread | Medium term (~ 3-4 yrs) |

| Global overcapacity post-pandemic triggering persistent price competition | −1.5% | Global, with early impacts in major export hubs | Medium term (~ 3-4 yrs) |

| U.S. Withhold-Release Orders on labor practices creating import uncertainty | −0.6% | U.S. inbound supply chains, spill-over to Malaysia & Thailand | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Volatility in Natural Rubber & Nitrile-Butadiene Feedstock Prices

Flooding in Thailand nudged natural latex prices higher in late 2024, forcing smaller glove makers to renegotiate supply contracts on shorter cycles. At the same time, a weakening USD versus Asian currencies narrowed export margins, prompting leading Malaysian producers to discuss average selling-price increases toward USD 21–22 per 1,000 pieces for Q4 2024. Acrylonitrile prices eased, giving nitrile-focused manufacturers brief margin relief, yet petrochemical volatility remains a planning headache. The pattern incentivizes vertical integration into raw-material streams and fuels R&D into alternative elastomers that display less commodity price sensitivity.

Intensifying Environmental & Sustainability Regulations on Single-Use Plastics

The Break Free From Plastic Pollution Act of 2023 sets an aggressive reduction target for single-use plastics by 2025, compelling healthcare facilities to justify glove utilization or adopt greener options. Conventional nitrile gloves can take up to two centuries to decompose, a statistic that pressures hospital sustainability officers to seek biodegradable substitutes. SHOWA’s lab data demonstrate that certain nitrile formulations decompose by 82% within 386 days in landfill-simulated conditions, showcasing viable pathways to regulatory compliance. Manufacturers that can offer verified environmental benefits without performance trade-offs position themselves for preferential supplier status in upcoming tender rounds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Examination Gloves Drives the Market

Examination gloves hold a 57.70% market share in the Disposable Medical Gloves market in 2025, reflecting their universal role across clinical and non-clinical settings. Hospitals report that standard examination SKUs account for nearly three-quarters of monthly glove lines on purchase orders, illustrating entrenched baseline demand. A growing share now features chemo-tested nitrile to satisfy broader formularies, subtly blending categories and lifting average selling prices. That shift suggests incremental revenue upside even within a mature subsegment.

Chemotherapy gloves post the fastest forecast expansion at 11.15% CAGR through 2031, propelled by oncology service growth and ASTM D6978 breakthrough-time requirements. Contract wins in large U.S. cancer networks show that suppliers offering full chemo-drug permeation panels secure multi-year agreements. Surgical gloves, growing at a significant percentage, benefit from rising procedure counts, while clean-room gloves gain from semiconductor fab expansions that impose stricter contamination thresholds. The specialized nature of these uses makes regulatory compliance a practical barrier that protects pricing power for qualified producers.

Material: Nitrile Commands the Disposable Medical Gloves Market

Nitrile commands 53.10% Disposable Medical Gloves market share and remains the mainstream choice due to hypoallergenic properties and chemical resistance. Purchasing databases indicate that nitrile volume surged nearly fivefold from 2010 to 2024, suggesting that the material shift is durable. Increased line-speed automation brings average unit cost down, enabling nitrile producers to defend share against lower-priced vinyl in cost-sensitive accounts. Stable nitrile demand, paired with moderate feedstock relief, underpins supplier cash flows for further capacity upgrades.

Neoprene exhibits the highest growth at 11.98% CAGR, mainly because its latex-like comfort eases clinician transition from legacy materials. Premium dental and surgical users note that neoprene’s elasticity reduces hand-fatigue complaints during long procedures, subtly influencing brand loyalty. Latex keeps a shrinking but sizeable foothold in regions where allergy policies are less stringent, while vinyl (PVC) and polyethylene serve budget-constrained or non-critical tasks. Sustainability considerations are steering R&D toward biodegradable nitrile blends that meet both performance and environmental criteria, indicating likely portfolio rebalancing in the next product-cycle.

Form: Powder-free Gloves Dominate Market

Powder-free gloves dominate with 74.05% Disposable Medical Gloves market size in 2025 and grow at 10.55% CAGR, reflecting global regulatory discouragement of powdered variants. FDA restrictions already removed powdered surgical gloves from the U.S. market, and similar rules are advancing elsewhere. Powder-free adoption reduces post-operative complication risk and simplifies reimbursement coding, an under-appreciated benefit for billing departments. Manufacturing advances such as polymer inner coatings improve donning ease, erasing legacy ergonomic concerns.

Powdered gloves continue to decline, yet retain presence in certain emerging markets where cost still trumps regulation. Importers in these regions increasingly request documentation on powder residue levels, hinting at impending stricter local standards. Some suppliers respond by offering low-powder transitional lines while customers adjust budgets. Overall trajectory implies eventual phasing-out, reinforcing powder-free as the enduring default in the Disposable Medical Gloves industry.

By Sterility: Non-sterile Gloves Fuel the Market

Non-sterile gloves account for 82.55% market share in 2025, a figure tied to the sheer volume of routine examinations and nursing tasks. Bulk tenders by group purchasing organizations frequently bundle non-sterile SKUs with other disposable items, streamlining procurement and sustaining high baseline throughput. Recent bids increasingly specify color-coding to reduce cross-contamination errors, revealing how infection-control refinements shape even low-acuity products. Demand outside hospitals, such as home-health services, adds incremental volume.

The sterile segment is forecast to grow 11.35% annually, outpacing overall market because minimally invasive procedures require ever-stricter aseptic technique. Packaging innovations that prolong shelf life in variable climates help emerging-market hospitals reduce wastage, freeing budget for higher-grade steriles. Diagnostic and interventional radiology suites now mandate sterile gloves for image-guided biopsies, broadening use cases. Such protocol expansions suggest that sterile consumption will diversify beyond traditional operating rooms.

By End-User: Hospitals Retain Disposable Medical Gloves Market

Hospitals retain 60.90% Disposable Medical Gloves market share in 2025, supported by large consolidated purchase agreements that guarantee volume visibility. Their shift toward value-based care incentivizes supply-chain efficiency, driving preference for vendors offering usage analytics alongside product. Internal benchmarking shows that facilities adopting right-sizing programs cut glove overuse by double-digit rates without compromising safety, implying that data-driven partnerships may become a key supplier-selection criterion.

Ambulatory surgical centers expand at 10.65% CAGR, reflecting payer efforts to migrate suitable procedures to lower-cost sites. Their streamlined purchasing cycles favor suppliers with agile logistics and smaller-case-quantity offerings. Diagnostic laboratories maintain steady growth due to routine testing, while dental clinics demand ultra-soft, tactile gloves to improve clinician comfort. Home-care is an emerging user base, where e-commerce bundles gloves with wound-care kits, illustrating new retail-style purchasing patterns.

Geography Analysis

North America leads with a 33.85% Disposable Medical Gloves market share, supported by high per-capita healthcare spending and rigorous infection-control regulations. The Centers for Medicare & Medicaid Services' proposal to adjust payments for domestically manufactured PPE narrows the cost disadvantage of U.S.-made gloves by approximately USD 0.13 per unit. That policy momentum spurs existing producers to expand capacity in states such as Texas and Alabama, and early evidence shows shorter lead times influencing hospital sourcing choices. The region also exhibits strong adoption of task-specific glove protocols, contributing to SKU proliferation within hospital formularies.

Asia Pacific’s 11.05% CAGR rests on healthcare infrastructure expansion, rising insurance coverage, and thriving medical tourism. Malaysian plants incorporate Industry 4.0 robotics to raise line speeds above 45,000 pieces per hour, cushioning wage inflation. Trade policy shifts, especially higher U.S. duties on Chinese gloves, benefit Southeast Asian exporters through order diversion. India’s government investment in 157 new medical colleges accelerates demand for examination and surgical gloves, and localized warehousing in Tier-2 cities reduces last-mile costs for distributors.

Europe sustains a notable share, underpinned by stringent environmental directives that elevate demand for eco-friendly glove alternatives. National health systems are piloting procurement frameworks that weigh carbon footprint alongside price, nudging suppliers toward biodegradable nitrile. The Middle East and Africa show rising penetration as governments invest in tertiary hospitals and universal health coverage schemes. In South America, Brazil leads adoption, and state purchase programs increasingly include training on correct glove disposal, an element contributing to broader infection-prevention capacity building.

Competitive Landscape

The top five suppliers hold a significant global Disposable Medical Gloves market share, yet the structure is less concentrated than many medical-device categories. Major producers pursue vertical integration, owning nitrile-butadiene capacity to insulate margins from feedstock swings. Plant automation, including AI-guided defect detection, cuts scrap rates, giving incumbents further cost advantage that smaller firms struggle to match. The sizable mid-tier cohort thrives by specializing in materials like accelerator-free formulations or by focusing on region-specific regulatory certifications.

Sustainability is becoming a competitive frontier. Only 1% of gloves currently use biodegradable materials, leaving considerable white space for differentiation. Suppliers that credibly validate landfill degradation times acquire preferred-supplier status in green-procurement pilots across European hospitals. Simultaneously, the antimicrobial-glove niche gains traction as infection-prevention committees seek supplementary barriers in high-risk wards. These value-added features support premium pricing, cushioning vendors from commoditization pressure.

Technology and service innovation influence deal wins. Mölnlycke’s 3-D hand-scanning tool customizes surgical-glove sizing, improving surgeon comfort and reducing wastage from sizing errors, a feature resonating with high-volume cardiac centers. U.S. start-ups, aided by federal PPE-onshoring grants, enter the market with modular micro-factories that enable just-in-time regional supply. Market participants also leverage data analytics to forecast demand spikes, enhancing resilience and differentiating themselves during tender evaluations that increasingly score supply security.

Disposable Medical Gloves Industry Leaders

-

Top Glove Corp. Bhd

-

Hartalega Holdings Bhd

-

Ansell Ltd.

-

Kossan Rubber Industries

-

Sri Trang Gloves PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Intco Medical introduced Syntex synthetic disposable latex gloves; the launch broadens material options for users seeking a latex feel without natural-rubber allergen exposure. The product’s early adoption by high-throughput clinics signals appetite for diversified synthetic blends.

- February 2025: SW Sustainability Solutions signed a national group-purchasing agreement with Premier, Inc. running from May 2025 to April 2028; the deal gives Premier members access to exam gloves incorporating EcoTek biodegradable technology. The multi-year term provides volume certainty that supports SW’s expansion of green-glove capacity.

- February 2024: Ansell released MICROFLEX Mega Texture 93-256, a nitrile glove designed for industrial settings, adding cross-industry diversification to its healthcare portfolio. Early distributor feedback notes that the high-texture grip suits emergency medical technicians handling wet equipment.

- January 2024: Medline completed the acquisition of United Medco, boosting distribution reach across U.S. post-acute-care facilities. The enlarged network accelerates Medline’s ability to supply examination gloves to home-health providers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the disposable medical gloves market as single-use nitrile, latex, vinyl, neoprene, and polyethylene gloves supplied sterile or non-sterile for surgical, examination, chemotherapy, and clean-room healthcare tasks worldwide. According to Mordor Intelligence, values capture fresh factory shipments that eventually reach professional end users through institutional, online, and pharmacy channels.

We exclude all disposable gloves intended mainly for food handling, industrial safety, cleaning, or consumer hobby use.

Segmentation Overview

-

By Application

- Surgical

- Examination

- Chemotherapy

- Clean-Room

-

By Material

- Nitrile (NBR)

- Latex (Natural Rubber)

- Vinyl (PVC)

- Neoprene (Polychloroprene)

- Polyethylene (CPE/TPE)

-

By Form

- Powder-Free

- Powdered

-

By Sterility

- Sterile

- Non-Sterile

-

By End-User

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Dental Clinics

- Home-Care Settings

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with hospital supply managers, global distributors, latex and nitrile compounders, and infection-control specialists across North America, Europe, ASEAN, and the Gulf. These conversations verify usage rates, price shifts, and regulatory timelines and plug gaps left by desk work.

Desk Research

We first map the demand pool using open sources such as World Health Organization surgery statistics, U.S. CDC infection reports, UN Comtrade trade lines (HS-4015), Malaysian Rubber Council export bulletins, and Questel patent trends. Company 10-Ks, hospital purchasing contracts, and Factiva-tracked price movements supply recent cost and margin signals that we then cross-check.

Public sources named here are illustrative only; many other regulatory notes, peer-reviewed journals, and trade bulletins informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down rebuild starts from production and trade volumes, converts them to end-market value through region-specific average selling prices, and is corroborated with supplier roll-ups plus sampled hospital invoices before totals are adjusted. Key variables tracked include surgical procedure counts, glove-per-patient norms, powder-free adoption ratios, raw latex price swings, and announced nitrile capacity additions. Multivariate regression blended with ARIMA projects the five-year outlook, while scenario tweaks from expert interviews bound upside and downside cases.

Data Validation & Update Cycle

Outputs pass multi-layer variance screens, peer review, and a final analyst walk-through before sign-off. We refresh every twelve months, with rapid revisions if material events, such as disease outbreaks or tariff shifts, alter underlying variables.

Why Mordor's Disposable Medical Gloves Baseline Remains Dependable

Published estimates often diverge because firms pick different product scopes, currency bases, and refresh cadences.

Some report conservative hospital-only demand, whereas others fold in industrial or consumer gloves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.48 B (2025) | Mordor Intelligence | |

| USD 7.49 B (2024) | Global Consultancy A | Excludes chemotherapy, home-care users, and e-commerce flows |

| USD 19.20 B (2023) | Trade Journal B | Combines medical and industrial gloves; broad ASP averaging across grades |

These contrasts show that Mordor's disciplined scope selection, annual refresh cycle, and dual-path validation give decision-makers a balanced, transparent baseline they can rely on.

Key Questions Answered in the Report

What is the current Disposable Medical Gloves market size?

The market size is USD 11.55 billion in 2026, on track to reach USD 18.81 billion by 2031.

Which region holds the largest Disposable Medical Gloves market share?

North America leads with a 33.85% share, driven by strict infection-control policies and high healthcare spending.

Why are synthetic gloves gaining ground in the Disposable Medical Gloves industry?

Synthetic materials like nitrile and neoprene avoid latex allergies and offer strong chemical resistance, making them the preferred choice in modern procurement guidelines.

How are sustainability regulations affecting glove producers?

New laws targeting single-use plastics push manufacturers to create biodegradable or recyclable glove options, influencing R&D priorities and tender requirements.

Which end-user segment is growing fastest?

Ambulatory surgical centers expand most rapidly at 10.65% CAGR as outpatient procedures rise.

Page last updated on: