Data Erasure Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

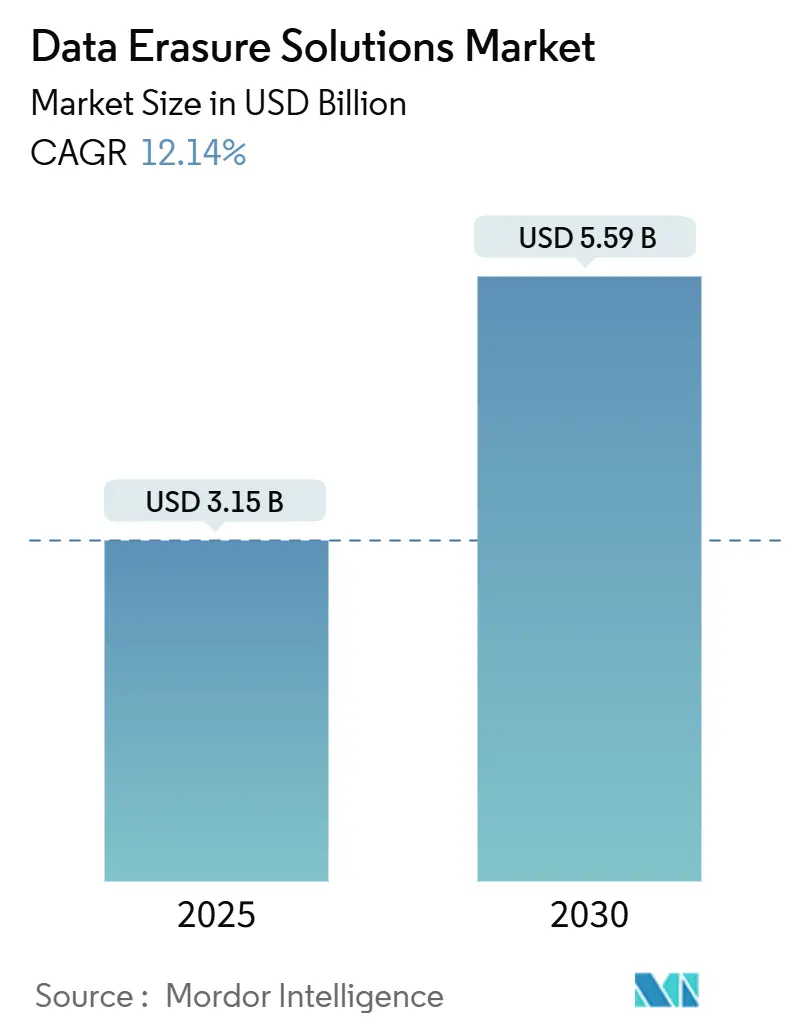

| Market Size (2025) | USD 3.15 Billion |

| Market Size (2030) | USD 5.59 Billion |

| Growth Rate (2025 - 2030) | 12.14% CAGR |

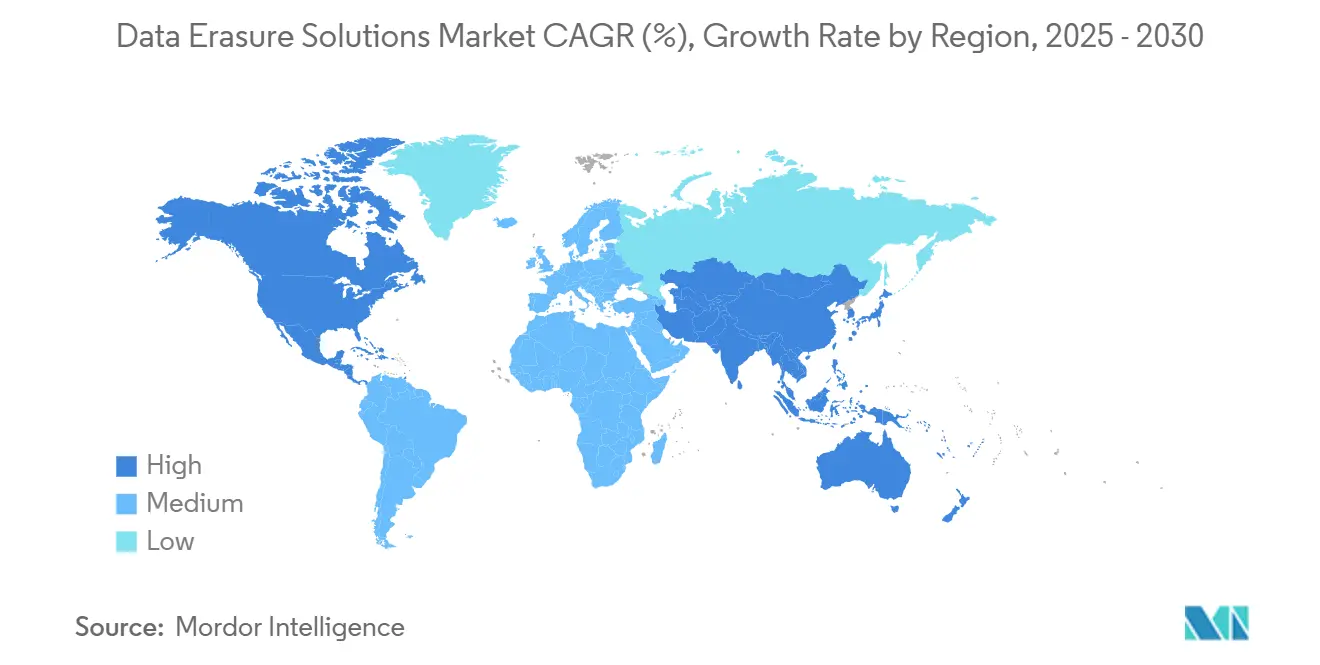

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Erasure Solutions Market Analysis by Mordor Intelligence

The data erasure solutions market size stands at USD 3.15 billion in 2025 and is projected to reach USD 5.59 billion by 2030, expanding at a 12.14% CAGR. Heightened enforcement of global privacy statutes, rising IT asset disposition (ITAD) volumes, and enterprise migration to hybrid cloud models collectively reinforce demand for certified software-based sanitization. Hyperscale data-center operators now process millions of drive erasures annually, while midsized organizations adopt subscription platforms that eliminate the need for dedicated appliances. Mobile and IoT proliferation amplifies the threat surface, prompting enterprises to extend erasure policies beyond traditional storage. Competitive differentiation increasingly centers on API integration, audit-grade reporting, and multicloud orchestration—capabilities that underpin long-term revenue resilience for vendors.

Key Report Takeaways

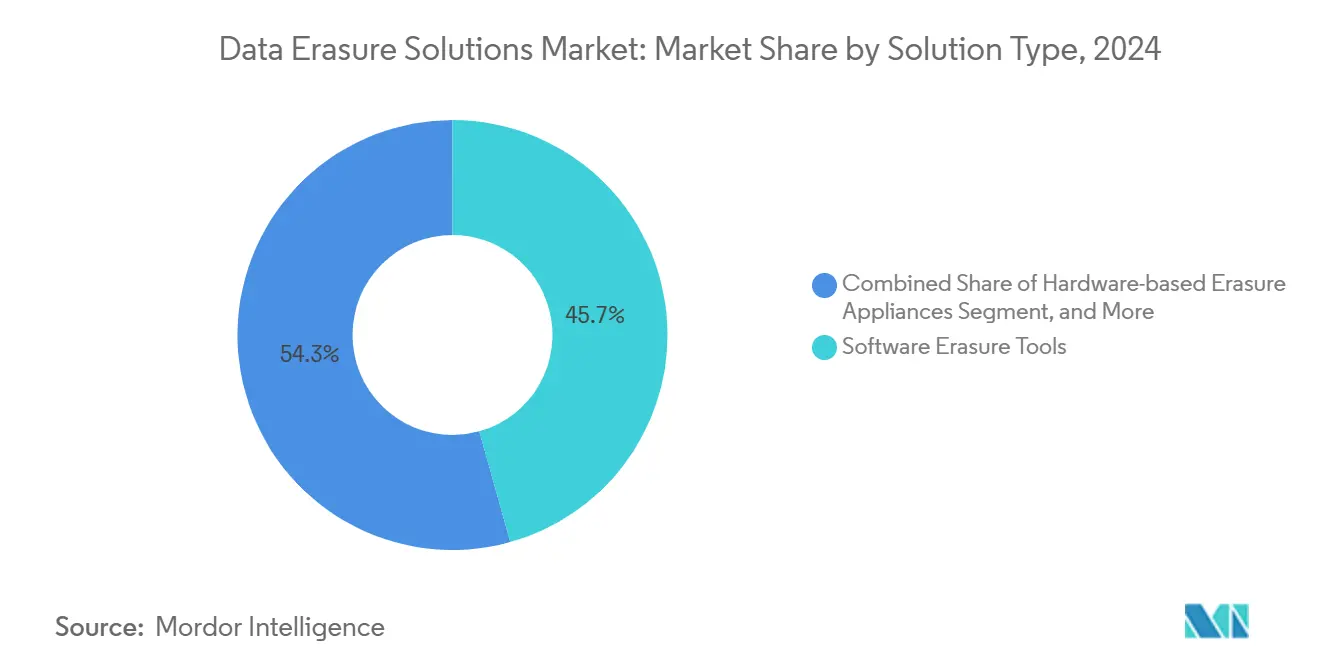

- By Solution Type, software erasure tools captured 45.67% of the data erasure solutions market share in 2024; cloud-delivered erase-as-a-service is advancing at a 12.89% CAGR through 2030.

- By Deployment Mode, on-premises deployment retained 56.98% of the data erasure solutions market size in 2024, while cloud-hosted architectures are forecast to expand at 13.64% CAGR to 2030.

- By Device / Media Type, hard disk drives held 37.42% share of the data erasure solutions market size in 2024; mobile devices represent the fastest-growing media category at 12.38% CAGR.

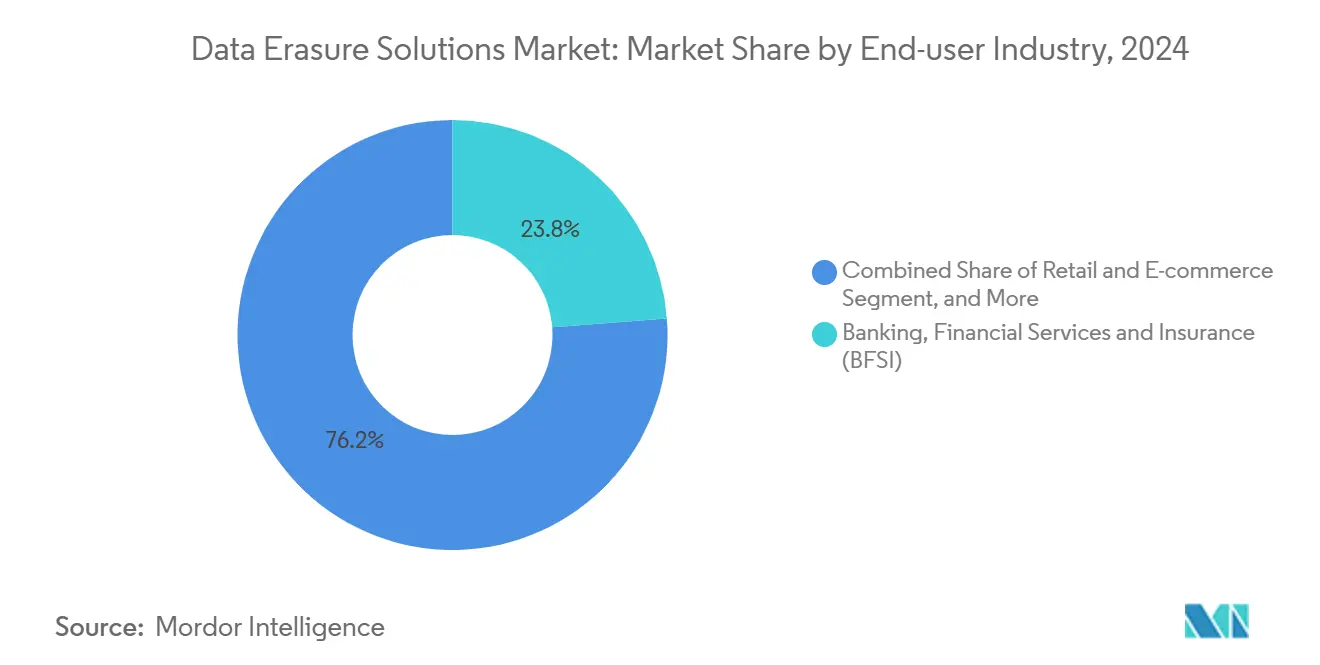

- By End-user Industry, BFSI accounted for 23.78% of the data erasure solutions market share in 2024; retail and e-commerce is the most dynamic vertical, rising at a 12.26% CAGR to 2030.

- By Organization Size, large enterprises commanded 61.63% of 2024 spending, yet SMEs are expanding at 13.77% CAGR through 2030, signaling democratization of enterprise-grade tools.

- By Geography, North America contributed 42.31% of 2024 revenue, whereas Asia-Pacific is projected to post a 12.86% CAGR on the back of rapid digitization and new privacy statutes.

Global Data Erasure Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global data-protection regulations | +3.2% | EU, North America, advanced Asia-Pacific | Medium term (2-4 years) |

| Surge in IT asset disposition volumes | +2.8% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid expansion of hyperscale DC decommissioning | +2.1% | Global, concentrated in major cloud regions | Long term (≥ 4 years) |

| Escalating cost of data-breach fines | +1.9% | EU, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Secondary-device trade-in boom | +1.4% | North America and Europe, growing global influence | Short term (≤ 2 years) |

| API-driven “erase-as-code” adoption | +0.8% | North America, EU, advanced Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Data-Protection Regulations Drive Market Expansion

Fines under GDPR surpassed EUR 1.6 billion (USD 1.8 billion) in 2024, with 23% attributed to retention and deletion lapses. Enterprises increasingly adopt certified erasure platforms that auto-generate tamper-proof logs, replacing manual deletion workflows that cannot withstand audits. Carrefour’s EUR 3 million penalty for erasure failures exemplifies the financial stakes. [1]CNIL, “Carrefour Fined 3 Million Euros for GDPR Violations,” cnil.fr California’s CPRA further widens erasure scope to derived and algorithmic data, compelling U.S. firms to modernize sanitization policies. Similar statutes emerging in India and China ensure global compliance remains a central spending driver for the data erasure solutions market.

Surge in IT Asset Disposition Volumes Accelerates Market Growth

The installed base of enterprise storage devices reached 2.8 billion units in 2024, with refresh cycles shrinking to 18–24 months for performance-critical gear. [2]IEEE, “Data Storage Security Standards,” ieee.org ITAD vendors now process bulk lots of decommissioned hardware within days, a pace sustainable only through automated erasure appliances capable of parallel drive wiping. Iron Mountain logged 40% growth in erase requests in 2024 as customers prioritized sustainability metrics alongside security. Certified erasure enables resale pathways that lower e-waste by up to 85% versus shredding, reinforcing ESG objectives. As device volumes swell, scalable software aligns with cost and environmental mandates, solidifying its role in the data erasure solutions market.

Rapid Expansion of Hyperscale Data-Center Decommissioning

Cloud operators regularly retire entire server pods, sometimes exceeding 15 million drives annually. Microsoft’s Azure team erased 2.5 million drives in 2024, achieving 99.7% first-pass completion through API-orchestrated workflows. [3]Microsoft, “Azure Security Compliance Data Erasure,” microsoft.com Next-generation liquid-cooled racks integrate NVMe and storage-class memory that demand firmware-aware wipe methods. Purpose-built appliances performing cryptographic erase at scale now constitute essential infrastructure inside decommissioning bays. As AI workloads compress hardware life cycles, continuous retirement streams bolster long-run revenue visibility for the data erasure solutions market.

Escalating Cost of Data-Breach Fines and Reputational Loss

Thirty-one percent of breach forensics in 2024 traced root cause to residual data on discarded media. Global breach costs averaged USD 4.45 million, with lost business dwarfing regulatory penalties. A leading European bank incurred EUR 85 million after customer files resurfaced on auctioned backup tapes. Insurers increasingly mandate wipe certificates before underwriting cyber coverage, turning erasure logs into de facto compliance currency. This cost-avoidance imperative sustains premium pricing within the data erasure solutions industry despite market fragmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low SME awareness and perceived complexity | -1.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Preference for physical destruction | -1.2% | Global, strongest in defense and healthcare | Long term (≥ 4 years) |

| Default firmware encryption in SEDs | -0.9% | Global, led by enterprise SSD uptake | Medium term (2-4 years) |

| Rare-earth component shortage | -0.7% | Global supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low SME Awareness and Perceived Complexity Limit Uptake

Sixty-seven percent of SMEs still rely on simple re-formatting, unaware that data remains recoverable with freeware tools. Limited cybersecurity staff and capex constraints stymie adoption of standalone appliances. Managed service providers now embed cloud-hosted wipe functions within broader IT bundles, lowering barriers but not eliminating skills gaps. Subscription models priced per device resonate with cost-sensitive firms yet require continued education. Unless awareness campaigns intensify, this knowledge deficit will temper SME contributions to the data erasure solutions market.

Preference for Physical Destruction in Highly Regulated Sectors

Defense and healthcare agencies default to shredding, citing Department of Defense rules mandating physical obliteration for TOP SECRET data. Although certified software erasure meets NIST standards for lower classifications, cultural perceptions of risk impede change. Hybrid policies are emerging: bulk erasure for non-classified workloads, shredding for select assets. Vendors offer combined services, yet hardware retirement contracts in these sectors still prioritize mechanical destruction, constraining penetration rates within the data erasure solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Software Dominance and Cloud Momentum

Software tools generated the largest revenue slice at 45.67% in 2024, confirming their versatility across heterogeneous fleets and operating systems. The data erasure solutions market size for software is projected to climb steadily as APIs embed wiping logic into IT service workflows. Vendors differentiate through certification breadth, support for encrypted media, and audit-grade log integrity. Hardware appliances cater to hyperscale operators needing multi-bay throughput exceeding 300 drives per hour, a niche but capital-intensive arena.

Erasure-as-a-service platforms exhibit the highest 12.89% CAGR, leveraging multitenant architectures that slash maintenance overhead for clients. Integration with CI/CD pipelines positions cloud services as foundational to DevSecOps, enabling “erase-as-code” triggers during automated build and test cycles. Providers monetize by tiered analytics, offering dashboards that map asset disposition against ESG targets. The data erasure solutions market therefore shifts from product sales toward consumption-based subscriptions without diluting software leadership.

By Deployment Mode: On-Premises Control Versus Cloud Agility

On-premises deployments commanded a 56.98% share in 2024, reflecting sovereignty mandates that keep sanitization inside corporate firewalls. These environments often pair wipe engines with air-gapped networks, ensuring zero external connectivity during erasure events. The data erasure solutions market share for on-premises is defended by banking, defense, and critical-infrastructure clients that treat wipe logs as internal classified documents.

Conversely, cloud-hosted deployments are advancing at 13.64% CAGR because centralized management reduces total cost of ownership. Multiregion dashboards allow security teams to enforce uniform policies across subsidiaries without shipping hardware. Hybrid models emerge when firms route low-risk assets to cloud workflows but reserve on-premises rigs for classified media. Over time, workload portability between the two hosting modes becomes a purchasing criterion in the data erasure solutions market.

By Device Type: HDD Legacy and Mobile Upswing

Hard disk drives retained 37.42% revenue in 2024, as enterprises continue using high-capacity spinners for archival storage. The data erasure solutions market size for HDD wiping remains substantial because each multi-terabyte unit holds significant regulated data. Parallel wiping innovations such as multi-channel SAS controllers keep throughput high, preserving the appliance value proposition.

Mobile devices, led by corporate smartphones and tablets, are growing at 12.38% CAGR. Wear-leveling on flash chips complicates sanitization, and standard factory resets fail root-level forensic tests. Advanced tools now access secure-enclave chips to overwrite metadata areas previously considered immutable. As bring-your-own-device policies proliferate, verifiable mobile wipe certificates become mandatory off-boarding artifacts, enlarging vendor addressable reach within the data erasure solutions market.

By End-user Industry: BFSI Maturity and Retail Rise

BFSI institutions held 23.78% of 2024 spending, anchored by PCI DSS and SOX rules that prescribe auditable destruction. The data erasure solutions market size within banking will expand steadily as regulators tighten requirements for cloud backup sanitization. Centralized branches allow banks to amortize high-end appliances while leveraging professional services for periodic audits.

Retail and e-commerce’s 12.26% CAGR mirrors explosive omnichannel data flows encompassing point-of-sale logs, loyalty platforms, and third-party analytics. After high-profile privacy breaches, merchants require erase-on-demand workflows that dismantle customer profiles across microservices. Edge store servers and handheld scanners further diversify endpoint types needing coverage, broadening vertical appeal of the data erasure solutions market.

By Organization Size: Enterprise Scale and SME Democratization

Large enterprises accounted for 61.63% revenue in 2024 because volume discounts justify dedicated wipe labs and in-house compliance teams. Integration with IT service management tools automates asset retirement tickets, lowering per-device processing costs and establishing predictable audit cadence. The data erasure solutions market share of enterprises remains high, yet growth moderates relative to smaller peers.

SMEs are accelerating at 13.77% CAGR, driven by MSP-packaged offerings that mask solution complexity behind web dashboards. Pay-per-wipe pricing aligns with operational budgets, while browser-based tutorials reduce skills friction. As local regulators roll out GDPR-style fines, risk calculus shifts, making certified erasure a baseline cyber-hygiene measure rather than discretionary spend. This democratization enlarges the total addressable pool for the data erasure solutions market.

Geography Analysis

North America generated 42.31% of 2024 revenue, anchored by CPRA mandates and a dense ecosystem of ITAD vendors. Multicloud estates across Fortune 500 firms drive steady appliance refresh cycles, while federal contractors adhere to NIST SP 800-88 for procurement clauses. Canada’s consumer privacy reform mirrors U.S. trends, extending regional tailwinds for the data erasure solutions market.

Asia-Pacific posts the fastest 12.86% CAGR as India’s Digital Personal Data Protection Act and China’s PIPL place erasure obligations on local enterprises. Hyperscale investments in Tokyo, Mumbai, and Jakarta create new high-volume decommissioning hubs requiring specialized wipe automation. Smartphone saturation among corporate workforces magnifies mobile erasure demand, underpinning double-digit expansion of the data erasure solutions market size across Asia-Pacific.

Europe maintains consistent growth under GDPR’s mature enforcement model. Sustainability policies urging device refurbish over shredding incentivize certified erasure, especially in Germany and the Nordics. Pan-European cloud initiatives adopt wipe-as-code frameworks to harmonize compliance across sovereign zones. Middle East and Africa and South America trail in adoption but gain momentum as regional privacy statutes tighten, gradually enlarging the global data erasure solutions market.

Competitive Landscape

The vendor arena remains moderately fragmented, with no single supplier exceeding 20% global revenue. Blancco leverages 20+ international certifications to anchor regulated sectors, whereas WhiteCanyon and Certus differentiate via lightweight cloud integration. ITRenew targets hyperscalers with robotic wipe bays capable of 1,200 drives per hour, a niche commanding premium margins.

Emerging entrants emphasize machine-learning verification that scans residual magnetization patterns, promising sub-1-in-10^18 bit recovery probability. Patent filings in quantum-resistant sanitization surged 27% in 2025, foreshadowing new competitive axes. Vendors court channel partners by embedding RESTful APIs that trigger wipes from ServiceNow or Jira tickets, positioning erasure as an ITSM microservice inside the data erasure solutions market.

Strategic moves center on alliance building: Blancco’s 2025 Azure integration embeds wipe hooks inside Cloud Shell, while KLDiscovery’s mobile platform supports iOS 18 and Android 15 enterprise APIs. Garner’s quantum-safe degausser and Stellar’s Southeast Asia expansion reflect focus on adjacent growth levers—technology depth and geographic reach. Collectively, these maneuvers reinforce vendor positioning without consolidating market power, keeping the data erasure solutions industry competitively dynamic.

Data Erasure Solutions Industry Leaders

Blancco Technology Group Ltd.

Kroll Ontrack LLC (KLDiscovery Ontrack)

Stellar Information Technology Pvt. Ltd.

Certus Software AG

ITRenew Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: KLDiscovery Ontrack launched AI-enhanced mobile erasure platform for iOS 18 and Android 15.

- July 2025: Garner Products introduced quantum-resistant degaussing technology for next-gen media.

- June 2025: Stellar Information Technology opened service centers in Singapore and Malaysia to tap Southeast Asian demand.

- May 2025: ITRenew secured USD 75 million Series C to scale hyperscale data-center decommissioning operations.

Global Data Erasure Solutions Market Report Scope

| Software Erasure Tools |

| Hardware-based Erasure Appliances |

| Erasure-as-a-Service (Cloud) |

| Professional and Managed Services |

| On-premises |

| Cloud-hosted |

| Hybrid |

| Hard Disk Drives (HDD) |

| Solid-State Drives (SSD) |

| Mobile Devices (Smartphones and Tablets) |

| Removable Media (USB, SD Cards) |

| Server and Data-Center Drives |

| Virtual Machines / LUNs |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Media and Entertainment |

| Education |

| Transportation and Logistics |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Solution Type | Software Erasure Tools | ||

| Hardware-based Erasure Appliances | |||

| Erasure-as-a-Service (Cloud) | |||

| Professional and Managed Services | |||

| By Deployment Mode | On-premises | ||

| Cloud-hosted | |||

| Hybrid | |||

| By Device / Media Type | Hard Disk Drives (HDD) | ||

| Solid-State Drives (SSD) | |||

| Mobile Devices (Smartphones and Tablets) | |||

| Removable Media (USB, SD Cards) | |||

| Server and Data-Center Drives | |||

| Virtual Machines / LUNs | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| IT and Telecommunications | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Media and Entertainment | |||

| Education | |||

| Transportation and Logistics | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the data erasure solutions market in 2030?

The market is forecast to reach USD 5.59 billion by 2030.

Which deployment model is growing fastest in data erasure?

Cloud-hosted erase-as-a-service solutions are expanding at a 13.64% CAGR.

Why are mobile devices a priority for secure erasure?

Smartphones and tablets store corporate email, app caches, and encrypted partitions that factory resets cannot fully wipe, driving 12.38% CAGR growth for certified mobile sanitization.

How do regulations influence adoption of data erasure platforms?

GDPR, CPRA, PIPL, and India’s DPDP Act impose verifiable deletion mandates, fueling multiyear investment in certified wipe tools.

Which region is expected to grow fastest?

Asia-Pacific leads with a 12.86% CAGR due to rapid digitization and new privacy laws.

What competitive factors differentiate leading vendors?

Certification breadth, API-first architecture, hyperscale throughput, and machine-learning verification increasingly define vendor selection.

Page last updated on: