Integration Platform-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.24 Billion |

| Market Size (2031) | USD 20.93 Billion |

| Growth Rate (2026 - 2031) | 17.75% CAGR |

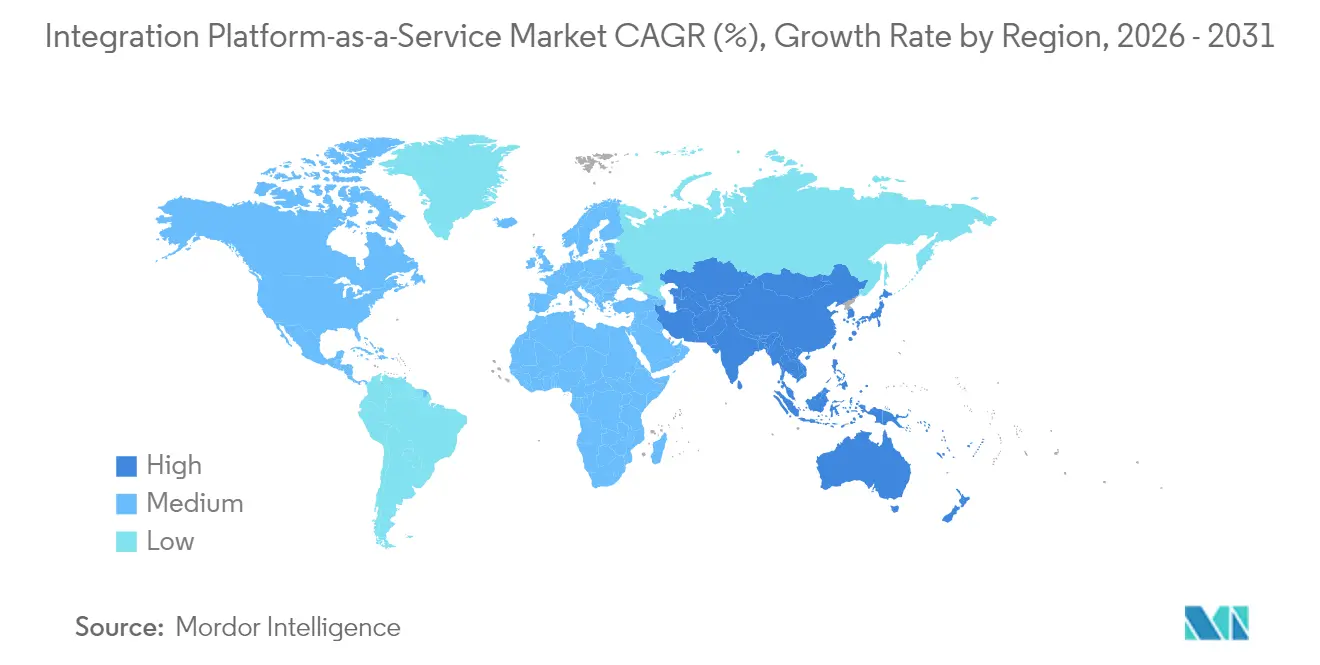

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integration Platform-as-a-Service Market Analysis by Mordor Intelligence

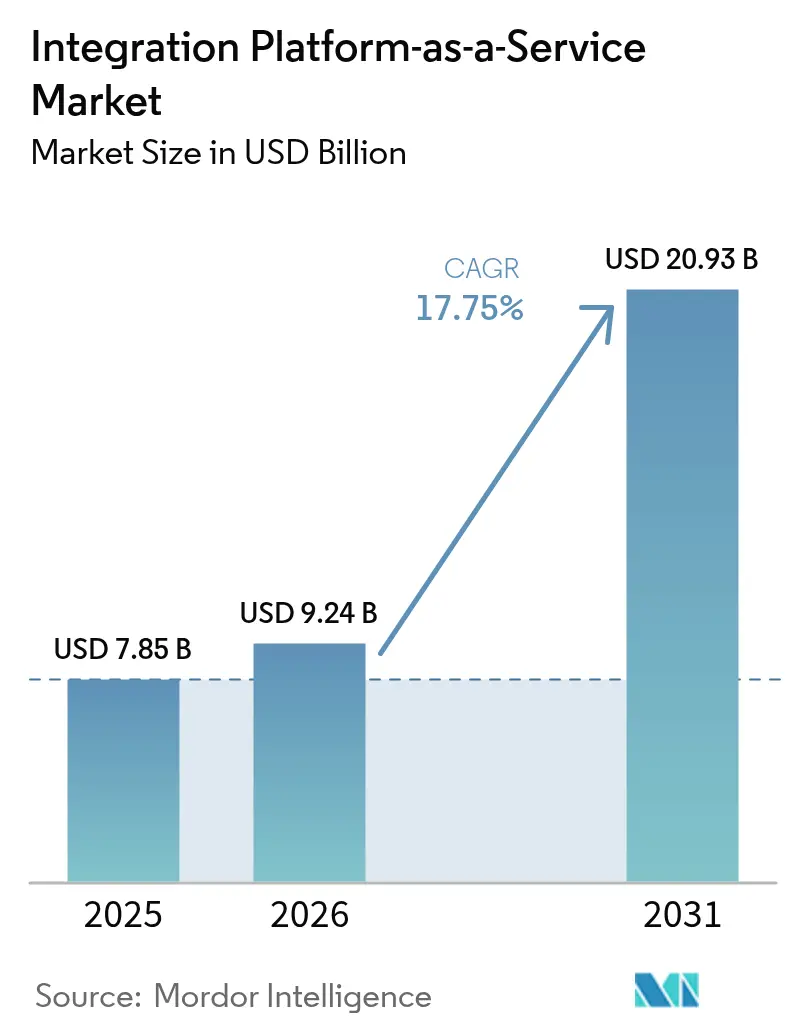

The Integration Platform-as-a-Service market size is expected to grow from USD 7.85 billion in 2025 to USD 9.24 billion in 2026 and is forecast to reach USD 20.93 billion by 2031 at 17.75% CAGR over 2026-2031. Expansion reflects mounting pressure on enterprises to connect proliferating SaaS, IoT, and edge assets while embedding AI in every integration flow. Event-driven architectures, GenAI design assistants, and sovereign-cloud mandates are reshaping platform requirements, nudging buyers away from hand-coded, point-to-point links toward intelligent, policy-aware fabrics. Competitive dynamics are equally fluid: hyperscale’s bundle native integration, independent vendors double down on multi-cloud openness and vertical specialization, and global system integrators form new alliance networks around data residency compliance. APAC’s manufacturing modernization, healthcare interoperability mandates, and consumption-based pricing for SMEs together create the strongest incremental demand signals over the next five years.

Key Report Takeaways

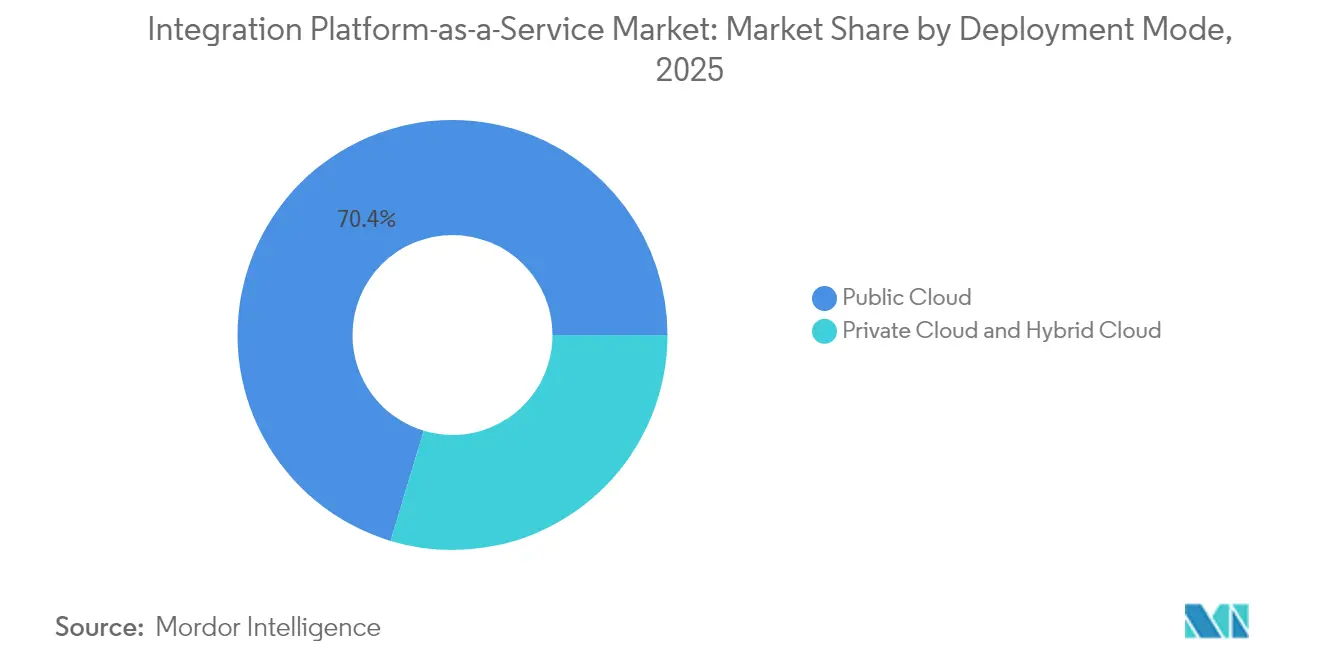

- By deployment model, Public Cloud led with 70.35% revenue share in 2025; Hybrid Cloud is projected to compound at a 27.35% CAGR through 2031.

- By end-user vertical, BFSI held 21.60% of the Integration Platform-as-a-Service market share in 2025, while Healthcare and Life Sciences is advancing at a 29.95% CAGR through 2031.

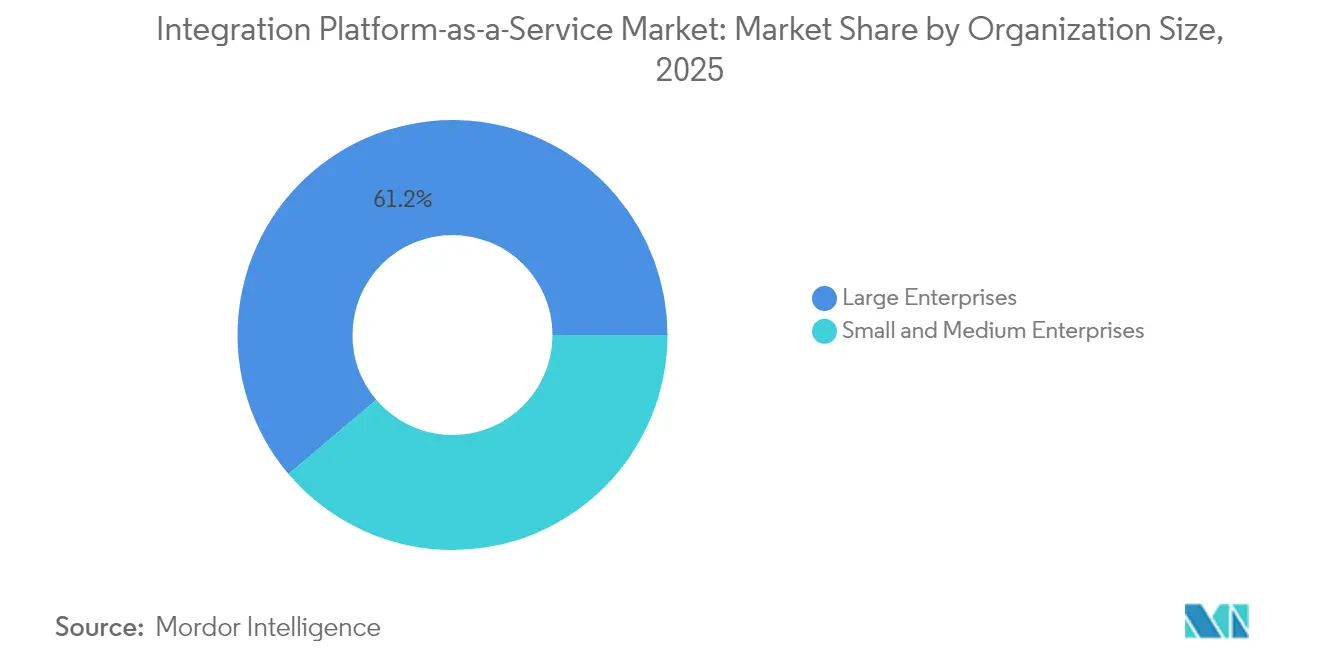

- By organization size, Large Enterprises accounted for 61.20% share of the Integration Platform-as-a-Service market size in 2025; SMEs are forecast to expand at a 32.10% CAGR between 2026-2031.

- By service type, Application Integration captured 41.40% of the Integration Platform-as-a-Service market size in 2025; API and Event Integration is accelerating at a 34.90% CAGR to 2031.

- By geography, North America commanded 45.40% share in 2025; APAC is set to grow fastest at 23.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Integration Platform-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-augmented integration and GenAI design assistants | +4.2% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| API-sprawl and composable enterprise mandates | +3.8% | Global, accelerated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Rise of event-stream and IoT edge integrations | +3.1% | APAC core, spill-over to North America manufacturing | Medium term (2-4 years) |

| Low-/no-code integration democratization | +2.9% | Global, strongest in SME segments | Short term (≤ 2 years) |

| CSP marketplace bundling of iPaaS SKUs | +1.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Pay-per-flow pricing unlocking SME adoption | +1.4% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-augmented integration and GenAI design assistants

Generative AI inside leading platforms such as MuleSoft’s Einstein and SnapLogic’s SnapGPT lets non-technical staff specify flows in plain language, trimming design cycles from weeks to hours.[1]Salesforce Press Room, “Salesforce to Acquire Informatica,” salesforce.com Monthly document throughput on SnapGPT reached 4.7 trillion in 2024, underscoring surging workload volumes. These assistants bring conversational tooling directly into IDEs, yet also raise governance questions whenever sensitive data travels through learning models. Providers able to marry secure prompts with enterprise policy controls gain a clear edge.

API-sprawl and “composable enterprise” mandates

Enterprises manage 400+ active APIs, a side-effect of microservices and SaaS adoption. Manufacturers digitising factories rely on real-time links between IoT sensors, ERP and digital-twin models to sustain predictive maintenance strategies. Composable business design, especially popular across APAC industrial hubs where 75% of service leaders plan extra digital spend in 2025, drives appetite for unified orchestration and streaming backplanes.[2]Fujifilm Business Innovation, “Digital Transformation Investment Survey 2025,” fujifilm.com

Rise of event-stream and IoT edge integrations

Factory and hospital edge nodes now require sub-second roundtrips to analytics tiers. Deployments using Apache Kafka connect edge sensors, cloud AI, and MES in a continuous loop, delivering 14.53% productivity gains and 13.9% energy savings in digital-twin pilots. Vendors such as Crosser illustrate how edge MLOps pipelines stretch iPaaS capabilities beyond the data-center perimeter.

Low-/no-code integration democratization

Analyst projections indicate non-technical users will craft 80% of digital solutions by 2025, accelerating the shift toward graphical flow builders. Embedded ML suggestions automate connector mapping, cutting development effort by up to 90% while preserving security guardrails. Platform vendors respond by integrating policy templates and audit trails into citizen-developer consoles to simplify oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hyperscale native-integration cannibalization | -2.8% | Global, strongest in mid-market | Short term (≤ 2 years) |

| Vendor lock-in and switching-cost anxiety | -1.9% | North America and EU enterprises | Medium term (2-4 years) |

| Data locality regulations prolonging sales cycles | -1.3% | EU and Middle East | Long term (≥ 4 years) |

| Talent scarcity in advanced event-stream architectures | -1.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing hyperscale native-integration cannibalization

AWS AppFlow, Azure Logic Apps, and Google Apigee Integration come bundled with core cloud services, undercutting standalone vendors on price and convenience.[3]AWS Blog, “Introducing AppFlow for Cross-Service Integration,” aws.amazon.com Mid-market buyers with existing cloud commitments often default to these native options, especially where feature depth beyond standard connectors is unnecessary. Independent vendors counter by emphasizing multi-cloud reach, industry-specific connectors, and advanced AI orchestration that hyperscalers do not yet match.

Vendor lock-in and switching-cost anxiety

Integrations become embedded in mission-critical operations, making platform migration costly. Research on lock-in dynamics links dependency levels with direct financial exposure, prompting enterprises to demand open standards and portable design artefacts. GDPR and similar rules intensify scrutiny in Europe, where data export or residency breaches carry significant penalties. Vendors respond through export APIs, containerized runtimes and transparent contract terms, but the tension between optimization and portability persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Cloud Bridges Sovereignty Gaps

Public Cloud retains the largest slice of the Integration Platform-as-a-Service market size at a 70.35% revenue contribution in 2025. Hybrid Cloud, though smaller, is cutting the gap at a rapid 27.35% CAGR to 2031 as firms reconcile cloud elasticity with sovereign data controls. This migration pattern correlates with GAIA-X frameworks and sector rules in finance and healthcare that restrict full public-cloud offload. Independent providers now position pre-engineered on-prem agents that mirror public-cloud runtimes, letting regulated workloads participate in shared integration fabrics while remaining in the country.

Enterprises increasingly allocate sensitive PII or trade-secret workloads to private cores yet orchestrate event streams across public edges for customer-facing services. European telcos use sovereign iPaaS layers to expose 5G network APIs safely to developers, while Japanese automakers mirror production-line telemetry into regional clouds for advanced analytics. The Integration Platform-as-a-Service market share advantage of Public Cloud narrows as these hybrid playbooks mature.

By End-user Vertical: Healthcare Accelerates Digital Integration

BFSI captured 21.60% of Integration Platform-as-a-Service market share in 2025, powered by open-banking APIs, real-time payments and compliance reporting. Healthcare and Life Sciences, meanwhile, charts the steepest growth at 29.95% CAGR on the back of EHR interoperability, HL7 FHIR mandates and telehealth infrastructure upgrades. Providers need instant data synchronization between clinical, claims and analytics systems to support value-based care.

Large hospital networks deploy streaming iPaaS nodes to collect vitals from connected devices and feed AI diagnostic models. Pharmaceutical R&D teams integrate LIMS with molecular simulation engines to cut cycle times. BFSI continues to invest in secure message protocols and anti-fraud event flows, yet regulatory deadlines in healthcare accelerate procurement decisions, tilting incremental spending toward specialized platforms with HIPAA-grade connectors.

By Organization Size: SME Growth Unlocks New Markets

Large Enterprises controlled 61.20% of Integration Platform-as-a-Service market size in 2025 by virtue of sprawling application estates and global compliance needs. SMEs, however, clock the fastest 32.10% CAGR through 2031, enabled by pay-per-flow or tiered subscription pricing that lowers adoption hurdles. Consumption models from vendors such as Frends start at EUR 30 per process, making enterprise-grade tooling affordable to smaller firms.

Low-code canvases and AI mapping assistants further shrink skills barriers, allowing business analysts to wire up CRM, e-commerce, and accounting tools without IT backlogs. Providers tailor onboarding with guided templates and community marketplaces, converting what were once complex three-month projects into same-day deployments. As SME contracts scale in volume, vendors must sustain multitenant elasticity and self-service support to preserve margins.

By Service Type: API Integration Drives Modern Architecture

Application Integration delivered 41.40% of Integration Platform-as-a-Service market size in 2025, cementing its role in bridging legacy ERPs with modern SaaS suites. Yet, API and Event Integration surges ahead at 34.90% CAGR to 2031 as organizations pivot to microservices and real-time analytics. Agentic AI now automatically generates OpenAPI specs and maps events to Kafka topics, letting teams spin up composable capabilities on demand.

Event gateways extend to edge clusters where sensor traffic triggers autonomous actions. Insurance companies stream telematics data to risk engines, while retailers analyze click-stream events in session. B2B file transfer and batch ETL retain niche relevance for regulated archival use cases, but spending gradually shifts toward API-first endpoints, serverless connectors and low-latency stream relays.

Geography Analysis

North America’s 45.40% revenue share in 2025 reflects entrenched enterprise cloud adoption and a dense concentration of iPaaS vendors. The region’s revenue mix tilts toward AI-augmented integration and multi-cloud automation, illustrated by Salesforce’s USD 8 billion Informatica acquisition in May 2025 that fused data management with workflow orchestration. Compliance-focused sectors such as finance and federal agencies still test sovereign extensions to mitigate lock-in risk.

APAC grows fastest at 23.20% CAGR through 2031, propelled by government digital-service programs and manufacturing overhauls under Industry 4.0 charters. The Asian Development Bank’s Digital Development Facility funnels technical assistance into AI and big-data platforms, indirectly raising demand for robust integration backbones. Japanese and Korean electronics giants connect smart-factory twins to cloud analytics, while ASEAN digital-ID schemes hinge on cross-agency API gateways. Europe balances opportunity and constraint: GAIA-X pushes open, federated cloud ecosystems, yet GDPR and pending AI laws prolong evaluation cycles. South America, Middle East and Africa currently register smaller revenues but show growing appetite for cloud-first integration where mobile adoption and fintech modernization are rapid.

Competitive Landscape

Moderate consolidation defines the Integration Platform-as-a-Service market. Salesforce (MuleSoft), Boomi and Informatica enjoy sizeable installed bases, sustained by global support desks, 1,000-plus connector catalogs and deep security certifications. Hyperscale’s, however, cross-sell native flows that ride on broader infrastructure contracts, compressing price points for straightforward workloads. Independent vendors counter with multi-cloud neutrality, sovereign-cloud deployment blueprints and GenAI-powered design copilots.

Strategic plays cluster around three themes. First, platform roll-ups: Salesforce’s Informatica purchase creates a vertically integrated data-to-workflow stack. Second, AI-first differentiation: IBM’s webMethods Hybrid Integration injects agentic AI to auto-manage APIs and B2B channels at scale. Third, vertical embedding: specialized connectors for HL7 FHIR, ISO 20022, or OPC-UA let providers win in regulated sectors resistant to generic cloud bundles.

Patent filings in automated schema mapping and streaming lineage attest to a continuing R&D arms race. Channel ecosystems also evolve, with system integrators weaving iPaaS blueprints into SAP, Oracle and cloud ERP modernization projects. For mid-market clients the battle narrows to simplicity, predictable consumption pricing and pre-built templates. For global enterprises it widens to data sovereignty, AI governance and advanced observability.

Integration Platform-as-a-Service Industry Leaders

Informatica Corporation

TIBCO Software Inc.

Oracle

IBM

Microsoft (Azure Logic Apps)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce agreed to acquire Informatica for USD 8 billion, combining integration, data management and AI Cloud assets into a single portfolio.

- May 2025: IBM unveiled the web Methods Hybrid Integration platform, adding agentic AI for automated API management plus consumption-based billing.

- March 2025: IBM released the Transformation Suite for SAP Applications to automate S/4HANA migration tasks.

- January 2025: IBM announced intent to buy Applications Software Technology LLC, extending Oracle Cloud consulting reach in government and education.

Global Integration Platform-as-a-Service Market Report Scope

An integration platform-as-a-service (iPaaS) is a managed solution primarily for hosting, designing, and integrating cloud data and applications. An iPaaS provides solutions from infrastructure and data warehousing to application design and DevOps environments. These iPaaS solutions can primarily simplify the integration of data, applications, security, and business compliance.

The studied market is segmented by deployment models (public cloud, private cloud, and hybrid cloud), end-user verticals (BFSI, retail & e-commerce, healthcare & life science, manufacturing, it & telecom, media & entertainment), and geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa). The impact of macroeconomic trends on the market is also covered under the scope of the study. Further, the disturbance of the factors affecting the market's evolution in the near future has been covered in the study regarding drivers and constraints. The market sizes and predictions are provided in terms of value in USD for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| BFSI |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| IT and Telecom |

| Media and Entertainment |

| Large Enterprises |

| Small and Mid-size Enterprises (SME) |

| Application Integration |

| Data / ETL Integration |

| API and Event Integration |

| B2B / E-commerce Integration |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By End-user Vertical | BFSI |

| Retail and E-commerce | |

| Healthcare and Life Sciences | |

| Manufacturing | |

| IT and Telecom | |

| Media and Entertainment | |

| By Organisation Size | Large Enterprises |

| Small and Mid-size Enterprises (SME) | |

| By Service Type | Application Integration |

| Data / ETL Integration | |

| API and Event Integration | |

| B2B / E-commerce Integration | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the projected size of the Integration Platform-as-a-Service market by 2031?

The market is forecast to reach USD 20.93 billion by 2031, expanding to an 17.75% CAGR.

Which deployment model is growing fastest?

Hybrid Cloud leads growth with a 27.35% CAGR from 2026-2031 as enterprises balance cloud agility with data sovereignty.

Which industry vertical shows the strongest expansion?

Healthcare and Life Sciences grows at a 29.95% CAGR to 2031, outpacing all other verticals due to EHR interoperability mandates.

How are hyperscales affecting independent iPaaS vendors?

AWS, Microsoft, and Google bundle native integration services that pressure pricing in the mid-market, pushing independents toward multi-cloud support, vertical expertise, and advanced AI features.

Why is APAC considered the most attractive growth region?

Coordinated government digital programs, manufacturing modernization, and rapid SME digitization drive a 23.20% CAGR for iPaaS across APAC markets.

What role does generative AI play in modern integration platforms?

GenAI design assistants automate connector mapping and workflow creation, enabling business users to build complex integrations in hours instead of weeks while providers embed governance controls to protect sensitive data.

Page last updated on: