Vitreous Tamponade Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

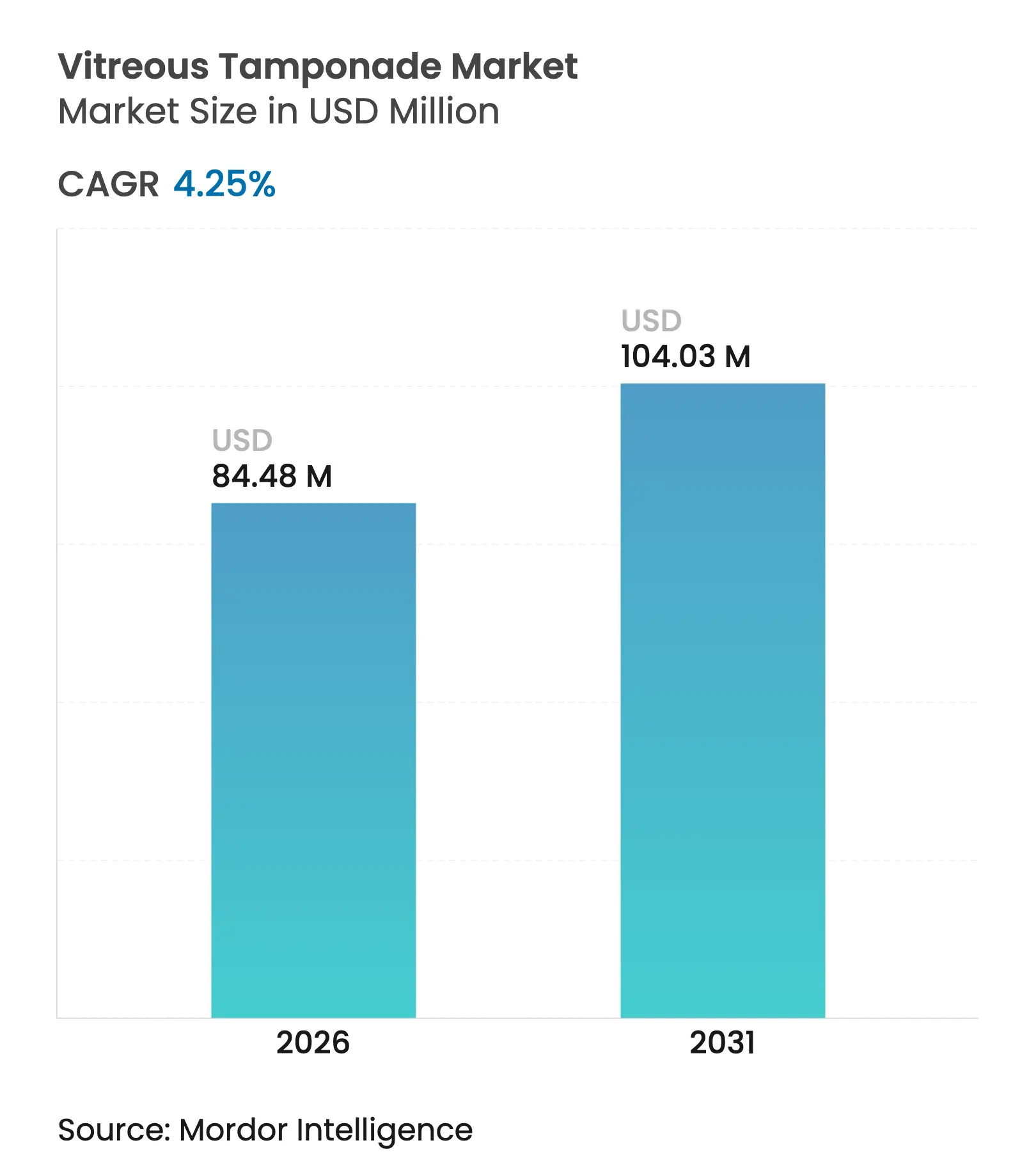

| Market Size (2026) | USD 84.48 Million |

| Market Size (2031) | USD 104.03 Million |

| Growth Rate (2026 - 2031) | 4.25 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Vitreous Tamponade Market Analysis by Mordor Intelligence

The vitreous tamponade market size was valued at USD 81.04 million in 2025 and estimated to grow from USD 84.48 million in 2026 to reach USD 104.03 million by 2031, at a CAGR of 4.25% during the forecast period (2026-2031). The expansion reflects a measured shift from volume growth toward precision-driven procedures helped by rising diabetic retinopathy prevalence and steady adoption of 25-gauge and 27-gauge micro-incision vitrectomy platforms. Hydrogels that emulate native biomechanics are on the cusp of regulatory approval, setting the stage for a technology refresh that reduces the revision burden linked to silicone oils. Hospitals keep case volumes high, yet day-case vitrectomy in ambulatory surgical centers is rising as payers reward lower facility costs. Competitive intensity centers on integrated surgical ecosystems, with platform clearances such as Alcon’s Unity system signalling tighter linkage between instrumentation and tamponade delivery.

Key Report Takeaways

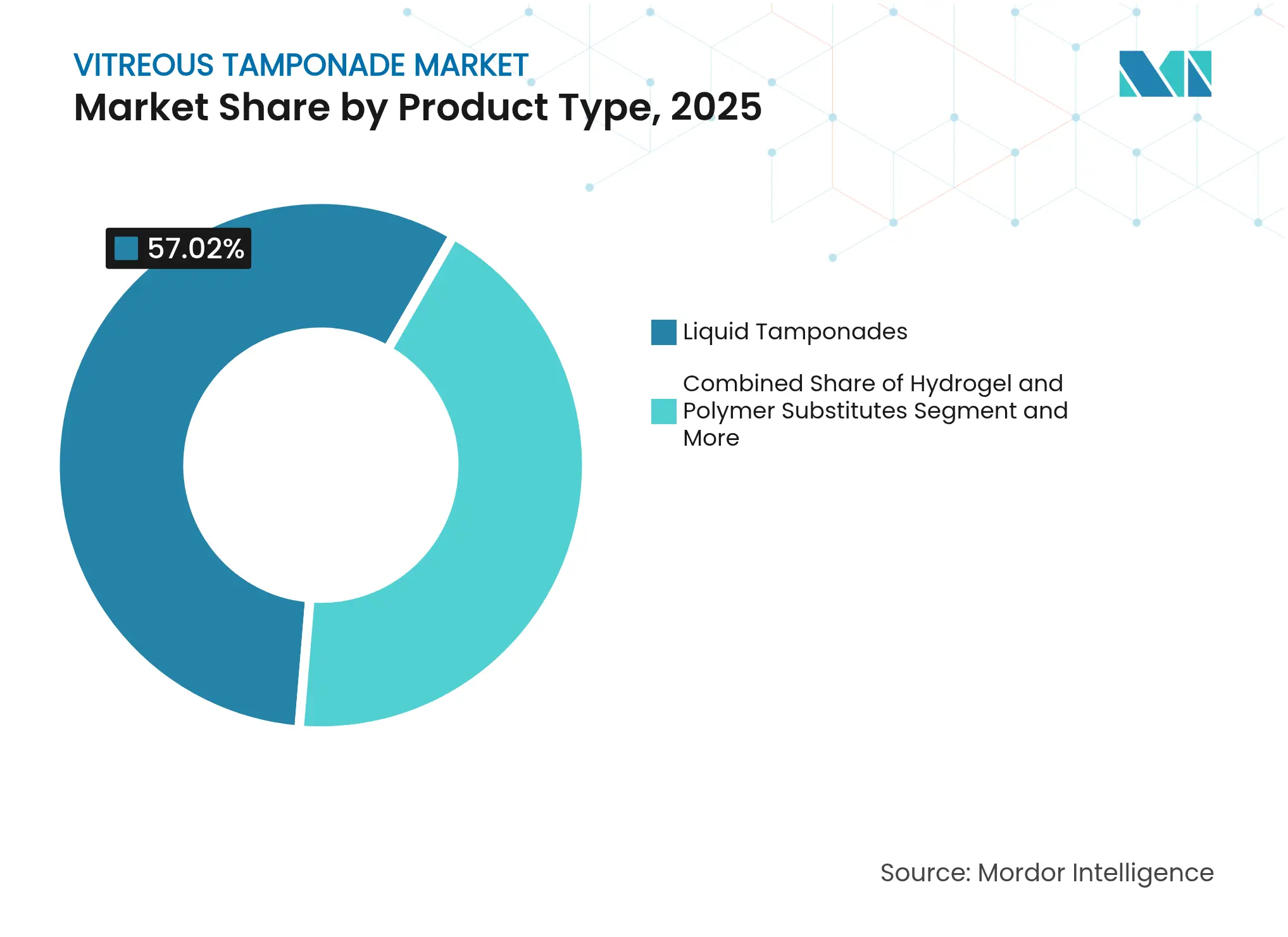

- By product type, liquid tamponades led with 57.02% of vitreous tamponade market share in 2025 while hydrogels are forecast to expand at a 13.92% CAGR to 2031.

- By application, rhegmatogenous retinal detachment accounted for 46.10% of the vitreous tamponade market size in 2025 and ocular trauma is advancing at an 8.63% CAGR through 2031.

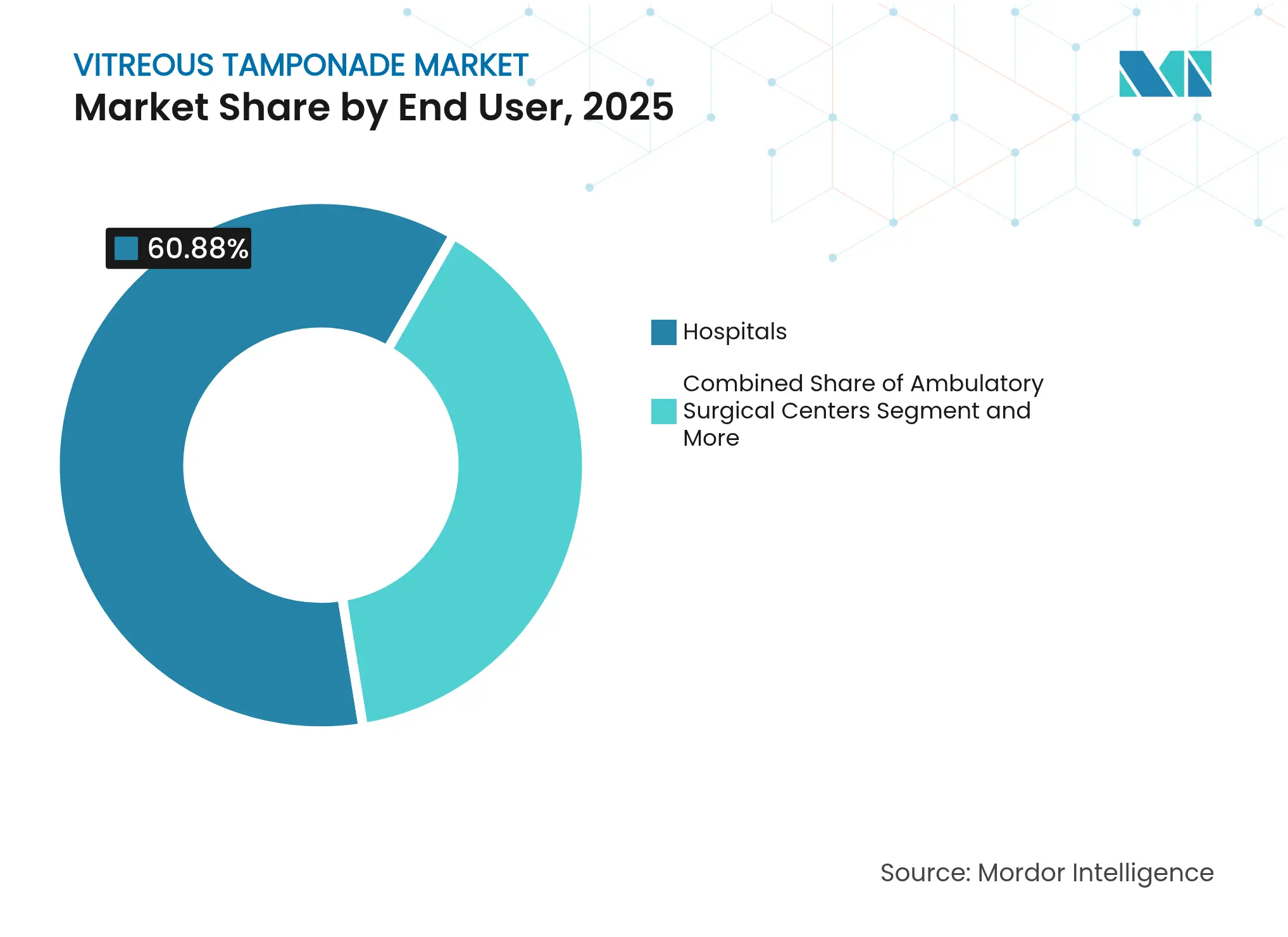

- By end user, hospitals held 60.88% of the vitreous tamponade market size in 2025, while ambulatory surgical centers record the highest projected CAGR at 8.42% to 2031.

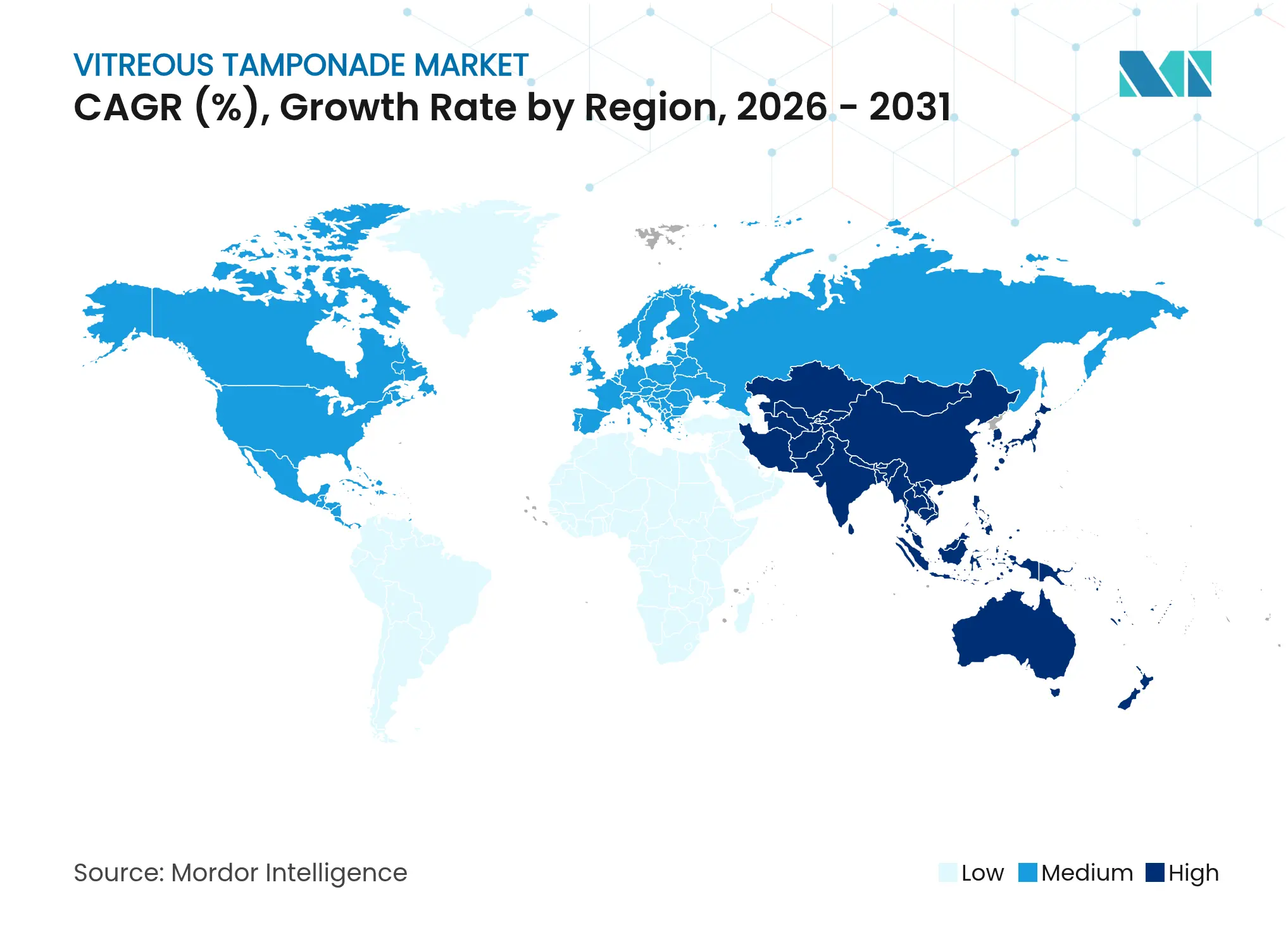

- By geography, North America controlled 35.90% revenue share in 2025 and Asia-Pacific is poised for an 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitreous Tamponade Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Burden Of Retinal Disorders & Diabetic Retinopathy

Rising

Burden Of Retinal Disorders & Diabetic Retinopathy

Rising

| +1.2% | Global, with highest impact in North America & Asia-Pacific | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, with highest impact in North America &

Asia-Pacific

| Impact Timeline:

Long term (≥ 4 years)

|

Rapidly Ageing Global Population

Rapidly Ageing Global Population

| +0.8% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Advances In 25/27-Gauge Minimally-Invasive Vitrectomy

Platforms

Advances In 25/27-Gauge Minimally-Invasive Vitrectomy

Platforms

| +0.6% | North America & Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Hydrogel Vitreous Substitutes Approaching First Approvals

Hydrogel Vitreous Substitutes Approaching First Approvals

| +0.5% | Global, with early adoption in developed markets | Medium term (2-4 years) | |||

Shift To Day-Case Vitrectomy In Ambulatory Surgical

Centres

Shift To Day-Case Vitrectomy In Ambulatory Surgical

Centres

| +0.4% | North America & Europe primarily | Short term (≤ 2 years) | |||

China's Fast Uptake Of Foldable Capsular Vitreous Body

(FCVB)

China's Fast Uptake Of Foldable Capsular Vitreous Body

(FCVB)

| +0.3% | China and expanding to Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Burden of Diabetic Retinopathy Rising

Diabetic retinopathy now affects 9.6 million Americans, and the number continues to grow across Latin America and South-East Asia[1]Centers for Disease Control and Prevention, “VEHSS Modeled Estimates: Prevalence of Diabetic Retinopathy,” cdc.gov. As pathology severity progresses, complex proliferative cases require tamponades able to stay in situ longer than traditional expansile gases, leading surgeons to opt for silicone oils or test late-stage hydrogels. Premium-priced substitutes gain traction because they shorten chair time by avoiding secondary extraction procedures. Payers in the United States continue to reimburse these advanced agents under existing vitrectomy codes, reinforcing commercial viability. In parallel, population health authorities in China have listed vitrectomy and tamponade on the essential medical services schedule, expanding the future pool of reimbursed patients.

Rapidly Ageing Global Population

Twenty-five percent of Japan’s citizens are at least 65 years old, and similar shifts are evident in Germany, Italy, and South Korea. Incidence of rhegmatogenous retinal detachment rises fivefold after age 60, leading to a constant flow of surgical referrals that sustains the vitreous tamponade market. Ophthalmology clinics in metropolitan areas have started weekend surgical sessions to cope with case backlogs. Governments respond by subsidising training for vitreoretinal fellows, which expands the skilled workforce capable of handling tamponade placement. Device makers target this demographic trend with simplified delivery kits that reduce set-up complexity for busy day-case theatres.

Advances in 25/27-Gauge Minimally Invasive Platforms

Cutting speeds of 20,000 cuts per minute delivered through dual-blade tips shorten procedure time by almost 30% compared with 10,000-cpm predecessors. Smaller wounds translate into fewer sutures and faster patient discharge, allowing many rhegmatogenous detachment repairs to be booked as outpatient cases. Instrument miniaturisation expands eligibility to paediatric and geriatric cohorts previously considered poor surgical candidates. The result is a larger addressable base for the vitreous tamponade market and lower per-case facility costs that appeal to health insurers. Manufacturers integrate pre-filled oil cartridges with these systems, enhancing procedural efficiency and reducing contamination risk.

Hydrogel Substitutes Approaching Approval

Alginate-based hydrogels now match the refractive index of natural vitreous and show no emulsification after six months in porcine models. More than 210 trials of therapeutic hydrogels are active worldwide, providing a regulatory learning curve that benefits ophthalmic applications[2]John R. Clegg, “Hydrogels in the Clinic: An Update,” AIChE Journal, aiche.onlinelibrary.wiley.com. Early human safety data demonstrate intraocular pressure stability and straightforward injection through 25-gauge ports. As removal becomes unnecessary, health systems can save on follow-up surgery, supporting premium reimbursement. Analysts expect first approvals in Europe in late 2026, after which North American and Asian regulators historically follow within 18 months, setting up a global revenue inflection point for the vitreous tamponade market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Price Of Ultra-Pure, High-Viscosity Silicone Oils

High Price Of Ultra-Pure, High-Viscosity Silicone Oils

| -0.7% | Global, with highest impact in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.7%

| Geographic Relevance:

Global, with highest impact in emerging markets

| Impact Timeline:

Medium term (2-4 years)

|

Post-Operative Complications Requiring Revision Surgery

Post-Operative Complications Requiring Revision Surgery

| -0.5% | Global, concentrated in complex case centers | Long term (≥ 4 years) | |||

Weak Reimbursement For Heavy Silicone Oils in EMs

Weak Reimbursement For Heavy Silicone Oils in EMs

| -0.4% | Emerging markets primarily | Long term (≥ 4 years) | |||

Regulatory Ambiguity Around Novel Hydrogel Substitutes

Regulatory Ambiguity Around Novel Hydrogel Substitutes

| -0.3% | Global, with varying regional impact | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Price of Ultra-Pure Silicone Oils

Medical-grade oils purified through two-step distillation and filtration command premiums of up to 40% above standard viscosities. Procurement teams in Latin America and parts of Africa increasingly cap reimbursement at lower viscosity grades, prompting surgeons to ration premium oils to the most complex proliferative detachments. Cost–utility analyses show that switching from 5,000 cSt to 1,000 cSt saves USD 510 per case but raises emulsification risk, creating a clinical dilemma. Parallel trade has emerged in some regions, complicating supply chain predictability. These dynamics create a pricing umbrella under which hydrogels and foldable capsular systems can compete on total cost of care rather than unit price alone.

Post-Operative Complications Requiring Revision Surgery

Retinal redetachment occurs in up to 24.6% of eyes after silicone oil removal, and cystoid macular edema affects 41.9% of silicone cases within nine months. Each revision adds USD 2,000–3,400 in direct operating costs and lengthens total recuperation by several weeks. Patient anxiety over possible repeat surgery lowers acceptance of elective tamponade procedures, particularly among older adults reluctant to undergo multiple anaesthetics. Surgeons respond by intensifying monitoring protocols, which raises follow-up costs not always covered by payers. Consequently, near-term volume gains in the vitreous tamponade market are tempered until safer substitutes reach routine practice.

Segment Analysis

By Product Type: Hydrogels Challenge Silicone Dominance

Liquid tamponades held 57.02% of vitreous tamponade market share in 2025, reflecting decades of positive outcomes with silicone oils in complex detachments. The segment anchors the vitreous tamponade market as surgeons continue to rely on known viscosity profiles and predictable tamponade duration. However, oil removal adds at least one additional surgery in 60% of cases, encouraging the clinical community to consider alternative materials. Hydrogels posted the fastest growth at 13.92% CAGR, propelled by their self-healing network and optical transparency that avoid emulsification. Pilot European clinics report reduced postoperative inflammation when hydrogels replace oil, creating early-adopter enthusiasm. Gas agents remain the choice for uncomplicated detachments needing short-term support, though strict positioning limits their wider appeal. Vendors are now bundling gas cylinders with single-use delivery sets to streamline logistics in high-volume centers. Collectively, these shifts underscore a gradual pivot from mere viscosity considerations toward biocompatibility and workflow efficiency in the vitreous tamponade market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Trauma Cases Drive Growth

Rhegmatogenous retinal detachment accounted for 46.10% of the vitreous tamponade market size in 2025 thanks to its high incidence and standardized clinical guidelines. Surgical success rates above 90% keep this segment stable even as demographics evolve. Macular holes and proliferative diabetic retinopathy together form a sizeable secondary cluster where tamponade choice is tailored to anatomical objectives and patient compliance. Ocular trauma, while smaller in absolute volume, posts an 8.63% CAGR by 2031. Broader availability of 23-gauge vitrectomy kits allows prompt removal of intraocular foreign bodies, which reduces infectious sequelae. Defense forces and urban trauma centers upgrade microsurgical suites, expanding tamponade demand in previously under-penetrated settings. The growing evidence base for silicone oil in traumatic endophthalmitis further widens therapeutic scope, bolstering the vitreous tamponade market.

By End User: ASCs Gain Surgical Volume

Hospitals captured 60.88% of vitreous tamponade market size in 2025, leveraging multidisciplinary teams that manage complicated detachments requiring intra-operative imaging and longer anaesthesia. Academic centers influence practice by conducting pivotal trials on novel tamponade materials, driving technology diffusion. Even so, ambulatory surgical centers register an 8.42% CAGR to 2031 because smaller-gauge platforms enable same-day discharge with minimal pain. Payer incentives in the United States raise ASC reimbursement by 2%, shifting case migration steadily outward from tertiary hospitals. Office-based theatre suites, common in Japan and now emerging in Europe, show 97.3% single-surgery anatomic success, cementing confidence. Manufacturers respond by releasing compact vitrectomy systems with pre-programmed settings that align with ASC staffing models. These structural shifts diversify outlets for the vitreous tamponade industry and accelerate adoption of user-friendly substitutes.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained a 35.90% revenue share in 2025 owing to established insurance coverage for vitrectomy and prompt uptake of FDA-cleared tamponade innovations such as the UNIPURE C3F8 gas delivery system. The region benefits from strong clinical trial infrastructure that speeds evidence generation for next-generation hydrogels. Nonetheless, ophthalmologist shortages in several rural states have slowed procedure growth, prompting tele-retina initiatives that may widen referral pipelines over the medium term. Canada mirrors United States dynamics but exhibits tighter price controls that temper premium oil adoption.

Asia-Pacific is forecast to post an 8.33% CAGR through 2031 and represents the fastest regional driver of the vitreous tamponade market. China’s National Medical Products Administration approved the foldable capsular vitreous body (FCVB) and surgeons report 100% reattachment in complex detachments after 12 months. Large diabetes cohorts in India, Indonesia, and the Philippines expand the candidate pool for tamponade procedures. Governments across the region invest in hub-and-spoke eye-care networks, pairing tertiary centers with mobile vitreoretinal units to reach under-served populations. Rising disposable income and increased awareness of modern eye care further support market penetration.

Europe shows steady but slower growth as regulators apply strict scrutiny to novel biomaterials. The European Medicines Agency has requested three-year real-world safety data for hydrogels, delaying commercial rollout beyond initial expectations. Nevertheless, ageing demographics and robust surgical training ecosystems maintain stable silicone oil volumes. Reimbursement reforms in Germany and France link payment more closely to patient-reported outcomes, thereby advantaging supplies that reduce revision rates. Rest-of-World territories, including parts of South America and the Middle East, experience incremental uptake as private hospitals import high-viscosity oils and portable vitrectomy consoles. These diverse regional patterns collectively reinforce a balanced growth outlook for the global vitreous tamponade market.

Competitive Landscape

Market Concentration

Moderate consolidation characterises the vitreous tamponade industry, with the top five suppliers accounting for significant global revenue in 2024. Alcon strengthened its lead by rolling out the Unity Vitreoretinal Cataract System, an integrated platform that streamlines posterior-segment work and tamponade delivery. Bausch + Lomb posted 13% surgical segment growth on the back of higher volumes for intraocular gases and silicone oils. Carl Zeiss Meditec AG acquired Dutch Ophthalmic Research Center, adding DORC’s dual-blade cutters and heavy oil portfolio to its armament.

Technology partnerships bloom around hydrogel pipelines, with start-ups licensing intellectual property to established OEMs that can accelerate regulatory submissions. Genentech’s continuous drug-delivery implant, Susvimo, illustrates convergence between pharmacotherapy and tamponade concepts, hinting at combination products that offer both structural support and anti-VEGF delivery. Robotics also enters the competitive field: Preceyes earned CE marking for a system that steadies surgeon motion at sub-micron accuracy, which could improve tamponade placement in delicate macular surgeries. Meanwhile, mid-tier Asian manufacturers focus on cost-optimised silicone oils to serve emerging markets resisting high import tariffs.

Pricing power remains with incumbents that bundle disposables with capital equipment under long-term service contracts. Tender documents from large hospital networks increasingly favour suppliers who can document lower complication rates, encouraging ongoing R&D into bio-inert materials. Overall, strategic acquisitions, platform ecosystems, and differentiated biomaterials will shape competitive positioning in the vitreous tamponade market through 2030.

Vitreous Tamponade Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: An IRIS Registry analysis of office-based pneumatic retinopexy found that nearly 10% of treated eyes later needed vitrectomy, highlighting the continued role of tamponades in secondary repair.

- January 2025: Fortis Medical Centre in Kolkata installed a microsurgical platform optimised for complex retinal work, expanding access to high-precision vitrectomy in Eastern India.

Table of Contents for Vitreous Tamponade Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Burden Of Retinal Disorders & Diabetic Retinopathy Rising

- 4.2.2Rapidly Ageing Global Population

- 4.2.3Advances In 25/27-Gauge Minimally-Invasive Vitrectomy Platforms

- 4.2.4Hydrogel Vitreous Substitutes Approaching First Approvals

- 4.2.5Shift To Day-Case Vitrectomy In Ambulatory Surgical Centres

- 4.2.6China's Fast Uptake Of Foldable Capsular Vitreous Body (FCVB)

- 4.3Market Restraints

- 4.3.1High Price Of Ultra-Pure, High-Viscosity Silicone Oils

- 4.3.2Post-Operative Complications Requiring Revision Surgery

- 4.3.3Weak Reimbursement For Heavy Silicone Oils in EMs

- 4.3.4Regulatory Ambiguity Around Novel Hydrogel Substitutes

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Liquid Tamponades

- 5.1.2Gas Tamponades

- 5.1.3Hydrogel & Polymer Substitutes

- 5.2By Application

- 5.2.1Rhegmatogenous Retinal Detachment

- 5.2.2Macular Holes

- 5.2.3Proliferative Diabetic Retinopathy & VH

- 5.2.4Ocular Trauma

- 5.2.5Others

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Ambulatory Surgical Centers

- 5.3.3Ophthalmology Clinics

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Rest of the World

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Alcon Inc.

- 6.3.2Bausch + Lomb Corp.

- 6.3.3Carl Zeiss Meditec AG (Dutch Ophthalmic Research Center BV)

- 6.3.4Fluoron GmbH

- 6.3.5Aurolab

- 6.3.6AL.CHI.MI.A. srl

- 6.3.7MedOne Surgical Inc.

- 6.3.8OCULUS Optikgerate GmbH

- 6.3.9Johnson & Johnson Vision

- 6.3.10Beaver-Visitec International (BVI)

- 6.3.11Santen Pharmaceutical Co.

- 6.3.12Vitreq B.V.

- 6.3.13HOYA Corporation

- 6.3.14Wacker Chemie AG

- 6.3.15Dow Inc.

- 6.3.16SilMag S.p.A.

- 6.3.17MIVI Surgical

- 6.3.18PfW Silicone Oil Manufacturing GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Vitreous Tamponade Market Report Scope

Vitreous tamponades are substances used to fill the eye's vitreous cavity during certain surgeries to support the retina or control intraocular pressure. They help maintain the shape of the eye and facilitate healing. These tamponades are available in two primary forms: liquids and gases. Intraocular gas tamponades, such as perfluoropropane (C3F8) and sulfur hexafluoride (SF6), are characterized by being non-toxic, odorless, colorless, and denser than air. Their effectiveness in maintaining adhesion is due to their high surface tension. Conversely, perfluorocarbon liquids (PFCL) are utilized to flatten detached retinas and displace subretinal fluid. Furthermore, the transparency of PFCL facilitates its application during intraoperative photocoagulation.

The vitreous tamponade market is segmented by product type and geography. By product type, the market is segmented into liquid tamponades and gas tamponades. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.