Ground Penetrating Radar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

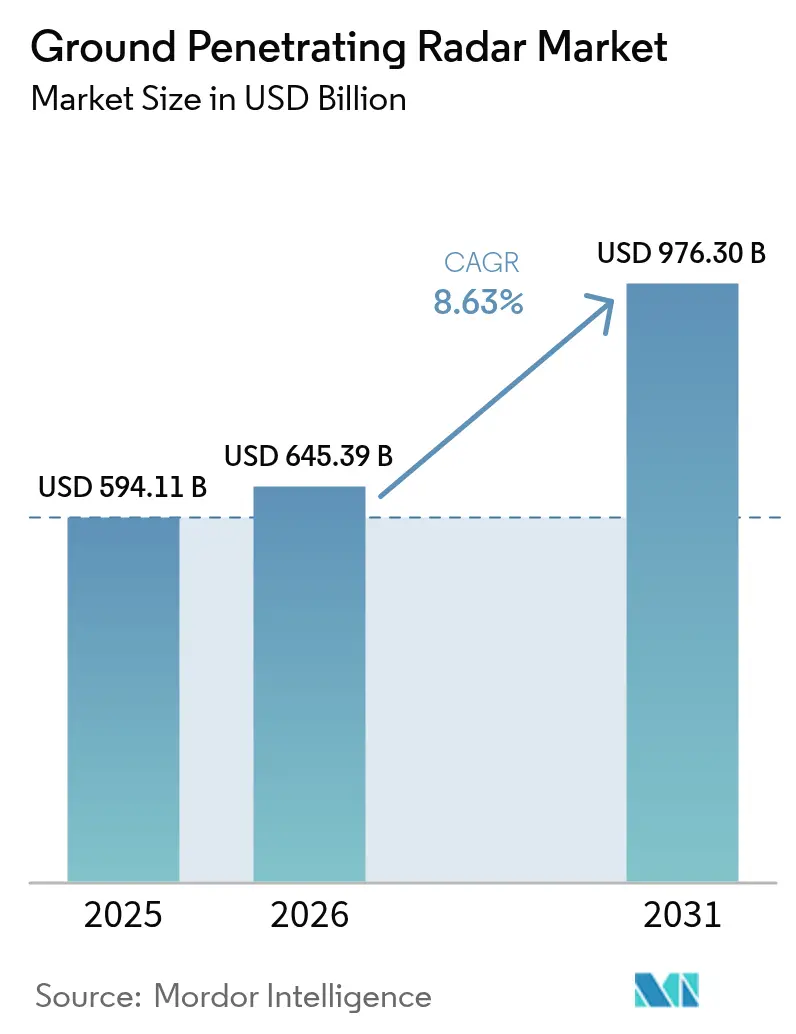

| Market Size (2026) | USD 645.39 Billion |

| Market Size (2031) | USD 976.30 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ground Penetrating Radar Market Analysis by Mordor Intelligence

Ground penetrating radar market size in 2026 is estimated at USD 645.39 billion, growing from 2025 value of USD 594.11 billion with 2031 projections showing USD 976.3 billion, growing at 8.63% CAGR over 2026-2031. Rising demand for non-invasive subsurface mapping, mandated utility-locating standards, and rapid AI integration are turning radar data into predictive maintenance insights that lower downtime and repair costs. UAV-mounted solutions extend survey reach into hazardous terrain, while high-frequency antenna arrays open concrete imaging and forensic opportunities. Regulatory harmonization in North America and the EU shortens product-approval cycles, and expanding infrastructure investments across Asia accelerate adoption. Competitive intensity is increasing as software-centric entrants challenge established hardware leaders by linking real-time GPR streams to digital-twin platforms.

Key Report Takeaways

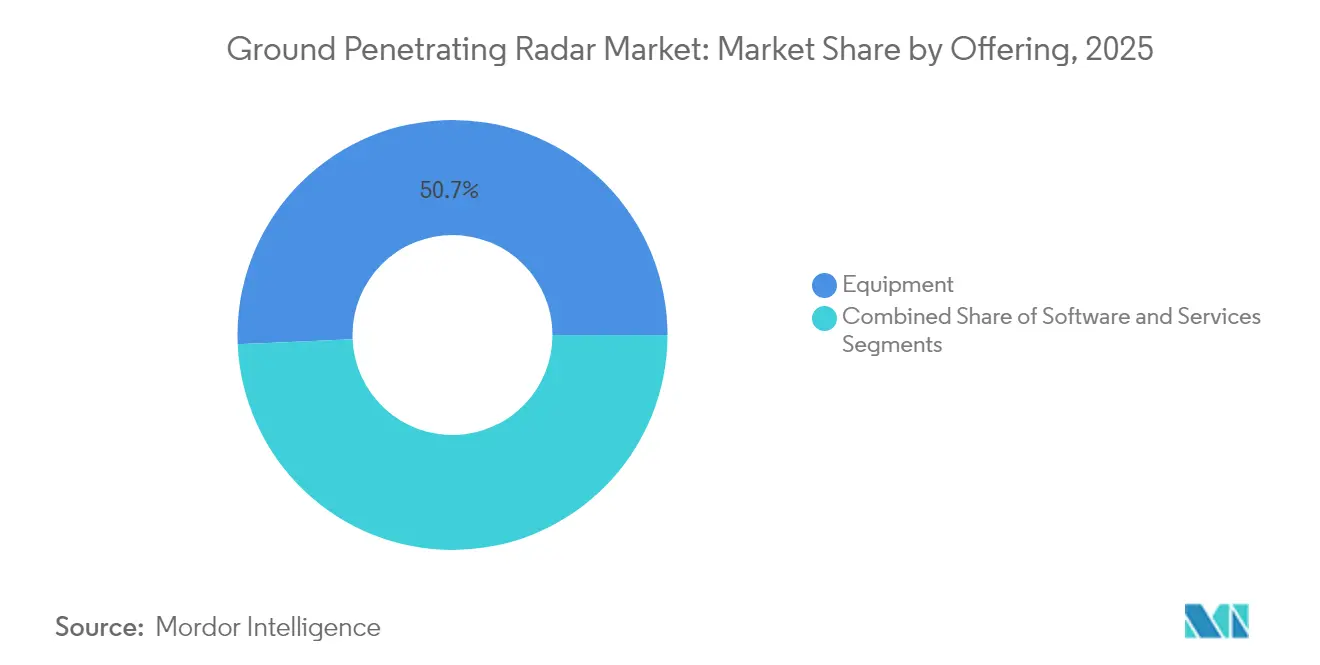

- By offering, equipment commanded 50.68% of the ground penetrating radar market share in 2025, while services are forecast to grow at a 9.05% CAGR to 2031.

- By product type, cart systems led with 41.35% revenue share in 2025; UAV-mounted units are projected to expand at an 10.9% CAGR through 2031.

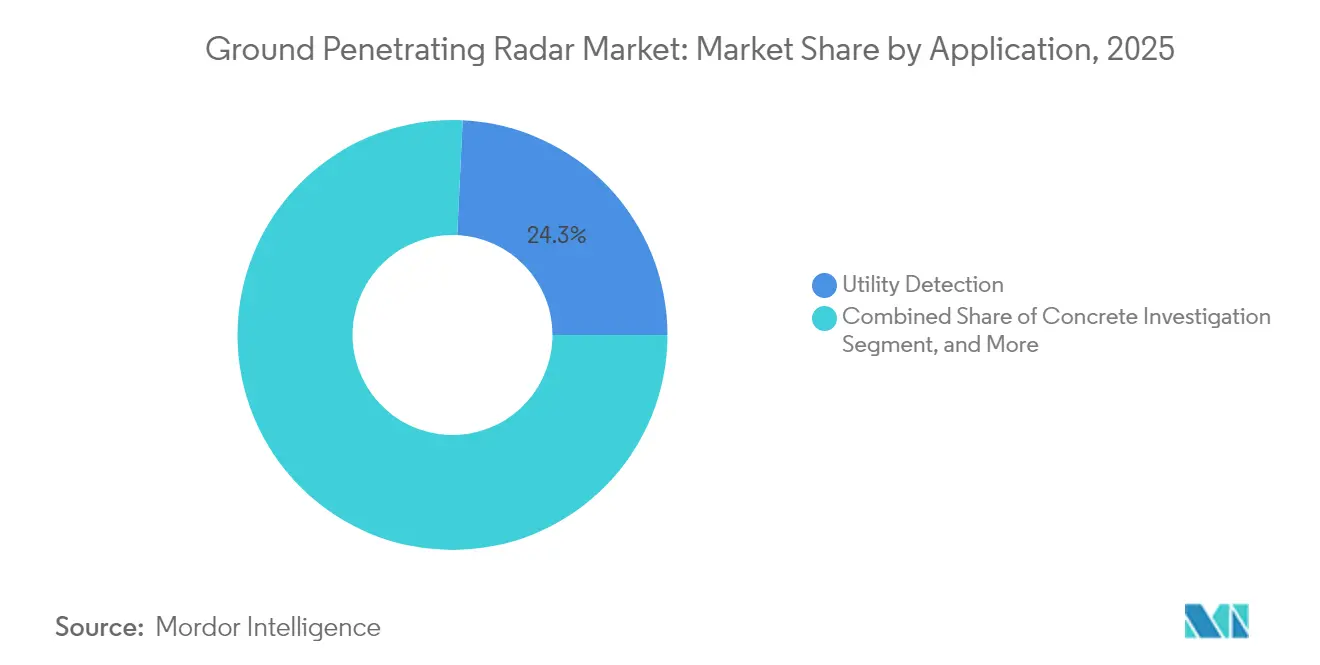

- By application, utility detection accounted for 24.25% of the ground penetrating radar market size in 2025; military and law-enforcement uses are advancing at a 9.95% CAGR to 2031.

- By end-user industry, construction and infrastructure remained the largest consumer segment in 2025, while defense is the fastest-growing vertical through the forecast horizon.

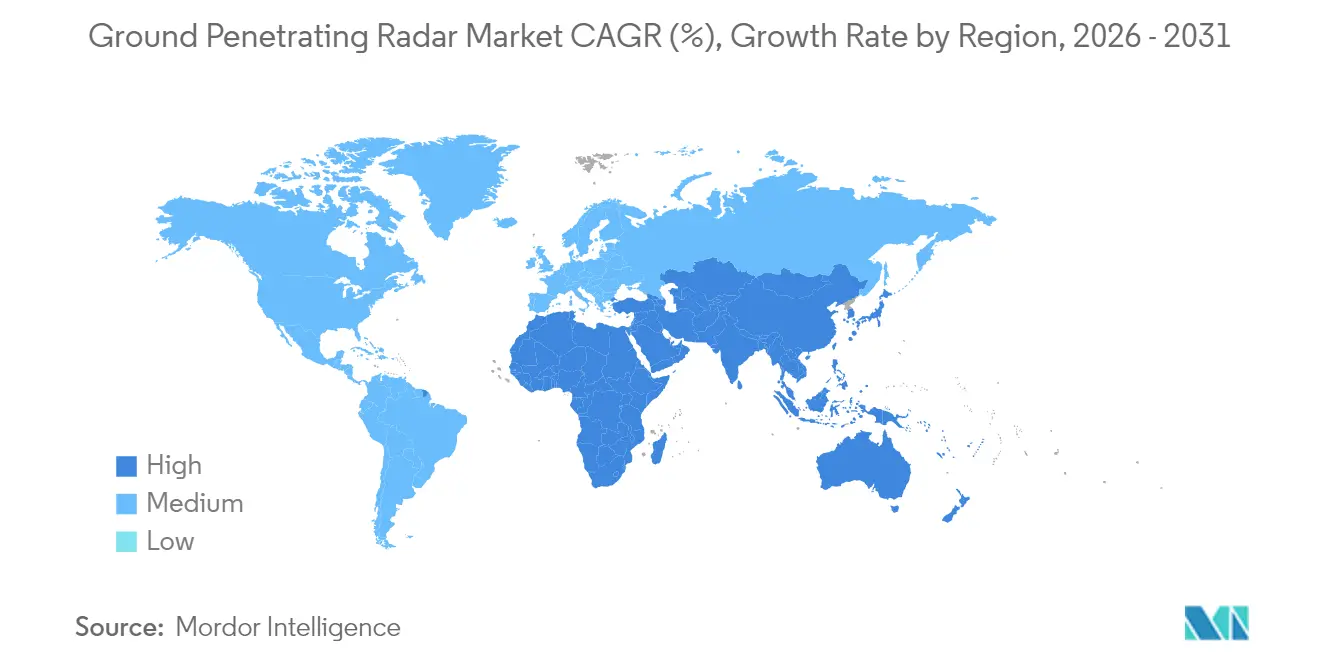

- North America dominated geographically with a 33.45% share in 2025; Asia-Pacific exhibits the quickest regional CAGR at 8.7% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ground Penetrating Radar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of urban underground transportation corridors | +1.80% | Asia-Pacific, spillover to Middle East | Medium term (2-4 years) |

| Mandated underground utility mapping standards | +1.20% | North America and Europe | Short term (≤ 2 years) |

| Rising adoption of high-frequency antenna arrays for concrete imaging | +0.90% | Global, developed markets | Medium term (2-4 years) |

| Integration of GPR with AI-enabled data analytics platforms | +1.50% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Growing demand for non-invasive subsurface mapping in renewable energy projects | +0.70% | Global, wind and solar corridors | Long term (≥ 4 years) |

| Increasing deployment of UAV-mounted GPR in remote and hazardous terrains | +1.10% | Global, mining and defense | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Urban Underground Transportation Corridors in Asia

Asia’s metro build-out from Beijing to Jakarta is fueling sustained purchases of network-ready GPR carts that couple live radar feeds with BIM dashboards. Contractors use continuous scans to guide tunnel-boring machines and avoid high-density utility clusters, reducing strike risk and schedule overruns. ESA’s TruewaveGPR trials logged 50% faster surveys once GNSS and IMU telemetry were embedded. [1]European Space Agency, “TruewaveGPR | ESA Space Solutions,” business.esa.int Government stimulus for climate-resilient infrastructure further underpins multi-year equipment demand.

Mandated Underground Utility Mapping Standards in North America and Europe

The Common Ground Alliance best-practice code now obliges electromagnetic verification before every dig, driving steady fleet renewals among locators and civil contractors. EU ultra-wideband harmonization delivers uniform frequency windows that simplify cross-border equipment logistics and reduce certification costs. [2]European Union, “Short Range Devices… Ultra-Wide Band Equipment,” eur-lex.europa.eu

Rising Adoption of High-Frequency Antenna Arrays for Concrete Imaging

Millimeter-resolution antenna grids spot rebar corrosion and voids before spalling appears. Smartphone-paired handheld units that use hyperbolic-curve-fitting reach depth errors below 3 mm in lab tests. [3]Wei Huang et al., “Millimeter Accuracy Depth Estimation in Concrete…,” pmc.ncbi.nlm.nih.gov Civil-asset owners increasingly embed periodic concrete scans into preventive-maintenance plans.

Integration of GPR with AI-Enabled Data Analytics Platforms

Machine-learning classifiers now parse raw traces to separate soil layers, utilities, and anomalies with accuracy above 88% in controlled settings. [4]Hong Xu et al., “Rock Layer Classification…,” doi.org Digital-twin links let facility managers overlay radar outputs on 3D asset models, enabling condition-based maintenance workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced GPR systems | -1.00% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Limited rental ecosystem for GPR equipment | -0.40% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Signal attenuation in high-conductivity soils | -0.80% | Global, clay-rich and saline zones | Long term (≥ 4 years) |

| Scarcity of skilled GPR data interpreters | -1.10% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Limited Rental Ecosystem in Emerging Economies

Industrial-grade systems with AI processors retail well above USD 100,000, a hurdle for small contractors. Sparse rental fleets in Africa and parts of Latin America curb project-based adoption.

Signal Attenuation in High-Conductivity Soils Limiting Depth Accuracy

Moisture-rich clay raises dielectric losses and trims effective range; detection accuracy drops markedly once water content tops 25%. Stepped-frequency compensation helps but cannot override fundamental electromagnetic limits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Equipment Dominance Drives Hardware Innovation

The equipment segment controlled 50.68% of the ground penetrating radar market in 2025, underscoring the capital-intensive role of transmit-receive hardware in survey workflows. Adopters upgrade to multichannel arrays that boost coverage speed without sacrificing depth resolution. Services, expanding at 9.05% CAGR, attract project owners seeking OPEX models and turnkey data interpretation. As AI modules migrate to edge processors inside control units, vendors bundle analytics subscriptions with hardware to build annuity revenue.

Services growth also reflects a widening skills gap; interpreting complex radar signatures now blends geophysics with data science. Fleet operators specializing in post-processing sell rapid-response scans to infrastructure owners that lack in-house expertise. Software-only providers exploit this shift, feeding classified traces into cloud-hosted neural networks that deliver automated layer picks and object tags within minutes.

By Product Type: Cart Systems Lead While UAVs Accelerate

Cart platforms held 41.35% revenue in 2025 by combining full ground coupling with ergonomic handling, a formula ideal for utility-locating and pavement surveys. Analytic dashboards turn live traces into color-coded depth slices viewable on-site. UAV payloads, although smaller, are scaling fastest at 10.9% CAGR. Mining firms fly radar beneath rotary-wing drones to map tailings-dam seepage paths, while defense teams use fixed-wing variants for border-tunnel sweeps. Despite lighter antennas limiting penetration versus carts, demand rises where ground access is restricted or hazardous.

Hybrid concepts are emerging: detachable sleds that clip to a drone harness for transit then pivot to wheel-based scanning once on site. This modularity lengthens flight endurance and maintains depth capability, hinting at future convergence of airborne and terrestrial designs.

By Component: Control Units Drive Integration Complexity

Modern control units embed GNSS receivers, inertial sensors, and AI accelerators that filter clutter in real time. Vendors advertise centimeter-level positioning accuracy even under dense tree canopy by fusing IMU drift corrections. Antenna innovation centers on metamaterial lenses and phased arrays that sharpen beam focus, while lightweight lithium-ion packs extend UAV sortie times above 30 minutes. Inter-component talk now rides on industrial Ethernet, easing tie-in to site networks and cloud servers.

R&D spending skews to software-defined transmitters able to sweep from 100 MHz to 3 GHz on the fly, tailoring frequency stacks to geology. This adaptability cuts multiple-pass requirements and lowers survey costs per kilometer.

By Frequency Range: Sub-500 MHz Dominates Deep Penetration Applications

Sub-500 MHz rigs remain indispensable for geologic sounding and large-diameter pipeline corridors, where deep reach outweighs fine detail. The 500–1000 MHz band balances penetration and resolution for utility-locating, supporting most municipal work orders. Frequencies above 1000 MHz thrive in concrete imaging and forensic work, mapping rebar grids and voids with millimeter clarity. Dual-mode units can hop bands mid-survey, yielding a single stitched data cube that blends depth and resolution tiers.

Laboratory tests on stepped-frequency prototypes record signal-to-noise uplifts above 3 dB, signalling a future where frequency agility becomes standard on flagship models.

By Application: Utility Detection Leads Amid Military Acceleration

Utility detection preserved 24.25% share of the ground penetrating radar market size in 2025 as cities enforce dig-safety laws. Radar traces feed GIS layers that asset owners update in real time, shrinking unplanned strike costs. Military and law-enforcement demand, growing at a 9.95% CAGR, covers tunnel hunting, UXO mapping, and perimeter security. Concrete investigation and transportation asset audits round out steady recurring work.

Archaeologists and environmental scientists add niche volume by scanning heritage sites and mapping contaminant plumes. Case studies in the UAE showed radar outlining buried stone foundations with minimal site disturbance.

By End-User Industry: Construction Dominance Amid Defense Acceleration

Construction firms anchor system sales, embedding radar scans into pre-bid risk assessments, pile-drive planning, and asset handover packages. Defense procurement picks up pace as agencies fund drone-borne arrays for border patrols and humanitarian de-mining, areas where traditional handheld metal detectors struggle. Renewable-energy EPCs form a rising cohort; wind-farm trenchers verify cable corridors with radar before trenchless boring.

Geography Analysis

North America led with 33.45% revenue in 2025 thanks to stringent Common Ground Alliance rules that mandate subsurface verification and to steady replacement cycles among fleet operators. State-backed infrastructure grants covering broadband, EV plants, and grid upgrades ensure a deep pipeline of scanning projects. Regional vendors couple radar with AI software to export turnkey offerings globally.

Asia-Pacific posts the highest regional CAGR at 8.7%. Mega-metro rail lines in China, India, and Southeast Asia require 24/7 radar monitoring during excavation. Smart-city programs layer radar outputs into digital twins of underground utility corridors, steering maintenance crews proactively. Japan and South Korea champion drone-based arrays for landslide-prone mountain routes, driving early adoption of lightweight antenna tech.

Europe retains healthy demand under harmonized UWB regulations that smooth certification workflows. Heritage-site managers in Italy and Greece deploy high-frequency rigs to audit cathedral foundations without drilling cores. Defense sensor contracts surged in 2025 as regional tensions prompted larger counter-measure budgets, benefitting suppliers of radar altimeters and electronic-warfare payloads.

Latin America, the Middle East, and Africa remain under-penetrated yet opportunity-rich. Brazil’s power-grid expansion and Saudi Arabia’s giga-projects, for example, include sizable allocations for underground-utility mapping. The constraint remains equipment affordability and interpreter availability, spurring interest in pay-per-scan service models.

Competitive Landscape

The ground penetrating radar market shows moderate fragmentation. Long-time innovators such as Geophysical Survey Systems Inc. leverage five decades of antenna IP and robust dealer networks to defend share. Trimble’s pivot toward software and recurring revenue yielded 62% subscription mix in a USD 3.2 billion sales base, underlining the profit pool shift toward analytics. Leica Geosystems integrated multi-array sensors with cloud dashboards to speed utility-map delivery.

Emerging challengers focus on AI-first workflows: distributed moving-transceiver prototypes from the University of Michigan enable 360-degree imaging without operator repositioning. Several startups bundle SaaS interpretation engines with low-cost antennas, lowering entry barriers for small contractors. Patent race intensity centers on phased arrays, metamaterial lenses, and neural-network-based clutter filters.

Strategic moves in 2024-2025 included OEM-service alliances, drone-payload partnerships, and defense-sector acquisitions. Chemring expanded production of miniature radar altimeters after booking GBP 26 million (USD 35.78 million) in new orders, targeting annual sales near GBP 800 million (USD 1100.89 million) by 2030. Overall, firms able to integrate hardware reliability with real-time analytics and cloud connectivity are positioned to capture the next growth wave.

Ground Penetrating Radar Industry Leaders

-

IDS Georadar

-

Sensors & Software Inc.

-

Chemring Group

-

Geophysical Survey Systems, Inc. (GSSI)

-

Guideline Geo AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Chemring Group PLC reported an order book of GBP 1,351 million (USD 1859.12 million) with a GBP 26 million (USD 35.78 million) award for Miniature Radar Altimeter systems, supporting its Sensors & Information expansion.

- December 2024: Trimble Inc. outlined a USD 72 billion addressable market at its Investor Day, prioritizing AI-driven digital transformation for field systems.

- November 2024: European Space Agency validated TruewaveGPR, demonstrating 50% faster rail surveys in partnership with Balfour Beatty and Network Rail.

- October 2024: Chemring Group PLC recorded GBP 638 million (USD 877.96 million) FY24 order intake, driven by counter-measures and sensor contracts.

Global Ground Penetrating Radar Market Report Scope

The scope of the study of the ground penetrating radar systems market is limited to the solutions offered by major players, including providers of equipment, services, and integrated solutions for a wide range of industries globally. The after-sales services are not considered for market estimation.

| Equipment |

| Software |

| Services |

| Handheld GPR |

| Cart-Based GPR |

| Vehicle-Mounted GPR |

| UAV/Drone-Mounted GPR |

| Control Unit |

| Antenna |

| Power Supply |

| < 500 MHz |

| 500 - 1000 MHz |

| > 1000 MHz |

| Utility Detection |

| Concrete Investigation |

| Municipal Inspection |

| Forensics and Archaeology |

| Transportation Infrastructure |

| Geotechnical and Environment |

| Disaster Inspection |

| Law Enforcement and Military |

| Construction and Infrastructure |

| Oil and Gas / Mining |

| Environmental and Agriculture |

| Defense and Security |

| Academic and Research |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Offering | Equipment | |

| Software | ||

| Services | ||

| By Product Type | Handheld GPR | |

| Cart-Based GPR | ||

| Vehicle-Mounted GPR | ||

| UAV/Drone-Mounted GPR | ||

| By Component | Control Unit | |

| Antenna | ||

| Power Supply | ||

| By Frequency Range | < 500 MHz | |

| 500 - 1000 MHz | ||

| > 1000 MHz | ||

| By Application | Utility Detection | |

| Concrete Investigation | ||

| Municipal Inspection | ||

| Forensics and Archaeology | ||

| Transportation Infrastructure | ||

| Geotechnical and Environment | ||

| Disaster Inspection | ||

| Law Enforcement and Military | ||

| By End-User Industry | Construction and Infrastructure | |

| Oil and Gas / Mining | ||

| Environmental and Agriculture | ||

| Defense and Security | ||

| Academic and Research | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Nigeria | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the ground penetrating radar market?

The ground penetrating radar market is valued at USD 645.39 billion in 2026.

How fast will the ground penetrating radar market grow through 2031?

The market is forecast to expand at a 8.63% CAGR, reaching roughly USD 976.3 billion by 2031.

Which segment holds the largest ground penetrating radar market share?

Equipment leads with 50.68% revenue share in 2025.

Why are UAV-mounted GPR systems gaining traction?

They enable surveys in hazardous or inaccessible areas and are projected to grow at 10.9% CAGR.

What is the main regulatory driver in North America?

Common Ground Alliance standards require electromagnetic utility verification before every excavation.

Which region is expected to post the fastest growth?

Asia-Pacific, driven by rapid subway construction and smart-city projects, is projected to grow at 8.7% CAGR.

Page last updated on: