Personal And Entry Level Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

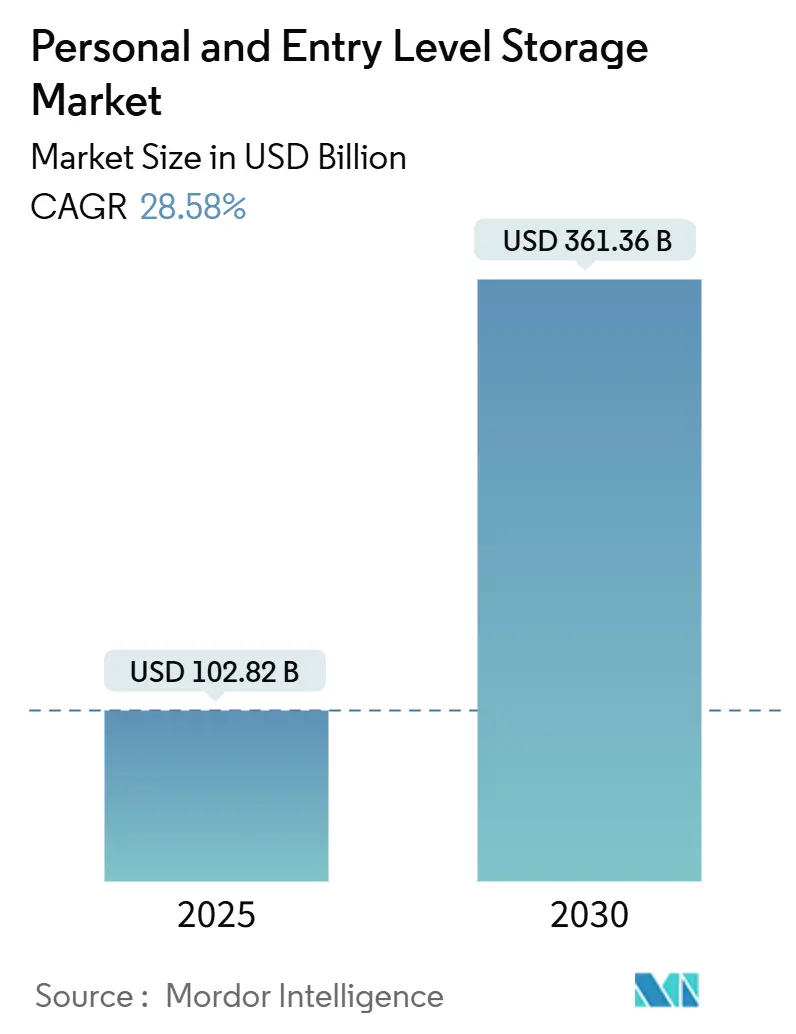

| Market Size (2025) | USD 102.82 Billion |

| Market Size (2030) | USD 361.36 Billion |

| Growth Rate (2025 - 2030) | 28.58% CAGR |

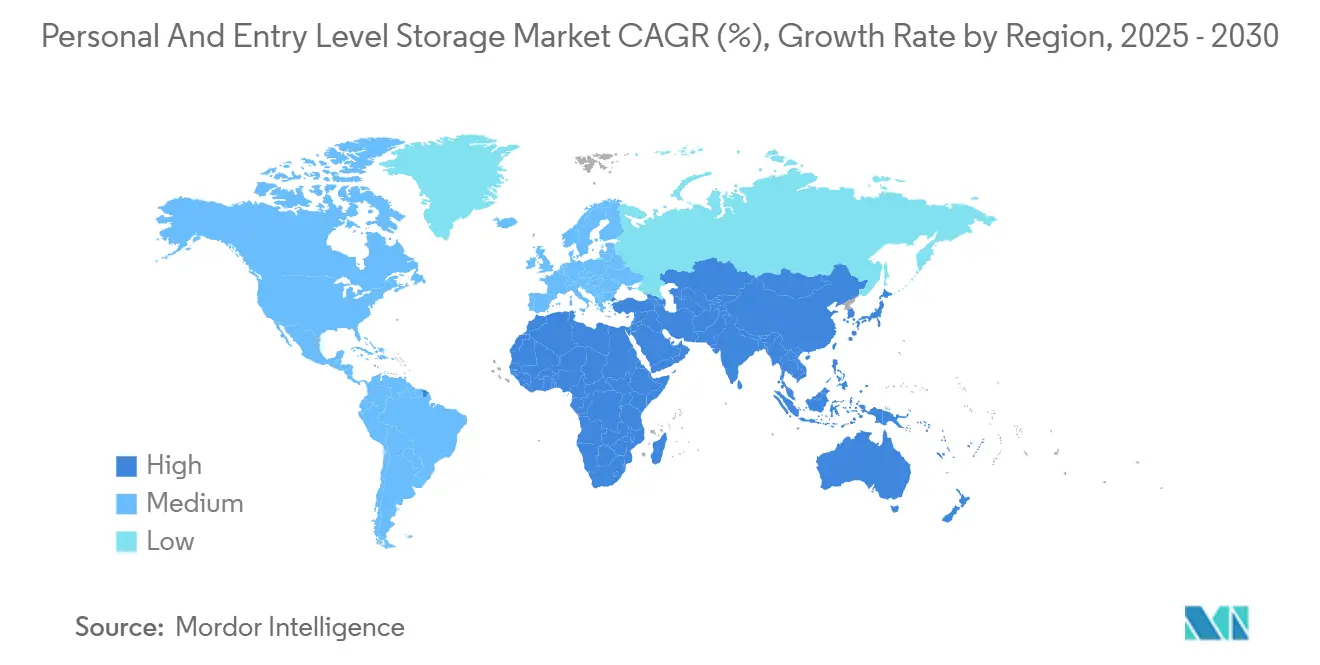

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

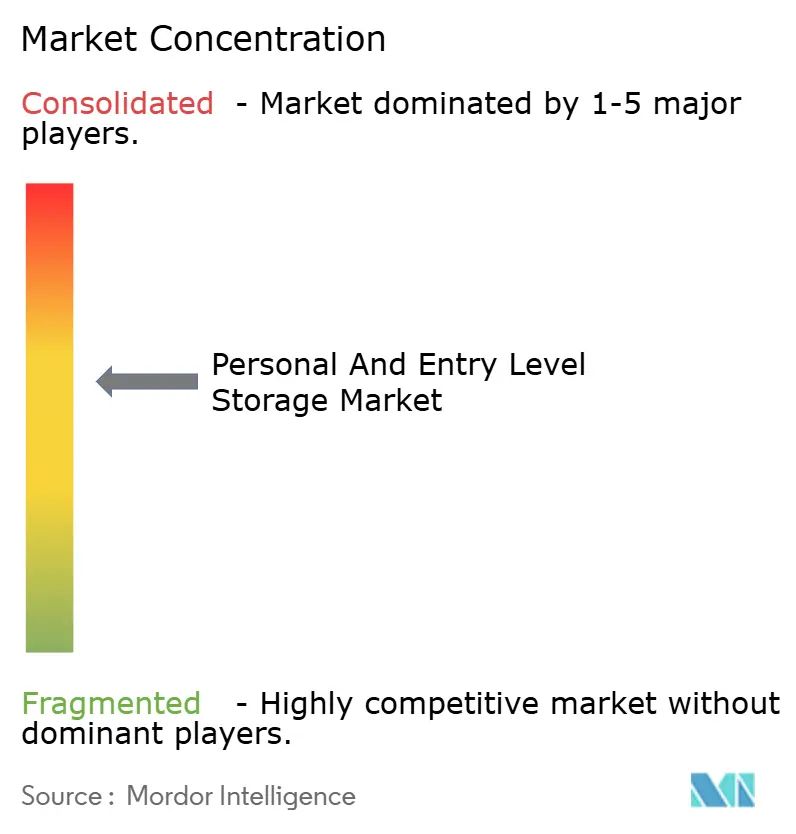

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal And Entry Level Storage Market Analysis by Mordor Intelligence

The personal and entry-level storage market was valued at USD 102.82 billion in 2025 and is forecast to reach USD 361.36 billion by 2030, translating into a robust 28.58% CAGR and underscoring a decisive shift toward local data control, security, and sovereignty concerns. Solid-state drive (SSD) prices continue to fall, making high-performance flash capacity available to the mass market, while Thunderbolt 5 and USB4 interfaces elevate portable storage throughput to workstation-class levels. Simultaneously, hybrid work patterns are amplifying demand for multi-bay NAS devices that combine on-premise speed with cloud synchronization. Additionally, smart-home integration is transforming storage appliances into digital lifestyle hubs. Emerging regional data-localization mandates in Europe and Asia-Pacific strengthen the appeal of keeping assets physically close, and resilient NAND-flash supply chains have restored pricing predictability, encouraging aggressive product launches.

Key Report Takeaways

- By product type, solid-state drives led with a 41.37% revenue share in 2024; network-attached storage is projected to expand at a 29.11% CAGR through 2030.

- By storage medium, SSD technology accounted for 47.89% of the personal and entry-level storage market size in 2024, while cloud-integrated personal storage showed the fastest growth at a 29.19% CAGR.

- By capacity range, the 100 GB-1 TB segment captured 45.92% of the personal and entry-level storage market share in 2024; capacities above 10 TB are projected to advance at a 29.07% CAGR to 2030.

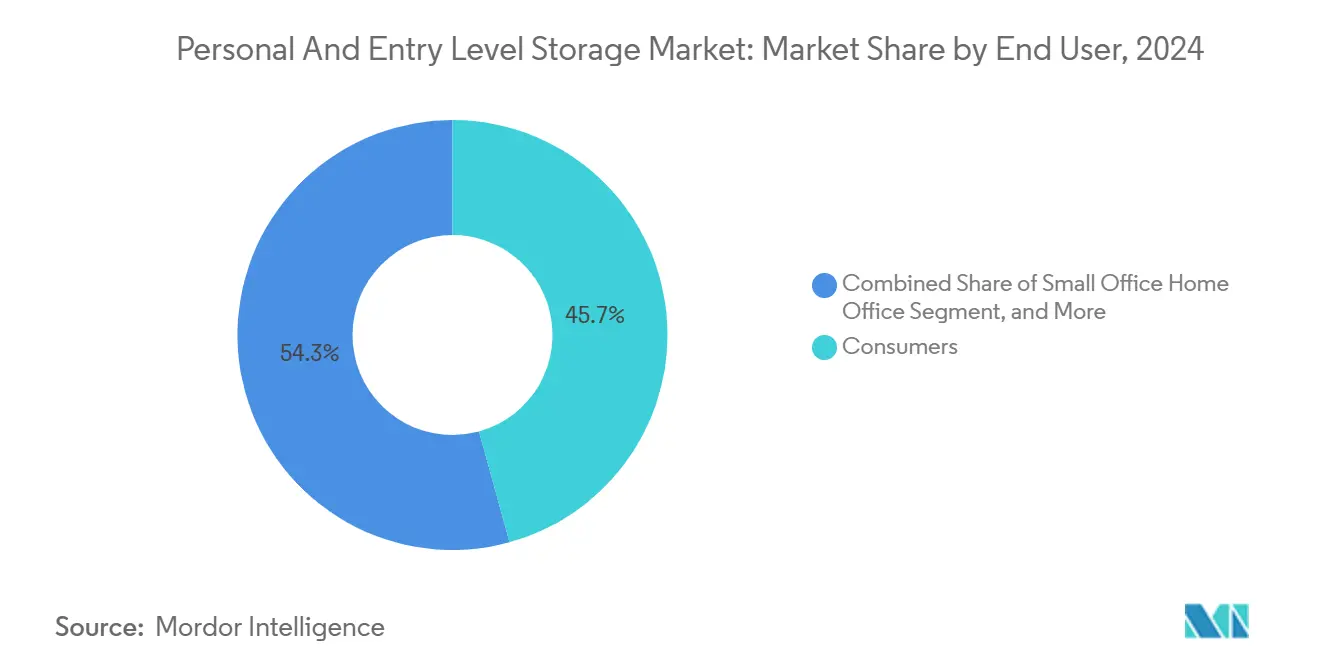

- By end user, consumers accounted for 45.73% of the overall revenue in 2024; demand for small office and home office solutions is rising at a 29.33% CAGR.

- By distribution channel, online retail dominated with a 54.91% share in 2024 and is projected to grow at a 29.22% annual rate to 2030.

- By geography, the Asia-Pacific region retained its leadership position with a 33.16% regional share in 2024, while the Middle East is forecast to post the fastest growth rate of 28.89% CAGR through 2030.

Global Personal And Entry Level Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of high-resolution consumer content creation | +7.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Declining cost per gigabyte of SSDs | +6.8% | Global | Short term (≤ 2 years) |

| Rising remote work and home office setups | +5.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of personal NAS with smart-home ecosystems | +4.1% | North America and Europe, urban Asia | Long term (≥ 4 years) |

| Regulatory push for local data-storage compliance in SMEs | +3.2% | Europe and Asia-Pacific, selective North America | Long term (≥ 4 years) |

| Under-penetrated emerging markets with growing middle class | +2.9% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of High-Resolution Consumer Content Creation

Creators now capture 8K video on mainstream devices, generating individual project files that regularly exceed 10 TB. Portable SSDs, such as LaCie’s Rugged SSD Pro5, deliver 6,700 MB/s read speeds, allowing editors to work directly off external media without relying on proxy workflows.[1]Andrew O’Hara, “LaCie leverages Thunderbolt 5 with Rugged SSD Pro5 for creative pros,” AppleInsider, appleinsider.com The growing use of AI-assisted color grading and object tracking further multiplies compute-adjacent storage needs, prompting professionals and enthusiasts alike to invest in multi-bay NAS units for on-site backup and shared editing.

Declining Cost per Gigabyte of SSDs

QLC NAND now undercuts triple-level cell equivalents by nearly 25%, widening the addressable price points for flash-based products.[2]Craig Hale, “16 TB portable SSDs pipeline as native USB4 controller debuts,” TechRadar Pro, techradar.com Western Digital’s strategic flash carve-out and renewed focus on HDDs improved fab efficiency, while gains in 200-plus-layer 3D NAND drive density sustain the downward price curve. Native USB4 controllers from Phison enable 16TB pocket drives with 4,000MB/s throughput, extending flash economics into archival-class capacities

Rising Remote Work and Home Office Setups

Distributed teams require local redundancy when bandwidth drops, so Thunderbolt 4 NASbooks such as QNAP’s TBS-h574TX offer hot-swappable M.2 SSD slots and hybrid-cloud sync for seamless off-site collaboration. Mesh storage networks spanning employee homes reduce latency for large design files and safeguard compliance-sensitive data in accordance with corporate policy.

Integration of Personal NAS with Smart-Home Ecosystems

Vendors embed Matter and Thread radios inside NAS devices, turning them into command centers for cameras, sensors, and media servers. Edge AI modules perform local facial recognition and energy usage prediction, reducing cloud calls and enhancing privacy. Bundled automation dashboards raise average selling prices and position storage as a cornerstone of the connected-home stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of cloud-storage subscriptions | -4.8% | Global, strong in North America and Europe | Short term (≤ 2 years) |

| Cybersecurity concerns over consumer-managed devices | -3.1% | Global, heightened in Europe and Asia-Pacific | Medium term (2-4 years) |

| Limited consumer technical proficiency | -2.4% | Global | Medium term (2-4 years) |

| Volatility in NAND flash supply pricing | -1.6% | Asia-Pacific manufacture-centric regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Cloud-Storage Subscriptions

Major platforms bundle terabytes of space with office suites, persuading casual users to offload data into SaaS lockers. Wasabi’s 2024 survey showed that 85% of enterprises ranked cloud as their primary infrastructure, squeezing entry-level hardware volumes. Hybrid-cloud gateways mitigate the threat by caching frequently accessed files locally, yet the convenience gap continues to pressure standalone drive sales.

Cybersecurity Concerns over Consumer-Managed Devices

Persistent ransomware campaigns exploited unpatched NAS firmware throughout 2024, prompting repeated security bulletins from QNAP and D-Link. Europe’s Cyber Resilience Act mandates five-year support and secure-by-default settings from December 2027, which will raise development costs for vendors.[3]European Commission, “Cyber Resilience Act documentation,” europa.eu Vendors adopting ISO/IEC 27040:2024 frameworks gain a compliance edge, but must simplify patch delivery for non-technical owners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: SSDs Outperform While NAS Surges

Solid-state drives generated 41.37% of revenue in 2024 as consumers shifted toward silent, shock-resistant flash storage. The personal and entry-level storage market size for SSDs is forecast to grow at a 22% CAGR through 2030 as 200-plus-layer stacks and QLC architectures reduce costs. In parallel, network-attached storage units post the fastest 29.11% CAGR, propelled by hybrid-work backup and smart-home automation tie-ins that extend beyond simple file sharing. External HDDs remain favored for their low cost, but spinning media is losing premium shelf space, especially in North America and Japan. LaCie’s Rugged SSD Pro5 and OWC’s Envoy Ultra showcase how Thunderbolt 5 elevates portable performance to workstation levels, narrowing the gap between internal and external drives.

The segment’s long-term outlook hinges on interface standardization and AI-embedded value adds. Vendors embed predictive maintenance in controller firmware, alerting owners before flash wear escalates. NAS suppliers integrate app stores, enabling surveillance, media streaming, and virtualization on a single chassis. Competition thus pivots from raw capacity toward ecosystem breadth, positioning software-rich brands such as Synology and QNAP to capture outsized value at the expense of commodity drive makers.

By Storage Medium: Flash Memory Widens the Lead

SSDs accounted for a 47.89% share in 2024, and continuing price erosion is expected to lift that figure above 55% by 2027. The personal and entry-level storage market share for SSD-centric devices is expanding fastest where internet bandwidth is costly, making local speed essential for 4K and 8K editing. Cloud-integrated personal storage is the medium to watch, charting a 29.19% CAGR as consumers seek the safety of off-site redundancy without sacrificing on-premise responsiveness. HDD technology still dominates capacities above 20 TB, but flash is encroaching as heat-assisted magnetic recording development slows.

Future competition will revolve around controller innovation. Phison’s native USB4 silicon already halves latency compared to USB3 and provides up to 16 TB per stick, while Micron’s 232-layer flash reduces die size. Optical disc shipments continue to decline, primarily serving niche archival workloads. Experimental DNA and holographic technologies remain laboratory curiosities but underscore the industry’s drive to transcend the limitations of electron storage.

By Capacity Range: Mid-Tier Balances Cost and Utility

Drives between 100 GB and 1 TB captured 45.92% of purchases in 2024, offering ample headroom for family photo libraries and office documents at price points below USD 120 per terabyte. However, units larger than 10 TB will deliver the steepest 29.07% CAGR because professional 8K footage and VR assets push single-project footprints well into multi-terabyte territory. The personal and entry-level storage market size for the >10 TB band is expected to benefit from declining enterprise-grade NAND costs and the adoption of multi-controller desktop DAS enclosures.

Consumers steadily migrate upward in capacity as smartphone sensors reach 100 MP and lossless audio archives expand. Manufacturers bundle backup software and ransomware protection, nudging buyers toward higher SKUs. Entry-level 256 GB flash still serves travel backup, but the value proposition weakens as higher tiers drop below USD 100. Premium models, such as LaCie’s 4 TB Rugged SSD, illustrate a willingness to pay for portable, shock-proof terabytes when professional workflows depend on them.

By End User: Hybrid Work Reshapes Demand

Individuals accounted for the largest 45.73% slice in 2024, but the small office home office cohort is accelerating at a 29.33% CAGR as remote staff replicate enterprise resiliency in spare bedrooms. The personal and entry-level storage market size, which is often attached to small studios and home agencies, benefits from tax-deductible hardware upgrades and a heightened need for version-controlled collaboration. Small and medium enterprises search for cost-effective substitutes to on-premise SANs, gravitating toward four-bay NAS towers with 10 GbE.

Photography and videography professionals form a lucrative niche; a single 8K documentary can consume up to 8 TB of storage space before post-production, creating repeat purchase cycles for high-capacity SSDs with sustained write capabilities. The education and government verticals pursue compliance-ready appliances that feature AES-256 encryption and audit logs. The lines between segments blur as creator-class features permeate consumer gadgets, lifting the average revenue per unit across the board.

By Distribution Channel: E-Commerce Captures the Upsell

Online retail controlled 54.91% of 2024 shipments and is on track for a 29.22% annual increase as customers rely on peer reviews and comparison tools when purchasing complex storage. Brick-and-mortar outlets remain relevant for urgent replacements and hands-on demos, yet foot traffic continues to migrate online. Direct sales through brand e-stores are rising among NAS vendors who bundle extended warranties and remote setup services. System integrators and value-added resellers prosper in the prosumer and SME space, tailoring RAID topology and off-site replication packages.

Digital storefront dominance encourages subscription add-ons. Vendors upsell cloud backup vouchers and AI photo-tagging services at checkout, padding recurring revenue and deepening customer lock-in. Flash-deal campaigns effectively move aging HDD inventory, while early-access programs let enthusiasts beta-test next-gen interfaces like Thunderbolt 5 before broad release.

Geography Analysis

The Asia-Pacific region led the personal and entry-level storage market with a 33.16% regional market share in 2024, reflecting strong government digital sovereignty mandates and a rapidly expanding middle class. China’s localization rules, India’s smartphone surge, and South Korea’s gaming ecosystem all funnel volume toward local drive manufacturers, while cost advantages in semiconductor fabrication support aggressive pricing. The personal and entry-level storage market size generated in this region also benefits from the domestic assembly of NAND flash and controller chips, which cushions currency volatility and shortens lead times. Mature early-adopter pockets in Japan and Australia continue to absorb premium Thunderbolt 5 and USB4 products despite macroeconomic caution. Geopolitical tensions and export-control policies, however, keep supply-chain managers alert to potential component disruptions.

North America ranks second, driven by Hollywood’s demand for 8K production pipelines and widespread gigabit broadband, which favors external SSDs with workstation-class throughput. United States buyers alone account for nearly half of the region’s turnover, while Canada and Mexico capture spillover growth as nearshoring pulls inventory closer to end markets. The Middle East is projected to post the fastest 28.89% CAGR through 2030, driven by hyperscale data center buildouts in the United Arab Emirates and Saudi Arabia, which create spillover demand for edge-tier backup devices. Government digital-transformation grants and consumer appetite for high-resolution streaming further accelerate unit shipments across Gulf Cooperation Council nations.

Europe maintains a steady trajectory as GDPR and sector-specific privacy statutes push small and medium-sized enterprises toward on-premises retention, lifting the region’s share of the personal and entry-level storage market size for security-sensitive verticals. Germany’s engineering sector and France’s creative industries invest in Thunderbolt 5 arrays for CAD and video rendering, while the United Kingdom sustains demand anchored by financial services compliance. The forthcoming EU Cyber Resilience Act, which mandates that consumer devices be secure by default starting in December 2027, is already influencing product design roadmaps. In Europe and South America, advances are made from a smaller base. Brazil drives regional adoption, whereas Argentina’s economic headwinds temper premium uptake and keep average selling prices below global norms.

Competitive Landscape

The personal and entry-level storage market remains moderately fragmented, with the top five vendors controlling approximately 55% of global revenue. Western Digital and Seagate protect their hard-drive cash flows while expanding NVMe and portable SSD lines to hedge against declining HDD volumes. Synology and QNAP secure premium pricing by bundling proprietary operating systems, application stores, and long-term firmware support, which narrows the gap between consumer and enterprise features. LaCie, OWC, and other interface leaders are temporarily differentiating themselves through Thunderbolt 5 designs that increase external-drive throughput above 6 GB/s; however, chipset commoditization is expected to erode this speed advantage within two years. Aggregate vendor concentration is therefore stable, allowing smaller specialists to win share through targeted innovation and channel agility.

Hardware commoditization is steering competition toward software-defined value. Synology integrates Hyper Backup, Active Backup, and surveillance suites that lock users into multi-year upgrade paths, while QNAP leverages QuTS hero to deliver ZFS-based data integrity for prosumer workloads. UGREEN introduces AI-powered photo categorization and predictive-failure alerts to its consumer NAS portfolio, leveraging machine-learning capabilities to deliver tangible user benefits. Early adopters of native USB4 controllers, such as Phison partners, introduce 16 TB pocket drives to the market, prompting rivals to accelerate updates to their controller roadmaps. Price competition persists at entry-level capacities, but vendors offset margin pressure by upselling cloud backup subscriptions and extended warranty bundles through online storefronts.

Security and compliance now rank alongside performance in purchase criteria. Vendors racing to achieve ISO/IEC 27040 alignment highlight encrypted boot, secure element key storage, and five-year firmware update guarantees on product pages. The upcoming EU Cyber Resilience Act further amplifies differentiation for brands that can certify secure-by-default configurations in advance of the 2027 deadline. Hybrid-cloud orchestration is another battleground: seamless backups to Wasabi, Backblaze, or S3 keep locally stored data synchronized without the need for manual scripts, appealing to small office owners with limited IT staff. White-space opportunities remain in ruggedized industrial IoT storage and edge analytics appliances, while long-horizon technologies such as DNA-encoded archives and quantum memory continue to reside in research labs, posing minimal commercial threats before 2030.

Personal And Entry Level Storage Industry Leaders

Western Digital Corporation

Seagate Technology Holdings plc

Synology Inc.

QNAP Systems Inc.

Buffalo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: LaCie introduced the Rugged SSD Pro5 featuring Thunderbolt 5 connectivity, 6,700 MB/s read speeds, and 2 TB and 4 TB capacities.

- January 2025: QNAP rolled out the TBS-h574TX Thunderbolt 4 all-flash NASbook, combining hot-swappable M.2 SSD slots with 13th-generation Intel Core processors for portable, high-performance workflows.

- January 2025: Oyen Digital launched the U34 Bolt 8 TB USB4 portable SSD, offering sustained 2,800 MB/s transfers and MIL-STD-810F rugged construction.

- January 2025: LaCie’s Rugged SSD Pro5 entered retail channels as the industry’s first mainstream portable drive built on the Thunderbolt 5 interface.

Global Personal And Entry Level Storage Market Report Scope

| External Hard Disk Drives |

| Solid State Drives |

| Network Attached Storage |

| Flash Drives |

| Other Product Type |

| Hard Disk Drive |

| Solid State Drive |

| Optical Discs |

| Cloud Integrated Personal Storage |

| Other Storage Medium |

| 1-99 GB |

| 100 GB-1 TB |

| 1-10 TB |

| greater than 10 TB |

| Consumers |

| Small Office Home Office |

| Small and Medium Enterprises |

| Photography/Videography Professionals |

| Other End User |

| Online Retail |

| Offline Retail |

| Direct Sales |

| Other Distribution Channel |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | External Hard Disk Drives | ||

| Solid State Drives | |||

| Network Attached Storage | |||

| Flash Drives | |||

| Other Product Type | |||

| By Storage Medium | Hard Disk Drive | ||

| Solid State Drive | |||

| Optical Discs | |||

| Cloud Integrated Personal Storage | |||

| Other Storage Medium | |||

| By Capacity Range | 1-99 GB | ||

| 100 GB-1 TB | |||

| 1-10 TB | |||

| greater than 10 TB | |||

| By End User | Consumers | ||

| Small Office Home Office | |||

| Small and Medium Enterprises | |||

| Photography/Videography Professionals | |||

| Other End User | |||

| By Distribution Channel | Online Retail | ||

| Offline Retail | |||

| Direct Sales | |||

| Other Distribution Channel | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the forecast value of the personal and entry level storage market in 2030?

The market is projected to reach USD 361.36 billion by 2030.

Which region shows the fastest growth rate through 2030?

The Middle East is expected to register a 28.89% CAGR through 2030.

Which product type currently leads revenue share?

Solid state drives led with 41.37% of 2024 revenue.

Why are small office home office buyers important for vendors?

They are adopting multi-bay NAS solutions at a 29.33% CAGR as hybrid work pushes enterprise-grade storage needs into homes.

How does Thunderbolt 5 influence portable storage demand?

It boosts external SSD throughput beyond 6,000 MB/s, allowing real-time 8K editing directly from the drive, which stimulates premium-segment sales.

What regulation will reshape consumer-storage security in Europe?

The EU Cyber Resilience Act will require secure-by-default devices and five-year update support starting December 2027.

Page last updated on: