Cell Based Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

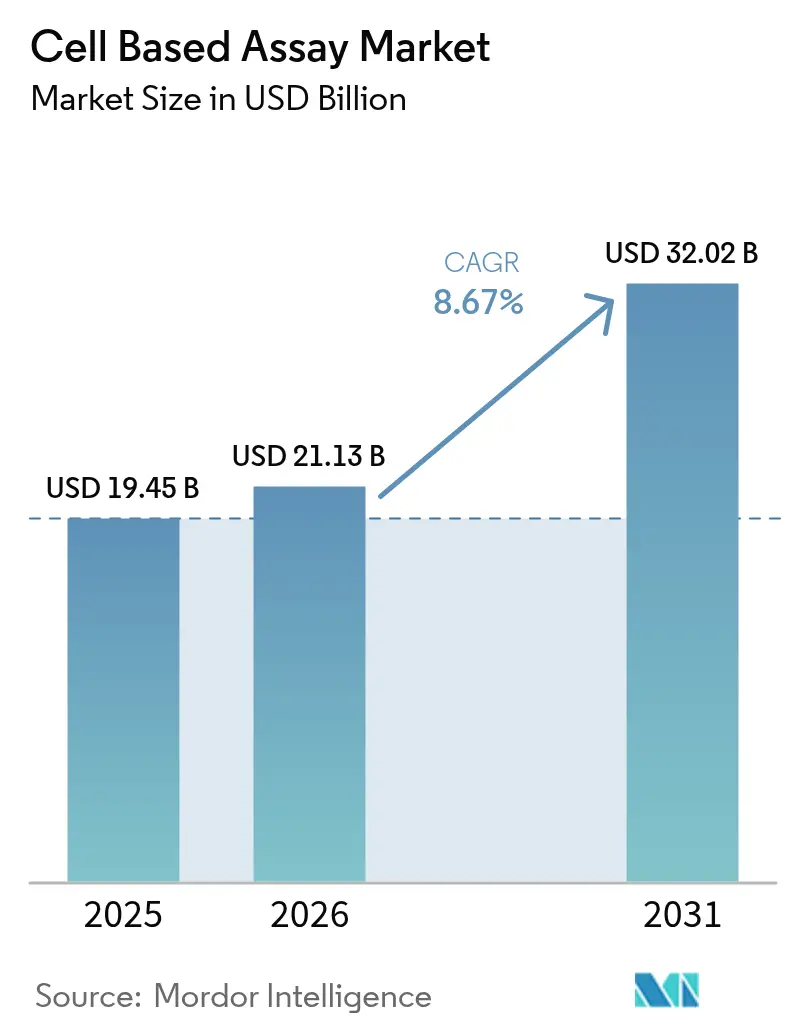

| Market Size (2026) | USD 21.13 Billion |

| Market Size (2031) | USD 32.02 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

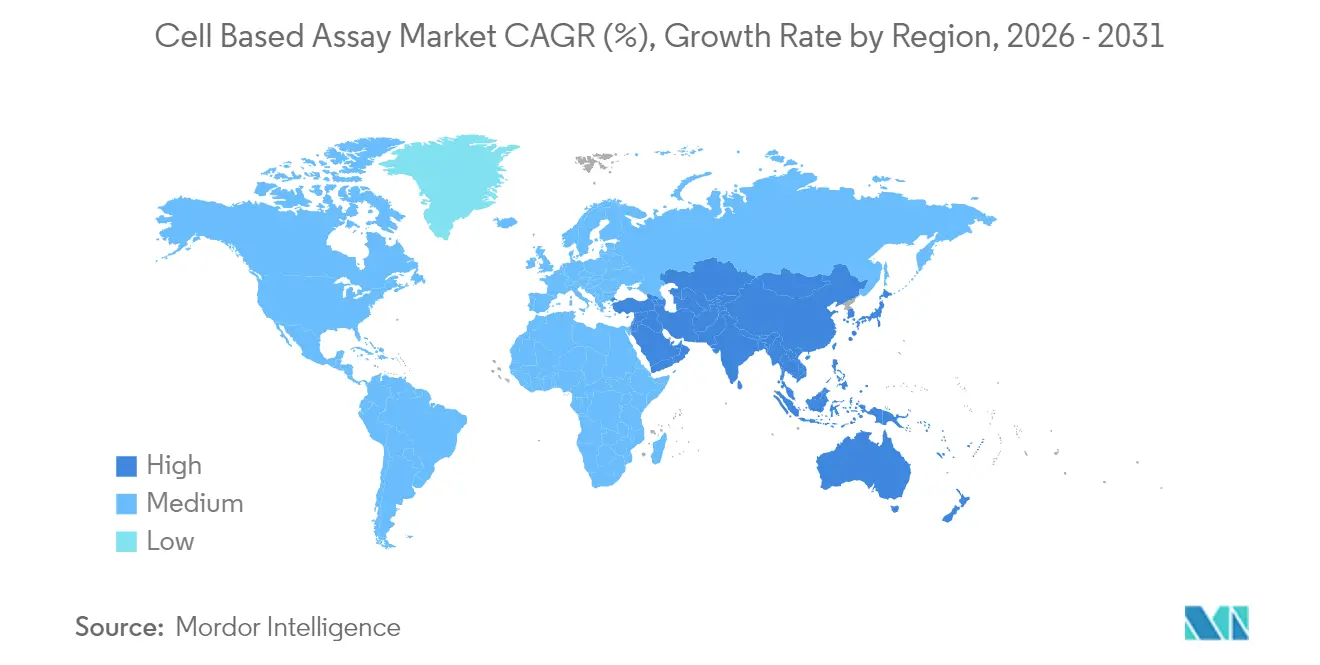

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Based Assay Market Analysis by Mordor Intelligence

The Cell Based Assay Market size was valued at USD 19.45 billion in 2025 and estimated to grow from USD 21.13 billion in 2026 to reach USD 32.02 billion by 2031, at a CAGR of 8.67% during the forecast period (2026-2031).

The transition from animal studies to human-relevant in vitro models, bolstered by the April 2025 FDA decision to phase out animal testing, positions validated cellular platforms at the center of regulatory-compliant development. Companies are rapidly expanding automation, AI-driven analytics, and 3-D organoid models to improve predictive accuracy and reduce cycle times, while investment flows from major biopharma groups signal confidence in next-generation screening technologies. At the same time, rising chronic-disease prevalence, oncology pipelines, and regenerative-medicine projects sustain a robust demand outlook for high-throughput formats and label-free detection systems.

Key Report Takeaways

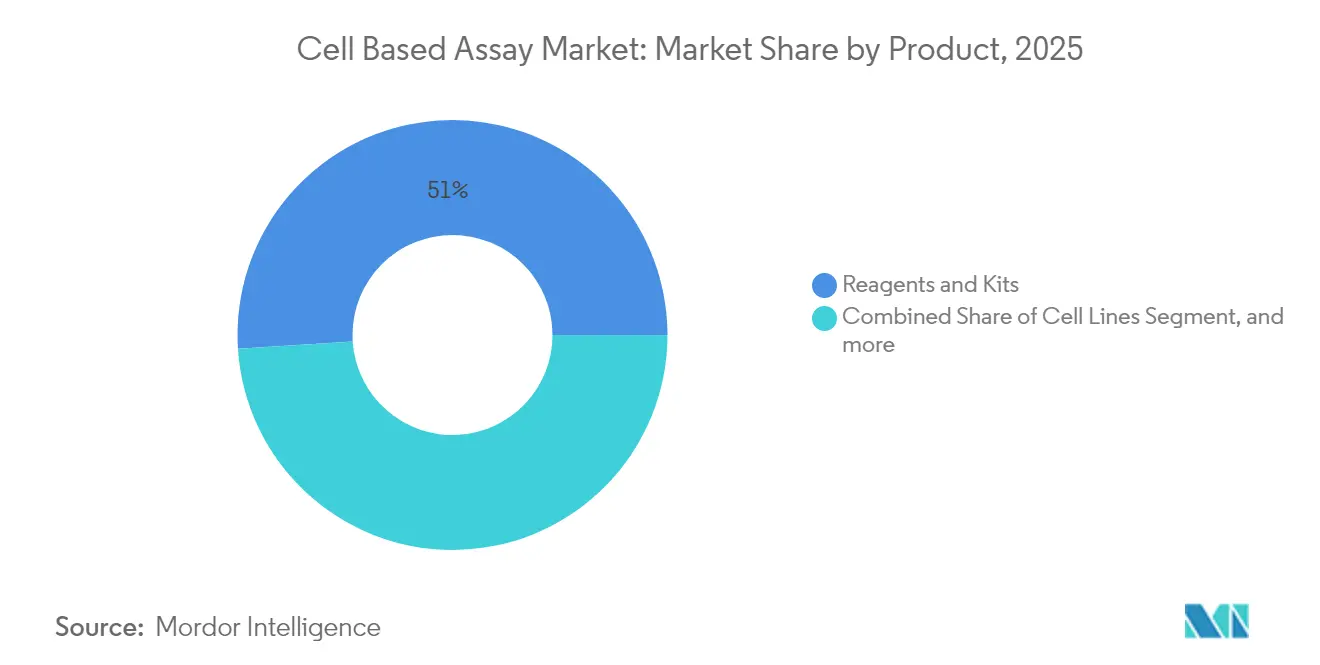

- By product category, reagents and kits led with 51.02% revenue share of the cell based assay market in 2025; cell lines are projected to expand at a 10.02% CAGR through 2031.

- By technology, high-throughput screening held 41.66% of the cell based assay market share in 2025, while 3-D cell-culture assays are poised for an 8.14% CAGR to 2031.

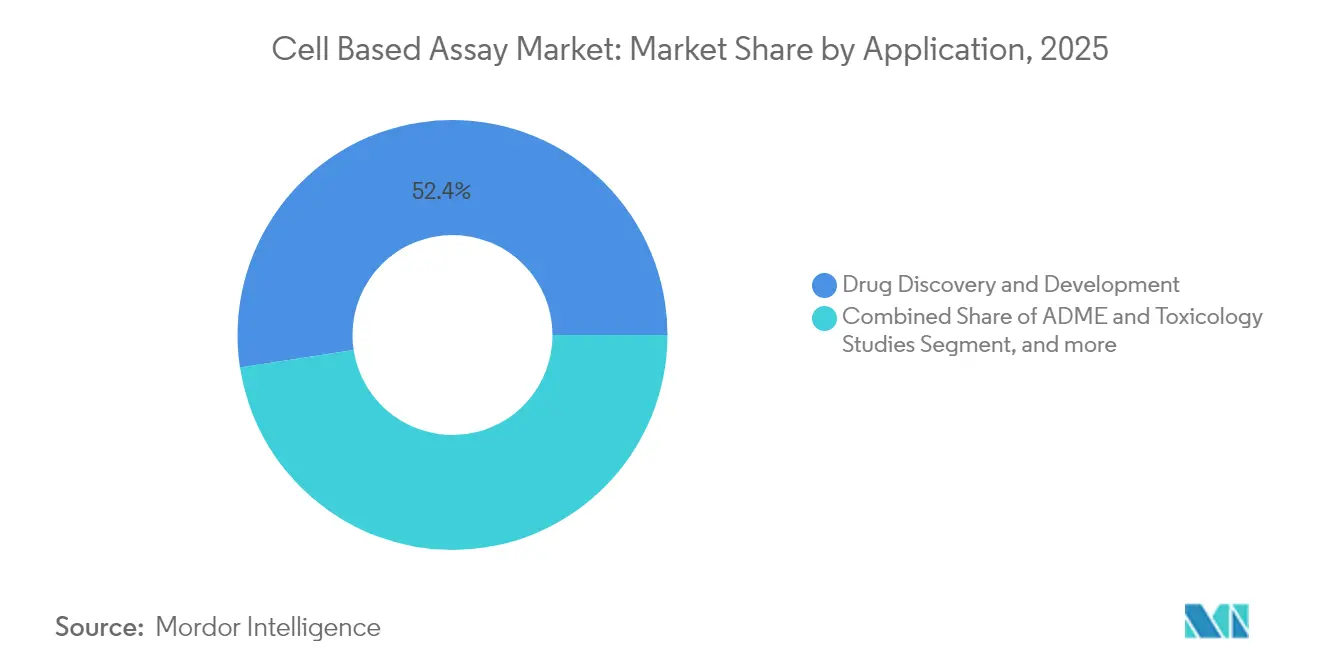

- By application, drug discovery and development accounted for 52.41% share of the cell based assay market size in 2025; precision and regenerative medicine is advancing at a 7.58% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies represented 48.05% demand in 2025; contract research organizations (CROs) exhibit the highest projected CAGR at 9.01% to 2031.

- By geography, North America commanded 40.85% of 2025 revenue, while Asia-Pacific is forecast to grow at 9.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Based Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Lifestyle Diseases | +1.8% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Escalating Pharma-Biotech R&D Spending on Drug Discovery | +2.1% | Global, concentrated in US, China, and EU | Short term (≤ 2 years) |

| Continuous Advances in High-Throughput & Label-Free Assays | +1.5% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Growing Adoption of 3-D Organoid Models for Precision Oncology | +1.2% | Global, with early adoption in US and Japan | Long term (≥ 4 years) |

| AI-Powered High-Content Analytics Accelerating Screening Cycles | +1.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Global Regulatory Shift Toward In Vitro Alternatives to Animal Tests | +2.3% | Global, led by US FDA and EU regulatory harmonization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Lifestyle Diseases

Escalating cancer and metabolic-disease incidence is intensifying demand for sophisticated phenotypic screens that shorten discovery cycles. The National Cancer Institute budget rose by USD 407.6 million in 2024, earmarking funds for high-content platforms aimed at oncology pipelines. Vertex Pharmaceuticals committed USD 240 million to scale stem-cell therapeutics for type 1 diabetes, illustrating how disease-driven investment accelerates the cell-based assay market.[1]Vertex Pharmaceuticals, “Vertex licenses C-Stem platform,” vrtx.com As aging demographics widen clinical need, pharmaceutical groups integrate organoid panels and multiplex flow cytometry to improve translational relevance, reinforcing long-term growth.

Escalating Pharma-Biotech R&D Spending on Drug Discovery

Thermo Fisher Scientific has budgeted USD 2 billion (2025–2028) for U.S. manufacturing and R&D sites that include cell-analysis capabilities. AstraZeneca’s USD 300 million cell-therapy facility in Maryland and Novo Nordisk’s USD 4.1 billion injectable-therapeutic plant reveal broad capital reallocation toward in vitro testing workflows. Contract manufacturers such as Fujifilm Diosynth follow with USD 1.6 billion expansions focused on mammalian-cell processes, indicating multistakeholder confidence in the cell based assay industry

Continuous Advances in High-Throughput & Label-Free Assays

BD’s FACSDiscover A8 now analyzes 50 parameters per cell, uniting spectral optics with imaging to capture richer biology in a single run.[2]BD Biosciences, “BD FACSDiscover A8 launch,” bd.com Beckman Coulter’s CytoFLEX mosaic module detects particles down to 80 nm, showing spectral flow’s rapid sensitivity gains. Academic breakthroughs such as Carnegie Mellon’s bioluminescent GPCR biosensors are expanding label-free assay menus that cut reagent costs and enable kinetic readouts.

Growing Adoption of 3-D Organoid Models for Precision Oncology

Following the FDA’s April 2025 animal-testing phase-out roadmap, organoid systems earned explicit recognition as validated toxicity and efficacy surrogates. Molecular Devices reports that automation and AI integration have halved plate-handling turnaround in organoid protocols, a prerequisite for high-volume screens. Roche and Vivodyne now deploy robotic tissue factories capable of assaying thousands of patient-specific tumors weekly, indicating commercial viability for precision oncology workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Advanced Platforms | -1.9% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Shortage of Multi-Disciplinary, Assay-Development Talent | -1.4% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Steep Learning Curve for Data Integration & Assay Interoperability | -0.8% | Global, affecting smaller biotech companies | Short term (≤ 2 years) |

| Fragile, Specialty-Reagent Supply Chains Post-Pandemic | -1.1% | Global, with regional concentration risks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Platforms

Spectral flow systems can exceed USD 500,000, while annual service contracts add 20% of that figure, limiting uptake in price-sensitive academic and emerging-market settings.[3]Bio-Rad Laboratories, “Q1 2025 Life Science segment results,” bio-rad.com Financing schemes, including Beckman Coulter’s modular upgrades, seek to lower entry barriers, but capital outlays remain a gating factor for broader cell-based assay market penetration.

Shortage of Multi-Disciplinary, Assay-Development Talent

Singapore forecasts a 29% rise in assay-development talent gaps by 2032 despite targeted training programs. A 2024 survey found 83% of biopharma supply-chain leaders aim to reskill staff in data science to support digital labs. This talent bottleneck slows custom-assay rollout and elevates CRO outsourcing demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cell Lines Drive Innovation Despite Reagent Dominance

Reagents and kits, benefiting from repeat-purchase economics, contributed 51.02% of the cell-based assay market in 2025, anchoring the consumables revenue base. Cell lines, however, represent the pivotal innovation engine, expanding at 10.02% CAGR on the back of induced pluripotent stem cell advances and CRISPR-engineered disease models. TreeFrog Therapeutics’ USD 240 million C-Stem licensing deal with Vertex underscores rising valuations for scalable, high-quality cellular material.

The microplates subsegment enjoys steady gains from laboratory-automation compatibility, while specialty media and buffers mirror overall market expansion. Stem-cell-derived lines increasingly replace primary cultures due to improved consistency, a critical requirement for high-content screens.

By Technology: 3-D Culture Disrupts High-Throughput Screening Paradigms

High-throughput screening (HTS) platforms, long the backbone of pharmaceutical discovery, delivered 41.66% revenue in 2025. Yet, demand is shifting toward physiologically relevant 3-D models that more accurately recapitulate in-vivo biology. The 3-D culture segment’s 8.14% CAGR is propelled by organoid standardization and regulatory endorsement. BD’s spectral flow integration with robotic arms illustrates how established vendors are future-proofing HTS through automation and multi-modal detection.

Label-free detection and spectral cytometry broaden assay readouts, while automated liquid handlers compress sample-prep times, enhancing throughput. Together, these advances are expanding the cell based assay market size for integrated platforms expected to post double-digit growth within oncology workflows.

By Application: Precision Medicine Accelerates Beyond Drug Discovery

Drug discovery and development retained a 52.41% share in 2025 as pharmaceutical sponsors lean on high-content phenotypic screens to reduce attrition in late-stage trials. Concurrently, precision and regenerative medicine are scaling at 7.58% CAGR, driven by patient-derived organoid assays and cell therapies targeting diabetes, cardiac, and neurodegenerative conditions. NIH’s USD 4.3 million commitment to molecular-analysis methods in oncology reinforces public-sector support for advanced cellular readouts.

ADME-tox and basic-research segments maintain stable mid-single-digit expansion. Collectively, they ensure diversified revenue streams across the cell-based assay industry while facilitating regulatory-compliant safety packages for complex biologics.

By End User: CROs Capitalize on Outsourcing Trends

Pharmaceutical and biotechnology enterprises accounted for 48.05% of 2025 end-user revenue. Their strategy centers on securing integrated platforms that bundle instrumentation, reagents, and software to compress screening timelines. The cell-based assay market size is attributable to CRO engagements as outsourcing gains popularity among small and mid-cap companies seeking specialized expertise. STEMCELL Technologies’ organoid assay services exemplify niche CRO offerings that capture value where internal capabilities are scarce.

Academic institutes and hospitals continue to adopt advanced assays for translational research, supported by targeted grants such as the NIH’s USD 960,000 contraceptive program that relies on high-content imaging. Collectively, varied end-user profiles sustain demand diversity and buffer cyclic R&D spending shifts.

Geography Analysis

North America generated 40.85% of 2025 revenue, underpinned by deep biopharma pipelines, NIH funding, and FDA guidance favoring human-relevant models. Government incentives and domestic manufacturing investments, for example, Thermo Fisher Scientific’s USD 2 billion plan, fortify regional supply chains and enlarge the cell based assay market.

Asia-Pacific posts the fastest expansion at 9.02% CAGR. China’s talent pool and infrastructure are scaling rapidly, highlighted by Cytek Biosciences’ 50,000 sq ft manufacturing hub in Wuxi targeting high-dimensional cytometry systems. Japan’s fast-track approval path for cell and gene therapies accelerates commercialization of assay-dependent products, reinforcing demand for 3-D cultures and AI-enhanced analytics.

Europe retains a substantial share through entrenched pharma clusters in Germany, Switzerland, and the UK. Harmonization of alternative-testing regulations with U.S. standards is catalyzing upgrades to label-free detection and organ-on-chip platforms. Meanwhile, Latin America, the Middle East, and Africa offer emerging opportunities where technology transfer and collaborative programs mitigate high-capital entry barriers. Collectively these regions add incremental volume to the global cell based assay market while progressing toward regulatory convergence.

Competitive Landscape

The cell-based assay market is moderately fragmented in nature due to the presence of several companies operating globally as well as regionally. Thermo Fisher Scientific’s USD 3.1 billion Olink purchase and pending USD 4.1 billion Solventum filtration acquisition demonstrate a vertical-integration play that marries proteomics, purification, and assay platforms. BD advances differentiation through spectral cytometry combined with robotic automation, targeting laboratories seeking richer data density with fewer manual steps.

Emerging players innovate around cost and accessibility. Rice University’s AI-aided flow cytometer prototype reduces entry cost by an order of magnitude, signaling potential disruption in price-sensitive segments. At the same time, organoid specialists such as CN Bio secure strategic alliances with CDMOs like Pharmaron to validate physiology-on-a-chip systems for regulated use cases. Competitive advantage increasingly hinges on proven regulatory-compliance pathways, data-analytics integration, and service models that address assay-development complexity.

Cell Based Assay Industry Leaders

Becton, Dickinson and Company

Bio-Rad Laboratories, Inc.

Corning Inc.

Merck KGaA

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific announced plans to invest USD 2 billion in US innovation and manufacturing capabilities over four years, including USD 1.5 billion in capital expenditures and USD 500 million in R&D focused on high-impact innovation to strengthen the healthcare supply chain and support domestic biopharmaceutical production.

- May 2025: BD launched the FACSDiscover A8 Cell Analyzer, featuring breakthrough spectral and real-time cell imaging technologies that enable analysis of up to 50 cellular characteristics simultaneously, representing the first commercial platform to combine spectral flow cytometry with real-time imaging capabilities for enhanced biomarker discovery applications.

- April 2025: CN Bio and Pharmaron established a long-term strategic partnership to develop Organ-on-a-Chip technologies for drug discovery and development, with the collaboration aimed at validating CN Bio's PhysioMimix technology for disease modeling, toxicity testing, and ADME studies to meet growing demand for human-relevant testing models.

- March 2025: Beckman Coulter Life Sciences launched the CytoFLEX mosaic Spectral Detection Module, the first modular spectral flow cytometry solution that enhances fluorescence sensitivity for complex multicolor experiments and can detect nanoparticles as small as 80 nanometers, available globally in two configurations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cell-based assay market as the total annual revenue generated by consumables, instruments, software, and related services used to interrogate live cells for research, screening, ADME-tox, and clinical applications across pharmaceutical, biotechnology, academic, CRO, and diagnostic settings. Results cover all assay technologies, including flow cytometry, high-throughput screening, high-content imaging, label-free detection, and emerging 3-D formats, sold through direct and distributor channels in 26 major countries.

Scope exclusion: animal-derived in-vivo functional tests and standalone biochemical assays are deliberately left outside our sizing.

Segmentation Overview

- By Product

- Cell Lines

- Primary Cell Lines

- Stem Cell Lines

- Induced Pluripotent Cell Lines

- Engineered / Recombinant Lines

- Others

- Reagents & Kits

- Assay Reagents

- Reporter Gene & Substrate Kits

- Buffers & Media

- Other Reagents

- Microplates

- Other Consumables

- Cell Lines

- By Technology

- High-Throughput Screening

- Flow Cytometry

- Automated Liquid Handling

- Label-free Detection

- 3-D Cell-Culture Assays

- Others

- By Application

- Drug Discovery & Development

- ADME & Toxicology Studies

- Basic Research

- Precision & Regenerative Medicine

- Other Applications

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Academic & Government Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with R&D directors at multinational pharma manufacturers, method-development scientists at CROs, and procurement managers from academic core facilities in North America, Europe, and Asia helped us gauge kit replacement cycles, emerging 3-D assay penetration, and regional price spreads. Follow-up surveys with cell-culture media suppliers provided fresh volume indicators that desk research alone could not surface.

Desk Research

We pulled base statistics on pharma R&D expenditure, clinical-trial volumes, and biologics pipelines from sources such as OECD Health Data, NIH RePORTER, EMA clinical-trial registry, and World Bank Indicators. Trade volumes for key reagents were mapped using UN Comtrade, while shipment trends for microplates and liquid handlers were cross-checked on Volza's customs dashboard. Supplementary insight was gathered from peer-reviewed journals (Nature Methods, Drug Discovery Today) and company 10-Ks to benchmark average selling prices of reagent kits. Our analysts also tapped paid platforms, D&B Hoovers for company financials and Questel for patent velocity, to validate competitive capacity additions. The sources listed illustrate our approach; many additional public and paid references informed data validation.

Market-Sizing & Forecasting

A top-down model starts from 2024 biomedical R&D outlays, applies historic assay spending ratios by end user, and then reconstructs demand pools through production and trade data for key kit components. Supplier roll-ups and sampled ASP-times-volume checks offer bottom-up contrasts that let us tune totals. Critical variables include:

Number of active oncology and immunology drug programs under investigation,

Average kit consumption per high-throughput plate screened,

Shift toward 3-D culture formats,

Regional labor cost differentials affecting in-house vs outsourced testing,

Currency movements against the U.S. dollar.

Forecasts to 2030 employ multivariate regression blended with ARIMA to project each driver, before scenario analysis adjusts for regulatory moves on animal-test reduction. Data gaps in bottom-up estimates are bridged using primary-derived utilization factors.

Data Validation & Update Cycle

Outputs are stress-tested via three-way triangulation, anomaly scans, and senior analyst review. We refresh models yearly; interim updates trigger when M&A, regulation, or macro shocks move any driver beyond preset thresholds.

Why Mordor's Cell-Based Assay Baseline Commands Confidence

Published estimates often diverge because firms pick different product mixes, price anchors, and refresh cadences.

Key gap drivers include narrower geographic coverage, omission of software revenues, and single-scenario forecasting used elsewhere, whereas Mordor combines dual-scenario views and annual primary checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.45 B | Mordor Intelligence | - |

| USD 18.72 B | Global Consultancy A | excludes software & smaller APAC markets |

| USD 18.13 B | Global Consultancy B | uses fixed ASP, no primary validation |

These contrasts show that Mordor's balanced scope choice and recurring field interviews deliver a dependable, transparent baseline clients can trace back to clear assumptions and reproducible steps.

Key Questions Answered in the Report

What is the current value of the cell based assay market?

The cell based assay market stands at USD 21.13 billion in 2026 and is projected to reach USD 32.02 billion by 2031.

Which product segment is expanding the fastest?

Cell lines are growing at the highest pace, with a 10.02% CAGR expected through 2031 as engineered and stem-cell models gain traction.

Why are 3-D cell-culture assays important?

3-D cultures better mimic human physiology than 2-D monolayers, improving predictive accuracy and aligning with regulatory moves away from animal testing.

Which region offers the strongest growth opportunity?

Asia-Pacific is forecast to post a 9.02% CAGR due to biotech expansion in China, Japan, and South Korea, supported by favorable regulatory frameworks.

How are CROs influencing market dynamics?

CROs are growing at 9.01% CAGR as sponsors outsource complex assay development and leverage specialized expertise to shorten development timelines.

What role does AI play in cell based assays?

AI-driven high-content analytics accelerates screening by identifying subtle cellular phenotypes and predicting drug synergies, cutting costs and timelines in discovery programs.

Page last updated on: