Transparent Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

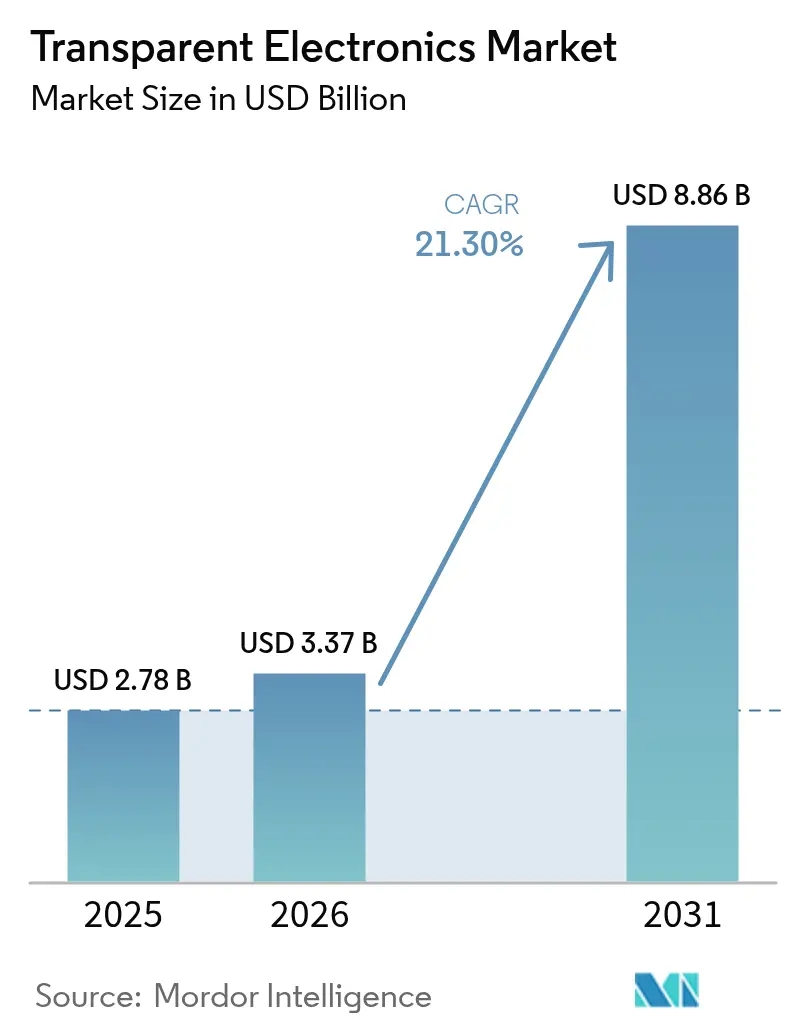

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 8.86 Billion |

| Growth Rate (2026 - 2031) | 21.30% CAGR |

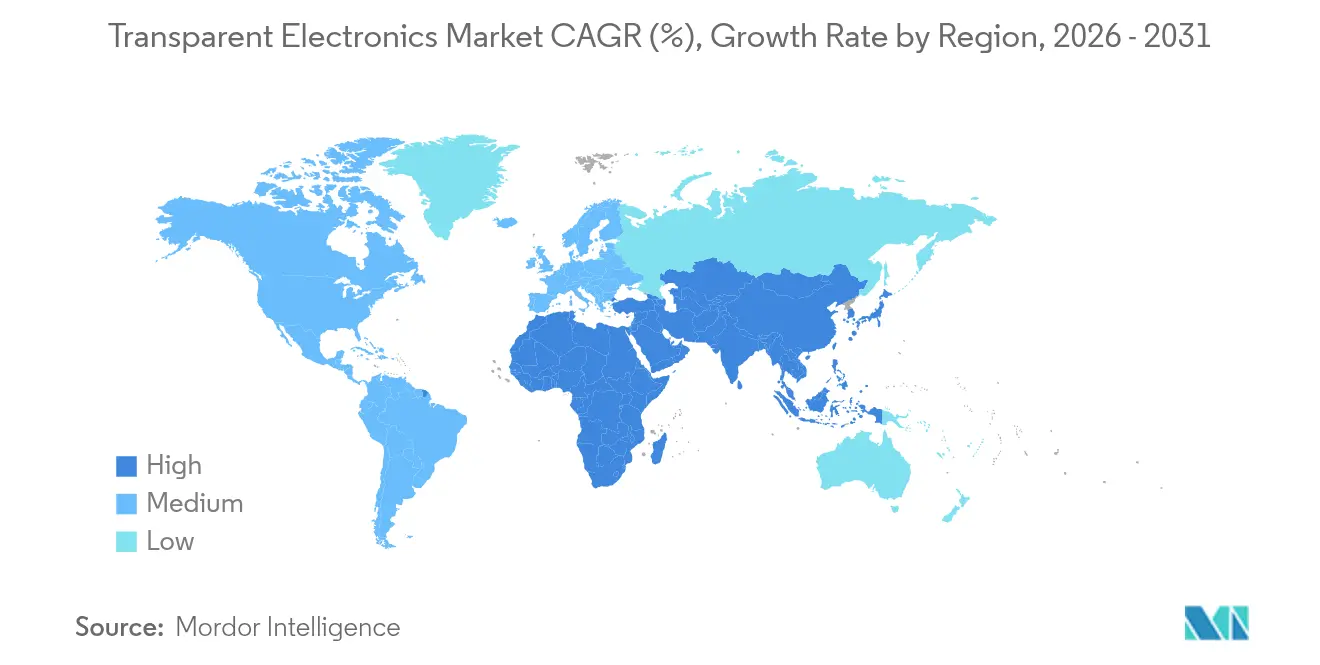

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

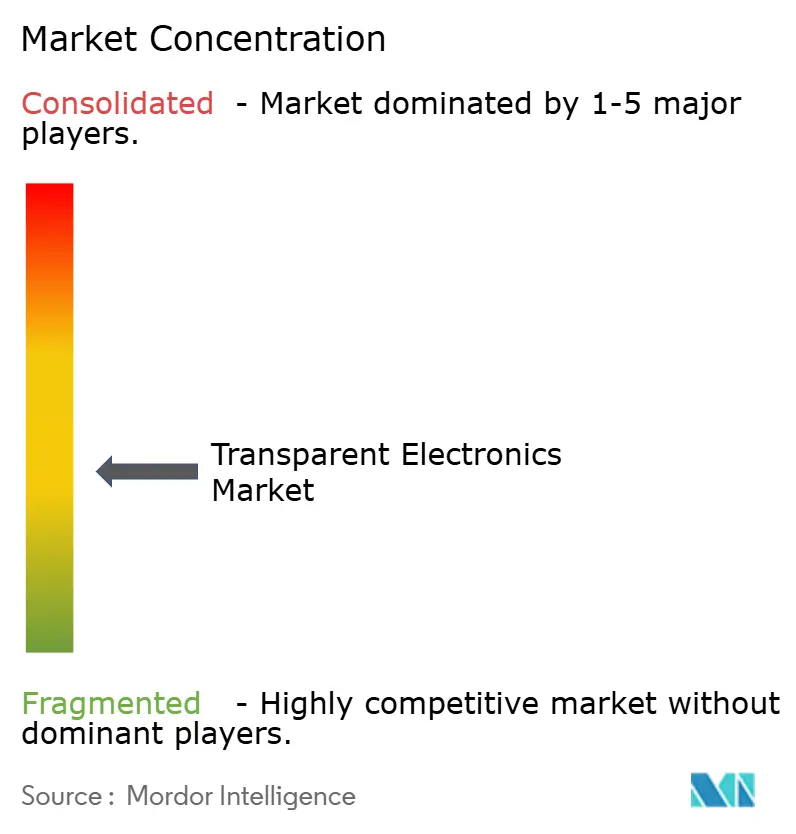

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transparent Electronics Market Analysis by Mordor Intelligence

The transparent electronics market size was valued at USD 2.78 billion in 2025 and estimated to grow from USD 3.37 billion in 2026 to reach USD 8.86 billion by 2031, at a CAGR of 21.30% during the forecast period (2026-2031). Product innovation that merges optical clarity with electronic functionality is shifting the technology from niche display uses toward mainstream roles in energy-smart buildings, advanced vehicle cockpits, and immersive retail. Regulatory pressure for net-zero construction, the electrification of transport, and rising demand for interactive commercial spaces are accelerating capital flows into transparent photovoltaic, micro-LED, and electrochromic platforms. Competitive advantage is increasingly determined by access to flexible materials and high-yield deposition processes rather than panel size alone. Manufacturers that diversify beyond indium tin oxide (ITO) and align with building-integrated photovoltaics (BIPV) or autonomous-vehicle electronics are positioned to capture the next wave of growth.

Key Report Takeaways

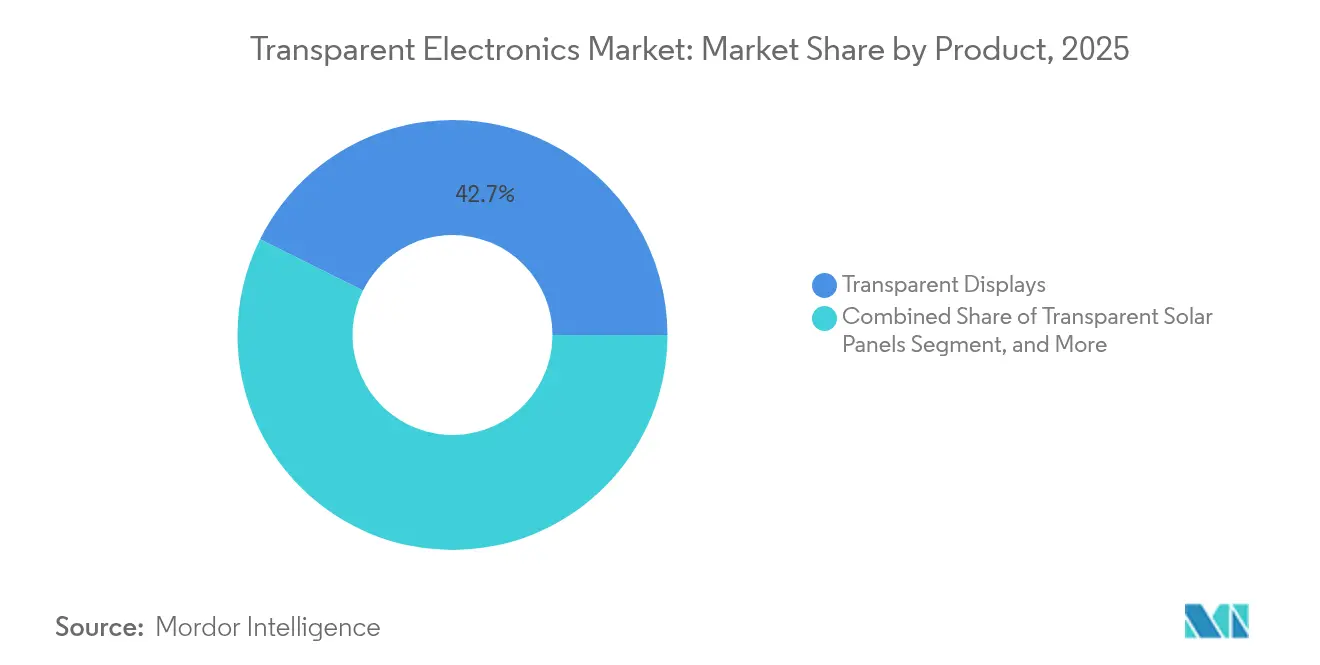

- By product, transparent displays led with 42.65% revenue share in 2025; transparent solar panels are projected to register the fastest CAGR at 25.05% through 2031.

- By material, indium tin oxide retained 51.35% share in 2025, while silver nanowire and metal mesh are advancing at 21.90% CAGR to 2031.

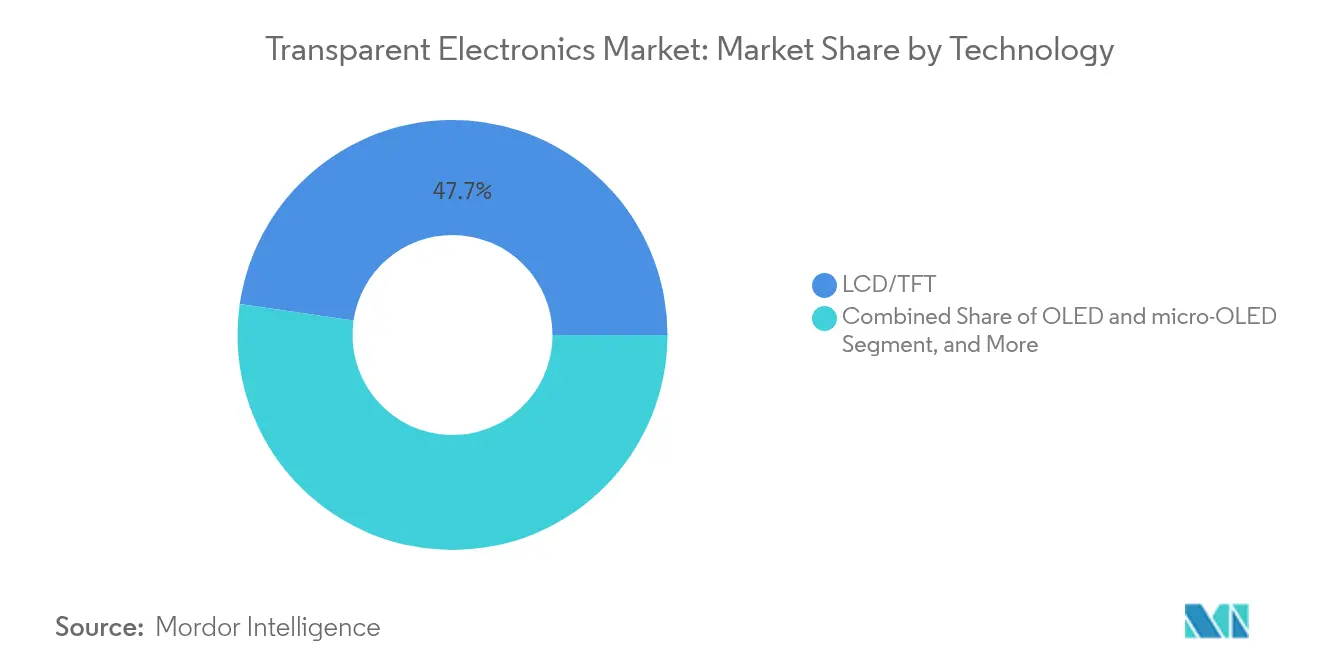

- By technology, LCD/TFT commanded 47.70% of the transparent electronics market size in 2025; OLED and micro-OLED are on track for a 22.80% CAGR to 2031.

- By end-user application, consumer electronics held 54.05% of the transparent electronics market size in 2025; building and infrastructure is forecast to expand at 25.10% CAGR to 2031.

- By geography, Asia Pacific captured 42.80% of transparent electronics market share in 2025, while the Middle East and Africa region is anticipated to grow at 22.15% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Transparent Electronics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-zero building codes accelerating smart-window adoption | +5.3% | European Union; spillover to North America | Medium term (2-4 years) |

| Rapid uptake of head-up displays in autonomous and EV cockpits | +4.8% | North America, Europe, China, Japan | Short term (≤ 2 years) |

| AR-enabled transparent retail signage surge in Asia’s tier-1 cities | +3.7% | Asia Pacific | Short term (≤ 2 years) |

| Building-integrated PV mandates spurring transparent solar panels | +4.2% | China; wider Asia Pacific | Medium term (2-4 years) |

| Wearable medical sensors requiring flexible transparent conductors | +3.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Net-zero building codes driving smart-window integration

European legislation that mandates nearly zero-energy performance for all new structures by 2030 is pushing architects toward electrochromic glazing that dynamically modulates solar gain. Pilot installations across Germany and Scandinavia have shown cooling-energy cuts exceeding 20%, and newer liquid-flow electrochromic designs added the ability to shift interior temperatures 5 °C seasonally[1]Yifeng Huang, “A Novel Liquid Flow Electrochromic Smart Window for All-Year-Round Dynamic Photothermal Regulation,” Energy and Environmental Science, rsc.org. Integration with building-automation systems is becoming standard, opening revenue streams for sensor and controls suppliers alongside panel manufacturers. Medium-term growth prospects are reinforced by funding under national renovation programs, which reserve dedicated budgets for envelope upgrades that include smart windows.

Autonomous vehicles accelerating transparent display adoption

Automakers are turning to large-format transparent head-up displays (HUDs) that project navigation, driver-assist, and infotainment data directly onto windshields. Recent micro-LED prototypes have achieved 85% transparency while retaining 1,000-nit brightness, overcoming prior glare limitations in variable daylight. This capability satisfies stringent driver-distraction and safety norms in the United States, Japan, and the EU, triggering design wins in mid-segment electric vehicles slated for 2026 release. Short-term demand is amplified by the transition to autonomous Level 3 functions, which require larger visual fields for system-status information.[2] Samsung Electronics, “AI-Driven and Sustainable Signage Solutions Earn Top Awards at ISE 2025,” news.samsung.com

Retail transformation through transparent digital signage

Flagship stores across Shanghai, Tokyo and Seoul are deploying augmented-reality retail walls that overlay dynamic content on physical merchandise without obstructing the view. The approach converts window space into interactive sales channels that raise foot-traffic conversion, especially in luxury goods and automotive showrooms. Rapid panel turnover cycles, driven by seasonal promotions, create repeat demand for lightweight, easy-change micro-LED glass modules. Category growth benefits from favorable shop-fittings regulations that classify transparent signage as façade enhancement rather than structural modification.

Building-integrated photovoltaics expanding transparent solar innovation

China’s BIPV quota that links commercial-property permits to rooftop or façade solar capacity is reshaping architectural glass procurement. Tandem perovskite-organic cells have reached 12.3% efficiency at 30% transparency, making them viable for curtain-wall applications where daylighting is critical[3]University of Southern Denmark, “Transparent Tandem Solar Cell Hits 12.3% Efficiency,” pv-magazine.com. Suppliers able to laminate photovoltaic layers within standard IGU formats are forming joint ventures with local façade contractors, accelerating market penetration over the next four years.

Restraints Impact Analysis of Transparent Electronics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Indium price volatility and supply concentration | −2.8% | Global; highest impact in Asia Pacific | Short term (≤ 2 years) |

| Low-yield scaling of large-area transparent OLED panels | −2.3% | Global manufacturing hubs | Medium term (2-4 years) |

| E-waste rules on heavy-metal oxide films | −1.7% | European Union | Medium term (2-4 years) |

| High CapEx for magnetron sputtering and ALD equipment | −1.9% | Global; emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Indium supply vulnerabilities threatening production stability

ITO remains the workhorse transparent conductor, yet more than half of refined indium originates from a single country, exposing panel producers to sudden spot-price swings above 30% per annum. These spikes compress display-maker margins and delay capacity-expansion decisions. Materials firms are responding with silver-nanowire alternatives that exhibit sub-30 Ω/sq resistance at 90% transmittance while tolerating 1,000 bending cycles[4]DuPont, “Activegrid Silver-Nanowire Films Advance Flexible Transparent Electronics,” dupont.com. The transition, however, requires new curing temperatures and patterning chemistries, prolonging qualification cycles for high-volume production.

Yield losses escalate sharply when transparent OLED panels exceed 30-inch diagonals, driven by particle contamination and non-uniform organic deposition. Premium interior-design installations carry price tags up to USD 60,000 for a 55-inch panel, restricting volume adoption. Ongoing R&D focuses on hybrid laser-vacuum encapsulation to minimize moisture ingress, but scalable commercial solutions are unlikely before 2027. In the interim, suppliers segment the market into smaller consumer devices and high-margin architectural showcases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Transparent Electronics Market Segment Analysis

By Product:

Transparent solar panels disrupt energy integrationTransparent displays generated the largest revenue share in 2025 at 42.65%, yet transparent solar panels are projected to grow at a 25.05% CAGR to 2031, propelled by building codes that reward on-site generation. A Swiss venture introduced a 400 W glass-like BIPV module that blends into standard façades without altering exterior aesthetics. The transparent electronics market size for solar panels is forecast to reach USD 2.26 billion by 2031, reflecting their dual role as power generators and daylighting surfaces. Product diversification now extends to transparent conductive films that underpin touch sensors and heaters, as well as rugged transparent ceramics for aerospace shielding. Smart-window units equipped with dynamic tinting continue to gain traction in commercial real estate, aided by operating-cost reductions that shorten payback periods to under five years in warm climates.

The transparent electronics market increasingly values interoperability between product categories. Emerging tandem solar cells share deposition tools with micro-LED backplanes, enabling multi-purpose manufacturing lines. Transparent sensors embedded in vehicle windshields are beginning to feed occupancy and environment data into advanced driver-assistance systems, illustrating how value migrates from stand-alone components to integrated functions.

By Material Type:

Silver nanowires challenge ITO dominanceIndium tin oxide accounted for 51.35% of transparent electronics market share in 2025, underscoring its entrenched position across LCD/TFT and touch-panel supply chains. Nevertheless, silver-nanowire composites and metal meshes are expected to erode this lead, climbing at 21.90% CAGR through 2031. Lab devices have demonstrated 26 Ω/sq sheet resistance at 90% transmittance, with only 10% resistance drift under 120% strain, making them viable for foldable phones and e-skin patches. Application-specific optimisation guides material choice. Conductive polymers such as PEDOT:PSS now coat injection-moulded plastic substrates for low-cost, flexible displays, while graphene manages heat and signal-uniformity challenges in wearable biosensors. Transparent ceramics secure niche demand in harsh-environment optics, and carbon-nanotube hybrids are emerging in electromagnetic-shielding layers where optical transparency is non-negotiable.

By Technology:

OLED innovations drive premium applicationsLCD/TFT remained the volume leader with 47.70% share in 2025 thanks to mature fabrication and cost efficiency. However, the transparent electronics market anticipates faster expansion in OLED and micro-OLED at a 22.80% CAGR to 2031, buoyed by their high contrast and thin-film form factors. Recent demonstrators integrate fingerprint and heart-rate sensing within the OLED stack, removing separate cover-glass components.

Quantum-dot emissive layers are improving colour purity, while transparent micro-LED tiles deliver 1,000-nit brightness for sunlit retail environments. Electrochromic and suspended-particle-device technologies, though outside the display mainstream, now achieve switching times under one second, enabling dynamic storefronts that alternate between full signage and clear window modes throughout the trading day.

By End-user Application:

Buildings emerge as growth catalystConsumer electronics held 54.05% of 2025 revenue, yet construction is poised to be the fastest-rising user segment at 25.10% CAGR. The transparent electronics market size for building applications is projected to surpass USD 1.24 billion by 2031 as smart façades combine power generation, daylight control and occupant-information displays. Electrochromic glazing linked to HVAC systems can cut annual cooling loads by 20% in temperate zones, bolstering facility-manager payback arguments.

Automotive suppliers weave transparent heaters into windshield HUDs to ensure all-weather performance, while agrivoltaic greenhouses employ semi-transparent photovoltaic roofs that balance light spectra for crop growth with electricity production. Healthcare is adopting stretchable transparent circuits in patches that unobtrusively track vital signs, signalling a move toward ambient, always-on medical diagnostics embedded in everyday surfaces.

Geography Analysis

APAC Transparent Electronics Market

Asia Pacific commanded 42.80% of 2025 revenue, anchored by high-volume fabs for displays and the world’s largest BIPV programme in China. Government incentives that link urban air-quality targets to renewable-energy capacity fuel adoption of transparent solar façades in megacities such as Shanghai and Shenzhen. Japanese and South Korean firms dominate OLED research, regularly showcasing prototypes that set new benchmarks in transmittance and pixel density.

North America and Europe Transparent Electronics Market

North America leverages its leadership in autonomous-vehicle software to accelerate demand for transparent HUDs and sensor-rich windshields. Building-energy rules vary by state, yet collectively favour electrochromic adoption in commercial retrofits. Europe’s strict 2030 climate agenda places smart glass and BIPV at the centre of renovation funding, driving a surge of cross-border partnerships between façade contractors and materials specialists.

MEA and LATAM Transparent Electronics Market

The Middle East and Africa is forecast to grow at 22.15% CAGR from 2026 to 2031 as smart-city investments integrate digital signage, adaptive shading and solar glass in landmark projects. Saudi Arabia’s Vision 2030 allocates multi-billion-dollar budgets to immersive heritage sites that blend transparent display walls with interactive content. Latin America represents an untapped frontier where abundant solar irradiance aligns with transparent PV adoption in urban high-rise developments, although supply-chain hurdles and financing costs temper near-term uptake.

Value Chain Analysis

Upstream value creation focuses on glass and polymer substrates, transparent conductors, and deposition and patterning consumables. Key inputs include architectural and automotive-grade glass from suppliers such as Corning and Saint-Gobain Sekurit, along with transparent conductor materials that still rely heavily on indium tin oxide (ITO), exposing the chain to indium price volatility and supply concentration. The move toward indium-free or reduced-indium stacks shows up in alternative TCO work (for example AZO) and in commercialization of silver-nanowire and hybrid films, such as CHASM licensing its AgeNT transparent conductive film technology to Mativ (January 2025) for heated-glass solutions.

Midstream manufacturing is driven by high-CapEx thin-film processes (magnetron sputtering, ALD, and OLED deposition), followed by lamination, encapsulation, and integration into finished modules such as transparent displays, smart glazing, and windshield systems. Bottlenecks center on yield losses in larger-format transparent OLED, contamination control, and long OEM qualification cycles for automotive and medical uses. Downstream, system integrators and installers connect transparent electronics to building automation, retail content platforms, and vehicle cockpit electronics, which raises the importance of cross-domain partnerships. This is illustrated by the December 2024 MOU among Eastman, Ceres Holographics, and Covestro to advance commercial production of holographic transparent display solutions for automotive HUDs, and by the February 2026 QuadAlliance (ZEISS, tesa, Saint-Gobain Sekurit, Hyundai Mobis) aimed at accelerating mass production of holographic windshield displays, spanning optical design, bonding/adhesives, glazing, and Tier-1 vehicle integration.

Competitive Landscape

The market structure is moderately concentrated, with the top five display panel makers, led by Samsung Display, LG Display and BOE Technology, accounting for the bulk of transparent OLED and micro-LED capacity. Materials leadership resides with Corning, AGC and NSG Group for glass substrates, while DuPont and Cambrios champion silver-nanowire conductive inks. Ecosystem collaborations are pivotal: Nanolumens and AUO Display Plus jointly unveiled a 64-inch transparent micro-LED wall in 2025 that targets high-traffic retail and museum venues. Start-ups focus on white-space opportunities. Ubiquitous Energy pursues visibly clear photovoltaic coatings, and Brite Solar targets greenhouse glazing that manages photosynthetically active radiation. Intellectual-property battles underline the stakes; 2025 saw patent litigation in the United States over AMOLED emitter stacks, signalling rising entry barriers for latecomers. Capital intensity for vacuum-deposition lines remains high, steering newcomers toward asset-light licensing or component niches rather than full-panel fabrication.

Transparent Electronics Industry Leaders

ClearLED Ltd

Corning Incorporated

Samsung Display Co., Ltd

LG Display Co., Ltd.

Brite Solar Inc.

- *Disclaimer: Major Players sorted in no particular order

Transparent Electronics Market Companies Covered in this Report

- BOE Technology Group Co., Ltd.

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Corning Incorporated

- AGC Inc.

- NSG Group (Pilkington)

- Saint-Gobain SA

- Ubiquitous Energy Inc.

- Brite Solar Inc.

- ClearLED Ltd.

- Panasonic Holdings Corp.

- Cambrios Technology Corp.

- Surmet Corporation

- 3M Company

- DuPont de Nemours Inc.

- PPG Industries Inc.

- Guardian Industries Holdings

- Shenzhen Nexnovo Technology Co., Ltd.

- Shenzhen AuroLED Technology Co., Ltd.

- Street Communication Inc.

- Apple Inc. (Transparent AR Glass R&D)

- JX Nippon Mining and Metals Corp.

- Heraeus Holding GmbH

- American Elements Corp.

Market Opportunities and Future Outlook

A key whitespace is scaling indium-reduced and indium-free transparent electrodes that can meet large-area, high-uniformity requirements while fitting industrial toolchains. Academic and pre-commercial results for aluminum-doped zinc oxide (AZO) made via spatial ALD, including low sheet resistance at high transmittance on large substrates, suggest an approach that aligns with manufacturable, high-throughput deposition rather than lab-only processes. This opportunity is supported by restraints already visible in the ecosystem, including indium supply vulnerabilities and the CapEx burden of sputtering/ALD equipment, which together increase the value of electrode stacks and process flows that reduce material risk and improve line yields.

Demand-side pull is broadening beyond showcase installations into repeatable deployment models across mobility, retail, and buildings, creating room for suppliers that package transparent electronics as integrated systems (display plus optics plus bonding plus control software) rather than as panels alone. Automotive windshield display roadmaps are also pushing ecosystem alignment, evidenced by the QuadAlliance formed in February 2026 to industrialize holographic windshield displays, and by the December 2024 Eastman-Ceres Holographics-Covestro collaboration targeting automotive HUD-ready solutions. On the capacity and capability front, next-generation OLED investments can function as enabling infrastructure for advanced form factors; LG Display announced a 1.1 trillion won investment in April 2026 for a sixth-generation OLED line expansion at Paju, indicating continued capital allocation to display process upgrades that can be adapted to higher-transparency and new interface concepts as adoption programs mature across end users.

Recent Industry Developments in Transparent Electronics Market

- June 2026: Corning and AUO demonstrated a dual-sided 17.3-inch transparent microLED display at SID Displayweek 2026 using Corning fusion-formed glass substrates. The prototype showed how glass and backplane choices can be engineered together to improve optical clarity and robustness, supporting commercialization of transparent microLED for premium retail and mobility interfaces.

- October 2025: LG Display reported increasing transparent OLED light transmittance to over 45%. Higher transparency improves suitability for window-like applications in retail, transportation, and architectural integration, and it raises the performance bar for competing transparent OLED and microLED solutions.

- December 2024: LG Electronics announced the global commercial launch of the 77-inch LG SIGNATURE OLED T, a transparent and true wireless 4K OLED TV. A commercial-scale consumer product helps validate supply chains for transparent OLED modules and electronics integration, with spillover into signage and showroom deployments that use similar transparency and switching concepts.

Transparent Electronics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market is defined as revenue from transparent electronic components and finished devices that keep high optical clarity while still performing an electronic function, and that are sold into end users across major regions.

Scope exclusions: We exclude refurbished units and most aftermarket retrofit films or coatings that are applied post-sale as add-ons.

Segments Covered in This Report

- By Product

- Transparent Displays

- Transparent Solar Panels

- Smart Windows/Smart Glass

- Transparent Conductive Films

- Transparent Ceramics and Aluminum

- Transparent Sensors and Others

- By Material Type

- Indium Tin Oxide (ITO)

- Alternative TCOs (AZO, FTO)

- Silver Nanowire and Metal Mesh

- Carbon-Based Nanomaterials (Graphene, CNT)

- Conductive Polymers (PEDOT:PSS)

- By Technology

- LCD/TFT

- OLED and micro-OLED

- Quantum-Dot and micro-LED

- Thin-Film Photovoltaic (CIGS, Perovskite)

- Electrochromic and SPD

- By End-user Application

- Consumer Electronics

- Automotive and Transportation

- Building and Infrastructure

- Energy and Utilities (BIPV, Agrivoltaics)

- Aerospace and Defense

- Healthcare and Wearables

- Retail and Digital Signage

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics (Denmark, Sweden, Norway, Finland)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a common fact base on where transparent electronics are actually being used and produced today. We relied on public sources such as the US Department of Energy publications, International Energy Agency datasets (for solar context), USITC and UN Comtrade trade statistics, IEEE and other peer-reviewed journals, and WIPO patent databases to understand technology maturity and adoption signals.

We also reviewed company annual reports, investor presentations, product datasheets, and press releases to pin down product definitions and typical price ranges, then checked import-export mix when trade codes were usable using a shipment-level import/export database. These sources helped us set realistic assumptions for volumes, pricing movement, and regional demand splits, and then keep the model aligned with what is visible in public records. The sources listed here are illustrative, and many other references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to pressure-test what qualifies as transparent electronics in real procurement and how buyers pay for it, whether at the component level or as integrated device pricing. We spoke with a mix of component suppliers, device makers, system integrators, and downstream adopters across APAC, EMEA, and the Americas, then re-checked assumptions when responses showed large variance by application.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 45% |

| Mid tier: 44% | Functional/Unit leaders: 35% | EMEA: 34% |

| Smaller Players: 20% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down structure where known demand pools were reconstructed by application, and then translated into revenue using adoption rates and average selling prices appropriate for transparent form factors. In practice, our team mapped indicators such as transparent display area shipped, smart window glazing installations, transparent conductive film usage intensity, see-through PV deployment activity, and typical optical transmittance performance requirements that affect usable material choices.

To keep totals realistic, the outputs were corroborated with selective bottom-up approximations such as supplier roll-ups for key materials, sampled ASP times volume checks for high-visibility applications, and channel feedback on what portion of projects move from pilot to scaled orders. Where bottom-up visibility was incomplete, gaps were handled by using conservative penetration bands anchored to interview feedback, then cross-checked against trade and patent momentum.

For forecasting, scenario analysis was used because adoption can move quickly when costs fall and when new product launches happen in displays and smart glazing. Key variables were projected using published capacity expansion signals, building and auto production outlooks, and expert inputs on ASP erosion and yield improvements. The final trajectory was then reviewed to match the practical pace of commercialization.

Data Validation & Update Cycle

Validation was done through multiple passes that compare the model against independent signals, followed by checks for outlier pricing, unrealistic penetration jumps, or regional splits that do not match known manufacturing footprints. When a mismatch was found, we revisited assumptions and, where needed, re-contacted industry participants to confirm whether the change was real or just a timing issue in the data.

Before sign-off, the work is reviewed by another analyst to confirm that definitions, math, and conversions are consistent across the full time series. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity additions, policy changes affecting smart building deployments, or notable shifts in display technology roadmaps. Right before delivery, a final review pass is completed so clients receive the most current view.

Mordor Intelligence's Transparent Electronics Market Sizing Compared With Other Published Estimates

Published market sizes for transparent electronics often vary because the category sits across displays, glazing, and energy, and each publisher draws the inclusion line differently. Differences also come from pricing level choices, component versus finished device, exchange-rate timing, and whether pilot projects are counted like scaled demand.

The table shows a clear spread that mainly comes from scope and pricing treatment, and then from the forecast window used. In the Mordor Intelligence model, only newly manufactured transparent electronic components and finished devices meeting a high optical transmittance threshold are counted. Refurbished units plus most aftermarket retrofit films are not treated as market revenue, which can move totals versus estimates that bundle add-on coatings or broader smart glass spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.37 B (2026) | |

| Industry Publisher A | USD 2.60 B (2026) | Uses a narrower product basket that centers on transparent displays and windows, and pricing is closer to factory-gate levels without consistently normalizing channel markups across regions. |

| Industry Publisher B | USD 2.14 B (2025) | Uses an earlier base year and applies a broader application list but provides limited clarity on transmittance thresholds and how pilot deployments are filtered, which can suppress the counted revenue in early years. |

Overall, the gap pattern is best explained by what gets included, how pricing is defined, and how early-stage demand is handled. When the scope is tied to clear product rules and the pricing logic is kept consistent across regions, the final number becomes easier to trace and repeat during updates, even when the market is moving fast.

Key Questions Answered in the Report

What is the current value of the transparent electronics market?

The transparent electronics market size reached USD 3.37 billion in 2026 and is projected to hit USD 8.86 billion by 2031.

Which segment is expanding the fastest?

Transparent solar panels are forecast to grow at a 25.05% CAGR between 2026 and 2031 as building-integrated photovoltaics gain policy support.

Why is Asia Pacific so dominant?

The region hosts the largest display-fabrication clusters, aggressive BIPV mandates in China and rapid retail adoption of transparent digital signage, giving it 42.80% revenue share in 2025.

How are material shortages being addressed?

Manufacturers are diversifying beyond indium tin oxide by adopting silver-nanowire and metal-mesh conductors that deliver comparable transparency with greater flexibility.

What role do smart windows play in energy efficiency?

Electrochromic glazing integrated with building-management systems can cut cooling energy use by about 20%, supporting EU net-zero construction directives.

Are transparent electronics limited to displays?

No. Applications now include solar-generating curtain walls, windshield heaters, stretchable medical sensors and greenhouse roofs, reflecting a shift toward multifunctional surfaces.

Page last updated on: