Laboratory Developed Tests Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

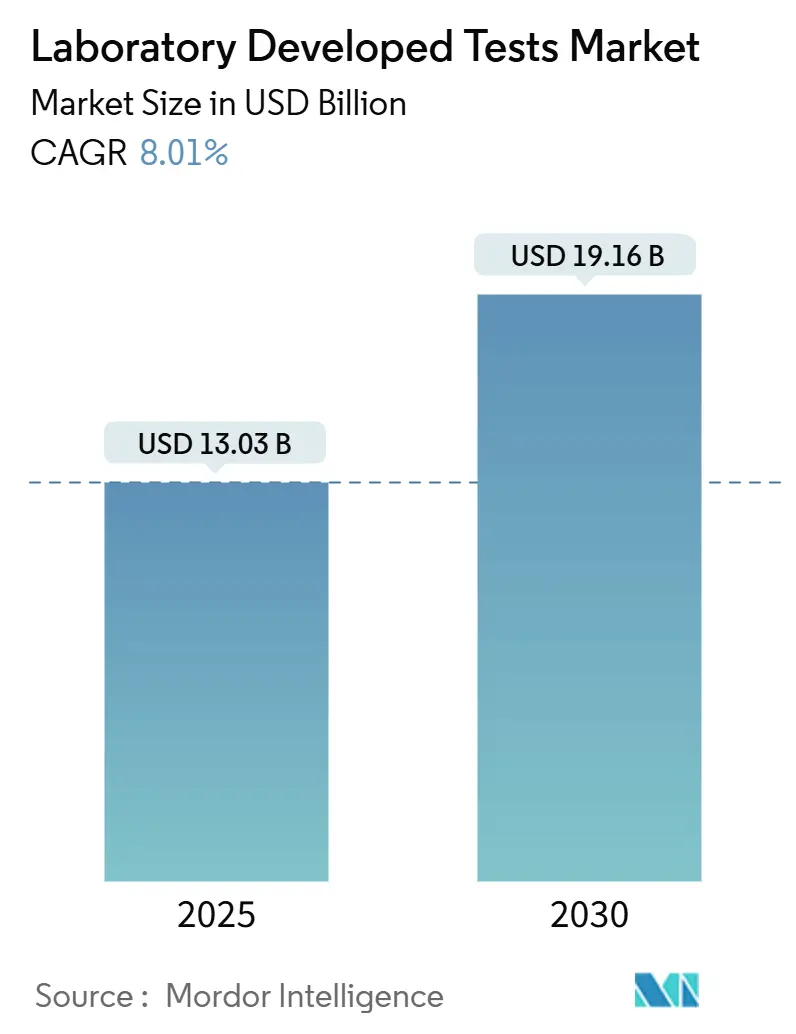

| Market Size (2025) | USD 13.03 Billion |

| Market Size (2030) | USD 19.16 Billion |

| Growth Rate (2025 - 2030) | 8.01% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Developed Tests Market Analysis by Mordor Intelligence

The Laboratory Developed Tests market size reached USD 13.03 billion in 2025 and is forecast to climb to USD 19.16 billion by 2030, reflecting an 8.01% CAGR over the period. This trajectory mirrors a structural pivot away from legacy diagnostics toward precision-medicine-driven assays that depend on rapid sequencing, cloud automation, and evolving oversight. Key forces accelerating growth include the U.S. Food and Drug Administration’s 2024 decision to treat laboratory developed tests as regulated medical devices, the steep slide in next-generation sequencing costs, and rising clinical demand for custom assays in oncology, pharmacogenomics, and rare-disease care. Competitive positioning hinges on balancing stringent compliance costs with innovation speed, a calculation that increasingly favors labs able to deploy AI-enabled workflows at scale. Direct-to-consumer brands also broaden public access, while non-invasive collection kits improve participation rates among pediatrics and remote populations.

Key Report Takeaways

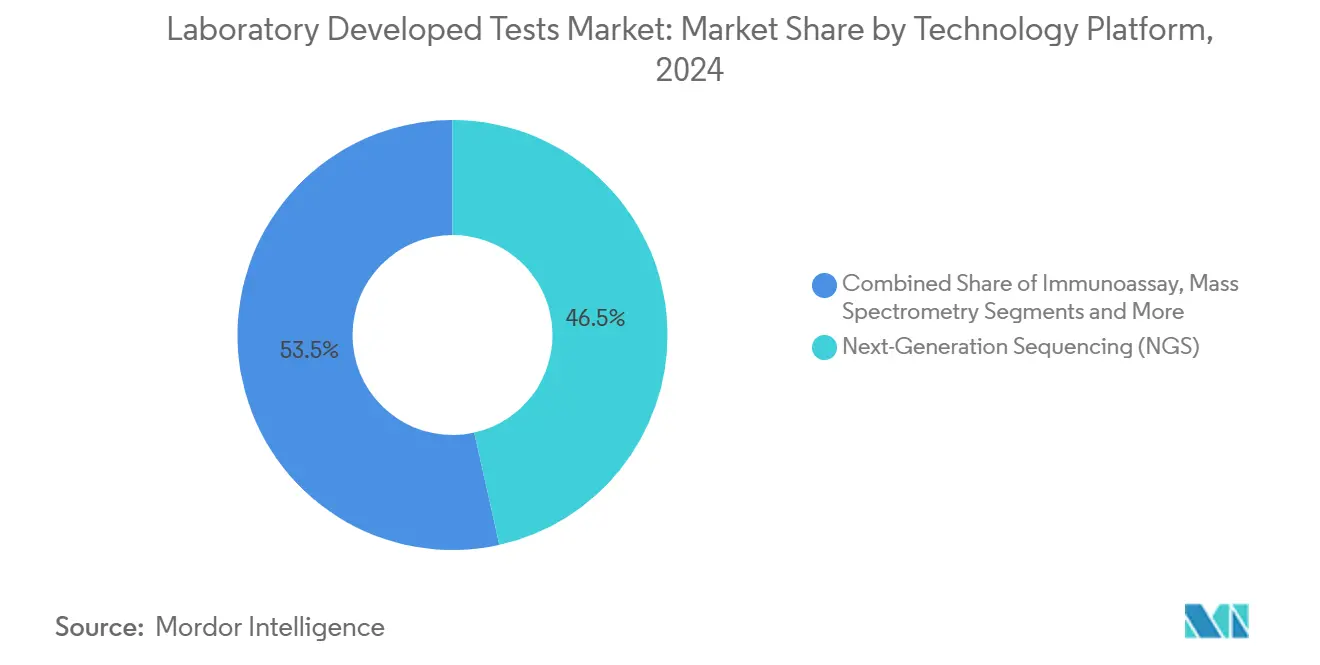

- By technology, next-generation sequencing accounted for 46.51% of the Laboratory-Developed Tests market share in 2024 and remains the fastest-growing platform, with a 12.78% CAGR through 2030.

- By application, oncology held 33.21% of the Laboratory-Developed Tests market in 2024, while rare-disease diagnostics is projected to expand at an 11.63% CAGR over the forecast period.

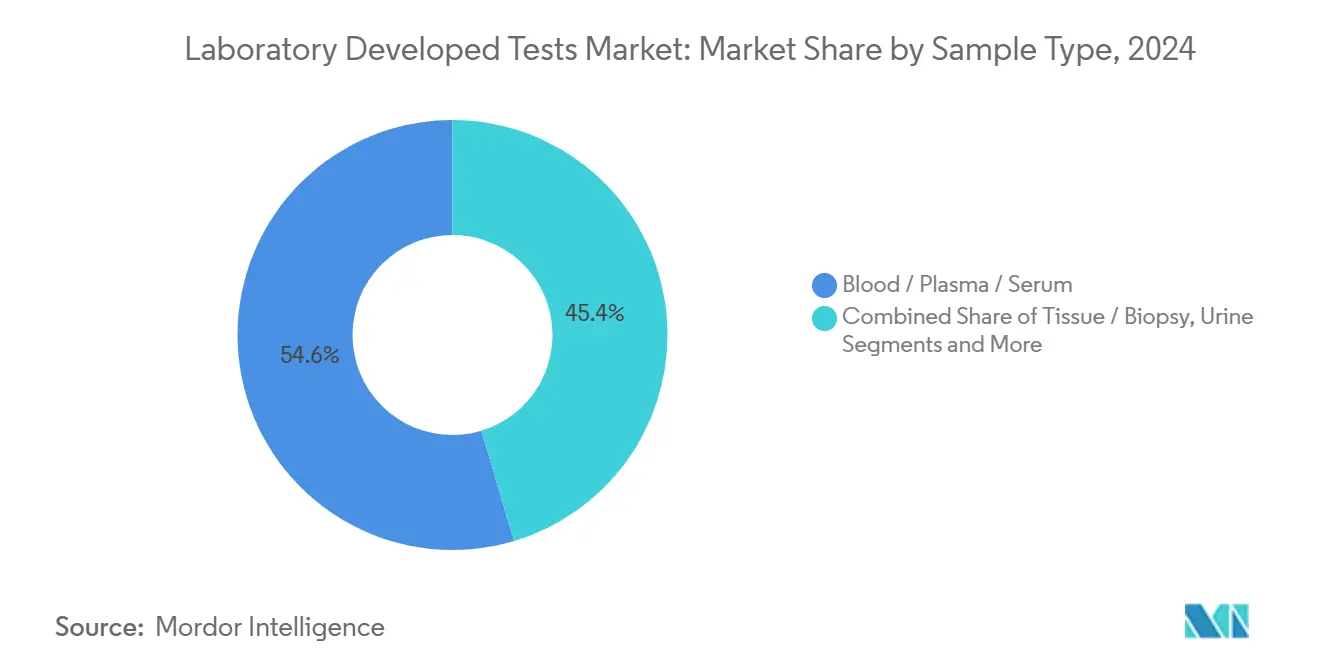

- By sample type, blood/plasma/serum represented 54.63% revenue in 2024; saliva and buccal swabs are advancing at the highest rate, registering an 11.83% CAGR to 2030.

- By end user, hospital-based laboratories captured 44.75% of 2024 revenue, whereas direct-to-consumer providers are growing most quickly at a 10.56% CAGR.

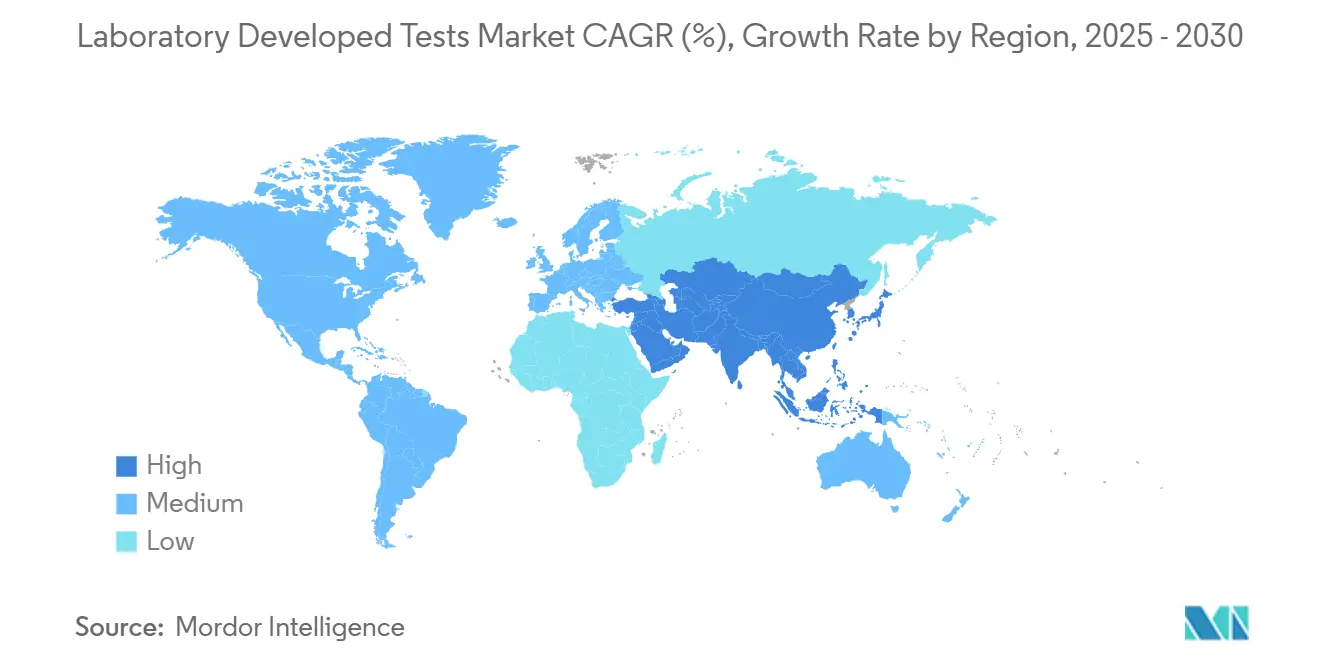

- By geography, North America led with 41.28% revenue share in 2024; Asia-Pacific is set to record a 10.89% CAGR, the fastest of all regions.

Global Laboratory Developed Tests Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-medicine push for genomic LDTs | +2.1% | Global, North America & EU lead | Medium term (2-4 years) |

| Rapid decline in NGS & molecular-diagnostic costs | +1.8% | Global, strongest in Asia-Pacific | Short term (≤ 2 years) |

| High disease burden demanding specialized tests | +1.5% | Global, emerging markets | Long term (≥ 4 years) |

| Regulatory flexibility under CLIA | +1.2% | North America | Medium term (2-4 years) |

| Cloud-based automation & bioinformatics platforms | +0.9% | Global, developed markets | Short term (≤ 2 years) |

| Multi-cancer early-detection liquid-biopsy LDTs | +0.6% | North America & EU, expanding Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision-medicine push for genomic LDTs

Pharmacogenomic assays now help lower adverse-drug-reaction rates by 30%, largely because cytochrome P450 genes influence 70%–80% of drug metabolism.[1]Mitesh Patel, “An Introduction to Pharmacogenomics: A V A Clinician’s Guide,” U.S. Department of Veterans Affairs, va.gov A pending Medicare coverage determination signals wider reimbursement, while AI tools streamline variant interpretation, encouraging hospitals to craft custom panels that commercial kits cannot match. The same framework stimulates bespoke rare-disease diagnostics, closing equity gaps in underserved cohorts.

Rapid decline in NGS & molecular-diagnostic costs

Whole-genome sequencing fell to USD 600 in 2024 from USD 2.7 billion for the first-ever genome, thanks to high-throughput instruments such as NovaSeq X and the UG 100 that shrink per-sample costs. Lower barriers allow regional labs to deploy multi-gene panels across oncology, immunology, and inherited disorders, accelerating the Laboratory Developed Tests market adoption curve.

High disease burden demanding specialized tests

Liquid-biopsy platforms screen multiple cancer types at once, tackling cancers with no routine protocols and supporting earlier interventions.[2]Elena Sokolova, “The Promise and Challenges of Multi-Cancer Early Detection Assays for Reducing Cancer Disparities,” Frontiers in Oncology, frontiersin.org Infectious-disease gaps persist; 90% of American Society for Microbiology member labs rely on LDTs where no FDA-cleared kit exists, especially for rare pathogens.[3]Lisa Sanders, “Promoting Lab Equity with Laboratory Developed Tests,” American Society for Microbiology, asm.org Growing chronic-disease loads in aging populations guarantee sustained demand.

Regulatory flexibility under CLIA

CLIA lets certified labs validate tests internally without device pre-market approval, fostering agility. New 2025 rules strengthen quality-system controls. The balance of oversight and autonomy keeps the Laboratory-Developed Tests market innovative even as FDA oversight rises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Looming FDA/VALID Act regulation & compliance cost | -1.4% | North America; global multinationals | Short term (≤ 2 years) |

| Reimbursement uncertainty for complex LDTs | -1.1% | Global, developed markets | Medium term (2-4 years) |

| Shortage of bioinformatics talent | -0.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Supply-chain fragility for specialized reagents | -0.5% | Global, vulnerable in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Looming FDA/VALID Act regulation & compliance cost

The 2024 final rule forces labs to absorb USD 1.29 billion in annual compliance spending for phased-in device requirements, sparking legal challenges and raising entry barriers for small facilities. High fixed costs may accelerate consolidation and slow innovation.

Reimbursement uncertainty for complex LDTs

Payers hesitate to cover multi-cancer blood tests and polygenic risk scores until long-term outcomes data emerge, creating financial risk for labs launching novel assays. Variable Medicare policies further complicate budgeting for test deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Sequencing Platforms Expand Clinical Reach

Next-generation sequencing held 46.51% of Laboratory Developed Tests market share in 2024 and is accelerating at a 12.78% CAGR, underscoring its transition from discovery research to routine patient care. Sequencing now anchors tumor profiling, carrier screening, and constitutional variant detection. Targeted panels dominate for cost efficiency, though whole-exome options grow in complex cases. Molecular-diagnostic stalwarts such as RT-PCR retain footholds where single-gene sensitivity or viral-load quantification is critical, but are losing share as multiplexed NGS panels prove more comprehensive. Immunoassay and mass-spectrometry platforms carve specialized niches—MALDI-TOF cuts microbial ID turnaround by a full day—yet cannot match sequencing breadth. The Laboratory Developed Tests market thus rewards hybrid laboratories that integrate NGS with orthogonal technologies to deliver end-to-end insights.

Clinical labs pursuing integrated workflows combine sequencing readouts with mass-spectrometry metabolite data for pharmacogenomic correlation and pair digital PCR with NGS for minimal-residual-disease tracking. Platform diversification hedges reimbursement risk and boosts throughput, positioning multi-modal facilities to capture cross-disciplinary demand.

By Application: Rare-Disease Testing Outpaces Oncology

Oncology retained 33.21% of 2024 revenue as liquid-biopsy assays gained traction; nonetheless rare-disease diagnostics is projected to log an 11.63% CAGR through 2030 as national newborn programs and patient-advocacy funding expand coverage. Multi-cancer early-detection blood tests broaden oncology reach, while digital-PCR monitoring improves chronic myeloid leukemia management precision. Infectious-disease panels sustain baseline volume amid respiratory-virus seasonality, whereas pharmacogenomics sees hospital formularies adopt CYP2C19 and DPYD tests for adverse-event mitigation.

Prenatal screening benefits from cell-free-DNA panels that now scan more than 1,000 genes, pushing detection beyond aneuploidy into monogenic disorders with clinical actionability. Each application line forces laboratories to refine validation protocols, but those that master multi-disciplinary assay design capture outsized referral streams.

By Sample Type : Non-invasive kits accelerate participation

Blood, plasma, and serum samples accounted for 54.63% of the Laboratory Developed Tests market share in 2024, reflecting entrenched clinical workflows for high-sensitivity assays. Saliva and buccal swab collections, however, represent the fastest-expanding category, with the Laboratory Developed Tests market size for these non-invasive specimens projected to grow at an 11.83% CAGR between 2025 and 2030. Validation studies confirm that saliva-derived genomic DNA delivers variant-calling concordance comparable with blood for whole-genome and whole-exome sequencing. Higher patient acceptance is another pull factor; FDA-cleared saliva kits yield 200% better donor-compliance rates than venipuncture, an advantage that broadens testing access for pediatric and home-collection programs.

Room-temperature stability and integrated stabilization reagents simplify global shipping logistics, eliminating cold-chain expense and enabling outreach into remote regions. Laboratories also benefit from streamlined automation because non-hazardous saliva matrices integrate easily with high-throughput liquid-handling robots. Tissue and biopsy samples remain indispensable for histopathological correlation and tumor-microenvironment studies, whereas urine and other bodily fluids service niche applications such as metabolic screening. Taken together, specimen diversification positions labs to capture wider demographic coverage while reducing pre-analytical barriers that historically suppressed testing volumes.

By End User : Hospital hubs dominate as direct-to-consumer growth quickens

Hospital-based laboratories captured 44.75% of 2024 revenue, leveraging embedded clinician networks and electronic medical record integration to retain complex case referrals. The Laboratory-Developed Tests market size tied to hospitals is forecast to expand more slowly than overall growth as budgetary pressures encourage outsourcing of esoteric assays. Direct-to-consumer providers, by contrast, are scaling at a 10.56% CAGR through 2030 by marketing mail-in kits, transparent pricing, and telehealth counseling that resonate with convenience-oriented patients.

Independent reference laboratories operate hub-and-spoke logistics that give community hospitals same-day access to sophisticated panels, while academic medical centers remain incubators for novel biomarkers and ultra-rare disease testing. Consolidation is intensifying: Quest Diagnostics’ and LabCorp’s hospital-lab acquisition sprees seek to widen geographic coverage and capitalize on economies of scale. Specialty clinics and physician-office labs hold unique turf in women’s health, fertility, and infectious-disease niches, often launching bespoke tests that fill gaps left by commercial kit makers. Competition therefore hinges on the ability to pair clinical credibility with digital-first service models that satisfy both physicians and empowered consumers.

Geography Analysis

North America generated 41.28% of global revenue in 2024 as CLIA flexibility and generous reimbursement frameworks fostered rapid Laboratory Developed Tests adoption, yet impending FDA device-style oversight introduces compliance costs that may favor large-scale operators. Canada contributes steady demand through provincial health plans that reimburse advanced sequencing, whereas Mexico’s private-sector expansion is creating fresh channels for custom oncology and prenatal panels.

Europe follows closely with mature diagnostic infrastructure but heterogeneous regulation. Germany’s alignment with IVDR imposes rigorous analytical-performance documentation, while the United Kingdom’s post-Brexit pathway lets domestic labs pilot novel tests under a bespoke notificational regime. Southern markets such as Italy and Spain show growing uptake of pharmacogenomics as payers weigh real-world cost-avoidance data. Collectively, these factors sustain mid-single-digit growth across the continent.

Asia-Pacific is the clear momentum story, with the Laboratory Developed Tests market size in the region forecast to climb at a 10.89% CAGR through 2030. China’s plan to modernize in vitro diagnostic regulation by 2027, coupled with large-scale hospital-network upgrades, underpins sequencing demand. Japan is evaluating a dedicated LDT framework to accelerate clinical implementation, and India’s genomics initiatives extend testing reach into secondary-care centers. Australia and South Korea round out developed-market dynamics with national insurance coverage for several NGS panels. Despite infrastructure gaps, Middle East and Africa are registering double-digit test-volume growth in Gulf Cooperation Council states that fund comprehensive cancer-screening programs, signaling long-term potential once laboratory capacity scales.

Competitive Landscape

Market concentration is moderate, leaving ample share for regional specialists. Quest Diagnostics and LabCorp deploy scale economics and acquisition playbooks, exemplified by Quest’s 2024 purchase of University Hospitals’ lab assets. Mayo Clinic Laboratories leverages academic prestige to win complex case referrals, while ARUP Laboratories focuses on esoteric assays. Oncology-centric companies such as Guardant Health and NeoGenomics capture fast-growing niches through proprietary liquid-biopsy and hematologic-malignancy panels. Technology alliances matter; Illumina’s 2025 pact with Tempus AI layers deep-learning analytics atop sequencing hardware, tightening end-to-end integration.

Automation, AI, and cloud connectivity now separate leaders from followers. Labs investing in robotic library prep and real-time QC achieve lower error rates and faster turnaround, while smaller players without capital scale may exit highly regulated segments post-2028. The Laboratory Developed Tests market thus balances consolidation with continual entry by specialized innovators addressing unmet needs.

Laboratory Developed Tests Industry Leaders

Quest Diagnostics

LabCorp

Mayo Clinic Laboratories

Eurofins Scientific

Sonic Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nordic Bioscience unveiled nordicEndotrophin, an automated assay quantifying intact Endotrophin hormone, demonstrating prognostic utility in fibrosis and oncology studies.

- April 2025: Illumina and Tempus AI formed a strategic alliance to standardize NGS workflows across oncology, cardiology, and neurology by embedding multimodal AI algorithms.

Global Laboratory Developed Tests Market Report Scope

| Molecular Diagnostics | RT-PCR |

| qPCR | |

| Digital PCR | |

| Next-Generation Sequencing (NGS) | Targeted Sequencing |

| Whole Genome Sequencing | |

| Whole Exome Sequencing | |

| Immunoassay | ELISA |

| Chemiluminescence Immunoassay | |

| Lateral Flow Assay | |

| Mass Spectrometry | MALDI-TOF |

| LC-MS | |

| Cytogenetics / Chromosomal Analysis | FISH |

| Karyotyping | |

| Others |

| Infectious Disease |

| Oncology |

| Genetic / Hereditary Testing |

| Prenatal Screening |

| Pharmacogenomics |

| Rare Disease Diagnostics |

| Others |

| Blood / Plasma / Serum |

| Tissue / Biopsy |

| Saliva / Buccal Swab |

| Urine |

| Other Bodily Fluids |

| Hospital-based Laboratories |

| Academic & Research Institutions |

| Independent Reference Laboratories |

| Specialty Clinics & Physician Office Labs |

| Direct-to-Consumer Testing Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology/Platform | Molecular Diagnostics | RT-PCR |

| qPCR | ||

| Digital PCR | ||

| Next-Generation Sequencing (NGS) | Targeted Sequencing | |

| Whole Genome Sequencing | ||

| Whole Exome Sequencing | ||

| Immunoassay | ELISA | |

| Chemiluminescence Immunoassay | ||

| Lateral Flow Assay | ||

| Mass Spectrometry | MALDI-TOF | |

| LC-MS | ||

| Cytogenetics / Chromosomal Analysis | FISH | |

| Karyotyping | ||

| Others | ||

| By Application | Infectious Disease | |

| Oncology | ||

| Genetic / Hereditary Testing | ||

| Prenatal Screening | ||

| Pharmacogenomics | ||

| Rare Disease Diagnostics | ||

| Others | ||

| By Sample Type | Blood / Plasma / Serum | |

| Tissue / Biopsy | ||

| Saliva / Buccal Swab | ||

| Urine | ||

| Other Bodily Fluids | ||

| By End User | Hospital-based Laboratories | |

| Academic & Research Institutions | ||

| Independent Reference Laboratories | ||

| Specialty Clinics & Physician Office Labs | ||

| Direct-to-Consumer Testing Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Laboratory Developed Tests market in 2025?

The market is valued at USD 13.03 billion in 2025 with an 8.01% CAGR expected through 2030.

Which technology leads Laboratory Developed Tests adoption?

Next-generation sequencing holds 46.51% revenue share in 2024 and is growing fastest at 12.78% CAGR.

What region is expanding most quickly?

Asia-Pacific is on track for a 10.89% CAGR owing to regulatory reforms and falling sequencing costs.

Why do saliva kits matter for clinical genomics?

Saliva collection drives 200% higher donor compliance versus blood and yields DNA quality comparable for whole-genome sequencing.

How will FDA oversight affect small laboratories?

New medical-device-style rules raise compliance spending, which may pressure smaller labs to merge or exit specialized testing segments.

Which end-user group shows the fastest growth?

Direct-to-consumer providers are advancing at 10.56% CAGR as home-collection kits and telehealth counseling gain popularity.

Page last updated on: