Opto-Isolator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

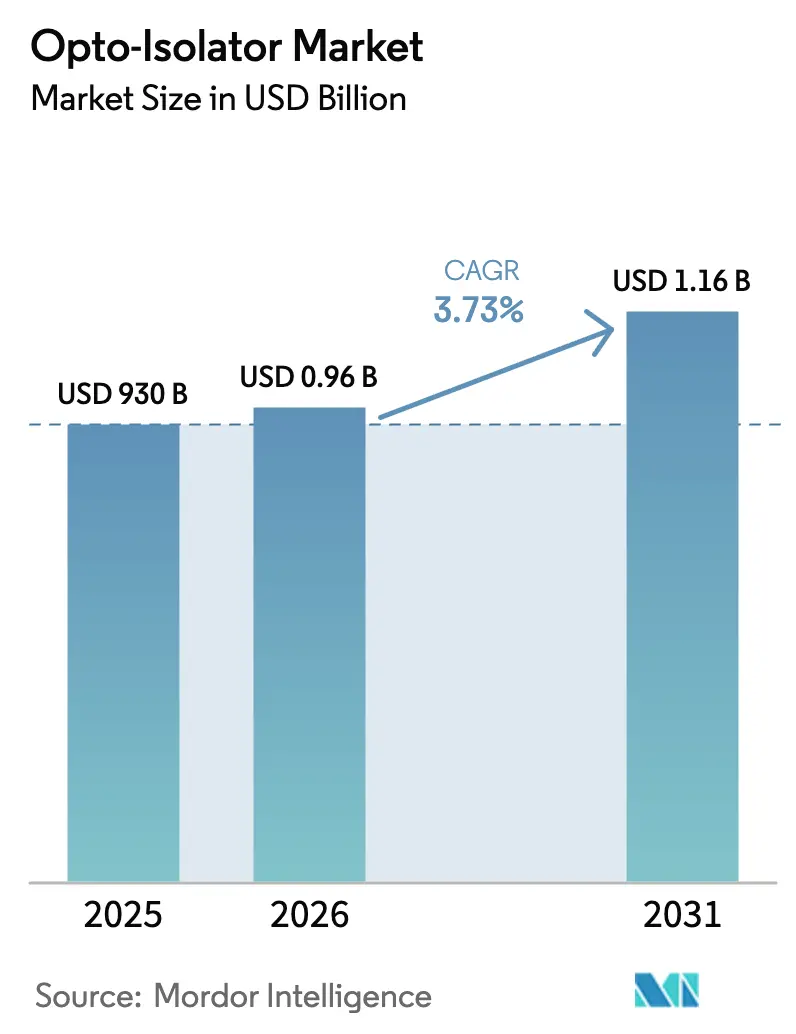

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

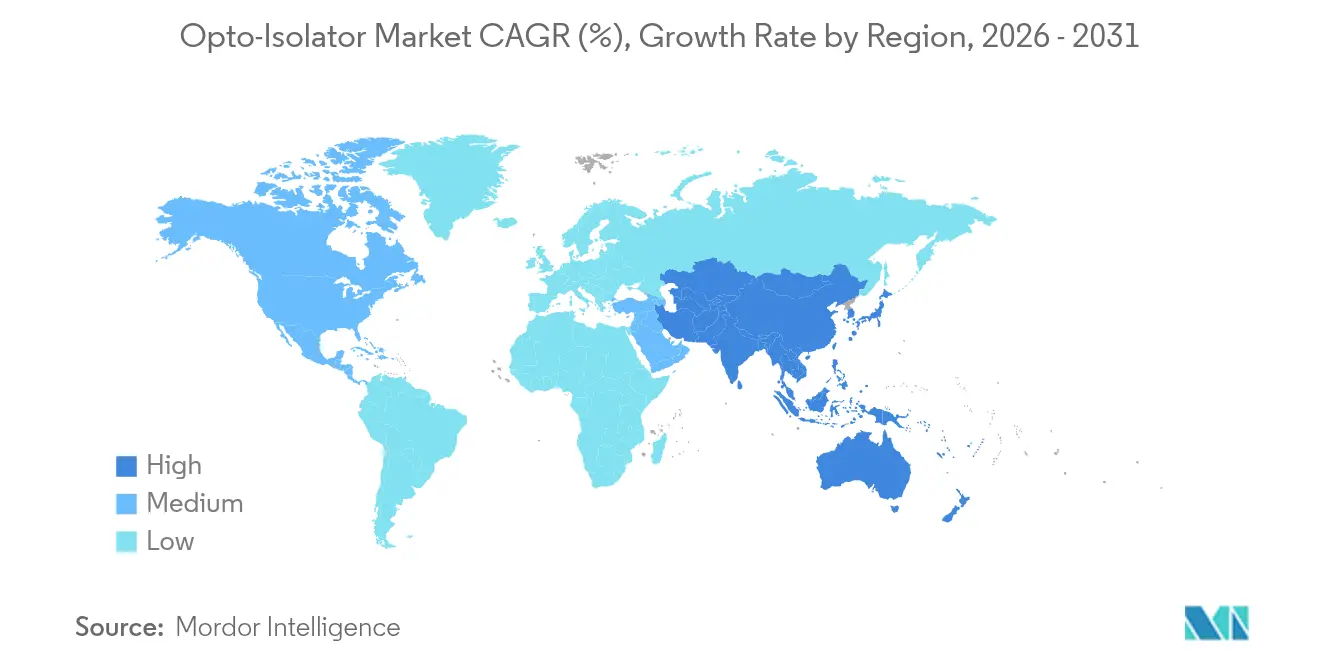

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Opto-Isolator Market Analysis by Mordor Intelligence

The opto-isolator market size was valued at USD 930 million in 2025 and estimated to grow from USD 964.69 million in 2026 to reach USD 1.16 billion by 2031, at a CAGR of 3.73% during the forecast period (2026-2031). Growth stems from the widening adoption of high-voltage power electronics in electric vehicles and renewable energy systems, stricter galvanic-isolation mandates in industrial automation, and the steady build-out of global fiber-optic infrastructure. A gradual pivot from discrete devices to photonic-integrated solutions is reshaping competitive dynamics as makers race to shrink form factors and improve bandwidth. North America keeps its lead through deep telecom investments and early moves in quantum computing, while Asia Pacific provides the fastest incremental demand. Competitive activity shows larger semiconductor firms bundling full isolation solutions, even as specialist vendors defend niches that demand isolation beyond 50 dB. Headwinds come from digital isolators that promise size and power advantages for some designs yet fall short at multi-gigahertz frequencies where optical devices excel.

Key Report Takeaways

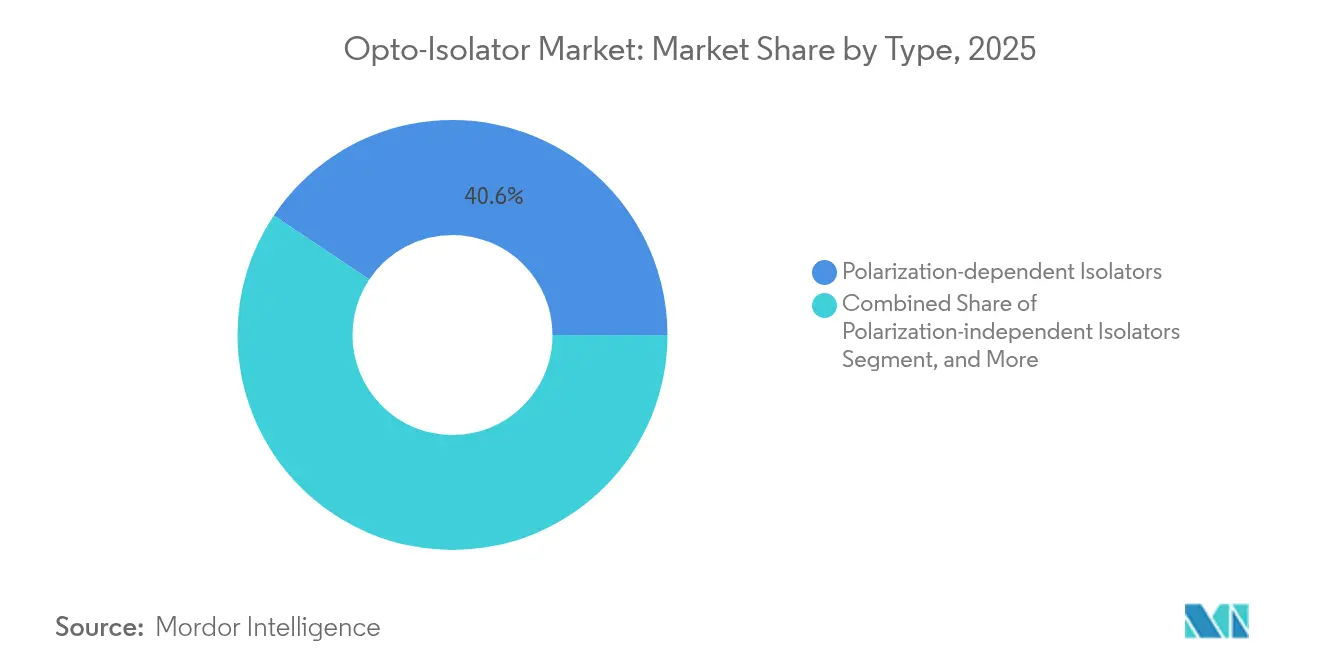

- By product type, polarization-dependent isolators led with 40.62% revenue share in 2025; photonic-integrated isolators are forecast to expand at a 4.12% CAGR to 2031.

- By power level, low-power devices (<1 W) accounted for 47.35% of the opto-isolator market share in 2025, while >10 W high-power units are projected to grow at 4.29% through 2031.

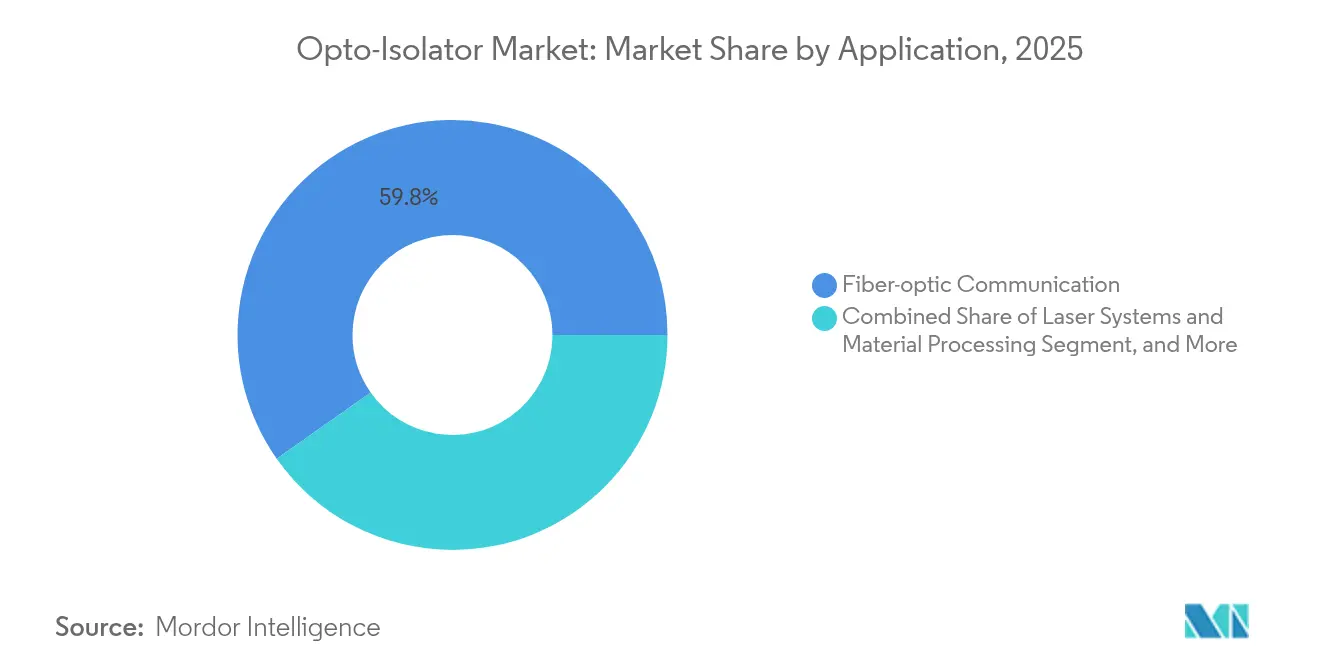

- By application, telecommunications held 59.76% of the opto-isolator market size in 2025; RF and microwave photonics is advancing at a 4.88% CAGR between 2026-2031.

- By end-user industry, telecom and data centers captured 54.28% of the opto-isolator market size in 2025 as automotive and EV rises at a 4.92% CAGR to 2031.

- By geography, North America commanded 31.62% of the global opto-isolator market share in 2025, whereas Asia Pacific is expanding at a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Opto-Isolator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of high-voltage power electronics in EV and renewables | +1.2% | North America, Europe, China | Medium term (2-4 years) |

| Expansion of fiber-optic telecom networks and hyperscale data centers | +0.9% | Global, high in North America & Asia Pacific | Short term (≤ 2 years) |

| Regulatory push for reinforced galvanic isolation in industrial automation (IEC 62368-1) | +0.7% | Europe, North America, Japan | Medium term (2-4 years) |

| Integration of isolators into photonic integrated circuits (PICs) | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Emergence of quantum-photonics instrumentation requiring ultra-low-noise isolation | +0.4% | North America, Europe, China | Long term (≥ 4 years) |

| Adoption in satellite laser-communication modules for space platforms | +0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of High-Voltage Power Electronics in EV and Renewables

Electric-drive platforms and utility-scale renewables have raised isolation voltages to 900 V in battery management and inverter stages. Suppliers responded with 5 kVrms opto-relays such as Toshiba’s TLX9152M, rated for 400 V battery strings and qualified to AEC-Q101. The shift from traditional LEDs-plus-photodiode couplers to semiconductor relays extends lifetime, widens temperature operating windows, and simplifies automotive qualification. As global EV sales accelerate, the opto-isolator market records stable volume orders across traction inverters, onboard chargers, and stationary energy storage converters.

Expansion of Fiber-Optic Telecom Networks and Hyperscale Data Centers

Global 5G backhaul, submarine cables, and hyperscale data-center interconnects routinely specify isolation above 40 dB and insertion loss below 0.5 dB for lasers operating between 1310 nm and 1610 nm. Carriers and cloud operators prioritize higher bandwidth density, driving volume purchases of inline fiber isolators that protect transmitters from back reflection. Molex anticipates robust demand for high-speed connectivity gear through 2025 as AI workloads surge, bringing thermal-management upgrades that complement advanced isolation.

Regulatory Push for Reinforced Galvanic Isolation in Industrial Automation

IEC 62368-1 superseded legacy IEC 60950-1 and IEC 60065 in 2024, raising the bar for reinforced isolation across factory automation. Industrial equipment must now pass 1.5 kVrms or 2.25 kVdc without flash-over, triggering redesigns that favor opto-isolators able to survive differential surges and common-mode transients over wide operating temperatures.[1]Texas Instruments, “Overview of Isolation Standards and Certifications,” ti.comVendors integrate isolation with gate drivers and current sensors to cut board area and certification time, which lifts the opto-isolator market in motion control, robotics, and smart-grid protection equipment.

Integration of Isolators into Photonic Integrated Circuits

Chip-scale non-magnetic isolators released by Yale operate across a 2 THz optical bandwidth, setting new benchmarks for on-chip back-reflection suppression.[2]Yale Engineering, “Revolutionary Chip-Scale Optical Isolator,” engineering.yale.edu Further demonstration on lithium niobate and indium-phosphide platforms signals a long-term evolution in which isolation, modulation, and detection co-reside on the same die. As packaging hurdles fade, the opto-isolator market benefits from lower cost per channel and higher reliability compared with micro-assembled bulk optics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution threat from digital / capacitive / transformer isolators | -0.8% | Global | Medium term (2-4 years) |

| High manufacturing cost of polarization-independent isolators | -0.6% | Global, acute in price-sensitive regions | Short term (≤ 2 years) |

| Supply-chain pinch on rare-earth garnets for Faraday rotators | -0.5% | Global, focus Asia Pacific | Medium term (2-4 years) |

| Thermal-stability limits in >10 W ultrafast-laser isolators | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution Threat from Digital, Capacitive, or Transformer Isolators

Capacitive and transformer isolators deliver compact footprints and lower quiescent current, which is especially appealing in automotive domain controllers and industrial sensors. Analog Devices reported 2.4 mA typical current against 10 mA for optocouplers in xEV designs. Skyworks introduced 6 kV capacitive isolators that continue operation after a single fault, narrowing performance gaps in safety certifications. While optical isolation retains superiority at multi-gigahertz rates and in high common-mode noise, pricing pressure in low-speed links could slow optoisolator market adoption.

High Manufacturing Cost of Polarization-Independent Isolators

Polarization-independent variants require precision alignment and exotic magneto-optic crystals, driving higher cost per unit compared with polarization-dependent products. Complexities arise further in high-power designs where thermal management dictates the use of ceramic housing and low-stress bonding. Automation and yield learning curves continue to improve, yet premium pricing still limits uptake in cost-sensitive consumer electronics. The opto-isolator industry, therefore, balances performance against total cost, encouraging dual-sourcing strategies that include cheaper polarization-dependent devices where feasible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polarization-Dependent Holds the Lead, Photonic-Integrated Picks Up Pace

Polarization-dependent devices controlled 40.62% of 2025 revenue, underpinning mainstream fiber networks that prize low insertion loss and cost. These isolators incorporate a Faraday rotator and polarizer pair inside a micro-cavity glass tube to block counter-propagating light with isolation near 35 dB. Their volume runs in the tens of millions, sustaining the opto-isolator market through steady replacement cycles in metro and long-haul systems. Competition centers on refining coatings and magnet assemblies that permit higher operating temperatures without raising loss.

Photonic-integrated isolators register the highest growth at a 4.12% CAGR from 2026-2031. Prototypes from Yale and Harvard marry non-magnetic modulation with waveguide engineering to create sub-millimetre footprints that slot directly into photonic integrated circuits. Early adopters in LiDAR and quantum instruments pursue bandwidth above 1 THz and isolation beyond 50 dB, valuing small size over absolute loss. As foundries add magneto-optic or opto-acoustic layers to silicon photonics lines, the opto-isolator market size for on-chip solutions is projected to multiply in the next decade.

Faraday-rotator free-space isolators keep a presence in scientific lasers and fibre amplifiers where isolation above 45 dB and aperture up to 6 mm are typical. TGG-based designs lower optical absorption and broaden wavelength coverage, attracting research labs and lithography tool makers. Fibre inline variants dominate telecom segments, while free-space products satisfy high-power requirements in additive manufacturing and ophthalmic systems. The overall opto-isolator market therefore spans a diverse mix of polarizer concepts, each optimised for power, bandwidth, or integration.

By Power Level: Low-Power Dominates, High-Power Climbs Fast

Low-power parts under 1 W form 47.35% of 2025 shipments, anchored in transceiver modules, EDFA pump lasers, and coherent pluggables. They promise under 0.5 dB insertion loss, making them indispensable for 400 G and 800 G datacom links. Cost efficiency, high volume, and maturing design rules assure their top position in the opto-isolator market through 2030.

High-power variants above 10 W grow the fastest at 4.29% as fibre-laser cutters, medical surgery lasers, and extreme-ultraviolet metrology expand. Newly released devices handle 50 W continuous optical power with <35 dB isolation, leveraging collimated beam geometries that spread heat over larger ferrite areas. Designers integrate thermally conductive metal-matrix sleeves and water-cooling blocks to mitigate hot spots, which broadens revenue streams for component makers.

Medium-power 1-10 W units occupy balanced ground in amplifiers and diagnostic lasers. Compact 3 mm-diameter isolators rated at 10 W enter optical amplifiers for sensing and spectroscopy, combining small footprints with reliability curves meeting telecom-class lifetimes. As high-mix production grows, medium-power products anchor the opto-isolator industry supply chain, acting as a bridge between commodity telecom parts and bespoke laser isolators.

By Application: Telecom Commands, RF and Microwave Photonics Accelerates

Telecommunications retained 59.76% of 2025 revenue, underscoring the centrality of back-reflection protection in long-haul, metro, and data-center optics. Global 5G-standalone rollouts and 400ZR pluggable adoption continue to pull large order volumes that stabilize the opto-isolator market. Operators specify dual-stage isolators to meet forward error correction budgets as wavelengths crowd around the C-band.

RF and microwave photonics post the fastest 4.88% CAGR through 2031. The segment benefits from integrated microwave photonic circuits on thin-film lithium niobate that deliver tunable notch filters with rejection >60 dB. Isolators tailored for 20-40 GHz analogue front ends support electrically small antennas and photonic true-time-delay beamforming, elevating performance in phased-array radars and satellite gateways. These emerging uses lift the opto-isolator market beyond classical optical transport.

Laser machining, medical therapy, imaging, and distributed fibre sensing round out demand. Uptake in laser-based additive manufacturing underpins high-power isolator sales, while distributed fibre sensing calls for miniature inline isolators that withstand harsh field environments without compromise on reliability.

By End-User Industry: Telecom & Data Centers Dominate, Automotive and EV Surges

Telecom and data-center operators consumed 54.28% of 2025 shipments, reflecting unrelenting bandwidth growth and hyperscale capital investment. Pluggable optics for 400 G and beyond count on isolators to secure transmitter reflection budgets while conserving power envelopes. Continuous cloud adoption and AI clusters anchor future unit sales for the opto-isolator market.

Automotive and EV grow at 4.92% CAGR. Vehicle platforms raise isolation ratings for onboard chargers and traction inverters, prompting adoption of automotive-grade optocouplers qualified to 3.75 kVrms. Digital isolators are also replacing legacy LED couplers where higher speed and lifetime matter; nonetheless, optical devices continue to protect differential-current sensors and drive-by-wire modules, preserving a sizeable share of the opto-isolator market.

Industrial automation, renewable-energy power conversion, consumer electronics, medical diagnostics, aerospace, and defense contribute the remainder. Industrial robots and smart drives value reinforced isolation aligned with IEC 62368-1. Aerospace users seek radiation-tolerant, space-qualified models that survive vacuum thermal cycling.

Geography Analysis

North America led with 31.62% revenue in 2025 on the back of its advanced telecom backbone, quantum-computing R&D, and a robust defense sector that specifies isolation above commercial limits. Institutions such as Yale have pioneered chip-scale non-magnetic isolators that set benchmarks for next-generation on-chip optics. The United States also benefits from vertically integrated suppliers like Broadcom and Coherent that shorten design-to-manufacture cycles, reinforcing regional supply security for critical infrastructure.

Asia Pacific shows the fastest 5.92% CAGR from 2026-2031. China’s fiber-to-the-home push, 5G densification, and domestic photonic component ecosystem raise unit volumes in the opto-isolator market. Japanese and Korean makers complement growth through high-performance automotive and consumer optical electronics. Regional foundries in Taiwan and mainland China now offer silicon photonics production that embeds isolation on indium-phosphide or silicon-nitride platforms, cutting cost per channel and extending opto-isolator market reach to mass-market modules.

Europe retains a strong industrial and renewable-energy base, demanding stringent IEC-compliant isolation for automation and grid conversion. Research programs on integrated optics at institutions in Germany and the Netherlands cultivate ultracompact isolators for LIDAR and metrology. The Middle East and Africa, plus South America, remain smaller contributors today yet display rising investment in 5G and industrial modernization, foreshadowing future opto-isolator market opportunities as supply chains mature.

Competitive Landscape

The top five suppliers account for roughly 60% of global revenue, indicating moderate concentration. Broadcom commands a broad catalog breadth from 15 MBd to 25 MBd reinforced optocouplers that meet failsafe industrial insulation requirements.[3]Broadcom, “Optocoupler ACPL-x7xL,” broadcom.com Infineon widens its share by targeting traction inverters and industrial drives, leveraging robust failure-in-time data and high common-mode transient immunity. Toshiba focuses on EV battery management and photovoltaic string inverters through ruggedized optical relays.

Texas Instruments pushes opto-emulators that slot into legacy optocoupler footprints but replace LEDs with CMOS isolation cores, capturing platforms that seek higher speed and extended life. Skyworks and Analog Devices introduce capacitive or transformer alternatives to expand adjacent markets. Niche specialists such as Thorlabs and Coherent focus on scientific and high-power laser isolators up to 100 W, providing peak isolation above 55 dB for research labs and advanced manufacturing. New entrants align around photonic-integrated technology, hoping to upset incumbents by embedding isolation directly on PIC wafers.

Industry consolidation is visible as larger semiconductor vendors integrate gate drivers, current sensing, and reinforced isolation into single packages to simplify design flows. Meanwhile, collaborative research links academia and industry, accelerating transfer of non-magnetic isolator designs into foundry PDKs. Supply resilience for magneto-optic garnets remains a watchpoint; firms diversify sourcing to mitigate geopolitical risk, which indirectly shapes competitive positioning within the opto-isolator market.

Opto-Isolator Industry Leaders

Broadcom Inc.

Infineon Technologies

Toshiba Corporation

Semiconductor Components Industries, LLC

Littelfuse, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Broadcom launched high-speed optocouplers with reinforced insulation and 25 MBd data rates for IEC 62368-1-compliant factory automation.

- March 2025: Toshiba released the TLX9152M in-vehicle optical relay rated at 900 V output and 5 kVrms isolation for EV battery packs.

- February 2025: Yale University unveiled a chip-scale optical isolator with 2 THz bandwidth that strengthens photonic integrated circuit performance.

- January 2025: Skyworks presented Si86Sx digital isolators offering 6 kV isolation and high noise immunity for AI data servers and EV charging.

Global Opto-Isolator Market Report Scope

The opto isolator market involves the production and sale of opto isolators, which are electronic components that provide electrical isolation between different parts of a system while allowing data to pass through in the form of light. These components are essential in protecting sensitive electronics from voltage spikes and noise, ensuring system reliability and longevity. Opto isolators are widely used in industries such as telecommunications, automotive, industrial automation, and consumer electronics for signal transmission, electrical isolation, and protection in high-voltage environments.

The Opto-Isolator Market is segmented by type (polarization-dependent optical isolators, polarization-independent optical isolators), power level (low power, medium power, high power), application (fiber optic communication, laser systems, imaging systems, instrumentation, other applications), end-use industry (telecommunications, industrial, automotive, consumer electronics, medical, aerospace and defense, and other end-use industries), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Polarization-dependent Isolators |

| Polarization-independent Isolators |

| Faraday-rotator Isolators |

| Free-space Isolators |

| Fiber Inline Isolators |

| Photonic-integrated Isolators |

| Low Power (Less than 1 W) |

| Medium Power (1-10 W) |

| High Power (Above 10 W) |

| Fiber-optic Communication |

| Laser Systems and Material Processing |

| Imaging and Sensing Systems |

| Instrumentation and Test Equipment |

| RF and Microwave Photonics |

| Others |

| Telecom and Data Centres |

| Industrial Automation and Power Electronics |

| Automotive and EV |

| Consumer Electronics |

| Medical and Life Sciences |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Type | Polarization-dependent Isolators | |

| Polarization-independent Isolators | ||

| Faraday-rotator Isolators | ||

| Free-space Isolators | ||

| Fiber Inline Isolators | ||

| Photonic-integrated Isolators | ||

| By Power Level | Low Power (Less than 1 W) | |

| Medium Power (1-10 W) | ||

| High Power (Above 10 W) | ||

| By Application | Fiber-optic Communication | |

| Laser Systems and Material Processing | ||

| Imaging and Sensing Systems | ||

| Instrumentation and Test Equipment | ||

| RF and Microwave Photonics | ||

| Others | ||

| By End-user Industry | Telecom and Data Centres | |

| Industrial Automation and Power Electronics | ||

| Automotive and EV | ||

| Consumer Electronics | ||

| Medical and Life Sciences | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the opto-isolator market?

The opto-isolator market size stands at USD 964.69 million in 2026 and is projected to reach USD 1.16 billion in 2031.

Which segment holds the largest share of the opto-isolator market?

Polarization-dependent isolators lead with 40.62% revenue share, driven by widespread telecom deployment.

Which region shows the fastest growth in the opto-isolator market?

Asia Pacific posts the highest CAGR at 5.92% through 2031 due to 5G rollout, fiber-to-the-home expansion, and electronics manufacturing scale.

How are integrated photonic isolators impacting the opto-isolator market?

Integrated solutions promise smaller footprints and broader bandwidth, growing at 4.12% CAGR as non-magnetic designs mature.

What threat do digital isolators pose to the opto-isolator market?

Capacitive and transformer isolators offer lower power and smaller size in some low-frequency links, trimming the optical share where bandwidth headroom is not vital.

Which industries outside telecom are driving new demand for opto-isolators?

Electric vehicles, industrial automation, high-power laser machining, and quantum computing all require robust optical isolation to meet safety and performance targets.

Page last updated on: