Date Sugar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

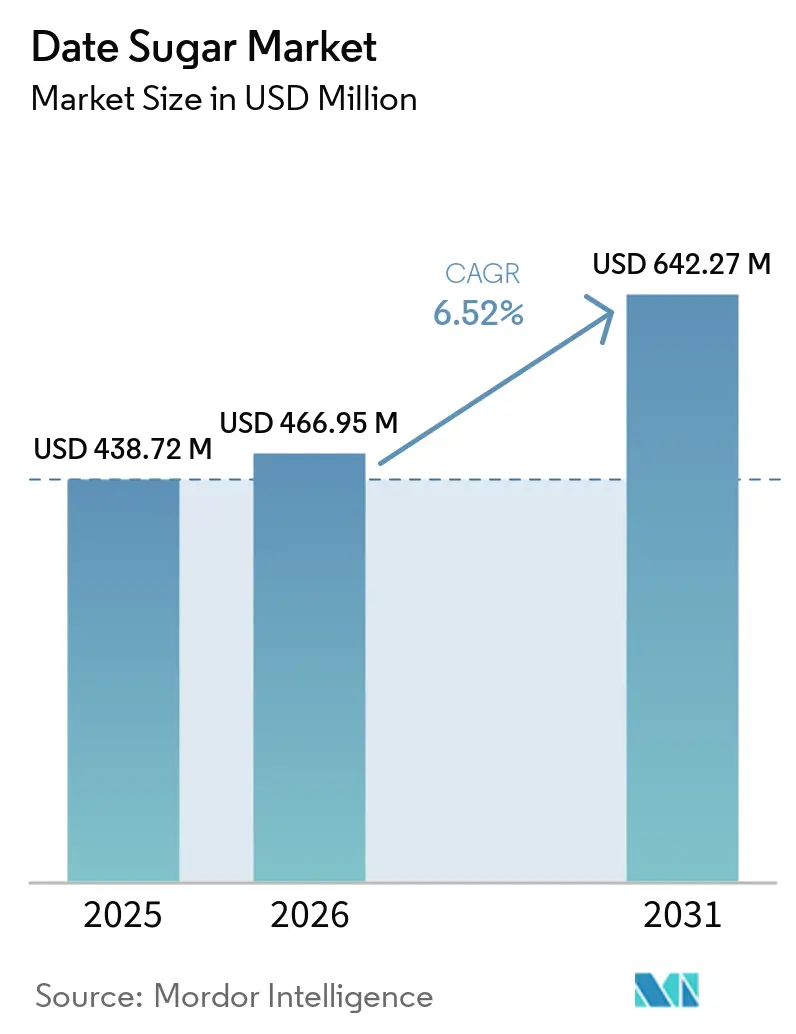

| Market Size (2026) | USD 466.95 Million |

| Market Size (2031) | USD 642.27 Million |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

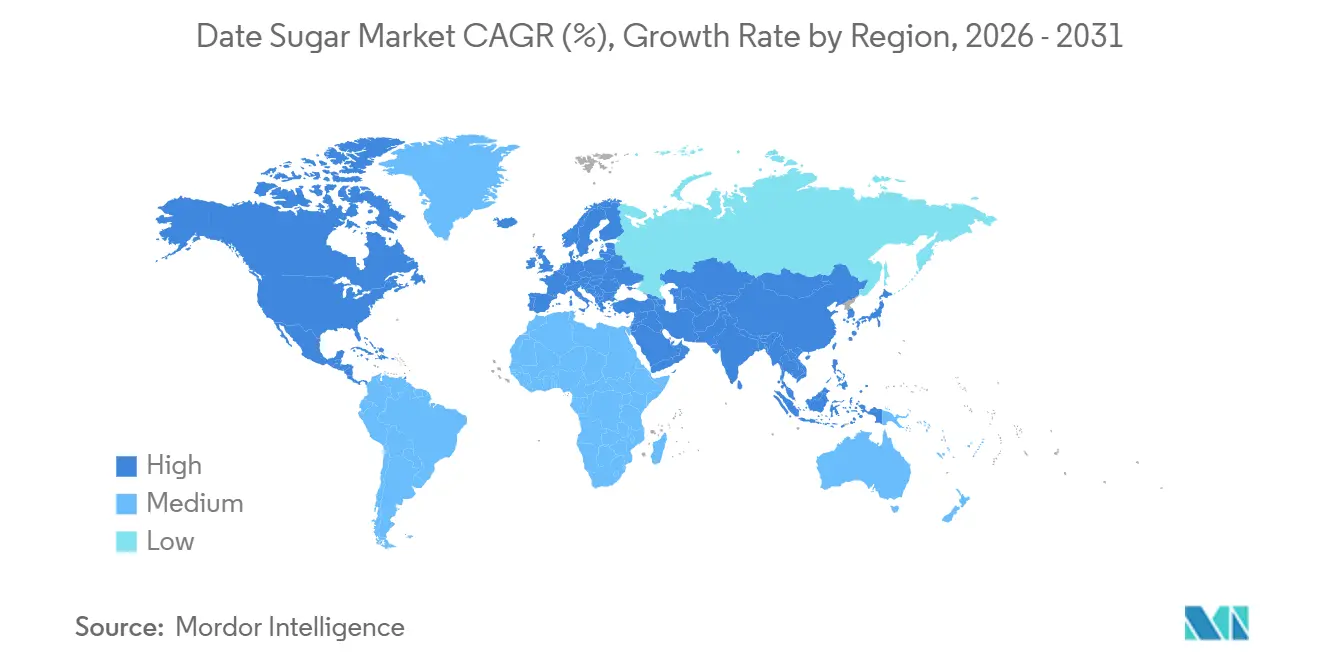

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Date Sugar Market Analysis by Mordor Intelligence

The global date sugar market was valued at USD 438.72 million in 2025 and is anticipated to reach USD 642.27 million by 2031, registering a CAGR of 6.52% during the forecast period of 2026–2031. The date sugar market is still showing clear momentum because buyers are shifting away from high-fructose corn syrup and synthetic sweeteners toward fruit-derived options with fiber, protein, and antioxidant value, which improves the case for premium pricing in packaged food and institutional procurement. Clinical and nutritional evidence is supporting the date sugar market as lower-glycaemic positioning becomes more important in mainstream food, dairy, and functional snack development, not only in specialty health channels.

Key Report Takeaways

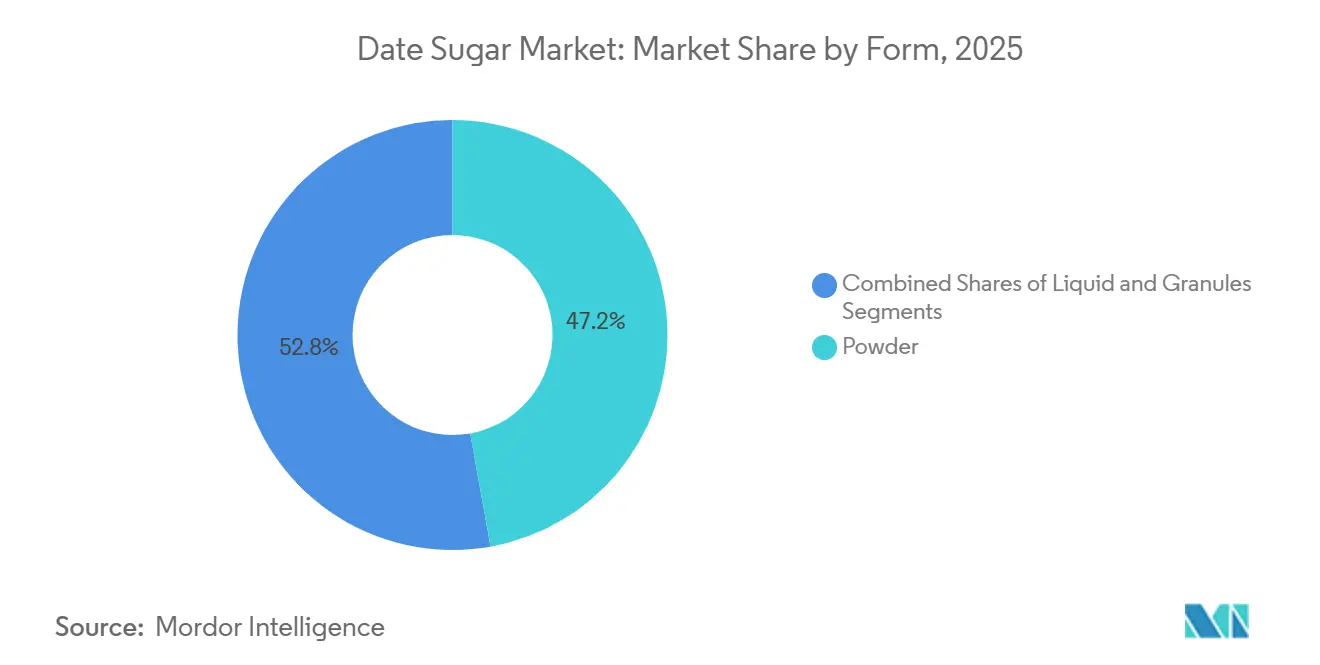

- By form, powder captured 47.18% of the date sugar market share in 2025 and is projected to expand at a 6.38% CAGR from 2026 to 2031, while liquid is set to record the fastest 7.72% CAGR through 2031.

- By Category, conventional variants accounted for 73.86% of 2025 revenue; organic is on track for the highest 7.58% CAGR to 2031.

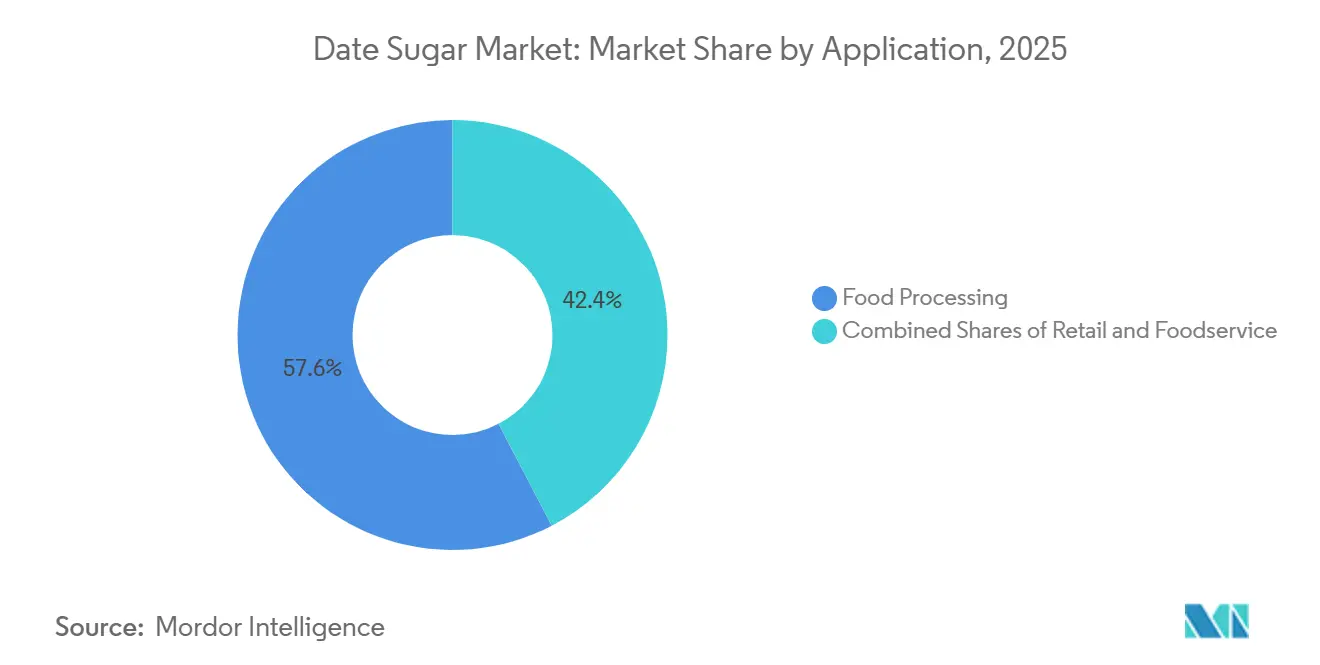

- By end-use, food processing led with 57.94% of revenue in 2025; retail is forecast to post a 7.26% CAGR through 2031.

- By geography, North America held the dominant market position with 34.97% of global sales in 2025, while Asia-Pacific is projected to record the strongest CAGR of 7.21% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Date Sugar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Growth in Consumer Demand for Natural and Organic Sweetening Solutions | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Expanding Adoption of Vegan and Gluten-Free Lifestyle Trends | +0.8% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing Market Preference for Clean-Label Food and Beverage Products | +1.1% | Global, led by developed markets | Short term (≤ 2 years) |

| Rising Consumer Inclination Toward Low-Glycaemic Sweetener Alternatives | +0.9% | Global, with emphasis on diabetic-prevalent regions | Medium term (2-4 years) |

| Ongoing Technological Innovations in Extraction and Processing Techniques | +1.3% | Middle East & North Africa production hubs, global processing | Long term (≥ 4 years) |

| Growing Integration in Sports Nutrition and Functional Snacking Applications | +0.7% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Consumer Demand for Natural and Organic Sweetening Solutions

Date sugar is emerging as a strategically important segment within the alternative sweetener industry, driving reformulation initiatives across multiple food and beverage categories. Regulatory developments are further accelerating adoption. For instance, the USDA’s added-sugar standards for school meal programs, scheduled for implementation in July 2025 across categories including breakfast cereals and yogurt, are encouraging manufacturers to transition toward whole-food-derived sweetening solutions[1]U.S. Department of Agriculture Food and Nutrition Service, “Added Sugars,” U.S. Department of Agriculture, fns.usda.gov. Supply-side conditions are also improving, with Morocco expecting a 55% increase in production to 160,000 tons during the 2025–2026 season as part of its broader date palm development program [2]Source: Food and Agriculture Organization of the United Nations, “The Date Palm in Morocco, Economic Pillar of Oases and Lever for Sustainable Development,” FAO, fao.org. Together, stronger demand indicators and improving raw material availability are providing the date sugar market with a more stable foundation across both consumer and institutional channels.

Increasing Market Preference for Clean-Label Food and Beverage Products

The date sugar market is also gaining momentum from the growing clean-label trend, as date sugar is produced by dehydrating and grinding whole fruit, allowing the ingredient to remain familiar and easily recognizable to both consumers and product developers. In addition, the FDA Human Foods Program’s planned 2026 draft guidance on fruit- and vegetable-derived juices as color additives is supporting broader interest in ingredients that can deliver both sweetness and natural coloring functions. This dual-purpose capability is particularly valuable for the date sugar market because formulators can streamline ingredient labels when a single fruit-based ingredient performs multiple roles within a formulation. The clean-label advantage is especially significant in premium bakery, dairy, and snack categories, where consumers closely evaluate ingredient lists and where synthetic-sounding alternatives can negatively affect brand perception [3]Federal Register, “Food Labeling, Nutrient Content Claims, Definition of Term ‘Healthy,’ Final Rule,” Federal Register, regulations.gov. As reformulation activity expands beyond niche health-focused brands to larger mainstream manufacturers, the date sugar market is positioned to benefit from wider adoption across everyday packaged food products rather than remaining limited to specialty natural offerings.

Rising Consumer Inclination Toward Low-Glycaemic Sweetener Alternatives

The date sugar market is benefiting from increasing consumer and industry interest in lower-glycaemic sweetening alternatives across food categories that extend beyond traditional health-focused products. Research published in 2025 indicated that freeze-dried Barhi dates maintained a glycaemic index range of 39.72 to 39.80 while preserving beneficial phenolic compounds and flavonoids, strengthening their suitability for better-for-you product development. As a result, the date sugar market is benefiting from a broader long-term shift in packaged food formulation toward sweetening systems perceived as more compatible with blood sugar management and wellness-oriented claims. This trend is particularly important in developing food markets, where reformulation activity began later and where future growth potential remains significant due to the relatively lower adoption of natural sweeteners.

Growing Integration in Sports Nutrition and Functional Snacking Applications

The date sugar market is expanding its presence in sports nutrition and functional snacking as manufacturers increasingly develop products around food-based energy solutions rather than synthetic ingredient systems. Date-based sports formulations are attracting interest because date paste naturally provides a 2:1 glucose-to-fructose ratio, a composition that is widely recognized as beneficial in endurance nutrition applications. The functional value proposition is also evolving beyond carbohydrate delivery, with preclinical research published in 2025 showing that date-derived polysaccharides from Deglet Noor helped reduce blood glucose levels, lower pro-inflammatory cytokines, and restore gut microbial diversity[3]Federal Register, “Food Labeling, Nutrient Content Claims, Definition of Term ‘Healthy,’ Final Rule,” Federal Register, regulations.gov. These findings increase the relevance of the date sugar market for products positioned around recovery support, digestive health, and sustained energy delivery rather than solely as sugar substitutes. This transition is commercially significant because consumers in the sports nutrition segment are generally more willing to pay premium prices for ingredients that combine performance-oriented positioning with clean-label appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Shelf Stability of Date-Based Sweetening Products | -0.6% | Global, particularly affecting long-distance trade | Short term (≤ 2 years) |

| Volatility in Seasonal Raw Material Availability and Supply Chain Stability | -0.4% | Middle East & North Africa production regions | Medium term (2-4 years) |

| Potential Risks Associated with Allergen Sensitivities | -0.3% | Global, with stricter regulations in developed markets | Long term (≥ 4 years) |

| Difficulties in Achieving Consistent Texture, Flavor, and Quality Across Batches | -0.5% | Global processing and manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Seasonal Raw Material Availability and Supply Chain Stability

The date sugar market continues to face exposure to agricultural supply volatility, as date palm cultivation is highly sensitive to factors such as salinity, water stress, and broader regional climate pressures. Supply-side expansion also remains constrained because date palms require several years to reach full productive maturity, limiting the industry’s ability to respond quickly to rising demand. As a result, supply risks within the date sugar market are not only seasonal in nature but also structural, particularly when new plantation development, irrigation infrastructure, and orchard management investments fail to keep pace with market growth. However, until such operational improvements become more widely adopted, the date sugar market is likely to remain vulnerable to fluctuations in raw material costs, procurement uncertainty, and inconsistent supply reliability.

Limited Shelf Stability of Date-Based Sweetening Products

The date sugar market also faces operational challenges related to storage and handling, as date sugar powder is highly hygroscopic and readily absorbs moisture from the environment. This moisture absorption contributes to caking, stickiness, and increased microbial risk, ultimately reducing shelf stability compared with conventional crystalline sucrose and creating additional warehouse management challenges, particularly in humid climates. Certain date varieties may offer relatively better resistance to stickiness, but product performance still remains highly dependent on packaging quality and moisture-control systems. These limitations are commercially significant across the date sugar market because retail, foodservice, and industrial distribution channels all require consistent flowability and reliable storage performance. The issue is generally less pronounced among processors with advanced packaging systems and stronger moisture-control capabilities, providing larger certified suppliers with a competitive operational advantage over smaller market participants. Until shelf-life stability and handling performance improve more consistently at commercial scale, date sugar is likely to remain less suitable for certain ambient applications compared with traditional refined sweeteners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Format's Beverage Momentum Challenges Powder's Industrial Dominance

Powder accounted for 47.18% of demand in 2025 and remained the dominant product form in the date sugar market due to its strong compatibility with dry-blend bakery, snack bar, and seasoning applications, where flow characteristics and clean-label positioning are prioritized over complete solubility. The format also supports formulations requiring sweetening, mild binding functionality, and partial nutrient retention from the original fruit source, reinforcing its relevance in large-scale food manufacturing.

Liquid date sugar is projected to expand at a CAGR of 7.72% through 2031, supported by increasing demand from beverage, dairy, and functional food manufacturers that require easier ingredient incorporation and processing efficiency compared with powder-based formats. This transition is strategically important for the date sugar market because liquid processing generally favors suppliers with stronger food-safety systems, advanced logistics capabilities, and established relationships with industrial-scale buyers. Crystalline date sugar continues to represent a smaller but more specialized segment within the date sugar market, primarily serving premium confectionery, nutraceutical, and frozen dessert applications.

By Category: Organic Segment's Premium Positioning Reshaping Industrial Procurement

Conventional date sugar accounted for 73.86% of the market in 2025, while organic date sugar represented 26.1%, highlighting the continued importance of cost efficiency, supply reliability, and scalable procurement in industrial purchasing decisions. Conventional variants remain the preferred option for large food manufacturers that prioritize dependable supply volumes and lower exposure to certification-related complexity. This dynamic keeps the date sugar market closely aligned with mainstream procurement practices, even as premium and health-focused segments continue to expand.

Organic date sugar is projected to grow at a CAGR of 7.58% through 2031, driven by rising demand from premium bakery, infant nutrition, and sports nutrition applications where certification standards carry greater commercial importance. Companies such as KoRo Handels GmbH have already introduced certified organic date sugar sourced from Tunisia and the UAE under the EU Bio certification framework, demonstrating that certified MENA-origin supply chains are becoming increasingly established within European distribution channels. As a result, the date sugar market offers certified suppliers a stronger competitive advantage when buyers seek both natural sourcing credentials and regulatory assurance.

By End-Use: Food Processing Dominance While Retail Demand Accelerates

Food processing accounted for 57.94% of end-user demand in 2025 and remained the dominant channel in the date sugar market, as manufacturers benefit from the ingredient’s ability to deliver browning, humectancy, flavor enhancement, and clean-label sweetening within a single formulation system. This strong position reflects the suitability of whole-fruit sweeteners in applications such as cookies, snack bars, fillings, spreads, bakery products, and functional foods, where texture and flavor variability can be managed more effectively than in highly standardized beverage systems.

Retail is projected to grow at a CAGR of 7.26% through 2031, making it the fastest-growing end-user segment in the date sugar market. Growth is being supported by rising consumer demand for natural sweeteners in home baking, wellness products, and premium packaged foods purchased through supermarkets, specialty health stores, and e-commerce channels. The expansion also reflects stronger adoption of date sugar in products such as flavored yogurt, prebiotic dairy beverages, and premium health-oriented foods that require sweetness, natural color contribution, and a cleaner ingredient narrative within a single formulation approach. Foodservice continues to represent a smaller but gradually expanding segment of the date sugar market, supported by growing interest in natural and minimally processed ingredients across cafés, restaurants, institutional catering, and specialty beverage outlets.

Geography Analysis

North America accounted for 34.97% of global demand in 2025 and remained the largest regional segment within the date sugar market, supported by the strong development of natural product retail, e-commerce distribution, and private-label health-focused product positioning. The region also benefits from a mature consumer base with high awareness of clean-label sweetening solutions and a greater willingness to pay premium prices for recognizable, food-based ingredients. Europe continues to represent another key regional market for date sugar, although demand dynamics there are influenced more heavily by certification standards, organic product positioning, and stricter label transparency requirements across the packaged food industry.

Asia-Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of 7.21% through 2031, making it the most significant long-term growth opportunity for the date sugar market. Regional expansion is being driven by increasing consumer awareness of lower-glycaemic sweetening alternatives, broader product accessibility through digital retail channels, and substantial reformulation potential compared with more mature Western markets. This creates opportunities for the date sugar market to expand across both premium health-oriented products and mainstream packaged food categories over the long term. South America remains a comparatively smaller market, although the growth of premium health food retail channels is creating visible entry opportunities in countries such as Brazil and Argentina.

The Middle East and Africa play a distinct role in the date sugar market, serving both as a key raw material source and an increasingly important processing and value-addition hub. However, supply-side challenges related to salinity, irrigation constraints, and post-harvest losses continue to influence the extent to which regional processors can expand into higher-value sweetener production. As manufacturers across the region increase investments in certifications, export infrastructure, and more controlled processing capabilities, the date sugar market is expected to achieve stronger regional value capture within MENA economies rather than remaining primarily dependent on raw date exports.

Competitive Landscape

The date sugar market remains highly fragmented, with no single supplier exercising dominant control over pricing, distribution channels, or raw material supply across major global regions. Competitive dynamics are shaped by multiple participant groups operating with distinct capabilities and business models. Large MENA-based processors primarily compete through raw material access, production scale, and export capacity, while specialized ingredient manufacturers differentiate themselves through processing expertise, formulation technology, and certification strength. Western health-focused brands generally compete through retail positioning, organic labeling, and direct-to-consumer market visibility, whereas smaller regional players focus on advantages such as local distribution access, flexible packaging formats, and niche health-oriented positioning.

In February 2026, Al Barakah Dates Factory entered into a commercial supply agreement with PT Savani Indo Makmur, supported by the Dubai Chamber of Commerce, strengthening its presence within Southeast Asian beverage supply chains. In parallel, Naturalia Ingredients SRL updated the technical specifications for its crystalDATESUGAR and crystalFRUCTODATE product lines in February 2025, reinforcing its positioning within premium food and nutraceutical ingredient segments. Companies with certifications such as IFS Food, ISO 9001, ISO 22005, USDA Organic, Halal, and Kosher are expected to gain a stronger competitive advantage in B2B procurement channels, where documentation quality, traceability, and regulatory compliance increasingly carry equal importance to ingredient pricing.

Date Sugar Industry Leaders

Ariafoods

Date Lady

NOW Health Group, Inc.

Let’s Date LLC

Panos Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: VIVANI, a German organic chocolate manufacturer, launched a "Dark Date Sugar" bar using finely ground dried organic dates as the sole sweetener in a 60% cocoa formulation, targeting health-conscious retail consumers across the EU.

- August 2023: Just Date expanded the retail availability of its Organic Date Sugar nationwide through Sprouts stores, highlighting strong consumer demand for healthier, minimally processed sugar alternatives that retain fiber and nutrients.

- March 2023: The Groovy Food Company launched its Organic Date Syrup in the UK market, available at Tesco and Ocado, positioning it as a versatile, low-GI, all-natural alternative to refined sugar. Made from 100% UAE-sourced dates, this vegan and additive-free syrup supports the rising demand for clean-label sweeteners in the date sugar market.

Global Date Sugar Market Report Scope

Date sugar is a natural sweetening ingredient produced from dehydrated and finely ground dates.

The global date sugar market is analyzed across multiple segments, including form, category, end-use, and geography. Based on form, the market is segmented into powder, liquid, and crystalline variants. By nature, the market is classified into conventional and organic products. Based on end-use, the market is categorized into retail, foodservice, and food processing. Geographically, the study covers key regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

For each segment, market sizing and forecasts have been estimated in terms of value (USD million) and volume (tons).

| Powder |

| Liquid |

| Crystalline |

| Organic |

| Conventional |

| Retail | |

| Foodservice | |

| Food Processing | Bakery |

| Confectionery | |

| Dairy Products | |

| Sauces and Spreads | |

| Beverages | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| Crystalline | ||

| By Category | Organic | |

| Conventional | ||

| By End-Use | Retail | |

| Foodservice | ||

| Food Processing | Bakery | |

| Confectionery | ||

| Dairy Products | ||

| Sauces and Spreads | ||

| Beverages | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the date sugar market?

The date sugar market size reached USD 438.72 million in 2026 and is projected to hit USD 642.27 million by 2031.

Which form of date sugar holds the largest share?

Powder form leads with 47.18% of 2025 revenue because it integrates easily into dry-blend bakery and snack formulations.

Which end-use segment is growing the fastest?

Retail sector is forecast to post a 7.11% CAGR, driven by consumer demand for clean-label products.

Why is organic date sugar gaining popularity?

Certification assures consumers of pesticide-free farming and traceability; as a result, the organic segment is expanding at a 7.43% CAGR.

Which region is expected to grow the most rapidly?

Asia-Pacific is set to register the fastest regional CAGR at 7.21% from 2026 to 2031, propelled by rising incomes and health awareness.

Page last updated on: