DataOps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

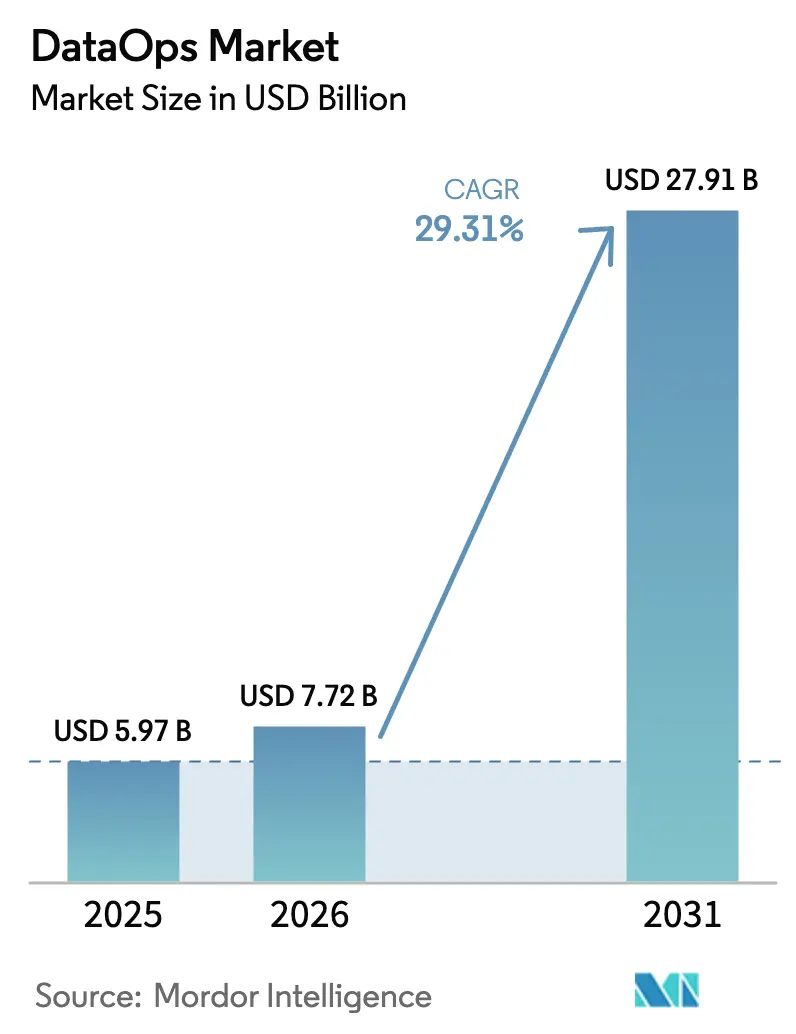

| Market Size (2026) | USD 7.72 Billion |

| Market Size (2031) | USD 27.91 Billion |

| Growth Rate (2026 - 2031) | 29.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DataOps Market Analysis by Mordor Intelligence

DataOps market size in 2026 is estimated at USD 7.72 billion, growing from 2025 value of USD 5.97 billion with 2031 projections showing USD 27.91 billion, growing at 29.31% CAGR over 2026-2031. Cloud-native data platforms, real-time analytics requirements and artificial intelligence initiatives are converging to push DataOps from a niche engineering practice into a core enterprise capability. Automated pipeline orchestration, data observability and lineage tracking have become mandatory features as sovereign data regulations tighten and as event-stream volumes accelerate across industries. Vendor competition is shifting toward unified lakehouse, mesh-ready architectures that promise lower latency, lower cost of ownership and faster deployment cycles. At the same time, managed service models and low-code tooling are opening adoption paths for organizations that lack deep engineering resources, especially in the mid-market and regulated verticals.

Key Report Takeaways

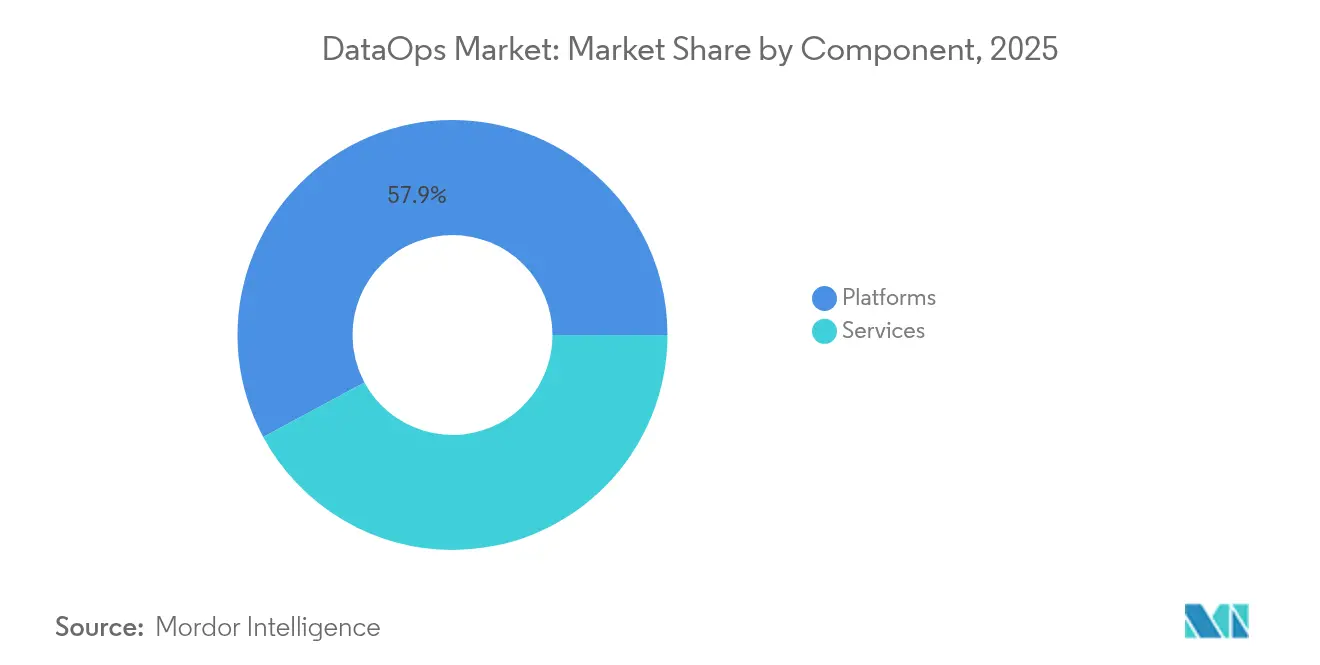

- By component, platforms led with 57.86% revenue share in 2025, while services are projected to expand at a 30.05% CAGR to 2031.

- By deployment, cloud captured 62.50% of the DataOps market share in 2025 and is advancing at a 31.25% CAGR through 2031.

- By enterprise size, large companies held 59.85% of revenue in 2025, whereas small and medium enterprises are forecast to grow at 32.45% CAGR during the period.

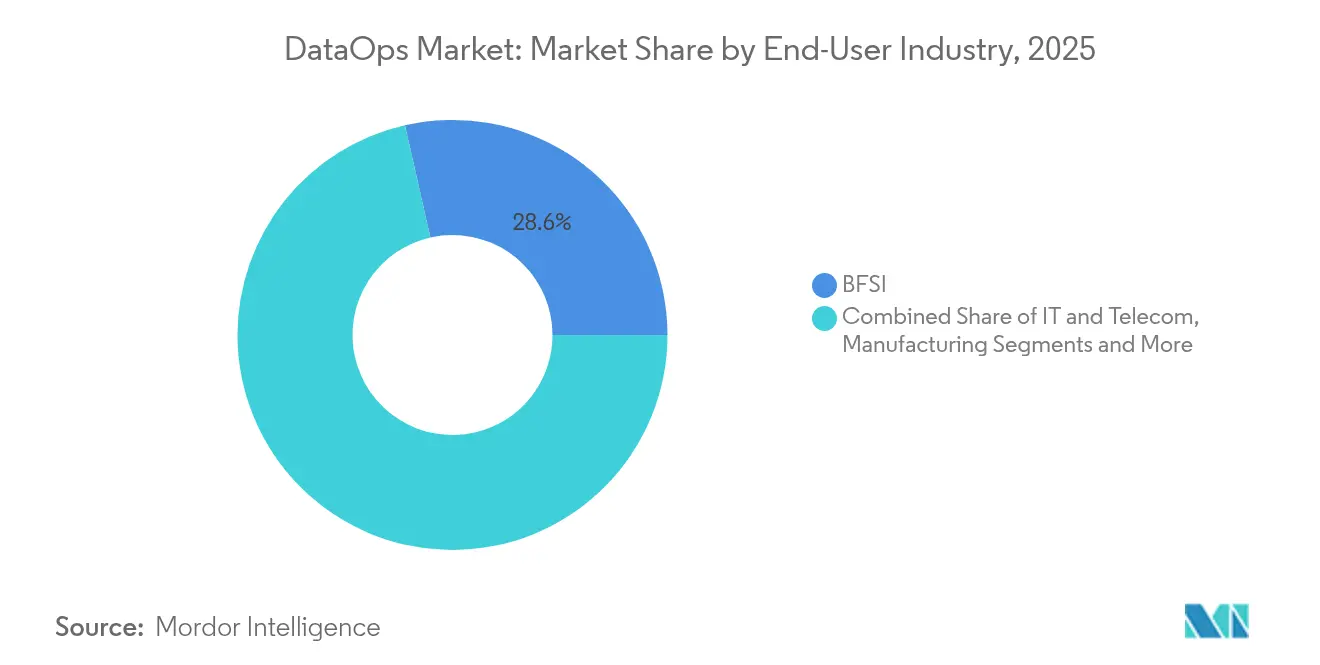

- By end-user industry, BFSI commanded 28.55% of the DataOps market size in 2025; healthcare is projected to register the fastest 34.70% CAGR to 2031.

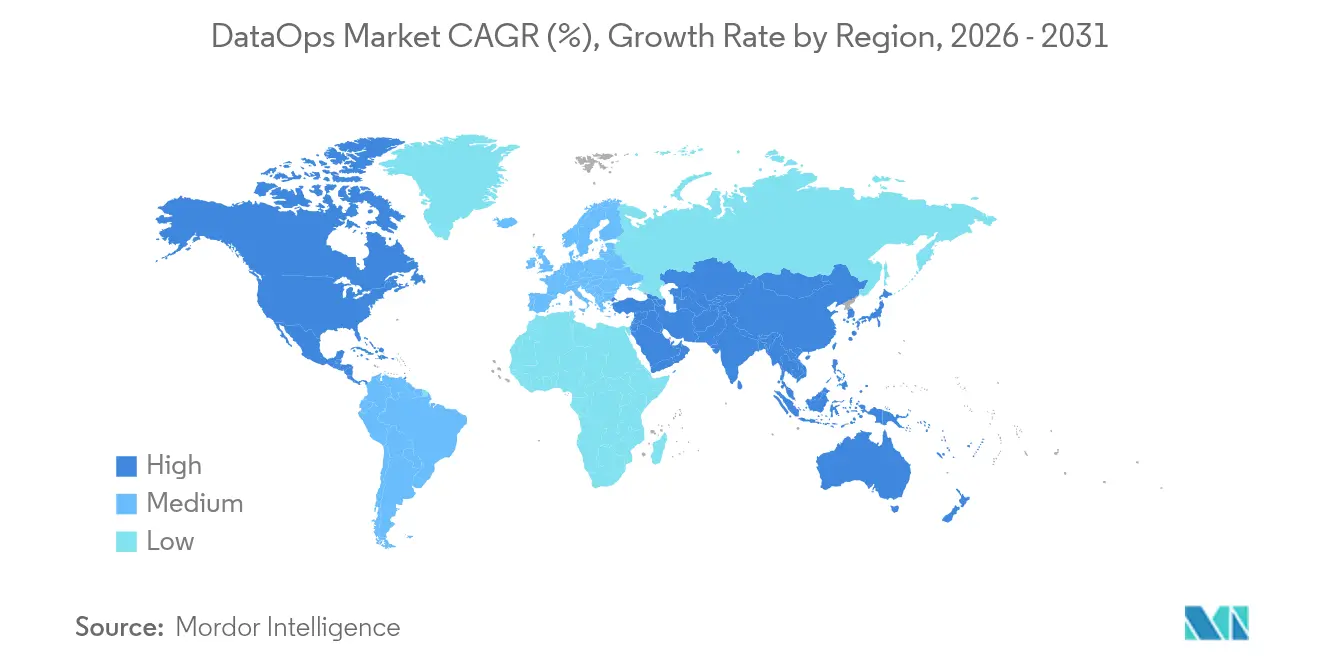

- By geography, North America represented 46.22% of 2025 revenue, while Asia-Pacific is set to grow at a 34.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global DataOps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of data volume | 8.5% | Global | Medium term (2-4 years) |

| Demand for real-time analytics | 7.2% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid adoption of cloud-native data stacks | 6.8% | Global | Medium term (2-4 years) |

| AI/ML initiatives requiring reliable pipelines | 5.9% | North America and EU | Long term (≥ 4 years) |

| Shift toward data-mesh architectures | 4.3% | Asia-Pacific and EU | Long term (≥ 4 years) |

| Sovereign-data laws driving automated lineage | 3.1% | EU and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of Data Volume

Enterprises are now moving petabytes of streaming and batch data across hybrid clouds, compelling the DataOps market to prioritize scalable, event-driven architectures. More than 150,000 organizations deploy Apache Kafka in production, underlining the shift to high-velocity pipelines that sustain sub-millisecond latency for digital payments and other real-time services.[1]PayPal Engineering, “Scaling Kafka for Sub-Millisecond Payments,” paypalobjects.com Platforms are integrating automatic schema evolution and real-time quality checks so that engineering teams can streamline both operational and analytical workloads within a single orchestration layer.

Demand for Real-Time Analytics

Business decision loops continue to shrink from days to minutes. Organizations that embed DataOps practices have documented 10-fold pipeline efficiency improvements along with lower total cost of ownership thanks to automated data quality monitoring.[2]Acceldata, “Case Study: Real-Time Analytics for Global Bank,” acceldata.ioFinancial institutions now process millions of fraud-screen transactions per second, and manufacturers lean on industrial DataOps to run predictive maintenance on sensor feeds, turning continuous data streams into operational savings.

Rapid Adoption of Cloud-Native Data Stacks

Enterprise cloud infrastructure spending topped USD 330 billion in 2024, and hyperscale providers are reporting double-digit annual growth, signaling an irreversible migration to cloud-hosted lakehouse and mesh-ready stacks. Amazon Web Services disclosed a USD 115 billion run rate in 2025, reflecting the pull of built-in DataOps capabilities such as serverless processing and automatic scaling.[3]Amazon Web Services, “AWS Announces First-Quarter 2025 Results,” aws.amazon.com Delta Lake and Apache Iceberg standards allow companies to fuse lake flexibility with warehouse performance, while infrastructure-as-code practices let data teams version control entire pipelines in the same repositories as application code.

AI/ML Initiatives Requiring Reliable Pipelines

Fifty-four percent of Asia-Pacific enterprises expect artificial intelligence to drive long-term revenue, making production-grade pipelines fundamental to avoiding model drift. The intersection of DataOps and MLOps brings unified platforms that manage data engineering, feature stores and model deployment. Financial firms now embed compliance-ready lineage into these pipelines, ensuring transparent audit trails for every inference executed in live systems.[4]Dataiku, “Regulatory Lineage for Financial Models,” dataiku.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and tooling costs | -4.2% | Global | Short term (≤ 2 years) |

| Shortage of skilled DataOps engineers | -3.8% | North America and EU | Medium term (2-4 years) |

| Tool-chain fragmentation and security gaps | -2.9% | Global | Medium term (2-4 years) |

| Cultural resistance in regulated sectors | -2.1% | EU and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Tooling Costs

Full-scale DataOps transformations often surpass USD 1 million once platform licensing, migration services and change-management programs are totaled. Organizations routinely underestimate cloud compute fees, with invoice overruns of up to 300% in early phases when pipeline workloads spike unpredictably. Fragmented tool-chains also inflate vendor-management overhead, prompting an industry pivot toward bundled, usage-based managed services that promise predictable spend.

Shortage of Skilled DataOps Engineers

Fifty-six percent of global enterprises plan to allocate at least a quarter of their data-mesh budgets to hiring, underlining a skills gap that commands salary premiums of 30-50% above standard data engineering roles. Academic programs lag behind market needs, prolonging time-to-competency. As a result, demand is rising for low-code orchestration tools and fully managed DataOps services that let business teams launch pipelines without deep engineering expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Drive Infrastructure Modernization

Platforms controlled 57.86% of 2025 revenue, evidencing the enterprise appetite for single-pane solutions that converge pipeline orchestration, observability and governance. Services revenue is forecast to scale at a 30.05% CAGR as buyers rely on managed deployments to mitigate talent shortages. Databricks reported USD 3.7 billion annualized revenue in 2025, underscoring platform momentum around lakehouse architectures. The DataOps market size attributable to platform revenues is growing in tandem with feature consolidation that now includes domain-centric mesh support, automated lineage and integrated security frameworks. Services providers remain vital for enterprises that must migrate complex legacy ETL into streaming pipelines quickly. Vendor consolidation, highlighted by recent hyperscaler acquisitions of orchestration startups, is expected to simplify tool selection while expanding support footprints.

A pivot toward low-code design spaces is further democratizing DataOps adoption. Citizen developers can author pipelines via drag-and-drop interfaces, freeing specialized engineers to tackle complex optimization. Consulting firms leverage accelerator blueprints to compress deployment cycles and to standardize governance templates across industries. As a result, the DataOps market continues to widen its addressable base beyond technology-centric organizations into traditionally conservative sectors such as healthcare and government.

By Deployment: Cloud Dominance Accelerates Hybrid Adoption

Cloud instances generated 62.50% of 2025 DataOps market share, and the segment is on track for a 31.25% CAGR as enterprises retire on-premise platforms or re-platform them into managed Kubernetes clusters. Sovereign cloud frameworks are influencing architectural patterns, particularly in Asia-Pacific, where governments stipulate local data residency. Microsoft Fabric bundles ingestion, transformation and BI under a unified SaaS model, offering customers simplified procurement and security. The DataOps market size attached to cloud deployments will benefit from multi-cloud and edge workloads that exert upward pressure on throughput and storage usage.

Hybrid patterns remain relevant. Heavily regulated verticals retain sensitive datasets on private racks while replicating non-critical data to the cloud for burst processing. Portable container images permit consistent runtime behavior across environments, and zero-trust policies encrypt pipeline traffic end-to-end. Security posture therefore becomes a prime evaluation criterion. As hyperscalers roll out nexus regions expressly for financial services and healthcare, the cloud share of total DataOps spend will likely climb further, though absolute on-premise expenditure will stay stable in monetary terms.

By Enterprise Size: SMEs Embrace Democratized DataOps

Large organizations accounted for 59.85% of 2025 revenue, leveraging expansive budgets to integrate broad DataOps feature stacks across multiple business lines. Yet SMEs are projected to register a 32.45% CAGR thanks to consumption-based pricing that removes capital barriers. The DataOps market size accruing to SMEs widens as vendors launch lightweight tiers that cover core orchestration and data quality functions without the overhead of enterprise governance modules. Astronomer’s Apache Airflow-as-a-Service illustrates this focus, combining turnkey clusters with predictable billing so mid-market firms can scale incrementally.

SMEs gravitate toward point solutions to solve immediate data movement challenges, later layering governance features as maturity grows. Managed DataOps subscriptions allow lean teams to outsource infrastructure, freeing them to concentrate on analytics value delivery. The skill shortage disproportionately affects this segment, pushing demand for auto-generated code, template libraries and AI assistants that translate business logic into deployable pipelines.

By End-User Industry: Healthcare Accelerates Digital Transformation

BFSI led 2025 adoption with 28.55% share as compliance workloads and fraud analytics demanded highly governed, high-throughput pipelines. Healthcare is forecast to compound at 34.70% per annum, the fastest among tracked verticals. A federated data-mesh program at Roche Diagnostics delivered over 200 production data products and USD 50 million in quantified benefits, spotlighting ROI when clinical datasets are organized as reusable assets. The DataOps market share inside healthcare is expanding on the back of electronic health record integration, predictive patient monitoring and stricter audit requirements.

Telecom and IT providers also invest heavily to manage network telemetry and subscriber analytics at petabyte scale. Manufacturers deploy Industrial DataOps for predictive maintenance, decreasing unplanned downtime and optimizing supply chains. Public-sector bodies are adopting DataOps to operationalize open-data programs and to power AI-assisted citizen services, especially as new digital infrastructure funds become available.

By Application: Real-Time Analytics Drives Innovation

Data integration remains the entry-point application because every advanced analytics initiative hinges on reliable ingestion and transformation. Yet pipeline orchestration and data observability are the fastest ascenders. Apache Airflow enjoys 92% user recommendations thanks to operational maturity at scale. Acceldata clients report 98% quality improvements and 50% downtime reduction after deploying AI-surfaced anomaly detection.

Real-time analytics applications now claim the highest growth rate as unified batch-and-stream processing removes historical silos between transaction systems and BI. Feature stores bridge data engineering and data science, supplying low-latency feature retrieval for online inference. Governance modules automate lineage graphing across heterogeneous tool-chains, satisfying auditors and reducing root-cause analysis times.

Geography Analysis

North America remained the largest regional contributor in 2025, attributing 46.22% of global revenue to early cloud adoption and deep venture capital that incubates specialist vendors. Enterprises in the United States selected DataOps to enforce stricter lineage and quality standards after high-profile data privacy fines, and federal agencies escalated investments as mission-critical workloads target zero-defect data pipelines. Canadian banks likewise expanded real-time fraud detection programs that depend on consistent event streaming.

Asia-Pacific is the fastest-growing geography at a 34.20% CAGR through 2031. Governments in South Korea and Singapore launched cloud-first mandates, with more than 10,000 public systems scheduled for migration to containerized, cloud-native environments by 2030. Local telecom operators and fintechs drive edge DataOps deployments to handle low-latency mobile transactions, and the manufacturing sector invests in Industrial DataOps to sharpen predictive maintenance.

Europe demonstrates robust momentum anchored by stringent sovereign data legislation. The United Kingdom’s post-Brexit data reform acts accelerate automated lineage tracking. The Digital Operational Resilience Act compels financial institutions to document data flows and control failures, leading to procurement of observability-centric DataOps engines. Nordic countries, characterized by advanced public digital services, embrace data-mesh blueprints that decentralize ownership yet maintain federated controls. Emerging regions in South America and the Middle East show rising interest but still need broader cloud infrastructure and specialist talent pools before large-scale DataOps rollouts become mainstream.

Competitive Landscape

The DataOps market is moderately fragmented. Amazon Web Services, Microsoft and Google capitalize on existing cloud relationships to upsell integrated pipeline, catalog and observability modules. AWS cited widespread uptake of its serverless data integrations as a contributor to its USD 115 billion run rate in 2025. Microsoft extends its reach through Fabric, amalgamating Synapse, Power BI and Purview into a single workspace, while Google presses an open-format approach with BigQuery and AlloyDB.

Specialist vendors thrive by focusing on developer experience. Astronomer, Prefect and Dagster deliver lightweight orchestration with pluggable APIs, winning deployments inside polyglot stacks where buyers avoid vendor lock-in. Observability innovators such as Acceldata, Monte Carlo and Metaplane differentiate on AI-driven anomaly detection. Consolidation has intensified: IBM absorbed StreamSets to bolster real-time integration, and Datadog acquired Metaplane to fold data quality into its observability suite. The rise of open standards like OpenLineage undermines proprietary lock-in, steering competition toward performance, cost and ecosystem breadth.

Industry-specific platforms are carving defensible niches. Healthcare-focused vendors integrate HIPAA compliance templates and FHIR mappings out of the box, while industrial suppliers attach OPC UA and time-series optimizations. Financial services platforms bundle Basel III and DORA compliance modules, shortening regulatory clearance cycles. This verticalization trend, coupled with intensifying vendor alliances, suggests continuing dynamism that benefits buyers through faster innovation and pricing pressure.

DataOps Industry Leaders

Amazon Web Services, Inc.

International Business Machines Corporation

Oracle Corporation

Microsoft Corporation

Informatica LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Databricks confirmed USD 3.7 billion annualized revenue, reflecting 50% year-over-year growth and new lakehouse enhancements for unified data and AI workloads.

- April 2025: Datadog acquired Metaplane to embed data quality monitoring within its full-stack observability product line.

- December 2024: Databricks raised USD 10 billion in Series J funding at a USD 62 billion valuation to finance AI product expansion and global reach.

- December 2024: Boomi announced the acquisition of Rivery, bringing modern pipeline automation into its integration platform portfolio.

Global DataOps Market Report Scope

DataOps is a collection of technical practices, workflows, cultural norms, and architectural patterns that enable rapid innovation and experimentation delivering new insights to customers with increasing velocity.

The dataops market is segmented by component (platform, services), by deployment (cloud, on-premises), by enterprises (large enterprises, medium and small enterprises), by end-user (BFSI, IT and telecom, Manufacturing, Retail and E-commerce, Healthcare, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platforms |

| Services |

| Cloud |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| IT and Telecom |

| Manufacturing |

| Retail and E-commerce |

| Healthcare |

| Government and Public Sector |

| Energy and Utilities |

| Data Integration and ETL |

| Pipeline Orchestration |

| Data Quality and Observability |

| Data Governance / Compliance |

| Real-time Analytics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Platforms | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Healthcare | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| By Application | Data Integration and ETL | ||

| Pipeline Orchestration | |||

| Data Quality and Observability | |||

| Data Governance / Compliance | |||

| Real-time Analytics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the DataOps market?

The DataOps market is valued at USD 7.72 billion in 2026 and is projected to reach USD 27.91 billion by 2031.

Which region shows the fastest growth in DataOps adoption?

Asia-Pacific is expected to advance at a 34.20% CAGR through 2031 as digital transformation programs and government cloud mandates accelerate demand.

Which component segment is expanding quickest?

Services are growing the fastest, with a 30.05% CAGR forecast because enterprises seek managed implementations to offset talent shortages.

Why is healthcare the fastest-growing end-user vertical?

Healthcare organizations pursue real-time patient analytics and regulatory compliance automation, driving a 34.70% CAGR for DataOps-enabled solutions.

How does cloud deployment influence DataOps strategies?

Cloud captured 62.50% of 2025 revenue and simplifies scaling, observability and security, prompting many firms to adopt hybrid or multi-cloud DataOps architectures.

Page last updated on: