Immuno Oncology Assays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

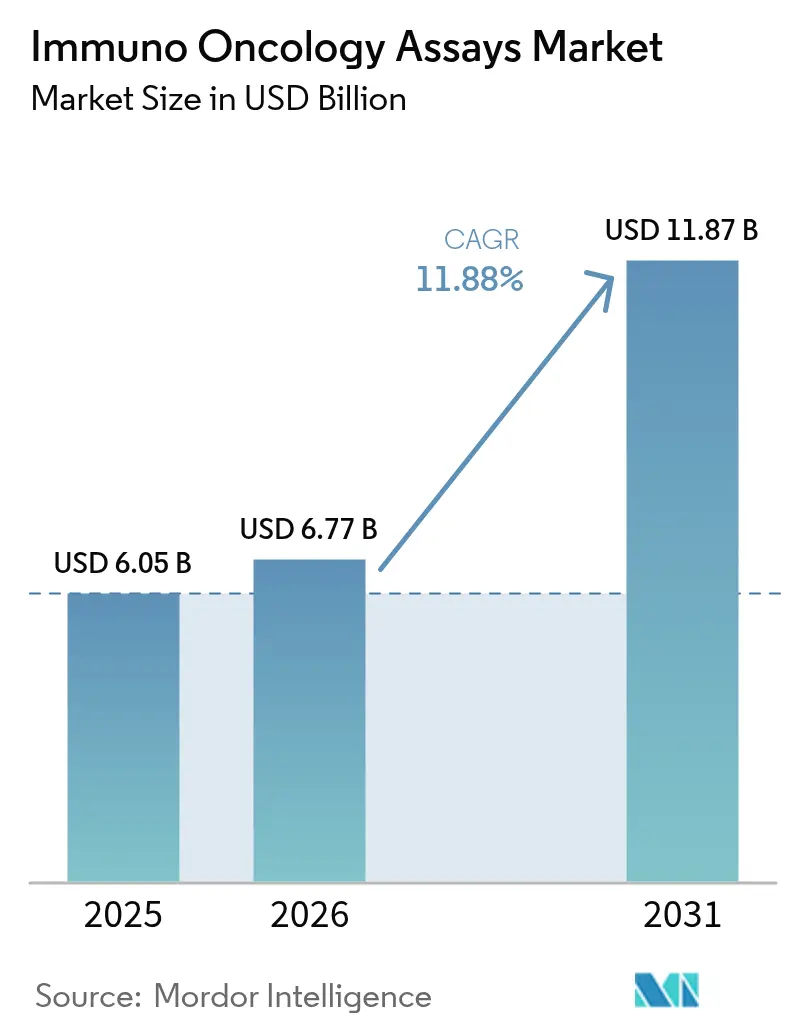

| Market Size (2026) | USD 6.77 Billion |

| Market Size (2031) | USD 11.87 Billion |

| Growth Rate (2026 - 2031) | 11.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immuno Oncology Assays Market Analysis by Mordor Intelligence

The immuno Oncology assays market size was valued at USD 6.05 billion in 2025 and estimated to grow from USD 6.77 billion in 2026 to reach USD 11.87 billion by 2031, at a CAGR of 11.88% during the forecast period (2026-2031). Rising global cancer incidence, steady regulatory support for companion diagnostics, and accelerating adoption of spatial biology platforms combine to spur demand for sophisticated immune profiling tests. Growing pharma–diagnostic partnerships shorten validation timelines and expand test menus, while artificial intelligence (AI) integration strengthens assay accuracy and throughput. North America maintains leadership through favorable reimbursement, but Asia-Pacific records the fastest uptake as healthcare infrastructure matures and clinical trial activity rises. Competitive strategies increasingly hinge on multi-omics integration and real-world evidence generation, positioning agile technology providers to capture sizeable share in community oncology settings.

Key Report Takeaways

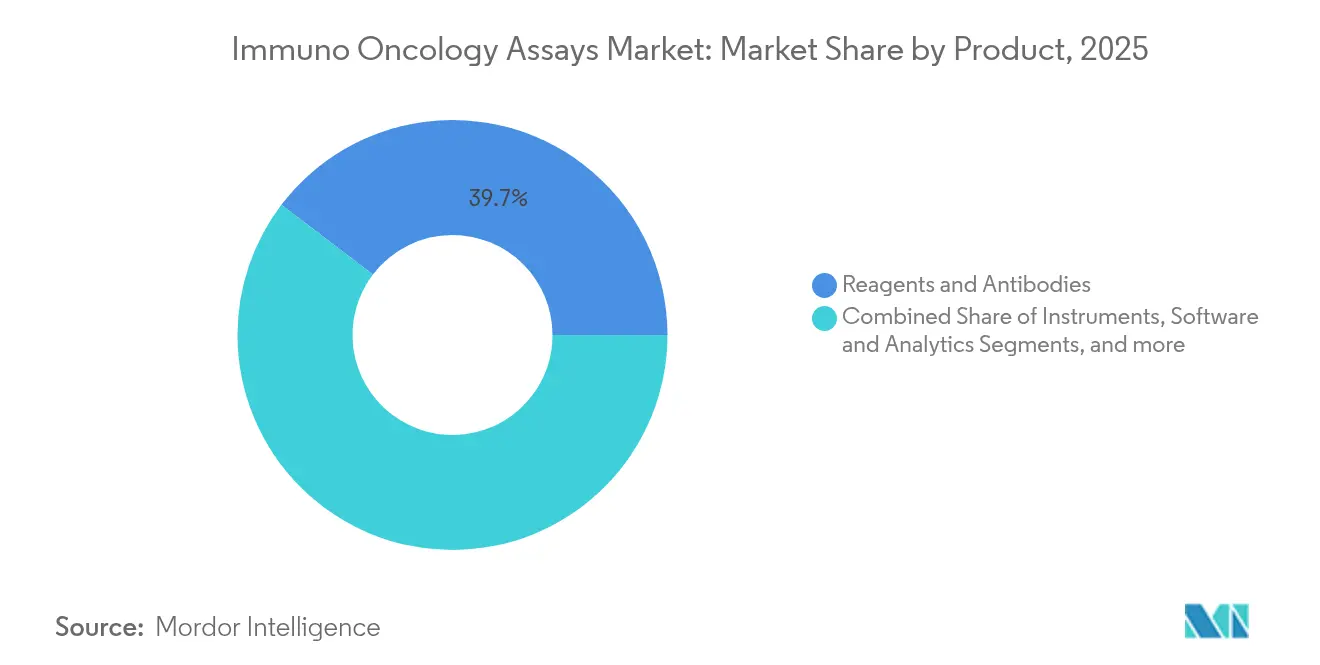

- By product, Reagents & Antibodies led with 39.65% of immuno-oncology assays market share in 2025; Software & Analytics is projected to grow at a 12.41% CAGR through 2031.

- By technology, Next-Generation Sequencing held 37.10% revenue share of the immuno-oncology assays market in 2025, while Multiplex Spatial Profiling is set to expand at a 12.48% CAGR to 2031.

- By assay type, Laboratory-Developed Tests accounted for 50.55% share of the immuno-oncology assays market size in 2025; Companion Diagnostics show the highest forecast CAGR at 12.44% through 2031.

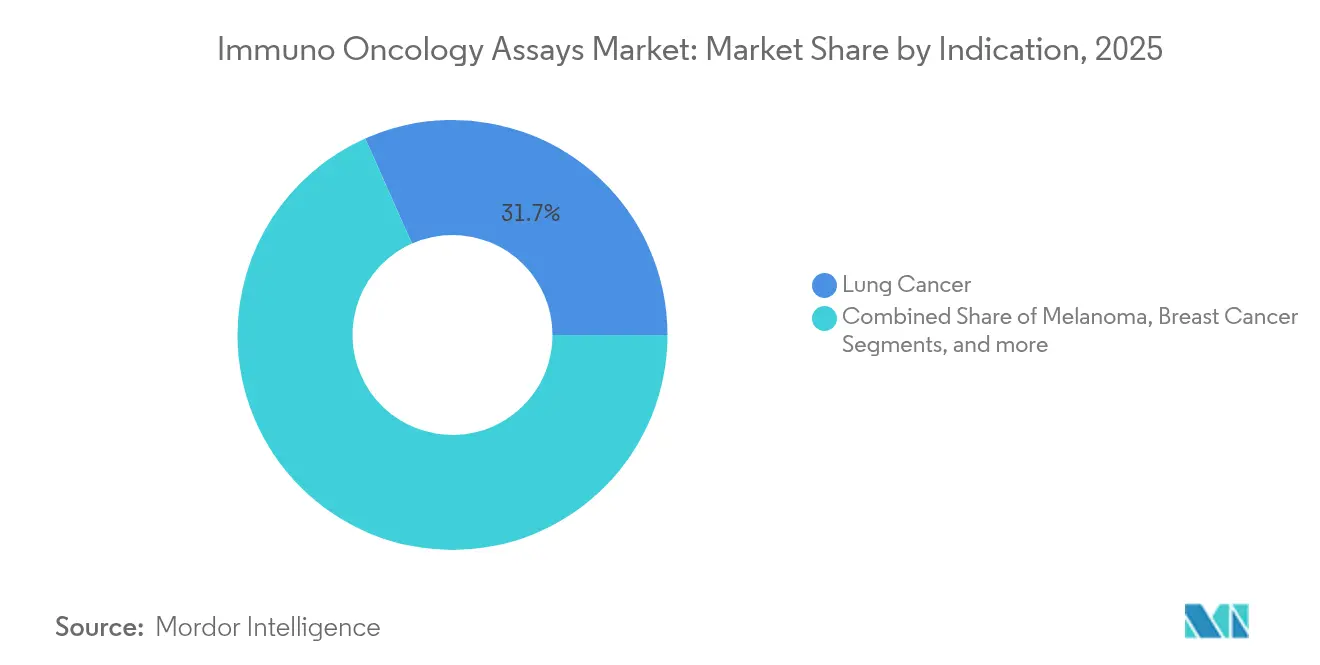

- By indication, Lung Cancer commanded 31.65% of immuno-oncology assays market size in 2025, whereas Breast Cancer is anticipated to grow at a 12.62% CAGR between 2026 and 2031.

- By sample type, Tissue Biopsy retained 52.35% share of the global immuno-oncology assays market in 2025; Liquid Biopsy is expected to post a 12.46% CAGR to 2031.

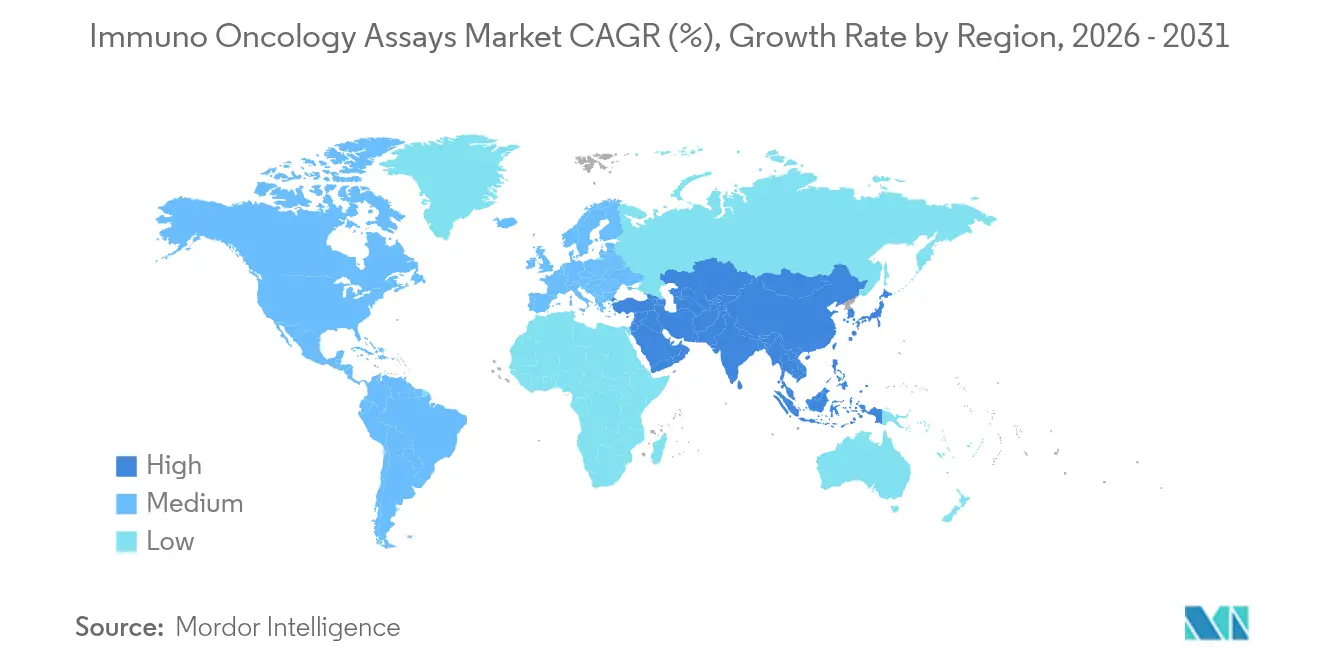

- By geography, North America captured 41.90% of the immuno-oncology assays market in 2025; Asia-Pacific represents the fastest-growing region with a 12.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immuno Oncology Assays Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained rise in global cancer incidence | 2.8% | Global, with highest impact in aging populations of North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Expanding adoption of immune-checkpoint inhibitors | 2.4% | Global, led by North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Regulatory approvals of companion Dx assays (PD-1/PD-L1, TMB) | 2.1% | North America and Europe primarily, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Pharma-Dx co-development partnerships accelerating test menus | 1.9% | Global, concentrated in major pharmaceutical hubs | Medium term (2-4 years) |

| AI-driven multiplex spatial profiling boosting biomarker discovery | 1.7% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Decentralised liquid-biopsy testing in community oncology | 1.2% | North America primarily, with gradual expansion to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Adoption of Immune-Checkpoint Inhibitors

Immune-checkpoint inhibitors reshape the therapeutic landscape, prompting wider deployment of companion tests that gauge PD-L1 status, tumor mutational burden, and microsatellite stability. Multiple FDA approvals in 2025, such as tislelizumab plus chemotherapy for esophageal squamous cell carcinoma and pembrolizumab-trastuzumab for HER2-positive gastric cancer, emphasise the need for robust predictive assays. The Society for Immunotherapy of Cancer lists biomarker panels that now guide routine clinical decision-making. Spatial omics platforms further refine response prediction, enabling multidimensional tumour micro-environment analysis that elevates assay specificity.

AI-Driven Multiplex Spatial Profiling Boosting Biomarker Discovery

Coupling AI with spatial biology technology uncovers cellular interactions previously hidden by conventional approaches. The Garvan Institute’s AAnet tool exemplifies this progress by differentiating five tumour-resident cell types to inform therapeutic strategies. Commercial systems such as the Hyperion XTi Imaging Mass Cytometer visualise 40+ markers simultaneously without autofluorescence noise, fostering deeper biomarker pipelines. Research in Molecular Cancer confirms that high-resolution 3D histology enhances understanding of tumour heterogeneity, accelerating assay innovation.

Regulatory Approvals of Companion Dx Assays (PD-1/PD-L1, TMB)

Recent FDA clearances, including the therascreen KRAS RGQ PCR kit for KRAS G12C mutations and the VENTANA MET (SP44) assay for c-Met expression, underscore a regulatory shift toward multi-parameter diagnostics. Breakthrough device designation for the Ventana TROP2 assay demonstrates how AI-enabled pathology speeds approval cycles. Expanded menus strengthen the immuno-oncology assays market by offering clinicians validated tools that match evolving therapy algorithms.

Pharma-Dx Co-Development Partnerships Accelerating Test Menus

Collaboration between drug developers and assay companies compresses R&D timelines. GeneCentric and Labcorp co-develop RNA gene signatures, marrying large clinical datasets with molecular analytics. Guardant Health and ConcertAI integrate 5.5 million real-world records with epigenomic profiles to refine evidence generation. These alliances reduce the cost and complexity of bringing novel biomarkers to market, expanding the immuno-oncology assays market footprint.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High assay costs & complex reimbursement pathways | -1.8% | Global, most pronounced in cost-sensitive markets and emerging economies | Medium term (2-4 years) |

| Stringent multi-jurisdiction regulatory validation demands | -1.4% | Global, with highest impact in markets requiring multiple regulatory approvals | Long term (≥ 4 years) |

| Scarcity of well-annotated matched tumour/normal biobanks | -1.1% | Global, particularly affecting research-intensive regions | Long term (≥ 4 years) |

| Lack of global standardisation in multiplex assay protocols | -0.9% | Global, with fragmentation most evident in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Assay Costs & Complex Reimbursement Pathways

Sharp increases in Medicare claim denial rates for NGS—from 16.8% to 27.4% in 2025—illustrate tightening US payer scrutiny. Capital investment exceeding USD 500,000 for full spatial-profiling setups further limits diffusion in community settings. Health technology assessments in Europe add 12-18 months to launch timelines, increasing financial risk for smaller developers. Consequently, price-tiering strategies become essential to sustain uptake in cost-sensitive regions.

Stringent Multi-Jurisdiction Regulatory Validation Demands

Divergent criteria among the FDA, EMA, and other regulators elongate validation cycles. Inter-lab coefficient-of-variation above 20% for PD-L1 testing highlights reproducibility hurdles. Organisations such as CIMAC-CIDC continue to explore harmonisation, yet localisation requirements inflate operational overheads. These obstacles temper the otherwise strong growth trajectory of the immuno-oncology assays market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Reagents Dominate, Software Accelerates

Reagents & Antibodies captured 39.65% of the immuno-oncology assays market in 2025, evidencing the consumable-heavy nature of immune testing workflows. Hospital and reference laboratories turn to validated antibody panels to meet SITC-endorsed biomarker requirements. Instruments enjoy steady demand as labs upgrade to imaging-mass-cytometry platforms capable of 40-plus marker detection.

Software & Analytics, projected to post a 12.41% CAGR through 2031, benefits from AI modules that automate cell-phenotype mapping and cloud-based data sharing. The Garvan Institute’s AAnet and similar solutions lower analysis times, creating new revenue streams for digital pathology vendors. This software upsurge diversifies revenue composition within the immuno-oncology assays market.

By Technology: NGS Leads, Spatial Profiling Transforms

Next-Generation Sequencing retained 37.10% share of the immuno-oncology assays market in 2025, remaining indispensable for broad mutational scans. High-depth panel sequencing supports tumour mutational burden calculation, directly guiding checkpoint inhibitor use.

Multiplex Spatial Profiling, forecast to grow at 12.48% CAGR, permits single-cell resolution mapping of protein and RNA markers within intact tissues. Illumina’s whole-transcriptome spatial platform highlights this shift toward context-rich analytics. Immunoassay, PCR, and flow cytometry modalities maintain complementary roles for targeted or high-throughput applications, collectively sustaining technology diversity inside the immuno-oncology assays market.

By Assay Type: LDTs Dominate, CDx Gains Momentum

Laboratory-Developed Tests held 50.55% of immuno-oncology assays market share in 2025, reflecting academic centers’ need for flexible assay design. Custom panels support exploratory research on neo-antigens and immune evasion pathways.

Regulatory acceleration in companion diagnostics fuels a 12.44% CAGR for CDx through 2031. FDA clearance of the VENTANA MET (SP44) assay and similar tests formalises biomarker criteria for therapy eligibility, driving clinical demand. Research-Use-Only panels continue to seed discovery pipelines, indirectly bolstering long-term market vitality.

By Indication: Lung Cancer Leads, Breast Cancer Accelerates

Lung Cancer generated 31.65% of immuno-oncology assays market size in 2025 thanks to established guidelines mandating PD-L1, KRAS, and EGFR profiling. High global incidence rates sustain testing volumes.

Breast Cancer is poised for a 12.62% CAGR as HER2-low, HER2-ultra-low, and immune biomarkers expand clinical decision trees. FDA approval of fam-trastuzumab deruxtecan-nxki, paired with the Ventana PATHWAY anti-HER-2 assay, underscores broader biomarker adoption. Growth across colorectal, melanoma, and other tumour types rounds out indication-level opportunity in the immuno-oncology assays market.

By Sample Type: Tissue Rules, Liquid Biopsy Transforms

Tissue Biopsy accounted for 52.35% share of the immuno-oncology assays market in 2025, supported by well-established protocols and rich histopathology context. Comprehensive tissue profiling remains the clinical gold standard for staging and therapeutic planning.

Liquid Biopsy’s forecast 12.46% CAGR reflects advances in circulating tumour DNA, exosome, and methylation assays. Guardant360 Tissue’s launch, analysing 1,100-plus DNA and RNA genes with 40% less material, exemplifies efficiency gains. Non-invasive monitoring augments, rather than replaces, tissue testing, reinforcing multimodal sampling across the immuno-oncology assays market.

Geography Analysis

North America generated 41.90% of 2025 global revenue through favourable reimbursement, early AI adoption, and dense networks of comprehensive cancer centres. Medicare’s evolving coverage for NGS diagnostics still poses short-term reimbursement uncertainty, but strong private-payer frameworks keep overall growth intact.

Europe maintains balanced progress as health technology assessments verify clinical benefit before wide rollout. EMA’s approval of agents such as tislelizumab shows regional commitment to immunotherapeutic expansion. Although multiple national approval layers can delay diagnostics launches, streamlined EU IVDR-compliant pathways promise to shorten time-to-market after 2026.

Asia-Pacific leads growth at a 12.55% CAGR as China deploys national cancer screening programs and Japan subsidises genomic testing. Emerging precision-medicine hubs in India and South Korea further stimulate demand. Simplified regulatory fast-tracks for innovative devices improve access, giving international suppliers a sizeable addressable base in the immuno-oncology assays market.

Middle East & Africa witnesses incremental uptake as Gulf states invest in oncology centres of excellence and procure multiplex platforms. South America records steady progress, led by Brazil’s public-private oncology partnerships and Argentina’s inclusion of genomic testing in national guidelines. Varying reimbursement coverage still restricts volume but long-term incidence trends underpin latent demand.

Competitive Landscape

The immuno-oncology assays market is moderately consolidated. Thermo Fisher Scientific’s USD 3.1 billion acquisition of Olink integrates high-throughput proteomics with existing NGS kits, reinforcing end-to-end service capability[2]Financial Times, “Thermo Fisher Moves into Proteomics with Olink Deal,” ft.com. Veracyte’s USD 95 million purchase of C2i Genomics extends into minimal residual disease monitoring.

Technology differentiation centres on AI-enabled multiplex imaging and data integration. Owkin’s TLS Detect achieves 97% sensitivity in detecting tertiary lymphoid structures, positioning the firm as a reference for spatial AI analytics[3]Owkin, “TLS Detect: AI Biomarker for Immunotherapy,” owkin.com. Guardant Health’s partnership with ConcertAI merges expansive electronic medical records with molecular data, advancing real-world evidence and payer acceptance.

White-space innovation targets decentralised workflows. Companies such as Mursla Bio focus on extracellular vesicle-based assays tailored for organ-specific signatures, complementing central lab services. Mid-size players leverage ISO-accredited manufacturing and regional distribution to serve hospitals adopting comprehensive immune panels. As clinical utility broadens, market success will favour firms that deliver integrated, regulator-ready, and clinician-friendly solutions.

Immuno Oncology Assays Industry Leaders

Agilent Technologies, Inc

Thermo Fisher Scientific

Illumina, Inc.

PerkinElmer, Inc.

Crown Bioscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: FDA granted accelerated approval to sunvozertinib (Zegfrovy) for metastatic NSCLC with EGFR exon 20 insertions; Oncomine Dx Express Test approved as companion diagnostic.

- May 2025: Roche obtained FDA approval for VENTANA MET (SP44) RxDx assay as first companion diagnostic for MET protein in non-squamous NSCLC.

- April 2025: Ventana TROP2 (EPR20043) RxDx assay received breakthrough device designation for datopotamab deruxtecan selection in NSCLC.

- April 2025: Guardant Health launched Guardant360 Tissue multiomic profiling test analysing 742 DNA and 367 RNA genes while using fewer slides.

Global Immuno Oncology Assays Market Report Scope

As per the scope of the report, Immuno oncology assays is a next-generation sequencing application that delivers real-time automated measurements of immune and tumor cell dynamics. With the help of this assay, people can analyze biological processes driving the immune response against cancer. It helps continuously examine and analyze key events from proliferation and activation to migration and immune cell killing without disturbing the existing body cells. The Immuno Oncology Assays Market is segmented by product (reagents and antibodies, instruments, software and consumables, and accessories), technology (immunoassay, PCR, NGS, Flow Cytometry, and other technologies), indication (lung cancer, colorectal cancer, Melanoma, and other cancers) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value in (USD million) for the above segments.

| Reagents & Antibodies |

| Instruments |

| Software & Analytics |

| Consumables & Accessories |

| Immunoassay (ELISA, CLIA) |

| Polymerase Chain Reaction (PCR/qPCR/ddPCR) |

| Next-Generation Sequencing (NGS) |

| Flow Cytometry |

| Multiplex Spatial Profiling (mIF, IMC, DSP) |

| Companion Diagnostic (CDx) Assays |

| Laboratory-Developed Tests (LDTs) |

| Research-Use-Only (RUO) Panels |

| Lung Cancer |

| Colorectal Cancer |

| Melanoma |

| Breast Cancer |

| Other Cancers |

| Tissue Biopsy |

| Liquid Biopsy (Blood, Plasma, cfDNA) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Reagents & Antibodies | |

| Instruments | ||

| Software & Analytics | ||

| Consumables & Accessories | ||

| By Technology | Immunoassay (ELISA, CLIA) | |

| Polymerase Chain Reaction (PCR/qPCR/ddPCR) | ||

| Next-Generation Sequencing (NGS) | ||

| Flow Cytometry | ||

| Multiplex Spatial Profiling (mIF, IMC, DSP) | ||

| By Assay Type | Companion Diagnostic (CDx) Assays | |

| Laboratory-Developed Tests (LDTs) | ||

| Research-Use-Only (RUO) Panels | ||

| By Indication | Lung Cancer | |

| Colorectal Cancer | ||

| Melanoma | ||

| Breast Cancer | ||

| Other Cancers | ||

| By Sample Type | Tissue Biopsy | |

| Liquid Biopsy (Blood, Plasma, cfDNA) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the immuno-oncology assays market by 2031?

The market is forecast to reach USD 11.87 billion by 2031, advancing at a 11.88% CAGR.

Which product category contributes the most revenue today?

Reagents & Antibodies lead with 39.65% of global revenue, reflecting the consumable-intensive nature of immune profiling workflows.

What technology segment is growing the fastest?

Multiplex spatial profiling is expanding at a 12.48% CAGR as laboratories adopt single-cell, context-rich analysis platforms.

Why are companion diagnostics gaining momentum?

Recent FDA approvals for assays targeting MET, KRAS G12C, and TROP2 validate multi-parameter testing and are pushing the companion diagnostic segment toward a 12.44% CAGR.

How significant is liquid biopsy to future growth?

Liquid biopsy tests, used for non-invasive monitoring of circulating tumor DNA, are expected to grow at a 12.46% CAGR and complement tissue-based assays.

Which region offers the highest growth potential?

Asia-Pacific is projected to post a 12.55% CAGR through 2031, driven by rising cancer incidence, expanding screening programs, and streamlined regulatory pathways.

Page last updated on: