Airborne Surveillance Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

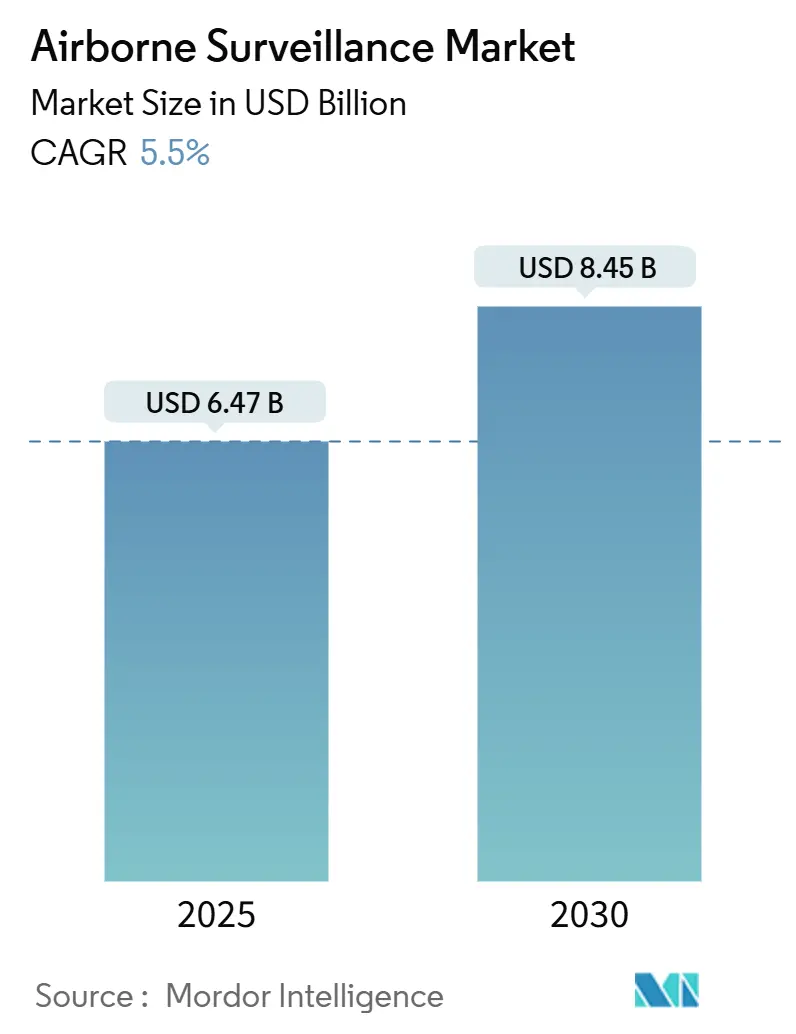

| Market Size (2025) | USD 6.47 Billion |

| Market Size (2030) | USD 8.45 Billion |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

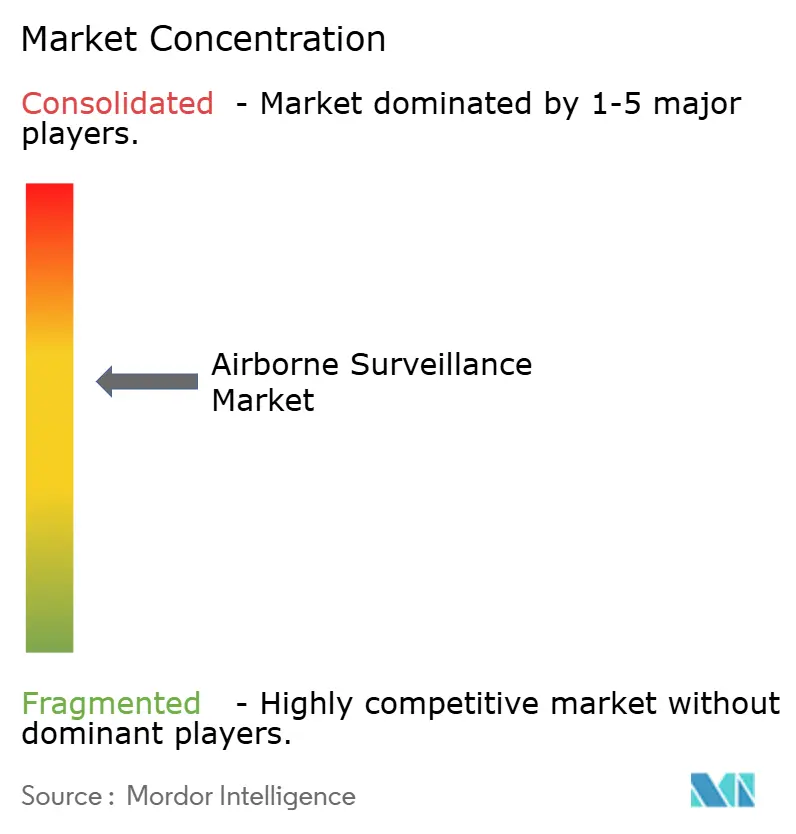

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airborne Surveillance Market Analysis by Mordor Intelligence

The airborne surveillance market size reached USD 6.47 billion in 2025 and is projected to climb to USD 8.45 billion by 2030, reflecting a 5.5% CAGR. Sovereign defense priorities, escalating border tensions, and the convergence of artificial intelligence with multi-sensor payloads anchor the current expansion of the airborne surveillance market. Defense ministries lengthen procurement pipelines for high-altitude, long-endurance platforms to shift from reactive patrols to predictive monitoring architectures, while commercial operators adopt smaller, autonomous systems to meet safety, environmental, and disaster-response mandates. The airborne surveillance market is also shaped by competitive investments in edge computing that compress decision cycles from hours to minutes, thereby broadening mission sets without commensurate crew growth. Simultaneously, modular open-systems architectures enable users to refresh sensors through software upgrades rather than costly airframe overhauls, preserving platform relevance over two-decade life cycles. Heightened collaboration between industry and regulators hastens certification of unmanned flights beyond visual line of sight, removing historical deployment bottlenecks for non-military stakeholders.

Key Report Takeaways

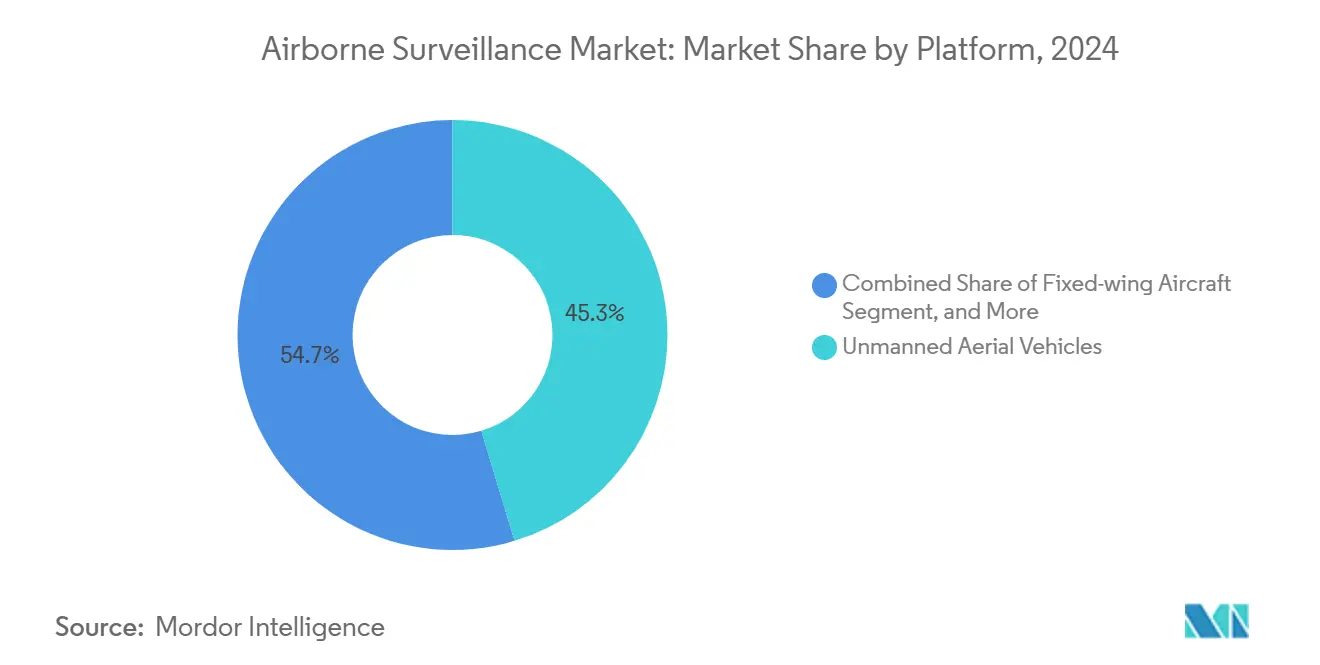

- By platform, unmanned aerial vehicles led with 45.34% of airborne surveillance market share in 2024; fixed-wing VTOL UAVs are advancing at a 6.82% CAGR through 2030.

- By component, sensors and payloads commanded 39.12% share of the airborne surveillance market size in 2024, while software and data processing is projected to expand at a 6.67% CAGR between 2025-2030.

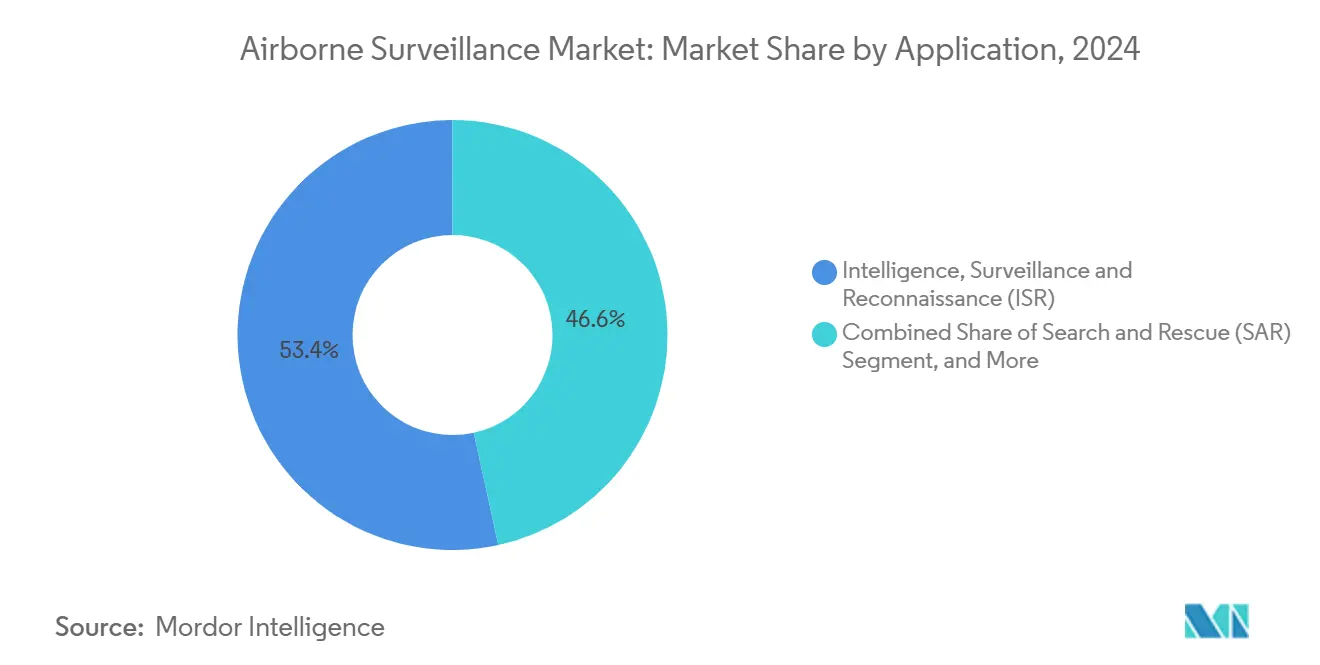

- By application, intelligence, surveillance and reconnaissance accounted for 53.41% of the airborne surveillance market size in 2024 and is advancing at a 5.50% CAGR through 2030; environmental monitoring represents the fastest-growing use case at a 6.13% CAGR.

- By end user, defense held 62.89% share of the airborne surveillance market size in 2024, whereas commercial and civil deployments are forecast to grow at a 7.49% CAGR to 2030.

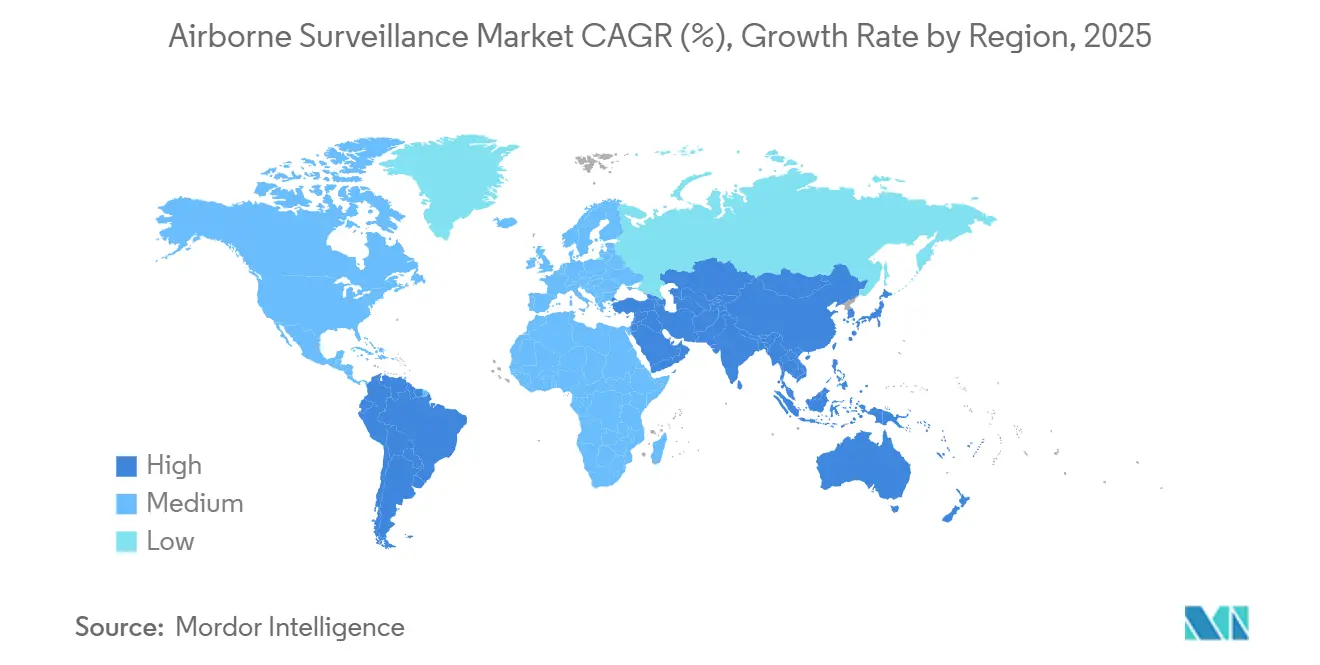

- By geography, North America captured 36.87% airborne surveillance market share in 2024; Asia-Pacific is expected to post the quickest regional uptick at a 5.91% CAGR through 2030.

Global Airborne Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense expenditure on ISR capabilities | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of UAV platforms for real-time intelligence | +0.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Advancements in AI-enabled multi-sensor data fusion | +1.1% | North America and EU core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Escalating border and maritime security threats | +0.9% | Global, heightened in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Emergence of high-altitude pseudo-satellite (HAPS) vehicles | +0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Stratospheric solar-powered drones for persistent coverage | +0.5% | Global, with early deployment in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Expenditure on ISR Capabilities

Defense ministries earmark a larger slice of budgets for intelligence, surveillance, and reconnaissance programs as information dominance eclipses platform mass as a war-fighting determinant. India’s USD 1.5 billion I-STAR project illustrates how emerging powers now favor sensor-rich aircraft that integrate directly with strike networks, narrowing response gaps exposed during the 2019 air engagements. [1]NDTV, “Air Force To Get Rs 10,000 Crore Indigenous I-STAR Spy Planes,” ndtv.com Similar patterns unfold in Southeast Asia, where mid-tier nations such as Malaysia increase defense budgets at an 8.4% clip to procure persistent monitoring assets. Multirole surveillance fleets also serve humanitarian and border-security roles, strengthening political support for high-ticket acquisitions. Because ISR airframes link seamlessly into existing command structures, armed forces can enhance situational awareness without recasting their organizational doctrine. The resulting demand reinforces a positive feedback loop that steers R&D toward lighter, software-defined payloads able to mature within the typical five-year budget cycle.

Rapid Adoption of UAV Platforms for Real-Time Intelligence

Unmanned aerial vehicles compress the sensor-to-decision timeline by streaming data continuously without risking aircrew lives. The U.S. Coast Guard’s V-BAT deployment underscores how runway-independent designs offer 105-minute endurance and automatic tracking, attributes that manned helicopters cannot economically replicate. [2]U.S. Coast Guard, “Cutter-Based Unmanned Aircraft System Capability,” dcms.uscg.mil AI-enabled optical sensors like ViDAR integrated on the VXE30 Stalker further reduce operator workload by autonomously flagging anomalies. Regulatory agencies hasten blanket approvals for beyond-visual-line-of-sight operations, prompting civilian utilities, pipeline operators, and insurance firms to adopt UAV-based monitoring. Overall cost savings of 30-40% versus rotary-wing sorties expand the addressable user base, particularly among state and local agencies with finite aviation budgets. As swarm logic matures, multi-drone operations will scale area coverage exponentially, embedding the airborne surveillance market deeper into routine public-safety workflows.

Advancements in AI-Enabled Multi-Sensor Data Fusion

Artificial intelligence shifts airborne systems from data collectors to autonomous sense-and-act nodes. General Atomics’ Agile Condor pod delivers 7.5 teraflops of onboard processing that executes object-recognition models during flight, obviating high-latency satellite relays. [3]General Atomics, “High-Powered Computing at the Edge with Agile Condor Pod,” ga.com SRC’s high-performance embedded computing packages condense what once required ground stations into modular airborne cards, preserving bandwidth for critical command traffic. Fusion algorithms synthesize electro-optical, infrared, synthetic-aperture radar, and signals intelligence feeds into a coherent operational picture, boosting target identification probability while filtering false positives. Edge processing also shrinks data footprints by 90%, keeping contested networks uncluttered during electronic-warfare scenarios. Together, these advances empower a new generation of cooperative autonomy in which platforms decide the optimal sensor mix for each task without waiting for ground-based cueing.

Escalating Border and Maritime Security Threats

Transnational crime, illegal fishing, and grey-zone naval maneuvers lift demand for persistent off-shore and border surveillance. China’s SS-UAV mothership concept, capable of launching swarms far from mainland airfields, signals how positional awareness is becoming central to maritime strategy. The Pentagon’s USD 4.2 billion aerostat initiative responds by placing radar-laden balloons above key border stretches for continuous wide-area coverage. Lengthy frontiers such as the 1,954-mile U.S.–Mexico border cannot be patrolled humanly without prohibitive flight hours; autonomous systems bridge this gap by staying aloft for days. Naval chokepoints like the Red Sea illustrate how surveillance shortfalls leave commercial shipping vulnerable to low-cost strikes, spurring governments to accelerate drone-based early-warning grids. As border incidents often unfold in austere zones, low-maintenance unmanned platforms become the only feasible solution for long-haul vigilance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle costs | -0.7% | Global, particularly constraining in emerging markets | Medium term (2-4 years) |

| Stringent and fragmented air-space regulations | -0.4% | Global, with varying intensity by region | Short term (≤ 2 years) |

| Data-link spectrum congestion and cyber vulnerabilities | -0.3% | Global, heightened in dense electromagnetic environments | Medium term (2-4 years) |

| ESG-driven capital constraints on defense suppliers | -0.2% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Costs

Complex airborne sensors, hardened datalinks, and mission-system integration push procurement budgets beyond the reach of some emerging economies. Lockheed Martin’s USD 71 billion revenue in 2024 underscores how marquee contractors command premium pricing for turnkey fleets. Supply-chain turbulence inflated component costs by 15-20% in 2024-2025, stretching lead times for processors and radar chips. Lifecycle expenses—maintenance, mid-life avionics refresh, and crew training—often triple the initial outlay over two decades, as evidenced by India’s Netra AWACS program exceeding USD 1.4 billion before reaching full operational capability. These economics compel budget-constrained buyers to prioritize multi-mission utility, lease services, or pursue staged capability insertions to smooth cash demands.

Stringent and Fragmented Air-Space Regulations

Civil aviation authorities proceed cautiously when integrating unmanned aircraft into crowded skies. The Federal Aviation Administration still restricts fully autonomous flights over populated zones without waivers, slowing commercial scale-up. Within Europe, divergent national policies hamper cross-border missions; operators must navigate unique clearance processes for each jurisdiction, extending planning cycles. Incidents such as the Texas rescue helicopter collision with a hobby drone highlight safety stakes and trigger temporary no-fly orders that can suspend legitimate surveillance operations. Compliance with cybersecurity frameworks from agencies such as CISA further prolongs certification, particularly for small enterprises lacking robust governance teams. The upshot is a patchwork regulatory environment that introduces deployment risk premiums into project budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: UAV Dominance Reshapes Surveillance Architecture

Unmanned platforms captured 45.34% of airborne surveillance market share in 2024, confirming a transition toward endurance-oriented, pilotless fleets. Rotary-wing and fixed-wing manned aircraft remain indispensable for missions that demand heavy payloads or passenger carriage, yet their higher operating costs curb extended use. Fixed-wing VTOL UAVs, advancing at a 6.82% CAGR, blend runway independence with long-leg efficiency, widening their appeal for shipborne and urban deployments. Aerostats deliver cost-effective, stationary coverage for border belts, but they suffer limitations in adverse weather and hostile action, nudging agencies toward powered craft for contested zones. High-altitude pseudo-satellites and solar-powered stratospheric drones now in testing could displace some geostationary satellite functions by offering continuous, lower-latency imaging at a fraction of orbital launch prices.

Operational doctrine is shifting accordingly. Military planners design layered surveillance grids in which long-endurance UAVs furnish maritime overwatch, manned turboprops conduct datum confirmation, and micro-drones perform last-mile reconnaissance. Commercial operators exploit the same stack for power-line inspection and disaster assessment, scaling from balloon-borne radios to quadcopters as circumstances dictate. The airborne surveillance market therefore gravitates toward open-architecture airframes capable of accepting mission kits across weight classes, ensuring that single procurement lines support multiple risk environments and regulatory regimes.

By Component: Software Processing Drives Next-Generation Capabilities

Hardware still commands 39.12% of spend, yet the strongest value-creation now lies in code. Software and data processing is growing at a 6.67% CAGR, boosted by algorithmic upgrades that unlock new mission profiles without airframe tweaks. Airborne early-warning radars continue to form the backbone of national air-defense nets, but artificial intelligence now filters radar clutter in real time, exposing low-observable intrusions that slipped past earlier generations. Command and control suites stitch together disparate sensor feeds, while secure communications maintain near-zero-latency links with ground commanders.

Modularity shortens technology refresh intervals; users can install containerized microservices aboard legacy aircraft, steering capability cycles toward biennial patches rather than once-a-decade retrofit programs. Vendors reinforce this shift by offering subscription-based analytics packages, turning capital-heavy procurement into scalable operating expenses. Because software doubles as a cyber-attack surface, air-worthiness authorities impose stringent verification and validation protocols, which in turn spur demand for digital-twin models that rehearse patches before field rollouts.

By Application: Environmental Monitoring Emerges as Growth Driver

Intelligence, surveillance and reconnaissance accounted for 53.41% of the airborne surveillance market size in 2024, anchored by defense and homeland-security taskings. Nonetheless, environmental monitoring is advancing at a 6.13% CAGR as regulators mandate independent verification of emissions, fisheries, and wildfire risks. Autonomous platforms carrying hyperspectral sensors help agencies capture pollutant plumes, while drone-mounted LiDAR maps post-storm infrastructure damage within hours. Dual-use flexibility allows defense fleets to pivot to humanitarian missions, improving asset utilization and political palatability.

Search-and-rescue, border patrol, and disaster management weave into this tapestry. Each benefit from persistent, high-resolution imaging streamed to command posts or directly to first-responders’ handhelds. Commercial operators finding value in these multi-mission payloads unlock private-sector revenue streams that cushion defense spending cycles, broadening the airborne surveillance market beyond its traditional military nucleus.

By End User: Commercial Uptake Accelerates

Defense establishments still own 62.89% of contracts, but commercial and civil customers post the liveliest 7.49% CAGR. Annualized cost savings, data-ownership incentives, and growing corporate responsibility agendas propel adoption across energy, insurance, and logistics verticals. Homeland security agencies bridge the gap, procuring dual-use drones that patrol ports by day and assist storm-relief by night. As insurance underwriters insist on granular catastrophe imagery before settling claims, utilities and municipalities lease flight hours rather than acquire fleets, spawning an “ISR-as-a-service” sub-segment that expands airborne surveillance market penetration.

Public-private partnerships smooth procurement by pooling maintenance and training functions, reducing overhead for small agencies. Meanwhile, regulations evolve to permit higher payloads and longer ranges once deemed military-only, providing impetus for manufacturers to tailor airframes to non-combat tasks without forfeiting ruggedness.

Geography Analysis

North America retained 36.87% airborne surveillance market share in 2024 on the strength of mature supply chains, stable defense budgets, and permissive innovation ecosystems. Programs such as the USD 4.2 billion aerostat network exemplify the region’s preference for persistent, wide-area coverage solutions. The United States supplements aerostats with UAV fleets, evidenced by the USD 198 million V-BAT contract that integrates vertical-takeoff assets into maritime patrol bases. Canada advances complementary surveillance through coastal domain awareness initiatives, while Mexico collaborates on shared sensor corridors along the southern border.

Asia-Pacific is the fastest climber, recording a 5.91% CAGR through 2030. Japan elevated defense allocations by USD 59 billion to bolster early-warning capabilities, and China’s SS-UAV mothership prototypes illustrate indigenous ambitions to project surveillance beyond territorial waters. India’s purchase of 12 AWACS and a trio of I-STAR aircraft enlarges airborne coverage over mountainous frontiers, highlighting how regional redundancies emerge to deter peer competitors. Australia and South Korea amplify demand via joint-development pacts that secure technology transfer while meeting interoperability goals.

Europe posts steadier gains underpinned by collective procurement frameworks and NATO modernization drives. France’s acquisition of Sweden’s GlobalEye underscores cross-border cooperation on command-and-control standards, while Airbus’s A321MPA program replaces aging Atlantique-2 fleets with sensor-dense jets aligned with future unmanned partners. Continental initiatives such as the Eurodrone set the stage for unified doctrines, even as individual states pursue niche capabilities tailored to Arctic, Mediterranean, or Baltic theaters. Elsewhere, Gulf states and North African nations prioritize coastal radar aerostats and MALE drones to secure shipping lanes, whereas South American air forces focus on forest-fire monitoring and narcotics interception, often leveraging surplus Western systems rebundled with new mission electronics.

Competitive Landscape

Market concentration remains moderate, with legacy aerospace integrators controlling most high-value defense contracts while agile entrants seize commercial niches. Lockheed Martin, Northrop Grumman, and Airbus leverage proven manufacturing ecosystems and export financing to defend incumbency, but face agile challengers such as Shield AI offering autonomous software layers interoperable with multiple airframes. Established vendors respond by partnering with AI specialists, as shown by Saab collaborating with Helsing to embed machine-learning code within the Arexis sensor suite.

Strategic plays emphasize vertical integration of data-processing stacks; players acquiring cloud-analytics firms can market end-to-end solutions rather than hardware alone. Patent filings on swarm intelligence and hybrid aerial-underwater vehicles hint at future ruptures in competitive order, where platform versatility outweighs mass production. Meanwhile, component suppliers invest in radiation-hardened processors and secure datalink chipsets to align with zero-trust architectures, embedding themselves deeper into value chains.

Commercial growth creates room for service-centric models where operators lease sensor time, emulating satellite remote-sensing subscriptions. This shift pressures pure-hardware vendors to diversify into analytics, maintenance, and pilot-training subsidiaries, smoothing revenue across procurement troughs. Overall, rivalry intensifies around software upgradability and total-cost-of-ownership metrics rather than speed or ceiling alone, reshaping differentiation across the airborne surveillance market.

Airborne Surveillance Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Northrop Grumman Corporation

Airbus SE

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Airbus rolled out Spain’s first C295 Maritime Surveillance Aircraft under the EUR 1.695 billion program, enhancing Europe’s sovereign maritime coverage.

- July 2025: Airbus Defence and Space won France’s A321MPA contract to replace Atlantique 2s, integrating Thales sensors for anti-submarine warfare.

- June 2025: France ordered four GlobalEye aircraft from Saab to modernize airborne early-warning capabilities, reinforcing Franco-Swedish defense ties.

- June 2025: India approved USD 1.5 billion for three indigenous I-STAR spy planes to bolster precision-strike intelligence.

Global Airborne Surveillance Market Report Scope

| Fixed-wing Aircraft |

| Rotary-wing Aircraft |

| Unmanned Aerial Vehicles (UAV) |

| Aerostats |

| High-Altitude Pseudo-Satellites (HAPS) |

| Sensors and Payloads |

| Airborne Early-Warning Radars |

| Communication Systems |

| Command and Control Systems |

| Software and Data Processing |

| Intelligence, Surveillance and Reconnaissance (ISR) |

| Search and Rescue (SAR) |

| Border and Coastal Patrol |

| Disaster Management |

| Environmental Monitoring |

| Defense |

| Homeland Security |

| Commercial and Civil |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Platform | Fixed-wing Aircraft | ||

| Rotary-wing Aircraft | |||

| Unmanned Aerial Vehicles (UAV) | |||

| Aerostats | |||

| High-Altitude Pseudo-Satellites (HAPS) | |||

| By Component | Sensors and Payloads | ||

| Airborne Early-Warning Radars | |||

| Communication Systems | |||

| Command and Control Systems | |||

| Software and Data Processing | |||

| By Application | Intelligence, Surveillance and Reconnaissance (ISR) | ||

| Search and Rescue (SAR) | |||

| Border and Coastal Patrol | |||

| Disaster Management | |||

| Environmental Monitoring | |||

| By End User | Defense | ||

| Homeland Security | |||

| Commercial and Civil | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the airborne surveillance market in 2025?

It stands at USD 6.47 billion, with momentum toward USD 8.45 billion by 2030.

Which platform type leads current procurement?

UAVs head the field with 45.34% share, reflecting their cost-efficient persistence.

What region exhibits the highest growth rate?

Asia-Pacific shows the fastest rise, advancing at a 5.91% CAGR through 2030.

Which application area grows quickest outside defense?

Environmental monitoring leads civilian uptake at a 6.13% CAGR.

How are costs influencing acquisition decisions?

High lifecycle expenses prompt buyers to favor modular upgrades and service-leasing models over outright ownership.

Which technology shift most reshapes capability?

AI-driven multi-sensor fusion shortens the intelligence cycle, allowing in-flight threat classification without reliance on ground nodes.

Page last updated on: