Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.38 Billion |

| Market Size (2031) | USD 75.66 Billion |

| Growth Rate (2026 - 2031) | 23.45% CAGR |

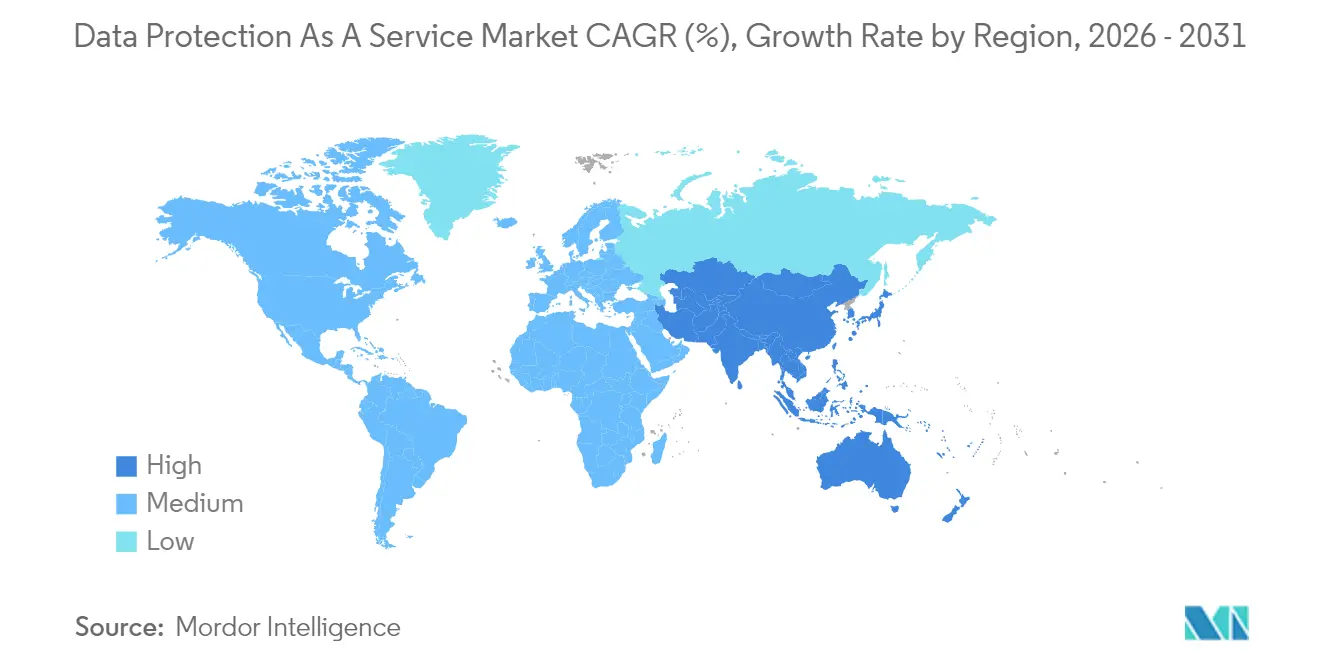

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

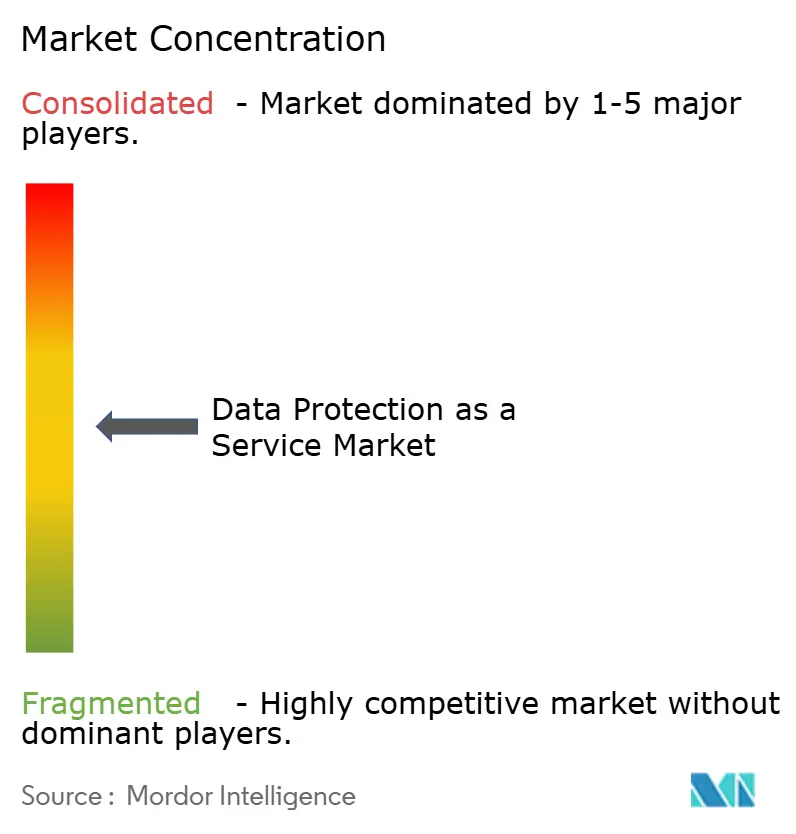

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Protection As A Service Market Analysis by Mordor Intelligence

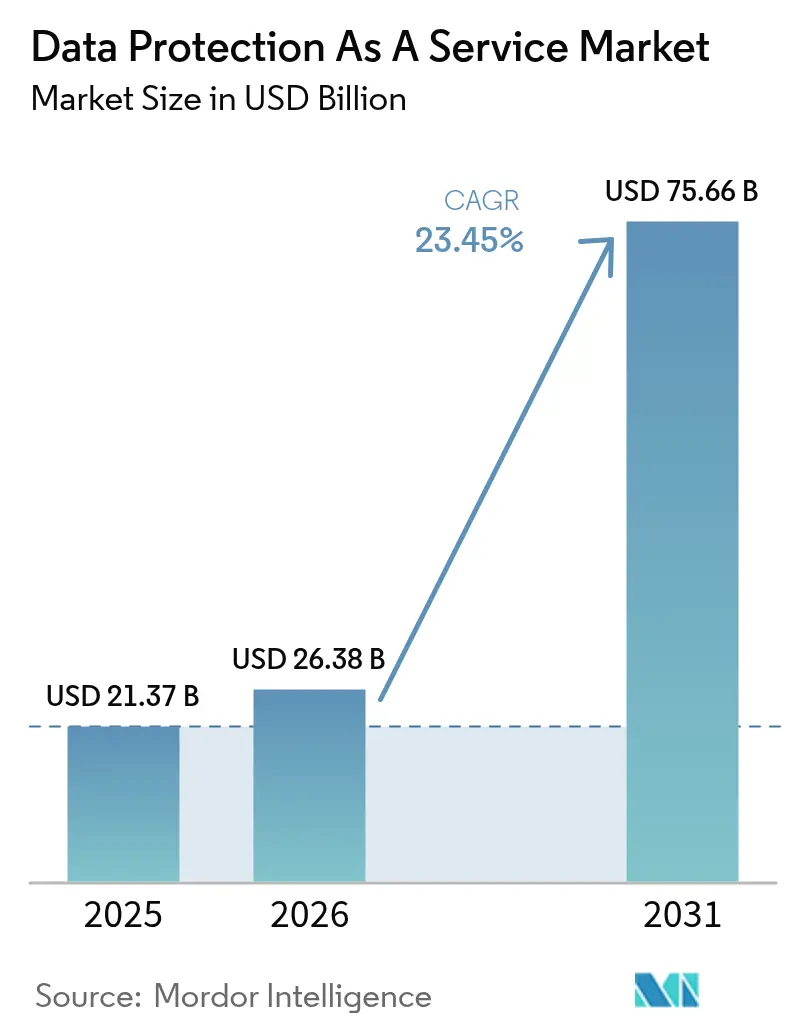

Data Protection As A Service Market size in 2026 is estimated at USD 26.38 billion, growing from 2025 value of USD 21.37 billion with 2031 projections showing USD 75.66 billion, growing at 23.45% CAGR over 2026-2031.

Growth is propelled by a surge in unstructured data, zero-trust mandates, and rising board-level concern over ransomware exposure. Enterprises are rapidly replacing capital-intensive, on-premises backup hardware with cloud-delivered subscriptions that offer usage-based pricing and elastic scale. Sovereign-cloud investments, quantum-safe encryption pilots, and cyber-insurance requirements are converging to reshape product roadmaps, while vendor consolidation is compressing market structure and accelerating feature integration.

Key Report Takeaways

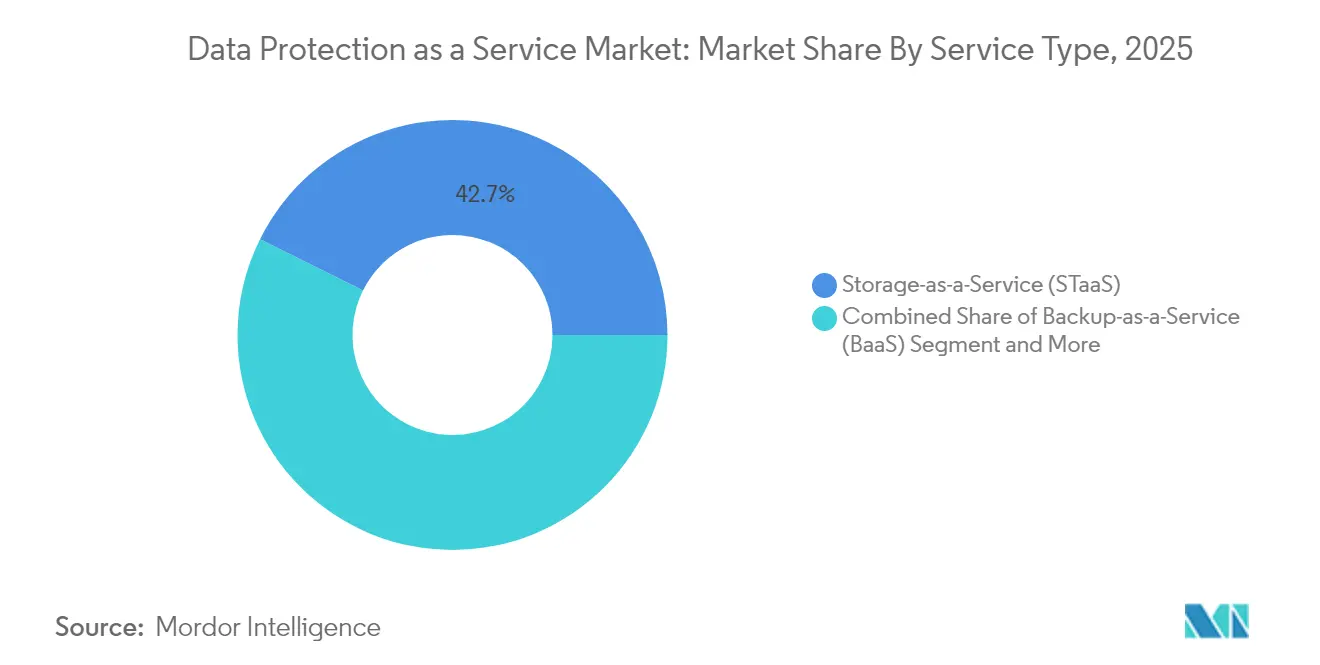

- By service type, Storage-as-a-Service held 42.65% of the data protection as a service market share in 2025; Disaster-Recovery-as-a-Service is projected to grow at a 28.9% CAGR through 2031.

- By deployment model, the private-cloud segment captured 43.05% of the data protection as a service market size in 2025, whereas hybrid-cloud adoption is expected to expand at a 30.6% CAGR between 2026-2031.

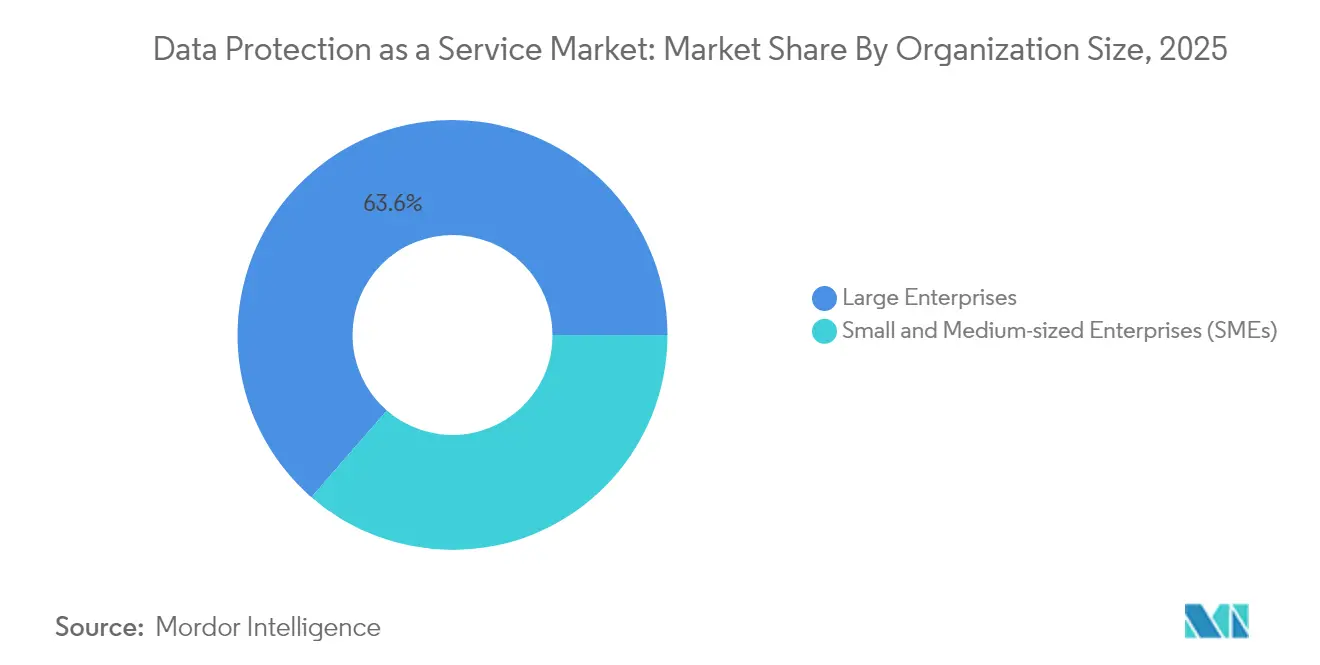

- By organization size, large enterprises retained 63.60% share of the data protection as a service market size in 2025, while SMEs are forecast to advance at a 33% CAGR to 2031.

- By end-use industry, BFSI led with 27.35% revenue share in 2025; healthcare and life sciences are on track for a 29.8% CAGR through 2031.

- By geography, North America commanded 37.25% of 2025 revenue, whereas Asia-Pacific is anticipated to register a 30.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Protection As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty regulations | +5.8% | EU, North America, APAC | Medium term (2-4 years) |

| Unstructured data explosion | +4.6% | Global | Long term (≥ 4 years) |

| Ransomware resiliency focus | +4.2% | North America, Europe, APAC | Short term (≤ 2 years) |

| Recovery vaults linked to cyber-insurance | +3.3% | North America, Europe | Medium term (2-4 years) |

| Sovereign-cloud build-outs | +2.5% | Middle East, APAC, Europe | Medium term (2-4 years) |

| Quantum-safe encryption pilots | +0.8% | North America, Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Sovereignty Regulations Reshape Global Protection

The roll-out of GDPR look-alike frameworks from Brazil to India is forcing firms to localize storage, adopt precise data-mapping, and build policy-based controls that govern cross-border flows. The EU Digital Operational Resilience Act took effect in January 2025, mandating near-real-time incident reporting for financial institutions. In the United States, new rules restrict sensitive data transfers to foreign adversaries, adding complexity for multinationals. As a result, procurement teams now rank sovereignty controls alongside RPO/RTO metrics when selecting DPaaS vendors. Providers are responding with region-specific key management, double-encryption options, and in-region recovery vaults that satisfy both national regulators and internal risk committees.

Edge Computing Revolutionizes Protection Architectures

Edge deployments move processing closer to sensor endpoints and branch locations, allowing workloads to meet latency targets without routing traffic back to centralized data hubs. Forty percent of large enterprises plan to run mission-critical applications at the edge by end-2025; that shift necessitates lightweight, policy-driven backup agents capable of executing locally and synchronizing asynchronously. Emerging offerings embed AI-based anomaly detection at edge gateways, reducing dwell time for ransomware incursions. Healthcare systems are piloting these capabilities in hospital campuses to comply with strict patient-data localization rules while ensuring immediate access for clinicians.

Ransomware Resilience Becomes a Board Priority

Ransomware volume doubled during 2024, prompting audit committees to request proof of immutable backups and verified restoration drills. DPaaS roadmaps now center on continuous data protection, air-gapped vaults, and machine-learning classification that prevents reinfection during recovery. Insurers are tying premium discounts to the presence of write-once storage and automated failover orchestration. Enterprises adopting these controls report materially lower recovery-time objectives and demonstrable savings on cyber-insurance renewals.

Cloud-Native Recovery Vaults Transform Resilience Economics

Cloud-native recovery vaults provide logically-isolated storage coupled with policy-driven replication. They minimize egress during restore events and give insurers clearer evidence of least-privilege access. Early adopters in financial services attribute double-digit drops in policy premiums to vault certification. Vendors differentiate through zero-trust authentication, generative AI forensic scans, and integration with SOC workflows. As vault adoption broadens, platform convergence across backup, archive, and cyber-recovery is accelerating.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hidden egress and API charges | -2.1% | Global | Medium term (2-4 years) |

| Proprietary backup formats | -1.6% | Global | Long term (≥ 4 years) |

| AI compression delaying upgrades | -1.3% | North America, Europe, APAC | Medium term (2-4 years) |

| Data-residency clauses in trade pacts | -1.0% | Regions with strict sovereignty | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hidden Cloud Costs Undermine Multi-Cloud Strategies

Variable traffic fees and per-API call pricing can inflate budgets, especially for analytics-heavy or regulatory inquiries that require frequent restores. Enterprises with limited negotiation leverage in smaller cloud regions feel the pinch most acutely. FinOps teams are investing in cost-observability dashboards, yet fragmented billing across storage tiers and hot-cold transitions remains a budgetary hazard.

Proprietary Formats Create Vendor Lock-In

Closed backup schemas complicate workload migration after mergers or provider exits. During the 2024 Cohesity-Veritas merger, integration teams faced multi-platform restore testing to preserve SLAs. Regulators are examining whether proprietary metadata structures inhibit competition. Customer RFPs increasingly insist on open-format exports, prompting newer entrants to adopt standardized APIs that promise smoother portability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: DRaaS Accelerates Amid Cyber Threats

The Disaster-Recovery-as-a-Service segment recorded a 28.9% CAGR outlook through 2031, outpacing other offerings as leadership teams elevate ransomware readiness to a strategic metric. More than 70% of enterprises intend to integrate DRaaS with SIEM telemetry by 2026, enabling automated failover based on threat scoring. Continuous data protection streams shrink recovery-point objectives to seconds, appealing to finance and healthcare workloads where data loss equates to compliance fines. Storage-as-a-Service, though still capturing 42.65% of the 2025 data protection as a service market share, is evolving toward intelligent tiering and policy-based immutability that aligns with zero-trust architectures. Converged platforms now bundle BaaS, STaaS, and DRaaS under unified policy engines, easing procurement and governance.

While DRaaS enthusiasm rises, storage subscriptions remain foundational. Object-store growth stays strong due to AI model training sets and video analytics that balloon unstructured data volumes. In response, providers are pushing petabyte-scale deduplication and compression to control the footprint. Full-stack offerings from cloud hyperscalers now integrate autonomous threat scanning, meaning that ransomware reels only the affected blocks rather than entire volumes. Such feature alignment signals a longer-term move toward platform-centric purchasing in which recovery automation, data classification, and compliance mapping exist inside a single control plane.

By Deployment Model: Hybrid Approaches Balance Security and Flexibility

Hybrid models show the fastest expansion at 30.6% CAGR. Regulators endorse architectures that keep sensitive datasets on local private clouds while allowing burstable analytics in regulated public regions. These patterns are especially evident among European banks subject to the Digital Operational Resilience Act, which mandates documented contingency arrangements for third-party services. Policy automation selects storage targets based on data-classification labels, optimizing both latency and compliance. The data protection as a service market size for hybrid solutions is forecast to double by 2028 as enterprises modernize legacy tape archives into cloud-connected vaults.

Private-cloud deployments retain a 43.05% share, favored by defense, utilities, and healthcare agencies that must assert custody over encryption keys. Vendors supplying private-cloud appliances increasingly embed FIPS-validated HSMs, role-based access, and air-gapped configuration management. Public-cloud approaches remain popular among digital-native firms that value region diversity over full sovereignty. However, sovereign-cloud initiatives, such as the AWS European Sovereign Cloud, blur lines: they deliver public-cloud agility under local legal control, pulling regulated workloads into environments previously deemed off-limits.

By Organization Size: SMEs Embrace Cloud-Based Protection

Rising cyber threats and limited IT staff push SMEs toward off-the-shelf SaaS backup portals that include preset compliance templates. Between 2026-2031, the data protection as a service market size revenue from SMEs is projected to climb at 33% CAGR, supported by managed service providers offering turnkey bundles. Simplified onboarding and consumption-based billing resonate with budget-conscious owners. Cyber-insurance questionnaires increasingly list the presence of immutable cloud snapshots as a prerequisite, nudging even micro-enterprises toward entry-level DPaaS tiers.

Conversely, large enterprises retain 63.60% revenue thanks to sprawling workloads, legacy mainframes, and stringent RTO targets. Many overlay DPaaS atop existing tape libraries for phased modernization, reducing forklift upgrades. AI-enhanced anomaly detection flags deviations in snapshot change rates, giving SOC teams early warning of encryption attacks. Vendors court this segment with SLA-backed availability guarantees and dedicated account teams that shepherd regulatory audits.

By End-User Industry: Healthcare Accelerates Protection Investments

Healthcare’s 29.8% CAGR reflects electronic health record mandates, connected devices, and cross-hospital data sharing requirements. Hospitals deploy immutable backups and air-gapped recovery vaults to satisfy HIPAA and EU harmonized patient data directives. Telemedicine expansions drive edge-node deployments inside clinical sites, requiring local snapshotting that synchronizes to sovereign cloud regions. Clinical research teams benefit from policy engine integration that differentiates between identifiable patient information and anonymized study datasets.

BFSI leads overall spending with 27.35% market share, underpinned by high transaction volumes and new breach-notification timelines. DORA obliges European banks to test full-scale disaster recovery at least annually, driving DRaaS adoption. Insurers collaborate with DPaaS vendors to offer premium incentives contingent on completed recovery drills. Government and defense programs invest aggressively as zero-trust strategies dictate continuous verification across classified networks. Finally, manufacturing and telecom firms rely on DPaaS to secure industrial Internet-of-Things telemetry, where downtime directly hits throughput.

Geography Analysis

North America preserves a 37.25% revenue share, anchored by robust cloud adoption and federal directives such as CISA Binding Operational Directive 25-01, which compels agencies to apply secure configuration baselines for SaaS. The Protecting Americans' Data from Foreign Adversaries Act restricts cross-border transfers of sensitive personal data, spurring demand for in-country vaults and key escrow. Enterprises prioritize compliance mapping features that generate automated attestation reports for auditors.

Asia-Pacific posts the fastest trajectory at 30.5% CAGR as digital-government programs in Japan, India, and Korea push data-localization rules. The Indian Digital Personal Data Protection Act codifies explicit localization for critical personal information, pressuring cloud providers to launch domestic recovery zones. Hyperscalers partner with domestic telecom carriers to establish sovereign facilities that allow foreign backup services while respecting legal custody constraints. Start-ups in Singapore and Australia roll out DPaaS offerings that combine secure local storage with global failover options, appealing to mid-market exporters balancing trade and compliance.

Europe remains a sophisticated adopter shaped by GDPR, DORA, the Cyber Resilience Act, and the EU Data Act, effective September 2025. National programs such as France’s Cloud de Confiance and Germany’s Gaia-X channel funding into federated, standards-based infrastructure that prizes transparency and vendor portability. Providers differentiate by offering in-region metadata processing, EU resident-only operations staff, and exportable audit trails. Sovereign options reduce regulatory friction, driving higher attach rates among public-sector entities.

Emerging markets in Latin America, the Middle East, and Africa register rising adoption from smaller bases. Gulf Cooperation Council governments finance sovereign-cloud platforms to diversify economies and lure fintech start-ups. Brazilian banks pilot quantum-safe encryption on cross-border replication links, anticipating future cryptographic requirements. African telcos deploy SaaS backup to protect rapidly expanding mobile money platforms, offsetting limited local data-center capacity.

Competitive Landscape

Industry consolidation intensifies with the December 2024 absorption of Veritas enterprise assets by Cohesity, forming a USD 7 billion entity serving over 12,000 global customers. Rubrik allies with Cisco to embed backup telemetry inside the Cisco XDR console, illustrating a pivot toward integrated detection-and-response suites. Broadcom’s quantum-resistant host bus adapters foreshadow a hardware-rooted defensive layer that competitors must match. AWS debuts a European Sovereign Cloud, undercutting regional providers by pairing hyperscale economics with local legal control.

Mid-tier specialists such as Druva and Clumio court SMEs by offering agentless, SaaS-native protection that deploys in minutes. N-able’s Adlumin acquisition folds SOC automation into managed-service offerings, signaling MSP channel importance for long-tail growth. Verticalization emerges: providers launch healthcare-specific blueprints featuring HIPAA templates, while BFSI packages integrate PCI-DSS tokenization. Competitive differentiation now hinges on turnkey ransomware recovery guarantees, hourly SLA credits, and automated compliance evidence generation.

Platform convergence is evident as vendors collapse STaaS, BaaS, and DRaaS silos into policy-driven fabrics. Buyer preference trends toward single-pane orchestration that simplifies audit traceability. However, proprietary snapshot formats risk customer lock-in, prompting open API initiatives. Vendors that expose portable metadata and cross-cloud replication options may gain share as regulatory scrutiny of interoperability mounts.

Data Protection As A Service Industry Leaders

IBM Corporation

Amazon Web Services Inc.

Hewlett Packard Enterprise Company

Dell Technologies Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AWS unveiled the AWS European Sovereign Cloud, operated solely by EU residents and governed under EU law.

- May 2025: JetStor introduced Infinite, a data-platform-as-a-service integrating native protection and compliance tooling.

- April 2025: HPE launched threat-adaptive security for HPE Private Cloud Enterprise, featuring air-gapped management to satisfy DORA requirements.

- February 2025: OpenText released Core Threat Detection and Response, an AI-powered module that integrates with Microsoft Security.

- January 2025: Broadcom delivered quantum-resistant network encryption for in-flight storage traffic, complying with CNSA 2.0 and EU DORA mandates.

- December 2024: Cohesity finalized its USD 7 billion purchase of Veritas enterprise backup, creating the largest pure-play provider.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Data Protection-as-a-Service (DPaaS) market as subscription-based cloud or hybrid offerings that back up, replicate, archive, and recover enterprise data across servers, endpoints, and SaaS workloads, while embedding policy management and encryption. According to Mordor Intelligence, revenues are counted on a recurring basis, net of one-time hardware or consulting fees, and cover Storage, Backup, and Disaster-Recovery-as-a-Service delivered globally to all industry verticals.

Scope Exclusions: Stand-alone on-premise backup software, professional services billed separately, and self-built private cloud instances are outside this scope.

Segmentation Overview

- By Service Type

- Storage-as-a-Service (STaaS)

- Backup-as-a-Service (BaaS)

- Disaster-Recovery-as-a-Service (DRaaS)

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- Government and Defense

- IT and Telecom

- Retail and E-commerce

- Manufacturing

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with CISOs, backup architects, MSP channel heads, and cloud-storage OEM product managers across North America, Europe, and Asia supplied real-world pricing tiers, retention policies, and seat penetration benchmarks. Surveys of SMEs in emerging hubs clarified willingness to shift from tape to DRaaS, closing gaps left by public filings.

Desk Research

We began by mapping the regulatory spine, GDPR, CCPA, India's DPDP Act, using publications from bodies such as the European Data Protection Board, NIST, and the FTC, which signal compliance-driven spending. Trade flows from UN Comtrade, breach tallies from the Verizon DBIR, and quarterly cloud revenue disclosures helped anchor demand and vendor share movement. Company 10-Ks, investor decks, and audited cloud ARR splits were then sifted to derive average contract values, which are vital in subscription models.

The desk phase also tapped paid datasets, D&B Hoovers for vendor financials and Dow Jones Factiva for deal news, alongside sector associations like the Cloud Security Alliance. This list is illustrative; many other reputable open and paid sources fed into data collection and cross-checks.

Market-Sizing & Forecasting

A top-down construct starts with worldwide enterprise IT spend, layers in cloud adoption ratios, and applies workload-level backup penetration rates. Results are stress-tested through bottom-up roll-ups of sampled vendor ARR and average selling price multiplied by contract volume checks. Variables such as unstructured-data growth (exabytes), ransomware incident frequency, sovereign-cloud capacity, cyber-insurance premium trends, and hyperscale data-center footprint expansion feed the model. Forecasts employ multivariate regression blended with scenario analysis, letting us flex regulatory shock or pricing compression cases while keeping base-case CAGR realistic. Where supplier splits are opaque, regional channel checks guide allocation before final triangulation.

Data Validation & Update Cycle

Outputs flow through anomaly screens, peer review, and a senior analyst sign-off. Models refresh annually, and we trigger interim reviews when breaches over USD 100 million, landmark regulations, or mega cloud outages occur. A last-mile validation is done just before publishing so clients receive the freshest view.

Why Mordor's Data Protection As A Service Baseline Commands Deep Stakeholder Confidence

Published figures often diverge because firms choose different service mixes, pricing assumptions, and refresh rhythms, and because some roll broader security bundles into DPaaS totals.

Key gap drivers include rivals counting one-time hardware revenue, excluding SMEs from uptake pools, using static price points despite aggressive vendor discounting, or applying blanket growth adders without breach-volume correlation. Mordor's model instead tracks live subscription ARRs, updates conversion ratios quarterly, and weights scenarios by primary-research consensus.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.37 B (2025) | Mordor Intelligence | - |

| USD 26.04 B (2024) | Global Consultancy A | Includes one-off appliance sales and license renewals |

| USD 38.81 B (2025) | Industry Association B | Uses list prices, limited SME sampling |

| USD 22.05 B (2023) | Trade Journal C | Applies straight-line CAGR, no regulatory scenario testing |

Taken together, the comparison shows that Mordor's disciplined scope choices, variable-level audits, and rolling refresh cadence provide a balanced, transparent baseline that decision-makers can replicate and defend.

Key Questions Answered in the Report

What is driving the rapid growth of the data protection as a service market?

Rising ransomware incidents, stricter data-sovereignty laws, and the need to protect expanding edge- and cloud-generated data are key catalysts.

Which service type is expanding the fastest within DPaaS?

Disaster-Recovery-as-a-Service is forecast to grow at 28.9% CAGR between 2026-2031 as firms prioritize ransomware resilience.

How are sovereign clouds influencing deployment decisions?

Sovereign clouds let organizations keep encryption keys and data under local jurisdiction while accessing public-cloud elasticity, boosting hybrid adoption.

Why are SMEs accelerating their DPaaS uptake?

Subscription pricing, minimal upfront infrastructure, and insurer demands for immutable backups make cloud-delivered protection attractive to smaller firms.

What role does quantum-safe encryption play in future DPaaS contracts?

Early pilots suggest quantum-resistant algorithms will become mandatory for critical industries, prompting refresh cycles that favor vendors with compliant offerings.

How do hidden cloud fees affect total DPaaS cost of ownership?

Egress and API charges can inflate budgets; organizations increasingly deploy FinOps tools to monitor and optimize multi-cloud spend.

Page last updated on: