Digital Radar Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

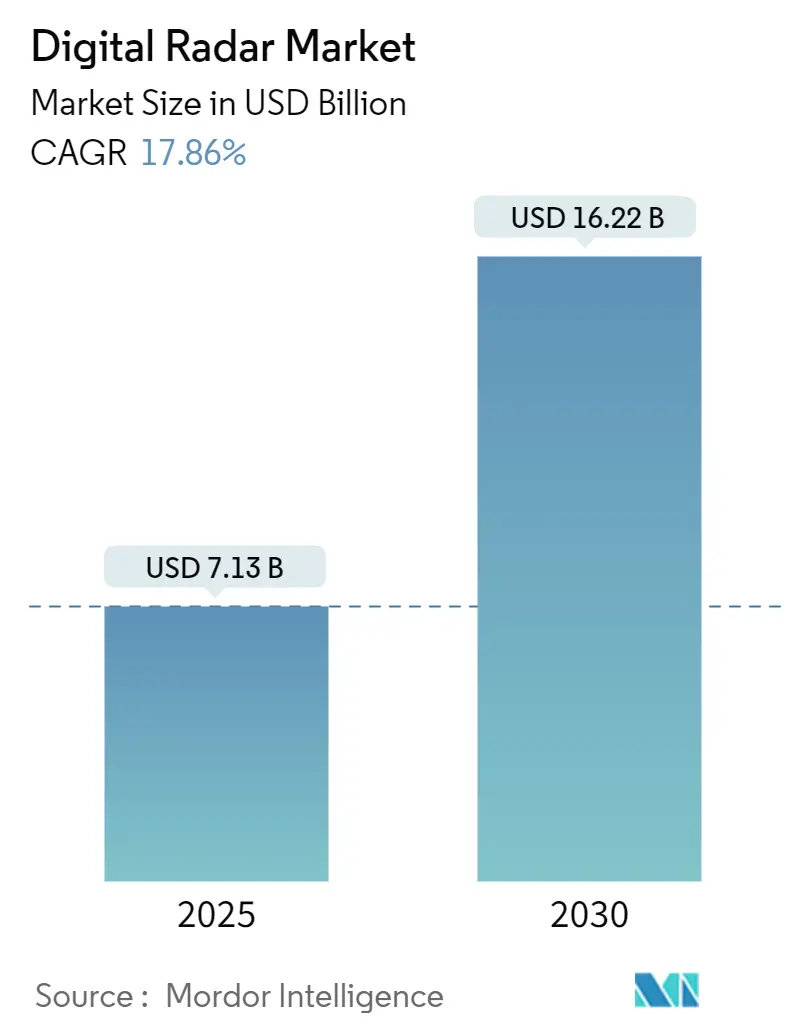

| Market Size (2025) | USD 7.13 Billion |

| Market Size (2030) | USD 16.22 Billion |

| Growth Rate (2025 - 2030) | 17.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Radar Market Analysis by Mordor Intelligence

The Digital Radar market size stands at USD 7.13 billion in 2025 and is forecast to expand to USD 16.22 billion by 2030, translating into a 17.86% CAGR over the period. This acceleration reflects simultaneous regulatory mandates for Advanced Driver Assistance Systems (ADAS), fast-moving semiconductor cost-down cycles, and defense modernization programs that are reshaping procurement priorities. Mandatory automatic emergency braking requirements in the European Union and the United States have pulled radar penetration into mass-market vehicles, while Asia-Pacific’s 76-79 GHz compliance rules are amplifying demand for higher-frequency solutions. In parallel, Texas Instruments, NXP, and other chipmakers have moved millimeter-wave radar power budgets below 1.35 W, unlocking broader platform integration. Defense agencies are sustaining multibillion-dollar contracts for Active Electronically Scanned Array (AESA) retrofits on F-16, F-15, and Eurofighter fleets, creating dual-use technology spillovers into civilian air-traffic control and weather radar. Market risks persist, notably spectrum congestion in the 60-90 GHz bands and supply-chain exposure to gallium nitride export controls, but the underlying growth levers remain strong.

Key Report Takeaways

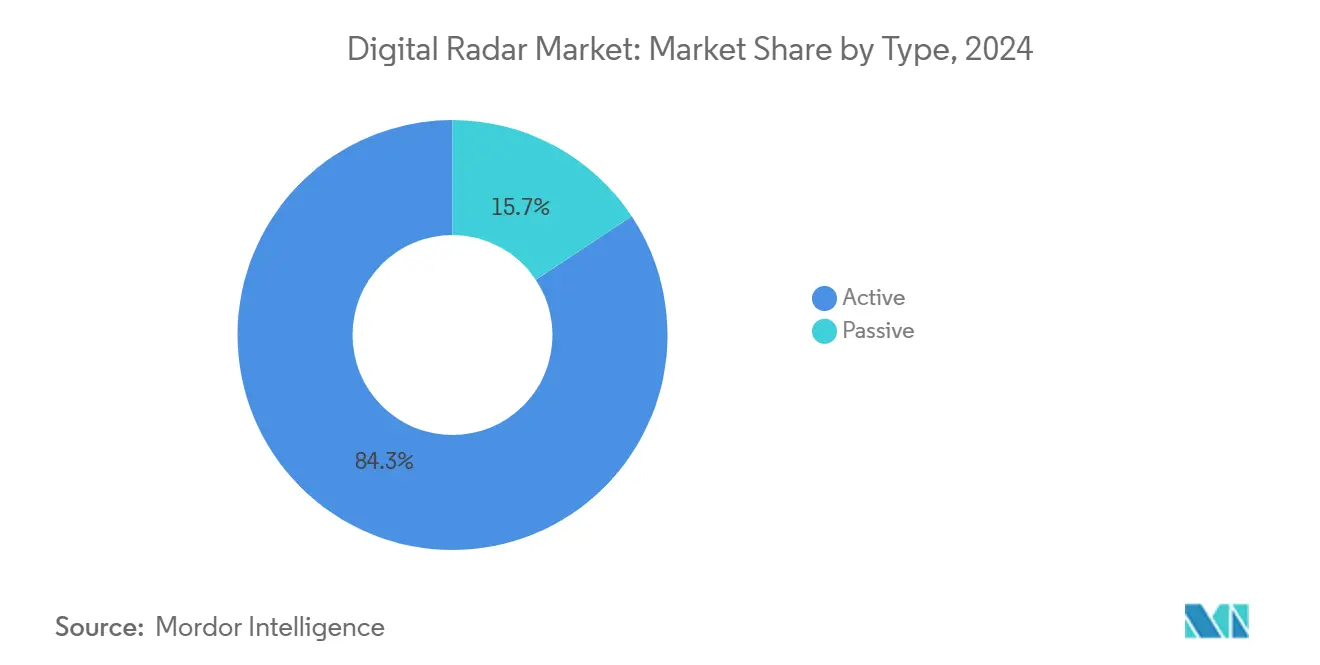

- By type, active systems held 84.32% of the Digital Radar market share in 2024. Passive radar systems are forecast to grow at an 18.86% CAGR through 2030.

- By dimension, 3D radar commanded 54% of the Digital Radar market size in 2024. 4D imaging radar is advancing at a 17.91% CAGR through 2030.

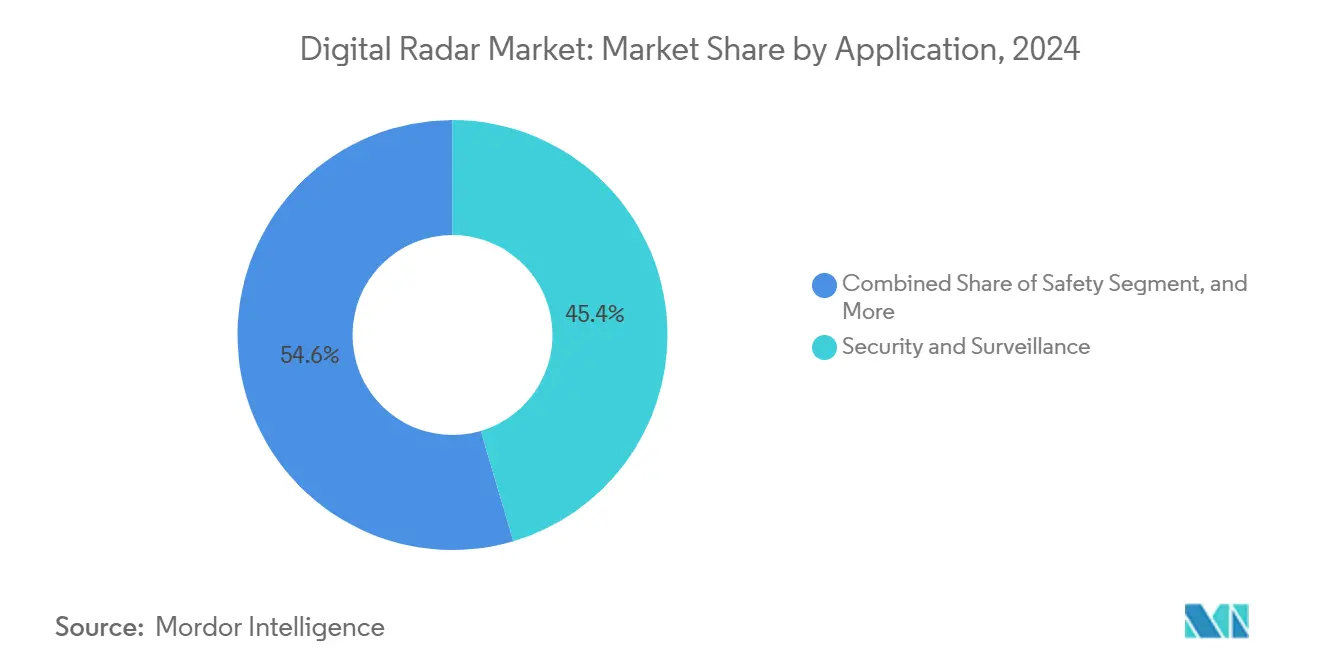

- By application, security and surveillance led with 45.43% revenue share in 2024; safety applications will expand at an 18.66% CAGR to 2030.

- By end user, defense and aerospace captured 57% of the Digital Radar market size in 2024, while automotive is projected to register an 18.83% CAGR between 2025-2030.

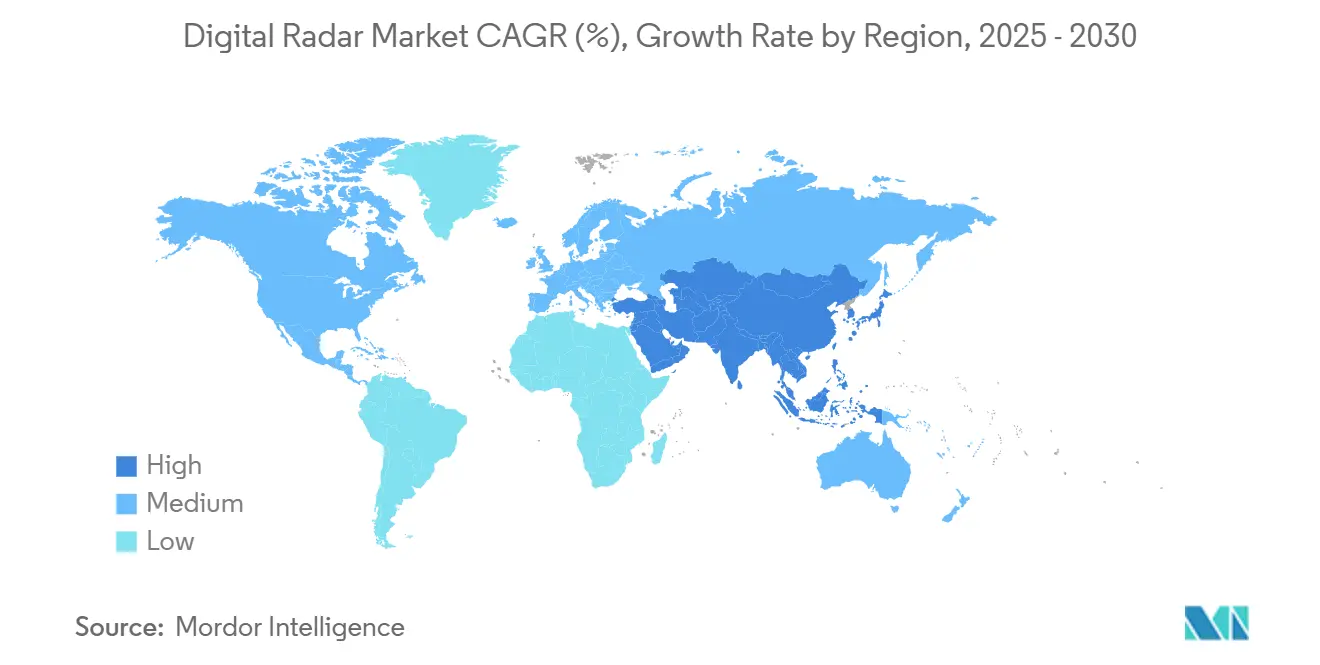

- By geography, North America accounted for 32% of the Digital Radar market share in 2024; Asia-Pacific is set to post a 17.94% CAGR over the forecast period.

Global Digital Radar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for mandatory ADAS radar in new vehicles | +4.2% | Global (early uptake in EU and U.S.) | Short term (≤ 2 years) |

| Miniaturization and cost-down of CMOS mmWave chipsets | +3.8% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| Defense transition from analog to fully digital AESA architectures | +2.9% | North America and Europe | Long term (≥ 4 years) |

| Rise of 4D imaging radar for autonomous mobility | +3.1% | Global premium automotive segments | Medium term (2-4 years) |

| AI-enabled software-defined radar upgrades | +2.4% | Technology-advanced regions | Medium term (2-4 years) |

| Phased-array retrofits for ATC and weather radar | +1.8% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Mandatory ADAS Radar in New Vehicles

Regulations mandating radar-enabled ADAS have compressed timelines for compliance across major automotive markets. The EU General Safety Regulation obliges new models launched after July 2024 to feature autonomous emergency braking, intelligent speed assistance, and driver monitoring, driving minimum radar sensor counts per car above six units on top-selling platforms. In the United States, automatic emergency braking becomes compulsory for most light vehicles by September 2029, with early adoption incentives already influencing procurement cycles. China outlawed legacy 24 GHz radar submissions in 2022, forcing automakers to migrate toward 76-79 GHz solutions that provide larger contiguous bandwidth and higher object-classification accuracy. Collectively these mandates are forecast to prevent thousands of fatalities while embedding radar content across mass-market vehicle tiers.

Miniaturization and Cost-Down of CMOS mmWave Chipsets

Single-chip RF-to-baseband integration has lowered the bill of materials for radar modules, pushing average selling prices close to the USD 1,000 threshold that analysts view as critical for widespread Level 3 autonomy. Texas Instruments’ AWR1x family consumes 1.35 W at 25% duty cycle less than half the power budget of prior two-chip SiGe architectures eliminating heat-sink requirements in many bumper-mount implementations. NXP’s TEF82xx transceiver and S32R41 processor extend channel counts to 48, enabling one-degree azimuth resolution at 370 m range. Low-cost eWLB packaging has simultaneously compressed form factors and fabrication costs, making Digital Radar market adoption economically viable for entry-segment passenger cars while opening pathways for industrial and medical sensing extensions.

Defense Transition from Analog to Fully Digital AESA Architectures

U.S. and allied air forces are replacing mechanically scanned antennas with software-defined AESA arrays that bring electronic beam steering, low probability-of-intercept modes, and integrated electronic-warfare functions. Northrop Grumman’s APG-83 upgrade for the F-16 adds fifth-generation detection fidelity without re-wiring the legacy airframe, underpinning a USD 128.5 million contract executed in 2024. Raytheon’s AN/APG-82 program extends to 2036 on a USD 3.1 billion ceiling, illustrating the durability of digital upgrade cycles. [1]Military & Aerospace Electronics, “Air Force Asks Northrop Grumman to Build 48 AESA Radars,” militaryaerospace.com European partners mirror this trajectory through Typhoon ECRS Mk.2 and SPY-6 maritime deployments, translating into steady Digital Radar market demand for GaN front-ends, thermal management subsystems, and AI-driven signal-processing upgrades.

Rise of 4D Imaging Radar for Autonomous Mobility

Elevating radar into the vertical dimension improves object classification and free-space mapping crucial for Level 4+ autonomy. Arbe Robotics’ ultra-high-resolution sensor yields 2,000-point clouds each frame and collaborates with NVIDIA’s DRIVE AGX platform for AI-based path planning. These systems differentiate overhead obstacles from road-level hazards where legacy 3D radar falters, mitigating false positives that hamper robo-taxi rollout. HiRain’s Chinese OEM production roadmap indicates volume shipments by late-2025, confirming that 4D imaging is transitioning from lab demonstration to mainstream procurement schedules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion in 60-90 GHz bands | -2.8% | Global urban corridors | Short term (≤ 2 years) |

| Export controls on next-gen GaN radar modules | -1.9% | Allied defense markets | Medium term (2-4 years) |

| Skilled-talent gap in MIMO/DSP algorithm design | -1.4% | North America and Europe | Long term (≥ 4 years) |

| Thermal management limits in compact automotive modules | -1.1% | Premium automotive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion in 60-90 GHz Bands

NHTSA studies show that mutual interference among automotive radars can elevate noise floors above target echo power in multi-lane traffic, degrading collision-avoidance reliability. [2]NHTSA, “Radar Congestion Study,” nhtsa.govThe NTIA’s updated 60 GHz guidelines address coexistence with unlicensed communications, yet industry alignment on waveform agility and time-division multiplexing remains incomplete. Without rapid consensus, congestion threatens short-term Digital Radar market credibility, prompting OEMs to experiment with cognitive radio schemes that dynamically adapt center frequencies.

Export Controls on Next-Gen Gallium-Nitride Radar Modules

Beijing’s 2023 gallium export restrictions exposed a supply-chain bottleneck for AESA transmit-receive modules, as China holds roughly 85% of global reserves required for high-power GaN wafers. U.S. and European defense primes have responded by stockpiling strategic materials and funding domestic crystal-growth facilities through a USD 49 billion microelectronics initiative. [3]Sourceability, “Large Investments in Microelectronics,” sourceability.com The resulting cost inflation and elongated lead times weigh on Digital Radar market profitability for military contractors, although alternative materials research is accelerating to offset dependency risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Active Systems Drive Market Leadership

Active architectures captured 84.32% of 2024 revenue, anchored by mandatory forward-looking radar in ADAS packages and multiband AESA arrays in air-defense platforms. Continental and Bosch continue to scale 77 GHz front-end production, leveraging CMOS cost advantages to preserve unit economics. Passive radar, while smaller in absolute terms, posts an 18.86% CAGR as defense agencies deploy covert systems that piggyback civilian broadcast emissions. Leonardo’s passive prototype for air-defense trials underscores rising procurement interest in low-probability-of-intercept solutions that sidestep spectrum allocation battles. Hybrid approaches combining active search with passive track could widen Digital Radar market adoption across border surveillance and maritime patrol by the late-2020s.

Active adoption also benefits from established qualification frameworks that compress validation cycles for automakers navigating 2024–2029 safety deadlines. Passive solutions, in contrast, must overcome integration complexities, including synchronization to external illuminators and sophisticated multistatic processing. Nevertheless, the passive roadmap aligns with electronic-warfare priorities for spectrum stealth, offering suppliers a high-growth niche. As cost curves converge, competitive positioning will pivot on algorithmic sophistication and AI-enabled situational awareness rather than raw RF horsepower, a trend that favors companies with vertically integrated hardware-software stacks.

By Dimension: 3D Dominance with 4D Acceleration

3D radar remains the volume workhorse with 54% share, supplying range, velocity, and azimuth data adequate for current adaptive-cruise and blind-spot functions. Mature test standards and proven ruggedization keep automaker risk appetites low, sustaining robust Digital Radar market size contributions from 3D products. However, 4D imaging sensors are ramping rapidly, taking advantage of falling channel costs to add elevation mapping that rivals LiDAR granularity at a fraction of the bill of materials. Arbe’s 48-Tx/48-Rx array demonstrates one-degree azimuth and two-degree elevation resolution at highway distances, validating the technology for Level 4 design cycles targeting 2027-2028 launches.

The transition is further catalyzed by AI-centric perception stacks that exploit dense 4D point clouds for sensor fusion, enhancing corner-case detection performance in adverse weather where cameras and LiDAR falter. Suppliers integrating proprietary neural-network accelerators into raw radar data pipelines can differentiate as compute-cost curves improve. 2D radar, largely relegated to industrial automation and low-end security, gradually loses relevance as 3D modules reach price parity, leaving 4D to command the innovation narrative for the next decade.

By Application: Security and Surveillance Lead, Safety Accelerates

Security and surveillance generated 45.43% of 2024 sales, fueled by air-defense modernization, border radar grids, and maritime domain awareness programs. Indra’s Lanza 3D deployments for Spanish Air and Space Forces illustrate sustained government budget allocations for early-warning modernization. Safety applications, however, show the steepest growth curve at 18.66% CAGR thanks to expanding ADAS mandates that insert Digital Radar market technologies into every new vehicle platform by 2030. Automakers are upgrading from single-chip corner radars toward multi-sensor clusters that enable cross-traffic assist and highway pilot features, multiplying unit counts per vehicle and broadening supplier bases.

Industrial radar use in robotics and logistics warehouses is emerging but remains below 10% of revenue. Medical sensing—heart-rate and occupancy detection is also embryonic, yet CMOS process migration could drive cost-effective short-range modules by the latter half of the forecast window. Weather monitoring modernization, led by FAA’s NextGen Surveillance and Weather Radar Capability, will add incremental demand but is unlikely to displace the automotive and defense duopoly in the near term.

By End User: Defense Leadership with Automotive Momentum

Defense and aerospace spending delivered 57% of Digital Radar market revenue in 2024, anchored by multiyear AESA upgrade contracts and distributed aperture radar programs for space situational awareness. The U.S. Army’s WiSPR program typifies emerging requirements for counter-APS ground surveillance that mandate wideband digital agility. Meanwhile, automotive OEMs and Tier-1 suppliers are closing the gap via double-digit growth rates. Cost compression and 4D imaging capabilities position radar to complement or, in some configurations, displace LiDAR in Level 3+ architectures, underpinning the segment’s 18.83% CAGR forecast.

Industrial automation, smart-city infrastructure, and healthcare monitoring round out the end-user mix, each leveraging Digital Radar market advances in chip integration and software-defined signal processing. Pilot deployments of traffic-management radars for city intersections and indoor people-tracking modules for elder-care facilities illustrate pathways for non-traditional adopters, but scale will depend on continued progress in miniaturization and regulatory spectrum harmonization.

Geography Analysis

North America retained 32% of 2024 revenue, propelled by defense expenditure and early ADAS legislation. The U.S. microelectronics drive directs USD 49 billion toward domestic semiconductor fabrication, fortifying supply chains for next-generation radar modules. FAA radar modernization and Arctic over-the-horizon research partnerships with Canada further sustain procurement momentum.

Asia-Pacific is on track for the fastest growth at 17.94% CAGR. China’s 76-79 GHz enforcement and multibillion-dollar silicon-foundry expansions are scaling local demand, while Japanese and South Korean OEMs integrate 4D radar into premium vehicle lines. Defense modernization across India and ASEAN adds long-range surveillance and coastal security contracts, reinforcing the Digital Radar market trajectory. Supply-chain localization efforts, however, must navigate export-control headwinds and skilled-labor shortages in millimeter-wave design.

Europe maintains steady performance, buoyed by the General Safety Regulation and Eurofighter radar upgrades. Industrial initiatives such as Indra’s expansion of one of Europe’s largest radar factories underscore supply-side resilience. Middle East and Africa and South America remain nascent but post rising tender volumes for border surveillance and critical-infrastructure protection, leveraging competitive procurement frameworks to import mature radar technologies.

Competitive Landscape

The Digital Radar market demonstrates moderate fragmentation: a handful of defense primes dominate classified programs while a diverse mix of Tier-1s, fabless chipmakers, and startups contend for automotive and civilian share. Raytheon, Lockheed Martin, and Northrop Grumman leverage scale, classified IP, and program-of-record incumbency to retain margins in military segments. Continental, Bosch, and Denso, by contrast, compete on cost and design-win velocity as automakers ramp ADAS volumes.

Semiconductor vendors NXP, Texas Instruments, and Infineon differentiate through RF-to-digital integration roadmaps, while Arbe Robotics, Uhnder, and smartmicro pioneer 4D imaging resolution and AI-native radar cubes. Recent consolidation—Anduril’s acquisition of Numerica’s Spyglass radar and indie Semiconductor’s purchase of Silicon Radar signals a tilt toward vertically integrated sensing-plus-software stacks. Competitive factors increasingly revolve around algorithmic IP, thermal management breakthroughs, and spectrum-sharing finesse rather than raw RF metrics.

Strategic moves illustrate this shift. RTX’s flight-tested cognitive radar warning receiver cuts threat-identification latency to near-zero for F-16 fleets, showcasing AI acceleration at the edge. Lockheed Martin’s AI-driven maritime SAR system auto-classifies vessels in real time, highlighting value creation via software updates rather than hardware refreshes. The race to deliver cognitive, software-defined functionality will likely intensify merger activity and licensing deals as suppliers vie for share in an expanding yet technologically demanding marketplace.

Digital Radar Industry Leaders

Lockheed Martin Corporation

Raytheon Technologies Corporation

Northrop Grumman Corporation

Thales Group

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Australia and Canada signed a cooperation pact on over-the-horizon radar R&D, leveraging JORN expertise for Arctic coverage.

- July 2025: Lockheed Martin unveiled AI-powered SAR technology for maritime surveillance with automated vessel classification.

- February 2025: Raytheon completed flight testing of the Cognitive Algorithm Deployment System, the first AI/ML-powered radar warning receiver for fourth-generation aircraft.

- January 2025: Arbe Robotics teamed with NVIDIA to integrate ultra-high-definition perception radar into the DRIVE AGX platform.

Global Digital Radar Market Report Scope

| Active |

| Passive |

| 2D |

| 3D |

| 4D |

| Security and Surveillance |

| Safety |

| Other Applications |

| Automotive |

| Defense and Aerospace |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | ||

| By Type | Active | ||

| Passive | |||

| By Dimension | 2D | ||

| 3D | |||

| 4D | |||

| By Application | Security and Surveillance | ||

| Safety | |||

| Other Applications | |||

| By End User | Automotive | ||

| Defense and Aerospace | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | |||

Key Questions Answered in the Report

How large is the Digital Radar market in 2025 and how fast is it growing?

The market is valued at USD 7.13 billion in 2025 and is on track for a 17.86% CAGR through 2030.

Which region is expanding the fastest for digital radar deployments?

Asia-Pacific is registering a 17.94% CAGR, propelled by Chinese 76-79 GHz mandates and large-scale semiconductor investments.

What technology trend is reshaping automotive radar design?

4D imaging radar adds elevation data to conventional 3D outputs, supporting higher-level autonomy while keeping sensor costs under USD 1,000 per vehicle.

Who leads defense radar modernization contracts today?

Northrop Grumman, Raytheon, and Lockheed Martin dominate with multibillion-dollar AESA upgrades for F-16, F-15, and maritime platforms.

What is the biggest short-term risk facing automotive radar suppliers?

Spectrum congestion in the 60-90 GHz bands threatens interference that can degrade collision-avoidance performance in dense traffic corridors.

How will export controls influence military radar production?

Gallium restrictions add cost and lead-time pressure on GaN-based AESA modules, driving defense primes to diversify material sourcing and invest in domestic wafer capacity.

Page last updated on: