Radar Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.06 Billion |

| Market Size (2031) | USD 49.44 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

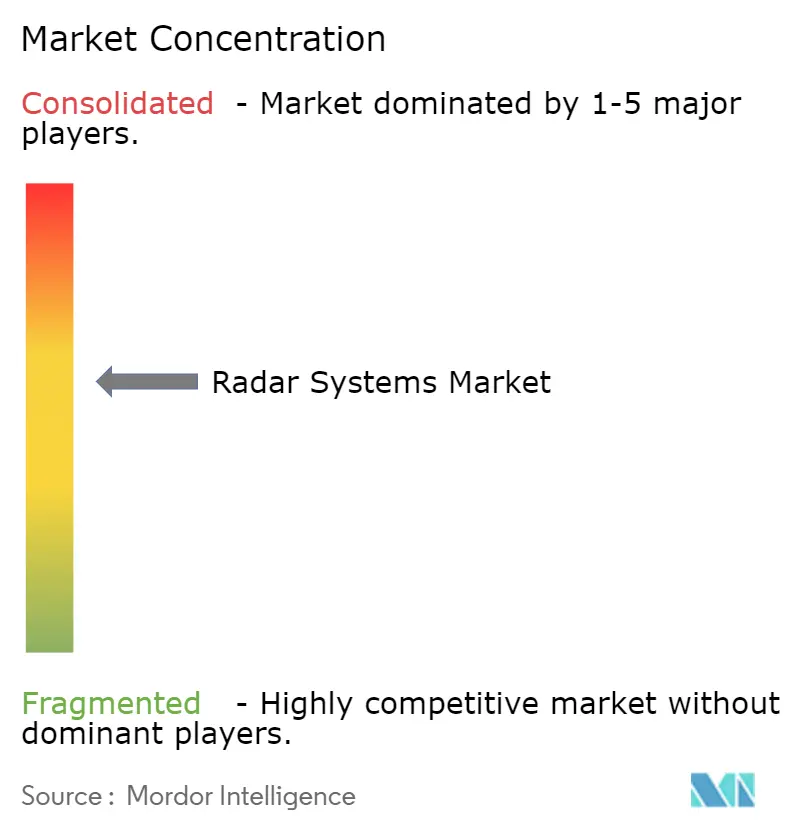

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radar Systems Market Analysis by Mordor Intelligence

The radar systems market size is expected to grow from USD 36.12 billion in 2025 to USD 38.06 billion in 2026 and is forecast to reach USD 49.44 billion by 2031 at 5.38% CAGR over 2026-2031. Current expansion is powered by steady defense funding, rapid automotive advanced driver-assistance adoption, and broad air-traffic control modernization programs. Military demand for long-range air and missile defense sensors, combined with the shift toward 4D imaging radar in vehicles and phased-array weather radars, is widening the radar systems market addressable base.[1]Federal Aviation Administration, “Facility Replacement and Risk Mitigation Program,” faa.gov Continuous wave architectures benefit from millimeter-wave upgrades in the 77-81 GHz band, while AI-enabled digital beamforming and software-defined designs accelerate performance cycles. Supply-chain risk for gallium nitride remains a near-term concern but is spurring second-source strategies and long-term material science investment.

Key Report Takeaways

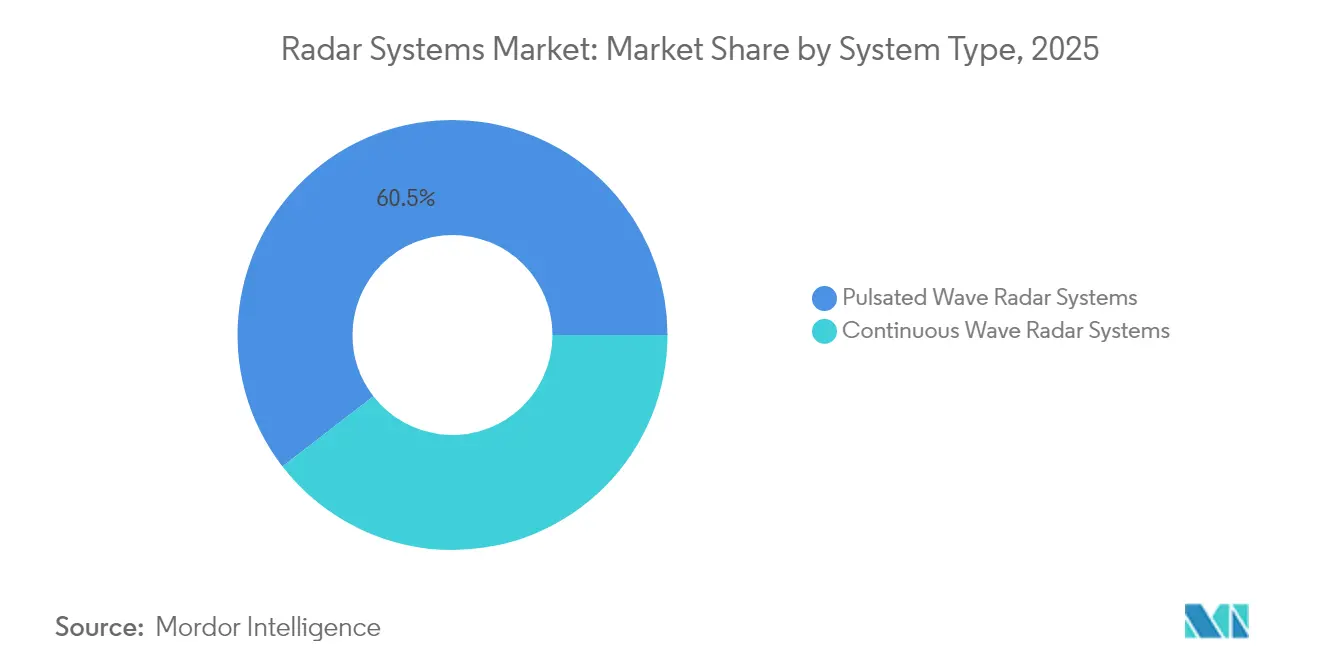

- By system type, pulsated wave systems led with 60.48% of radar systems market share in 2025, while continuous wave architectures posted the fastest 5.74% CAGR through 2031.

- By frequency, C-X band held 38.11% share of the radar systems market size in 2025, and millimeter-wave bands above 40 GHz are projected to expand at a 5.86% CAGR 2031.

- By component, antenna modules accounted for 32.35% of the radar systems market size in 2025; software and services represent the fastest-growing segment at 5.89% CAGR 2031.

- By end user, military and defense dominated with 57.12% radar systems market share in 2025; the automotive sector is forecast to advance at a 5.97% CAGR 2031 .

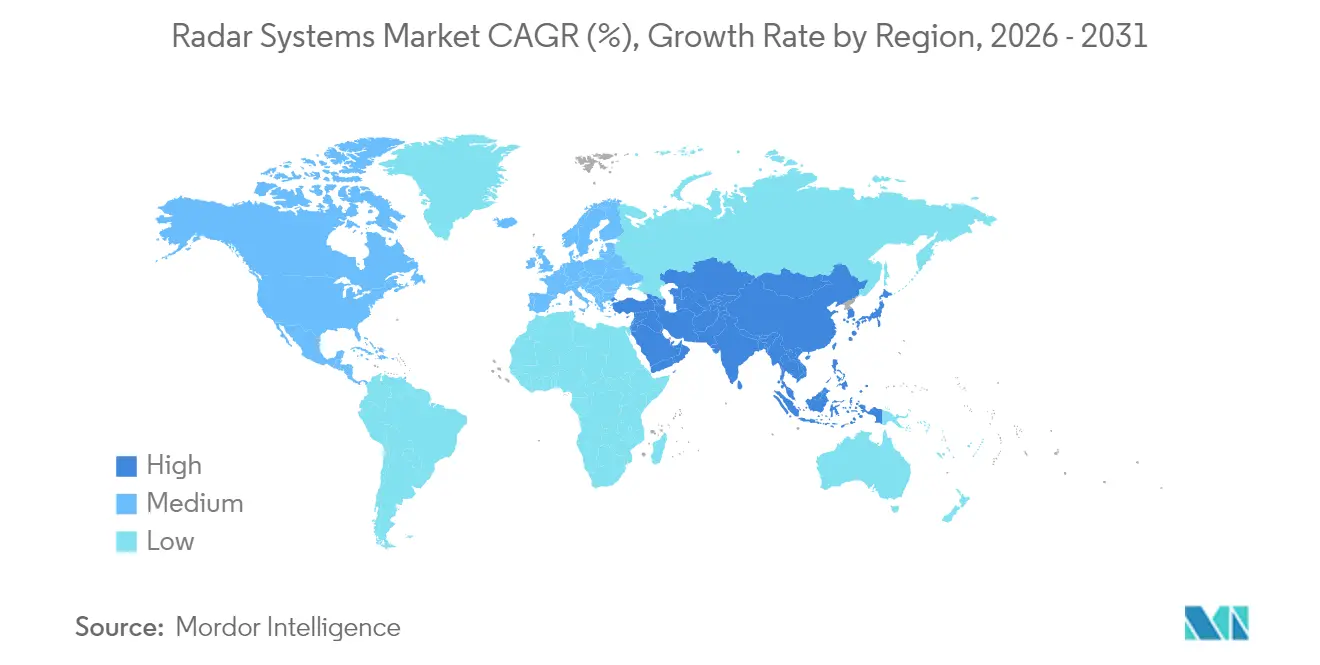

- By geography, north america led with 36.94% revenue share in 2025; asia pacific is projected to expand at a 6.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radar Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global defense budgets | +1.8% | Global, led by North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Rapid adoption of automotive ADAS radar | +1.5% | Global, strongest in North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Air-traffic control modernization programmes | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Increasing demand for advanced weather surveillance | +0.9% | North America, Asia Pacific | Medium term (2-4 years) |

| Miniaturized radar for small-UAV integration | +0.7% | North America, Europe | Short term (≤ 2 years) |

| AI-enabled digital beamforming-based radars | +0.6% | North America, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Defense Budgets

Defense ministries continue to channel funding toward next-generation sensors. The United States Department of Defense allocated USD 1.7 billion for the Lower Tier Air and Missile Defense Sensor and USD 537 million for ongoing AN/SPY-6 production in fiscal-year 2025. Similar momentum is visible in Europe, where Latvia and Slovenia ordered HENSOLDT TRML-4D systems worth EUR 100 million (USD 109 million) to reinforce integrated air defense. Asia Pacific defense investment is accelerating through Hanwha Systems’ AESA radar contracts for the KF-21 fighter and L-SAM II missile battery. Multilateral frameworks, such as NATO standardization agreements, ease cross-border technology flow and support volume procurement efficiencies.

Rapid Adoption of Automotive ADAS Radar

Automotive manufacturers are extending radar nodes from adaptive cruise control to full 360-degree perception. Arbe Robotics and NVIDIA cooperated on a 4D imaging radar that maps elevation and velocity for Level-3 autonomy requirements.[2]Arbe Robotics, “4D Imaging Radar Technology,” arberobotics.com NXP Semiconductors partnered with Bitsensing to raise resolution and reduce latency for safety functions across multiple vehicle classes. Regulatory push adds urgency: European rules mandate advanced emergency braking in all new cars, and the U.S. National Highway Traffic Safety Administration promulgated similar proposals. Transition to the 77-81 GHz band provides higher range resolution and smaller antenna footprints, enabling mass-market deployment.

Air-Traffic Control Modernization Programmes

The Federal Aviation Administration’s USD 8 billion Facility Replacement and Risk Mitigation initiative will swap 618 aging radars for solid-state systems with improved reliability and weather penetration. Europe’s Single European Sky program prioritizes digital radar integration and networked sensing, fostering interoperable solutions among air navigation service providers. The International Civil Aviation Organization’s Global Air Navigation Plan harmonizes performance baselines, encouraging suppliers to design globally certifiable platforms. Software-defined architectures allow future algorithm upgrades without hardware change, aligning with growing air-traffic volumes.

Increasing Demand for Advanced Weather Surveillance

National Weather Service completion of its USD 150 million NEXRAD upgrade in 2024 demonstrated dual-polarization benefits for precipitation discrimination. China has fielded more than 50 X-band phased-array radars, indicating global adoption of higher-frequency weather surveillance. AI algorithms fused with radar outputs improve severe-storm forecasting, creating new revenue for data analytics. Technology vendors now offer service contracts bundling hardware, cloud processing, and predictive insights, strengthening recurring-revenue models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront acquisition and lifecycle costs | −1.1% | Emerging markets worldwide | Long term (≥ 4 years) |

| Radio-frequency spectrum congestion and allocation barriers | −0.8% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Supply-chain concentration for gallium nitride devices | −0.5% | Global | Short term (≤ 2 years) |

| Skills gap in advanced RF engineering | −0.4% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Acquisition and Lifecycle Costs

Premium AESA radars strain budgets. Egypt’s order for a single AN/TPS-78 installation reached USD 304 million, and the Ivory Coast’s GM200 radar cost EUR 50 million (USD 54.5 million). Beyond procurement, gallium nitride module maintenance and specialized calibration prolong the total cost of ownership. Mercury Systems is targeting an 80% reduction in radar assembly size, weight, and power under a USD 8.5 million Department of Defense contract, illustrating industry moves to compress lifecycle expense

Radio-Frequency Spectrum Congestion and Allocation Barriers

Expanding 5G deployments overlap radar bands, threatening interference. The U.S. National Spectrum Strategy notes conflicts in 24 GHz and 28 GHz allocations, pushing automotive and weather radar operators to refine waveforms.[3]MITRE Corporation, “Spectrum Management and Modernization,” mitre.org Regulatory negotiations consume resources and delay rollout. Dynamic spectrum sharing solutions exist but demand cognitive radar upgrades, adding complexity and capital expenditure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Continuous Wave Systems Gain Momentum

The pulsated wave category accounted for 60.48% of radar systems market share in 2025, supported by long-range missile defense radars such as AN/SPY-6 and TPY-2. Pulsated wave technology continues to anchor strategic early-warning missions due to its superior peak power and range-gate discrimination. Continuous wave designs, however, are forecast to register a 5.74% CAGR, reflecting their suitability for automotive ADAS, small UAV sense-and-avoid, and compact maritime safety installations. 4D imaging radar solutions from Arbe Robotics capitalize on frequency-modulated continuous wave modulation to deliver precise elevation data, promoting adoption across Level-3 autonomy programs.

Continuous wave radars reduce size, weight, and power, easing integration in space-constrained platforms. Leonardo’s Osprey family demonstrates low-SWaP performance for unmanned aerial vehicles. Regulatory allocation in the 77-81 GHz band favors continuous wave automotive sensors, reinforcing volume production economics. Over the next five years, the radar systems market size revenue split between the two architectures is expected to narrow as automotive, drone, and infrastructure deployments outpace traditional defense spending.

By Component: Software and Services Lead Growth

Antenna modules anchored 32.35% of the overall revenue in 2025, propelled by gallium nitride transmit-receive modules enabling simultaneous multi-mission operations. As phased-array density climbs, antenna tiles integrate control, calibration, and health-monitoring sensors, boosting subsystem value. Transmit-receive and power amplifier modules transition from gallium arsenide to gallium nitride for higher thermal margins, while mixed-signal RFIC integration shrinks board count.

Software and services will rise at 5.89% CAGR through 2031, buoyed by AI-driven threat classification, radar-data analytics, and cloud-hosted post-processing. AI frameworks such as RTX Corporation’s Cognitive Aircraft Defense System demonstrate real-time electromagnetic environment learning. As procurement migrates to capability-as-a-service models, vendors secure recurring revenue through algorithm updates and cybersecurity patches. Regulatory compliance, including FCC certification and ISO-9001 quality audits, stimulates demand for professional services, accelerating ecosystem monetization.

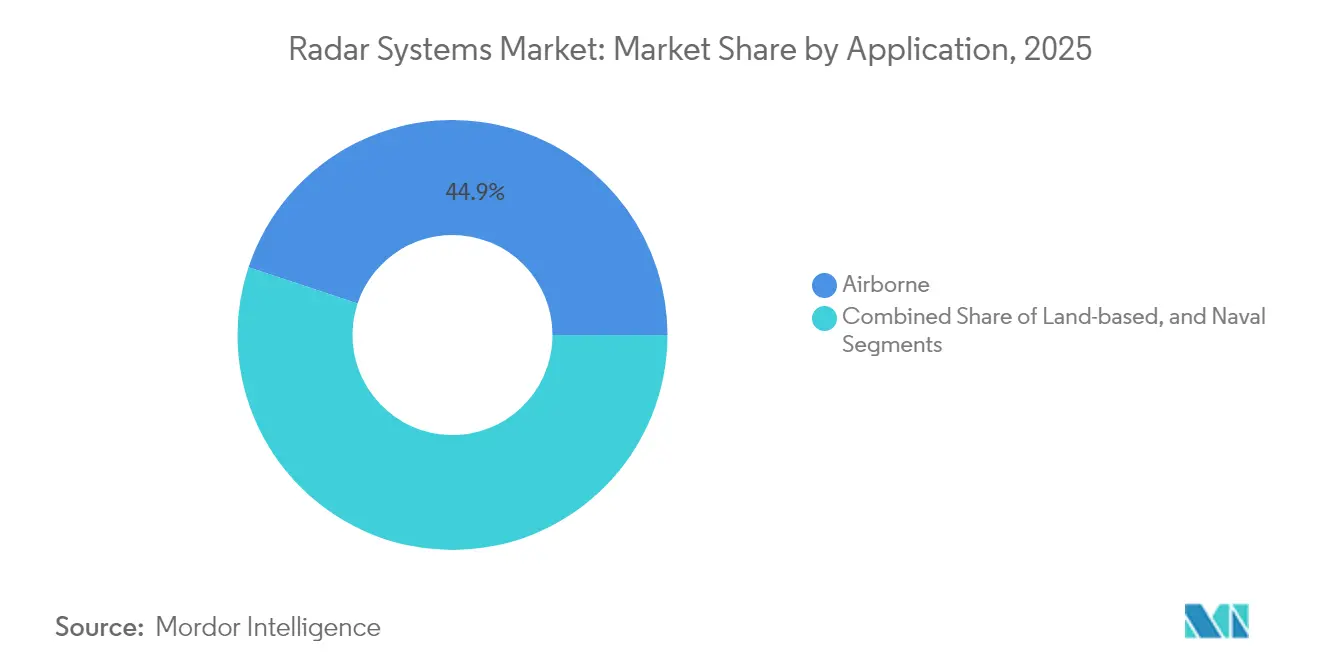

By Application: Land-Based Systems Show Promise

Airborne platforms claimed 44.89% revenue share in 2025, reflecting active combat aircraft upgrades and commercial aviation fleet expansion. Fighter programs integrate AESA radars that merge air-to-air, air-to-ground, and electronic warfare modes into a single aperture. Naval demand persists via destroyer and frigate modernization schedules featuring modular SPY-6 variants.

Land-based sensors are poised for a 5.63% CAGR, propelled by counter-battery missions, border surveillance, and emergent counter-drone requirements. Ukraine’s deployment of TRML-4D radars illustrates multirole land-based utility, tracking 1,500 targets across 250 kilometers. Ground-based weather radars enjoy stable civil funding, while vehicle-to-infrastructure radar nodes gain momentum in intelligent transportation pilots.

By End-User Industry: Automotive Sector Drives Innovation

Military and defense retained 57.12 of % radar systems market share in 2025, sustained by the multi-domain operations doctrine that stresses joint-force sensor fusion. Naval, ground, and space-based radar investments converge under integrated air and missile defense architectures. Aviation organizations, both military and civil, recapitalize surveillance and weather radars to meet capacity demands

The automotive community is on track for a 5.97% CAGR, the highest among end users, driven by mandated automatic emergency braking and lane-keeping systems. OEMs are evolving from single-function corner radars to centralized 4D imaging arrays linked via high-speed in-vehicle networks. Standardization bodies such as ISO and SAE establish performance metrics that guide mass-manufacturing economies of scale, pushing cost per sensor downward and fueling broader adoption across economy-class models.

Geography Analysis

North America held 36.94% of 2025 revenue, underpinned by the United States Department of Defense’s USD 849.8 billion fiscal-year 2025 allocation and the FAA’s USD 8 billion radar replacement program. Canada advances NORAD upgrades, while Mexico invests in air-traffic management and coastal surveillance. Automotive adoption grows in tandem with U.S. and Canadian EV manufacturing, supporting sensor demand.

Asia Pacific is the fastest-growing region at 6.09% CAGR. China fielded more than 50 X-band phased-array weather radars and invests in maritime surveillance for the South China Sea CIIS. South Korea’s Hanwha Systems supplies AESA units to the KF-21 and L-SAM II, and Japan accelerates fighter radar upgrades. Automotive radar deployment accelerates on domestic electric and autonomous vehicle platforms, supported by regulatory clarity in the 77-81 GHz band.

Europe sees steady uptake, anchored by NATO commitments and Single European Sky modernization. Latvia and Slovenia ordered EUR 100 million (USD 109 million) of TRML-4D units, while Leonardo’s ECRS Mk2 completed its first Typhoon flight. Thales GM400α radars bolster Baltic defense. Advanced driver-assistance mandates in Germany, France, and Italy accelerate automotive radar penetration, reinforcing cross-segment demand.

Regulatory Landscape

Radar systems face a mix of spectrum-allocation rules, equipment authorization requirements, and defense export controls that vary by geography but increasingly converge on harmonized bands and tighter security assurance. At the global level, the ITU Radio Regulations update that entered into force on 1 January 2025 (reflecting outcomes agreed at WRC-23) provides the baseline framework national administrations use when assigning bands for aviation surveillance, weather radar, and automotive short-range radar.

In key commercialization corridors, compliance is shaped by regional standards and approval workflows. In Europe, ETSI technical standards underpin radio equipment compliance under the EU Radio Equipment Directive (Directive 2014/53/EU), affecting automotive and short-range radar devices placed on the market. In the United States, FCC equipment authorization remains a gating step for radar-related radio devices, and a final rule effective 15 June 2026 introduced a fast-track priority review pathway for devices tested under Pre-Approval Guidance in trusted test laboratories, changing how vendors plan certification timelines and test-lab sourcing. In India, the Department of Telecommunications issued G.S.R. 468(E) in June 2026 to de-license the 77-81 GHz band for short-range automotive radar systems, reducing licensing friction for OEMs and Tier-1 suppliers building ADAS radar platforms around this band.

Value Chain Analysis

The radar systems value chain spans upstream RF materials and semiconductors (notably gallium nitride devices), midstream module and subsystem production (T/R modules, antenna arrays, power supplies, signal processors), and downstream integration into end platforms such as air and missile defense, air-traffic surveillance, weather networks, and automotive ADAS. A key constraint sits upstream in the compound semiconductor stack, where dependence on refined gallium supply and limited GaN capacity concentrates risk around T/R module availability, which then propagates into array build schedules and final radar deliveries.

In response, primes and subsystem suppliers are restructuring procurement and industrial partnerships to secure critical components and localize production where possible. HENSOLDT signed a long-term agreement with United Monolithic Semiconductors in March 2026 to secure 900,000 GaN semiconductor components through 2030, while Lockheed Martin formalized a Japan-based supply chain element in February 2026 via a purchase order with Fujitsu for a SPY-7 radar antenna subarray suite power supply unit. Downstream, regional co-development and production arrangements are also expanding the chain, including the April 2026 MoU involving EDGE, Indra, and SIATT for next-generation radar development and production in Brazil. Government-led programs can accelerate late-stage adoption and sustainment demand as well, illustrated by Canada signing agreements with Australia in June 2026 to acquire Arctic over-the-horizon radar technology and move that program into a delivery-oriented phase, affecting integrators, test, and field support providers.

Competitive Landscape

The radar systems market exhibits moderate concentration: incumbents Lockheed Martin, RTX Corporation, and Thales Group leverage decades of frequency-domain IP and established program performance records to win marquee contracts. Consolidation intensifies as Anduril acquired Numerica’s radar business in June 2024, augmenting its autonomous defense stack, while Voyager Technologies purchased ElectroMagnetic Systems Inc. in August 2025 for space-based analytics capacity.

Startups focus on niche opportunities such as counter-drone detection, distributed aperture configurations, and low-cost imaging. Zendar’s distributed aperture architecture demonstrates high-resolution automotive radar without large antennas.[4]Zendar, “Distributed Aperture Radar,” zendar.io Academic breakthroughs, such as DGIST’s algorithm that doubles FMCW resolution, stimulate software-only performance leaps. Competitive differentiation centers on AI integration, software upgradeability, and lifecycle service models. Spectrum policy and International Traffic in Arms Regulations remain critical to market entry, affecting non-U.S. vendor reach.

Radar Systems Industry Leaders

Leonardo S.p.A.

General Dynamics Corporation

NXP Semiconductors N.V.

BAE Systems plc

Airbus Defense and Space, Inc. (Airbus SE)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Defense and civil infrastructure recapitalization programs are creating near-term whitespace for capacity expansion, modernization kits, and services tied to higher-volume production and sustainment. In air and missile defense, RTX stated in June 2026 that it invested USD 100 million in Portsmouth, Rhode Island to expand LTAMDS testing and Patriot GEM-T subcomponent production, and Raytheon also received a USD 515 million U.S. Navy award for SPY-6 radar family support and upgrades for Flight IIA destroyers. These steps broaden opportunities for radar test automation, calibration, spares, and software-driven upgrades across installed fleets as platforms move toward software-defined architectures and recurring sustainment packages.

Civil aviation and mass-market automotive are also opening lanes for differentiated offerings beyond traditional long-range defense radars. For air-traffic control, Collins Aerospace invested USD 26.5 million in May 2026 to expand radar production in Florida supporting the FAA Radar System Replacement Program (including Condor Mk3 and ASR-XM), reinforcing demand for solid-state primary surveillance radar, site modernization, and lifecycle service contracts. In compact and distributed radar, Echodyne opened an 86,350-square-foot manufacturing facility in Washington State in July 2026 after a USD 40 million investment to support capacity for up to 30,000 MESA radars annually, pointing to pull from counter-UAS and perimeter security deployments that favor low-SWaP sensors and faster fielding. For automotive, productization of cost-focused radar silicon in June 2026, including NXP introducing the SAF8444 radar SoC, supports opportunities in one-chip corner radar designs and higher-volume 77-81 GHz implementations where certification, EMC testing, and functional-safety-aligned software tooling become differentiators.

Recent Industry Developments

- July 2026: Echodyne opened a new 86,350-square-foot radar manufacturing facility in Washington State backed by a USD 40 million investment, scaling capacity to as many as 30,000 MESA radars per year. The added footprint supports higher-volume delivery for counter-UAS and perimeter surveillance programs where low-SWaP radars are procured in large quantities. It also increases competitive pressure on suppliers of compact radars by pairing production scale with faster lead times.

- June 2026: NXP Semiconductors launched the SAF8444 automotive radar system-on-chip aimed at front and corner radar designs for cost-sensitive ADAS implementations. The product supports the one-chip radar architecture trend that reduces BOM complexity and helps OEMs expand radar placement across vehicle trims. It also strengthens the supplier ecosystem for 77-81 GHz sensors that are migrating toward software-defined vehicle platforms.

- December 2025: Leonardo received an award from Italian TELEDIFE to develop and deliver the first four Italian next-generation long-range ballistic defense radars using digital AESA GaN technology. The program signals continued procurement momentum for high-end, long-range sensors and reinforces the industry shift toward GaN-based arrays for higher power density and multi-mission capability. It also supports follow-on opportunities in training, sustainment, and upgrade cycles for national integrated air and missile defense architectures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from radar systems sold for detection, tracking, navigation, and surveillance across defense and civil uses, including the core hardware and the supporting software and services that make the system operational.

Scope exclusions: Non-radar sensing-only solutions and generic communications equipment that does not perform radar functions are excluded.

Segmentation Overview

- By System Type

- Continuous Wave Radar Systems

- Pulsated Wave Radar Systems

- By Component

- Antenna Modules

- Transmit-Receive Modules

- Power Amplifiers and Oscillators

- Signal Processors and Controllers

- Software and Services

- By Application

- Airborne

- Land-based

- Naval

- By End-user Industry

- Aviation

- Maritime Applications

- Automotive

- Military and Defense

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand map and set realistic constraints before running the market model. We relied on public sources such as defense budget documents, procurement and contract award portals, and air traffic management publications, because these typically indicate where radar upgrades are planned and where replacements are due.

We also used sources from aviation and maritime regulators, spectrum and telecommunications authorities (for frequency allocations), and customs and trade statistics for selected radar-related categories. Peer-reviewed journals on radar hardware trends, including GaN power devices and digital beamforming, helped inform how system capabilities and component mix are evolving. Company annual reports, investor presentations, and reputable press releases were used to confirm product-mix shifts between airborne, naval, and land-based applications. To stitch company coverage and capture deal signals faster, we used paid subscriptions for company financials and intelligence, patents, and defense-related contract tracking. These examples are not exhaustive, and other public sources were reviewed for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys focused on radar system suppliers, component specialists, integrators, and informed buyers across defense, aviation, maritime, and automotive use cases. The discussions were used to confirm how programs convert into deliveries, how average selling prices move with technology shifts, and where upgrade cycles are accelerating or being delayed across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 26% | EMEA: 32% |

| Smaller Players: 19% | Managers: 58% | Americas: 27% |

Market-Sizing & Forecasting

The sizing model starts from a top-down build where defense procurement signals, civil aviation surveillance upgrades, and platform fleet trends are converted into an addressable demand pool for radar installations and replacements. After establishing the baseline, we corroborate results with selective bottom-up approximations, such as sampled program volumes multiplied by typical system ASP ranges and a roll-up of publicly visible supplier revenue exposure, before adjusting final totals.

To keep the model grounded, we track inputs such as radar shipments tied to aircraft and naval retrofit cycles, modernization and replacement timelines, adoption of AESA and software-defined architectures, mix shifts across continuous wave versus pulsed approaches, and pricing effects of key components like transmit-receive modules and signal processors. Where direct volume data is thin, we use proxy indicators, including contract values, delivery schedules, and observed platform commissioning patterns, which are then checked during follow-up calls.

For forecasting, scenario analysis is used so timing risk from programs, budget changes, and civil infrastructure funding cycles is reflected in the outlook. Growth assumptions are aligned to expert consensus on variables such as defense allocations, airport and coastal surveillance projects, and technology penetration, and they are revisited during validation.

Data Validation & Update Cycle

Validation is done through multiple checks so results do not drift away from real demand signals. We compare model outputs against independent metrics such as procurement pipelines, fleet modernization cadence, and regional spending patterns, then investigate any large variances by revisiting assumptions behind volumes, pricing, and delivery timing.

Before sign-off, the model and its drivers go through step-by-step analyst reviews. When anomalies appear, we run deeper source checks and selectively re-contact interviewees. Reports are refreshed annually, with interim updates when material events occur, including major program awards, policy shifts, or supply constraints. Before delivery, a fresh pass is completed so the final view reflects the latest available data.

Mordor Intelligence's Radar Systems Market Size Versus Other Published Estimates

Published market sizes for radar systems can differ even when the market name sounds the same, because the counted components, the selected base year, and the treatment of service revenue are not always consistent. Differences can also come from whether an estimate relies more on announced programs versus waiting for delivery evidence to show up as measurable demand.

The main gap is whether software and services are counted only when tied to a delivered radar system, and this is where Mordor Intelligence keeps the scope aligned to system-level revenue rather than folding in adjacent, non-radar electronics spend. Variance is also driven by base year choices, assumptions on how ASPs rise with AESA and digital beamforming adoption, and how currency conversion timing is applied when aggregating multi-region defense and civil demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 36.12 B (2025) | |

| Global Consultancy A | USD 36.04 B (2024) | Uses a 2024 base year and a 2024 to 2031 forecast window, which can shift the near-term number when program deliveries are lumpy. The published view also provides limited clarity on how software and service revenue is attached to radar system sales versus broader electronics spend. |

| Industry Research House B | USD 36.12 B (2024) | Anchors the market at 2024 and carries the trajectory to 2032, which changes the implied ramp timing for modernization cycles. The scope is presented with broad segmentation, but the public summary does not clearly explain how components and platform retrofits are converted into annual system revenue. |

The spread in the table is mainly explained by year selection and by how closely each estimate ties service and software value to actual radar system deliveries. By keeping the model traceable to procurement, fleet, and upgrade indicators, the final number stays practical to review and repeat when new contracts, delivery schedules, or technology mix shifts become visible.

Key Questions Answered in the Report

What is the current value of the radar systems market?

The radar systems market size stood at USD 38.06 billion in 2026 and is projected to reach USD 49.44 billion by 2031.

Which radar type is expanding fastest?

Continuous wave architectures are forecast to grow at a 5.74% CAGR through 2031, fueled by automotive and UAV deployment.

Why are millimeter-wave bands important for radar?

Frequencies above 40 GHz enable compact antennas and high-resolution detection, making them essential for 4D imaging automotive sensors.

Which region leads radar demand growth?

Asia Pacific records the highest growth trajectory at a 6.09% CAGR, driven by defense modernization and autonomous vehicle production.

How are software-defined radars impacting the market?

Software-defined designs allow capability upgrades via code, boosting recurring revenue from services and accelerating innovation cycles.

What challenges limit wider radar deployment?

High upfront acquisition costs and spectrum congestion remain the primary restraints, particularly in emerging markets and crowded frequency bands.

Page last updated on: