Digital Phase Shifter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

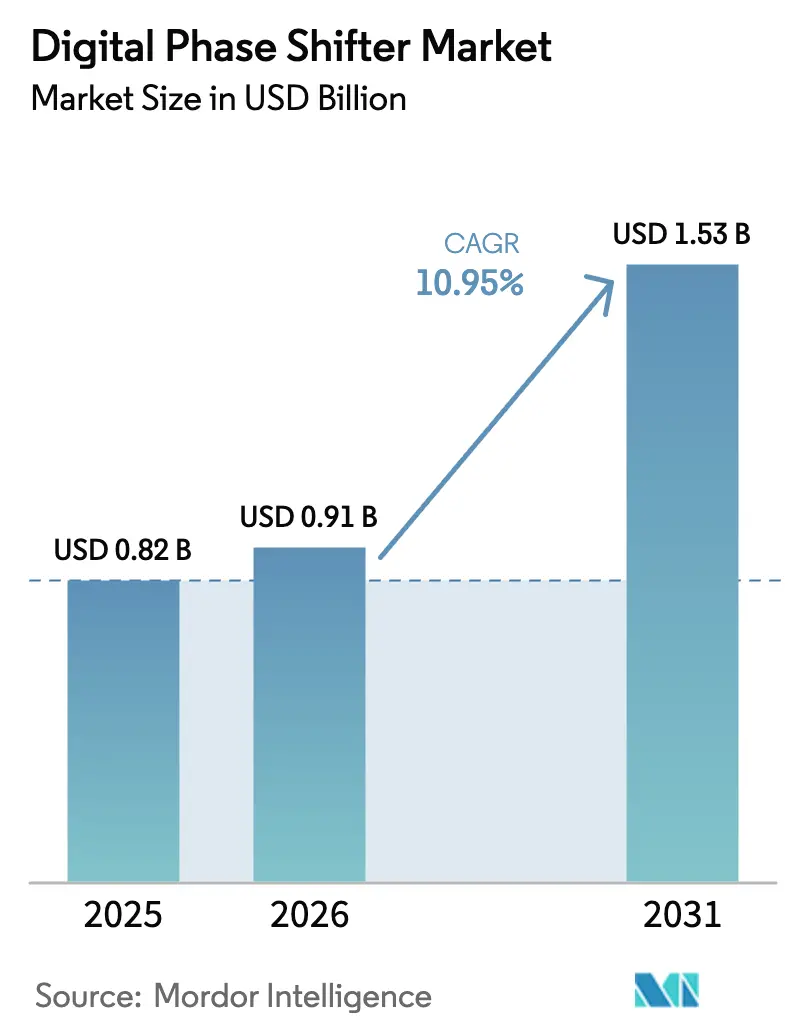

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 10.95% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Phase Shifter Market Analysis by Mordor Intelligence

The digital phase shifter market size was valued at USD 0.82 billion in 2025 and estimated to grow from USD 0.91 billion in 2026 to reach USD 1.53 billion by 2031, at a CAGR of 10.95% during the forecast period (2026-2031). Expanded 5G mmWave roll-outs, ongoing AESA radar upgrades, and the rapid adoption of imaging radar in next-generation vehicles collectively underpin this strong growth. Demand intensifies as massive-MIMO sites add hundreds of high-precision phase-shifter elements, while defense customers migrate from mechanically steered antennas to software-defined beam steering. Automotive tier-ones accelerate 4D radar programs that need sub-degree phase accuracy, and satellite operators standardize flat-panel antennas for Ku/Ka-band broadband links. Supply chain control of gallium and the expansion of vertically integrated RF front-end vendors further influence the digital phase shifter market.

Key Report Takeaways

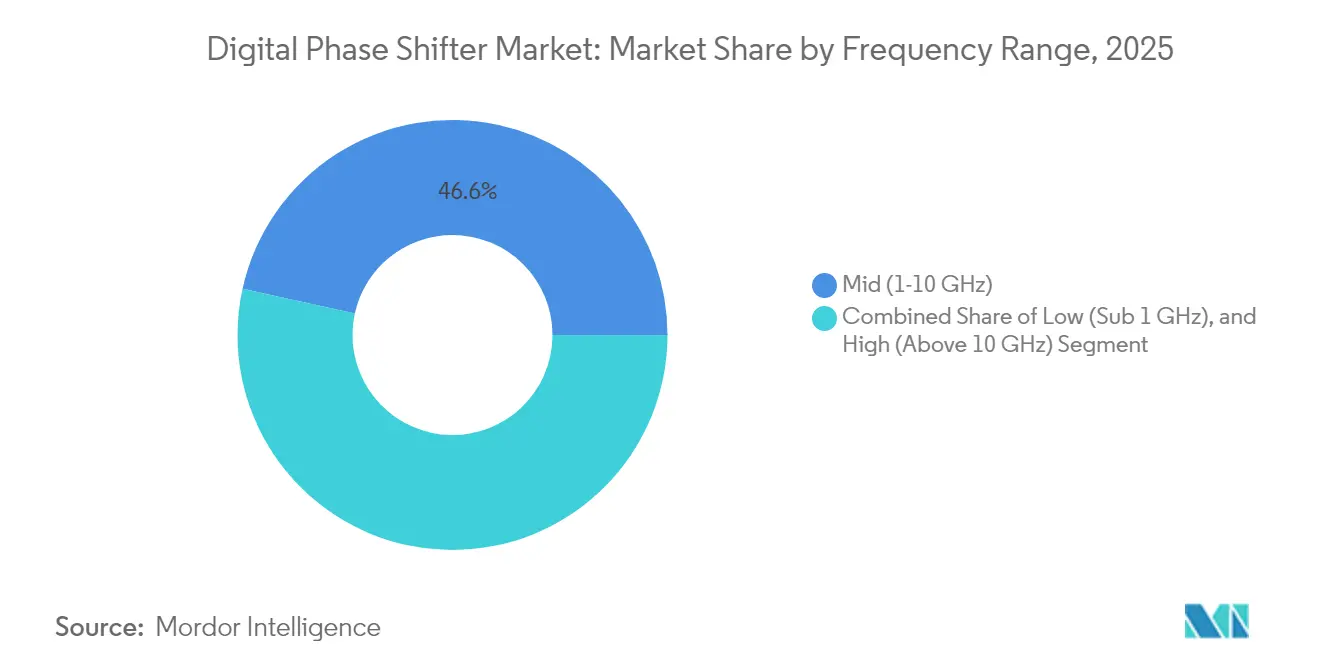

- By frequency range, the mid-range (1–10 GHz) segment accounted for 46.55% digital phase shifter market share in 2025, whereas the high-frequency (>10 GHz) band is forecast to post a 11.74% CAGR through 2031.

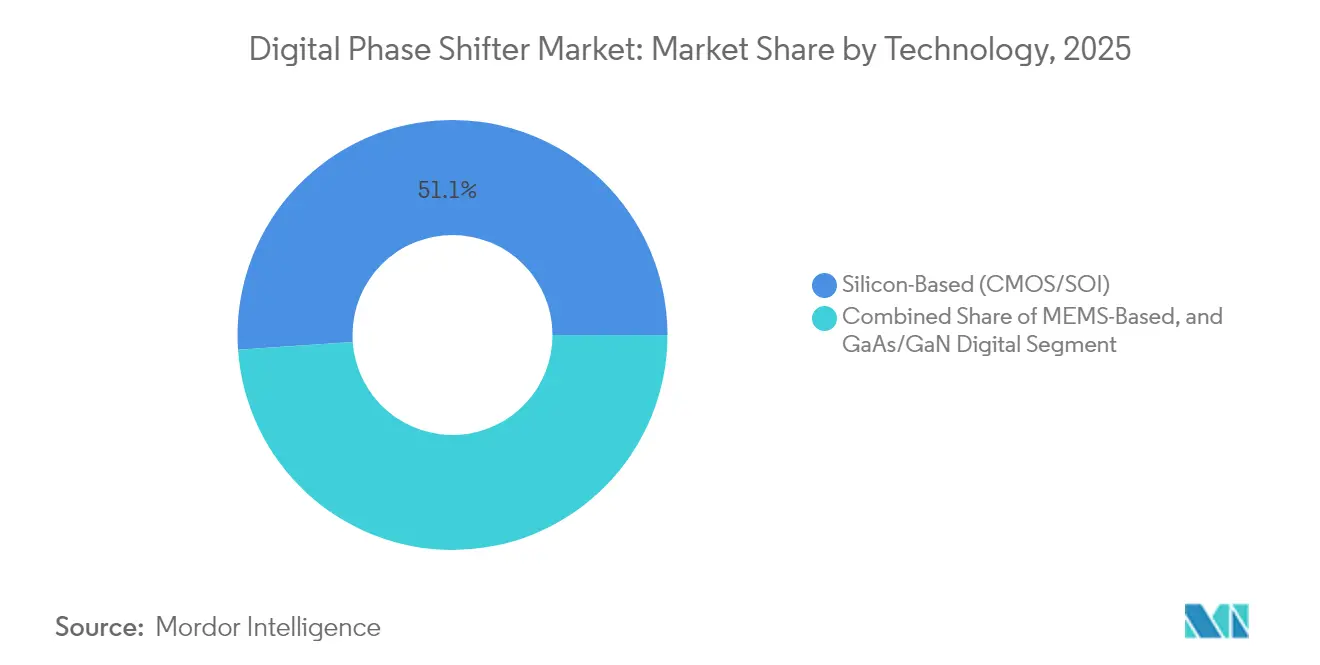

- By technology, silicon-based solutions held 51.10% revenue share in 2025; MEMS devices register the fastest 12.78% CAGR to 2031.

- By industry vertical, telecommunications led with a 54.10% stake in 2025, while automotive and transportation is expanding at 13.65% CAGR.

- By bit resolution, 4-bit devices captured 35.35% share in 2025, and the 7-bit-and-higher class records an 11.45% CAGR.

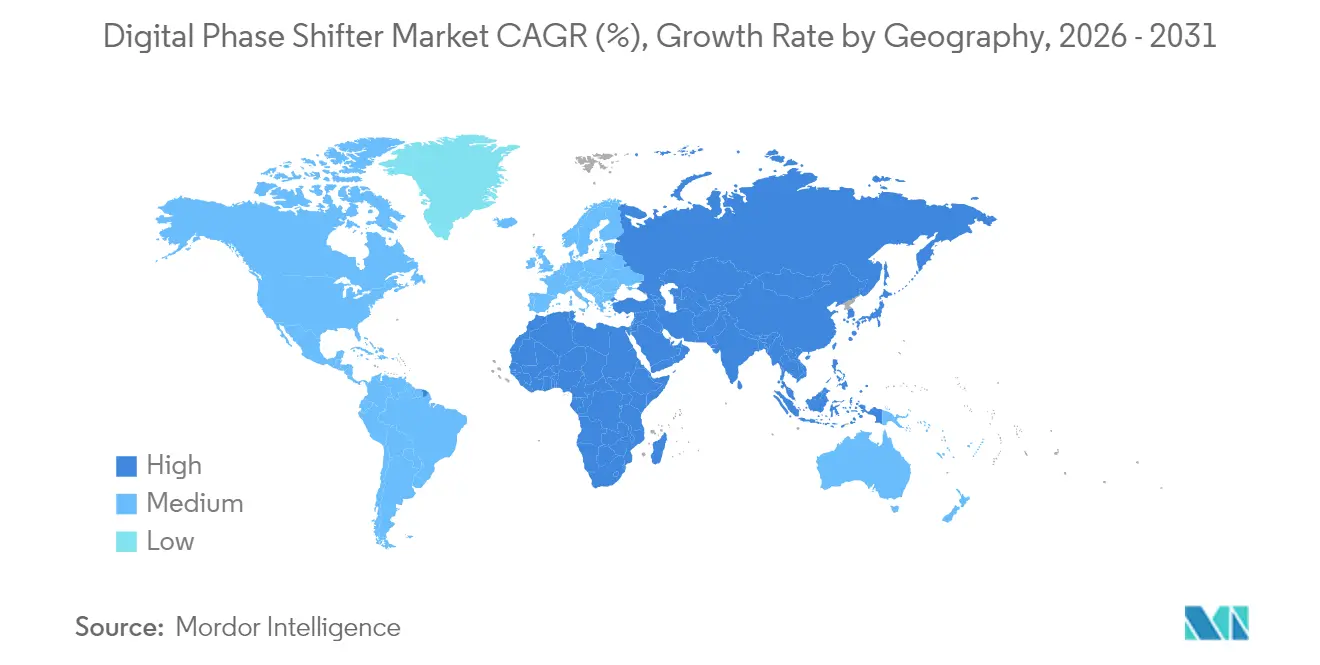

- By geography, Asia-Pacific represented 40.25% of the digital phase shifter market in 2025; the Middle East & Africa region is rising at an 11.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Phase Shifter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G mmWave massive-MIMO roll-out in urban Asia-Pacific and North America | +2.8% | Asia-Pacific core, North America urban centers | Medium term (2–4 years) |

| AESA radar modernisation across NATO fleets | +1.9% | North America & Europe | Long term (≥4 years) |

| Automotive imaging radar for L3+ autonomy in Europe | +1.6% | Europe core, expanding to North America and China | Medium term (2–4 years) |

| Ku/Ka-band phased-array payloads in satellite mega-constellations | +1.4% | Global launches centred in North America | Long term (≥4 years) |

| SWaP-C-driven beam-steering modules for UAS | +1.2% | North America & Europe | Short term (≤2 years) |

| CMOS integration replacing analog ferrite shifters | +2.1% | Global, led by Asia-Pacific manufacturing | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

5G mmWave massive-MIMO roll-out in urban Asia-Pacific and North America

Major operators in China, Japan and the United States activated 5G-Advanced sites during 2025 that rely on dense antenna arrays with digital beamforming.[1]Catherine Sbeglia Nin, “Six operators advancing on 5G-Advanced,” RCR Wireless News, rcrwireless.com Each base station integrates hundreds of phase-shifter channels, magnifying demand per site. Silicon CMOS devices with embedded control logic dominate because they permit remote re-calibration and fit stringent form-factor limits. The commercial case is compelling given that mmWave cells require up to five times more sites than sub-6 GHz layers. Enhanced spectral efficiency and urban-core capacity gains reinforce continuous investment, keeping the digital phase shifter market on a steep volume trajectory.

AESA radar modernisation across NATO fleets

The United States Air Force, joined by European allies, funds multi-year conversions of legacy mechanically steered radars to AESA front ends.[2]John Keller, “Air Force places a USD 30 million order to Northrop Grumman for additional AESA airborne radar systems for F-16,” Military & Aerospace Electronics, militaryaerospace.com Contracts such as the APG-83 program embed high-power GaN phase-shifter tiles that deliver rapid electronic steering and resilient jamming resistance. Long qualification cycles lock suppliers into decade-long production, providing revenue visibility. Performance thresholds proven in fighter-aircraft programs often cascade into naval and ground radar upgrades, extending the opportunity set far beyond the initial platforms. Export-control rules constrain non-aligned buyers, giving approved vendors premium pricing leverage.

Automotive imaging radar for L3+ autonomy in Europ

German and Swedish OEMs run validation fleets equipped with 77–81 GHz imaging radar that requires sub-degree phase resolution to build 4D point clouds. The transition from FMCW to phase-coded waveforms drives demand for digital architectures that can switch modulation schemes over-the-air. Unit-price targets below USD 50 force suppliers to embed phase shifting, control logic and calibration memory on a single die, stimulating CMOS-MEMS co-integration efforts. As regulatory approvals for conditional autonomy approach 2027, vehicle platforms commit to volume hardware, placing the digital phase shifter market at the centre of ADAS cost curves.

Ku/Ka-band phased-array payloads in satellite mega-constellations

Flat-panel terminals adopt Ku/Ka-band phase shifters to link dynamically with LEO and GEO spacecraft.[3]ThinKom Solutions, “ThinKom and KSAT Explore Radically New Approach to Satellite Ground Stations,” thinkom.comSpace-qualified chips must tolerate radiation and thermal shock without phase drift. Mega-constellation economics reward suppliers able to manufacture tens of thousands of identical beam-steering tiles. Ground-segment operators gain multi-orbit flexibility, allowing aircraft, maritime and land vehicles to roam seamlessly. These requirements favour robust GaN-on-SiC substrates and drive collaborations between satellite primes and RF front-end specialists, enlarging the digital phase shifter market footprint in space communications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High insertion-loss above 28 GHz | -1.8% | Global, concentrated in mmWave work | Short term (≤2 years) |

| Thermal yield losses in dense arrays | -1.3% | Global, high-power systems | Medium term (2–4 years) |

| ITAR/EAR export constraints on dual-use RF chips | -2.1% | Global except domestic US | Long term (≥4 years) |

| SOI and GaN-SiC substrate shortages | -1.7% | Global, acute in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High insertion-loss above 28 GHz

Switched-line topologies show 3 dB or higher insertion loss at W-band, cutting effective radiated power and shrinking link budgets. Reflection-type designs improve flatness but enlarge die area and complicate calibration. Aggregate losses across arrays of 256 or more elements can halve total antenna gain, forcing designers to over-specify power amplifiers. Research into MEMS-assisted structures demonstrates <0.2 dB loss yet struggles with automotive-grade switching speed. Continual materials optimisation and tighter on-wafer process control are essential to offset this technical headwind in the digital phase shifter market.

ITAR/EAR export constraints on dual-use RF chips

Revised US export rules place GaN devices above X-band under licensing regimes, fragmenting global supply. Contractors serving foreign programs face long approval cycles, while domestic fabs gain protected demand. Several European primes accelerate indigenous phased array projects to mitigate risk, yet duplication raises R&D costs that pass through to system prices. Over time, these controls could re-shape regional sourcing patterns and introduce parallel technology stacks, complicating scale economies that previously benefited the digital phase shifter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Range: High-Band Drives mmWave Innovation

Mid-range phase shifters captured 46.55% of 2025 revenue as operators refreshed sub-6 GHz networks and defense agencies overhauled legacy S-band radars. At the same time, the >10 GHz tier advances with a 11.74% CAGR, positioning it as the principal growth engine within the digital phase shifter market. Design trade-offs include greater insertion loss, steeper thermal gradients and stricter packaging constraints, but elevated average selling prices offset these hurdles.

Demand for sub-THz devices rises as standards bodies outline 6G candidate bands. Suppliers leverage existing 28 GHz portfolios to seed development kits for 140 GHz proof-of-concept links. Volume today remains centred on 24–39 GHz infrastructure and 77–81 GHz automotive sensors, yet the pipeline of satellite gateways and backhaul radios ensures the high-band segment will extend its influence on digital phase shifter market expansion.

By Bit Resolution: Higher Precision Commands Premium

4-bit products, offering 22.5-degree steps, held a 35.35% share in 2025 because they balance cost, control bus width and phase-noise limits. Complex radar modalities and satellite tracking, however, lift demand for 7-bit-plus devices that post an 11.45% CAGR, reflecting buyers’ need for sub-degree steering. The digital phase shifter market size for high-resolution parts is expected to grow steadily alongside spacecraft payload counts and imaging radar adoption.

Higher bit counts escalate gate-count and calibration overheads. New MEMS-inside-CMOS test vehicles integrate analog trimming fuses that self-correct process drift, lowering field-calibration costs. Automotive programs offset bit-depth limitations through algorithmic beam sharpening, demonstrating that software compensation can defer premium silicon where bill-of-materials pressure is acute.

By Technology: Silicon Integration Accelerates

Silicon CMOS held 51.10% revenue share in 2025, propelled by its ability to co-locate phase shifters, DACs and control logic on one die. This architecture trims board count, simplifies inventory and enables firmware-centric upgrades that align with network-operator DevOps workflows. The digital phase shifter market benefits as smartphone and base-station vendors converge on common fabs, enhancing economies of scale.

MEMS devices enjoy a 12.78% CAGR thanks to near-zero DC power draw and low insertion loss. Co-packaged optics and silicon photonics demonstrators show optical beam steering below 1° with nanosecond switching. GaN remains indispensable in high-power military arrays, and breakthroughs in defect control promise even higher breakdown voltages. These parallel paths indicate that no single material platform will dominate; instead, application-tailored hybrids will characterise the next wave of the digital phase shifter industry.

By Industry Vertical: Automotive Transformation Accelerates

Telecom operators accounted for 54.10% of 2025 revenue, reflecting the vast installed base of macro sites. Yet automotive volumes rise sharply as Level 3 autonomy pilots scale. The digital phase shifter market size for automotive radars is projected to climb with a 13.65% CAGR, underpinned by Europe-led 4D sensing roll-outs. Defense and aerospace preserve high margins through stringent qualification, securing stable cash flows for GaN suppliers.

Vehicle OEMs demand AEC-Q100 qualification, over-the-air firmware upgrade paths and price points aligned with high-volume electronics. Suppliers respond with wafer-level packaging and integrated self-test features that cut end-of-line calibration minutes. Satellite and industrial automation segments round out demand, ensuring balanced exposure and cushioning suppliers against telecom-sector capex swings.

Geography Analysis

Asia-Pacific contributed 40.25% of 2025 revenue, reflecting unmatched 5G macro build-outs and a dense semiconductor supply chain. National production of gallium and silicon carbide substrates strengthens vertical integration, supporting local device makers even as export regulations tighten. Tier-one automotive suppliers in Japan embed 77 GHz imaging radar across premium vehicle lines, widening regional demand.

North America follows, driven by large defense budgets and early mmWave deployments in urban corridors. Programs such as the Next Generation Jammer and satellite mega-constellations sustain premium demand for space-grade and ruggedised parts. Government incentives under the CHIPS Act spur fab construction that could rebalance global supply by the late 2020s.

Europe displays diversified end-markets across telecom, automotive and aerospace. Policy initiatives aimed at technological sovereignty propel local sourcing of RF front-ends. Meanwhile, the Middle East & Africa shows the fastest 11.25% CAGR, with sovereign defense upgrades and emerging 5G networks driving imports of turnkey phased-array subsystems. These patterns underscore how geopolitics and industrial policy shape the regional contours of the digital phase shifter market.

Competitive Landscape

The digital phase shifter market exhibits moderate consolidation. Top suppliers integrate wafer fabrication, packaging and RF systems design to maximise yield control and intellectual-property leverage. Recent moves such as Qorvo’s acquisition of Anokiwave expand access to active-array know-how and accelerate time-to-market for multi-chip modules.

MEMS start-ups target niches where sub-dB insertion loss and low standby power confer edge, particularly in ultra-low-power IoT satellites and compact UAV datalinks. Large IDMs counter with system-in-package offerings that bundle drivers and control firmware, lowering total-cost-of-ownership for network operators. Supply risks around gallium and silicon carbide motivate several players to sign long-term raw-material contracts or qualify secondary sources to hedge geopolitical exposure.

Export-control regimes split market access. US-licensed vendors win captive demand in defense programs, while Chinese suppliers pivot toward domestic telecom infrastructure. European OEMs pursue dual-sourcing between US and indigenous fabs to ensure continuity. As software-defined radios proliferate, platform stickiness will hinge on update frameworks and API openness rather than raw RF figure-of-merit, reshaping how firms capture recurring value in the digital phase shifter market.

Digital Phase Shifter Industry Leaders

General Electric Company (GE)

Schneider Electric SE

ABB Ltd.

Siemens AG

Analog Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: L3Harris demonstrated a digital phased-array antenna system that merges software beamforming with traditional RF chains.

- February 2025: ThinKom introduced a retrofit kit bringing multi-orbit phased-array connectivity to 50+ single-aisle aircraft.

- January 2025: Skyworks Solutions posted USD 1.068 billion in quarterly revenue, citing 5G content and automotive connectivity growth

- January 2025: STMicroelectronics reported soft industrial and automotive demand in FY-2024 results .

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

At Mordor Intelligence, we define the digital phase shifter market as finished solid-state or MEMS devices that programmatically set the phase of RF and microwave signals from sub-GHz bands through 40 GHz, sold as stand-alone chips, connectorized modules, or integrated beam-forming tiles to telecom, defense, aerospace, automotive, and industrial test-equipment OEMs.

Scope exclusion; for clarity, we exclude passive mechanical line stretchers and analog varactor or ferrite phase shifters.

Segmentation Overview

- By Frequency Range

- Low (Sub 1 GHz)

- Mid (1-10 GHz)

- High (Above 10 GHz)

- By Bit

- 4-Bit

- 5-Bit

- 6-Bit

- 7 and Higher-Bit

- By Technology

- MEMS-Based

- Silicon-Based (CMOS/SOI)

- GaAs/GaN Digital

- By Industry Vertical

- Telecommunications

- Defense and Aerospace

- Automotive and Transportation

- Industrial and Test Equipment

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interview insights from design engineers at radar primes, sourcing managers at antenna integrators, tower owners, and specialty distributors across North America, Europe, and high-growth Asia-Pacific allow us to verify calibration ranges, bit-depth migration timing, and negotiated average selling prices.

Desk Research

We start by mapping demand drivers through International Telecommunication Union 5G cell counts, Federal Communications Commission equipment authorizations, NATO procurement notices, Euroconsult satellite manifests, and peer-reviewed IEEE papers that quantify phased-array adoption. Only after cross-checking these signals with supplier disclosures and investor decks do we accept a figure into the model.

Our analysts also tap D&B Hoovers for revenue splits, Dow Jones Factiva for component shipment headlines, and IMTMA production indices that flag Asian foundry output swings, which help us calibrate regional multipliers. The sources cited above are illustrative; many additional public documents complement data collection and validation.

Market-Sizing & Forecasting

A top-down build begins with counts of massive-MIMO 5G sites, AESA radar retrofits, and Ku/Ka-band flat-panel antenna production, which are then translated into component volumes through typical device-per-system ratios. Supplier roll-ups and sampled ASP × volume checks provide bottom-up sense tests that refine totals.

Key variables modeled include share of 6-bit and higher devices, ASP erosion, GaN wafer starts, regional defense capital outlays, and MEMS adoption rates. We employ multivariate regression blended with ARIMA smoothing to project each driver, followed by scenario analysis that captures upside from early 6G trials or downside from defense spending pauses.

Data Validation & Update Cycle

Outputs pass automated variance flags, peer analyst audits, and sector-lead sign-off. We refresh every twelve months, trigger interim updates for material events, and rerun critical assumptions just before release so clients receive the latest view.

Why Our Digital Phase Shifter Baseline Earns Decision-Maker Trust

Stakeholders often notice that published estimates diverge, and we observe gaps stemming from differing device definitions, currency bases, and update cadences.

Major gap drivers include whether analog units are blended with digital, if captive consumption is netted out, the treatment of sub-6 GHz telecom demand, and the refresh frequency.

Mordor's model isolates purely digital units, applies consistent 2025 USD, and benefits from the freshest 5G rollout data, making the baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.82 B (2025) | Mordor Intelligence | - |

| USD 0.78 B (2024) | Global Consultancy A | Mixes analog with digital and counts gross supplier revenue |

| USD 0.75 B (2023) | Trade Journal B | Converts to USD at spot rates and omits Asian merchant fabs |

| USD 0.48 B (2023) | Industry Association C | Excludes telecom infrastructure demand below 6 GHz |

The comparison shows that scope choices and data freshness, not arithmetic, drive the spread. By rooting estimates in transparent drivers and repeatable steps, Mordor Intelligence provides a balanced baseline that executives can trust for strategic decisions.

Key Questions Answered in the Report

What is the current size of the digital phase shifter market?

The market is valued at USD 0.91 billion in 2026 and is forecast to reach USD 1.53 billion by 2031.

Which frequency band generates the most revenue?

Mid-range 1–10 GHz devices lead with 46.55% 2025 revenue because they serve established 5G and radar upgrades

Which application vertical is growing the fastest?

Automotive and transportation posts a 13.65% CAGR as imaging radar becomes standard for Level 3 autonomy suites.

Why are MEMS-based phase shifters gaining momentum?

MEMS devices combine very low insertion loss with negligible standby power, pushing a 12.78% CAGR in cost-sensitive IoT and automotive designs

How do export controls impact the industry?

ITAR/EAR regulations limit GaN device shipments above X-band, encouraging domestic sourcing and regional technology duplication

Which region will see the highest growth by 2031?

The Middle East & Africa is set to expand at 11.25% CAGR, driven by defense modernisation and new satellite communication projects.

Page last updated on: