Data Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

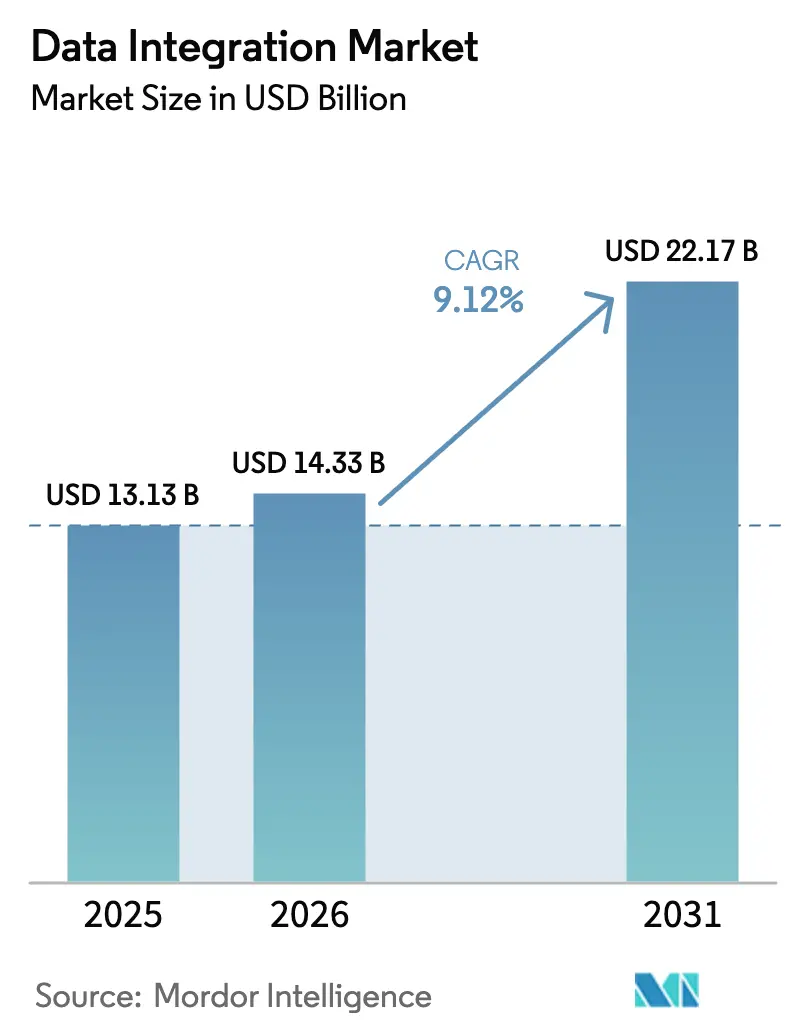

| Market Size (2026) | USD 14.33 Billion |

| Market Size (2031) | USD 22.17 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Integration Market Analysis by Mordor Intelligence

The data integration market size is expected to grow from USD 13.13 billion in 2025 to USD 14.33 billion in 2026 and is forecast to reach USD 22.17 billion by 2031 at 9.12% CAGR over 2026-2031. Momentum came from enterprises replacing batch‐oriented workflows with real-time pipelines to operationalize artificial intelligence, meet transparency rules, and unify sprawling data estates. Cloud-first modernization remained the dominant deployment pattern, yet hybrid architectures gained importance as firms balanced sovereignty rules with elastic scale. Generative-AI initiatives increased demand for governed semantic layers that cut model hallucination rates, while a steady stream of mergers bundled ingestion, transformation, activation, and governance into single platforms. At the same time, skills shortages and rising egress fees tempered adoption speed, compelling many organizations to outsource integration operations.

Key Report Takeaways

- By deployment, cloud models led with 58.74% revenue share in 2025; hybrid-cloud deployments are projected to expand at a 16.62% CAGR to 2031.

- By enterprise size, large enterprises held 55.62% of the data integration market share in 2025, whereas small enterprises are poised to grow at a 15.36% CAGR through 2031.

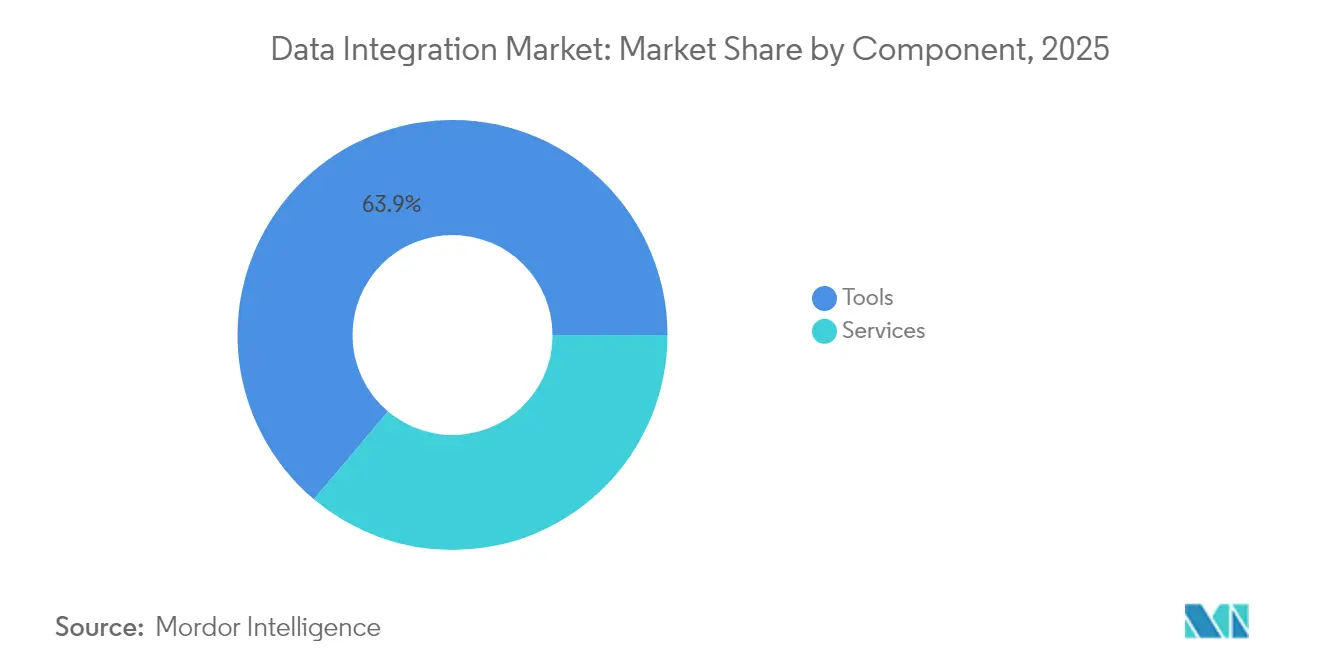

- By component, tools captured 63.85% of the data integration market size in 2025; services are on track to rise at a 14.08% CAGR between 2026-2031.

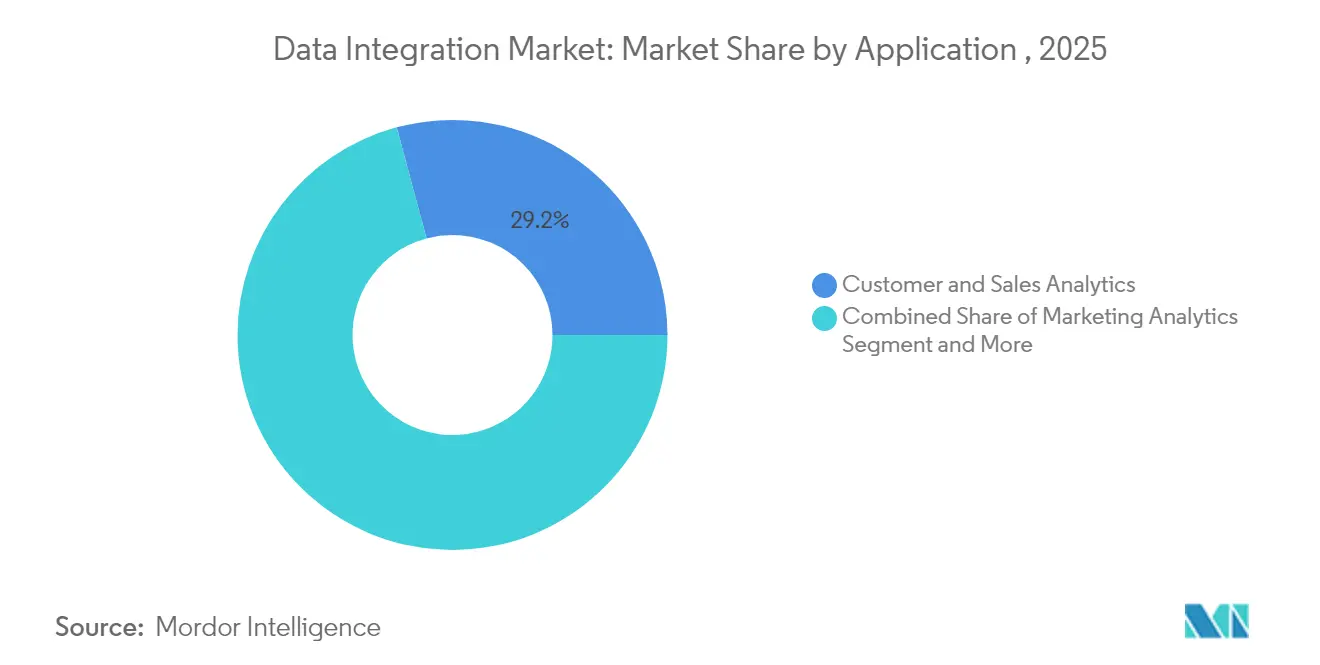

- By application, customer and sales analytics accounted for 29.18% of 2025 revenue, while operations and supply-chain optimization is the fastest-growing segment at 15.74% CAGR.

- By end-user vertical, the Banking, Financial Services, and Insurance sector commanded 24.12% revenue in 2025; healthcare and life sciences is projected to climb at a 18.91% CAGR through 2031.

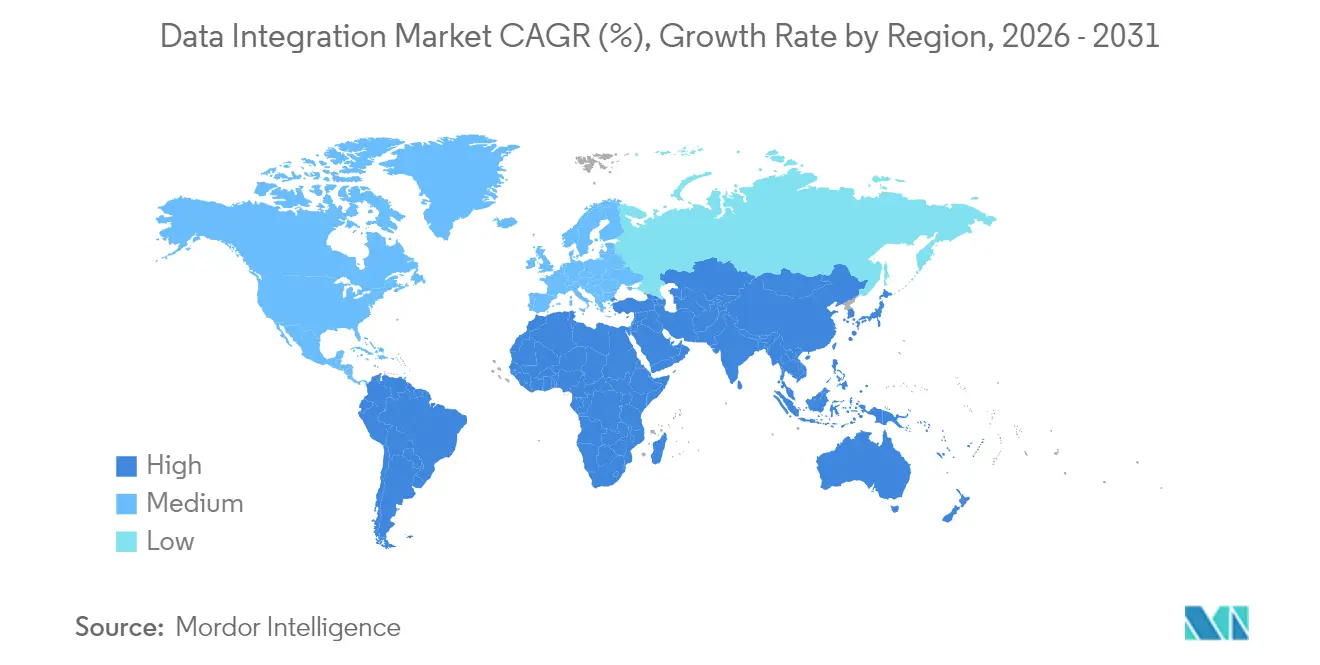

- By geography, North America accounted for 38.35% of 2025 revenue, while Asia-Pacific is the fastest-growing region at 17.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first modernisation of enterprise stacks | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Shift from batch ETL to real-time streaming and CDC | +2.1% | Global, strongest in APAC manufacturing hubs | Short term (≤ 2 years) |

| Self-service, low-code data pipelines for citizen developers | +1.4% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Regulatory push for data lineage and auditability | +1.9% | Europe and North America, spreading globally | Short term (≤ 2 years) |

| Emergence of generative-AI-ready semantic layers | +1.8% | Global tech-forward enterprises | Long term (≥ 4 years) |

| Edge and in-sensor analytics | +1.2% | APAC manufacturing, North America IoT | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first modernisation of enterprise stacks

By 2025, most Fortune 100 firms had shifted integration workloads into subscription cloud services, cutting infrastructure costs and simplifying upgrades. [1]Informatica Corp., “Introduction to Informatica,” informatica.com Cloud R&D investments exceeding USD 1 billion spurred zero-ETL patterns that read schemas on demand, freeing teams from rigid pre-defined transformations. Case studies such as HCLTech’s engagement with Unilever showed 30% infrastructure savings after embracing cloud-native integration. Vendors converged on lakehouse designs that unite warehouses and data lakes, with Iceberg and Delta formats enabling open file storage across platforms. Managed lake services further accelerated adoption by automating table maintenance and format conversion for more than 500 sources. [2]Fivetran Inc., “Fivetran Expands Snowflake Partnership,” fivetran.com

Shift from batch ETL to real-time streaming and CDC

Streaming reverse ETL tools launched in 2024 synchronised data warehouse tables to operational systems within seconds, supporting live customer engagement. Financial institutions integrated CDC pipelines that cut fraud detection windows from hours to seconds. Manufacturing firms applied IoT streams to predict machine failure, reducing unplanned downtime by 40%. [3]IBM, “Real-Time Analytics on IoT Data,” ibm.comZero-ETL concepts emerged, moving raw data directly between stores while applying transformations at query time, slashing latency and operating cost. Cloud platforms simplified orchestration via declarative streaming services such as Dynamic Tables and Delta Live Tables.

Regulatory push for data lineage and auditability

The Digital Operational Resilience Act, effective January 2025, required roughly 22,000 EU financial entities to maintain real-time lineage and incident reporting or risk penalties up to 2% of turnover. In the United States, the 21st Century Cures Act banned information blocking and mandated Fast Healthcare Interoperability Resources APIs for patient data access. Hospitals faced reductions in Medicare incentives when failing to comply, prompting accelerated investments in governed integration layers. Vendors responded with automated data catalogs that map lineage end-to-end and embed audit trails into pipeline metadata. As overlapping rules proliferated, enterprises adopted semantic layers to centralize definitions and streamline compliance reporting.

Emergence of generative-AI-ready semantic data layers

Semantic layers evolved into AI alignment engines that anchored large-language-model outputs on governed tables, cutting hallucination rates by two-thirds. Model-driven definitions in LookML allowed deterministic KPI calculations to be reused across dashboards and chat interfaces. Progress Software embedded generative AI to auto-build ontologies and surface relationships hidden in unstructured data. Context Layer innovations processed trillions of rows while adapting queries to user intent, expanding the scope of conversational analytics. Together, these advances made semantic governance a prerequisite for scalable enterprise AI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage in advanced integration architectures | −1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Escalating cloud egress and data-movement costs | −1.2% | Global, highest in multi-cloud setups | Medium term (2-4 years) |

| Data-sovereignty restrictions splintering pipelines | −1.5% | APAC, Europe, emerging elsewhere | Long term (≥ 4 years) |

| Vendor lock-in risk from proprietary iPaaS | −0.9% | Global enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent shortage in advanced integration architectures

In 2025, 76% of enterprises reported severe shortages in AI and data engineering talent, delaying deployments and inflating consulting spend. Security, networking, and data skills each showed gaps exceeding 35%, forcing CIOs to fund upskilling programs and managed services partnerships. Surveys projected the talent deficit could drain USD 5.5 trillion from global output by 2026. European manufacturers highlighted automation and green-tech skills as especially scarce, leading to project backlogs across mid-sized plants. These constraints slowed the rollout of real-time streaming, semantic layers, and edge pipelines despite clear ROI potential.

Data-sovereignty restrictions splintering multi-region pipelines

China’s Personal Information Protection Law compelled critical infrastructure operators to store data locally and clear cross-border transfers through security reviews, driving regionalized integration architectures. Across Asia-Pacific, privacy regulations grew 25%, with Thailand, Indonesia, and Sri Lanka issuing comprehensive statutes MorrisonFoerster. Europe’s GDPR continued to influence global policy, requiring privacy-by-design controls and tight legal bases for transfers. Enterprises responded by standing up localized processing nodes and adopting hybrid storage models to balance sovereignty with analytics scale. Multi-cloud egress fees added cost pressure as data was shuttled among compliant zones, reinforcing the need for intelligent workload placement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale Faster Than Tools

Services revenue expanded at a 14.08% CAGR through 2031 as organizations sought expert guidance on cloud migrations, streaming architectures, and compliance frameworks. The tools category still held 63.85% of the data integration market in 2025, reflecting entrenched ETL, CDC, and virtualisation platforms. Professional services surged around semantic layer rollouts and generative-AI integration, where tailored governance and ethical design were vital. Managed services gained popularity for 24/7 monitoring and automated optimisation of multi-cloud pipelines.

Within tools, ETL/ELT suites remained staple investments for batch workloads, while CDC engines gained momentum for instant analytics. Streaming platforms became critical in IoT scenarios, and data virtualisation rose alongside mesh architectures that decouple access from storage. Data quality and master data management tools found renewed relevance as AI models demanded trusted inputs. The widening skills gap further amplified demand for service providers who can orchestrate these diverse products into cohesive solutions.

By Deployment: Hybrid-Cloud Ascends

Hybrid configurations recorded a 16.62% CAGR, reflecting the trade-off between sovereignty and flexibility that dominates data strategy decisions. Public cloud retained the largest overall share because hyperscalers offered elastic scale and a rich ecosystem of native services. Private clouds persisted in highly regulated environments such as finance and healthcare, where control over hardware and network configurations remained essential.

On-premise estates shrank but did not disappear, supporting legacy mainframes and latency-sensitive workloads. Edge nodes emerged as micro-integration points, processing sensor data locally before forwarding summaries to central stores. The data integration market size for hybrid-cloud deployments is forecast to expand steadily as more firms adopt mesh patterns that federate domain teams while sustaining centralized governance. Adoption accelerated as platforms introduced single control planes spanning warehouses, lakes, and edge clusters.

By Enterprise Size: Democratization Takes Hold

Small enterprises posted a 15.36% CAGR as low-code interfaces and pay-as-you-go pricing removed historical entry barriers. Citizen developers built pipelines without deep scripting skills, enabling real-time insights previously limited to large corporates. Medium enterprises leveraged the same tools to scale analytics programs and compete on customer experience.

Large enterprises, while holding 55.62% revenue in 2025, shifted focus to optimizing complex estates rather than rapid expansion. They adopted AI-driven observability to reduce pipeline downtime and implemented strict data contracts across thousands of sources. The data integration industry saw micro-enterprises begin trials using hosted ingestion services bundled with SaaS applications, signalling future volume growth at the long tail of the market.

By Application: Supply-Chain Optimisation Surges

Operations and supply-chain optimisation achieved the highest growth rate at 15.74% CAGR as manufacturers and retailers required end-to-end visibility. IoT sensors streamed machine metrics, enabling predictive maintenance and inventory balancing in near real time. Customer and sales analytics remained dominant at 29.18% share because personalised engagement and revenue acceleration stayed top priorities.

Marketing analytics advanced on the back of cross-channel attribution models, while finance teams integrated real-time feeds to satisfy stringent reporting deadlines. HR functions adopted people analytics to address turnover and DEI goals, and R&D groups unified datasets to shorten product cycles. The data integration market size for operations-focused workloads is expected to widen as autonomous supply chains mature, linking factory, logistics, and storefront data in continuous loops.

By End-User Vertical: Healthcare Accelerates

Healthcare and life sciences outpaced all sectors with a 18.91% CAGR, driven by Fast Healthcare Interoperability Resources mandates that forced real-time patient record exchange. Providers integrated disparate electronic health record systems, labs, and wearable feeds to deliver coordinated care and meet information-blocking rules.

Banking, Financial Services, and Insurance retained a 24.12% share because anti-fraud, regulatory reporting, and customer personalisation demanded mature pipelines. Manufacturing advanced through Industry 4.0 programs, while retail invested in omnichannel platforms that blend online and point-of-sale data. Government, energy, and media all stepped up adoption to modernise services, monitor critical infrastructure, and personalise content, respectively.

Geography Analysis

North America held 38.35% of global revenue in 2025 thanks to early cloud adoption, robust venture funding, and a dense ecosystem of system integrators. Federal infrastructure programs, including a USD 65 billion grid modernisation package, drove additional demand for real-time energy data integration. Canada mirrored these patterns, investing in healthcare and financial services modernization while navigating cross-border compliance.

Asia-Pacific delivered the fastest growth at an 17.78% CAGR, fuelled by hyperscale data-center rollouts and large public-sector digitalisation projects. China earmarked USD 442 billion for smart-grid upgrades that require streaming data platforms, while India allocated INR 3.03 trillion (USD 0.012 trillion) to infrastructure that embeds analytics at its core. Japan’s USD 155 billion in digital infrastructure budgets further expanded the addressable base for the data integration market. Local data-localisation laws, however, encouraged hybrid architectures that process data in-country before selective aggregation.

Europe showed solid momentum despite privacy rules. The European Commission planned EUR 584 billion (USD 669.87 billion) in smart-grid investments by 2030, spurring integration projects that combine renewable generation data with consumer demand response. DORA compliance spending escalated within banking, while GDPR-aligned edge solutions let enterprises analyse data locally. Overall, the data integration market size for the region is projected to climb steadily as sovereign clouds and open standards mitigate regulatory headwinds.

Competitive Landscape

The market stayed moderately fragmented. Informatica led with a 14.1% share, leveraging its Intelligent Data Management Cloud to serve more than 80% of Fortune 100 firms. Consolidation accelerated; Fivetran bought Census to merge ingestion and activation, and Snowflake added Crunchy Data for PostgreSQL support, signalling vendor quests for end-to-end stacks.

Technology convergence blurred boundaries between warehouse, lake, and mesh solutions. Cloud data stores adopted vectorized engines and open table formats, while integration specialists embedded generative AI to automate mapping and error resolution. Niche entrants carved positions in reverse ETL, edge analytics, and semantic governance, appealing to buyers with targeted pain points.

Strategic alliances grew in importance. Teradata partnered with Fivetran on a native connector that moves data from 700-plus sources into VantageCloud for AI workloads. Vendors also courted hyperscalers’ marketplaces to simplify procurement and reach mid-market buyers. Competitive intensity remained high as pricing pressure, open-source tools, and skills shortages forced suppliers to differentiate through service quality, security certifications, and ecosystem breadth.

Data Integration Industry Leaders

IBM Corporation

Microsoft Corporation

Informatica Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake finalized its purchase of Crunchy Data, adding enterprise PostgreSQL to its AI Data Cloud.

- May 2025: Fivetran agreed to acquire Census to unify ingestion and reverse ETL capabilities.

- May 2025: Teradata and Fivetran announced a destination connector for VantageCloud, due to launch in Jun 2025.

- March 2025: Fivetran expanded Microsoft Fabric integration with 700+ connectors for Iceberg and Delta support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data integration market as all software tools and platforms-on-premise, cloud, or hybrid-that move, transform, virtualize, synchronize, or stream data across heterogeneous sources so it can be queried as a single, governed asset. The scope spans extraction-transformation-load (ETL/ELT) suites, integration-platform-as-a-service (iPaaS), real-time change-data-capture pipelines, data virtualization layers, and associated maintenance subscriptions.

Scope exclusion: one-off custom scripting or staff-augmentation services without an accompanying licensed platform are not counted.

Segmentation Overview

- By Component

- Tools

- ETL and ELT Platforms

- Data Replication and CDC

- Data Virtualisation

- Streaming Integration

- Data Quality and MDM Tools

- Services

- Professional Services

- Managed Services

- Tools

- By Deployment

- Cloud

- Public Cloud

- Private Cloud

- Hybrid Cloud

- On-Premise

- Cloud

- By Enterprise Size

- Micro Enterprises (1-49)

- Small Enterprises (50-249)

- Medium Enterprises (250-999)

- Large Enterprises (1,000+)

- By Application

- Customer and Sales Analytics

- Operations and Supply-chain Optimisation

- Marketing Analytics

- Finance and Risk Management

- Human Resources Analytics

- Product and RandD Data Integration

- Others

- By End-user Vertical

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Government and Defense

- Energy and Utilities

- Media and Entertainment

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Benelux

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with integration architects, data engineering leads, and channel partners across North America, Europe, and fast-growing Asia Pacific. Interviews explored average contract values, migration timelines, and emerging AI-driven workloads, allowing us to challenge desk assumptions and fine-tune price-volume curves before final triangulation.

Desk Research

We start with public datasets such as the US Bureau of Labor Statistics ICT spending tables, Eurostat Digital Economy indicators, and China's MIIT software revenue filings, which anchor regional software outlays. Trade associations like the Cloud Native Computing Foundation and the Open Data Institute provide technology adoption ratios, while patent analytics from Questel hint at innovation pacing. Company 10-Ks, investor decks, and voluntary ESG filings sharpen vendor-level splits, and news flows parsed in Dow Jones Factiva flag material events. These are illustrative; numerous additional open sources supported data gathering and validation.

Market-Sizing & Forecasting

A top-down model scales national software-spend baselines by verified penetration rates for integration platforms, then aligns outputs with bottom-up checks derived from sampled vendor revenue, typical seat counts, and average selling prices. Key variables include cloud workload share, volume of real-time pipelines per enterprise, data-center egress pricing trends, regulatory localization rules, and merger activity among tool vendors. Forecasts employ multivariate regression blended with scenario analysis to capture sensitivity around AI adoption and edge compute growth. Assumption gaps in smaller geographies are bridged by regional analogs validated through expert calls.

Data Validation & Update Cycle

Outputs undergo variance tests versus independent indicators such as iPaaS billing data and hyperscale marketplace listings. Senior reviewers sign off only after anomalies are resolved; reports refresh annually, with interim pulses when material events, large acquisitions, and new regulation shift baselines.

Why Mordor's Data Integration Baseline Commands Reliability

Published estimates often diverge because firms choose different component mixes, base years, and currency conversions.

Key gap drivers include some publishers bundling data quality or enterprise service bus software, others projecting from vendor guidance without end-user spend rebasing, and several using 2024 baselines rolled forward by constant CAGR, whereas Mordor rebuilds 2025 from fresh spend signals and real contracts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.13 B (2025) | Mordor Intelligence | |

| USD 17.58 B (2025) | Global Consultancy A | Wider scope adds data quality suites and uses unadjusted vendor revenue |

| USD 15.18 B (2024) | Industry Journal B | Base year differs and extrapolates iPaaS totals with uniform CAGR |

The comparison shows that Mordor's disciplined scope selection, annual refresh, and dual-path modeling yield a balanced, transparent baseline that decision-makers can trace to verifiable variables, avoiding over-inflated totals while still capturing transformational growth.

Key Questions Answered in the Report

What was the global data integration market size in 2026?

The market reached USD 14.33 billion in 2026.

Which deployment model is growing fastest?

Hybrid-cloud deployments are forecast to rise at a 16.62% CAGR between 2026-2031.

Which application area will see the strongest growth through 2031?

Operations and supply-chain optimisation is expected to lead with a 15.74% CAGR.

Why is healthcare adopting data integration so rapidly?

The 21st Century Cures Act mandates real-time interoperability, pushing healthcare and life sciences toward a 18.91% CAGR.

How are regulations like DORA influencing purchasing decisions?

Financial firms face real-time lineage and incident-reporting requirements under DORA, accelerating investment in governed integration platforms.

What is driving consolidation among integration vendors?

Providers are acquiring complementary capabilities such as reverse ETL and database support to deliver end-to-end data movement ecosystems and stay competitive.

Page last updated on: