Sterility Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.96 Billion |

| Growth Rate (2026 - 2031) | 10.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterility Testing Market Analysis by Mordor Intelligence

The sterility testing market size was valued at USD 1.59 billion in 2025 and estimated to grow from USD 1.76 billion in 2026 to reach USD 2.96 billion by 2031, at a CAGR of 10.92% during the forecast period (2026-2031). This trajectory mirrors the convergence of EU GMP Annex 1’s zero-CFU requirement, the commercialization of complex biologics pipelines, and rapid-release methods that compress drug-to-patient cycles. Persistent venture capital inflows into cell and gene therapy, mounting public-sector vaccine procurement, and the migration of sterile fill-finish capacity to contract partners further energize demand. Membrane filtration maintains its long-established foothold, yet rapid microbial detection platforms are gaining regulatory favor, enabling batch disposition in hours rather than weeks. North America’s sophisticated regulatory ecosystem underpins its leadership, while Asia Pacific’s emerging mega-plants, preferential tax regimes, and harmonized pharmacopeial updates push it toward the highest regional CAGR.

Key Report Takeaways

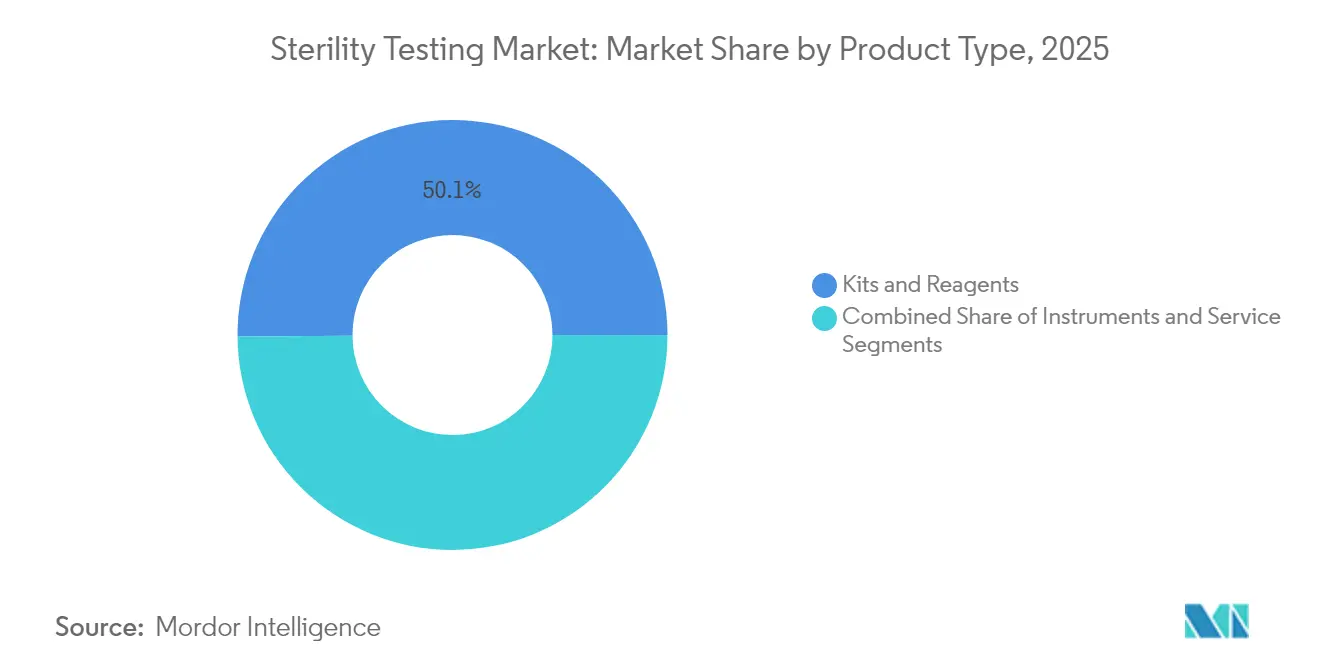

- By product type, kits and reagents commanded 50.12% of the sterility testing market share in 2025; meanwhile, services are on track to expand at a 10.48% CAGR through 2031.

- By test type, membrane filtration captured 70.85% of the sterility testing market in 2025, whereas rapid sterility tests show a 14.45% CAGR outlook to 2031.

- By application, pharmaceutical and biologics manufacturing contributed 64.55% of the sterility testing market size in 2025, with outsourced CDMO testing accelerating at 12.05% CAGR into 2031.

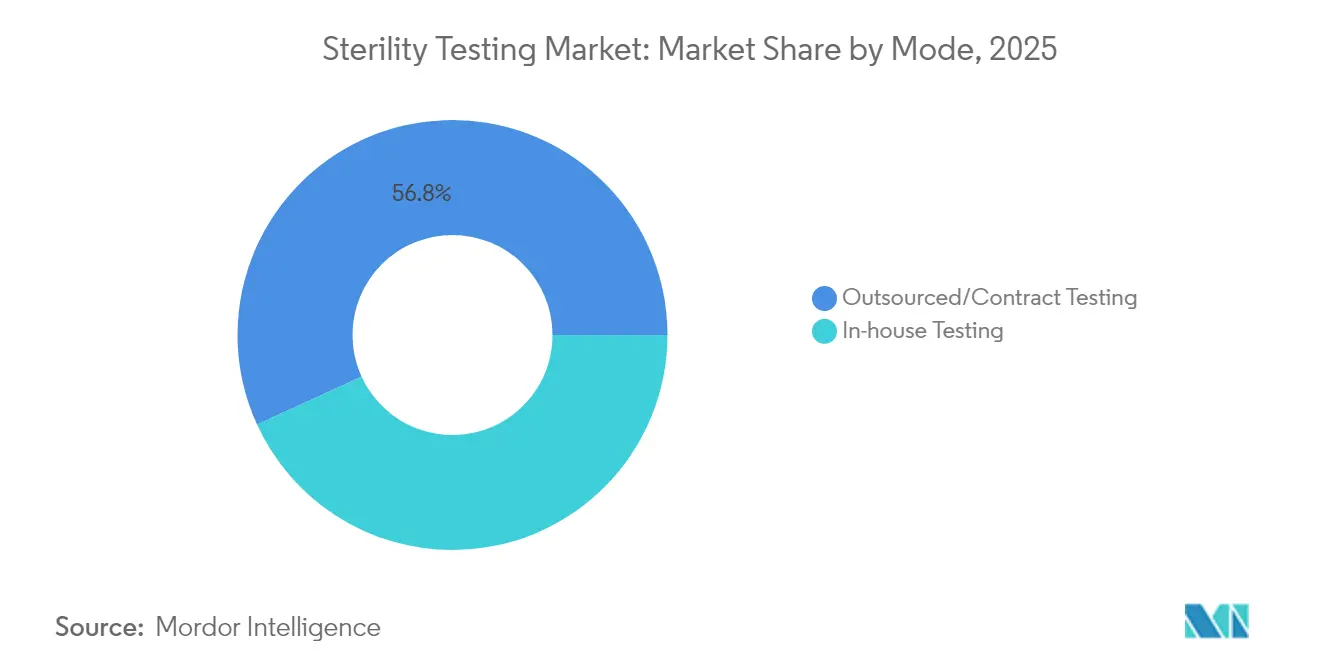

- By mode, outsourced/contract testing captured 56.84% of the sterility testing market share in 2025 and is projected to grow at an 8.54% CAGR between 2026 and 2031.

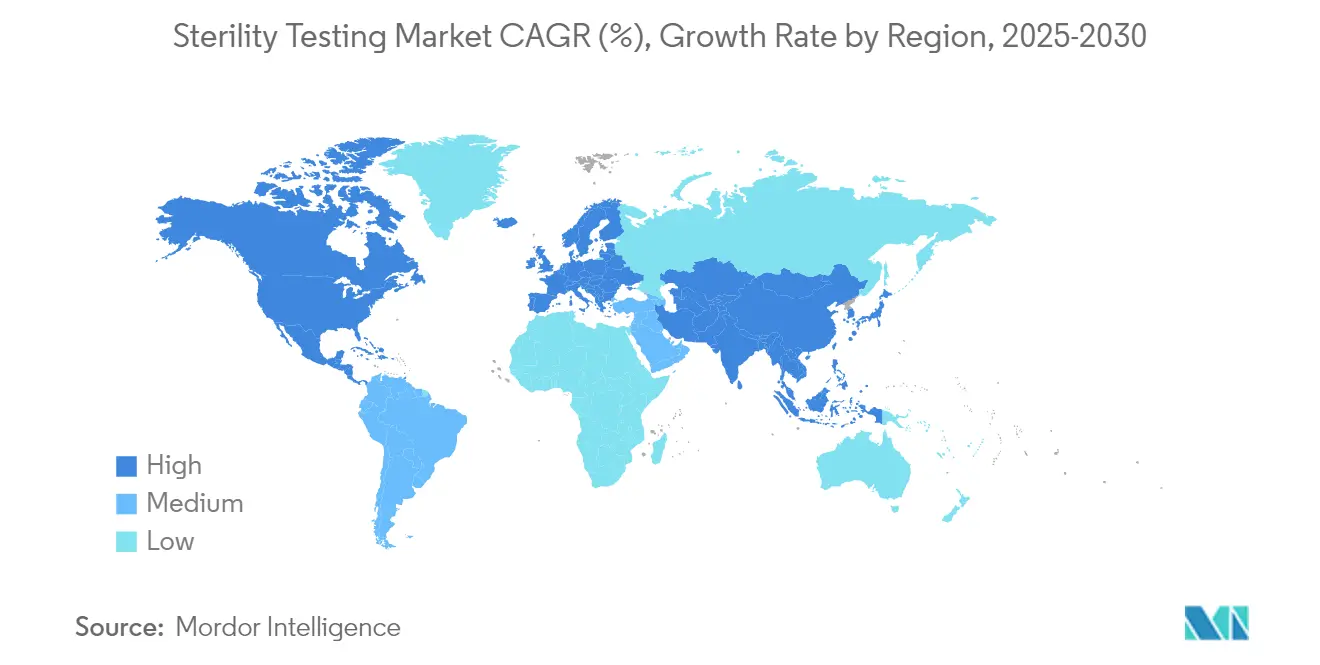

- By geography, North America generated 41.86% of global revenue in 2025, while Asia Pacific is projected to climb at 9.58% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sterility Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GMP upgrades for advanced biologics pipelines | +2.80% | Global, spearheaded by the EU and US | Medium term (2-4 years) |

| Surge in cell & gene-therapy commercial batches needing rapid-release tests | +2.10% | North America and EU, rippling into APAC | Short term (≤ 2 years) |

| Shift from in-house QC to outsourced CDMO sterility services | +1.90% | Worldwide, strongest in North America | Medium term (2-4 years) |

| Adoption of modular isolator systems that curb false positives | +1.50% | EU and North America, expanding toward APAC | Long term (≥ 4 years) |

| Regulatory push for validated rapid microbiological methods | +1.30% | Global, with EU GMP Annex 1 as catalyst | Medium term (2-4 years) |

| Rising demand for single-use technology compatible test kits | +1.00% | Biologics hubs worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent GMP Upgrades For Advanced Biologics Pipelines

The revision of EU GMP Annex 1 lengthened guidance from 16 to 59 pages and formalized the zero-CFU tolerance in Grade A environments, prompting a surge in capital expenditures on isolators, viable monitoring, and pre-use post-sterilization integrity testing.[1]European Commission, “Annex 1 Manufacture of Sterile Medicinal Products,” ec.europa.eu PUPSIT protocols, mandatory airflow diagrams, and digital data-integrity logs have become baseline requirements for marketing-authorization sponsors operating multi-site networks. Harmonization between the EMA and FDA narrows procedural divergence, letting multi-country manufacturers standardize validation master plans and accelerate lot-release decisions.

Surge In Cell & Gene-Therapy Commercial Batches Needing Rapid-Release Sterility Tests

More than 1,200 active US clinical studies and a wave of autologous approvals intensify the call for sterility confirmation within a 4-hour window to safeguard living-cell potency. bioMérieux’s SCANRDI exploits solid-phase cytometry to detect single viable but non-culturable organisms, cutting time-to-result from 14 days to under 150 minutes while meeting USP <1223> acceptance criteria. FDA biologics license applications referencing rapid methods validate their commercial reliability and embolden smaller sponsors to replace legacy protocols.

Shift From In-House QC To Outsourced CDMO Sterility Services

Current CDMO industry’s growth illustrating the pharma sector’s reliance on specialty partners for sterility analytics at scale. Eurofins now operates more than 45 GMP labs that integrate sterility, endotoxin, and particulate testing, creating one-stop hubs for global batch release. The model shields drug owners from skilled labor shortages while ensuring 24/7 redundancy across continents.

Adoption Of Modular Isolator Systems That Curb False Positives

Modular isolators yield ISO 14644-7 compliance, sustain Grade A uni-directional airflow, and reduce operator-triggered excursions that previously drove 35% of false-positive investigations. IonHP+ decontamination cycles yield ≥6-log microbial reduction in 15 minutes without chlorine residuals. Capital-weighted business cases showcase breakeven within two high-value product write-offs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of Class B isolator infrastructure | -1.80% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Limited global harmonization of compendial test standards | -1.20% | Global, with regional variations in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Acute shortage of skilled microbiologists in emerging markets | -1.00% | Asia Pacific, Latin America, and MEA | Medium term (2-4 years) |

| False-positive risk in direct-inoculation tests delaying releases | -0.80% | Global, with higher impact in high-volume manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Class B Isolator Infrastructure

Acquiring a dual-chamber isolator with automatic leak-test modules costs upward of USD 300,000, excluding validation and annual service contracts. Inspections citing data-integrity lapses at under-spec Chinese sterility labs underscore the risk of under-investment and force even start-ups to allocate disproportionate capex.

Limited Global Harmonization of Compendial Standards

Disparities among USP, EP, JP, and the Chinese pharmacopeia drive duplicative validation, elevate consumables inventory, and expose multinational sponsors to asynchronous revisions. China’s YY 1001-2024 standard for glass syringes illustrates region-specific mandates that extend analytical timelines and inflate compliance cost structures.[2]CRDB, “YY 1001-2024 Glass Syringe Standard,” crdb.gov.cn

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Expand as the Sector’s Workhorse

Services exhibit a 10.48% CAGR, reflecting industry eagerness to outsource sophisticated assays amid microbiologist scarcity. The sterility testing market benefits as leading CDMOs embed QC suites next to aseptic filling lines, enabling “test where you make” paradigms that slash logistic dwell. Kits and reagents, holding 50.12% revenue share, remain resilient by servicing decentralized quality-control points at small and midsize manufacturers. Single-use manifolds, color-change growth media, and off-the-shelf 0.45 µm hydrophilic PVDF membranes preserve relevance even as automation spreads. Instruments form the leanest revenue slice yet the highest innovation quotient. Growth Direct modules now incubate 126 cassettes simultaneously and integrate AI image analytics, delivering official sterility reads in 48 hours at high confidence thresholds.

Continued commoditization of agar plates pressures kit margins, motivating suppliers to bundle cloud-based analytics and traceability software. Services vendors capitalize on their consultative expertise, providing deviation investigations, contamination-source mapping, and right-first-time documentation for pre-approval inspections. Jabil’s 360,000-sq-ft Pii campus in Maryland integrates sterile fill-finish with on-site microbiology labs, illustrating horizontal expansion that keeps samples on campus and reduces chain-of-custody risk. In parallel, regional labs in Ireland, Singapore, and São Paulo run 24-hour shifts to absorb accelerated release testing for parenterals destined for pandemic-preparedness stockpiles. As sponsors pivot from supplier-of-last-resort to strategic partnership mentality, service revenue streams gain multi-year visibility—bolstering the sterility testing market as a dependable annuity.

By Test Type: Membrane Filtration Dominance Faces Rapid-Test Momentum

Membrane filtration continues to anchor at 70.85% usage and is preferred for low-viscosity injectables and ophthalmics. Its entrenched pharmacopoeial footprint, uncomplicated consumables, and 0.45 µm nominal pore size facilitate consistent validation. Yet the 14-day incubation window conflicts with biologic shelf lives. The sterility testing market is therefore witnessing a 14.45% CAGR swell for rapid sterility tests validated under USP <71> alternative methods language. Nelson Labs’ 6-day post-inoculation bioluminescence readout meets EP Chapter 2.6.1 requirements for finished product release, providing tangible inventory-holding savings.

Direct inoculation, while simple for small-volume liquids, is increasingly scrutinized: complex excipients hinder turbidity interpretation and amplify false positives. Redberry’s optical-density-free fluorescence enumeration enables detection of single organisms in opaque matrices within 4 days, matching risk-based release drives without sacrificing sensitivity. Nonetheless, regulators still expect dual validation across legacy and alternative methods, prolonging transitional overlap. As AI-driven digital colony counters receive 510(k) clearance, the sterility testing market anticipates a progressive blend, where membrane filtration dominates bulk biologics and rapid tests liberate cell-therapy lots from cold-chain bottlenecks.

By Mode: Outsourcing Displaces In-House Paradigms

Outsourced/contract testing captured 56.84% of the sterility testing market share in 2025, as chronic labor gaps underscore the sterility testing market’s structural pivot to outsourcing. Industry surveys reveal 34% of newly budgeted hires target QC microbiology, yet fill rates lag at 66%. Meanwhile, biopharma 4.0 initiatives usher in data-rich processes that outpace legacy skill sets. CDMOs offset talent scarcity through centralized training academies and robotic workflows. The APAS Independence colony analyzer, cleared in the US, EU, and Australia, enables lights-out environmental monitoring with AI pattern recognition, reinforcing service-provider economies of scale.

Sponsors are still performing in-house sterility testing of face capex waves: isolator retrofits, Annex 1-compliant HVAC recertification, and electronic batch-record integration. Consequently, the sterility testing market reports double-digit service revenue growth while in-house kit consumption inches forward at mid-single digits. As regulators advocate data integrity via GAMP 5 and ALCOA+ principles, midsize firms concede that outsourcing brings both technical depth and compliance audit preparedness.

Geography Analysis

North America’s 41.86% revenue share stems from its dense biologics licensure pipeline, aggressive venture funding, and the FDA’s well-articulated sterility guidelines that incentivize early adoption of rapid methods. STERIS commissioned two new validation labs in Massachusetts and California during 2024 which provide same-day membrane filtration setup, shortening cross-country shipment lags. The region houses a mature CDMO cluster across the North-East corridor and the Texas-North Carolina biologics belt, generating network effects in consumables procurement and method harmonization. Workforce gaps persist; vacancy rates surpass 15% among QC analysts, pushing firms to create apprenticeship pathways with local colleges.

Asia Pacific exhibits a 9.58% CAGR, the fastest among all regions, driven by policy incentives, scaled vaccine campaigns, and private equity funding for multi-tenant bioparks. China’s recent mandate aligning domestic test standards with PIC/S intensifies demand for Annex 1-grade isolators. Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) actively pilots remote inspections aided by cloud-based environmental monitoring, spurring adoption of digital platforms. India’s Hyderabad Genome Valley adds 1.8 million sq ft of sterile manufacturing space by 2026, widening downstream sterility testing workloads. However, inconsistent enforcement across ASEAN nations necessitates dual testing strategies, mildly eroding margin realization for service exporters. The sterility testing market benefits as global sponsors opt to replicate critical tests in US or EU labs before product launch.

Europe’s outlook remains steady, buoyed by Annex 1’s full enforcement in August 2023. Germany, the UK, and France lead in isolator retrofits, with small-batch biologics plants upgrading to fully integrated HEPA-filtered barrier systems. The EU’s Fit-for-55 carbon targets spur suppliers to engineer low-energy vaporized hydrogen peroxide cycles, an emerging purchasing criterion. Smaller European economies such as Belgium and Denmark leverage national life-science clusters to court CDMO expansions, adding regional service capacity for Scandinavian and Benelux markets. Meanwhile, Central and Eastern Europe pitch cost-efficient labor pools, though slower regulatory turnaround times temper rapid testing adoption.

Regulatory Landscape

Sterility testing requirements are being tightened through GMP expectations for sterile drug manufacturing and updated sterilization and biocompatibility standards for medical devices. In Europe, the full enforcement of EU GMP Annex 1 (effective August 2023) continues to anchor contamination control strategy requirements, reinforcing validated sterility assurance practices and the documentation needed for batch release. In the United States, FDA guidance for 510(k) submissions for devices labeled as sterile (updated in January 2024) and FDA actions focused on sterilization continuity, including finalized enforcement discretion in November 2024 for certain EtO sterilization facility changes for Class III devices, influence how manufacturers update processes while maintaining supply.

Standards harmonization is also progressing. In April 2025, the EU published Commission Implementing Decision (EU) 2025/679, harmonizing EN 556-1:2024 and EN 556-2:2024 for terminally sterilized and aseptically processed medical devices. In January 2026, Commission Implementing Decision (EU) 2026/197 harmonized EN ISO 17665:2024 (moist heat sterilization) among referenced standards. ISO updates affecting sterility assurance workflows include ISO 10993-7:2026 (published April 2026), which updates limits and testing procedures for residual ethylene oxide and ethylene chlorohydrin, increasing the need for aligned test methods and traceable, audit-ready data packages across jurisdictions.

Competitive Landscape

The sterility testing market displays moderate fragmentation. bioMérieux’s 3P ENTERPRISE merges smart plates, automated incubation, and real-time colony enumeration, freeing operators from subjective plate reads while feeding audit-ready datasets into LIMS. Thermo Fisher’s planned USD 4.1 billion takeover of Solventum’s Purification & Filtration business extends its capabilities across upstream filtration and downstream QC, promising bundled offers that couple sterilizing-grade filters with membrane-filtration validation discs. Charles River Laboratories scales its Celsis platform, integrating ATP-bioluminescence with provenance-tracking barcodes to meet Annex 1’s contamination-control strategy documentation.

KBI Biopharma partners with Argonaut Manufacturing Services to knit upstream cell-culture analytics with aseptic fill-finish. Equipment makers like Syntegon embed settle-plate changers into modular fillers, offloading 80% of manual viable monitoring steps. Robotics firms, exemplified by Stäubli’s Sterimove, push autonomous Grade A/B payload transfer, reducing gowning contamination risk. For emerging markets, suppliers embed remote-maintenance modules and augmented-reality troubleshooting, helping offset local talent deficits.

White-space opportunities concentrate on training and digitalization. Firms offering virtual-reality aseptic-process simulations and AI-driven root-cause analytics cultivate loyalty among resource-constrained manufacturers. Meanwhile, ESG mandates prompt providers to develop low-chemical decontamination and recyclable single-use consumables, carving fresh differentiation lanes. Overall, the sterility testing market rewards vendors able to bundle compliant technology, global service networks, and workforce upskilling under a unified value proposition.

Sterility Testing Industry Leaders

Charles River Laboratories

bioMérieux SA

Merck KGaA

SGS SA

Sotera Health (Nelson Laboratories, LLC)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Service capacity additions and more integrated CDMO testing models are creating space for accelerated sterility assurance offerings, especially when sponsors seek shorter logistics chains and faster batch disposition. Pace Life Sciences expanded its Lebanon, New Jersey microbial limits testing laboratory in April 2026 to increase throughput for sterility and microbial testing services. Nelson Labs initiated a major cleanroom expansion at its Salt Lake City, Utah headquarters in June 2025 to double existing ISO-classified cleanroom capacity. In Europe, Nelson Labs expanded its Wiesbaden, Germany facility in August 2025 by adding four new laboratories for microbiological and packaging testing, pointing to continued demand for regionalized sterility and release-support services.

A second opportunity lane is the practical deployment of rapid microbial testing methods and isolator-based sterility testing aligned to Annex 1 contamination-control expectations, where validation effort and reference standards remain gating items. In May 2026, 3PBIOVIAN strengthened sterility testing capabilities by integrating isolator-based testing into its CDMO portfolio, reflecting a broader move toward barrier-based workflows that reduce operator intervention and investigation burden. Method modernization is also supported by standardization work such as NIST-led efforts on rapid microbial testing methods and reference materials beyond CFU, which provides a clearer path for wider adoption of alternative methods in regulated release testing.

Recent Industry Developments

- June 2026: bioMerieux launched SCANRDI CELL-BURST technology for same-day sterility testing in cell and gene therapy manufacturing. The introduction targets short-lived products where traditional incubation timelines constrain release decisions. This strengthens the commercial case for rapid sterility testing platforms in advanced therapies QC.

- May 2026: Charles River Laboratories and MEDIPOST Co., Ltd. signed a strategic non-exclusive MOU to collaborate on GMP-compliant testing solutions supporting MEDIPOSTs global cell therapy pipeline. The collaboration expands the role of outsourced testing partners in complex biologics quality control. It reinforces service-led demand for validated rapid and specialized microbiology workflows.

- May 2024: Merck KGaA (MilliporeSigma) launched M-Trace Software and a mobile app to digitize microbial quality control workflows and provide end-to-end data traceability in sterility testing laboratories. This supports data integrity and faster investigations by reducing manual documentation steps. It also integrates traceable records into QC operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from sterility testing kits and reagents, instruments, and outsourced laboratory services used to confirm the absence of viable microorganisms before release of finished pharmaceutical, biopharmaceutical, and medical device batches.

Scope exclusions: Environmental monitoring consumables and in-process bioburden tests performed during upstream production are excluded.

Segmentation Overview

- By Product Type

- Instruments

- Kits & Reagents

- Services

- By Test Type

- Membrane Filtration

- Direct Inoculation

- Rapid Sterility Tests

- By Application

- Pharmaceutical & Biologics Manufacturing

- Medical Device Manufacturing

- Others

- By Mode

- In-house Testing

- Outsourced/Contract Testing

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- Saudi Arabia

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the factual base for the model and to set realistic boundaries on what sterility testing revenues include. We typically rely on public sources such as the US FDA, the European Medicines Agency, pharmacopeia compendia and public monographs (USP and EP), and the World Health Organization for sterility related expectations and testing norms. To ground demand signals, we also refer to sources such as US CDC, OECD health statistics, and customs or trade statistics where relevant for lab instruments and consumables.

Alongside official sources, we reviewed company annual reports, 10-K style filings, investor presentations, product catalogs, and reputable press coverage to map testing adoption, outsourcing trends, and pricing direction across pharma and device manufacturing. A paid subscription for company financials and intelligence was used selectively to normalize revenues and business mix for private and public participants. The sources listed here are illustrative, and many other public and paid sources were also reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with quality leaders, microbiology lab managers, and service providers supporting sterile manufacturing release. Respondent inputs were used to sanity check sterility test volumes, the split between in-house and outsourced testing, and the pace of rapid sterility test adoption across major regions. This also helped tighten assumptions where public sources did not specify enough detail on test mix and service intensity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 20% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where sterile drug and device production activity is translated into a testing demand pool, and then mapped to spend on sterility testing consumables, instruments, and services. Results are cross-checked using selective bottom-up approximations, such as sampled service provider revenue bands, lab capacity logic, and a simple ASP times volume check for commonly used kits and reagents.

Key inputs used in the model include the mix of sterile dosage forms and implantable devices, outsourcing penetration for batch release testing, the share of membrane filtration versus direct inoculation in routine workflows, adoption timing of rapid sterility tests in high value therapies, and inflation or price changes for consumables and instrument servicing. Where a bottom-up roll-up cannot be completed due to limited disclosure, gaps are handled through calibrated ratios from primary inputs, and those ratios are only applied after basic plausibility checks against sterile production scale.

For the forecast, scenario analysis is used so growth can be flexed based on regulatory inspection intensity, capacity additions in biologics manufacturing, and outsourcing lead times, which are then reviewed with experts for reasonableness. Shorter term momentum is also checked against recent investment cycles in sterile fill-finish and lab automation before the final numbers are locked.

Data Validation & Update Cycle

Validation is done by triangulating model outputs across multiple independent signals, and then running variance checks at region and application level to spot outliers early. When a number looks too high or low, assumptions are revisited, and follow-up calls are triggered to recheck items such as test mix, outsourcing share, and price progression.

Before sign-off, the full model goes through stepwise analyst reviews so inputs, calculations, and logic can be traced back to clear sources or interview notes. Reports are refreshed annually, and interim updates are made when material events occur that can shift sterile manufacturing activity or testing capacity. Right before delivery, a final review pass is completed so clients receive the most current view that matches the latest available information.

Mordor Intelligence's Sterility Testing Market Size Compared With Other Published Estimates

Published market sizes for sterility testing do not always match because the included revenue streams and the starting year can be different, even when the market name looks the same. Differences also show up when one estimate emphasizes outsourced services while another leans more toward instrument sales or only a narrower pharmaceutical definition.

The biggest gaps usually come from scope cutoffs and how the testing workflow is counted, especially around whether environmental monitoring consumables and upstream bioburden activities are included, and how rapid sterility tests are treated versus compendial methods. Currency conversion timing and refresh cadence matter as well, because pricing for kits and reagents and service rates can move within a year, which then shifts the current-year market value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.59 B (2025) | |

| Global Consultancy A | USD 1.28 B (2025) | This figure appears to use a narrower revenue frame that leans toward core sterility testing offerings and may undercount services intensity in high compliance manufacturing, which lowers the 2025 total. |

| Industry Publisher B | USD 1.74 B (2025) | This figure likely applies a broader definition that can blend adjacent quality control items into sterility testing, and may assume a faster near-term price lift for consumables, which pushes the 2025 value upward. |

The table shows that the spread is largely explained by what is counted as sterility testing spend and how current-year prices are carried into the model. When environmental monitoring consumables and upstream bioburden are kept out, and when rapid sterility tests are counted only when they are used for release decisions, the 2025 total lands differently, which is the approach used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the sterility testing market?

The sterility testing market is valued at USD 1.76 billion in 2026 and is projected to reach USD 2.96 billion by 2031.

Which segment is growing fastest within the sterility testing market?

Outsourced services show the strongest momentum, advancing at a 10.48% CAGR through 2031 as pharmaceutical sponsors pivot to CDMOs for specialized expertise.

Why are rapid sterility tests gaining traction?

Rapid tests can deliver results within hours or a few days, enabling faster product release for cell and gene therapies that possess limited shelf lives.

Which region leads sterility testing revenue, and which grows fastest?

North America holds the largest share at 41.86%, while Asia Pacific is the fastest-growing region with a 9.58% CAGR forecast to 2031.

How is EU GMP Annex 1 influencing market demand?

Annex 1’s zero-CFU mandate forces manufacturers to upgrade isolators, adopt PUPSIT, and install advanced environmental monitoring, fueling new equipment and service contracts.

What technologies are key to reducing false-positive sterility test results?

Modular isolator systems, AI-enabled colony counters, and solid-phase cytometry platforms reduce manual intervention and contamination risk, curbing false-positive rates and associated costs.

Page last updated on: