Dermal Toxicity Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dermal Toxicity Testing Market Analysis by Mordor Intelligence

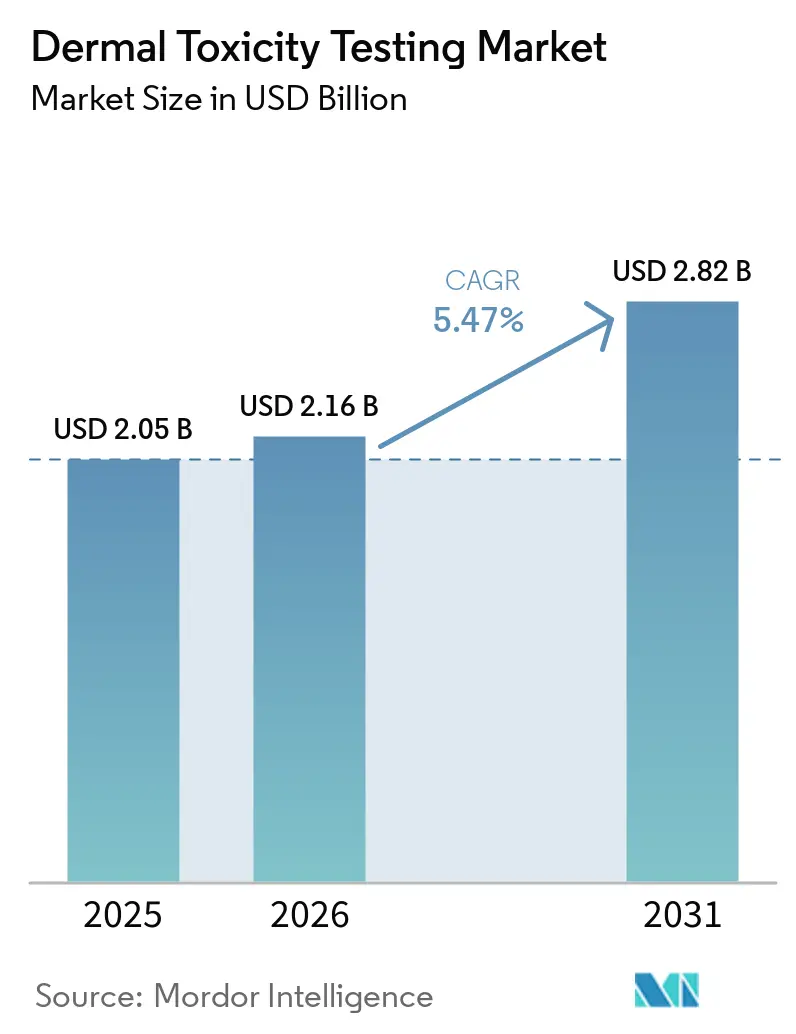

The Dermal Toxicity Testing Market size is projected to be USD 2.05 billion in 2025, USD 2.16 billion in 2026, and reach USD 2.82 billion by 2031, growing at a CAGR of 5.47% from 2026 to 2031.

Greater regulatory pressure for cruelty-free safety data, rapid validation of reconstructed human epidermis (RHE) systems, and breakthroughs in AI-driven in-silico models collectively underpin this expansion. Intensifying ESG mandates amplify spending among cosmetics leaders seeking “no-animal-testing” labels, while pharmaceutical sponsors accelerate pilot programs after the FDA’s April 2025 roadmap streamlined submissions based on New Approach Methodologies (NAMs). North America maintains first-mover advantages through deep CRO networks and venture funding, yet Asia-Pacific registers the fastest revenue gains as Chinese and Japanese regulators codify alternative-testing guidance. Competitive intensity is rising as incumbents add bioprinting and computational modules, and validation hurdles remain high because OECD ring-trial results must satisfy 40-plus national authorities.

Key Report Takeaways

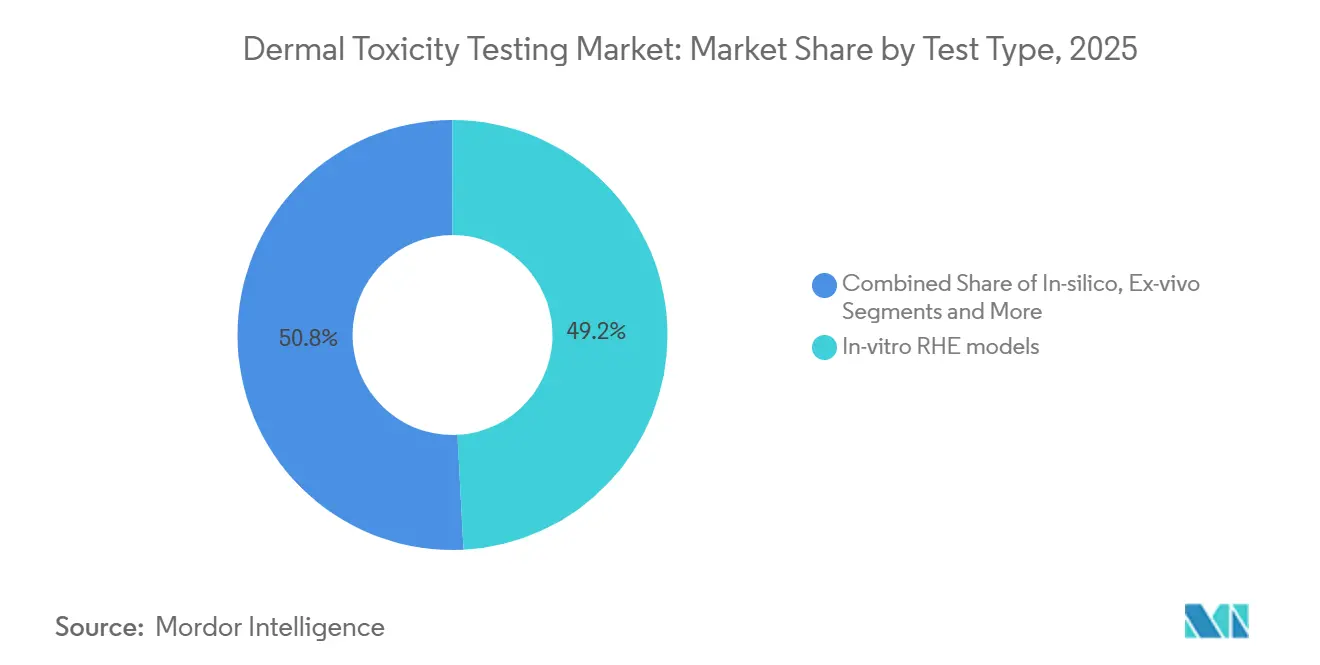

- By test type, in-vitro reconstructed human epidermis models captured 49.19% of dermal toxicity testing market share in 2025, whereas in-silico computational methods are projected to deliver a 5.62% CAGR through 2031.

- By toxicity endpoint, skin irritation captured 37.66% of the dermal toxicity testing market share in 2025, whereas dermal sensitization is projected to deliver a 6.09% CAGR through 2031.

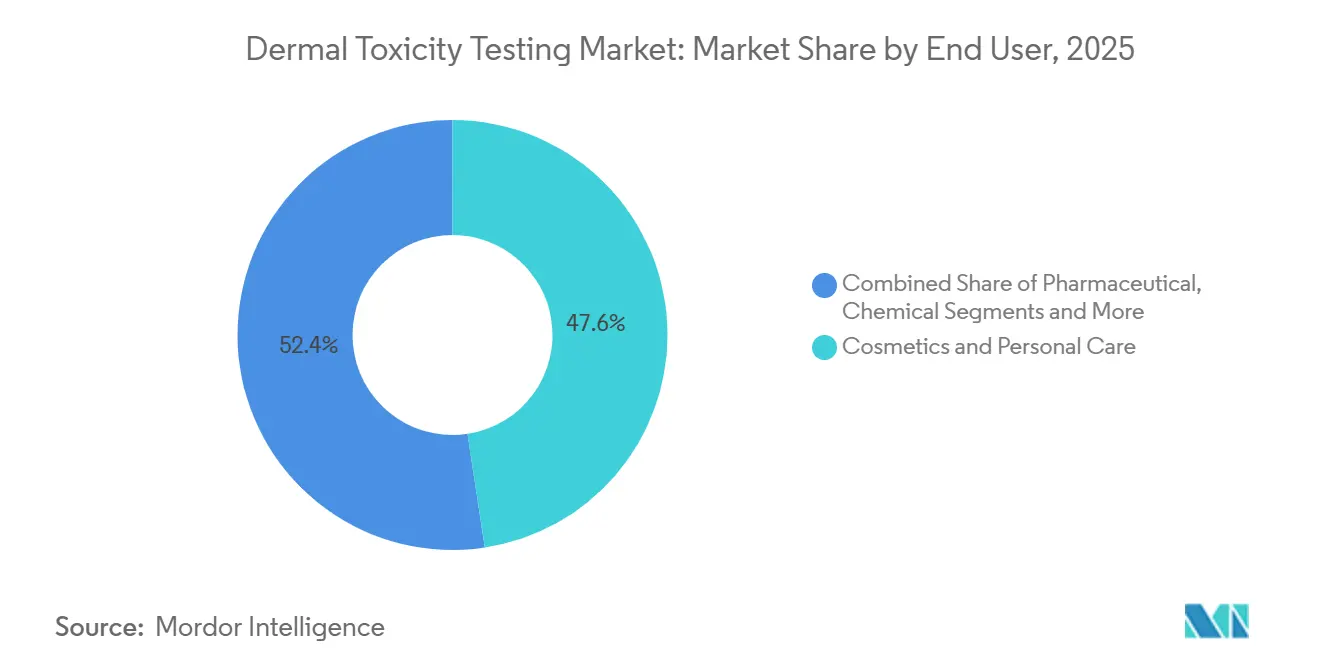

- By end user, cosmetics and personal care accounted for 47.69% share of the dermal toxicity testing market size in 2025, while pharmaceutical and biotech firms are advancing at a 6.04% CAGR to 2031.

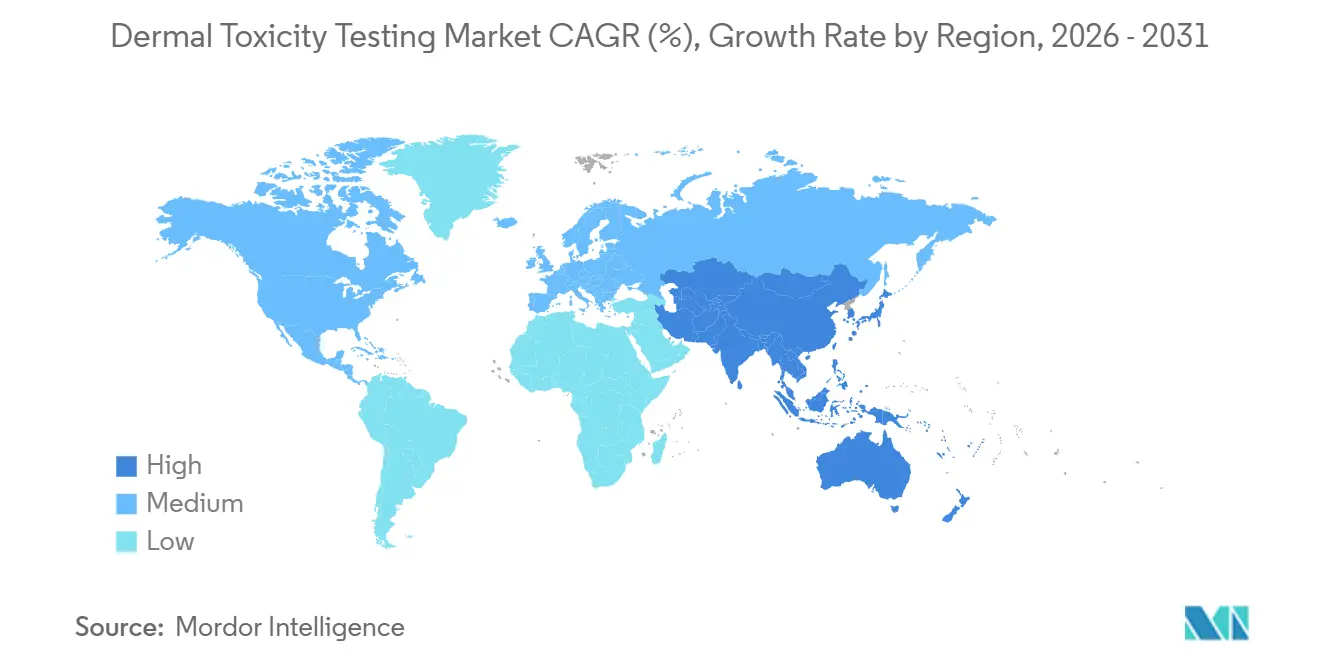

- By geography, North America led with 42.68% revenue share in 2025; Asia-Pacific is poised to expand at a 6.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dermal Toxicity Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on animal testing in cosmetics | +2.10% | Global (EU & North America leading) | Medium term (2-4 years) |

| Accelerated FDA & OECD acceptance of in-vitro & in-silico assays | +1.80% | Global (North America & Europe) | Short term (≤ 2 years) |

| Growth of bioprinted 3-D human skin models | +1.40% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| AI-enabled high-content imaging for irritation screens | +1.20% | Global technology hubs | Long term (≥ 4 years) |

| Rising dermatological drug pipeline needs early dermal safety | +0.90% | Global pharma clusters | Medium term (2-4 years) |

| ESG-driven demand for cruelty-free product claims | +0.80% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Animal Testing in Cosmetics

Multiple jurisdictions codified animal-testing prohibitions, creating a structural demand shift favoring the dermal toxicity testing market. Twelve U.S. states enforced comprehensive bans by 2024, echoing the European Union’s decade-old marketing restriction.[1]Animal Law Info, “Laws Banning Cosmetics Testing on Animals,” animallaw.info Canada’s December 2023 law extended the momentum across North America. Regulatory focus now spans chemicals and pharmaceuticals; the U.S. EPA had cleared 140 alternative methods for dermal endpoints by late 2024, and the FDA’s 2025 roadmap formally encourages NAMs within Investigational New Drug filings. Japan issued guidance on non-animal protocols in 2024, confirming Asia-Pacific alignment. Collectively, these actions elevate compliance risk for companies lacking NAM data and redirect testing budgets toward validated in-vitro and in silico services.

Accelerated FDA & OECD Acceptance of In-Vitro & In-Silico Assays

The FDA’s April 2025 “Roadmap to Reducing Animal Testing in Preclinical Safety Studies” endorses organ-on-chip, AI-based modeling, and virtual-patient simulations, granting early-adopter firms a streamlined review pathway.[2]National Law Review, “Navigating FDA’s Proposed Guidance on AI and Non-Animal Models,” natlawreview.com OECD fast-tracked updates to Test Guidelines 497 and 496 in 2024, integrating omics-based readouts and data-sharing frameworks. Canada released a complementary draft strategy under CEPA in September 2024, targeting full transition to NAMs by 2035. Faster acceptance removes a historic bottleneck—regulatory uncertainty—and magnifies return on R&D for platform providers entrenched in the dermal toxicity testing market.

Growth of Bioprinted 3-D Human Skin Models

Bioprinting advances deliver tissue constructs with extracellular-matrix complexity and perfusable microvasculature, narrowing the in-vitro–in-vivo translation gap. Researchers from Graz University demonstrated 3-D-printed skin containing living cells with robust mechanical properties in April 2025.[3]Staff Writer, “3D-Printed Skin Imitation Equipped With Living Cells Could Replace Animal Testing,” Phys.org, phys.org EPISKIN expanded its SkinEthic RHE portfolio, adding dermis-plus-hypodermis formats in 2024. The FDA approved its first human trial using a bioprinted skin product, signaling regulatory readiness to evaluate 3-D tissues for safety screening. Although unit costs remain high, North America hosts roughly 75 active bioprinting firms, accelerating scale-up innovation.

AI-Enabled High-Content Imaging for Irritation Screens

Machine-learning algorithms now deliver 80% predictive accuracy for irritation profiling using LSTM networks that parse molecular descriptors. The MolToxPred platform achieved 87.76% AUROC by combining random-forest and LightGBM classifiers, spotlighting competitive gains from algorithm ensembles. High-content imaging systems automate cell-morphology analytics, compressing assay timelines from weeks to days and standardizing output over global lab networks. The FDA’s 2025 roadmap cites AI-driven computational toxicology as a priority, yet developers must provide granular model documentation proportional to patient-safety risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Predictive Correlation of Some In-Vitro Assays with Human Outcomes | -1.60% | Global, particularly affecting regulatory acceptance | Medium term (2-4 years) |

| High Capital Cost of 3-D Tissue Culture Platforms | -1.20% | Global, with greater impact on emerging markets | Short term (≤ 2 years) |

| Scarcity of Skilled Cell-Culture Toxicologists in Emerging Markets | -0.80% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Absence of Harmonized Global Regulatory Guidelines | -0.60% | Global, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Predictive Correlation of Some In-Vitro Assays with Human Outcomes

Regulators remain cautious when assay outputs diverge from clinical observations, especially for complex endpoints like dermal sensitization that involve innate and adaptive immunity. Human predictive patch-test datasets reveal variability that current RHE models struggle to reproduce. OECD requires multi-laboratory ring trials prior to guideline approval, prolonging commercialization timelines. Smaller developers face steep funding hurdles to finance these studies. Integrating omics-level analytics with 3-D tissues promises richer mechanistic insight, yet standard protocols are still being harmonized.

High Capital Cost of 3-D Tissue Culture Platforms

CapEx for bioreactors, sterile processing suites, and GMP-grade quality systems tops the budget of many mid-tier labs, constraining NAM adoption beyond wealthy multinationals. Charles River Laboratories estimates that fully equipped 3-D tissue facilities can exceed USD 10 million in start-up spend. Additionally, scale-up challenges in maintaining cell viability under automated handling raise operating costs. While long-term economics favor animal-free testing, the near-term cash burden delays investment, particularly in emerging markets where skilled labor is also scarce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: In-Vitro Dominance with Computational Upswing

In-vitro RHE systems held the largest 49.19% slice of the dermal toxicity testing market share in 2025, anchored by OECD TG 439 and TG 431 acceptance. The dermal toxicity testing market size for RHE platforms is projected to advance steadily as validation pipelines for vascularized constructs finalize. In-silico assays record the fastest 5.62% CAGR through 2031, fueled by AI libraries ingesting millions of cheminformatics records.

RHE maturity partly stems from its replicable barrier-function metrics and ease of transfer into GLP labs. Iterative improvements—such as iPSC-derived keratinocyte sourcing—reduce donor-variability risks and secure unlimited cell banks. Hybrid strategies that pair quick in-silico screens with confirmatory RHE tests compress development cycles and trim reagent costs, an attractive proposition for firms scaling global portfolios. Yet, 3-D bioprinted skin still faces throughput bottlenecks, limiting its near-term share expansion despite superior physiological relevance.

OECD endorsement of ex-vivo skin (MUG-hOSEC) solidifies niche adoption for immuno-competent assays. Incorporation of hypodermal adipose layers elevates metabolic fidelity, revealing surfactant-induced lipid disturbances undetectable in simpler tissues. Chem-informatics algorithms, in parallel, unlock predictive toxicology for new-to-market UV filters where empirical data are scarce. This dual trajectory—biological sophistication and digital simulation—positions the dermal toxicity testing market as an integrated testing ecosystem rather than a binary choice between wet and dry labs.

By Toxicity Endpoint: Irritation Leads While Sensitization Accelerates

Skin-irritation protocols contributed 37.66% of 2025 revenues, securing the largest slice of the dermal toxicity testing market size because every cosmetic and chemical submission mandates this endpoint. Dermal sensitization, however, registers the 6.09% CAGR through 2031, propelled by the OECD adverse outcome pathway that opened multiple in-vitro and in-silico entry points.

Traditional corrosion assays deliver binary readouts and therefore show moderate growth. Phototoxicity testing climbs gradually as awareness about UV-synergistic reactions permeates sunscreen and systemic-drug markets; benzophenone-4 next-generation risk assessments underscore how NAMs can finalize regulatory dossiers without animal models. Cross-endpoint platforms are gaining favor: a single 3-D model may now quantify irritation, corrosion, and preliminary absorption, minimizing sample use and analyst time. Consequently, vendors capable of multiplexing assays on unified platforms strengthen client retention and recurring revenues across the dermal toxicity testing market.

By End User: Cosmetics Still Largest, Pharma Gains Velocity

Cosmetic and personal-care producers retained 47.69% revenue in 2025 as EU and state-level bans compelled full transition to NAMs. Their early adoption built sizable internal labs but also a robust outsourcing channel for tier-2 brands. Pharmaceutical and biotech sponsors, though smaller, are on a 6.04% growth path to 2031, catalyzed by the FDA’s 2025 guideline that explicitly recognizes organ-chip data for IND safety sections.

Chemical and agrochemical firms display steady replacement of Draize and rabbit-irritation assays to comply with REACH renewals. Contract research organizations—SGS, Charles River, Eurofins—expand NAM capacity to serve multi-sector demand surges, investing in global GLP footprints that reassure regulators. ESG-driven procurement policies now permeate board-level risk matrices; companies must document cruelty-free testing to secure shelf space in major retailers. Such pressures integrate across segments, weaving an adoption fabric that elevates the dermal toxicity testing industry beyond niche status.

Geography Analysis

North America’s 42.68% 2025 share reflects a mature CRO landscape, proactive FDA stances, and ample venture capital. The region also hosts the densest cluster of bioprinting start-ups, feeding a continuous pipeline of advanced tissue formats. U.S. tech hubs leverage AI talent to refine toxicity algorithms, while Canada’s 2023 cosmetics ban further entrenches NAM demand.

Europe sustains robust growth through collaborative industry–academic consortia under Horizon grants. France anchors much of the tissue-engineering supply chain, with EPISKIN’s Lyon facility exporting SkinEthic RHE kits worldwide. The dermal toxicity testing market benefits from the EU’s mutual recognition regime, enabling test portability across member states and lowering duplicate-testing expenditures.

Asia-Pacific posts the fastest 6.20% CAGR through 2031 as regulators converge on alternative-testing norms. China’s February 2025 provisions streamline ingredient registration via non-animal data, while its May 2025 comprehensive safety rules and July implementation timetables spur domestic labs to upgrade their capabilities. Japan solicits public feedback on Chemical Substances Control Law updates due by late-2025, aligning with OECD TG revisions. Capacity constraints persist; training programs for cell-culture toxicologists lag demand, creating openings for Western CRO joint ventures. Nonetheless, rising local manufacturing of RHE kits is set to moderate import dependency and deepen the dermal toxicity testing market footprint across Asia.

South America and the Middle East & Africa remain nascent. Brazil pushes regional adoption through ANVISA alignment with OECD TG 439, but fragmented regulations impede uniform adoption. Gulf Cooperation Council countries display interest, especially where luxury-cosmetic imports require cruelty-free certification. Technology transfer partnerships and mobile testing units could bridge infrastructure gaps and drive incremental revenues.

Competitive Landscape

The dermal toxicity testing market exhibits moderate fragmentation: global CROs (SGS, Charles River, Eurofins Scientific) command multi-end-point service suites, while specialized tissue and AI developers cultivate niche differentiation. Barriers to entry include high validation costs, GLP accreditation, and decades-long regulatory rapport. MatTek and EPISKIN maintain leadership in commercial RHE kit supply, leveraging proprietary cell lines and OECD inclusion.

Strategic alliances intensify. L'Oréal’s 10% stake in Galderma in August 2024 merges cosmeceutical biology with clinical dermatology pipelines, amplifying translational research reach. CROs merge or acquire AI firms to capture digital toxicology’s value chain; US BioTek’s March 2024 purchase of RealTime Laboratories broadened diagnostic coverage and expanded geographic reach. Start-ups like MolToxPred license computational engines to incumbents lacking in-house data science, monetizing via per-compound subscription models.

Technology roadmaps favor integrated platforms that can run irritation, sensitization, and absorption tests in a single tissue construct while feeding raw images into cloud-AI dashboards. OECD GLP and ISO 9001 certifications remain market prerequisites, creating compliance moats that protect incumbent share. White-space continues in pediatric dermatology models, microbiome-inclusive skins, and genotype-specific tissues that align with personalized medicine. Vendors addressing these gaps with NAM-ready validation may secure outsized margins over the next five years within the dermal toxicity testing market.

Dermal Toxicity Testing Industry Leaders

Eurofins Scientific

SGS SA

Charles River Laboratories

Labcorp Drug Development

Intertek Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Genoskin showcased fresh findings at the 2026 Society of Toxicology (SOT) annual meeting, underscoring the efficacy of its HypoSkin ex vivo human skin platform as a pioneering human-centric New Approach Methodology (NAM) for proactive safety evaluations.

- April 2025: Researchers from Graz University of Technology and Vellore Institute of Technology developed 3D-printed living skin models for testing cosmetic nanoparticles. These models are stable, non-cytotoxic, and can grow skin tissue, offering a viable alternative to animal testing.

- February 2025: China's NMPA introduced new rules, effective February 6, 2025, to encourage alternative dermal toxicity testing methods. These changes simplify safety assessments and promote faster adoption of non-animal testing in the cosmetics market.

Global Dermal Toxicity Testing Market Report Scope

As per the scope of the report, dermal toxicity testing is the process of evaluating the potential harmful effects of a substance when it comes into contact with the skin. This type of testing assesses whether a chemical or product can cause skin irritation, allergic reactions, or systemic toxicity through dermal exposure.

The segmentation for the dermal toxicity testing market is categorized by test types including in-vitro, in-silico or computational, ex-vivo human skin, and in-vivo animal; by toxicity endpoints such as skin irritation, skin corrosion, dermal sensitization, percutaneous absorption, and phototoxicity and photo-allergy; by end users comprising cosmetics and personal-care companies, pharmaceutical and biotech firms, chemical and agro-chemical manufacturers, CROs and independent toxicology labs, and academic and government research institutes; and by geography covering North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| In-vitro (2-D & 3-D reconstructed human epidermis) |

| In-silico / Computational |

| Ex-vivo Human Skin |

| In-vivo Animal |

| Skin Irritation |

| Skin Corrosion |

| Dermal Sensitization |

| Percutaneous Absorption |

| Phototoxicity & Photo-allergy |

| Cosmetics & Personal-Care Companies |

| Pharmaceutical & Biotech Firms |

| Chemical & Agro-chemical Manufacturers |

| CROs & Independent Toxicology Labs |

| Academic & Government Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | In-vitro (2-D & 3-D reconstructed human epidermis) | |

| In-silico / Computational | ||

| Ex-vivo Human Skin | ||

| In-vivo Animal | ||

| By Toxicity Endpoint | Skin Irritation | |

| Skin Corrosion | ||

| Dermal Sensitization | ||

| Percutaneous Absorption | ||

| Phototoxicity & Photo-allergy | ||

| By End User | Cosmetics & Personal-Care Companies | |

| Pharmaceutical & Biotech Firms | ||

| Chemical & Agro-chemical Manufacturers | ||

| CROs & Independent Toxicology Labs | ||

| Academic & Government Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the dermal toxicity testing market?

It stood at USD 2.16 billion in 2026 and is projected to reach USD 2.82 billion by 2031.

Which test type generates the greatest revenue in dermal safety screening?

Reconstructed human epidermis in-vitro models lead with 41.9% 2025 revenue share.

Why is Asia-Pacific growing fastest in alternative dermal testing?

Chinese and Japanese regulators have issued 2025 guidance that favors non-animal methods, driving a 6.20% CAGR through 2031 for the region.

How are AI tools changing dermal toxicity assessment?

Machine-learning platforms now predict irritation with up to 87.76% AUROC, cutting assay timelines from weeks to days.

Which end-user segment shows the highest future growth?

Pharmaceutical and biotech firms are adopting NAMs rapidly, expanding at a 6.04% CAGR through 2031.

What main barrier limits broad adoption of 3-D tissue models?

High capital costs for GMP-grade bioprinting infrastructure challenge smaller labs, especially in emerging markets.

Page last updated on: