Synthetic Aperture Radar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.86 Billion |

| Market Size (2031) | USD 9.78 Billion |

| Growth Rate (2026 - 2031) | 10.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Aperture Radar Market Analysis by Mordor Intelligence

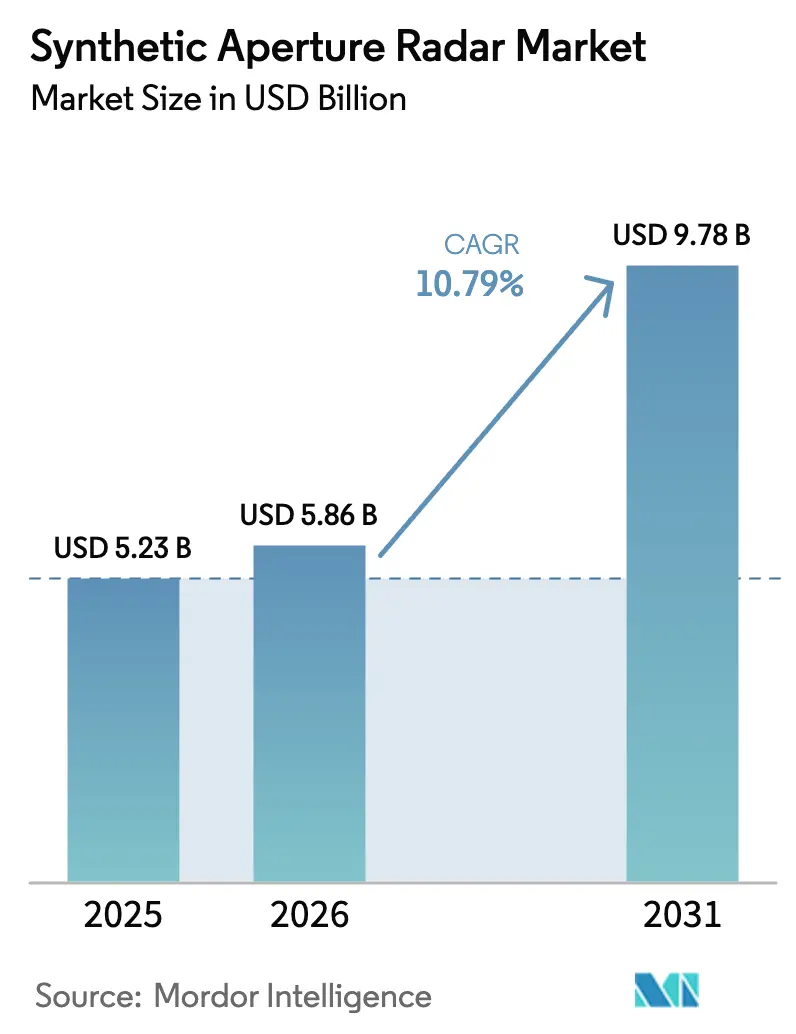

The Synthetic Aperture Radar Market size is projected to expand from USD 5.23 billion in 2025 and USD 5.86 billion in 2026 to USD 9.78 billion by 2031, registering a CAGR of 10.79% between 2026 to 2031.

This growth reflects an industry pivot toward proliferated small-satellite constellations that compress revisit times to less than one day and push commercial image resolution toward 16 centimeters. Defense ministries in Europe and North America are reallocating procurement budgets from bespoke platforms to subscription-based data feeds, while commercial customers adopt SAR data for infrastructure integrity, maritime domain awareness, and disaster response. Competitive pressure is intensifying as new-space operators adopt cloud-native delivery models, and spectrum congestion in X-band and C-band is nudging the industry toward Ka-band architectures. Government carbon-monitoring mandates in Europe and North America add another durable growth vector by institutionalizing the use of interferometric techniques for surface-deformation tracking.

Key Report Takeaways

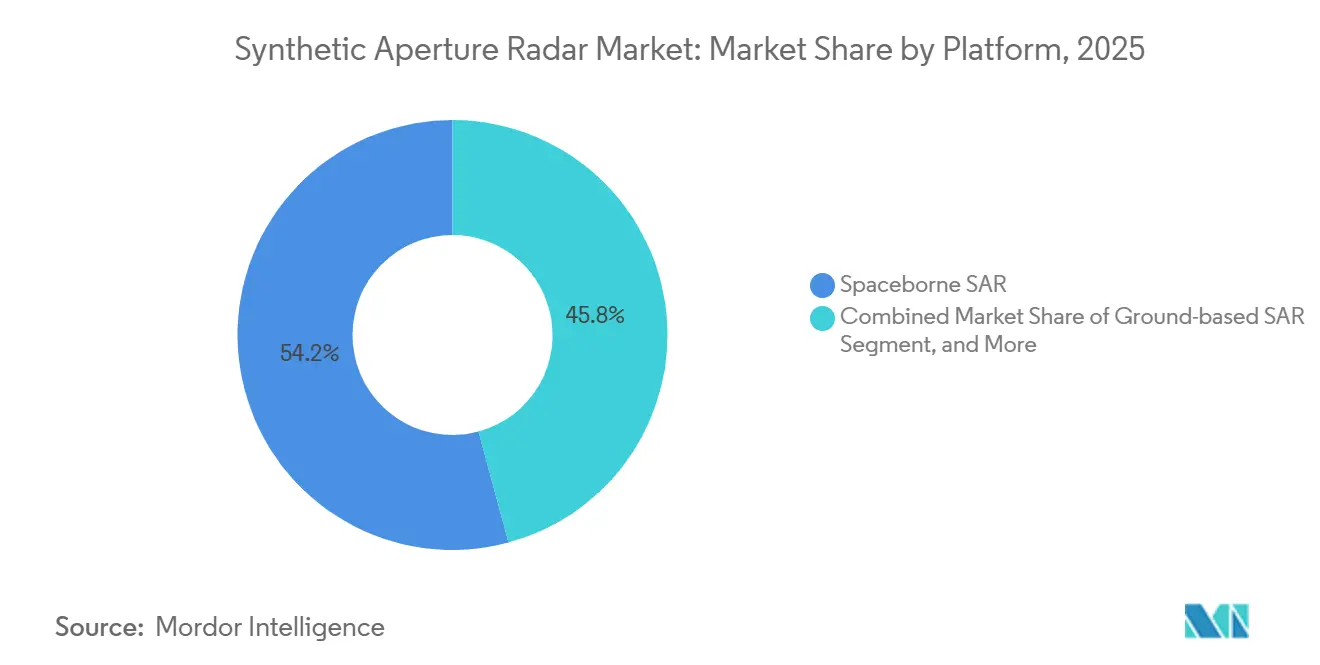

- By platform, spaceborne systems led with 54.19% revenue share in 2025; maritime-based systems are projected to expand at an 11.29% CAGR through 2031.

- By frequency band, X-band commanded 35.28% revenue share in 2025; Ka-band is forecast to grow at an 11.16% CAGR to 2031.

- By component, antennas held 27.16% share of the synthetic aperture radar market size in 2025, while data processor and software is expected to advance at a 12.01% CAGR through 2031.

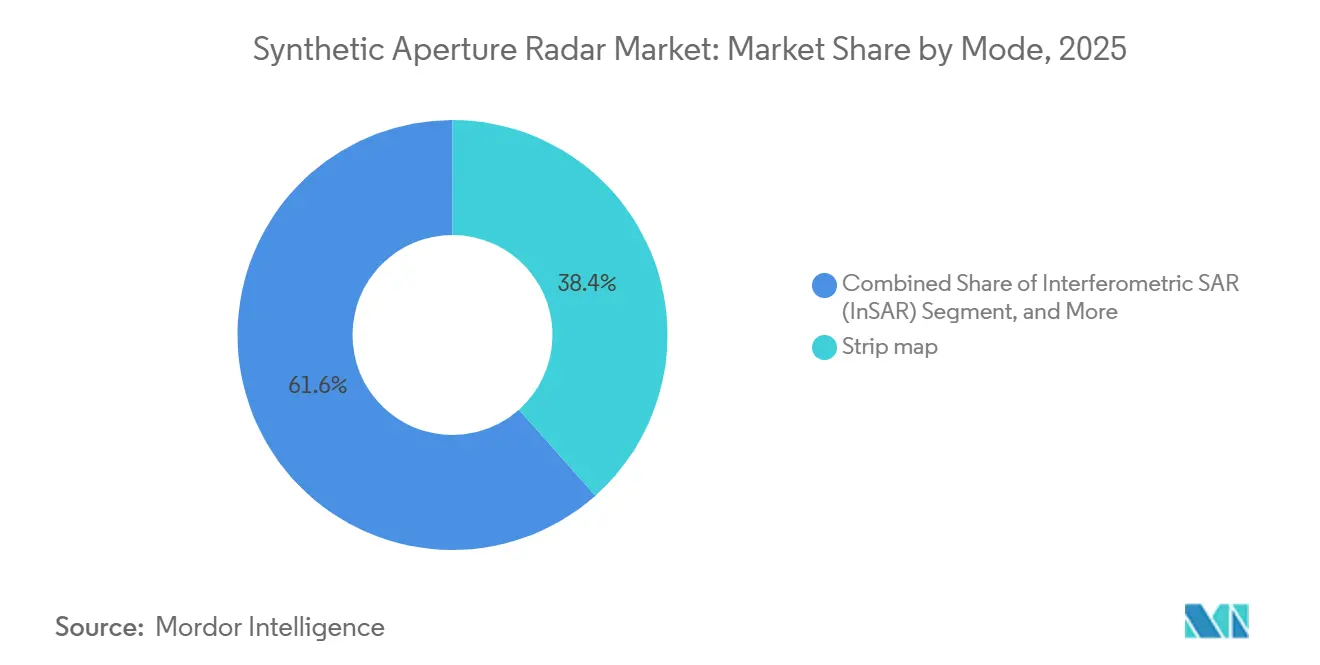

- By mode, stripmap captured 38.43% of synthetic aperture radar market share in 2025; interferometric SAR is poised to grow at an 11.59% CAGR through 2031.

- By application, military and defense accounted for 48.67% of 2025 revenue; infrastructure monitoring is projected to post an 11.95% CAGR to 2031.

- By geography, North America led with 41.39% share in 2025; Asia-Pacific is forecast to be the fastest-growing region at a 12.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Synthetic Aperture Radar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Defence-Sector Surveillance Budgets | +2.30% | Global, concentrated in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Proliferation of Small-Satellite SAR Constellations | +2.80% | Global, led by North America and Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| All-Weather Disaster-Response Imaging Demand | +1.40% | Global, peak impact in Asia Pacific, South America, and Africa | Medium term (2-4 years) |

| AI-Driven SAR Analytics Service Models | +1.90% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Multi-Static SAR Constellations (≤30-Minute Revisit) | +1.20% | Global, initial deployments in North America and Europe | Long term (≥ 4 years) |

| Sovereign ISR Demand From Mid-Tier Nations | +1.60% | Asia Pacific, Middle East, and South America | Medium term (2-4 years) |

| Carbon-Monitoring Mandates for Net-Zero Compliance | +1.10% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Defense-Sector Surveillance Budgets

Defense agencies now prioritize commercial SAR subscriptions over sovereign satellite builds because subscriptions cut acquisition time and spread geopolitical risk across multiple vendors. Finland awarded ICEYE EUR 158 million (USD 172 million) in November 2024 for persistent coverage, and Poland followed with a USD 227 million contract in 2025.[1]Jason Rainbow, “ICEYE Wins EUR 158 Million Finnish Defense Contract,” SpaceNews, spacenews.com Greece and the Netherlands signed additional agreements totalling USD 150 million, showing that smaller NATO members view rapid-refresh SAR as essential for intelligence dominance. The United Kingdom’s Oberon program dedicated GBP 127 million (USD 161 million) to integrate commercial feeds into joint fusion centers, sidestepping traditional prime-contractor models.[2]UK Ministry of Defence, “Defence Space Strategy: Oberon Program,” gov.uk These deals indicate that budget allocations increasingly favour analytics software and ground-segment upgrades rather than new spacecraft builds.

Proliferation of Small-Satellite SAR Constellations

Operators have validated that constellations of 50-100 satellites deliver sub-hourly revisit intervals at lower capital risk than a single heavy spacecraft. ICEYE operated 62 satellites by November 2025, each weighing under 100 kilograms yet offering 16-centimeter resolution and 400-kilometer swath widths.[3]ICEYE, “Generation 4 Product Sheet,” iceye.com Capella Space’s Acadia series targets 36 satellites by 2027 with sub-meter resolution, and Umbra plans further launches to broaden global coverage.[4]Capella Space, “Acadia Constellation Expansion,” capellaspace.com The distributed model supports incremental technology refresh every two years and enables tasking to surge during crises without compromising uptime.

AI-Driven SAR Analytics Service Models

Machine-learning models now automate vessel detection, change analysis, and deformation mapping, moving revenue toward cloud-delivered insights rather than pixel downloads. The European Space Agency’s mission proved that onboard AI could filter scenes and cut downlink volume by 70%. ICEYE’s AI4SAR toolkit delivers pretrained models through cloud APIs, while Amazon Web Services and Google Earth Engine host SAR libraries that non-specialists can query at petabyte scale. These advances unlock new addressable markets in insurance, finance, and logistics, where users lack remote-sensing expertise yet demand actionable intelligence.

All-Weather Disaster-Response Imaging Demand

Emergency management agencies rely on SAR for flood mapping, earthquake deformation, and landslide detection because optical sensors fail at night or under clouds. The Copernicus Emergency Management Service processed more than 1,200 SAR activations in 2024-2025, often delivering wall-to-wall coverage within 12 hours. NASA integrates forthcoming NISAR L-band data to monitor Asian river basins where monsoon clouds block optical revisits for weeks. Operators are pre-positioning ground stations near disaster-prone regions to slash latency and meet humanitarian response timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Spaceborne SAR Development and Launch Costs | -1.80% | Global, most acute in emerging markets and mid-tier nations | Medium term (2-4 years) |

| Power and Down-Link Limits in Small-Sat Platforms | -1.30% | Global, concentrated in small-satellite operators | Short term (≤ 2 years) |

| RF-Spectrum Congestion in X / C Bands | -0.90% | Global, peak interference in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Export-Control Barriers for Dual-Use SAR Payloads | -1.10% | Global, most restrictive for technology transfers to Middle East, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Spaceborne SAR Development and Launch Costs

Even miniaturized SAR payloads require precision phased-array antennas, high-power transmitters, and radiation-hardened processors, keeping unit hardware costs in the USD 15 million–USD 30 million range. Although rideshare launches have lowered ticket prices, a 500-kilogram class mission still pays USD 10 million–USD 20 million for launch alone. Mid-tier nations often pivot to data subscriptions because sovereign programs demand upfront financing and long qualification cycles. Insurance premiums add another 10%-15% because deployable antennas and high-power amplifiers raise on-orbit risk profiles.

Power and Down-Link Limits in Small-Sat Platforms

A 100-kilogram satellite generates only 200-400 watts from solar arrays, yet a high-resolution stripmap requires peak power near 1 kilowatt, forcing operators to duty-cycle imaging and accept gaps. A single high-resolution scene can exceed 10 gigabits, but typical X-band or Ka-band downlinks peak at 1 gigabit per second, necessitating several ground passes. ICEYE offsets the mismatch with onboard compression and queued downloads, but operators still must balance revisit frequency against data-throughput bottlenecks. Transitioning to Ka-band eases spectrum congestion yet introduces rain-fade challenges in tropical regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Spaceborne Dominance with Emerging Maritime Upside

Spaceborne platforms generated 54.19% of revenue in 2025, underscoring their unmatched ability to image denied areas and deliver global coverage without overflight clearances. The synthetic aperture radar market size for spaceborne systems is set to climb steadily thanks to falling launch prices, smaller bus architectures, and direct-to-cloud downlink pipelines that shorten tasking-to-delivery cycles. Maritime-based systems, although small today, are expected to log an 11.29% CAGR to 2031 as navies equip patrol craft with compact X-band radars that close gaps left by satellite revisit intervals.

Spaceborne constellations benefit from economies of scale, and operators refresh technology every 24 months rather than the decade-long cadence of legacy spacecraft. Maritime installations exploit ship power and hull stability to host larger antennas than aerial drones, improving detection of low-observable vessels in littoral zones. Airborne SAR, spanning manned aircraft and UAVs, retains tactical relevance because real-time line-of-sight links enable rapid target prosecution. Ground-based SAR remains a niche used for millimeter-precision monitoring of dams and mines yet contributes invaluable calibration data to on-orbit systems. Collectively, these dynamics ensure that the synthetic aperture radar market continues integrating multi-platform architectures that trade coverage for latency in mission-specific ratios.

By Frequency Band: X-Band Maturity Versus Ka-Band Precision

X-band captured 35.28% of 2025 revenue and will remain the synthetic aperture radar market’s workhorse because its 3-centimeter wavelength balances resolution against atmospheric attenuation. Operators favour X-band for day-night maritime surveillance, moving-target indication, and urban mapping. Ka-band, now advancing at an 11.16% CAGR, promises sub-decimeter resolution that unlocks infrastructure monitoring use cases, yet it struggles with rain fade that limits reliability in equatorial climates.

L-band’s longer wavelength penetrates vegetation and soil, making it indispensable for deforestation analysis and earthquake deformation studies as highlighted by the upcoming NISAR mission. C-band sits in the middle, offering wider swath coverage for ice tracking and maritime domain awareness, while S-band and Ku-band support specialized missions such as dual-frequency interferometry and high-throughput experiments. Frequency diversity strategies that blend X-band dependability with Ka-band acuity are emerging, allowing operators to tier services based on customer tolerance for weather risk and resolution needs.

By Component: Hardware Share Shifts Toward Software Differentiation

Antenna assemblies accounted for 27.16% of 2025 component revenue because phased-array technologies still command premium prices. However, data processor and software lines are forecast to grow at a 12.01% CAGR as value migrates from hardware to algorithms that deliver analytics in near real time. The synthetic aperture radar market size tied to cloud processing rises each time an operator exposes APIs that let non-experts query deformation or vessel-tracking products in minutes.

Gallium-nitride power amplifiers and software-defined radios are commoditizing transmitters and receivers, lowering entry barriers for new-space firms. Power subsystems face thermal constraints on small buses, forcing innovations in deployable radiators and battery chemistries to sustain high-duty operation. Antenna vendors respond with lighter meta surface reflectors and digital beam-forming networks that cut mass without sacrificing gain, yet the strategic locus now sits in AI models that classify ships, predict floods, or flag millimetre-scale bridge sagging.

By Mode: Stripmap Breadth Competes with InSAR Precision

Stripmap retained 38.43% revenue share in 2025 because it delivers a pragmatic blend of resolution and wide-area coverage for reconnaissance and land-use change detection. In contrast, interferometric SAR is projected to expand at an 11.59% CAGR through 2031, driven by regulatory mandates that require continuous deformation monitoring of bridges, pipelines, and rail corridors across the European Union.

Spotlight mode offers resolutions below 50 centimeters, prized by defense agencies for denied area targeting, yet its narrow scene size limits commercial scalability. ScanSAR covers swaths beyond 400 kilometres, making it indispensable for maritime patrol and disaster assessment, though resolution tops out near 20 meters. Polarimetric SAR unlocks biomass estimation and land-cover classification but remains research-centric due to high processing complexity. As customers demand both coverage and precision, operators increasingly blend modes within a single pass, scheduling spotlight on high-priority targets while collecting stripmap context on the flanks, a practice that optimizes revenue per orbit in the synthetic aperture radar market.

By Application: Defense Core, Infrastructure Momentum

Military and defense contributed 48.67% of 2025 revenue, cementing their role as anchor customers for the synthetic aperture radar market. Infrastructure monitoring, projected to grow at an 11.95% CAGR, is scaling because millimetre-accurate InSAR reveals structural fatigue before catastrophic failure. Earth observation and environmental monitoring remain indispensable for climate science and carbon accounting, while oil and gas operators deploy SAR to detect offshore leaks and onshore subsidence.

Maritime surveillance uses wide-swath modes to spot illegal fishing and oil spills, with 500,000 vessel detections processed by the European Maritime Safety Agency in 2024 alone. Disaster-management authorities leverage SAR’s cloud-penetration to map floods within hours, and agriculture stakeholders integrate soil-moisture snapshots into yield models. As cloud platforms automate analytics, nontraditional verticals such as insurance and commodity trading enter the demand pool, ensuring that the synthetic aperture radar market opportunities diversify well beyond the defense sector.

Geography Analysis

North America commanded 41.39% of 2025 revenue thanks to multi-year imagery procurements by the National Reconnaissance Office and the National Geospatial-Intelligence Agency, whose collective contracts with ICEYE, Capella Space, and Umbra exceeded USD 400 million. Canada’s RADARSAT Constellation Mission reinforced Arctic sovereignty by supplying C-band data for ice charting and maritime safety. Mexico initiated pilot programs for flood response and border surveillance, albeit on constrained budgets, leveraging commercial subscriptions rather than sovereign spacecraft.

Asia Pacific is projected to lead growth at a 12.22% CAGR through 2031 as China, India, Japan, and South Korea invest in sovereign constellations to secure strategic autonomy. India’s NASA-ISRO NISAR mission, scheduled for 2026, will yield 12-day repeat-pass interferometry over all land masses, empowering Himalayan landslide monitoring and coastal subsidence studies. Japan’s ALOS-4, launched in March 2024, introduced enhanced L-band penetration for crop and forest analytics. China’s Gaofen-3 series and burgeoning commercial players scale capacity for Belt and Road monitoring, while South Korea targets a 2027 launch for its first indigenous high-resolution SAR. Southeast Asia leverages the Copernicus Emergency Management Service for typhoon and flood mapping, with over 200 activations recorded in 2024-2025.

Europe sustains leadership in open-data policy through Sentinel-1 and the European Ground Motion Service mandate, which requires millimetre-precision deformation monitoring of critical infrastructure. Germany, France, Italy, and the United Kingdom have parallel national programs that hedge dependency on shared assets. The Middle East accelerates adoption, exemplified by the UAE’s Space42 Foresight constellation launched in 2024 for Gulf maritime security. Africa and South America trail in absolute spending but exploit international charters to access imagery for agriculture and disaster relief, with Brazil focusing on Amazon deforestation oversight.

Regulatory Landscape

Commercial SAR operations and cross-border technology transfer are shaped by a dual-use compliance stack that varies by geography and affects payload design, licensing timelines, and addressable export markets. In the United States, commercial remote sensing is licensed under 15 CFR Part 960 through the Department of Commerce framework used by NOAA’s Commercial Remote Sensing Regulatory Affairs, where applicants provide technical performance disclosures such as resolution and polarization capabilities. In parallel, SAR payload hardware and related defense articles fall under U.S. Department of State export controls (ITAR/USML), which adds a gate for international hardware shipments and technical assistance.

Export-control thresholds remain a constraint for dual-use SAR payloads, influencing whether systems are sold as hardware or delivered as data services. In October 2024, the U.S. Department of State proposed updates to ITAR Category XV(a)(8), including adjusting SAR export bandwidth thresholds (from 300 MHz to 500 MHz in the proposal). Industry commentary at the time noted that the proposed level still sits below common commercial SAR bandwidths. Outside the United States, multilateral regimes such as the Wassenaar Arrangement continue to shape licensing outcomes for sensitive remote sensing technologies, while allied-partner pathways under U.S. commerce licensing support transfers to select partner nations and keep tighter controls on broader destinations.

Competitive Landscape

Competition in the synthetic aperture radar market centers on resolution, revisit frequency, and latency from tasking to delivery. Legacy defense contractors Lockheed Martin, Northrop Grumman, RTX, BAE Systems, Thales, Leonardo, Airbus dominate capital-intensive large-satellite and airborne segments. New-space firms such as ICEYE, Capella Space, and Umbra tilt the playing field by launching agile constellations that refresh technology every two years, forcing incumbents to partner, acquire, or build their own small-sat units.

ICEYE’s Generation 4 bus achieves 16-centimeter resolution with a 400-kilometer swath width on sub-100-kilogram spacecraft, proving that small satellites can rival legacy systems while reducing unit risk. Capella Space secured an approximately USD 150 million National Geospatial-Intelligence Agency contract extension in 2025, underlining government appetite for commercial capacity. Umbra’s sub-meter constellation broadens coverage over contested maritime corridors, prompting traditional primes to market hosted-payload slots or data-subscription bundles to stay relevant.

Regulatory regimes shape competition: Wassenaar export restrictions limit dual-use technology transfers, which indirectly protect Western suppliers by constraining new entrants in the Middle East and Africa. Spectrum congestion in X-band and C-band incentivizes investments in Ka-band and multi-static architectures that distribute transmitter and receiver functions, thereby cutting per-satellite power budgets. Standards initiatives such as IEEE P3397 for image-quality metrics give customers transparent benchmarks and, over time, may commoditize basic imagery, shifting value capture toward analytics and fusion services.

Synthetic Aperture Radar Industry Leaders

Lockheed Martin Corporation

Airbus SE

Aselsan A.S.

BAE Systems PLC

Cobham PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Defense and security buyers are moving SAR from episodic imagery purchases toward programmatic access to imagery and processing capacity, which creates whitespace for dedicated sovereign or quasi-sovereign constellations, localized manufacturing, and integration into national fusion centers. Germany’s December 2025 award to ICEYE and Rheinmetall for a EUR 1.7 billion sovereign SAR reconnaissance constellation (SPOCK), with satellite production scheduled to begin in Q3 2026, is a clear proof point. The United Kingdom’s Oberon program selected Airbus in February 2025 to build two SAR satellites for UK Ministry of Defence ISR. Together, these procurement routes pull demand toward end-to-end offerings that combine spacecraft, ground segment, and mission integration rather than raw scenes alone.

Commercial opportunities are also widening where buyers prioritize latency and usability alongside resolution. ICEYE’s 2026 constellation expansion, including six satellites launched on March 30, 2026 (SpaceX Transporter-16) and four more on July 7, 2026 (SpaceX Transporter-17), increases revisit and surge capacity for disaster response, maritime domain awareness, and infrastructure monitoring workflows that require rapid refresh. At the same time, RF congestion in mature X/C bands and the push toward higher-throughput architectures keep Ka-band payload roadmaps, onboard filtering, and cloud-native delivery models in focus for customers consuming analytics via APIs instead of downloading pixels.

Recent Industry Developments

- July 2026: ICEYE launched four new SAR satellites on SpaceX Transporter-17, expanding its constellation to 76 satellites. The added capacity supports higher revisit rates and surge tasking for defense, maritime surveillance, and disaster-response customers, strengthening subscription-style delivery at scale.

- December 2025: ICEYE and Rheinmetall secured a EUR 1.7 billion Bundeswehr-backed contract for a sovereign SAR reconnaissance constellation under the SPOCK program. The award accelerates the shift toward dedicated national SAR capacity and reinforces Europe-centric production and integration pathways for all-weather ISR.

- February 2025: Airbus won the UK Ministry of Defence Oberon contract to build two SAR satellites for space-based intelligence, surveillance, and reconnaissance. The program formalizes a national procurement route for radar-imaging satellites and increases competitive pressure on commercial-only providers to offer defense-grade integration and delivery assurances.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from synthetic aperture radar systems that are newly delivered for airborne and spaceborne platforms, including the SAR payload hardware and the ground processing software and electronics used to generate usable SAR imagery for defense, civil, and commercial users.

Scope exclusions: It excludes terrestrial fixed-site perimeter radars and purely passive radar data-analytics services.

Segmentation Overview

- By Platform

- Airborne SAR

- Manned Aircraft

- UAV

- Spaceborne SAR

- Small Satellites (Less than equal 500 kg)

- Large Satellites (Greater than 500 kg)

- Ground-Based SAR

- Maritime-Based SAR

- Airborne SAR

- By Frequency Band

- X-Band

- L-Band

- C-Band

- S-Band

- Ku-Band

- Ka-Band

- Others, Frequency Band

- By Component

- Antenna

- Transmitter

- Receiver

- Data Processor and Software

- Power Supply

- Others, Component

- By Mode

- Stripmap

- Spotlight

- ScanSAR (Wide-Swath)

- Interferometric SAR (InSAR)

- Polarimetric SAR (PolSAR)

- By Application

- Military and Defence

- Earth Observation and Environmental Monitoring

- Oil and Gas Exploration

- Infrastructure Monitoring

- Maritime Surveillance

- Disaster Management and Agriculture

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base on missions, procurement, and imaging demand, then aligning it with what is financially measurable. We relied on public sources such as space agency mission catalogs and satellite SAR publications for payload trends, defense budget documents and parliamentary disclosures for program timing, and spectrum and licensing references from telecom regulators where SAR downlink constraints can affect delivered system configuration.

To keep assumptions realistic, we also reviewed sources such as UN Comtrade trade statistics for relevant electronics categories, patent databases to track where key design activity is rising, and peer reviewed remote sensing journals for resolution, revisit, and processing improvements that can change average pricing. This was combined with company filings, investor presentations, and credible press to identify contract awards and delivery schedules, then cross-checked with a paid subscription used for company financials and news intelligence. These examples are not exhaustive, and many other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with SAR payload and subsystem suppliers, platform integrators, downstream imagery users, and procurement side stakeholders who see budget releases and program slips early. Because this is a global market, we checked inputs across APAC, EMEA, and the Americas to confirm delivery volumes, typical payload pricing, and how ground processing and licensing are bundled in actual contract structures.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 20% | APAC: 38% |

| Mid tier: 43% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 20% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where satellite and airborne SAR program pipelines, payload delivery schedules, and budgeted procurement are translated into an addressable revenue pool by year. When the demand pool is reconstructed this way, the main totals come together only after platform counts, expected payload adoption per platform, and typical contract structures are applied.

To keep the numbers from drifting, we corroborate them with selective bottom-up checks, such as sampled contract values, supplier revenue signals, and a volume by average selling price view for representative payload classes. The model uses practical inputs like the number of SAR satellites and aircraft being delivered or upgraded, average payload pricing by resolution class, mix shift between defense and civil missions, refresh cycles for ground processing electronics, and observed timing gaps between award and delivery. For forecasting, scenario analysis is used around procurement timing and launch cadence, then refined with expert consensus on how budgets and mission priorities are likely to move. Where direct deal values are not visible, gaps are handled through conservative price bands and sensitivity checks, and then tightened after primary feedback confirms what is typically included in a contract.

Data Validation & Update Cycle

Validation is done through triangulation across three layers, program counts and schedules, financial and contract signals, and expert feedback on pricing and bundling. Outliers are reviewed by checking whether a value jump is explained by a new constellation award, a delayed delivery moving into the next year, or a currency and inflation timing issue. Before sign-off, the model and key assumptions are reviewed in multiple analyst passes, and re-contacts are triggered when a major program is re-baselined or a large contract is announced.

The report is refreshed annually, and interim updates are made when material events can change deliveries or pricing assumptions. Right before delivery, we complete a final review pass so clients receive an updated view aligned with the latest public releases and interview validation.

Mordor Intelligence's Synthetic Aperture Radar Market Size Versus Other Published Estimates

Published market sizes for synthetic aperture radar can look far apart, even when everyone is describing the same core technology. The differences usually come from what is counted as SAR revenue, what year is treated as the anchor, and how procurement timing is converted into annual sales.

The main gap comes from scope. Some estimates fold in broader radar families, downstream imagery services, or multi-year contract totals that are not tied to annual deliveries, which can push the number up quickly. Different pricing paths also matter because average payload prices vary with resolution and revisit needs, and whether ground processing software is bundled. Not every publisher refreshes these inputs when new constellation awards shift the mix.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.86 B (2026) | |

| Global Consultancy A | USD 6.17 B (2025) | Uses a different anchor year and a broader revenue roll-up that can blend multi-year program value into the annual market, which typically inflates near-term totals when large defense awards occur. |

| Industry Publisher B | USD 6.94 B (2025) | Treats the base year and forecast window differently and may apply a higher average selling price progression, especially when software and services are bundled without clearly separating one-time payload sales from recurring items. |

Scope and timing choices explain most of the spread in the table, and currency timing and bundling assumptions add another layer. The main gap comes from counting only new airborne and spaceborne SAR system deliveries and explicitly separating ground processing electronics from unrelated radar and service revenues, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the synthetic aperture radar market today?

The market was valued at USD 5.86 billion in 2026 and is projected to reach USD 9.78 billion by 2031.

Which platform segment leads revenue?

Spaceborne systems generated 54.19% of 2025 revenue, well ahead of airborne, maritime, and ground-based platforms.

What region will grow the fastest through 2031?

Asia Pacific is forecast to record a 12.22% CAGR as China, India, Japan, and South Korea deploy sovereign constellations.

Why is Ka-band attracting attention?

Ka-band enables sub-decimeter resolution that supports urban infrastructure monitoring, even though it faces rain-fade challenges.

What is driving uptake in infrastructure monitoring?

European Ground Motion Service mandates and cloud-based InSAR analytics reveal millimeter-scale deformation, prompting asset owners to adopt SAR subscriptions.

How are small-satellite constellations changing SAR economics?

Constellations of 50-100 low-mass spacecraft deliver sub-hourly revisits, lower capital risk, and faster technology refresh than traditional large satellites.

Page last updated on: