Gabapentin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

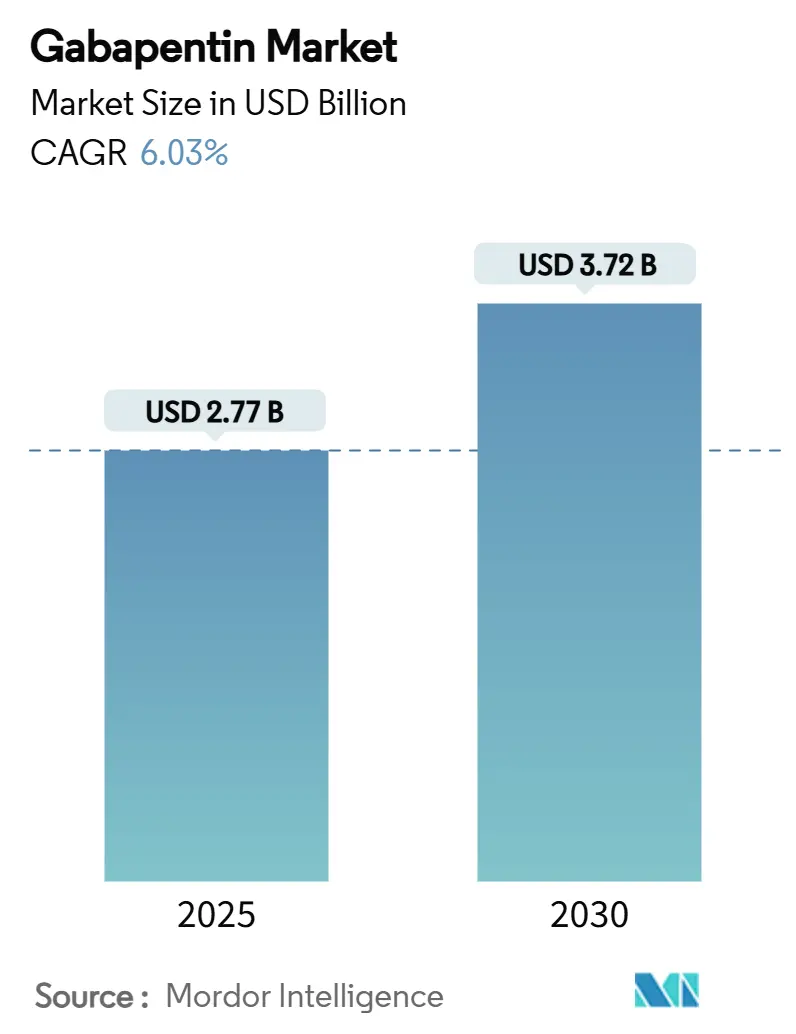

| Market Size (2025) | USD 2.77 Billion |

| Market Size (2030) | USD 3.72 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

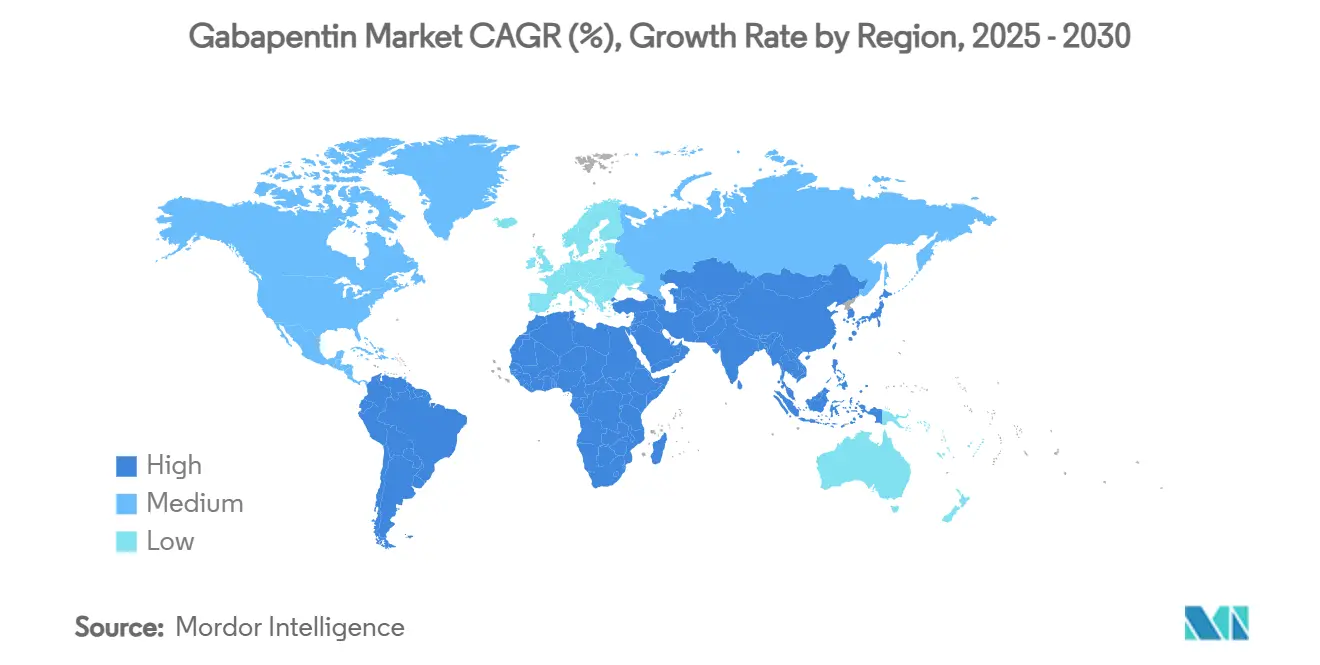

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gabapentin Market Analysis by Mordor Intelligence

Gabapentin market size reached USD 2.77 billion in 2025 and is forecast to touch USD 3.72 billion by 2030, translating into a 6.03% CAGR over the period. Momentum rests on the molecule’s widening therapeutic reach, a growing appetite for opioid-sparing regimens, and the advantage of remaining a non-controlled substance in most jurisdictions despite isolated state-level scheduling moves in the United States.[1]North Carolina Medical Board, “Gabapentin Added to NC’s PDMP,” ncmedboard.org Capsules commanded 51.23% revenue in 2024, yet extended-release tablets are expanding fastest at 9.38% CAGR as clinicians gravitate to once-daily dosing that improves adherence. Post-herpetic neuralgia held 32.57% gabapentin market share in 2024, while restless leg syndrome leads growth at 8.90% CAGR after 2024 guidelines promoted the drug to first-line status. North America remained the largest territory with 37.43% share on the back of mature prescribing norms, but Asia-Pacific is the growth engine, advancing 8.67% CAGR thanks to regulatory harmonisation and next-generation gabapentinoids such as mirogabalin securing Chinese approval in 2024. Competitive pressure intensifies as generic manufacturers face price erosion, extended-release entrants pursue premium niches, and digital pharmacy channels scale at 10.44% CAGR on the back of investments in e-commerce and tele-health integration.

Key Report Takeaways

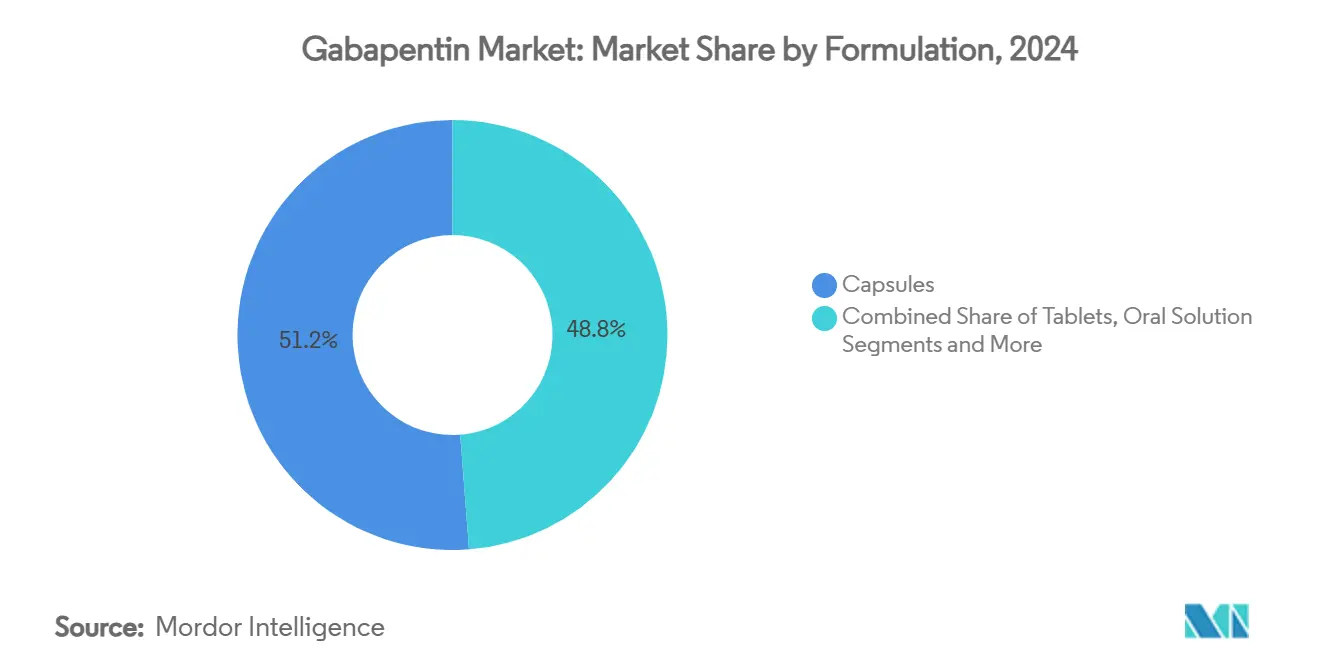

- By formulation, capsules secured 51.23% of gabapentin market share in 2024, whereas extended-release tablets are projected to register the strongest 9.38% CAGR through 2030.

- By indication, post-herpetic neuralgia led with 32.57% revenue share in 2024, while restless leg syndrome is poised to accelerate at an 8.90% CAGR to 2030.

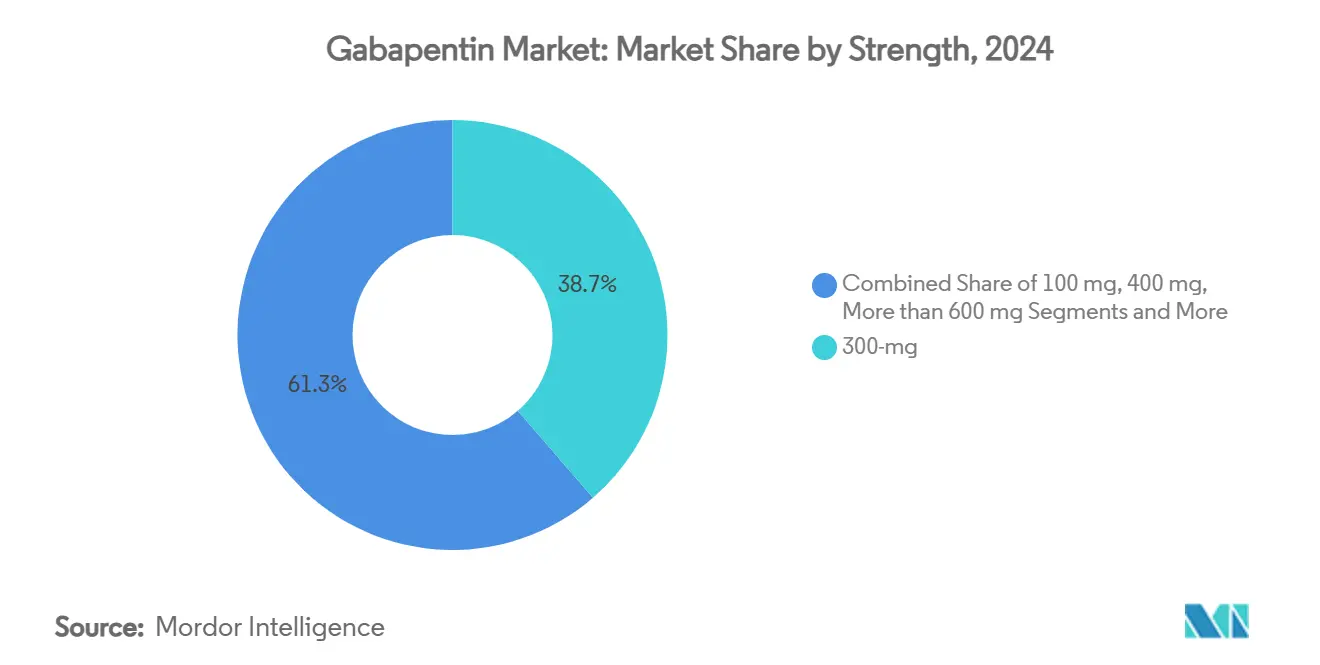

- By strength, the 300 mg segment accounted for 38.66% of the gabapentin market size in 2024; high-dose ≥600 mg formats are forecast to expand at 10.08% CAGR over 2025-2030.

- By distribution channel, retail pharmacies controlled 47.68% of 2024 sales, yet online and mail-order outlets are advancing at a 10.44% CAGR through 2030.

- North America held 37.43% of global value in 2024; Asia-Pacific is anticipated to post the fastest 8.67% CAGR during the outlook period.

Global Gabapentin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neuropathic pain | +1.2% | Global, concentrated in aging populations of North America & Europe | Long term (≥ 4 years) |

| Growing off-label prescribing as an opioid-sparing alternative | +1.8% | North America & Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Aging population increasing epilepsy incidence | +0.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| High demand growth in lower-middle-income countries | +1.1% | Asia-Pacific core, spill-over to Middle East & Africa, Latin America | Medium term (2-4 years) |

| Emerging sustained-/extended-release formulations | +0.9% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of digital & mail-order pharmacies | +0.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neuropathic Pain

Neuropathic pain workloads climb as diabetes and shingles rates rise among aging cohorts, pushing demand for cost-effective therapy. Controlled trials report gabapentin cutting postoperative pain scores by 2.75 points two hours after surgery, reinforcing its appeal beyond anticonvulsant use.[2]Li-Wei Chen, “The Efficacy of Gabapentin Supplementation for Pain Control,” Medicine (Lippincott Williams & Wilkins), lww.comDeveloping markets adopt the molecule quickly because generic pricing undercuts branded alternatives, while physicians trust its well-characterised safety profile relative to opioids. Together, demographic change and robust evidence make neuropathic pain the primary engine powering the gabapentin market.

Growing Off-Label Prescribing as an Opioid-Sparing Alternative

An estimated 96.1% of U.S. gabapentin scripts fall outside the FDA label, reflecting clinician urgency to curb opioid exposure. Real-world analyses show average postoperative opioid consumption falling 3.51 mg when gabapentin is added to multimodal regimens. The FDA’s January 2025 nod to suzetrigine underscores regulators’ interest in non-opioid approaches, although new safety advisories covering suicidal ideation and withdrawal symptoms compel balanced risk–benefit decisions.

Aging Population Increasing Epilepsy Incidence

Rising life expectancy uncovers latent seizure disorders, cementing steady demand for gabapentin’s original indication. Elderly patients value minimal drug–drug interactions, while guidelines sustain the molecule as an adjunct for partial-onset seizures. This foundational use buffers volatility elsewhere in the gabapentin market.

High Demand Growth in Lower-Middle-Income Countries

Regulatory streamlining and industrial expansion push Asia-Pacific demand. China’s 2024 launch of mirogabalin illustrates regional openness to gabapentinoids, and Aurobindo’s new Pen-G plant in Andhra Pradesh boosts active-ingredient self-sufficiency. Broader insurance coverage means patients who once lacked access now receive chronic pain therapy, expanding the gabapentin market size.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory scrutiny & scheduling | -1.5% | North America with potential spill-over elsewhere | Short term (≤ 2 years) |

| Generic price erosion squeezing manufacturer margins | -1.1% | Global, most intense in North America & Europe | Medium term (2-4 years) |

| Evidence gaps for off-label chronic-pain efficacy | -0.7% | Global | Medium term (2-4 years) |

| Rising reports of misuse, diversion & adverse events | -0.9% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Scrutiny & Scheduling

Patchwork state-level rules see Michigan briefly classify gabapentin as Schedule V in January 2025 before reversing in April, while Utah requires controlled-substance licences, creating paperwork burden. CDC data showing the drug in 9.7% of overdose deaths fuels oversight concerns.[3]Centers for Disease Control and Prevention, “Trends in Gabapentin Detection and Overdose Deaths,” cdc.govUncertainty disrupts supply planning and could shift prescribing toward unscheduled alternatives.

Generic Price Erosion Squeezing Manufacturer Margins

With dozens of approved suppliers, U.S. wholesale prices decline annually. Viatris flagged “low- to mid-single-digit” sales erosion in 2025, echoing a sector-wide squeeze. Firms pursue complex generics and extended-release innovations to restore profitability, yet these demand higher R&D spend and carry longer regulatory cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Extended-release innovation outpaces legacy formats

Capsules captured 51.23% of the gabapentin market share in 2024, reflecting decades of clinician familiarity and streamlined manufacturing economics. Extended-release tablets, however, are projected to advance at a 9.38% CAGR through 2030, the fastest among all dosage forms, as once-daily dosing improves adherence and mitigates the saturable absorption that limits immediate-release bioavailability. This shift reallocates a growing slice of the gabapentin market size toward technologies that embed swellable polymers and gastro-retentive matrices, allowing steady plasma levels without increasing pill burden. Oral solutions and topical compounded gels hold niche positions for paediatric, geriatric or localised neuropathic-pain use, sustaining a small but steady revenue stream.

Competition intensifies as Camber’s January 2025 launch of generic Gralise undercuts branded prices, while pending 2025–2026 patent expiries for Horizant invite further generic entrants. The higher technical barrier to produce controlled-release beads and bilayer tablets protects margins compared with commoditised capsules, but scale players must still counter generic price erosion through process efficiencies and targeted physician outreach. Manufacturers pairing extended-release products with automated digital-pharmacy refills gain an extra adherence boost that supports formulary positioning. Over the forecast period, sustained-release options are set to narrow the volume gap with immediate-release capsules, gradually redefining prescribing norms within key neuropathic-pain protocols.

By Indication: Restless-leg guidelines reshape therapeutic hierarchy

Post-herpetic neuralgia accounted for 32.57% of 2024 revenue, underscoring its entrenched place in pain management algorithms. The American Academy of Sleep Medicine’s 2024 upgrade of gabapentin to first-line status catapults restless leg syndrome to an 8.90% CAGR—the fastest among tracked conditions—and reorders demand priorities. Diabetic peripheral neuropathy expands in parallel with global diabetes prevalence, adding incremental volume, while epilepsy remains a stable core that anchors baseline utilisation as populations age. Off-label back and musculoskeletal pain treatments contribute high prescription counts despite contested efficacy, reinforcing the molecule’s versatility.

Horizant’s indication-specific pharmacokinetics strengthen restless-leg positioning just as dopamine agonists face augmentation concerns, prompting prescribers to transition patients who require long-term control. Comparative analyses show gabapentin’s tolerability advantage over pregabalin, appealing to geriatric cohorts wary of dizziness and weight gain. Yet emerging sodium-channel modulators such as suzetrigine threaten acute-pain share, forcing manufacturers to defend neurologic niches through continued real-world evidence generation. Collectively, indication dynamics suggest a gradual redistribution of the gabapentin market size toward sleep-related and diabetic neuropathies while maintaining a resilient epilepsy foundation.

By Strength: High-dose formats consolidate pill burden

The 300 mg strength represented 38.66% of global revenue in 2024, an optimal midpoint for titration across most chronic regimens. High-dose ≥600 mg tablets are forecast to expand at 10.08% CAGR to 2030 after Strides Pharma’s 2025 FDA approval enabled broader U.S. access. These strengths let clinicians reach 1,800 - 3,600 mg daily targets with fewer units, lifting adherence and shrinking dispensing fees for payers.

Absorption ceilings mean bioavailability plateaus at higher doses, so manufacturers increasingly pair large strengths with extended-release matrices that prolong gastric residence and smooth plasma peaks. Custom compounding meets specialised demand for strengths outside commercial ranges, especially in refractory neuropathic-pain clinics. Supply resilience remains critical; Teva’s 800 mg shortage in early 2025 prompted pharmacies to pivot to alternative suppliers, revealing the strategic value of diversified high-strength portfolios. Over the outlook period, large-format doses should gain share in hospital protocols and long-term-care settings where tablet load directly affects nursing efficiency.

By Distribution Channel: Digital fulfilment scales chronic therapies

Retail pharmacies retained 47.68% of 2024 turnover, bolstered by walk-in refills and immediate access for acute prescriptions. Online and mail-order platforms are projected to climb at a 10.44% CAGR through 2030, outpacing all other routes as insurers incentivise 90-day supplies and patients embrace doorstep delivery. Hospital pharmacies maintain a stable share through perioperative and inpatient seizure management, while physician-dispensing remains limited to select U.S. states.

E-pharmacy growth aligns with gabapentin’s chronic-use profile: AI-driven auto-refill reminders, tele-neurology consults and consolidated logistics lower overhead and improve adherence. Scheduling variability complicates national fulfilment, but most jurisdictions still classify the drug as non-controlled, easing digital expansion. Supply disruptions at single manufacturers highlight the resilience advantage of central mail-order hubs that can reroute volume quickly. Looking forward, omnichannel integration—allowing synchronized brick-and-mortar pickup or courier drop—should solidify digital channels as the fastest-rising pillar of the gabapentin market share landscape.

Geography Analysis

North America posted the lion’s share at 37.43% in 2024 on the back of broad off-label uptake, favourable reimbursement and clinician familiarity. State-by-state scheduling nonetheless clouds outlook, and selective shortages have spotlighted supply chain concentration risks.

Asia-Pacific is poised to deliver the quickest 8.67% CAGR as governments streamline approvals, expand insurance and encourage local API production. China’s mirogabalin clearance in 2024 illustrates appetite for newer gabapentinoids, while Indian manufacturers scale capacity, consolidating the region’s role as a global supply hub.

Europe maintains steady expansion anchored by established neurology networks and consistent EMA guidance. Parallel import rules and reference pricing push ongoing cost containment, benefiting health systems but compressing supplier margins. Eastern Europe and southern tier markets offer incremental upside as neurologist density and diagnostic rates rise.

Competitive Landscape

The gabapentin market shows moderate fragmentation: the top five suppliers hold roughly 45% global revenue, yielding a concentration score of 6 on a 1-to-10 scale. Viatris, Teva and Aurobindo, each balancing broad immediate-release catalogues against margin erosion. Teva’s 2025 shortage episode reveals the fragility of concentrated capacity, while Camber and Strides jockey for position in extended-release and high-strength niches. Innovators hedge commoditisation via delivery-technology upgrades; generics follow post-patent expiry, compressing premiums. External threats loom from novel sodium-channel inhibitors such as Vertex’s suzetrigine, which could draw acute-pain scripts away from the gabapentin market.

Digital pharmacies add a new competitive axis as Amazon Pharmacy and CVS health-tech units weaponise logistics data to lock in refill-intensive molecules. Manufacturers that integrate real-time inventory feeds and e-prescribing APIs will enjoy preferential shelf position in these fast-growing channels.

Gabapentin Industry Leaders

Viatris

Teva Pharmaceutical Industries

Aurobindo Pharma

Sun Pharmaceutical Industries

Pfizer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sunshine Biopharma’s Nora Pharma arm launches generic gabapentin in Canada.

- April 2025: FDA revises prescribing information for all gabapentinoids, adding withdrawal warnings for neonates and treated adults.

- March 2024: Strides Pharma Global obtains USFDA approval for 600 mg and 800 mg gabapentin tablets.

Global Gabapentin Market Report Scope

| Capsules |

| Tablets |

| Oral Solution |

| Extended-Release Tablets |

| Epilepsy – Partial-Onset Seizures |

| Post-Herpetic Neuralgia |

| Diabetic Peripheral Neuropathy |

| Restless Leg Syndrome |

| Off-Label Chronic Back / Musculoskeletal Pain |

| 100 |

| 300 |

| 400 |

| ≥600 |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online & Mail-Order Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Formulation | Capsules | |

| Tablets | ||

| Oral Solution | ||

| Extended-Release Tablets | ||

| By Indication | Epilepsy – Partial-Onset Seizures | |

| Post-Herpetic Neuralgia | ||

| Diabetic Peripheral Neuropathy | ||

| Restless Leg Syndrome | ||

| Off-Label Chronic Back / Musculoskeletal Pain | ||

| By Strength (mg) | 100 | |

| 300 | ||

| 400 | ||

| ≥600 | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online & Mail-Order Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current gabapentin market size?

The gabapentin market size stands at USD 2.77 billion in 2025 and is forecast to reach USD 3.72 billion by 2030.

2. Which formulation is growing fastest?

Extended-release tablets are the fastest-growing formulation, expanding at a 9.38% CAGR through 2030 as once-daily dosing improves adherence.

3. Why is Asia-Pacific the growth hotspot?

Regulatory harmonisation, rising healthcare access and local API capacity are pushing Asia-Pacific toward the highest 8.67% CAGR.

4. How is digital pharmacy changing distribution?

Online and mail-order channels combine AI refill tools and tele-health integration to grow at 10.44% CAGR, capturing share from retail outlets.

5. What threats could restrain gabapentin growth?

Heightened regulatory scrutiny, generic price erosion and emerging sodium-channel blockers such as suzetrigine pose headwinds for demand and margins.

Page last updated on: