Digital Signal Processor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 3.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

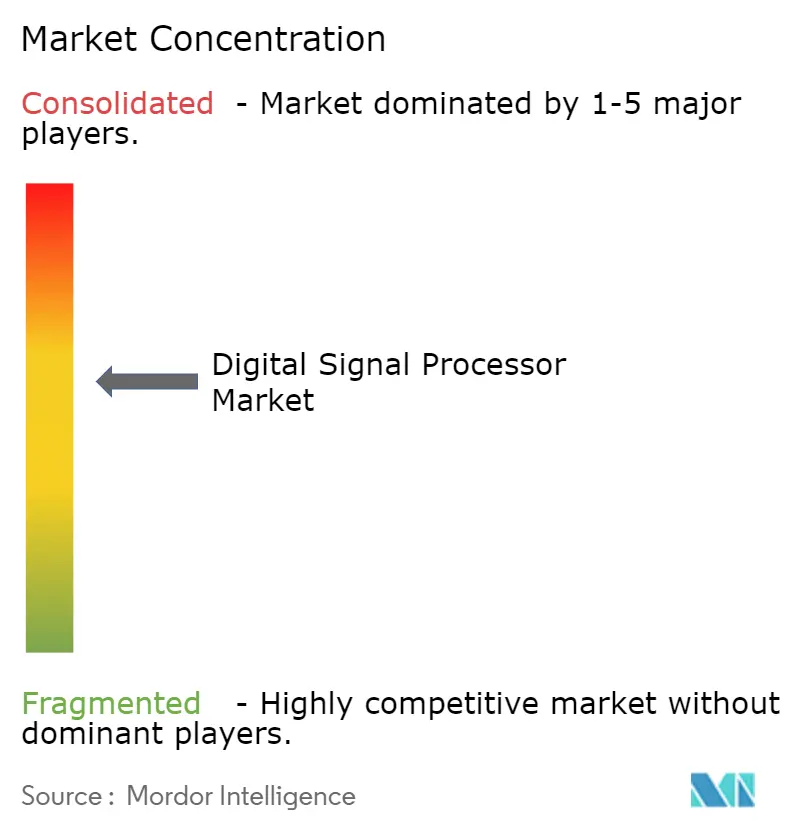

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Signal Processor Market Analysis by Mordor Intelligence

The digital signal processor market size is expected to grow from USD 2.69 billion in 2025 to USD 2.77 billion in 2026 and is forecast to reach USD 3.23 billion by 2031 at 3.10% CAGR over 2026-2031. This steady headline number conceals a deeper architectural shift from stand-alone chips toward highly integrated system-on-chip (SoC) solutions that fuse DSP, CPU, and neural engines for edge artificial-intelligence workloads. Semiconductor vendors are prioritizing power-efficient multicore designs, hybrid numeric formats, and software ecosystems that shorten design cycles. 5G Open RAN roll-outs, automotive ADAS demand, emerging cloud-native radio access networks, and factory-floor machine-vision upgrades are sustaining volume growth even as unit pricing moderates. Meanwhile, supply-chain uncertainty at process nodes below 7 nm keeps lead-times volatile, giving added value to platforms that can migrate quickly between mature and advanced nodes.

Key Report Takeaways

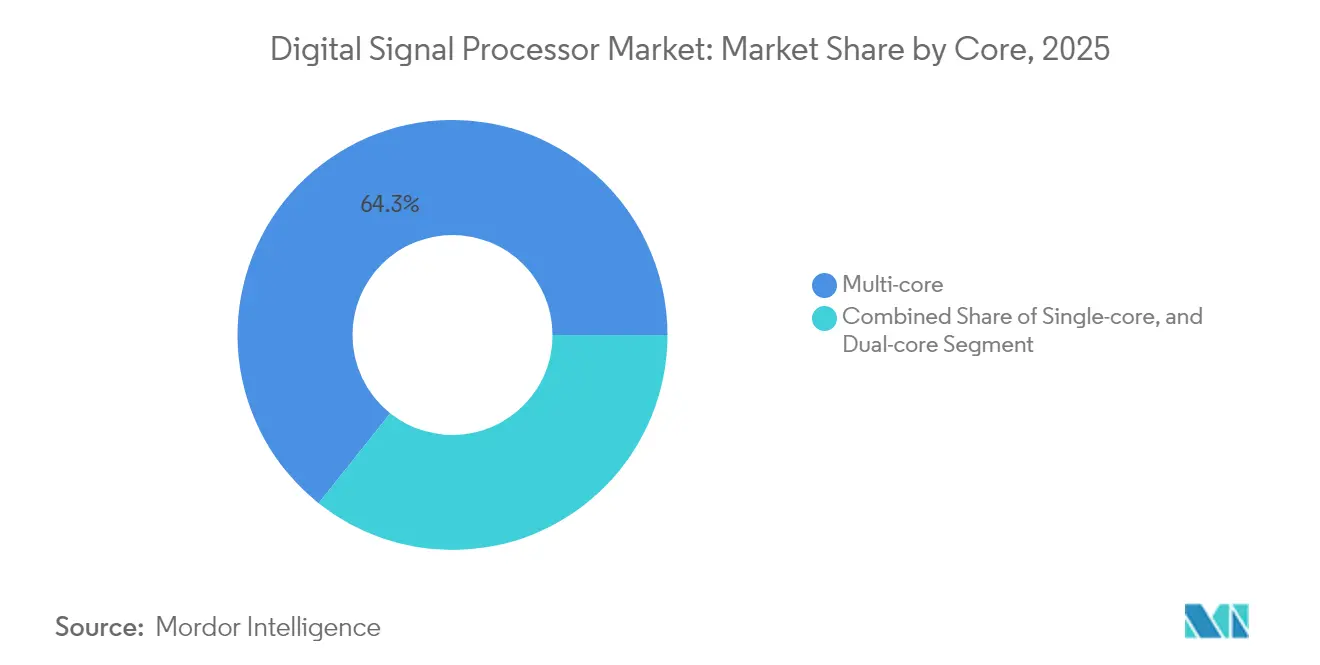

- By core type, multi-core devices led with 64.30% digital signal processor market share in 2025; the segment will expand at a 3.64% CAGR through 2031.

- By product type, application-specific DSPs captured 47.60% of the digital signal processor market size in 2025, while embedded DSP IP cores are projected to grow at a 4.02% CAGR to 2031.

- By architecture, SIMD designs accounted for 51.85% of the digital signal processor market size in 2025; VLIW cores record the fastest 4.21% CAGR to 2031.

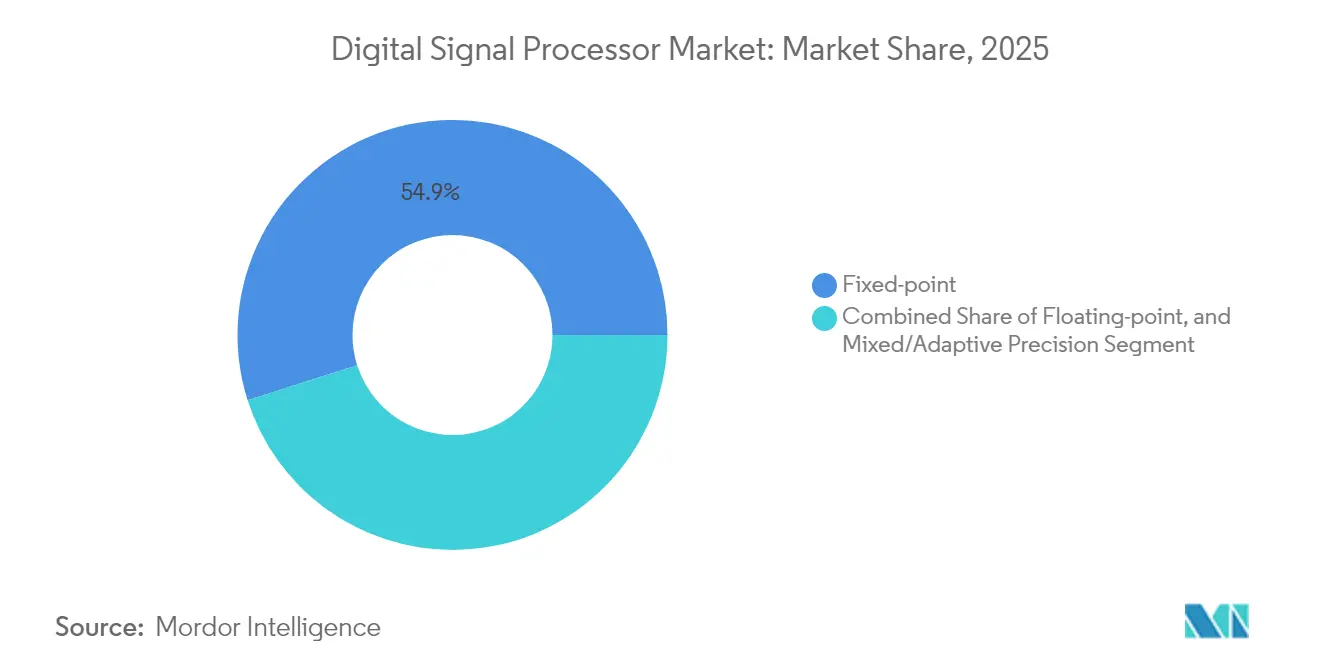

- By numeric format, fixed-point processors held 54.90% of 2025 revenue; floating-point devices are advancing at a 4.62% CAGR.

- By end-user industry, communications retained 39.65% revenue share of the digital signal processor market size in 2025, whereas automotive applications are rising at a 5.29% CAGR.

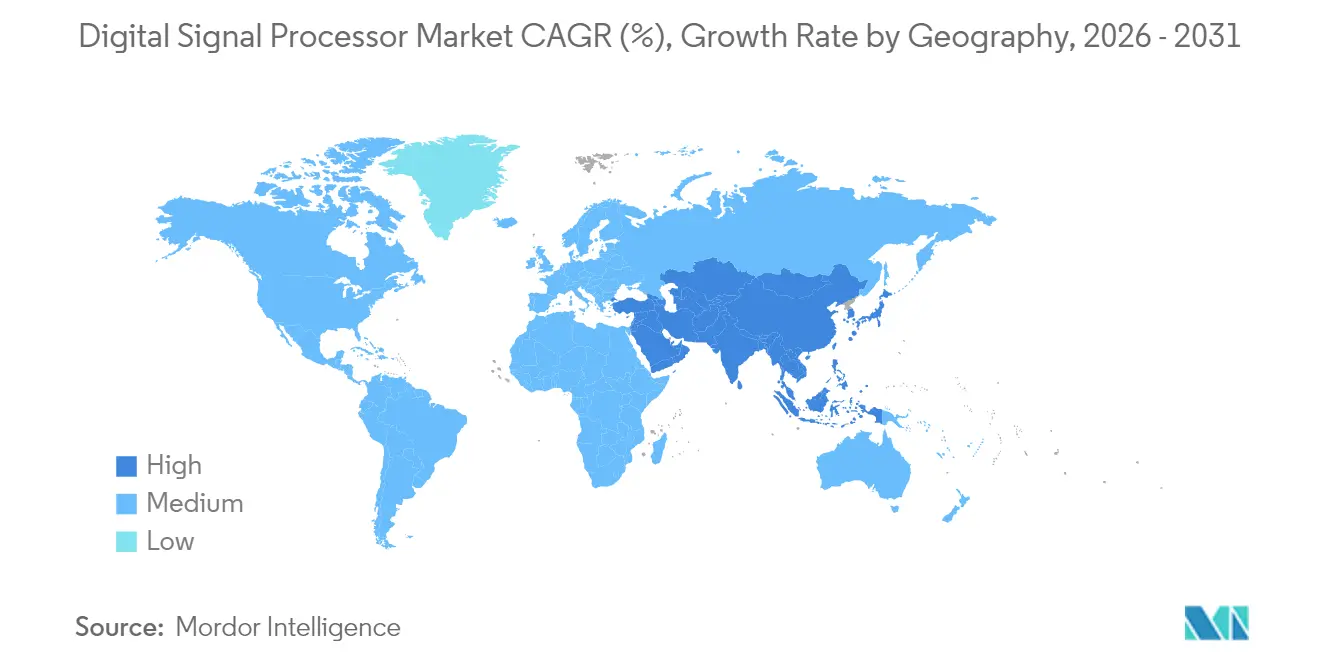

- By geography, Asia-Pacific dominated with 48.20% revenue in 2025 and is on course for a 3.74% CAGR through 2031.

- Texas Instruments, Analog Devices, Qualcomm, Intel, and NXP commanded a combined 64.20% share of global revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Signal Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Open-RAN deployments | +0.8% | Asia-Pacific, spillover to North America | Medium term (2-4 years) |

| ADAS migration to DSP-centric SoCs | +0.7% | Global, strong in Europe & Asia-Pacific | Medium term (2-4 years) |

| AI-enhanced audio & voice in hearables | +0.5% | North America, Europe, Urban Asia | Short term (≤ 2 years) |

| Software-defined radar adoption | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Edge machine vision for Quality 4.0 | +0.3% | Europe, North America | Medium term (2-4 years) |

| Cloud-native RAN baseband demand | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Open-RAN Deployments in Asia

Open RAN architectures separate hardware and software functions, replacing proprietary baseband cards with programmable DSP platforms that can be retargeted in software. Operators in China, Japan, and South Korea are using these open stacks to trim vendor lock-in and speed feature updates. Testbeds combining NVIDIA ARC GPUs with high-performance DSP cores have exceeded 500 Mbps downlink under multi-user loads.[1]Davide Villa et al., “An Open, Programmable, Multi-vendor 5G O-RAN Testbed,” Northeastern University, northeastern.edu This performance proof drives a procurement wave for multicore, floating-point-capable DSPs that execute beam-forming, channel estimation, and fronthaul compression in real time. The resulting pull-through effect is lifting orders for both merchant silicon and licensable DSP IP in Asia-Pacific and secondary deployments in North America.

Automotive ADAS Tier-1 Designs Migrating from MCU to DSP-centric SoCs

As camera, radar, and LiDAR counts rise per vehicle, microcontrollers lack the throughput to perform real-time sensor fusion. Tier-1 suppliers are therefore shifting to heterogeneous SoCs combining multi-core DSP engines with AI accelerators. AMD’s Zynq UltraScale+ XA MPSoC shows how a tightly coupled DSP fabric processes radar chirps while adjacent AI engines classify objects, all inside a single safety-certified package.[2]Advanced Micro Devices, “Advanced Driver Assistance Systems (ADAS),” amd.com The automotive supply chain in Europe and East Asia is committing design wins through 2027, anchoring double-digit unit growth even as average selling prices drift lower.

AI-enhanced Audio & Voice Processing in Hearables and Smart Speakers

Wearables now blend classic audio DSP functions—noise suppression, echo cancellation—with on-device AI that personalizes frequency response and recognizes spoken intent. Specialist cores must execute both fixed-point FIR pipelines and neural-network inference within milliwatt budgets. Edge-AI audio chips announced in 2025 integrate on-chip SRAM to cut DRAM accesses and deliver double-digit battery-life gains.[3]EE Times Europe Staff, “Redefining the Future of Audio Chips with AI,” eetimes.euUnit volumes in earbuds and voice assistants sustain an attractive long-tail revenue stream for mid-range DSP suppliers.

Adoption of Software-Defined Radar in Aerospace & Defense

Defense prime contractors are re-architecting radar platforms so that mission modes from weather scanning to electronic support measures run on common reprogrammable DSP engines. AMD’s Versal AI Edge integrates DSP, AI, and programmable logic to reconfigure pulse compression or target-tracking kernels between sorties. Longer program lifecycles and demand for rapid field upgrades underpin a steady replacement market for high-end floating-point DSPs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced-node foundry volatility | –0.6% | Global, concentrated in Asia | Short term (≤ 2 years) |

| Fixed- vs floating-point trade-offs in battery devices | –0.4% | Global | Medium term (2-4 years) |

| Rising royalties for licensable cores | –0.3% | Global, higher in emerging markets | Medium term (2-4 years) |

| Export-control restrictions | –0.5% | China, Russia, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-chain Volatility in Advanced Node (≤ 7 nm) Foundries

A limited pool of ultra-modern fabs in Taiwan and South Korea faces periodic geopolitical and logistics disruptions. When capacity tightens, DSP lead-times stretch beyond 40 weeks, pushing designers to retape-out on mature processes that meet neither power nor performance targets. Chipmakers with multi-foundry strategies and adaptable physical-design kits remain better insulated than rivals locked to single-source partnerships.

Integration Trade-offs Between Fixed- and Floating-Point Precision in Battery-Powered Devices

Wearables, hearables, and IoT sensors must choose between power-lean fixed-point math and the higher numeric fidelity of floating-point. Academic work using Polynomial Chaos Expansions models quantization noise to right-size word lengths, yet implementation still adds weeks to verification schedules.[4]M. Rao and N. N., “Estimating Word Lengths for Fixed-Point DSP Implementations,” MDPI Electronics, mdpi.comAs algorithms grow more AI-centric, many OEMs find they need mixed-precision pipelines, complicating IP selection and tool flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core: Multi-core dominance reflects rising parallel workloads

Multi-core devices generated 64.30% of 2025 revenue, equivalent to a USD 1.73 billion slice of the digital signal processor market size, underscoring their essential role in 5G baseband, automotive radar, and industrial vision. The digital signal processor market favors these parts because task-level parallelism maps naturally to multiple homogeneous cores, allowing deterministic latency under real-time constraints. Texas Instruments’ C66x family demonstrates how eight fixed-/floating-point cores harness a unified Multicore Navigator fabric to eliminate copy overhead. The configuration headroom supports product-line variants spanning medical imaging, motor control, and SATCOM terminals.

Single-core and dual-core options survive in deeply embedded, price-sensitive end-nodes such as smart meters, while heterogeneous multi-core SoCs that blend DSP, CPU, and AI accelerators are gaining traction. Sustained 3.64% CAGR through 2031 keeps the multi-core slice of the digital signal processor market expanding faster than overall industry revenue. As open-source toolchains mature, multicore programming burdens fall, reinforcing supplier roadmaps that prioritize scalable tile-based fabrics, scratchpad memory hierarchies, and inter-core message passing.

By Product Type: Application-specific solutions accelerate differentiation

Application-specific DSPs captured 47.60% of revenue in 2025, or USD 1.28 billion of the digital signal processor market size, because tightly focused instruction sets and accelerator blocks deliver watt-efficient performance in smartphones, base stations, and infotainment head units. Their growth aligns with OEM demands for BOM savings and board-space reductions. Qualcomm’s modem-integrated DSP blocks and Analog Devices’ RF-optimized cores exemplify this fit-for-purpose approach.

The fastest expansion, however, comes from licensable embedded DSP IP inserted into wider SoC projects. At a 4.02% CAGR, this vector raises the total addressable slice for EDA vendors and soft-IP houses. General-purpose discrete DSPs now orient toward military, aerospace, and laboratory instrumentation niches that value long product lifecycles. FPGA-based hybrids fill customization gaps where mid-volume customers need reconfigurability without ASIC risk.

By Architecture: SIMD stays king while VLIW outruns on growth

SIMD implementations delivered 51.85% of 2025 revenue, equating to USD 1.39 billion within the digital signal processor market. They thrive on workloads such as beam-forming and audio filtering that broadcast one instruction across long data vectors. Compiler maturity, predictable latency, and small area per MAC keep SIMD attractive versus newer schemes.

VLIW devices, though smaller in absolute dollars, accelerate at 4.21% CAGR on complex math in automotive perception and industrial analytics. Synopsys’ ARC VPX5 mixes VLIW control with SIMD datapaths, attaining 512-bit vector operations for floating-point linear algebra. The approach extracts instruction-level parallelism without the control-flow overhead faced by superscalar CPUs. Emerging SIMT and heterogeneous instructional formats appear in research prototypes but are yet to move the revenue needle.

By Numeric Format: Fixed-point efficiency holds, floating-point precision rises

Fixed-point processors dominated 2025 with 54.90% share, roughly USD 1.48 billion of digital signal processor market revenue. Their low-leakage multipliers and narrow data paths keep thermal budgets in check for earbuds, tablets, and IoT gateways. Toolchains now automate saturation arithmetic and scaling, easing developer burdens once unique to fixed-point coding.

Floating-point SKUs, however, advance at a faster 4.62% CAGR. IEEE-754 compliance eliminates overflow guardrails, boosting productivity in Matlab-to-silicon flows for predictive maintenance and medical ultrasound. Synopsys confirms that an optimized VLIW/SIMD fusion can deliver single-precision throughput at under 0.5 mW/MFLOP. A hybrid future looms where adaptive precision engines switch format per kernel, letting end-products toggle between power sipping and accuracy as use-case dictates.

By End-user Industry: Communications remain anchor, automotive surges fastest

Communications systems consumed 39.65% of 2025 shipments, translating to USD 1.07 billion of the digital signal processor market size. Massive-MIMO antennas, front-haul compression, and open-interface virtual DU stacks rely heavily on multithreaded DSP arrays to meet sub-millisecond scheduling deadlines. As operators densify 5G picocells and experiment with 6G terahertz trials, platform refresh cycles shorten to three-year windows, cementing recurring silicon demand.

Automotive revenues clock the strongest 5.29% CAGR as Level-2+ autonomy proliferates. Radar and camera attach rates now exceed eight sensors per premium vehicle, each streaming data to DSP-accelerated fusion hubs. The digital signal processor industry plays a pivotal role here, with European and Japanese OEMs lining up 32-TOPS heterogeneous SoCs for 2027 model years. Consumer electronics, industrial automation, aerospace, and healthcare sectors round out the demand map, each leaning on distinct blends of throughput, power, and certification.

Geography Analysis

Asia-Pacific generated 48.20% of worldwide revenue in 2025, just under half of the global digital signal processor market. China alone drives more than one quarter of wafer demand as its telecom operators build ultra-dense 5G grids and EV makers load vehicles with radar and infotainment processors. South Korea and Japan add further pull through their advanced memory, sensor, and automotive supply chains. A 3.74% CAGR keeps the region at the top of the growth league, and its installed fab capacity secures a supply advantage when advanced-node allocations tighten.

North America ranks second in both revenue and R&D depth. Silicon Valley start-ups and Austin-based incumbents push leading-edge multicore architectures and neural-DSP hybrids, while US defense projects guarantee a steady market for rad-hard floating-point parts. Federal incentives under the CHIPS and Science Act catalyze domestic fab expansions scheduled to come online by 2027, promising to ease node scarcity for local DSP houses.

Europe completes the triad with robust demand from German and French automakers and a growing cohort of machine-vision integrators. Regional initiatives such as IPCEI Micro-electronics support pilot lines for 12-in wafers, narrowing the production gap with Asia. Meanwhile, South America plus the Middle East & Africa contribute an emerging tail, largely tied to telecom infrastructure roll-outs and satellite broadband gateways that rely on high-throughput DSP-based modems.

Mordor Intelligence provides coverage of the digital signal processor market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The five largest vendors—Texas Instruments, Analog Devices, Qualcomm, Intel, and NXP—controlled roughly 65% of global revenue in 2024, pointing to a moderately concentrated structure. Texas Instruments and Analog Devices continue to amplify domain-specific portfolios, delivering reference software and analog front-ends that lock in automotive and industrial customers for decade-long lifecycles. Qualcomm leverages modem expertise to fold DSP subsystems into smartphone basebands, while Intel bundles signal-processing cores within heterogeneous x86 platforms aimed at telecom DUs.

Competition intensifies where AI inference blurs classical DSP borders. Cadence promotes licensable Tensilica cores as drop-in neural accelerators, arguing that soft-IP averts obsolescence in rapidly evolving AI models. Start-ups like Retym attract venture outlays by targeting ultra-low-power inference at the sensor edge, betting on architectural innovations outside the x86/ARM hegemony. Differentiators now cluster around compiler toolchains, model-compression libraries, and end-to-end security, rather than raw MAC counts.

Strategic partnerships span optical DSP roadmaps-MaxLinear and Marvell both unveiled 1.6 Tbit/s PAM4 devices to feed AI datacenter interconnects-as well as automotive AI compute, where AMD’s Versal AI Edge Gen 2 stakes a claim for sensor-fusion supremacy. Suppliers are also bundling encrypted over-the-air update frameworks to lock firmware revenues. For late entrants, white-space opportunities exist in mixed-signal sensor hubs and medical imaging, markets still underserved by generalist megacaps.

Digital Signal Processor Industry Leaders

Texas Instruments Inc.

Intel Corporation

Analog Devices Inc.

Infineon Technologies AG

NXP Semiconductors NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MaxLinear introduced the Rushmore DSP, a low-power 1.6 T PAM4 device optimized for AI/ML optical links, fabricated on Samsung CMOS, operating below 25 W per module.

- April 2025: Marvell Technology launched the first 1.6 T PAM4 DSP for active electrical cables, collaborating with 3M, Amphenol, and Luxshare-Tech to meet cloud-AI bandwidth demand.

- March 2025: Cadence rolled out the Tensilica NeuroEdge 130 AI Co-Processor, obtaining more than 30% area savings and 20% lower power while pairing seamlessly with NPUs.

- March 2025: Ericsson released the Cat-B ULPI fronthaul interface specification, pledging to migrate its entire RAN portfolio to the standard beginning in 2024.

- January 2025: DSP plc acquired UK partner Acardia to strengthen Oracle-centric infrastructure offerings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital signal processor (DSP) market as all newly fabricated integrated circuits or licensable IP cores whose internal architecture is purpose built to execute high-speed mathematical routines that condition, compress, or analyze real-world signals in consumer, industrial, automotive, telecom, and defense electronics.

Scope exclusion: Discrete graphics processors and general-purpose CPUs that merely embed limited DSP instructions are left outside the count.

Segmentation Overview

- By Core

- Single-core

- Dual-core

- Multi-core

- By Product Type

- General-purpose Stand-alone DSPs

- Application-specific DSP (ASSP/ASIP)

- Embedded DSP IP Cores

- FPGA/SoC-based Hybrid DSPs

- By Architecture

- SIMD (Single Instruction Multiple Data)

- VLIW (Very-long-instruction-word)

- SIMT/Vector DSPs

- MLIW and Novel Heterogeneous Designs

- By Numeric Format

- Fixed-point

- Floating-point

- Mixed/Adaptive Precision

- By End-user Industry

- Communication

- Cellular Infrastructure (4G/5G, Open-RAN)

- Data Center and Cloud Edge

- VoIP and IP Video

- Automotive

- ADAS and Autonomous Driving

- In-vehicle Infotainment

- Consumer Electronics

- Smartphones and Tablets

- Hearables/Wearables

- Smart TVs and STBs

- Industrial

- Motor Control and Drives

- Machine Vision and Robotics

- Smart Grid and Energy

- Aerospace and Defense

- Radar and EW Systems

- Satellite and Space Electronics

- Healthcare

- Medical Imaging

- Patient Monitoring and Diagnostics

- Communication

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured calls with foundry account managers, automotive Tier 1 electronics architects, smartphone ODM procurement leads, and regional distributor heads across North America, Europe, China, and ASEAN. These conversations clarify real ASP movements, node migration timelines, and inventory swings, then validate the assumptions harvested from desk work.

Desk Research

We start with public domain benchmarks, Semiconductor Industry Association output tables, United States International Trade Commission HS-level shipment data, OECD broadband and 5G rollouts, and filings housed on EDGAR, supplemented by trade bodies such as the Japan Electronics and Information Technology Industries Association. Engineering insights are drawn from IEEE Xplore papers on multi-core DSP designs. To refine company revenue splits, we query D&B Hoovers and screen press releases through Dow Jones Factiva. This list is illustrative; many additional sources inform each variable reviewed.

Market-Sizing & Forecasting

A production and trade driven top-down model converts global wafer starts into packaged DSP units, applies region-specific yields, and multiplies by live ASP curves. Supplier roll-ups and sampled contract pricing offer a bottom-up cross-check before totals are locked. Key inputs include smartphone DSP attach rates, 5G base station build counts, automotive ADAS ECU penetration, average die size shrink factors, and foundry utilization. A multivariate regression coupled with an ARIMA overlay projects each driver forward, while scenario analysis tests upside from AI edge workloads.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst sign-off, and a senior review board. Figures are refreshed annually, with interim revisions triggered by material fab outages, policy shifts, or mega design wins, ensuring clients always receive the latest vetted view.

Why Mordor's Digital Signal Processor Baseline Commands Reliability

Published estimates often diverge because firms choose different product taxonomies, apply varying ASP ladders, or refresh at uneven cadences.

Key gap drivers in this market include whether embedded DSP IP royalties are counted, how voice assistant devices are classified, and the aggressiveness of 3 nm cost downs baked into forecasts. By anchoring on verified production data and updating every twelve months, Mordor minimizes these sources of error.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.69 B (2025) | Mordor Intelligence | |

| USD 10.10 B (2024) | Global Consultancy A | counts generic microcontrollers with DSP blocks, older ASP benchmarks |

| USD 14.99 B (2024) | Trade Journal B | includes royalty streams from legacy audio codecs, assumes constant 7.5 % CAGR without node pricing decay |

| USD 19.36 B (2024) | Industry Association C | mixes packaged chips and licensed IP; no yield adjustment for advanced nodes |

Taken together, the comparison shows that when scope creep and pricing shortcuts are removed, Mordor delivers a balanced, transparent baseline grounded in measurable production realities and repeatable steps.

Key Questions Answered in the Report

What factors are driving growth in the digital signal processor market between 2026 and 2031?

Demand from 5G Open RAN deployments, automotive ADAS sensor-fusion needs, cloud-native radio access networks, and edge-based machine-vision upgrades are the primary forces expanding the digital signal processor market at a 3.10% CAGR.

How big is the digital signal processor market in 2026 and what value will it reach by 2031?

The digital signal processor market is valued at USD 2.77 billion in 2026 and is projected to reach USD 3.23 billion by 2031.

Which region leads the digital signal processor market today?

Asia-Pacific holds 48.20% of global revenue and posts the fastest 3.74% regional CAGR, keeping it firmly at the top of the digital signal processor market rankings.

Why are multi-core devices so dominant in the digital signal processor market?

Parallel workloads in 5G baseband, radar, and industrial vision map efficiently to multi-core architectures, giving these parts 64.30% of the digital signal processor market and sustaining a 3.64% growth rate.

How will floating-point adoption affect the digital signal processor market?

Rising AI and high-precision workloads are lifting floating-point shipments at a 4.62% CAGR, nudging vendors to add mixed-precision engines that widen addressable opportunities inside the digital signal processor market.

Who are the key players in the digital signal processor market and how concentrated is it?

Texas Instruments, Analog Devices, Qualcomm, Intel, and NXP collectively control about 64.20% of the digital signal processor market, indicating a moderately concentrated competitive landscape.

Page last updated on: