PCSK9 Inhibitor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

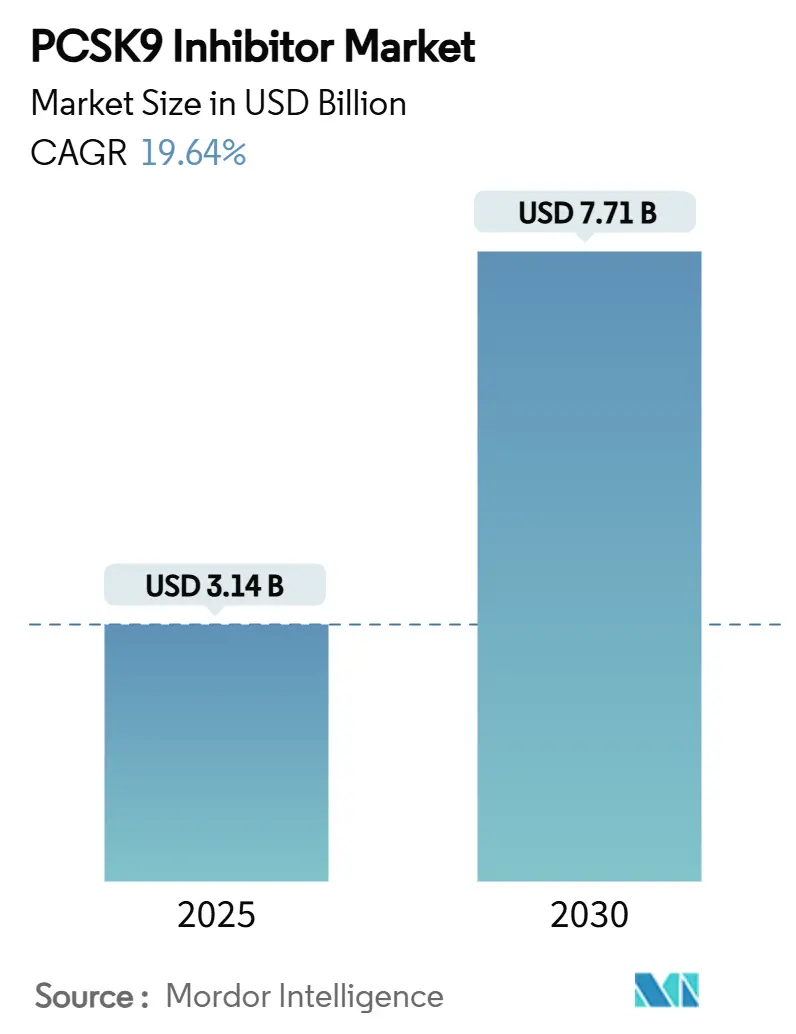

| Market Size (2025) | USD 3.14 Billion |

| Market Size (2030) | USD 7.71 Billion |

| Growth Rate (2025 - 2030) | 19.64% CAGR |

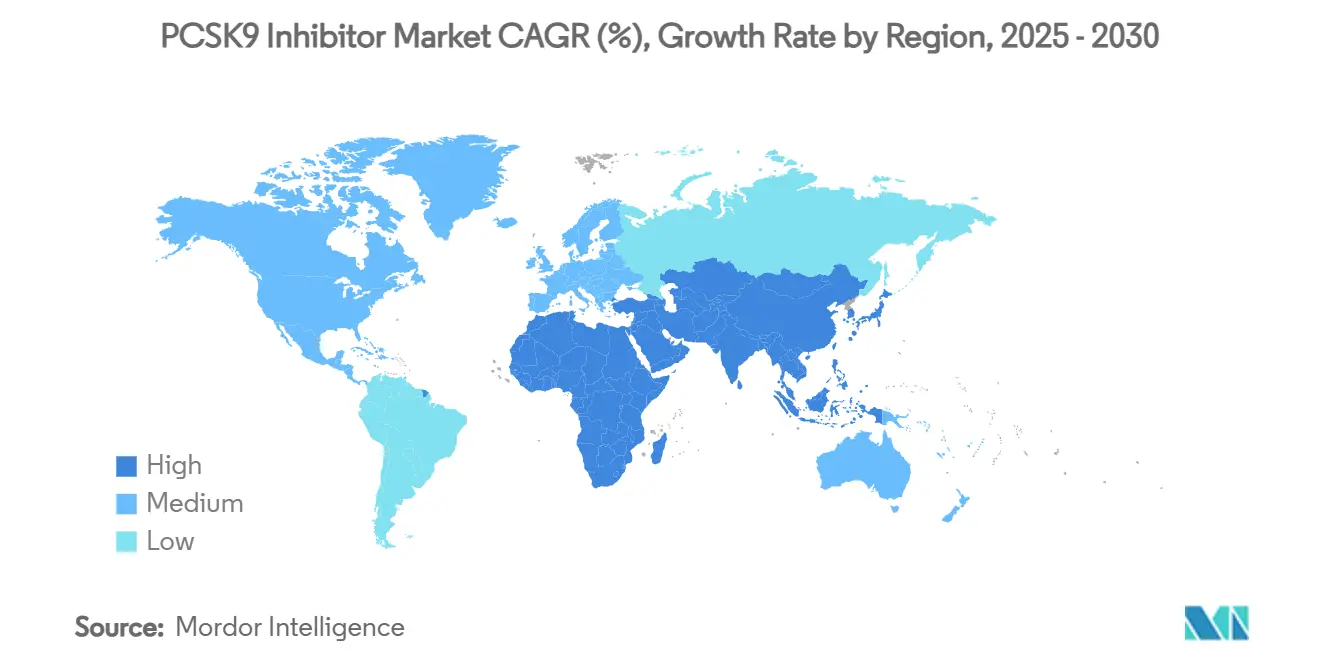

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PCSK9 Inhibitor Market Analysis by Mordor Intelligence

Current estimates place the PCSK9 inhibitor market size at USD 3.14 billion in 2025 and forecast its value to reach USD 7.71 billion by 2030, expanding at a 19.64% CAGR over the period under review. Uptake accelerates because precision lipid-management approaches now complement traditional statins, genetic screening uncovers far more familial hypercholesterolemia cases than earlier thought, and physician confidence rises on the back of longer-term cardiovascular-outcome data. Monoclonal antibodies still dominate revenue, yet RNA-interference options such as inclisiran are reshaping adherence expectations with twice-yearly dosing. Demand also benefits from employer-led value-based contracts, growing digital pharmacy ecosystems, and supportive guideline updates that tighten LDL-C targets. In parallel, payers and providers explore innovative contracting to balance high therapy efficacy with budget impact, while manufacturers prepare for biosimilar pressure as core patents expire.

Key Report Takeaways

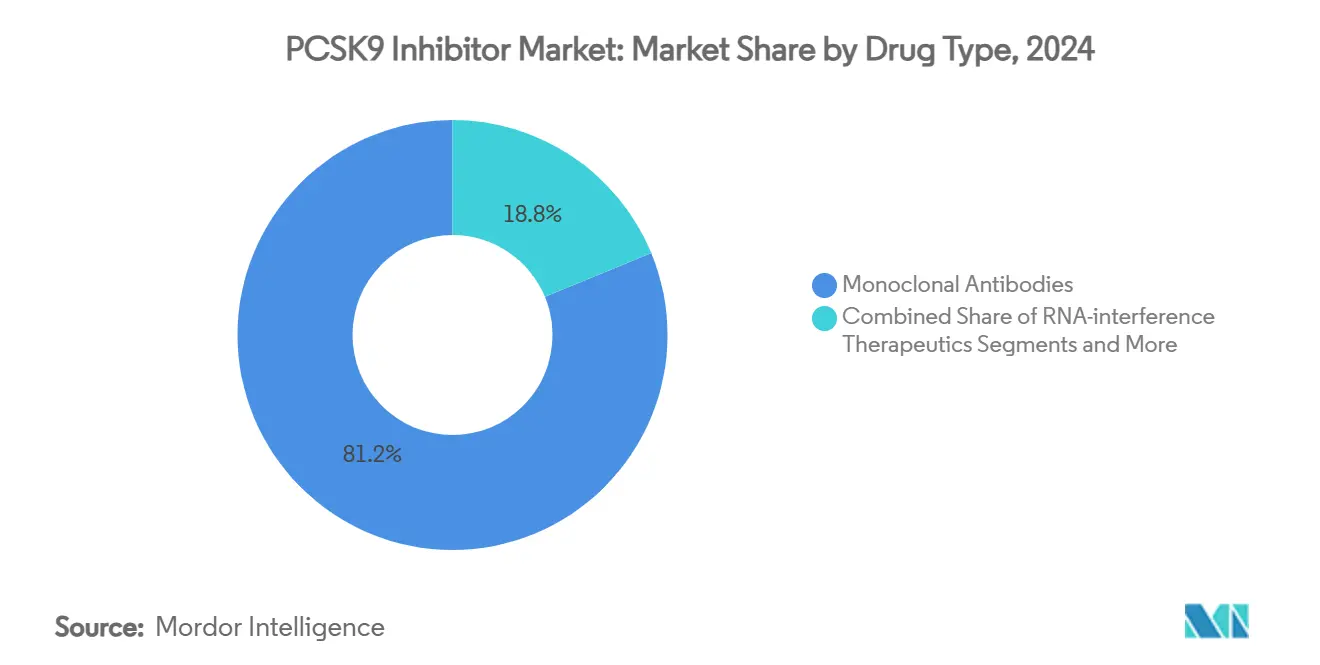

- By drug type, monoclonal antibodies led with 81.23% of PCSK9 inhibitor market share in 2024, whereas RNA-interference therapeutics are projected to grow at a 23.69% CAGR through 2030.

- By route of administration, subcutaneous injection accounted for 88.77% of the PCSK9 inhibitor market size in 2024 and is forecast to post a 21.47% CAGR to 2030.

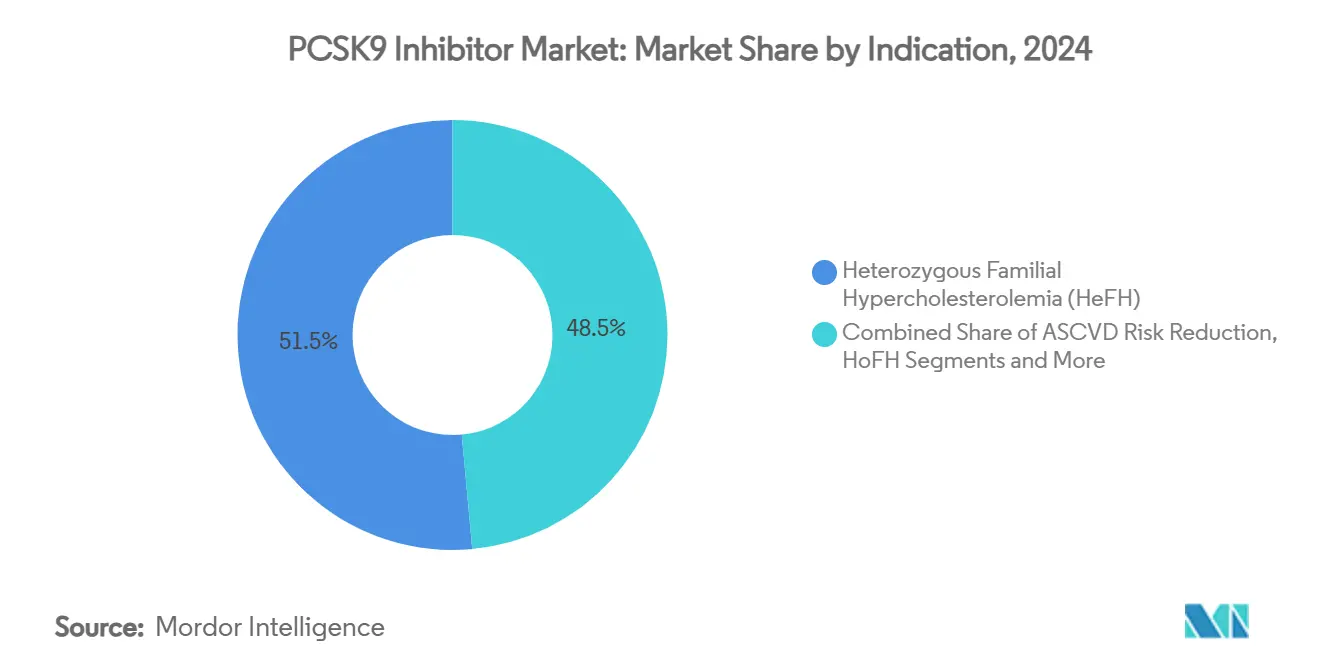

- By indication, heterozygous familial hypercholesterolemia captured 51.46% revenue share in 2024; homozygous familial hypercholesterolemia is set to advance at a 22.12% CAGR through 2030.

- By distribution channel, hospital pharmacies held 44.38% of the PCSK9 inhibitor market share in 2024, while online pharmacies are advancing at a 21.89% CAGR through 2030.

- By geography, North America retained 46.59% share in 2024, whereas Asia-Pacific is on track for a 22.13% CAGR over the forecast horizon.

Global PCSK9 Inhibitor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Familial Hypercholesterolemia & Uncontrolled LDL-C | +3.2% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Escalating Cardiovascular Morbidity & Tighter Guideline LDL-C Targets | +2.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| Positive Long-Term Outcome Data Boosting Physician Confidence | +2.1% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Improved Dosing Regimens (E.G., Twice-Yearly Inclisiran) Raising Adherence | +1.9% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Employer Value-Based Contracts Accelerating Payer Uptake | +1.4% | North America core, expanding to EU | Medium term (2-4 years) |

| AI-Driven Lipidomics Expanding Eligible Patient Pools | +1.1% | APAC core, spill-over to developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising FH Prevalence & Uncontrolled LDL-C

Genetic testing now shows familial hypercholesterolemia in 1 in 16 patients with premature coronary artery disease compared with historic 1 in 600 estimates.[1]Antti Jokiniitty, “Genetic Testing for Familial Hypercholesterolemia in a Finnish Cohort of Patients With Premature Coronary Artery Disease and Elevated LDL-C Levels,” Frontiers in Cardiovascular Medicine, frontiersin.org Universal pediatric screening advocated by the US National Heart, Lung, and Blood Institute broadens early detection, while regional consensus statements highlight that fewer than 1% of eligible patients currently receive therapy.[2]Mirna Mamdouh Shaker, “2024 Egyptian Consensus Statement on the Role of Non-Statin Therapies for LDL Cholesterol Lowering in Different Patient Risk Categories,” Egypt Heart Journal, ejhij.org Enhanced AI-enabled lipidomics and wider access to direct-to-consumer gene panels therefore expand the PCSK9 inhibitor market by identifying high-risk cohorts earlier and more accurately.

Escalating Cardiovascular Morbidity & Tighter LDL-C Targets

New clinical pathways from the American College of Cardiology recommend PCSK9 inhibitors for very-high-risk patients when LDL-C remains above guideline limits despite maximally tolerated statins.[3]American College of Cardiology Task Force, “2024 ACC Consensus Decision Pathway for the Management of LDL Cholesterol,” American College of Cardiology, acc.org Australia’s reimbursement threshold recently shifted downward, reflecting a global move toward aggressive targets that promote earlier initiation. Meta-analyses confirm an extra 15% cardiovascular-event reduction beyond statin therapy, reinforcing the notion that intensive lipid lowering is clinically worthwhile.

Positive Long-Term Outcome Data Boosting Physician Confidence

Four-year follow-up of FOURIER-OLE shows sustained benefit in elderly patients with no safety compromises.[4]Robert Giugliano, “Long-Term Evolocumab in Elderly Patients,” Journal of the American College of Cardiology, jacc.org Independent cognitive data dispel concerns around very low LDL-C, while real-world Asia-Pacific studies align with pivotal trials on durability of effect. Together these findings remove historical hesitancy and encourage wider specialist adoption, supporting the PCSK9 inhibitor market expansion.

Improved Twice-Yearly Dosing Regimens Raising Adherence

Inclisiran demonstrated a 46.5% LDL-C drop with just two injections per year versus 11.2% for ezetimibe in primary prevention settings. Real-world Italian cohorts reached guideline targets within one month, and global manufacturing scale-up underpins supply reliability. Reduced dosing frequency addresses major adherence obstacles, which is particularly important as patients now often require lifelong therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy Cost & Strict Reimbursement Prior-Authorizations | -4.1% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Emerging Oral/Bempedoic & Gene Therapies Intensifying Competition | -2.3% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Cold-Chain & Autoinjector Logistics In Low-Income Regions | -1.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Long-Term Neuro-Cognitive Safety Concerns | -1.2% | Global, higher impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Strict Prior Authorizations

Despite 60% price cuts, payer rejection rates remain near 31% in the United States. Complex documentation requirements slow initiation, and cost-effectiveness models indicate substantial additional discounts are needed in price-sensitive markets like China. These factors keep utilization far below eligibility levels even when clinical benefit is clear, limiting overall PCSK9 inhibitor market penetration.

Emerging Oral and Gene-Based Competitors

Phase IIb oral PCSK9 candidates from Merck and AstraZeneca show ≥50% LDL-C reductions. Bempedoic acid already offers oral convenience at a lower price point, while gene-silencing platforms targeting lipoprotein(a) approach late-stage trials. As these modalities progress, they may redirect share away from injectable options and moderate the PCSK9 inhibitor market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: RNA-Interference Therapies Gain Momentum

Monoclonal antibodies held an 81.23% PCSK9 inhibitor market share in 2024, yet RNA-interference agents are positioned for a 23.69% CAGR to 2030. Clinical convenience drives this shift, with inclisiran delivering a biannual regimen that yields a 56.9% mean LDL-C reduction within a month of first dose. The PCSK9 inhibitor market size tied to small-molecule oral candidates is set to unlock once regulatory approvals arrive, potentially widening patient reach among those averse to injections. Competitive narratives increasingly revolve around administration ease rather than efficacy alone, and third-generation constructs such as lerodalcibep promise monthly self-administration with 50%-plus LDL-C reductions.

The existing antibody franchise remains resilient on the back of proven cardiovascular-outcome data and first-mover advantage, yet portfolio diversification toward RNA and oral categories signals a maturing innovation cycle. Manufacturers are also pursuing differentiated value propositions that bundle therapy with adherence apps, coaching, and co-pay assistance to cement brand loyalty in the PCSK9 inhibitor market.

By Route of Administration: Subcutaneous Today, Oral Tomorrow

Subcutaneous injection secured 88.77% share of the PCSK9 inhibitor market size in 2024, driven by autoinjector familiarity among specialists. However cold-chain logistics pose hurdles; antibodies can lose potency after 9 hours above room temperature. Inclisiran mitigates frequency burdens but not refrigeration needs, leaving open space for ambient-stable oral tablets now in late-phase testing. The PCSK9 inhibitor market anticipates oral entrants from 2027 onward, with Merck’s MK-0616 already showing 60% LDL-C cuts in Phase IIb. Intravenous formats stay niche, mostly in clinical-trial environments.

Broader patient choice is expected to raise overall adoption rather than cannibalize usage because oral, twice-yearly, and monthly options target distinct compliance obstacles. This multi-modal landscape aligns with payer preferences for tiered formularies in which injectable and oral rebates can be negotiated separately, reinforcing competitive intensity within the PCSK9 inhibitor market.

By Indication: HoFH Growth Outpaces HeFH Base

Heterozygous familial hypercholesterolemia contributed 51.46% revenue in 2024, reflecting its higher prevalence, yet homozygous familial hypercholesterolemia commands a 22.12% CAGR that will increasingly reshape specialty focus. Recent FDA expansion of alirocumab to children aged 8 and above creates earlier lifelong treatment pathways. In the broader atherosclerotic cardiovascular disease prevention arena, the VICTORION-1 PREVENT program could add 22 million US adults to the eligible pool, amplifying the PCSK9 inhibitor market size for primary prevention. Molecular diagnosis now often guides therapy selection, so drug makers invest in companion genetic-testing partnerships to secure share among newly identified extreme-risk patients.

Rare dyslipidemias remain a minor slice of revenue but benefit indirectly as more physicians familiarize themselves with PCSK9 biology. Future growth in these sub-groups hinges on further label expansions and real-world evidence demonstrating outcome benefit beyond LDL-C lowering.

By Distribution Channel: Shift Toward Digital Fulfillment

Hospital pharmacies retained 44.38% of PCSK9 inhibitor market share in 2024 because prior authorization paperwork is typically coordinated in the inpatient or specialist-clinic setting. Nevertheless online dispensing platforms are tracking a 21.89% CAGR to 2030 as virtual cardiology visits normalize and specialty pharmacies refine remote cold-chain delivery. Retail pharmacies occupy an intermediary role, offering walk-in injection training and on-site adherence counseling, thereby supporting patient confidence in self-administration.

Manufacturers amplify digital engagement through integrated support programs that schedule reminder texts, coordinate lab work, and streamline insurance appeals. These services will remain pivotal for capturing underserved populations once oral SKUs launch, potentially enabling direct-to-patient models that further expand the PCSK9 inhibitor market.

Geography Analysis

North America commands 46.59% of 2024 revenue, anchored by experienced lipidologists, extensive insurance coverage, and brisk uptake of guideline updates. Even so, rejection rates near 31% illustrate a balancing act between clinical innovation and payer cost controls. Employer coalitions warn that widespread use could translate into USD 23 billion of incremental pharmacy spend, prompting experimentation with value-based contracts that tie reimbursement to LDL-C targets. Domestic manufacturing commitments such as AstraZeneca’s USD 50 billion investment underscore long-term confidence in a stable policy climate.

Asia-Pacific posts the fastest advance at 22.13% CAGR, buoyed by rising cardiovascular risk and improved insurance penetration. Real-world HALES data confirm therapy effectiveness, strengthening physician willingness to prescribe in diverse ethnic groups. Yet affordability barriers persist; cost-effectiveness modeling in China suggests inclisiran requires price cuts exceeding 88% to meet local thresholds. Cold-chain gaps further slow expansion of injectable lines, making the region an early adopter candidate for oral formulations once approved.

Europe maintains steady growth under the umbrella of robust public health systems. ESC/EAS guidelines recommend LDL-C below 1.4 mmol/L for very-high-risk patients, fostering specialist support, though reimbursement criteria may still lag in some countries. Novartis’ CHF 70 million Swiss facility secures regional supply of inclisiran, while national funding bodies debate how best to align budget constraints with outcome evidence. The Middle East and Africa show under-1% utilization today but offer sizeable upside as diagnostic infrastructure matures and biosimilar pricing materializes.

Competitive Landscape

Market concentration is moderate. Amgen’s evolocumab and Sanofi/Regeneron’s alirocumab together account for most historical sales, but RNA-interference rival inclisiran, oral candidates, and new protein scaffolds dilute that dominance. Patent expiries between 2030-2031 open the door to biosimilars, pressuring incumbent pricing. Legal battles over rebate bundling, highlighted by Regeneron’s USD 406.8 million antitrust victory, illustrate competitive friction around access strategy.

Strategic moves emphasize manufacturing scale and convenience. Novartis is spending CHF 70 million to broaden inclisiran output in Europe, while AstraZeneca earmarks USD 50 billion to establish US production of oral PCSK9 assets. LIB Therapeutics seeks first-in-class approval for the monthly adnectin lerodalcibep, pitching a differentiated profile to clinicians and payers. Pediatric indications create fresh battlegrounds; alirocumab secured the first label for children aged 8+ with heterozygous FH, positioning Regeneron and Sanofi as early movers in a long-duration segment.

Overall, rivalry is expected to intensify as delivery modalities proliferate and payer scrutiny sharpens. Success will hinge on demonstrating real-world outcome benefits, convenient dosing, and clear value propositions to gatekeepers who ultimately mediate broad access in the PCSK9 inhibitor market.

PCSK9 Inhibitor Industry Leaders

Innovent Biologics

Amgen

Sanofi

Novartis

Eli Lilly & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AstraZeneca confirmed a USD 50 billion US manufacturing and R&D plan covering oral PCSK9 inhibitors and other metabolic drugs.

- February 2025: FDA accepted LIB Therapeutics’ BLA for lerodalcibep targeting LDL-C reduction in ASCVD and genetic hypercholesterolemia populations.

- March 2024: Praluent gained FDA approval for children aged 8+ with heterozygous familial hypercholesterolemia, marking the first pediatric label in the class.

Global PCSK9 Inhibitor Market Report Scope

| Monoclonal Antibodies |

| RNA-interference Therapeutics |

| Small-Molecule/Oral PCSK9 Inhibitors |

| Subcutaneous Injection |

| Oral |

| Intravenous |

| Heterozygous Familial Hypercholesterolemia (HeFH) |

| Homozygous Familial Hypercholesterolemia (HoFH) |

| ASCVD Risk Reduction |

| Other Dyslipidemias |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Monoclonal Antibodies | |

| RNA-interference Therapeutics | ||

| Small-Molecule/Oral PCSK9 Inhibitors | ||

| By Route of Administration | Subcutaneous Injection | |

| Oral | ||

| Intravenous | ||

| by Indication | Heterozygous Familial Hypercholesterolemia (HeFH) | |

| Homozygous Familial Hypercholesterolemia (HoFH) | ||

| ASCVD Risk Reduction | ||

| Other Dyslipidemias | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the PCSK9 inhibitor space be by 2030?

Forecasts point to USD 7.71 billion in 2030, up from USD 3.14 billion in 2025.

Which therapeutic class is expanding fastest within PCSK9 inhibition?

RNA-interference options are on track for a 23.69% CAGR through 2030.

What makes Asia-Pacific the quickest-growing geography?

Rising cardiovascular risk, broader insurance coverage and improving guideline alignment support a 22.13% CAGR.

How does twice-yearly dosing improve real-world adherence?

Inclisiran’s two-dose schedule has delivered a 56.9% LDL-C reduction within one month in clinical practice, reducing injection fatigue.

What competitive shift is expected once current patents expire?

Biosimilars could launch after 2030-2031 antibody patent expiries, heightening price competition.

Which single barrier most limits wider uptake today?

High therapy cost coupled with strict prior-authorization rules still rejects nearly 31% of prescriptions in the United States.

Page last updated on: