Market Overview

| Study Period | 2020 - 2031 |

|---|---|

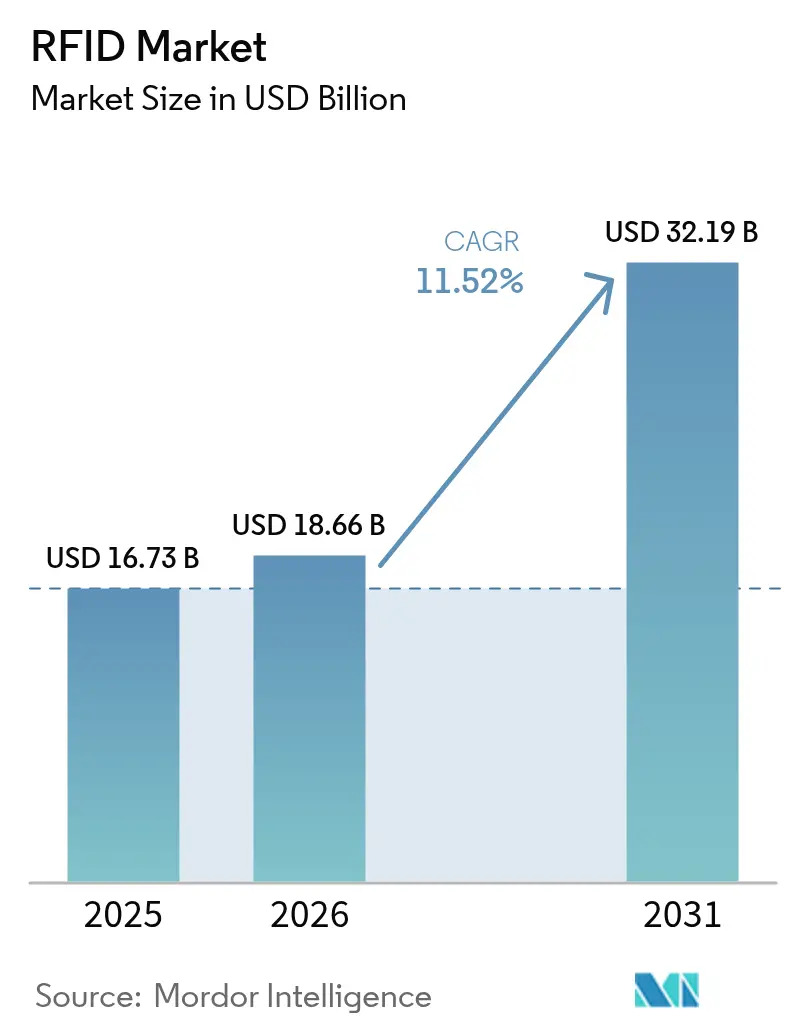

| Market Size (2026) | USD 18.66 Billion |

| Market Size (2031) | USD 32.19 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

RFID Market Analysis by Mordor Intelligence

The RFID market size was valued at USD 16.73 billion in 2025 and estimated to grow from USD 18.66 billion in 2026 to reach USD 32.19 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031). The current upswing reflects the technology’s shift from a niche tool into a core enabler of omnichannel retail, regulated healthcare, and government digital-infrastructure programs. Sustained reductions in UHF inlay pricing below USD 0.04 have lowered entry barriers, while improved Gen2v3 protocols enhance read reliability in crowded environments. Government mandates such as the FDA DSCSA and India’s FASTag scheme continue to pull large-volume deployments. At the same time, cloud analytics platforms convert raw tag reads into predictive maintenance and inventory-planning data that executive teams use for faster decision making. As a result, the RFID market is on course to penetrate high-growth verticals, reinforcing a multi-year investment cycle in tags, readers, and software ecosystems.

Key Report Takeaways

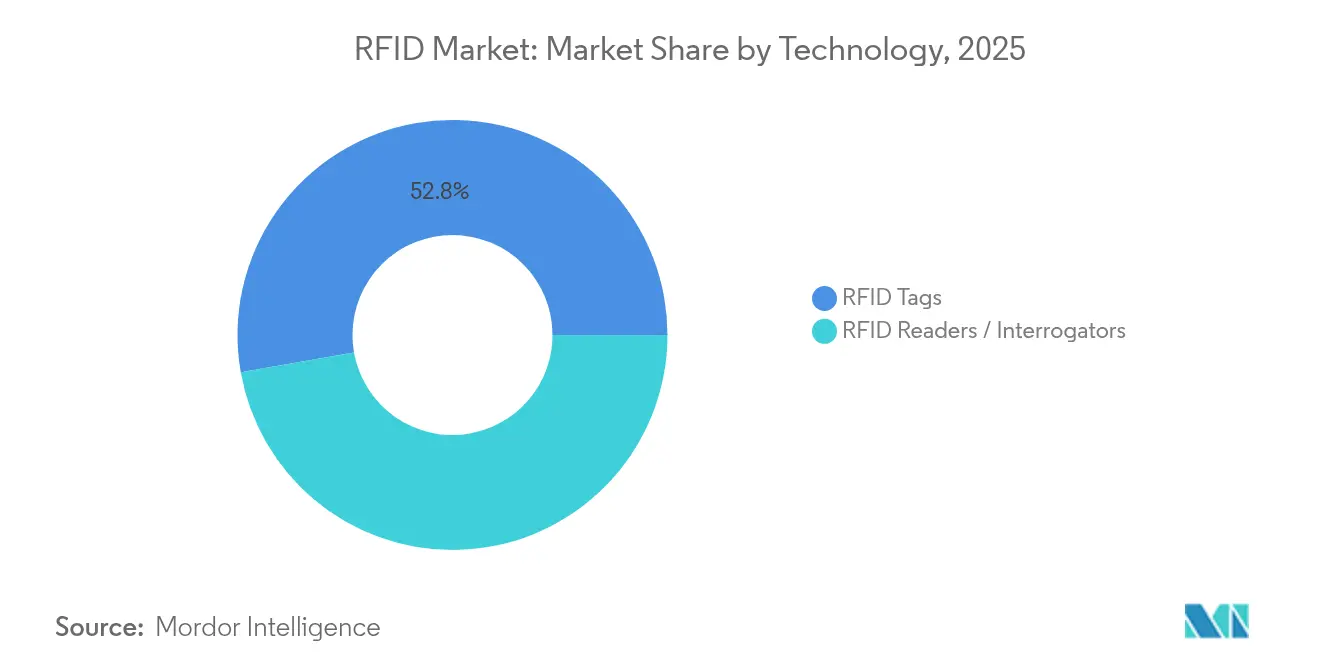

- By technology, RFID Tags led with a 52.78% revenue share in 2025; Active RFID/RTLS infrastructure is expected to expand at a 12.52% CAGR to 2031.

- By frequency band, Ultra-High Frequency systems commanded 40.72% of RFID market share in 2025, while the same band posts the fastest 12.45% CAGR through 2031.

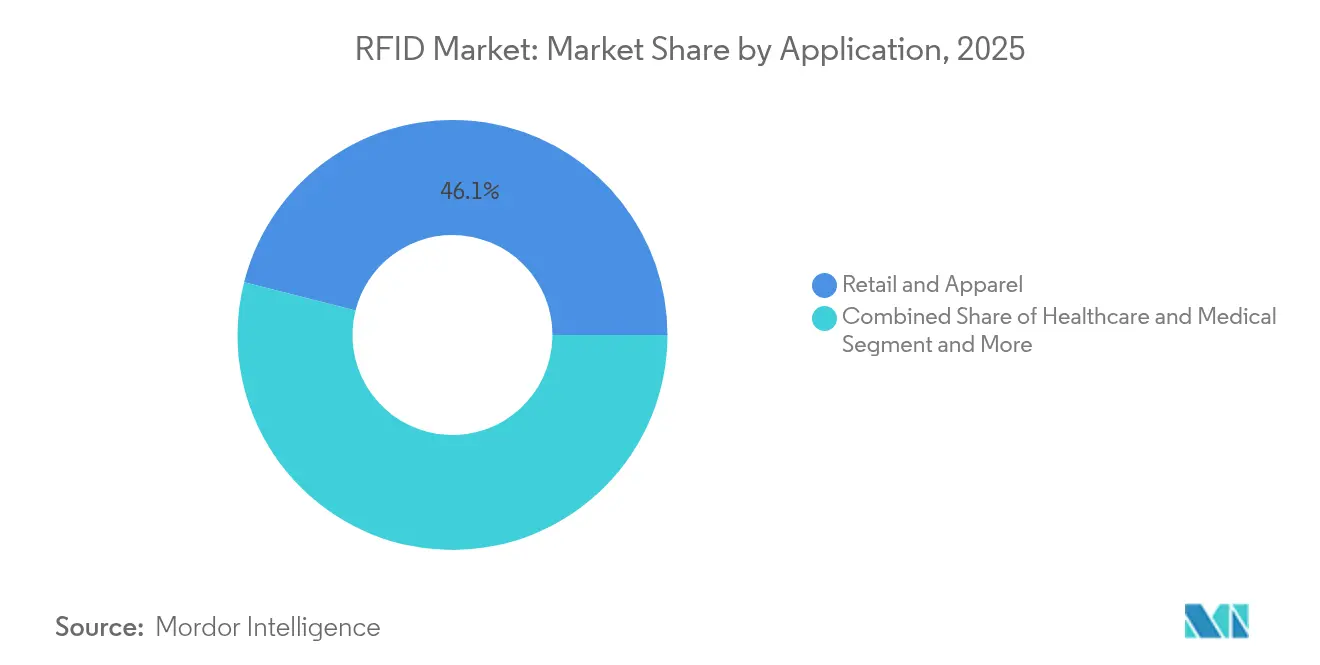

- By application, Retail & Apparel accounted for a 46.05% share of the RFID market size in 2025; Data Center Asset Tracking is advancing at an 11.56% CAGR through 2031.

- By end-user industry, Retail held 34.65% of the RFID market size in 2025; Entertainment exhibits the highest 11.88% CAGR outlook to 2031.

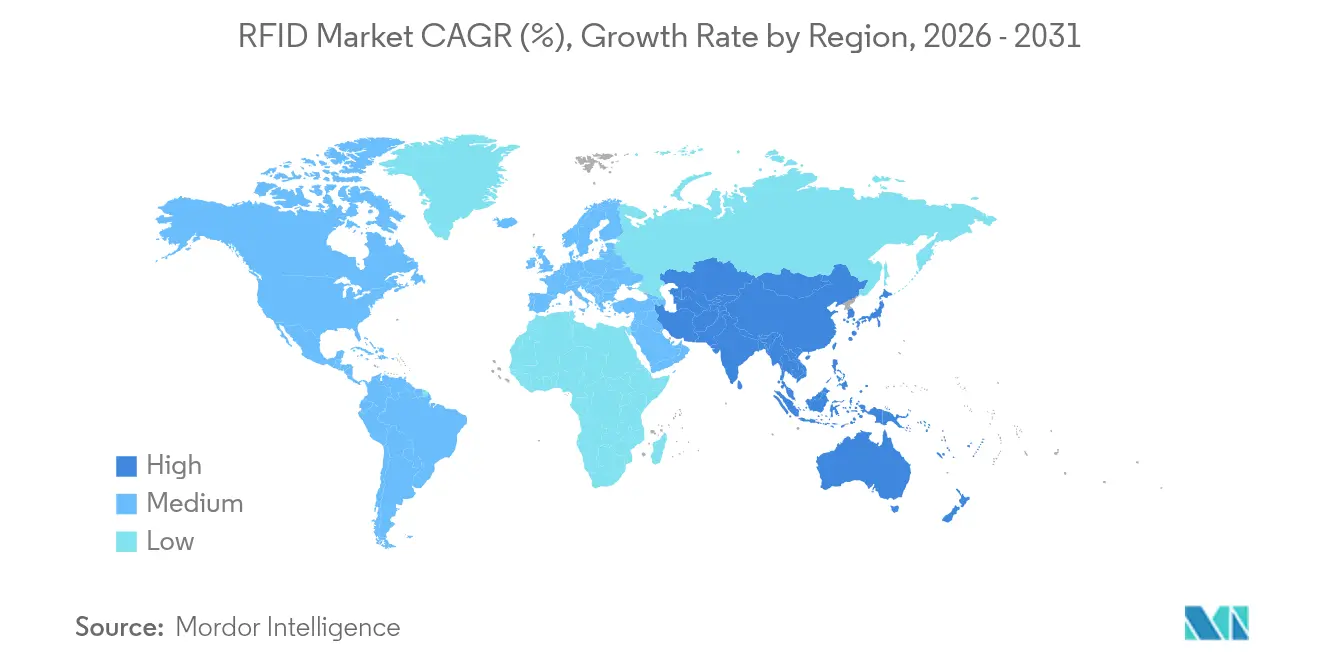

- By geography, North America dominated with 37.15% share in 2025; Asia Pacific leads growth at a 12.58% CAGR thanks to manufacturing digitization and national toll-tag programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RFID Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Serialization Mandates (FDA DSCSA, EU FMD) | +2.8% | North America and EU, expanding globally | Medium term (2-4 years) |

| Item-level RFID Roll-outs by Retail Majors | +2.1% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Government-backed Toll and Vehicle Tag Programs | +1.9% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Data-center and Hospital Asset-tracking Demands | +1.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Sub-USD 0.04 UHF Inlay Pricing | +1.5% | Global, particularly benefiting emerging markets | Short term (≤ 2 years) |

| IoT-Cloud Analytics Integration | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Serialization Mandates Accelerating Pharmaceutical Supply-Chain Transformation

Pharmaceutical legislation in the United States and European Union now obliges distributors to maintain end-to-end electronic track-and-trace capabilities. RFID’s capacity to house serialized identifiers, expiration data, and aggregation codes inside a single tag has proved superior to 2D barcodes for managing high transaction volumes.[1]Healthcare Packaging,"Fresenius Kabi Goes Above and Beyond DSCSA Requirements with RFID," healthcarepackaging.com Fresenius Kabi’s deployment underscores how embedded tag data automates lot-level recalls and strengthens patient-safety checks. With compliance deadlines converging, pharmaceutical executives increasingly regard RFID as a strategic asset rather than a regulatory expense, reinforcing long-term demand in the RFID market.

Item-Level RFID Mandates Transforming Retail Inventory Management

Large retailers are widening RFID requirements from apparel into electronics, stationery, and perishables. Walmart’s latest mandate and Kroger’s bakery rollout illustrate how accurate, real-time stock visibility lifts on-shelf availability above 95% and reduces stockouts by up to 30%. Faster self-checkout and labor savings enhance store economics, making RFID adoption attractive even for mid-tier retailers. As omnichannel models demand unified inventory views, item-level tagging is set to anchor near-term revenue for the RFID market.

Government Infrastructure Programs Driving UHF Volume Growth

Transportation authorities are turning to RFID to streamline tolling and vehicle identification. India’s FASTag program has achieved 97% penetration, offering annual unlimited travel passes that transform occasional users into predictable revenue streams. Similar mandates in China and Latin America are building economies of scale that push tag costs lower and encourage domestic manufacturing. These projects inject millions of tags into the supply chain each quarter, boosting unit volumes across the global RFID market.

Data-Center and Hospital Asset-Tracking Demands

The growth of AI workloads has tightened uptime requirements, driving data-center operators toward Real-Time Location Systems that integrate RFID tags with environmental sensors. RF Code has sold 3 million tags into this vertical, demonstrating enterprise willingness to invest in continuous asset visibility. Hospitals mirror this trend, with RTLS deployments cutting equipment search time and improving patient-throughput metrics. High-value asset environments, therefore, represent a durable demand pillar for the RFID market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy-surveillance Concerns Triggering Stricter EU GDPR-style RFID Governance | -1.8% | EU leading, expanding to other regions with similar privacy frameworks | Medium term (2-4 years) |

| Electromagnetic Interference from Metals/Liquids Hindering Industrial Read Accuracy | -1.2% | Global, particularly in manufacturing and industrial environments | Short term (≤ 2 years) |

| Tag Collision and Dense-read Environment Performance Limitations | -0.9% | Global, concentrated in high-density retail and warehouse applications | Short term (≤ 2 years) |

| Low-cost BLE and UWB Alternatives Competing for Indoor Tracking Budgets | -0.8% | North America & Europe initially, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy Regulations Creating Implementation Complexity

GDPR and analogous laws mandate data-minimization principles that complicate RFID projects capturing personal information. Retailers must embed privacy-by-design controls, shift sensitive data to back-end databases, and offer opt-out pathways, adding legal review cycles to implementation roadmaps.[2]OECD ,"Radio-Frequency Identification: A Focus on Information Security and Privacy," oecd.org The resulting compliance overhead slows deployment decisions and trims near-term growth expectations within the RFID market.

Electromagnetic Interference Limiting Industrial Applications

Radio-wave propagation faces intrinsic challenges around metals and liquids. Despite anti-metal tag innovation, dense-read environments continue to experience collision errors that raise integration spend and lengthen pilots. Competing alternatives like UWB gain traction in high-interference sites, introducing technology-substitution risk for a portion of the RFID market.[3]EnCstore ,"Understanding Interference Issues in RFID, encstore.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Tags Drive Volume While Active Systems Lead Growth

RFID Tags delivered USD 8.83 billion in 2025 revenue, equating to a 52.78% slice of overall RFID market share thanks to their low unit cost and maintenance-free design. Sub-USD 0.04 UHF inlays unlock high-volume consumer-goods labeling, while pharmaceutical serialization adds defensible premium-tag demand. Readers and interrogators, though lower in shipment numbers, generate higher average-selling prices as enterprises adopt multi-protocol, cloud-connected devices. RFID Antennas and middleware form the integration fabric that converts raw reads into operational data, turning simple identification into end-to-end visibility.

Active RFID and RTLS infrastructure is projected to increase at a 12.52% CAGR, reflecting executive priority on real-time location and environmental monitoring inside data centers and hospitals. The RFID market size for active platforms is forecast to exceed USD 6.45 billion by 2031, benefiting from bundled sensor sales and software subscriptions. Battery-assisted passive tags occupy a hybrid position, expanding viability in warehouse automation where longer read ranges are required without full battery cost. Printed and chipless formats remain at pilot scale, yet breakthroughs in roll-to-roll manufacturing could unlock future price disruption inside the broader RFID market.

By Frequency Band: UHF Dominance Across Share and Growth Metrics

UHF captured 40.72% of 2025 revenue, with the RFID market size for this band on track to surpass USD 14.9 billion by 2031 amid a 12.45% CAGR. Retail inventory cycles favor UHF for fast, multi-item reads, while serialization programs value the added data capacity. Recent Gen2v3 improvements boost performance in tag-dense settings, expanding suitability for mixed-material warehouses.

High-Frequency/NFC remains indispensable for contactless payments and consumer-electronics pairing, though its single-digit growth reflects near-saturation in many mature markets. Low-Frequency tags hold niche roles in livestock management and automotive immobilizers where metal penetration is critical. Microwave deployments meet high-speed tolling and industrial automation needs but face cost hurdles. Vendors are now experimenting with frequency-selective antennas capable of reading LF, HF, and UHF tags in parallel, an innovation that could blur segment boundaries in the RFID market.

By Application: Retail Leadership Challenged by Data-Center Growth

Retail and Apparel produced USD 7.7 billion in 2025 sales, equal to a 46.05% contribution to the RFID market. Item-level tagging restores inventory accuracy, averts shrinkage, and furnishes the real-time stock data required for buy-online-pickup-in-store models. Mandates from Walmart and other big-box leaders are forcing suppliers to embed tags at the point of manufacture, pushing adoption upstream.

Data Center Asset Tracking is expanding at an 11.56% CAGR, moving its RFID market share from 3.15% in 2025 toward an anticipated 5.25% by 2031. AI-driven racks intensify power densities, so operators treat downtime risk as a board-level threat. Continuous RTLS combines tag IDs with temperature and humidity metrics, letting facility teams predict failures and automate compliance reporting. Other applications such as healthcare, logistics, and manufacturing sustain steady double-digit growth, reflecting the RFID market’s versatility across physical flows.

By End-User Industry: Retail Dominance Faces Entertainment Sector Challenge

Retail companies absorbed 34.65% of global spend in 2025 as omnichannel initiatives demanded unified inventory views. Store operators report that RFID reduces cycle-count labor by up to 70% and underpins frictionless self-checkout kiosks. FMCG brands are next in line, embedding tags on high-velocity items to counter counterfeiting and improve freshness rotation.

Entertainment, including sports analytics and theme-park operations, is the fastest mover with a 11.88% CAGR. The NFL’s use of Zebra-engineered tags on players and footballs showcases real-time performance data that heightens fan engagement. Government, energy, and public-sector agencies adopt RFID for secure identification and asset maintenance in critical infrastructure, reinforcing a broadening customer mix for the RFID market.

Geography Analysis

North America retained 37.15% revenue share in 2025, anchored by DSCSA compliance, aggressive retail mandates, and large-scale data-center footprints. Healthcare providers accelerate RTLS rollouts to cut asset hoarding and enhance patient throughput, while cloud operators expand tag-enabled monitoring across hyperscale campuses. Policy certainty and mature channel partnerships support continued capital allocation toward RFID deployments, keeping the region at the forefront of the RFID market.

Asia Pacific delivers the strongest trajectory at a 12.58% CAGR. India’s FASTag program alone introduced more than 60 million tags in the past 18 months, fostering domestic tag assembly lines and lowering regional BOM costs. Chinese OEMs integrate RFID into factory-floor MES systems under the Made-in-China 2025 framework, while Southeast Asian retailers adopt the technology to leapfrog manual inventory methods. These vectors combine to elevate the RFID market across Asia Pacific.

Europe sustains high-single-digit growth powered by the EU Falsified Medicines Directive and emerging Digital Product Passport legislation. Privacy regulation slows consumer-facing deployments but encourages innovation in recyclable labels and secure cloud architectures. Middle East & Africa and South America remain nascent, though government identity and toll projects signal future step-ups in local RFID market demand.

Competitive Landscape

The RFID market features moderate fragmentation yet shows rising consolidation as scale economics and platform breadth become competitive differentiators. Avery Dennison, Impinj, and Zebra Technologies pursue vertical integration, bundling semiconductor design, intelligent labels, and analytics software into turnkey solutions. Their go-to-market strategies prioritize ecosystem partnerships that accelerate customer onboarding.

M&A activity continues to reshape the field. TOPPAN Holdings acquired HID’s Citizen Identity Solutions assets to deepen public-sector credentials and cross-sell tags into e-Passport programs. Multi-Color Corporation’s purchase of Starport Technologies broadens intelligent packaging capability, creating upsell paths from pressure-sensitive labels to RFID-enabled smart labels. These moves consolidate fragmented production bases and expand application reach inside the RFID market.

Intellectual property enforcement also shapes dynamics. Impinj secured nearly USD 15 million in damages against NXP for patent infringement and gains ongoing royalties, reinforcing the value of R&D investment. Vendors increasingly differentiate through software analytics and cloud dashboards that unlock recurring revenue beyond hardware margin, signaling a strategic pivot toward platform economics across the RFID market.

RFID Industry Leaders

-

Avery Dennison Corporation

-

Alien Technology Corporation

-

William Frick & Company

-

Invengo Technology Pte Ltd.

-

CCL Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: Zebra Technologies launched the EM45 RFID enterprise mobile device, a product-extension strategy aimed at deepening share of retail workflows through integrated scanning and analytics.

- January 2025: SML IIS and Zebra Technologies unveiled an RFID ceiling-reader solution, positioning overhead infrastructure to reduce floor congestion and lift read accuracy in large retail spaces.

- January 2025: ASSA ABLOY acquired 3millID and Third Millennium for USD 21 million to extend its physical-access portfolio and cross-leverage RFID credentials in the commercial security market.

- October 2024: TOPPAN Holdings and TOPPAN Next purchased HID’s Citizen Identity Solutions unit to integrate secure-ID platforms and strengthen government-sector positioning.

Global RFID Market Report Scope

RFID (Radio Frequency Identification) is a wireless system that comprises two components: tags and readers. The reader is a device with antennas that emit radio waves and receive signals from RFID tags. Tags are passive or active, communicating their identity and other information to nearby readers via radio waves. Passive RFID tags do not have a battery. The reader powers them. Batteries are usually used to power active RFID tags.

The RFID market is Segmented by technology (RFID tags, RFID interrogators, RFID software/services, and active RFID/RTLS), application (retail, healthcare and medical, passenger transport/automotive, manufacturing, and consumer products), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Technology

| RFID Tags | Passive (LF, HF, UHF) |

| Active | |

| Battery-Assisted Passive | |

| Printed / Chipless | |

| RFID Readers / Interrogators | Fixed Portal |

| Handheld | |

| Integrated Mobile | |

| RFID Antennas | |

| RFID Middleware and Software | |

| Active RFID / RTLS Infrastructure |

By Frequency Band

| Low Frequency (125-134 kHz) |

| High Frequency / NFC (13.56 MHz) |

| Ultra-High Frequency (860-960 MHz) |

| Microwave (2.45 GHz) |

By Application

| Retail and Apparel |

| Healthcare and Medical |

| Transportation and Logistics |

| Manufacturing and Industrial IoT |

| Automotive and Passenger Mobility |

| Agriculture and Livestock |

| Data Centers and IT Assets |

| Aerospace and Defence |

| Consumer Electronics and Smart Home |

| Payments and Access Control |

By End-User Industry

| FMCG and CPG |

| Government and Public Sector |

| Hospitality and Entertainment |

| Energy and Utilities |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Nordics (Sweden, Norway, Finland, Denmark) | |

| Germany | ||

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Technology | RFID Tags | Passive (LF, HF, UHF) | |

| Active | |||

| Battery-Assisted Passive | |||

| Printed / Chipless | |||

| RFID Readers / Interrogators | Fixed Portal | ||

| Handheld | |||

| Integrated Mobile | |||

| RFID Antennas | |||

| RFID Middleware and Software | |||

| Active RFID / RTLS Infrastructure | |||

| By Frequency Band | Low Frequency (125-134 kHz) | ||

| High Frequency / NFC (13.56 MHz) | |||

| Ultra-High Frequency (860-960 MHz) | |||

| Microwave (2.45 GHz) | |||

| By Application | Retail and Apparel | ||

| Healthcare and Medical | |||

| Transportation and Logistics | |||

| Manufacturing and Industrial IoT | |||

| Automotive and Passenger Mobility | |||

| Agriculture and Livestock | |||

| Data Centers and IT Assets | |||

| Aerospace and Defence | |||

| Consumer Electronics and Smart Home | |||

| Payments and Access Control | |||

| By End-User Industry | FMCG and CPG | ||

| Government and Public Sector | |||

| Hospitality and Entertainment | |||

| Energy and Utilities | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Nordics (Sweden, Norway, Finland, Denmark) | ||

| Germany | |||

| France | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the RFID market?

The RFID market is valued at USD 18.66 billion in 2026 and is forecast to grow to USD 32.19 billion by 2031.

Which technology segment leads the RFID market?

RFID Tags hold the largest share at 52.78% of 2025 revenue, supported by low inlay pricing and wide retail adoption.

What factors drive the fastest growth segment in the RFID market?

Active RFID/RTLS infrastructure grows at a 12.52% CAGR because real-time location data is critical for data centers and hospitals.

Which region offers the highest growth opportunity for RFID vendors?

Asia Pacific shows the highest 12.58% CAGR, propelled by large-scale government toll programs and manufacturing digitization.

Page last updated on: