Data Monetization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

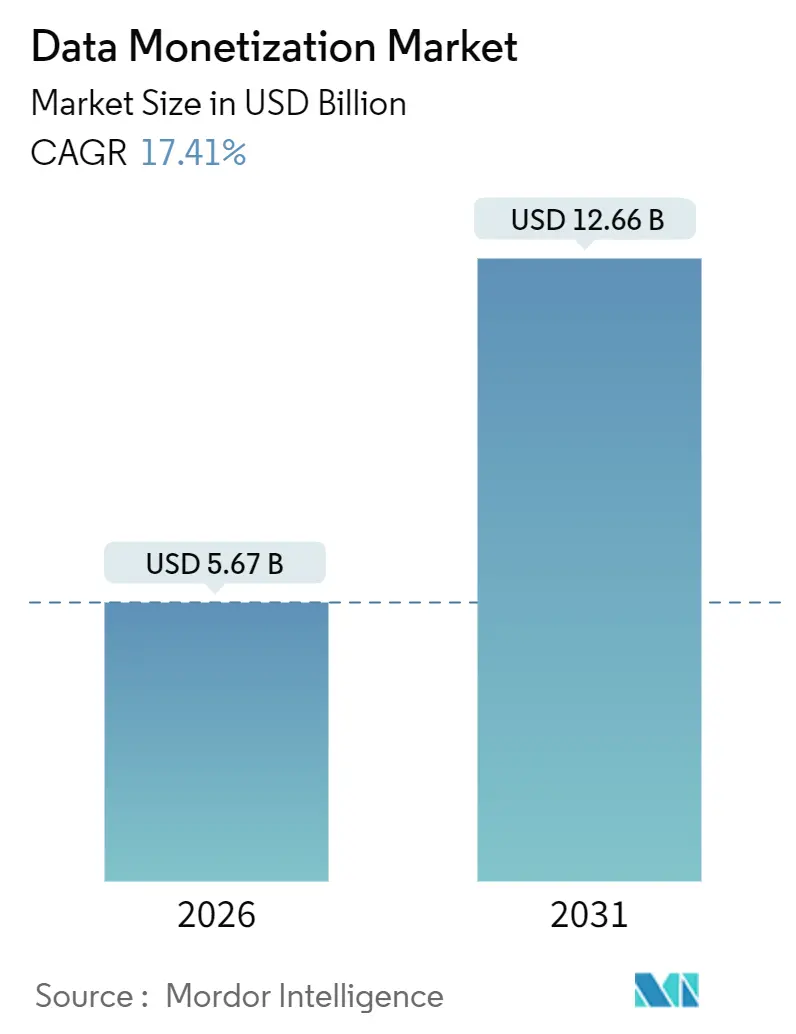

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 12.66 Billion |

| Growth Rate (2026 - 2031) | 17.41% CAGR |

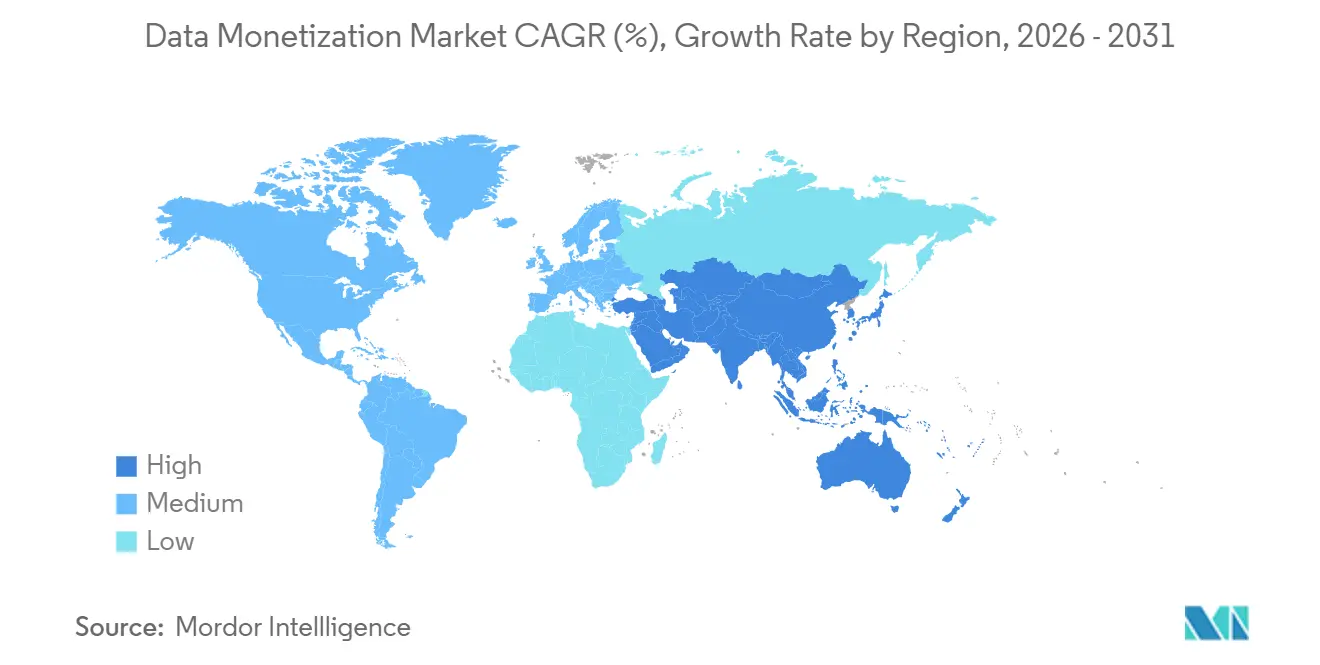

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

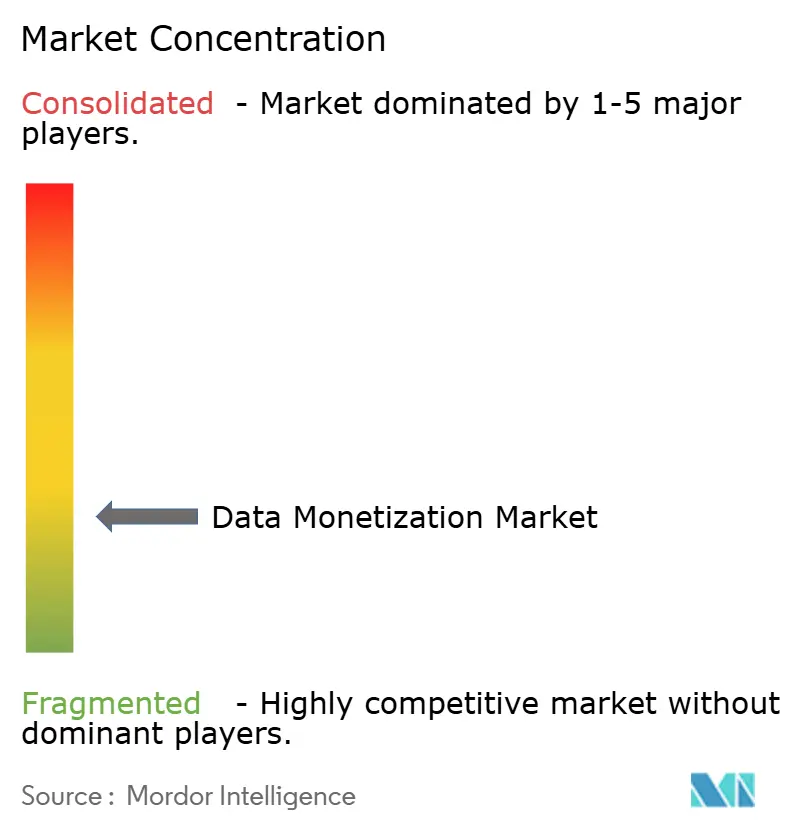

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Monetization Market Analysis by Mordor Intelligence

The data monetization market size is USD 5.67 billion in 2026 and is projected to reach USD 12.66 billion in 2031, advancing at a 17.41% CAGR. Demand is accelerating because enterprises now view data as a tradeable asset, and tokenization plus synthetic-data techniques have lowered historic privacy barriers. Regulatory open-data mandates in the European Union and India, combined with self-service cloud marketplaces, are shortening sales cycles and pulling new buyers into the ecosystem. Competitive intensity sits in a mid-range band, with no vendor holding double-digit share, yet hyperscalers remain gatekeepers through bundled marketplace capabilities and control of cloud-egress pricing. Risks stem from fragmented privacy laws and continuing cloud-egress fees that depress cross-platform trading economics. Asia Pacific is the fastest-growing region, while North America still generates the largest absolute revenue.

Key Report Takeaways

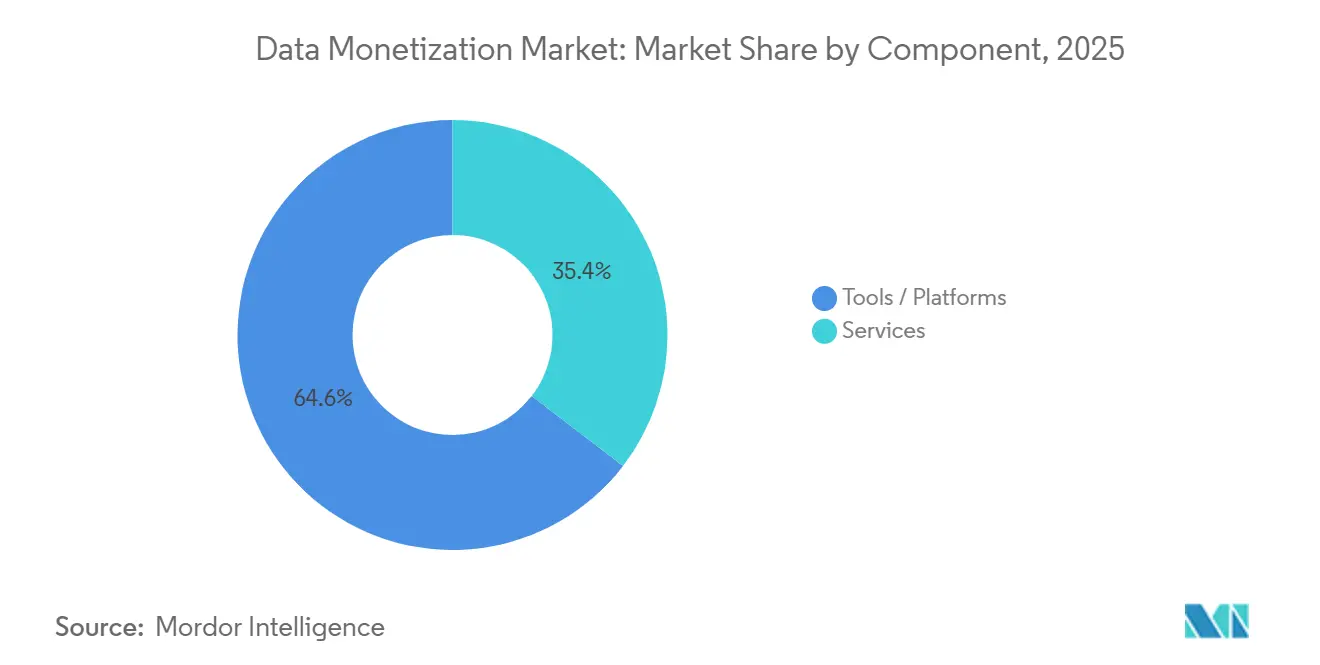

- By component, software and tools accounted for 64.58% of the data monetization market share in 2025, while services are forecast to expand at a 19.02% CAGR through 2031.

- By deployment mode, on-premises installations retained 59.76% share in 2025, yet cloud deployment is expected to advance at a 19.66% CAGR to 2031.

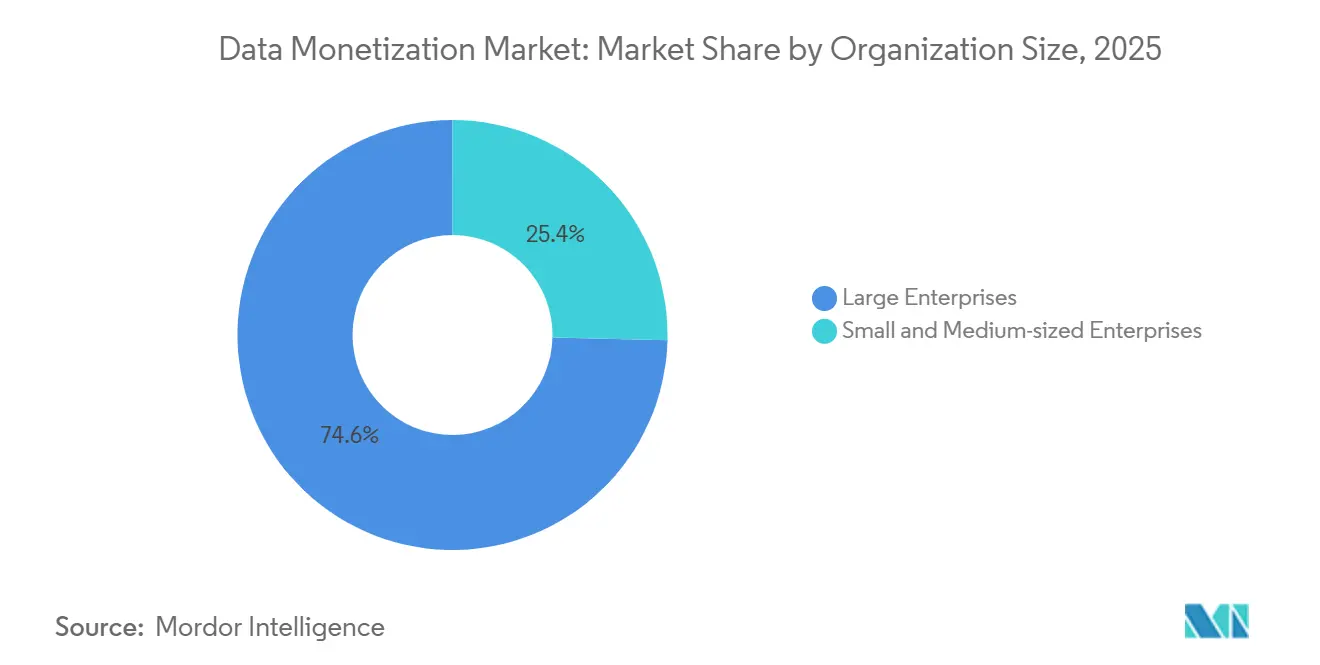

- By organization size, large enterprises contributed 74.62% share in 2025 whereas small and medium-sized enterprises are projected to grow at a 20.64% CAGR through 2031.

- By end-user industry, IT and telecommunications led with 29.22% of 2025 revenue, while retail and e-commerce is anticipated to register a 17.88% CAGR to 2031.

- By geography, North America dominated with 45.26% share in 2025, and Asia Pacific is set to post an 18.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Data Monetization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Advanced Analytics and Visualization | +3.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Increasing Volume and Variety of Enterprise Data | +4.1% | Global, accelerated in APAC manufacturing and telecom hubs | Long term (≥ 4 years) |

| Regulatory Mandates Driving Open-Data Ecosystems | +2.8% | Europe (EU Data Act), North America (state-level initiatives), APAC (India, China) | Short term (≤ 2 years) |

| Enterprise Adoption of Data Marketplaces Enabling B2B Data Trading | +3.5% | North America and Europe early movers, APAC following | Medium term (2-4 years) |

| Generative AI-Enabled Creation of Privacy-Safe Synthetic Data | +2.6% | Global, with healthcare and finance leading in North America and Europe | Medium term (2-4 years) |

| Tokenization of Data Assets Via Blockchain for New Revenue Streams | +1.3% | Pilot-stage in North America and Middle East, limited near-term scale | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Advanced Analytics and Visualization

Self-service business-intelligence platforms are collapsing the time from raw data ingestion to monetizable insight, enabling product managers and sales teams to package analytics as standalone offerings without relying on centralized IT. SAP Analytics Cloud and Microsoft Power BI now support embedded analytics that let software vendors white-label dashboards inside their applications, converting telemetry into recurring revenue streams. MicroStrategy's HyperIntelligence overlays contextual metrics on top of enterprise workflows, reducing the friction of switching between operational systems and analytics consoles.

Increasing Volume and Variety of Enterprise Data

IoT sensor deployments, edge-computing arrays, and application-programming-interface ecosystems are generating petabyte-scale datasets that exceed the absorptive capacity of internal analytics teams, pushing enterprises to externalize surplus data through marketplaces or direct licensing. Manufacturing plants now instrument assembly lines with vision systems and vibration sensors that produce real-time quality metrics, which equipment vendors monetize by offering predictive-maintenance subscriptions to peer factories. Telecom operators capture anonymized mobility patterns from cell-tower handoffs, selling aggregated flows to urban planners and retail-site selectors.

Regulatory Mandates Driving Open-Data Ecosystems

The EU Data Act, effective September 2025, compels manufacturers of connected products to provide data access to users and authorized third parties, effectively legislating interoperability and lowering the switching costs that previously locked datasets inside proprietary ecosystems, according to the European Commission. India's Digital Personal Data Protection Act of 2023 introduced consent managers that let individuals grant and revoke data-sharing permissions in real time, creating a compliance-friendly channel for enterprises to acquire consumer data for monetization.

Enterprise Adoption of Data Marketplaces Enabling B2B Data Trading

Snowflake's Data Marketplace, which hosts over 2,000 live datasets as of early 2025, allows providers to list curated tables that buyers can query without egress fees, eliminating the friction of file transfers and format conversions, according to Snowflake. AWS Data Exchange similarly enables sellers to publish APIs and S3 snapshots, with automated billing tied to consumption metrics. These platforms are shifting data transactions from bespoke contracts negotiated over months to self-service purchases completed in minutes, a velocity change that mirrors the SaaS revolution of the prior decade.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Hurdles with Legacy Architectures | -2.1% | Global, acute in North America and Europe with aging enterprise IT | Medium term (2-4 years) |

| Data Quality Inconsistencies Hindering Monetization Potential | -1.8% | Global, pronounced in manufacturing and healthcare sectors | Short term (≤ 2 years) |

| Fragmented and Evolving Data-Privacy Regulations | -1.5% | Global, with divergence between EU, US state-level, and APAC frameworks | Long term (≥ 4 years) |

| Escalating Cloud-Egress Fees Undermining Data-Sharing ROI | -1.2% | Global, concentrated among multi-cloud enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interoperability Hurdles with Legacy Architectures

Enterprises operate a median of 14 distinct data repositories, including relational databases, data lakes, SaaS application silos, and on-premises warehouses, each with proprietary schemas and access protocols that resist federation. Integrating these sources into a unified monetization layer requires extract-transform-load pipelines, API gateways, and semantic harmonization, investments that can exceed USD 5 million for a Fortune 500 firm and take 18 months to operationalize. The strategic risk is that by the time integration completes, the datasets may have lost market relevance or regulatory permissions may have expired.

Data Quality Inconsistencies Hindering Monetization Potential

IBM's 2024 study quantified that poor data quality costs the average organization USD 12.9 million annually through rework, compliance penalties, and lost revenue opportunities, according to IBM. Inconsistent timestamps, duplicate records, and missing values degrade the utility of datasets, forcing buyers to invest in cleansing before they can extract insights. The monetization consequence is that sellers must either pre-clean data absorbing costs that compress margins or discount prices to reflect quality risk, which depresses market valuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Capture Growth Momentum

Services are forecast to outpace tools, climbing at 19.02% from 2026 to 2031 even though tools commanded 64.58% of 2025 revenue. This variation shows that enterprises buy expertise to translate raw datasets into saleable products. Professional integrators design governance frameworks and negotiate marketplace onboarding, which compresses launch timelines. Within the tooling stack, data-integration platforms dominate because they harmonize disparate schemas, yet analytics front-ends are accelerating as no-code interfaces lower adoption barriers.

Managed services appeal to mid-sized firms that lack in-house data engineers, allowing them to offer subscription-based data products without capital expenditure. The data monetization market size contribution from services is set to rise as confidential computing reduces residency concerns. Partnerships between cloud providers and global systems integrators further expand service catalogs. Microsoft reported that 40% of Azure Synapse revenue flowed through managed-service channels in 2025.[1]Microsoft, “Azure Synapse Analytics Partner Ecosystem Report,” MICROSOFT.COM

By Deployment Mode: Cloud Adoption Accelerates

On-premises still held 59.76% share in 2025, largely within finance and healthcare. Confidential-computing enclaves now encrypt data in use, which satisfies auditors and unlocks cloud migration. Cloud installations are projected to advance at 19.66% CAGR, narrowing the historical gap. Hybrid fabrics combine on-premises warehouses with cloud lakes, creating a single logical layer from which sellers expose tables without relocation.

The EU Data Act obliges providers to support data portability, which eases fears of lock-in and boosts cross-border trading.[2]European Commission, “Data Act,” EUROPA.EU BigQuery Omni and Snowflake cross-cloud replication neutralize egress fees inside the same region, yet replication costs remain a consideration. Vendors that abstract location while preserving governance, such as data-mesh platforms, enjoy rising demand. Overall, the deployment mix is shifting toward flexible fabrics that support monetization at scale.

By Organization Size: SMEs Scale Quickly

Large enterprises supplied 74.62% of the organization-size segmentation in 2025, reflecting the metric’s isolation from other cuts. SMEs, however, will expand at 20.64% CAGR through 2031, driven by freemium analytics tiers and consumption-based cloud pricing. Marketplaces handle payment processing and compliance, so a regional logistics firm can list geospatial datasets beside Fortune 500 offerings. SMEs focus on high-fidelity niches such as hyperlocal weather or specialty retail baskets that fetch premium prices due to scarcity.

Deloitte found that SME data products carry 30% higher margins than those from large firms. Discoverability remains a hurdle; keyword-rich catalog entries and automated quality scores help smaller sellers gain visibility. Platform providers that offer marketing toolkits for SMEs therefore capture additional gross merchandise value. The segment’s velocity evidences democratization within the data monetization market.

By End-User Industry: Retail Media Networks Surge

IT and telecommunications held 29.22% revenue share in 2025 by monetizing anonymized mobility data for urban-planning buyers. Retail and e-commerce is poised for the fastest growth at 17.88% CAGR to 2031 as retail media networks convert first-party shopper data into advertising inventory. Closed-loop attribution gives retailers a clear edge over traditional advertising channels. Healthcare institutions rely on synthetic electronic health records that mirror clinical patterns without exposing identifiers, opening new licensing paths for drug-discovery partners.

Manufacturing, logistics, and energy trail in maturity but produce vast telemetry, so these verticals represent future white-space. Financial institutions monetize credit-bureau feeds and transaction analytics, though cross-border transfers remain tightly regulated. Government agencies publish open data that private resellers enrich with analytics. Each vertical shows distinct privacy and interoperability constraints that shape the monetization strategy.

Geography Analysis

North America delivered 45.26% of 2025 revenue, reflecting mature analytics stacks, dense buyer ecosystems, and the early rollout of enterprise data marketplaces. State-level privacy statutes such as the California Consumer Privacy Act introduce compliance complexity, yet they also encourage investment in governance tools that streamline sharing and thus stimulate monetization. The region’s hyperscalers provide bundled marketplace rails, driving favorable network effects for sellers that already store data on the same platforms. Urban planners, hedge funds, and advertising agencies collectively underpin robust demand, making liquidity high relative to other regions.

Asia Pacific is the fastest-growing territory with an 18.24% CAGR through 2031, supported by India’s Digital Personal Data Protection Act and China’s Personal Information Protection Law, both of which clarify consent protocols for commercial data use. Regulatory certainty has lowered legal risk and encouraged multinationals to base data-exchange hubs in Singapore and Tokyo. Manufacturing telemetry from smart factories in Japan and South Korea comprises a fresh supply pool, while Southeast Asian e-commerce and fintech players create rising demand. Governments across the region are funding data-center capacity, which reduces latency and keeps residency in-country.

Europe exhibits steadier growth because GDPR remains stringent, yet the EU Data Act now obliges connected-device manufacturers to provide user-level data access, expanding B2B trading potential. Industrial IoT datasets, especially automotive and machinery telemetry, stand to benefit from mandated interoperability. However, localization rules can delay cross-border deals, urging vendors to adopt federated learning that leaves data in place. Latin America, the Middle East, and Africa represent nascent markets where digital infrastructure is improving but buyer ecosystems are still forming. Smart-city projects and mobile-money systems present future opportunities once legal frameworks stabilize. Collectively, geographic diversification helps to smooth cyclical variances in individual economies.

Competitive Landscape

The field remains moderately fragmented, with no participant exceeding a 10% revenue share. Hyperscalers such as AWS, Microsoft Azure, and Google Cloud bundle data-exchange services into their infrastructure portfolios, thus anchoring sellers that already rely on their storage and compute offerings. Snowflake differentiates by eliminating intra-cloud egress fees and offering cross-cloud replication, which addresses the USD 100 billion egress friction identified by Cloudflare. Governance specialists like Collibra and Informatica focus on metadata lineage, supplying the audit trails required for GDPR and CCPA compliance. Niche exchanges, including Dawex and Narrative, curate vertical catalogs, for example, industrial IoT or advertising identifiers.

White-space resides in industries with heavy telemetry but limited data-trading norms, especially manufacturing, logistics, and energy. Vendors are piloting federated learning so sellers can earn royalties on model outcomes without relinquishing raw files, sidestepping privacy and egress hurdles. Tokenization remains experimental yet strategically significant; blockchain rails could automate royalty distribution once regulatory clarity emerges.[3]World Economic Forum, “Tokenization of Real-World Assets,” WEFORUM.ORG Consolidation is underway as governance and quality-scoring providers merge to create end-to-end platforms. Collibra’s 2025 acquisition of Alation’s metadata unit exemplifies the move toward integrated control planes. Overall competition is shifting from single-function tools toward ecosystem plays that span ingestion, quality, compliance, and marketplace exposure.

Data Monetization Industry Leaders

Accenture plc

Adastra Corporation

Amazon Web Services Inc.

Cisco Systems Inc.

Collibra NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Snowflake added regulated-industry datasets to its marketplace after rolling out confidential computing enclaves, expanding addressable sellers and buyers.

- September 2025: The EU Data Act entered into force, legally obliging connected-product makers to open data APIs and spurring industrial data-exchange investment.

- July 2025: Microsoft launched Synapse Data Sharing to federate on-premises SQL Server databases with Azure Synapse Analytics, enabling data monetization without migration.

- May 2025: The World Economic Forum projected tokenized real-world assets, including data, could reach USD 4 trillion by 2035, spotlighting supply-chain provenance as an early use case.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global data monetization market as the revenue generated when enterprises convert internal or partnered datasets into sellable products, APIs, insights, or revenue-sharing services across all industries. The valuation covers software platforms, enabling tools, implementation services, and license or subscription income derived from direct and indirect monetization models.

Scope does not cover standalone consumer data-brokerage services that resell raw personally identifiable information.

Segmentation Overview

- By Component

- Tools / Platforms

- Data Integration and Management Tools

- Analytics and Visualization Tools

- Services

- Professional Services

- Managed Services

- Tools / Platforms

- By Deployment Mode

- On-Premises

- Cloud

- Hybrid

- By Organization Size

- Small and Medium-Sized Enterprises

- Large Enterprises

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Telecom and IT

- Manufacturing

- Healthcare and Life Sciences

- Retail and E-Commerce

- Transportation and Logistics

- Energy and Utilities

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed chief data officers at cloud hyperscalers, product managers at data-as-a-service platforms, analytics consultants serving retail media networks, and privacy compliance advisors in North America, Europe, and Asia. Their insights clarified typical license pricing ladders, regional regulatory friction, and uptake timelines, allowing us to tighten assumptions surfaced during desk work.

Desk Research

We collected foundational numbers from open government sources such as the U.S. Bureau of Economic Analysis for ICT spending trends, Eurostat for cloud adoption ratios, and the International Telecommunication Union for global data traffic volumes. Trade associations including the Interactive Advertising Bureau and GSMA provided spend on first-party data and average devices per user, while peer-reviewed papers in IEEE Xplore illustrated price points of synthetic data sets. To enrich company-level inputs, Mordor analysts extracted revenue splits from 10-K filings and investor decks, then verified news flows through Dow Jones Factiva and firmographics via D&B Hoovers. The sources listed illustrate our approach and are not exhaustive; many additional records informed data checks.

Market-Sizing & Forecasting

A top-down reconstruction starts with global ICT outlays, applies the share spent on advanced analytics, and then layers monetization penetration rates by industry. Select bottom-up checks, such as sampled average selling price multiplied by active marketplace listings and vendor roll-ups, test and adjust totals. Key variables powering the model include enterprise cloud storage costs, average data marketplace transaction values, counts of retail media networks, GDPR/CCPA enforcement fine totals, synthetic-data share of anonymization workflows, and per-capita mobile data usage. Forecasts to 2030 employ multivariate regression blended with ARIMA smoothing, with coefficients validated against consensus views gathered in primary research. Data gaps in niche verticals are bridged by proportional allocation using publicly disclosed pilot volumes.

Data Validation & Update Cycle

Outputs pass variance checks against independent benchmarks before a two-step analyst review. Models refresh each year, and interim updates are triggered when events, such as landmark privacy laws or major platform acquisitions, materially shift an input. A final sense-check is performed just before report release so clients receive the latest view.

Why Mordor's Data Monetization Baseline Sets the Industry Standard

Published estimates frequently diverge because firms pick different service inclusions, apply varied license-fee assumptions, convert currencies at dissimilar dates, and refresh at uneven cadences.

Key gap drivers in this market stem from whether indirect value capture is counted, how aggressively platform-as-a-service growth is projected, and whether enforcement costs temper adoption rates. Mordor Intelligence reports the full funnel tools and services but removes pure PII reselling; some peers either over-add adjacent governance software or understate emerging marketplace fees, which enlarges or shrinks their totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.78 B | Mordor Intelligence | - |

| USD 4.05 B | Global Consultancy A | Excludes implementation services and applies 2023 exchange rates |

| USD 5.22 B | Industry Analyst B | Includes consumer data brokers and forecasts with unverified 30% CAGR |

| USD 3.47 B | Trade Journal C | Uses 2024 base year and assumes conservative marketplace uptake |

These comparisons show that by selecting transparent scope boundaries, verifying input ratios with practitioners, and revisiting models annually, Mordor delivers a balanced baseline that decision-makers can track, replicate, and trust.

Key Questions Answered in the Report

How big is the data monetization market in 2026?

The data monetization market size is USD 5.67 billion in 2026.

What is the forecast CAGR for data monetization through 2031?

The market is projected to grow at a 17.41% CAGR from 2026 to 2031.

Which region shows the fastest growth for data monetization?

Asia Pacific leads with an expected 18.24% CAGR to 2031.

Which component of data monetization is expanding most quickly?

Services, including consulting and managed analytics, are forecast to rise at 19.02% CAGR.

What vertical will add revenue fastest?

Retail and e-commerce will climb at a 17.88% CAGR as retail media networks monetize first-party shopper data.

How do cloud-egress fees affect data monetization?

Egress charges create cost friction that favors intra-cloud transactions and shape vendor strategies around cross-cloud replication.

Page last updated on: