Vegan Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.45 Billion |

| Market Size (2031) | USD 24.56 Billion |

| Growth Rate (2026 - 2031) | 14.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Meat Market Analysis by Mordor Intelligence

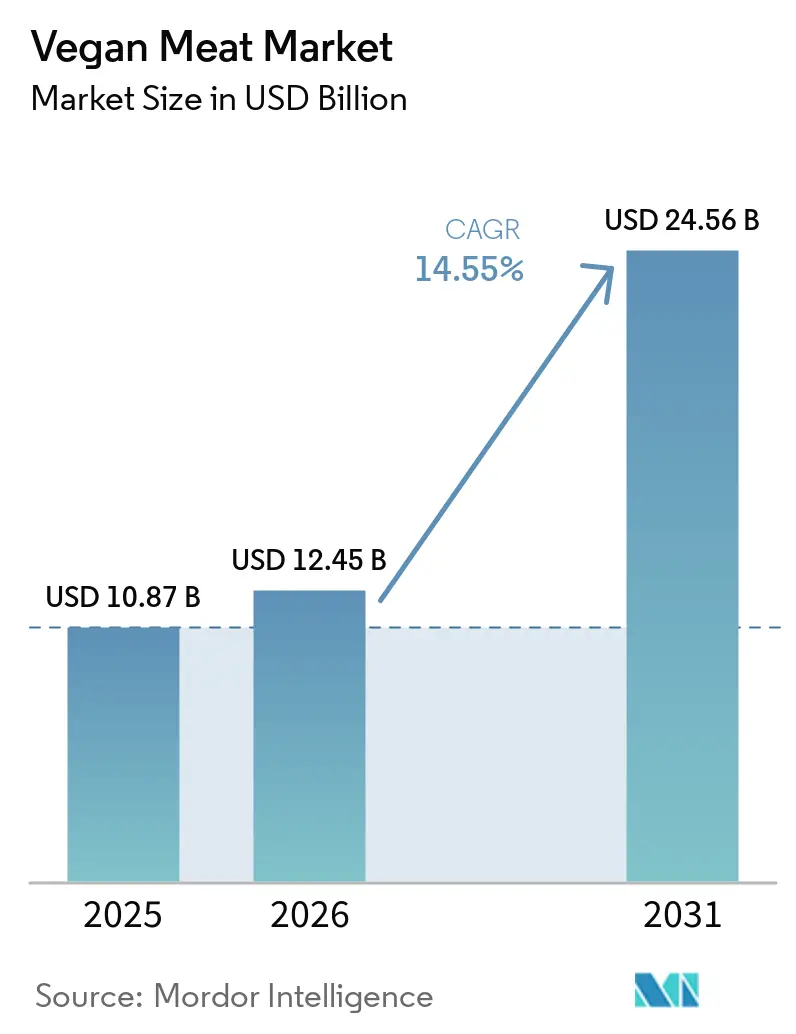

The global vegan meat market was valued at USD 10.87 billion in 2025, reached USD 12.45 billion in 2026, and is projected to grow to USD 24.56 billion by 2031, registering a CAGR of 14.55% during the forecast period of 2026–2031. This growth is primarily driven by the increasing adoption of plant-based diets, as consumers prioritize health, environmental sustainability, and ethical concerns associated with conventional meat consumption. Additionally, the growing demand for clean-label and natural ingredient-based products is prompting manufacturers to focus on minimally processed formulations with transparent labeling, enhancing consumer trust. Product innovation is also playing a significant role in market growth, with improvements in taste, texture, and nutritional profiles making vegan meat products more comparable to traditional meat, thereby attracting a wider consumer base, including flexitarians.

Key Report Takeaways

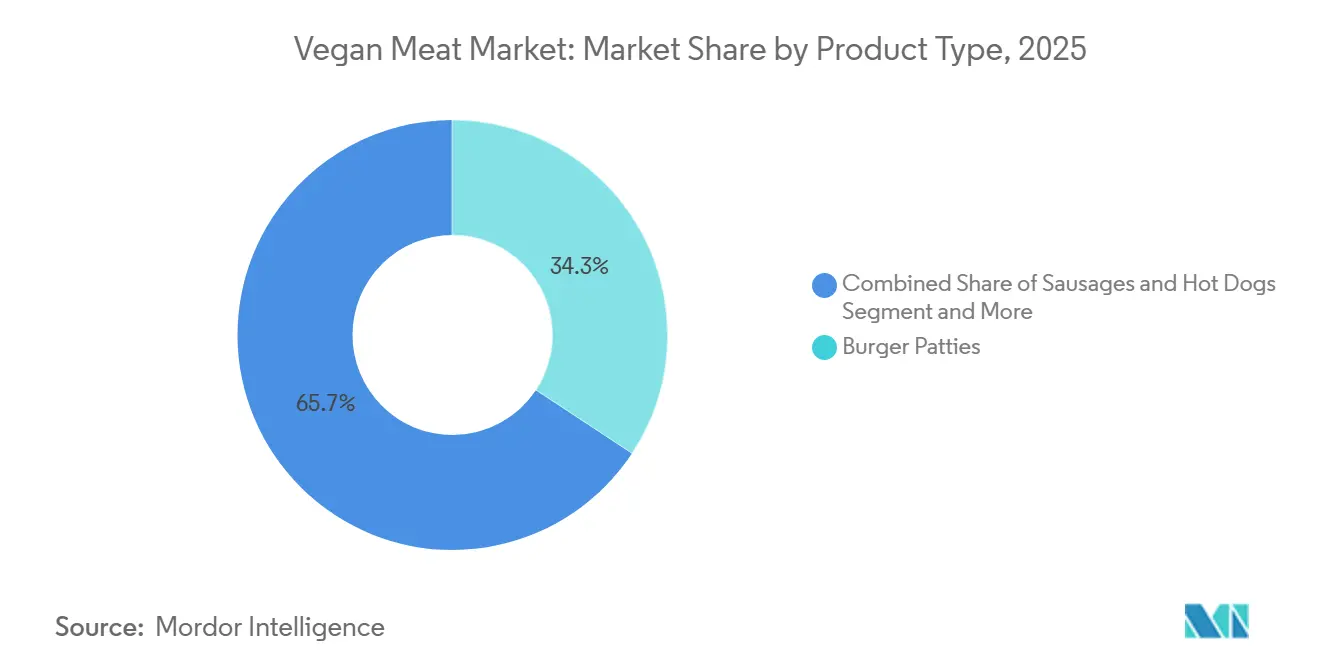

- By product type, burger patties led with 34.27% of vegan meat market share in 2025; meatballs are forecast to expand at a 15.69% CAGR through 2031.

- By source, soy accounted for 60.09% share of the vegan meat market size in 2025, while pea protein is advancing at a 15.43% CAGR through 2031.

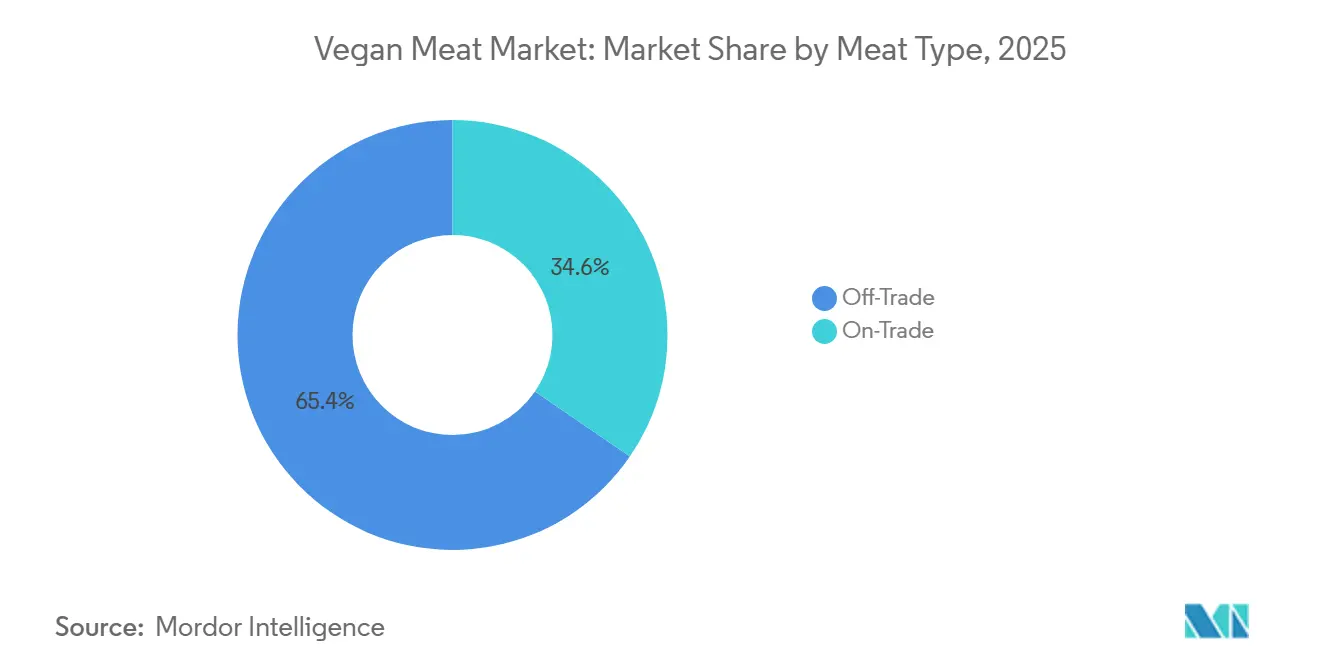

- By distribution channel, off-trade captured 65.44% revenue share in 2025, whereas on-trade is projected to grow at a 14.63% CAGR to 2031.

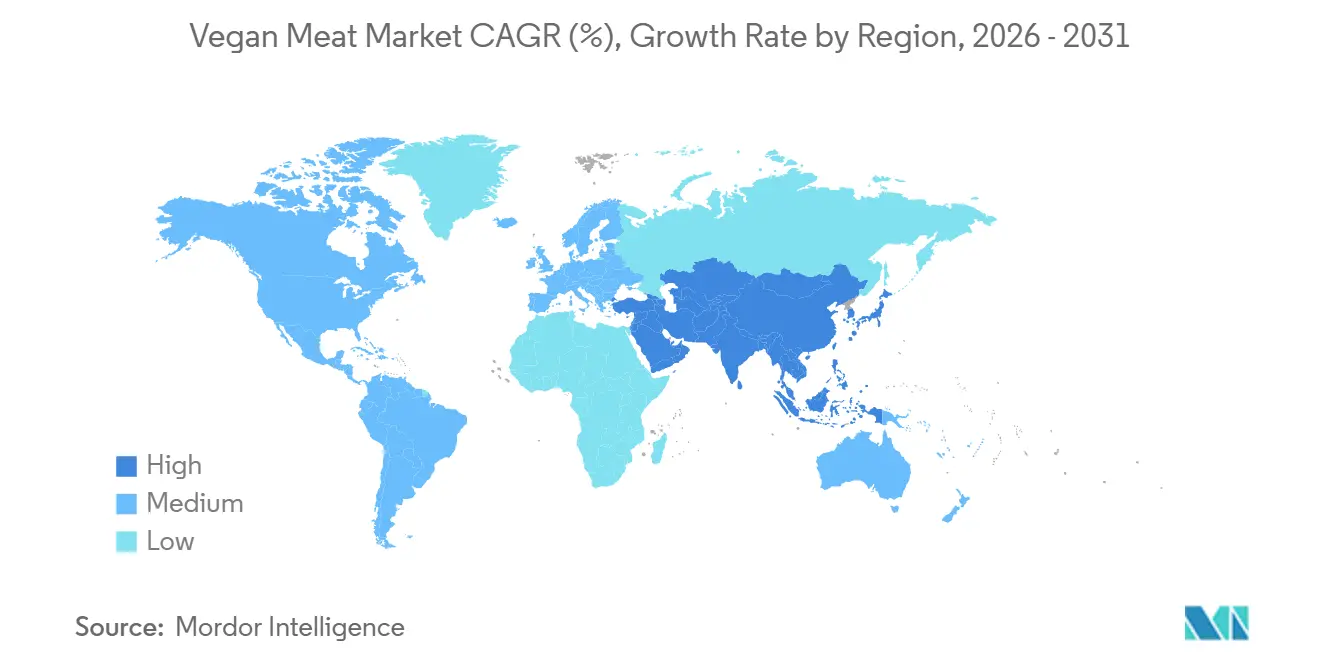

- By geography, North America generated 40.65% of 2025 revenue; Asia-Pacific is projected to register a 16.43% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vegan Meat Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of plant-based diets | +3.2% | Global, with strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Preference for clean-label products | +2.8% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Product innovation and improved taste/texture | +3.5% | Global | Short term (≤ 2 years) |

| Increasing allergen- and dietary-friendly options | +1.9% | North America, Europe, Middle East | Medium term (2-4 years) |

| Technological advancements in texture, flavor, and nutrition | +2.6% | Global, led by North America and Europe Research and Development hubs | Long term (≥ 4 years) |

| Government initiatives and policies promoting sustainable proteins | +1.5% | Europe, China, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of plant-based diets

The increasing adoption of plant-based diets is driving the growth of the global plant-based meat market, as consumers shift toward sustainable, ethical, and health-conscious eating habits. This shift is supported by rising awareness of the environmental impact of conventional meat production, concerns about animal welfare, and the perceived health benefits of plant-based alternatives, such as lower cholesterol levels and reduced saturated fat content. Furthermore, the growing availability of innovative plant-based products that replicate the taste, texture, and appearance of traditional meat is enabling consumers to integrate these alternatives into their diets without sacrificing sensory satisfaction. According to the Good Food Institute (GFI), in 2025, approximately 68% of consumers in the United States are aware of plant-based meat products, highlighting the strong penetration and visibility of these offerings in the mainstream market [1]Source: Good Food Institute (GFI), "Plant-based meat", gfi.org.

Preference for clean-label products

The increasing demand for clean-label products is a key factor driving the growth of the plant-based meat market, as consumers prioritize transparency, simplicity, and natural ingredients in their food choices. Modern consumers are paying closer attention to ingredient lists, preferring products that exclude artificial additives, preservatives, genetically modified organisms (GMOs), and synthetic chemicals. This trend is particularly prominent among health-conscious and younger demographics, who associate clean-label products with improved nutritional value, safety, and overall well-being. In response, plant-based meat manufacturers are actively reformulating their products to include recognizable, minimally processed ingredients such as pea protein, soy, wheat, and natural flavorings. Additionally, they are emphasizing these attributes on their packaging through clear labeling and marketing efforts to align with consumer expectations and build trust.

Product innovation and improved taste/texture

Product innovation and continuous improvements in taste and texture are supporting the market. Manufacturers are investing significantly in research and development to replicate traditional meat flavors using advanced technologies such as high-moisture extrusion, fermentation, and novel protein blends. These advancements are enabling plant-based products to closely resemble traditional meat, appealing not only to vegetarians and vegans but also to flexitarian consumers seeking occasional meat alternatives without compromising on taste. Additionally, companies are enhancing the nutritional profile of these products by incorporating higher protein content, added fiber, and essential nutrients, thereby strengthening their value proposition. For example, in December 2025, Richmond introduced a new meat-free sausage range that is high in protein and fiber, seasoned with a blend of herbs and spices, and designed to offer improved taste and texture while catering to health-conscious consumer preferences.

Increasing allergen- and dietary-friendly options

The increasing availability of allergen- and dietary-friendly options is a key factor driving the growth of the plant-based meat market. Manufacturers are addressing the diverse dietary needs and sensitivities of modern consumers by offering alternative formulations. A rising number of individuals are affected by common allergens such as gluten and dairy, creating demand for products that meet these restrictions without compromising taste or nutritional value. To meet this demand, companies are innovating with a variety of protein sources, including pea, rice, chickpea, and fava bean, to develop allergen-free products. Additionally, advancements in food technology and ingredient processing are enabling the creation of plant-based meat products with improved texture, flavor, and nutritional profiles. This diversification and innovation are enhancing the inclusivity and accessibility of plant-based meat products, appealing to a wider consumer base, including those with food intolerances, allergies, or specific dietary preferences such as vegan, vegetarian, or flexitarian lifestyles.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture issues | -2.1% | Global, particularly price-sensitive markets in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Short shelf life and storage challenges | -1.4% | Emerging markets with limited cold-chain infrastructure | Medium term (2-4 years) |

| Regulatory and labeling challenges | -0.9% | Europe, North America | Medium term (2-4 years) |

| Supply chain constraints for key ingredients | -1.2% | Global, with acute pressure in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Taste and texture issues

Taste and texture limitations remain a significant restraint on the growth of the plant-based meat market, as many consumers perceive these products as lacking in flavor authenticity and mouthfeel compared to conventional meat. Although advancements in food technology have been made, replicating the juiciness, fibrous structure, and savory taste of animal-based meat remains challenging, particularly for whole-cut formats like steaks or chicken fillets. Some plant-based products may have off-flavors, such as beany or earthy notes, and inconsistent textures, which can negatively impact consumer satisfaction. This issue is particularly important for flexitarian and first-time consumers, whose repeat purchase decisions heavily depend on their sensory experience. Addressing these sensory gaps through further innovation and ingredient optimization will be crucial for driving market growth and improving consumer acceptance.

Short Shelf Life and Storage Challenges

Short shelf life and storage challenges serve as significant restraints in the plant-based meat market. These products are highly perishable and require controlled storage conditions to preserve their quality, safety, and sensory attributes. The absence of traditional preservatives and the reliance on natural or clean-label ingredients make plant-based meat alternatives more prone to microbial spoilage, oxidation, and texture degradation over time. This necessitates consistent refrigeration or freezing throughout the supply chain, which increases logistical complexity and costs for manufacturers, retailers, and foodservice providers. Furthermore, maintaining cold chain infrastructure poses additional challenges in emerging markets or regions with limited storage facilities, thereby restricting product availability and distribution reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meatballs Surge as Hybrid Formats Gain Traction

The burger patties segment accounted for 34.27% of the global vegan meat market in 2025, driven by its widespread consumer familiarity, versatility, and seamless integration into existing food consumption habits. Burger patties are among the most recognizable and easily replaceable formats of conventional meat, enabling both vegan and flexitarian consumers to transition without significantly altering their meal preferences. Furthermore, this segment has become a focal point for product innovation, with manufacturers focusing on improving taste, texture, aroma, and appearance to closely replicate conventional meat, thereby increasing consumer acceptance and repeat purchases. The format also supports versatility in meal preparation, allowing consumers to customize flavors and ingredients based on regional and personal preferences, enhancing its universal appeal.

The meatballs segment, projected to grow at a CAGR of 15.69% through 2031, is emerging as one of the fastest-growing categories within the global vegan meat market. This growth is attributed to its strong alignment with evolving consumption patterns and culinary adaptability. Unlike more standardized formats, vegan meatballs offer significant flexibility for use across a wide range of global cuisines, including pasta dishes, rice-based meals, wraps, and fusion recipes, enhancing their appeal across diverse cultural preferences. This versatility enables consumers to incorporate plant-based options into everyday meals without requiring major dietary changes, thereby accelerating adoption. Additionally, meatballs provide a home-style and comfort-oriented eating experience, resonating with consumers seeking familiar, hearty meal options in plant-based formats.

By Source: Pea Protein Gains as Soy Faces Allergen Headwinds

The soy-based segment, which is expected to account for 60.09% of the global vegan meat market by source in 2025, continues to drive and dominate the market due to its established functionality, nutritional benefits, and extensive applicability in plant-based meat production. Soy has been a key ingredient in meat alternatives because of its high protein content and complete amino acid profile, making it an effective substitute for replicating the nutritional value of animal meat. Furthermore, its superior texturization capabilities allow manufacturers to closely replicate the fibrous structure and chewiness of conventional meat, a critical factor in improving consumer acceptance. The versatility of soy in various formulations and its ability to deliver consistent quality further solidify its position as a preferred choice in the vegan meat industry.

The pea-based segment, anticipated to grow at a CAGR of 15.43% through 2031, is emerging as one of the fastest-growing sources in the global vegan meat market. This growth is driven by its alignment with consumer preferences for clean-label, allergen-friendly, and sustainable protein alternatives. Pea protein is gaining popularity due to its non-allergenic properties compared to soy and gluten, making it suitable for a wider consumer base, including individuals with dietary restrictions. Additionally, its ability to blend seamlessly with other plant-based ingredients and deliver a neutral flavor profile enhances its appeal in product development. This characteristic is increasingly significant as consumers prioritize ingredient sensitivity and seek inclusive food options.

By Distribution Channel: On-Trade Rebounds as QSRs Expand Menus

The off-trade distribution channel, projected to account for 65.44% of the global vegan meat market in 2025, is a key driver of market growth. This channel aligns closely with evolving consumer behaviors focused on at-home meal preparation and convenience. Consumers increasingly prefer purchasing vegan meat products for home use, as it offers greater control over ingredients, portion sizes, and meal customization to suit personal tastes and dietary needs. This trend has led to higher purchase frequency, with vegan meat products becoming a staple in daily cooking routines rather than being limited to occasional use. The dominance of off-trade channels is further supported by the availability of a wide range of packaged products, allowing consumers to explore various types, flavors, and formats of vegan meat at their convenience.

The on-trade distribution channel, expected to grow at a CAGR of 14.63% through 2031, is gaining significance as a growth driver in the global vegan meat market. This expansion is supported by the robust growth of the foodservice industry. According to the United States Department of Agriculture (USDA), food sales at foodservice outlets reached USD 1.52 trillion in 2024, underscoring the vast consumption base and opportunities for integrating plant-based meat into dining establishments [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov. The growth of this channel is primarily fueled by the increasing inclusion of vegan meat options in mainstream menus, exposing consumers to plant-based alternatives in familiar and experiential dining environments. On-trade channels play a pivotal role in shaping consumer perceptions by offering first-time trials of professionally prepared vegan meat dishes that closely replicate traditional meat in taste, texture, and presentation.

Geography Analysis

North America is projected to dominate the global vegan meat market, accounting for 40.65% of total revenue in 2025. This leadership is driven by strong consumer acceptance of plant-based diets, high levels of product innovation, and widespread familiarity with meat alternatives. The region benefits from a well-established ecosystem where consumers prioritize sustainable and health-oriented food choices, facilitating the rapid adoption of vegan meat products in daily consumption. Additionally, the presence of established plant-based brands and ongoing advancements in taste, texture, and product variety contribute to market growth. North America's ability to integrate vegan meat into conventional dietary habits without requiring significant behavioral changes further solidifies its position as a key revenue generator in the global market.

Asia-Pacific is emerging as the fastest-growing region in the vegan meat market, with a projected CAGR of 16.43% through 2031. This growth is supported by shifting dietary patterns, increasing acceptance of plant-based proteins, and the region's strong culinary adaptability. Traditional diets in many Asian countries already include plant-based ingredients such as soy, tofu, and legumes, providing a favorable foundation for vegan meat adoption. This cultural compatibility minimizes resistance to plant-based alternatives and allows manufacturers to develop products tailored to local cuisines. Factors such as rapid urbanization, evolving food preferences, and heightened awareness of sustainability and health further drive demand, positioning Asia-Pacific as a significant growth driver in the global vegan meat market.

Europe and South America exhibit contrasting dynamics within the vegan meat market. In Europe, regulatory fragmentation across countries poses challenges for manufacturers, particularly regarding labeling standards, ingredient approvals, and product definitions. These complexities can hinder uniform market expansion, despite strong consumer interest in plant-based foods. Conversely, South America remains a relatively nascent market but holds substantial long-term potential due to its robust agricultural base. For example, according to the Soybean Processors Association of India (SOPA), Brazil produced 169 million metric tons of soybeans in 2024-2025, underscoring the availability of raw materials that could support future growth in plant-based protein production [3]Source: Soybean Processors Association of India (SOPA), "World Soybean Production", sopa.org.

Competitive Landscape

The global vegan meat market is moderately fragmented, featuring a mix of established food corporations and specialized plant-based innovators vying for market share. Key players, including Beyond Meat Inc., Impossible Foods Inc., Maple Leaf Foods Inc., Conagra Brands Inc., and Tyson Foods Inc., are actively shaping the competitive landscape through ongoing product innovation and portfolio diversification. While specialized brands emphasize premium, next-generation plant-based products, large multinational food companies leverage their scale, distribution networks, and Research and Development (R&D) resources to strengthen their market presence. This dynamic fosters a competitive environment where niche innovators and diversified food giants coexist, intensifying market competition.

Technology has become a critical factor in the vegan meat market, with companies investing significantly in advanced processing techniques to enhance product quality and differentiation. Innovations such as high-moisture extrusion are enabling the creation of more realistic meat-like textures, while precision fermentation is being utilized to improve flavor profiles and functional properties. Additionally, advancements in shelf-life extension technologies are enhancing product stability and reducing food waste, which is essential for scaling plant-based meat production globally. These technological advancements are increasingly shaping competitive advantages, as brands capable of closely replicating the sensory experience of conventional meat are better positioned to attract and retain consumers.

Companies are placing greater emphasis on allergen-free formulations to appeal to a wider consumer base, particularly those avoiding soy or gluten. There is also a growing focus on halal-certified vegan products, allowing brands to cater to specific dietary preferences and expand into new geographic markets. Furthermore, the development of hybrid formats, which combine plant proteins with cultivated fat or mycoprotein, is gaining momentum as a means to improve taste, texture, and nutritional value. These innovations are expected to reshape product development strategies and create new opportunities for differentiation, further intensifying competition in the evolving vegan meat market.

Vegan Meat Industry Leaders

-

Beyond Meat Inc.

-

Impossible Foods Inc.

-

Maple Leaf Foods Inc.

-

Conagra Brands Inc.

-

Tyson Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Meatless Farm launched Crispy Nuggets, featuring a chicken-style center coated in golden tempura batter. The product contains a chicken-style soy protein designed to replicate the taste and texture of meat.

- December 2025: Richmond expanded its meat-free portfolio with the introduction of Veggie Tasty, a new sub-range of vegetable-based sausages. These sausages are made with 42% vegetables, including broccoli, carrot, sweetcorn, and peas.

- June 2025: Prime Roots unveiled the refreshed version of its first fresh-sliced plant-based deli meats at the Summer Fancy Food Show in New York City. These products are gluten-free, soy-free, GMO-free, nitrate-free, and free from artificial ingredients.

Global Vegan Meat Market Report Scope

Vegan meat, or plant-based meat, is a, meat analogue designed to mimic the taste, texture, and appearance of animal-based meat using plant ingredients. The vegan meat market is segmented by product type, source, distribution channel, and geography. Based on product type, the market is segmented into burger patties, sausages and hot dogs, nuggets and tenders, grounds and mince, meatballs, deli slices, and others. Based on source, the market is segmented intosoy, wheat, pea, and others. Based on distribution channel, the market is segmented into on-trade and off-trade. Off-trade segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Burger Patties |

| Sausages and Hot Dogs |

| Nuggets and Tenders |

| Grounds and Mince |

| Meatballs |

| Deli Slices |

| Others |

| Soy |

| Wheat |

| Pea |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Burger Patties | |

| Sausages and Hot Dogs | ||

| Nuggets and Tenders | ||

| Grounds and Mince | ||

| Meatballs | ||

| Deli Slices | ||

| Others | ||

| By Source | Soy | |

| Wheat | ||

| Pea | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the vegan meat market expected to grow between 2026 and 2031?

It is forecast to expand at a 14.55% CAGR, rising from USD 12.45 billion in 2026 to USD 24.56 billion by 2031.

Which product type will add the most absolute dollars to sales through 2031?

Meatballs are projected to be the fastest-growing item at a 15.69% CAGR, adding the largest incremental revenue due to hybrid formulations that improve juiciness.

Why is pea protein gaining share over soy?

Pea's are allergen-friendly, highly digestible, and now priced within reach due to capacity additions from suppliers such as Roquette, driving a 15.43% CAGR in their adoption.

Which regions show the strongest future growth potential?

Asia-Pacific leads with a projected 16.43% CAGR to 2031, supported by governmental R&D funding in China and rapid menu localization across Japan and Southeast Asia.

Page last updated on: